Advanced Financial Accounting: BHP Billiton Segment Analysis

VerifiedAdded on 2023/06/08

|12

|2462

|461

Report

AI Summary

This report provides a detailed analysis of BHP Billiton, a leading resource company, focusing on its business operations, major customers, and markets. It examines recent developments and changes in segment reporting, including the adoption of new accounting standards like AASB 15/IFRS 15 and IFRS 9/AASB 9. The report also presents a profit and loss analysis by operating segments (Petroleum, Copper, Iron Ore, and Coal), highlighting Iron Ore's consistent profitability. Furthermore, it emphasizes the importance of segment data for investors, as it provides a more granular view of the company's performance compared to consolidated financial statements, aiding in better investment decisions. The report concludes that BHP Billiton complies with IFRS 8 'Operating Segments' and that segment data is essential for investment analysis.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced Financial Accounting

Name of the Student

Name of the University

Author’s Note

Advanced Financial Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED FINANCIAL ACCOUNTING

Executive Summary

The report involves in the analysis of different business and financial data of BHP Billiton. The

report talks about the major business operations of BHP Billiton along with the analysis of major

customers and market. After that, the discussion also shows the upcoming changes in segment

reporting as well as disclosure of BHP Billiton for financial reporting. The report sheds light on

the profit or loss of all four reportable segments of BHP Billiton. Lastly, the report analyzes the

reason for considering segment data for the investors.

Executive Summary

The report involves in the analysis of different business and financial data of BHP Billiton. The

report talks about the major business operations of BHP Billiton along with the analysis of major

customers and market. After that, the discussion also shows the upcoming changes in segment

reporting as well as disclosure of BHP Billiton for financial reporting. The report sheds light on

the profit or loss of all four reportable segments of BHP Billiton. Lastly, the report analyzes the

reason for considering segment data for the investors.

2ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Background of BHP Billiton...........................................................................................................3

Recent Developments and Changes.................................................................................................4

Information about Major Customers and Markets...........................................................................5

Profit or Loss by Operating Segments.............................................................................................6

Analysis of BHP Billiton’s Report and Why Segment Data is Essential to the Investment

Analysis Process..............................................................................................................................7

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

Table of Contents

Introduction......................................................................................................................................3

Background of BHP Billiton...........................................................................................................3

Recent Developments and Changes.................................................................................................4

Information about Major Customers and Markets...........................................................................5

Profit or Loss by Operating Segments.............................................................................................6

Analysis of BHP Billiton’s Report and Why Segment Data is Essential to the Investment

Analysis Process..............................................................................................................................7

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED FINANCIAL ACCOUNTING

Introduction

In today’s business world, it has become the prime responsibility of the business entities

to provide all the crucial information about their operational and financial activities through

various mediums like company website, annual report and others. This helps the investors and

other users in judging the current business as well as financial position of their companies (Weil,

Schipper & Francis, 2013). The main aim of this company is the analysis of different kinds of

business information of one of the major Australian mining companies, BHP Billiton. Different

parts of this report analyze and evaluate different business information of the company related to

business segments, recent development and changes, customer as well as market and the analysis

of annual report.

Background of BHP Billiton

BHP Billiton is regarded as one of the world’s leading resource companies. BHP Billiton

emerged as a major resource company in the year of 2001 as a result of the merger of Broken

Hill Property Company Limited (BHP) and Billiton Plc. The company is headquartered at

Melbourne, Australia. The main business operation of the company can be seen in extracting and

processing minerals, oil and gas with the assistance of more than 60,000 employees and

contractors; and this major business operation of BHP Billiton can be seen in the regions of

Australia and America (bhp.com, 2018). It needs to be mentioned that BHP Billiton has its

presence all over the world; and they sell their product through sales and marketing led through

Singapore and Houston, United States. It is interesting to mention the fact that the legal entity of

BHP Billiton carries out their operations under a structure of dual listed company that has two

parent companies; they are BHP Billiton Limited and BHP Billiton Plc; the main intention of this

Introduction

In today’s business world, it has become the prime responsibility of the business entities

to provide all the crucial information about their operational and financial activities through

various mediums like company website, annual report and others. This helps the investors and

other users in judging the current business as well as financial position of their companies (Weil,

Schipper & Francis, 2013). The main aim of this company is the analysis of different kinds of

business information of one of the major Australian mining companies, BHP Billiton. Different

parts of this report analyze and evaluate different business information of the company related to

business segments, recent development and changes, customer as well as market and the analysis

of annual report.

Background of BHP Billiton

BHP Billiton is regarded as one of the world’s leading resource companies. BHP Billiton

emerged as a major resource company in the year of 2001 as a result of the merger of Broken

Hill Property Company Limited (BHP) and Billiton Plc. The company is headquartered at

Melbourne, Australia. The main business operation of the company can be seen in extracting and

processing minerals, oil and gas with the assistance of more than 60,000 employees and

contractors; and this major business operation of BHP Billiton can be seen in the regions of

Australia and America (bhp.com, 2018). It needs to be mentioned that BHP Billiton has its

presence all over the world; and they sell their product through sales and marketing led through

Singapore and Houston, United States. It is interesting to mention the fact that the legal entity of

BHP Billiton carries out their operations under a structure of dual listed company that has two

parent companies; they are BHP Billiton Limited and BHP Billiton Plc; the main intention of this

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED FINANCIAL ACCOUNTING

structure is to carries out operation as a single entity. The presence of a unified Board and

Management can be seen for controlling the business operations of BHP Billiton (bhp.com,

2018).

Recent Developments and Changes

As per the 2017 Annual Report of BHP Billiton, the company prepares their financial

statements as per UK Companies Act 2006; and presents their financial statements as per the

requirements of Financial Reporting Standard 101 ‘Reduced Disclosure Framework’ IFRS

101) (bhp.com, 2018). The company has been following these regulations for years. However,

some changes in the accounting principles will be applied from the year 2018 related to some

specific financial treatments. The first changed principle will be the adoption of AASB 15/IFRS

15 ‘Revenue from Contracts with Customers’. This modified standard involves determining

when to recognize revenue and how much revenue to be recognized. The next standard will be

IFRS 9/AASB 9 ‘Financial Instrument’ and this modified standard will include the

classification as well as financial assets measurement of the company (bhp.com, 2018). The next

principle will be IFRIC 22 ‘Foreign Currency Transactions and Advanced Consideration’

and this modified standard will include the required interpretation for the clarification of the

exchange rate to be used for assets, liabilities, incomes and expenses. The last standard will be

IFRS 16/AASB 16 ‘Leases’ and this modified regulation will make BHP Billiton to give an

explanation for leases under an on-balance sheet model with the difference between finance

leases and operating leases removed. These are the recent development and changes in the

segment reporting and disclosure of BHP Billiton (bhp.com, 2018).

structure is to carries out operation as a single entity. The presence of a unified Board and

Management can be seen for controlling the business operations of BHP Billiton (bhp.com,

2018).

Recent Developments and Changes

As per the 2017 Annual Report of BHP Billiton, the company prepares their financial

statements as per UK Companies Act 2006; and presents their financial statements as per the

requirements of Financial Reporting Standard 101 ‘Reduced Disclosure Framework’ IFRS

101) (bhp.com, 2018). The company has been following these regulations for years. However,

some changes in the accounting principles will be applied from the year 2018 related to some

specific financial treatments. The first changed principle will be the adoption of AASB 15/IFRS

15 ‘Revenue from Contracts with Customers’. This modified standard involves determining

when to recognize revenue and how much revenue to be recognized. The next standard will be

IFRS 9/AASB 9 ‘Financial Instrument’ and this modified standard will include the

classification as well as financial assets measurement of the company (bhp.com, 2018). The next

principle will be IFRIC 22 ‘Foreign Currency Transactions and Advanced Consideration’

and this modified standard will include the required interpretation for the clarification of the

exchange rate to be used for assets, liabilities, incomes and expenses. The last standard will be

IFRS 16/AASB 16 ‘Leases’ and this modified regulation will make BHP Billiton to give an

explanation for leases under an on-balance sheet model with the difference between finance

leases and operating leases removed. These are the recent development and changes in the

segment reporting and disclosure of BHP Billiton (bhp.com, 2018).

5ADVANCED FINANCIAL ACCOUNTING

Information about Major Customers and Markets

The presence of some major customers can be seen in the business of BHP Billiton. BHP

Billiton delivers their products to the customers of some of the major countries like China, Japan,

Chili, Mexico and United States. BHP Billiton sells iron ore to China for making steel; they sell

copper cathode to their customers in Japan and Chili; they sell petroleum to their major

customers in Mexico and United States (bhp.com, 2018). It needs to be mentioned in this context

that BHP the marketing business segment of BHP Billiton plays a crucial role in understanding

the needs of these customers so that the right products can be delivered to them for the

maximization of business value (bhp.com, 2018).

The business operations of BHP Billiton can be seen in metals, minerals and mining

industry. It needs to be mentioned that this is the largest industry sector of Australian Security

Exchange (ASX) with the presence of over 600 companies. This industry contributes largely

towards the Gross Domestic Product (GDP) of Australia; for example, this industry contributes

10% towards the total GDP of Australia in 2012-13 (ga.gov.au, 2018). In the year 2012, the

mining industry provided employment to 266000 people directly. According to Bureau of

Resources and Energy Economic (BREE), this industry resulted to the export worth $107 billion

in 2012-13 (ga.gov.au, 2018). Some of the major competitors of BHP Billiton in this industry are

Rio Tinto, Newcrest Mining, OneSteel, Alumina Limited and others.

Information about Major Customers and Markets

The presence of some major customers can be seen in the business of BHP Billiton. BHP

Billiton delivers their products to the customers of some of the major countries like China, Japan,

Chili, Mexico and United States. BHP Billiton sells iron ore to China for making steel; they sell

copper cathode to their customers in Japan and Chili; they sell petroleum to their major

customers in Mexico and United States (bhp.com, 2018). It needs to be mentioned in this context

that BHP the marketing business segment of BHP Billiton plays a crucial role in understanding

the needs of these customers so that the right products can be delivered to them for the

maximization of business value (bhp.com, 2018).

The business operations of BHP Billiton can be seen in metals, minerals and mining

industry. It needs to be mentioned that this is the largest industry sector of Australian Security

Exchange (ASX) with the presence of over 600 companies. This industry contributes largely

towards the Gross Domestic Product (GDP) of Australia; for example, this industry contributes

10% towards the total GDP of Australia in 2012-13 (ga.gov.au, 2018). In the year 2012, the

mining industry provided employment to 266000 people directly. According to Bureau of

Resources and Energy Economic (BREE), this industry resulted to the export worth $107 billion

in 2012-13 (ga.gov.au, 2018). Some of the major competitors of BHP Billiton in this industry are

Rio Tinto, Newcrest Mining, OneSteel, Alumina Limited and others.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED FINANCIAL ACCOUNTING

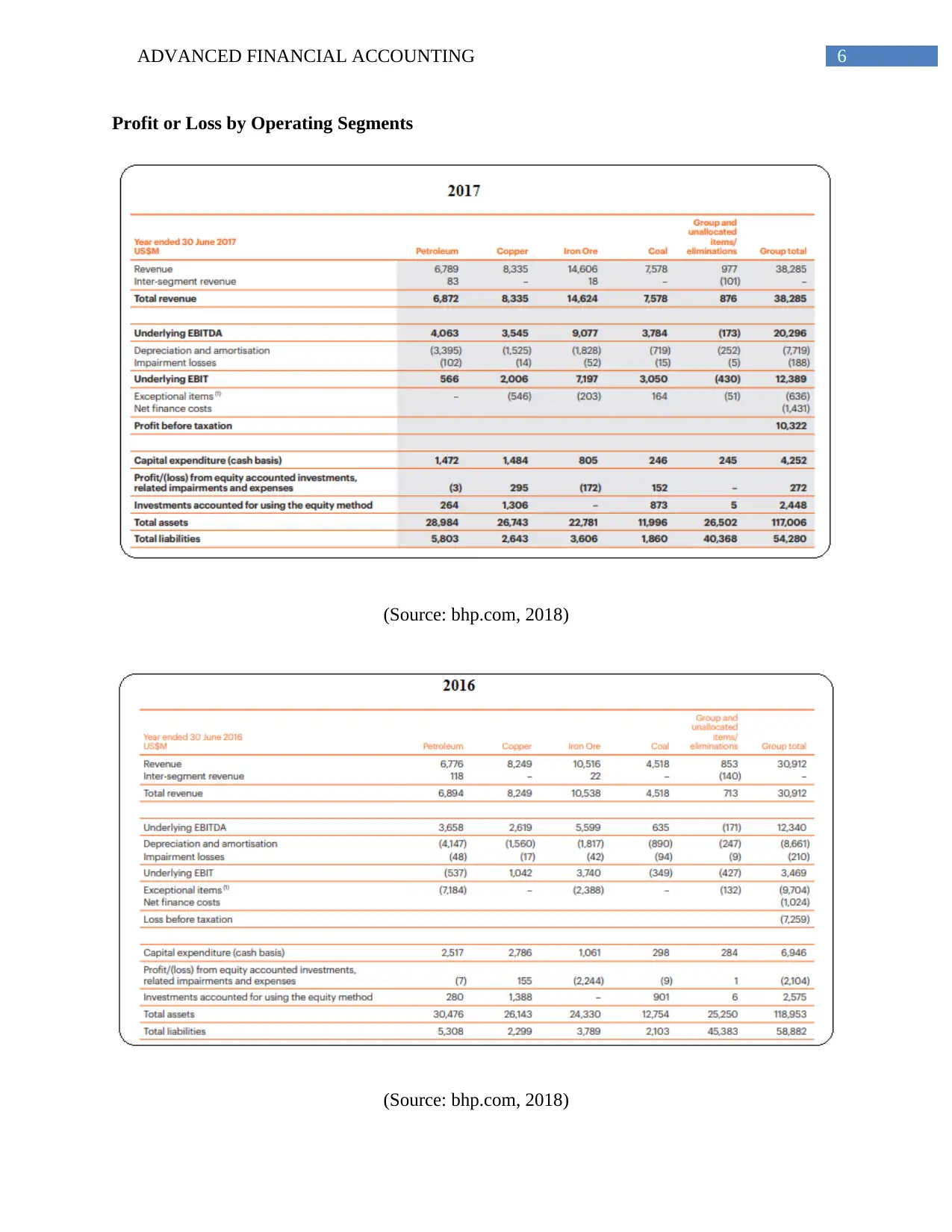

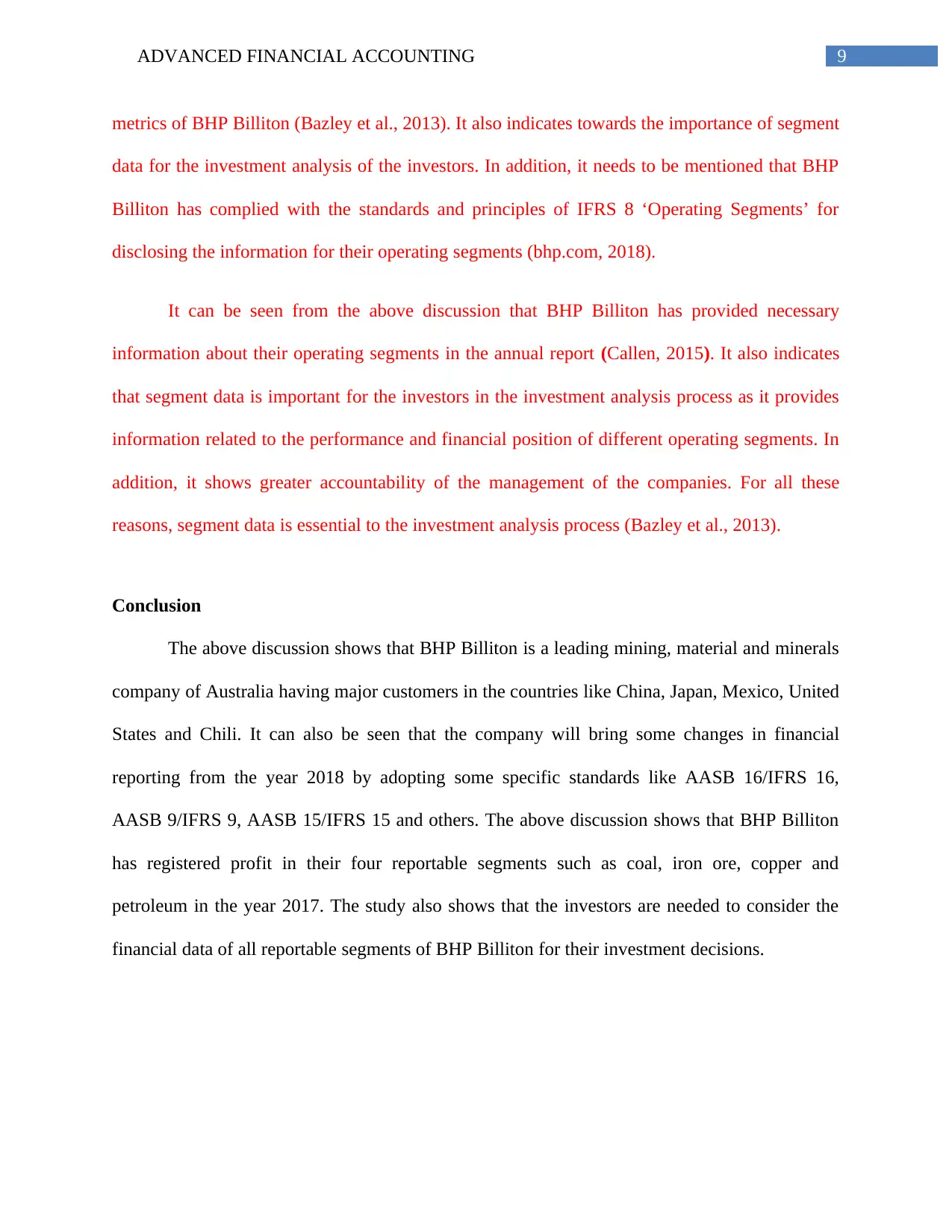

Profit or Loss by Operating Segments

(Source: bhp.com, 2018)

(Source: bhp.com, 2018)

Profit or Loss by Operating Segments

(Source: bhp.com, 2018)

(Source: bhp.com, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED FINANCIAL ACCOUNTING

As per the 2017 Annual Report of BHP Billiton, the entity has four reportable segments;

they are Petroleum, Copper, Iron Ore and Coal; and the company has provided financial

information about all of these reportable segments. According to the above figure, the underlying

EBITDA for petroleum, copper, iron ore and coal are $4063 million, $3545 million, $9077

million and $3784 million respectively (bhp.com, 2018). Thus, it is visible that iron ore segment

has reported highest underlying EBITDA. After that, the EBIT for petroleum, copper, iron ore

and coal are $566 million, $2006 million, $7197 million and $3050 million respectively. Here

also iron ore registered highest amount of EBIT. According to the 2017 Annual Report of BHP

Billiton, the profit before tax from petroleum, copper, iron ore and coal are $566 million, $1460

million, $6994 million and $3214 million respectively (bhp.com, 2018). Hence, it can be

observed that iron ore has been consistent in registering most amount of profit for the company.

It can also be observed that none of these reportable segments of BHP Billiton has reported loss

in the financial year of 2017. When compared to the 2016 financial results, it can be seen that all

the segments have improved figures of profit in 2017 as compared to 2016 (bhp.com, 2018). In

2016, petroleum and iron ore registered loss in EBIT that resulted to the loss before taxation for

the company. However, effective financial strategy and good performance of these segments

contributed towards profit before taxation for BHP Billiton in 2017 (bhp.com, 2018).

Analysis of BHP Billiton’s Report and Why Segment Data is Essential to the Investment

Analysis Process

Users of the financial statements only get an aggregate view of the financial performance

of the companies by understanding the information from the consolidated financial statements. It

is needed for the business entities to supplement the consolidated financial statements with the

information about their various operating segments in order to avoid the issue of information

As per the 2017 Annual Report of BHP Billiton, the entity has four reportable segments;

they are Petroleum, Copper, Iron Ore and Coal; and the company has provided financial

information about all of these reportable segments. According to the above figure, the underlying

EBITDA for petroleum, copper, iron ore and coal are $4063 million, $3545 million, $9077

million and $3784 million respectively (bhp.com, 2018). Thus, it is visible that iron ore segment

has reported highest underlying EBITDA. After that, the EBIT for petroleum, copper, iron ore

and coal are $566 million, $2006 million, $7197 million and $3050 million respectively. Here

also iron ore registered highest amount of EBIT. According to the 2017 Annual Report of BHP

Billiton, the profit before tax from petroleum, copper, iron ore and coal are $566 million, $1460

million, $6994 million and $3214 million respectively (bhp.com, 2018). Hence, it can be

observed that iron ore has been consistent in registering most amount of profit for the company.

It can also be observed that none of these reportable segments of BHP Billiton has reported loss

in the financial year of 2017. When compared to the 2016 financial results, it can be seen that all

the segments have improved figures of profit in 2017 as compared to 2016 (bhp.com, 2018). In

2016, petroleum and iron ore registered loss in EBIT that resulted to the loss before taxation for

the company. However, effective financial strategy and good performance of these segments

contributed towards profit before taxation for BHP Billiton in 2017 (bhp.com, 2018).

Analysis of BHP Billiton’s Report and Why Segment Data is Essential to the Investment

Analysis Process

Users of the financial statements only get an aggregate view of the financial performance

of the companies by understanding the information from the consolidated financial statements. It

is needed for the business entities to supplement the consolidated financial statements with the

information about their various operating segments in order to avoid the issue of information

8ADVANCED FINANCIAL ACCOUNTING

loss. In addition, in the presence of information related to operating segments, the users of the

financial statements become able to obtain information about different activities of the business

along with their performance and associated risks (Weil, Schipper & Francis, 2013). Operating

segment information highlights the financial performance of various parts of the organizations

and helps the users in better predicting the future profitability of the organizations. For this

reasons, it is needed for the business organizations to comply with the standards of IFRS 8

‘Operating Segments’ for disclosing information of the operating segments with the help of

financial statements and various notes to the financial statements. For this reason, regardless of

size, the investors should consider analyzing the financial performance of all reportable segments

for getting the actual financial performance of the companies (May, 2013).

It needs to be mentioned that the financial reports of the large companies consist of

footnotes to the financial statements where the companies provide the information about

different reportable and the same can be found in the 2017 Annual Report of BHP Billiton.

According to the 2017 Annual Report of BHP Billiton, the Consolidated Income Statement of

the company for 2017 states that the company has registered $10322 million profit before that

compared to a loss of $7259 million in 2016. At the same time, the company has registered

revenue worth $38285 in 2017. All these figures are convincing for the investors on overall basis

(bhp.com, 2018). However, when they consider the segment information for the year 2017, they

will see that petroleum segment has reported the lowest amount of profit before tax in 2017

where iron ore registered the highest. They can also see that iron ore has fetched more revenues

compared to the other segments. After the consideration segment data, investors might consider

investing in the business of iron ore instead of petroleum. It implies that the investors would

never be able to know the profitability of each segment by only considering the key financial

loss. In addition, in the presence of information related to operating segments, the users of the

financial statements become able to obtain information about different activities of the business

along with their performance and associated risks (Weil, Schipper & Francis, 2013). Operating

segment information highlights the financial performance of various parts of the organizations

and helps the users in better predicting the future profitability of the organizations. For this

reasons, it is needed for the business organizations to comply with the standards of IFRS 8

‘Operating Segments’ for disclosing information of the operating segments with the help of

financial statements and various notes to the financial statements. For this reason, regardless of

size, the investors should consider analyzing the financial performance of all reportable segments

for getting the actual financial performance of the companies (May, 2013).

It needs to be mentioned that the financial reports of the large companies consist of

footnotes to the financial statements where the companies provide the information about

different reportable and the same can be found in the 2017 Annual Report of BHP Billiton.

According to the 2017 Annual Report of BHP Billiton, the Consolidated Income Statement of

the company for 2017 states that the company has registered $10322 million profit before that

compared to a loss of $7259 million in 2016. At the same time, the company has registered

revenue worth $38285 in 2017. All these figures are convincing for the investors on overall basis

(bhp.com, 2018). However, when they consider the segment information for the year 2017, they

will see that petroleum segment has reported the lowest amount of profit before tax in 2017

where iron ore registered the highest. They can also see that iron ore has fetched more revenues

compared to the other segments. After the consideration segment data, investors might consider

investing in the business of iron ore instead of petroleum. It implies that the investors would

never be able to know the profitability of each segment by only considering the key financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCED FINANCIAL ACCOUNTING

metrics of BHP Billiton (Bazley et al., 2013). It also indicates towards the importance of segment

data for the investment analysis of the investors. In addition, it needs to be mentioned that BHP

Billiton has complied with the standards and principles of IFRS 8 ‘Operating Segments’ for

disclosing the information for their operating segments (bhp.com, 2018).

It can be seen from the above discussion that BHP Billiton has provided necessary

information about their operating segments in the annual report (Callen, 2015). It also indicates

that segment data is important for the investors in the investment analysis process as it provides

information related to the performance and financial position of different operating segments. In

addition, it shows greater accountability of the management of the companies. For all these

reasons, segment data is essential to the investment analysis process (Bazley et al., 2013).

Conclusion

The above discussion shows that BHP Billiton is a leading mining, material and minerals

company of Australia having major customers in the countries like China, Japan, Mexico, United

States and Chili. It can also be seen that the company will bring some changes in financial

reporting from the year 2018 by adopting some specific standards like AASB 16/IFRS 16,

AASB 9/IFRS 9, AASB 15/IFRS 15 and others. The above discussion shows that BHP Billiton

has registered profit in their four reportable segments such as coal, iron ore, copper and

petroleum in the year 2017. The study also shows that the investors are needed to consider the

financial data of all reportable segments of BHP Billiton for their investment decisions.

metrics of BHP Billiton (Bazley et al., 2013). It also indicates towards the importance of segment

data for the investment analysis of the investors. In addition, it needs to be mentioned that BHP

Billiton has complied with the standards and principles of IFRS 8 ‘Operating Segments’ for

disclosing the information for their operating segments (bhp.com, 2018).

It can be seen from the above discussion that BHP Billiton has provided necessary

information about their operating segments in the annual report (Callen, 2015). It also indicates

that segment data is important for the investors in the investment analysis process as it provides

information related to the performance and financial position of different operating segments. In

addition, it shows greater accountability of the management of the companies. For all these

reasons, segment data is essential to the investment analysis process (Bazley et al., 2013).

Conclusion

The above discussion shows that BHP Billiton is a leading mining, material and minerals

company of Australia having major customers in the countries like China, Japan, Mexico, United

States and Chili. It can also be seen that the company will bring some changes in financial

reporting from the year 2018 by adopting some specific standards like AASB 16/IFRS 16,

AASB 9/IFRS 9, AASB 15/IFRS 15 and others. The above discussion shows that BHP Billiton

has registered profit in their four reportable segments such as coal, iron ore, copper and

petroleum in the year 2017. The study also shows that the investors are needed to consider the

financial data of all reportable segments of BHP Billiton for their investment decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ADVANCED FINANCIAL ACCOUNTING

References

Annual Report 2017. (2018). Retrieved from

https://www.bhp.com/-/media/documents/investors/annual-reports/2017/

bhpannualreport2017.pdf

Bazley, M., Hancock, P., Fisher, C., Lovell, A., Berk, J., DeMarzo, P., ... & DeMarzo, P. (2013).

Financial Accounting: An Integrated. Thomson Pty Ltd, South Melbourne.

BHP. (2018). BHP. About us Retrieved 14 August 2018, from https://www.bhp.com/our-

approach/our-company/about-us

BHP. (2018). BHP. Marketing and supply Retrieved 14 August 2018, from

https://www.bhp.com/our-businesses/marketing-and-supply

BHP. (2018). BHP. Structure and strategy Retrieved 14 August 2018, from

https://www.bhp.com/our-approach/our-company/strategy

Callen, J. L. (2015). A selective critical review of financial accounting research. Critical

Perspectives on Accounting, 26, 157-167.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial accounting.

Pearson Higher Education AU.

May, G. O. (2013). Financial accounting. Read Books Ltd.

Minerals Basics - Geoscience Australia. (2018). Ga.gov.au. Retrieved 14 August 2018, from

http://www.ga.gov.au/scientific-topics/minerals/basics

References

Annual Report 2017. (2018). Retrieved from

https://www.bhp.com/-/media/documents/investors/annual-reports/2017/

bhpannualreport2017.pdf

Bazley, M., Hancock, P., Fisher, C., Lovell, A., Berk, J., DeMarzo, P., ... & DeMarzo, P. (2013).

Financial Accounting: An Integrated. Thomson Pty Ltd, South Melbourne.

BHP. (2018). BHP. About us Retrieved 14 August 2018, from https://www.bhp.com/our-

approach/our-company/about-us

BHP. (2018). BHP. Marketing and supply Retrieved 14 August 2018, from

https://www.bhp.com/our-businesses/marketing-and-supply

BHP. (2018). BHP. Structure and strategy Retrieved 14 August 2018, from

https://www.bhp.com/our-approach/our-company/strategy

Callen, J. L. (2015). A selective critical review of financial accounting research. Critical

Perspectives on Accounting, 26, 157-167.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial accounting.

Pearson Higher Education AU.

May, G. O. (2013). Financial accounting. Read Books Ltd.

Minerals Basics - Geoscience Australia. (2018). Ga.gov.au. Retrieved 14 August 2018, from

http://www.ga.gov.au/scientific-topics/minerals/basics

11ADVANCED FINANCIAL ACCOUNTING

Weil, R. L., Schipper, K., & Francis, J. (2013). Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Weil, R. L., Schipper, K., & Francis, J. (2013). Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.