Financial Performance Analysis of BHP Billiton using Ratio Analysis

VerifiedAdded on 2019/11/20

|12

|2514

|255

Report

AI Summary

This report provides a comprehensive financial performance analysis of BHP Billiton from 2012 to 2016, focusing on the impact of fluctuating commodity prices on the company's financial health. The analysis utilizes ratio analysis to assess profitability, efficiency, liquidity, and solvency. The report highlights the significant influence of commodity prices on BHP Billiton's profitability, particularly the decline in profits and the operating loss in FY2016 due to falling prices. It also examines the company's efforts to improve efficiency and manage its cash cycle, with positive results observed in inventory and receivables turnover. The study further investigates the company's liquidity and solvency ratios, revealing improvements in short-term liquidity but a deterioration in long-term solvency, especially in FY2016. The conclusion emphasizes the cyclical nature of the mining industry and the importance of commodity prices in determining BHP Billiton's financial outcomes. This report offers valuable insights into the financial strategies and performance of a leading mining company during a period of industry turbulence.

ACCOUNTING FOR FINANCE & MANAGER

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUTNING FOR FINANCE & MANAGER

EXECUTIVE SUMMARY

In wake of the falling commodity prices and the visible turbulence in the mining companies,

BHP Billiton has been selected as the company for which financial performance analysis has

been carried out. The key enabling tool in this regard has been taken as ratio analysis and the

time period for consideration has been taken as FY2012-FY2016 as it represents a transition

period for the mining industry. Various ratios such as profitability, liquidity, solvency and

efficiency have been computed using the financial statements and interpretations have been

drawn about the performance of the company. Based on the existing environment and the

past financial performance of the company, view has been presented with regards to the

likely future performance of the company.

1

EXECUTIVE SUMMARY

In wake of the falling commodity prices and the visible turbulence in the mining companies,

BHP Billiton has been selected as the company for which financial performance analysis has

been carried out. The key enabling tool in this regard has been taken as ratio analysis and the

time period for consideration has been taken as FY2012-FY2016 as it represents a transition

period for the mining industry. Various ratios such as profitability, liquidity, solvency and

efficiency have been computed using the financial statements and interpretations have been

drawn about the performance of the company. Based on the existing environment and the

past financial performance of the company, view has been presented with regards to the

likely future performance of the company.

1

ACCOUTNING FOR FINANCE & MANAGER

TABLE OF CONTENTS

INTRODUCTION.................................................................................................................................2

CRITICAL ANALYSIS........................................................................................................................3

Profitability Ratios.............................................................................................................................3

Efficiency Ratios...............................................................................................................................5

Liquidity Ratios.................................................................................................................................6

Solvency Ratios.................................................................................................................................7

CONCLUSION.....................................................................................................................................8

REFERENCES......................................................................................................................................9

APPENDIX.........................................................................................................................................11

2

TABLE OF CONTENTS

INTRODUCTION.................................................................................................................................2

CRITICAL ANALYSIS........................................................................................................................3

Profitability Ratios.............................................................................................................................3

Efficiency Ratios...............................................................................................................................5

Liquidity Ratios.................................................................................................................................6

Solvency Ratios.................................................................................................................................7

CONCLUSION.....................................................................................................................................8

REFERENCES......................................................................................................................................9

APPENDIX.........................................................................................................................................11

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUTNING FOR FINANCE & MANAGER

INTRODUCTION

The company selected is BHP Billiton which is a leading mining company based out of

Australia. It was formed in 2001 as a result of the Australia based BHP group and UK based

Anglo Dutch Billiton Plc. The business of the company is divided across five verticals

namely iron ore, coal, petroleum, potash and copper. The company has mine presence

worldwide with majority of them located in Australia, South America, USA, Canada and

Africa. The company is listed on both the ASX (Australia Stock Exchange) and LSX

(London Stock Exchange) and has a market capitalisation in excess of $ 110 billion (BHP

Billiton, 2016). The mining sector has recently been in quite a lot of turbulence on account of

the falling commodity prices. While it is a testing time for these companies, but from an

investor perspective this provides an opportunity for investment. Keeping this in mind, the

objective of the given report is to highlight the financial performance of the company

considering the available financial statements for the last five years. Based on the analysis of

the financial performance and the underlying parameters, the guidance for future financial

and market performance would be offered.

CRITICAL ANALYSIS

For the purpose of analysis of the financial performance of the company, a period of last five

years i.e. 2012-2016 has been chosen. The reason behind choosing this period is to

demonstrate the linkage between the financial performance of the company and the

commodity pricing cycle. In order to critically analyse the same, the key tool that has been

deployed is ratio analysis. It is an enabling tool which tends to highlight the performance of

the company in various aspects and has been preferred over trend analysis which does not

bifurcate the financial performance in this manner. The critical analysis of the company’s

financial performance through ratio analysis is discussed below.

3

INTRODUCTION

The company selected is BHP Billiton which is a leading mining company based out of

Australia. It was formed in 2001 as a result of the Australia based BHP group and UK based

Anglo Dutch Billiton Plc. The business of the company is divided across five verticals

namely iron ore, coal, petroleum, potash and copper. The company has mine presence

worldwide with majority of them located in Australia, South America, USA, Canada and

Africa. The company is listed on both the ASX (Australia Stock Exchange) and LSX

(London Stock Exchange) and has a market capitalisation in excess of $ 110 billion (BHP

Billiton, 2016). The mining sector has recently been in quite a lot of turbulence on account of

the falling commodity prices. While it is a testing time for these companies, but from an

investor perspective this provides an opportunity for investment. Keeping this in mind, the

objective of the given report is to highlight the financial performance of the company

considering the available financial statements for the last five years. Based on the analysis of

the financial performance and the underlying parameters, the guidance for future financial

and market performance would be offered.

CRITICAL ANALYSIS

For the purpose of analysis of the financial performance of the company, a period of last five

years i.e. 2012-2016 has been chosen. The reason behind choosing this period is to

demonstrate the linkage between the financial performance of the company and the

commodity pricing cycle. In order to critically analyse the same, the key tool that has been

deployed is ratio analysis. It is an enabling tool which tends to highlight the performance of

the company in various aspects and has been preferred over trend analysis which does not

bifurcate the financial performance in this manner. The critical analysis of the company’s

financial performance through ratio analysis is discussed below.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUTNING FOR FINANCE & MANAGER

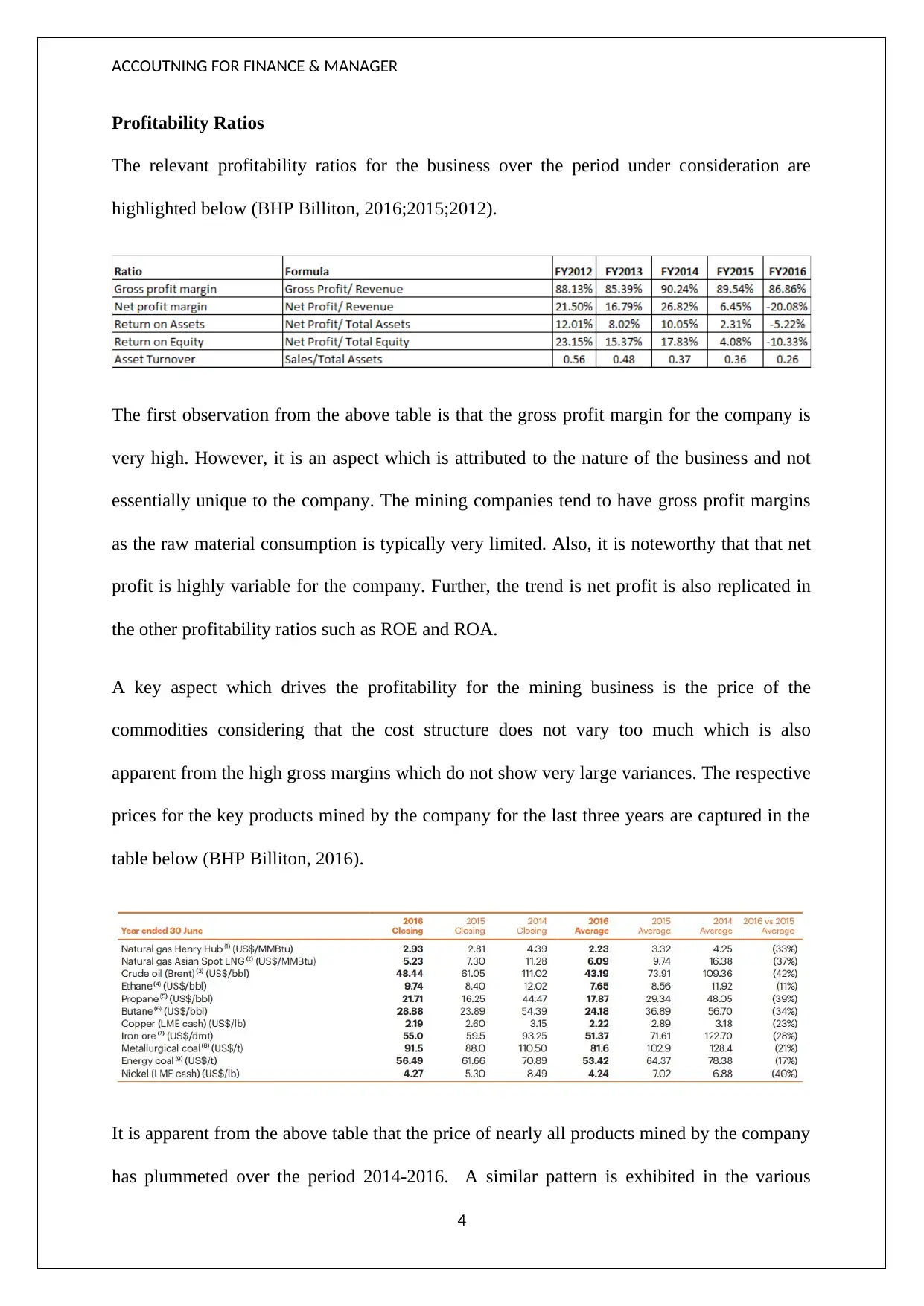

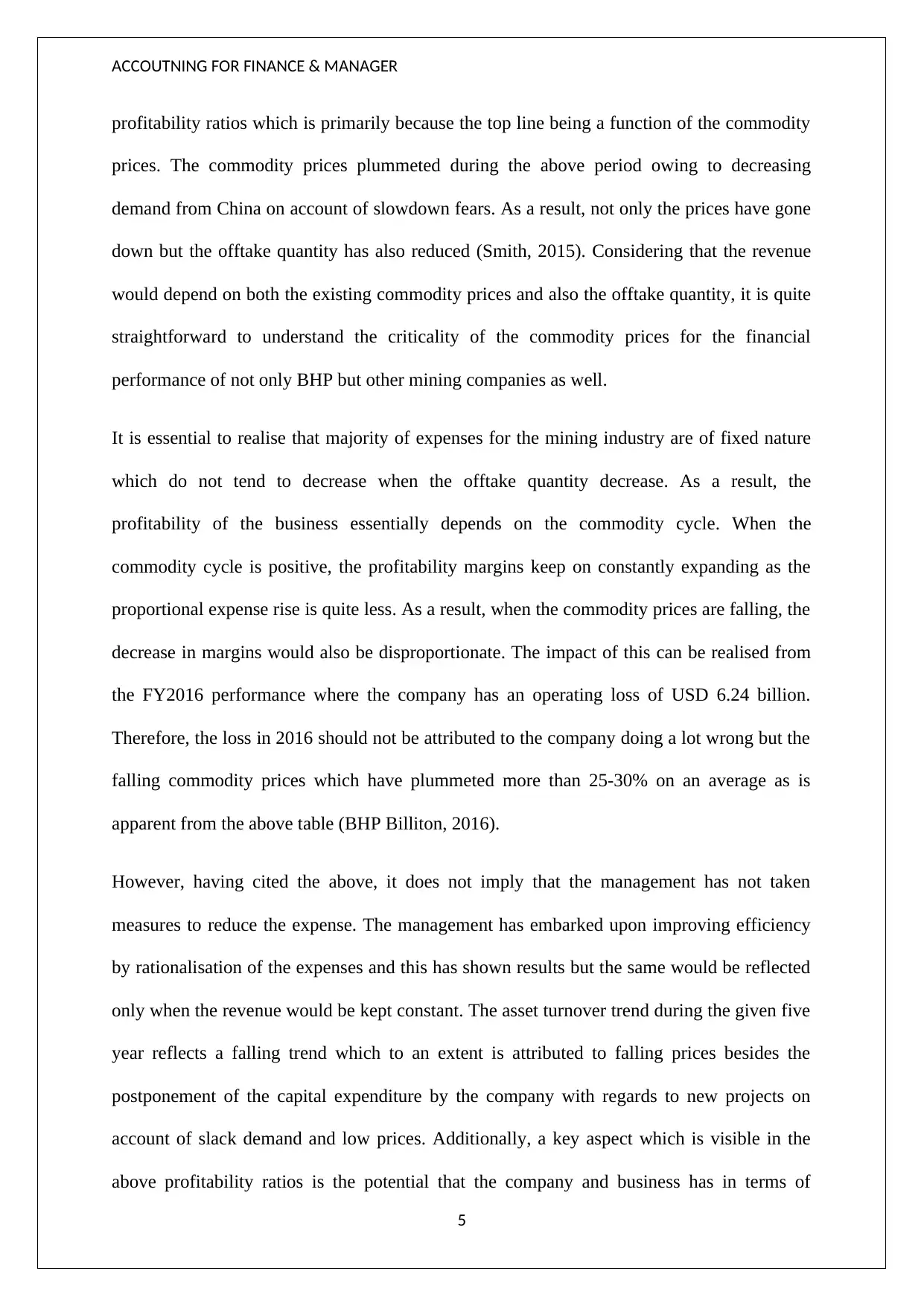

Profitability Ratios

The relevant profitability ratios for the business over the period under consideration are

highlighted below (BHP Billiton, 2016;2015;2012).

The first observation from the above table is that the gross profit margin for the company is

very high. However, it is an aspect which is attributed to the nature of the business and not

essentially unique to the company. The mining companies tend to have gross profit margins

as the raw material consumption is typically very limited. Also, it is noteworthy that that net

profit is highly variable for the company. Further, the trend is net profit is also replicated in

the other profitability ratios such as ROE and ROA.

A key aspect which drives the profitability for the mining business is the price of the

commodities considering that the cost structure does not vary too much which is also

apparent from the high gross margins which do not show very large variances. The respective

prices for the key products mined by the company for the last three years are captured in the

table below (BHP Billiton, 2016).

It is apparent from the above table that the price of nearly all products mined by the company

has plummeted over the period 2014-2016. A similar pattern is exhibited in the various

4

Profitability Ratios

The relevant profitability ratios for the business over the period under consideration are

highlighted below (BHP Billiton, 2016;2015;2012).

The first observation from the above table is that the gross profit margin for the company is

very high. However, it is an aspect which is attributed to the nature of the business and not

essentially unique to the company. The mining companies tend to have gross profit margins

as the raw material consumption is typically very limited. Also, it is noteworthy that that net

profit is highly variable for the company. Further, the trend is net profit is also replicated in

the other profitability ratios such as ROE and ROA.

A key aspect which drives the profitability for the mining business is the price of the

commodities considering that the cost structure does not vary too much which is also

apparent from the high gross margins which do not show very large variances. The respective

prices for the key products mined by the company for the last three years are captured in the

table below (BHP Billiton, 2016).

It is apparent from the above table that the price of nearly all products mined by the company

has plummeted over the period 2014-2016. A similar pattern is exhibited in the various

4

ACCOUTNING FOR FINANCE & MANAGER

profitability ratios which is primarily because the top line being a function of the commodity

prices. The commodity prices plummeted during the above period owing to decreasing

demand from China on account of slowdown fears. As a result, not only the prices have gone

down but the offtake quantity has also reduced (Smith, 2015). Considering that the revenue

would depend on both the existing commodity prices and also the offtake quantity, it is quite

straightforward to understand the criticality of the commodity prices for the financial

performance of not only BHP but other mining companies as well.

It is essential to realise that majority of expenses for the mining industry are of fixed nature

which do not tend to decrease when the offtake quantity decrease. As a result, the

profitability of the business essentially depends on the commodity cycle. When the

commodity cycle is positive, the profitability margins keep on constantly expanding as the

proportional expense rise is quite less. As a result, when the commodity prices are falling, the

decrease in margins would also be disproportionate. The impact of this can be realised from

the FY2016 performance where the company has an operating loss of USD 6.24 billion.

Therefore, the loss in 2016 should not be attributed to the company doing a lot wrong but the

falling commodity prices which have plummeted more than 25-30% on an average as is

apparent from the above table (BHP Billiton, 2016).

However, having cited the above, it does not imply that the management has not taken

measures to reduce the expense. The management has embarked upon improving efficiency

by rationalisation of the expenses and this has shown results but the same would be reflected

only when the revenue would be kept constant. The asset turnover trend during the given five

year reflects a falling trend which to an extent is attributed to falling prices besides the

postponement of the capital expenditure by the company with regards to new projects on

account of slack demand and low prices. Additionally, a key aspect which is visible in the

above profitability ratios is the potential that the company and business has in terms of

5

profitability ratios which is primarily because the top line being a function of the commodity

prices. The commodity prices plummeted during the above period owing to decreasing

demand from China on account of slowdown fears. As a result, not only the prices have gone

down but the offtake quantity has also reduced (Smith, 2015). Considering that the revenue

would depend on both the existing commodity prices and also the offtake quantity, it is quite

straightforward to understand the criticality of the commodity prices for the financial

performance of not only BHP but other mining companies as well.

It is essential to realise that majority of expenses for the mining industry are of fixed nature

which do not tend to decrease when the offtake quantity decrease. As a result, the

profitability of the business essentially depends on the commodity cycle. When the

commodity cycle is positive, the profitability margins keep on constantly expanding as the

proportional expense rise is quite less. As a result, when the commodity prices are falling, the

decrease in margins would also be disproportionate. The impact of this can be realised from

the FY2016 performance where the company has an operating loss of USD 6.24 billion.

Therefore, the loss in 2016 should not be attributed to the company doing a lot wrong but the

falling commodity prices which have plummeted more than 25-30% on an average as is

apparent from the above table (BHP Billiton, 2016).

However, having cited the above, it does not imply that the management has not taken

measures to reduce the expense. The management has embarked upon improving efficiency

by rationalisation of the expenses and this has shown results but the same would be reflected

only when the revenue would be kept constant. The asset turnover trend during the given five

year reflects a falling trend which to an extent is attributed to falling prices besides the

postponement of the capital expenditure by the company with regards to new projects on

account of slack demand and low prices. Additionally, a key aspect which is visible in the

above profitability ratios is the potential that the company and business has in terms of

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUTNING FOR FINANCE & MANAGER

generating profits when the commodity prices tend to favour which is apparent for 2012

(BHP Billiton, 2016;2015;2012).

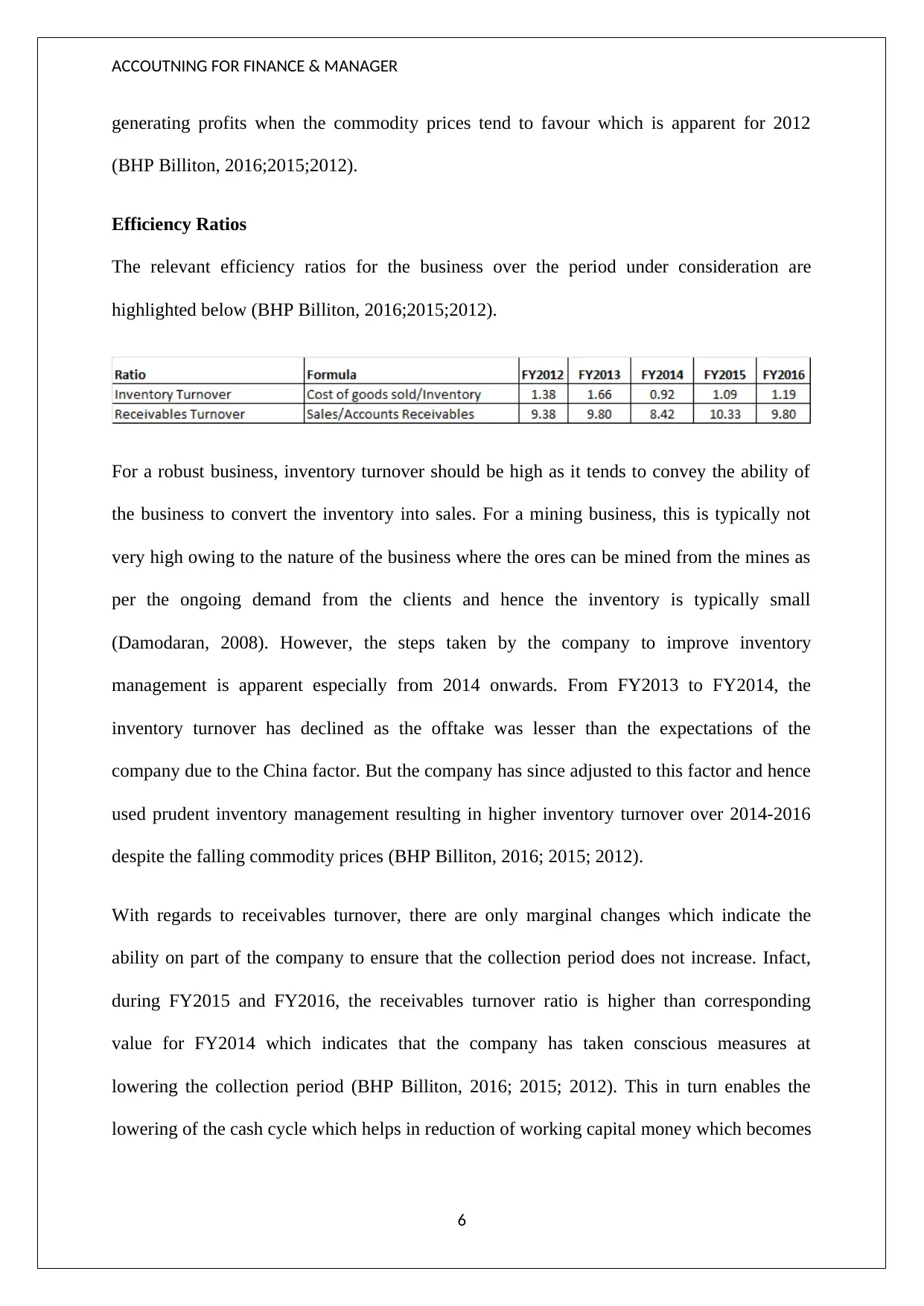

Efficiency Ratios

The relevant efficiency ratios for the business over the period under consideration are

highlighted below (BHP Billiton, 2016;2015;2012).

For a robust business, inventory turnover should be high as it tends to convey the ability of

the business to convert the inventory into sales. For a mining business, this is typically not

very high owing to the nature of the business where the ores can be mined from the mines as

per the ongoing demand from the clients and hence the inventory is typically small

(Damodaran, 2008). However, the steps taken by the company to improve inventory

management is apparent especially from 2014 onwards. From FY2013 to FY2014, the

inventory turnover has declined as the offtake was lesser than the expectations of the

company due to the China factor. But the company has since adjusted to this factor and hence

used prudent inventory management resulting in higher inventory turnover over 2014-2016

despite the falling commodity prices (BHP Billiton, 2016; 2015; 2012).

With regards to receivables turnover, there are only marginal changes which indicate the

ability on part of the company to ensure that the collection period does not increase. Infact,

during FY2015 and FY2016, the receivables turnover ratio is higher than corresponding

value for FY2014 which indicates that the company has taken conscious measures at

lowering the collection period (BHP Billiton, 2016; 2015; 2012). This in turn enables the

lowering of the cash cycle which helps in reduction of working capital money which becomes

6

generating profits when the commodity prices tend to favour which is apparent for 2012

(BHP Billiton, 2016;2015;2012).

Efficiency Ratios

The relevant efficiency ratios for the business over the period under consideration are

highlighted below (BHP Billiton, 2016;2015;2012).

For a robust business, inventory turnover should be high as it tends to convey the ability of

the business to convert the inventory into sales. For a mining business, this is typically not

very high owing to the nature of the business where the ores can be mined from the mines as

per the ongoing demand from the clients and hence the inventory is typically small

(Damodaran, 2008). However, the steps taken by the company to improve inventory

management is apparent especially from 2014 onwards. From FY2013 to FY2014, the

inventory turnover has declined as the offtake was lesser than the expectations of the

company due to the China factor. But the company has since adjusted to this factor and hence

used prudent inventory management resulting in higher inventory turnover over 2014-2016

despite the falling commodity prices (BHP Billiton, 2016; 2015; 2012).

With regards to receivables turnover, there are only marginal changes which indicate the

ability on part of the company to ensure that the collection period does not increase. Infact,

during FY2015 and FY2016, the receivables turnover ratio is higher than corresponding

value for FY2014 which indicates that the company has taken conscious measures at

lowering the collection period (BHP Billiton, 2016; 2015; 2012). This in turn enables the

lowering of the cash cycle which helps in reduction of working capital money which becomes

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUTNING FOR FINANCE & MANAGER

imperative for the company when the commodity cycle is negative (Parrino & Kidwell,

2011).

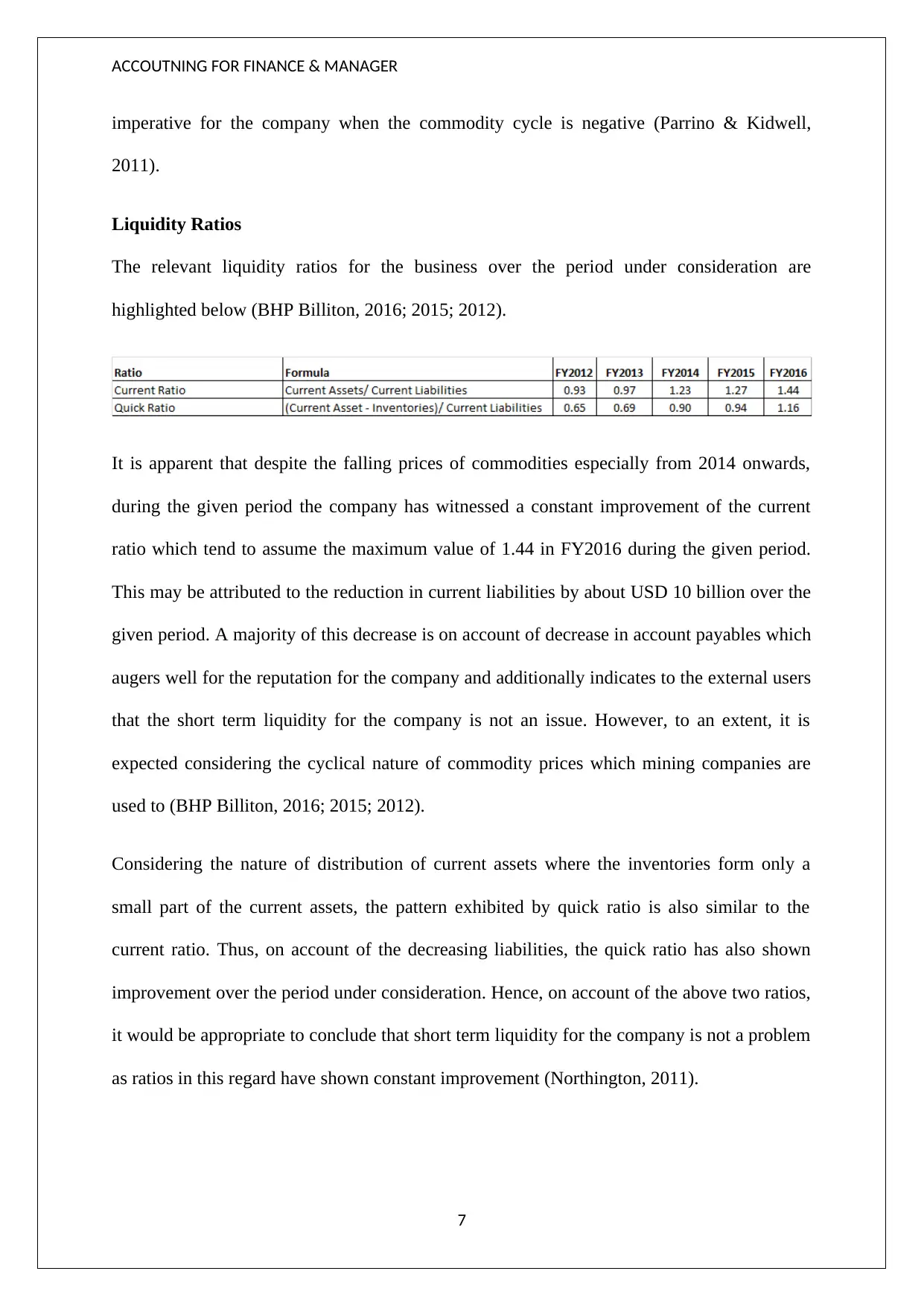

Liquidity Ratios

The relevant liquidity ratios for the business over the period under consideration are

highlighted below (BHP Billiton, 2016; 2015; 2012).

It is apparent that despite the falling prices of commodities especially from 2014 onwards,

during the given period the company has witnessed a constant improvement of the current

ratio which tend to assume the maximum value of 1.44 in FY2016 during the given period.

This may be attributed to the reduction in current liabilities by about USD 10 billion over the

given period. A majority of this decrease is on account of decrease in account payables which

augers well for the reputation for the company and additionally indicates to the external users

that the short term liquidity for the company is not an issue. However, to an extent, it is

expected considering the cyclical nature of commodity prices which mining companies are

used to (BHP Billiton, 2016; 2015; 2012).

Considering the nature of distribution of current assets where the inventories form only a

small part of the current assets, the pattern exhibited by quick ratio is also similar to the

current ratio. Thus, on account of the decreasing liabilities, the quick ratio has also shown

improvement over the period under consideration. Hence, on account of the above two ratios,

it would be appropriate to conclude that short term liquidity for the company is not a problem

as ratios in this regard have shown constant improvement (Northington, 2011).

7

imperative for the company when the commodity cycle is negative (Parrino & Kidwell,

2011).

Liquidity Ratios

The relevant liquidity ratios for the business over the period under consideration are

highlighted below (BHP Billiton, 2016; 2015; 2012).

It is apparent that despite the falling prices of commodities especially from 2014 onwards,

during the given period the company has witnessed a constant improvement of the current

ratio which tend to assume the maximum value of 1.44 in FY2016 during the given period.

This may be attributed to the reduction in current liabilities by about USD 10 billion over the

given period. A majority of this decrease is on account of decrease in account payables which

augers well for the reputation for the company and additionally indicates to the external users

that the short term liquidity for the company is not an issue. However, to an extent, it is

expected considering the cyclical nature of commodity prices which mining companies are

used to (BHP Billiton, 2016; 2015; 2012).

Considering the nature of distribution of current assets where the inventories form only a

small part of the current assets, the pattern exhibited by quick ratio is also similar to the

current ratio. Thus, on account of the decreasing liabilities, the quick ratio has also shown

improvement over the period under consideration. Hence, on account of the above two ratios,

it would be appropriate to conclude that short term liquidity for the company is not a problem

as ratios in this regard have shown constant improvement (Northington, 2011).

7

ACCOUTNING FOR FINANCE & MANAGER

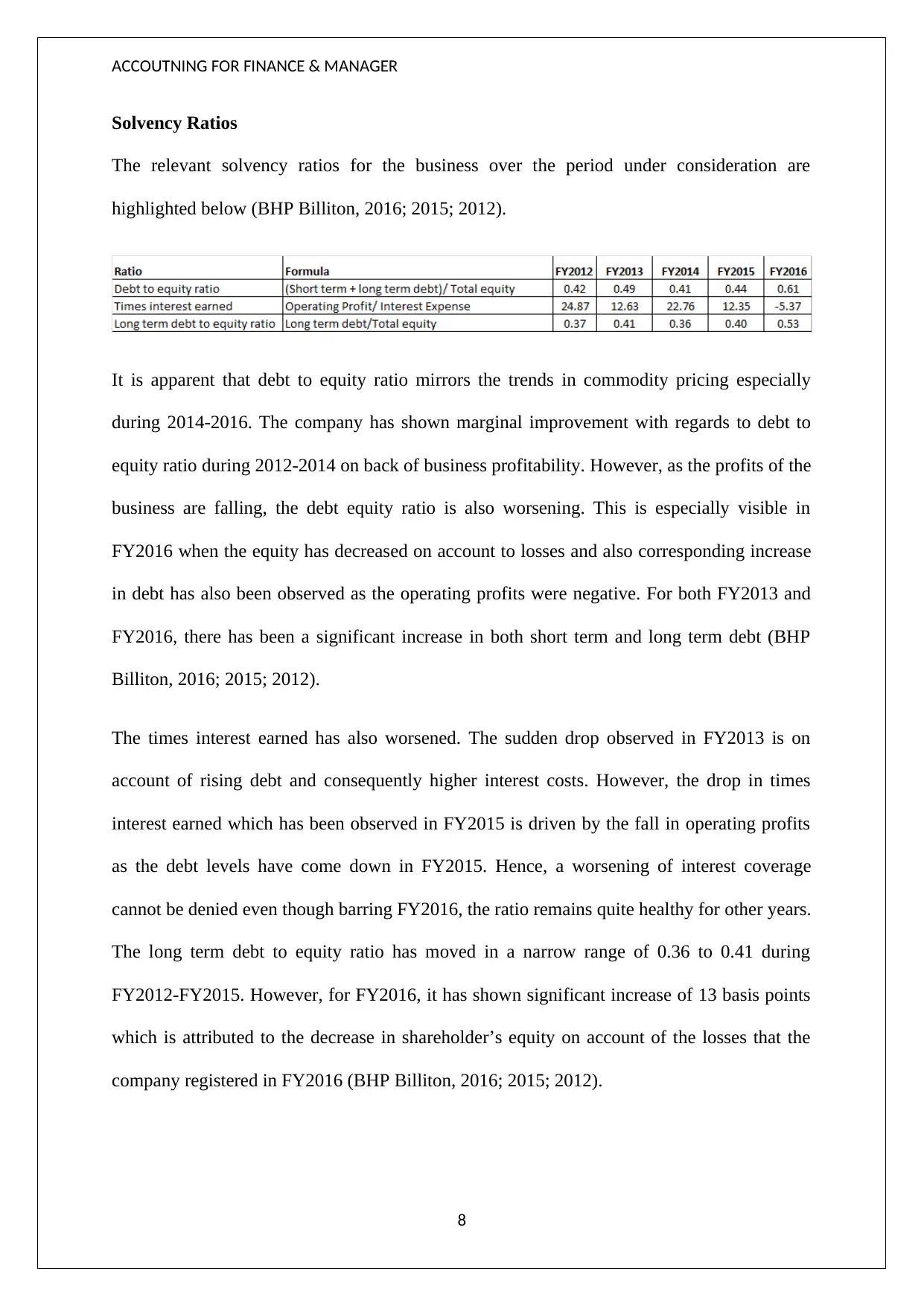

Solvency Ratios

The relevant solvency ratios for the business over the period under consideration are

highlighted below (BHP Billiton, 2016; 2015; 2012).

It is apparent that debt to equity ratio mirrors the trends in commodity pricing especially

during 2014-2016. The company has shown marginal improvement with regards to debt to

equity ratio during 2012-2014 on back of business profitability. However, as the profits of the

business are falling, the debt equity ratio is also worsening. This is especially visible in

FY2016 when the equity has decreased on account to losses and also corresponding increase

in debt has also been observed as the operating profits were negative. For both FY2013 and

FY2016, there has been a significant increase in both short term and long term debt (BHP

Billiton, 2016; 2015; 2012).

The times interest earned has also worsened. The sudden drop observed in FY2013 is on

account of rising debt and consequently higher interest costs. However, the drop in times

interest earned which has been observed in FY2015 is driven by the fall in operating profits

as the debt levels have come down in FY2015. Hence, a worsening of interest coverage

cannot be denied even though barring FY2016, the ratio remains quite healthy for other years.

The long term debt to equity ratio has moved in a narrow range of 0.36 to 0.41 during

FY2012-FY2015. However, for FY2016, it has shown significant increase of 13 basis points

which is attributed to the decrease in shareholder’s equity on account of the losses that the

company registered in FY2016 (BHP Billiton, 2016; 2015; 2012).

8

Solvency Ratios

The relevant solvency ratios for the business over the period under consideration are

highlighted below (BHP Billiton, 2016; 2015; 2012).

It is apparent that debt to equity ratio mirrors the trends in commodity pricing especially

during 2014-2016. The company has shown marginal improvement with regards to debt to

equity ratio during 2012-2014 on back of business profitability. However, as the profits of the

business are falling, the debt equity ratio is also worsening. This is especially visible in

FY2016 when the equity has decreased on account to losses and also corresponding increase

in debt has also been observed as the operating profits were negative. For both FY2013 and

FY2016, there has been a significant increase in both short term and long term debt (BHP

Billiton, 2016; 2015; 2012).

The times interest earned has also worsened. The sudden drop observed in FY2013 is on

account of rising debt and consequently higher interest costs. However, the drop in times

interest earned which has been observed in FY2015 is driven by the fall in operating profits

as the debt levels have come down in FY2015. Hence, a worsening of interest coverage

cannot be denied even though barring FY2016, the ratio remains quite healthy for other years.

The long term debt to equity ratio has moved in a narrow range of 0.36 to 0.41 during

FY2012-FY2015. However, for FY2016, it has shown significant increase of 13 basis points

which is attributed to the decrease in shareholder’s equity on account of the losses that the

company registered in FY2016 (BHP Billiton, 2016; 2015; 2012).

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUTNING FOR FINANCE & MANAGER

CONCLUSION

From the above discussion, it may be concluded that the financial performance of BHP

Billiton is heavily dependent on the commodity prices considering that the cost structure is

largely fixed and hence the overall costs do not undergo a major change. As a result, the

profitability of the business is driven by the commodity price which is apparent in the period

under consideration also. From 2014 onwards, the commodity prices have plummeted and

hence the profitability ratios of the company have worsened leading to losses in FY2016. The

other profitability ratios also are driven by the profits only. In terms of efficiency however,

the company has taken measures to reduce the overall cash cycle so to keep the incremental

financing needs within limits. These measures of the company have worked and

improvement is visible post 2014.

With regards to short term liquidity, the company has shown improvement during the period

as represented from the liquidity ratios. However, the same cannot be said about the long

term liquidity or solvency. The various ratios in this regard have been deterioration especially

in FY2016. However, despite the increasing leverage on the balance sheet, the financial

position continues to remain strong considering the market share and the deep financial

pockets. However, going forward, it is expected that the commodity prices would start

improving as China is coming back on track and hence in the near to medium term, the

commodity prices would firm up. Considering the performance of the company in FY2012, it

may be fair to expect that the company would see better days going ahead in terms of both

the financial performance coupled with market performance.

9

CONCLUSION

From the above discussion, it may be concluded that the financial performance of BHP

Billiton is heavily dependent on the commodity prices considering that the cost structure is

largely fixed and hence the overall costs do not undergo a major change. As a result, the

profitability of the business is driven by the commodity price which is apparent in the period

under consideration also. From 2014 onwards, the commodity prices have plummeted and

hence the profitability ratios of the company have worsened leading to losses in FY2016. The

other profitability ratios also are driven by the profits only. In terms of efficiency however,

the company has taken measures to reduce the overall cash cycle so to keep the incremental

financing needs within limits. These measures of the company have worked and

improvement is visible post 2014.

With regards to short term liquidity, the company has shown improvement during the period

as represented from the liquidity ratios. However, the same cannot be said about the long

term liquidity or solvency. The various ratios in this regard have been deterioration especially

in FY2016. However, despite the increasing leverage on the balance sheet, the financial

position continues to remain strong considering the market share and the deep financial

pockets. However, going forward, it is expected that the commodity prices would start

improving as China is coming back on track and hence in the near to medium term, the

commodity prices would firm up. Considering the performance of the company in FY2012, it

may be fair to expect that the company would see better days going ahead in terms of both

the financial performance coupled with market performance.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUTNING FOR FINANCE & MANAGER

REFERENCES

BHP Billiton (2013), Annual Report 2013, BHP Billiton Website, Retrieved on September

10, 2017 from

http://www.bhp.com/-/media/bhp/documents/investors/reports/2013/bhpbillitonannual

report2013_interactive.pdf?la=en

BHP Billiton (2015), Annual Report 2015, BHP Billiton Website, Retrieved on September

10, 2017 from http://www.bhp.com/~/media/bhp/documents/investors/annual-

reports/2015/bhpbillitonannualreport2015.pdf?la=en

BHP Billiton (2016), Annual Report 2016, BHP Billiton Website, Retrieved on September

10, 2017 from http://www.bhp.com/-/media/bhp/documents/investors/annual-

reports/2016/bhpbillitonannualreport2016_interactive.pdf

Damodaran, A. (2008), Corporate Finance (2nd ed.), London: Wiley Publications

Northington, S. (2011), Finance (6th ed.), New York: Ferguson

Parrino, R. & Kidwell, D. (2011), Fundamentals of Corporate Finance (3rd ed.), London:

Wiley Publications,

Smith, G. (2015, July 24), China’s slowdown pushes commodity prices to new lows, Fortune

Website, Retrieved on September 10, 2017 from

http://fortune.com/2015/07/24/chinas-slowdown-pushes-commodity-prices-to-new-

lows/

10

REFERENCES

BHP Billiton (2013), Annual Report 2013, BHP Billiton Website, Retrieved on September

10, 2017 from

http://www.bhp.com/-/media/bhp/documents/investors/reports/2013/bhpbillitonannual

report2013_interactive.pdf?la=en

BHP Billiton (2015), Annual Report 2015, BHP Billiton Website, Retrieved on September

10, 2017 from http://www.bhp.com/~/media/bhp/documents/investors/annual-

reports/2015/bhpbillitonannualreport2015.pdf?la=en

BHP Billiton (2016), Annual Report 2016, BHP Billiton Website, Retrieved on September

10, 2017 from http://www.bhp.com/-/media/bhp/documents/investors/annual-

reports/2016/bhpbillitonannualreport2016_interactive.pdf

Damodaran, A. (2008), Corporate Finance (2nd ed.), London: Wiley Publications

Northington, S. (2011), Finance (6th ed.), New York: Ferguson

Parrino, R. & Kidwell, D. (2011), Fundamentals of Corporate Finance (3rd ed.), London:

Wiley Publications,

Smith, G. (2015, July 24), China’s slowdown pushes commodity prices to new lows, Fortune

Website, Retrieved on September 10, 2017 from

http://fortune.com/2015/07/24/chinas-slowdown-pushes-commodity-prices-to-new-

lows/

10

ACCOUTNING FOR FINANCE & MANAGER

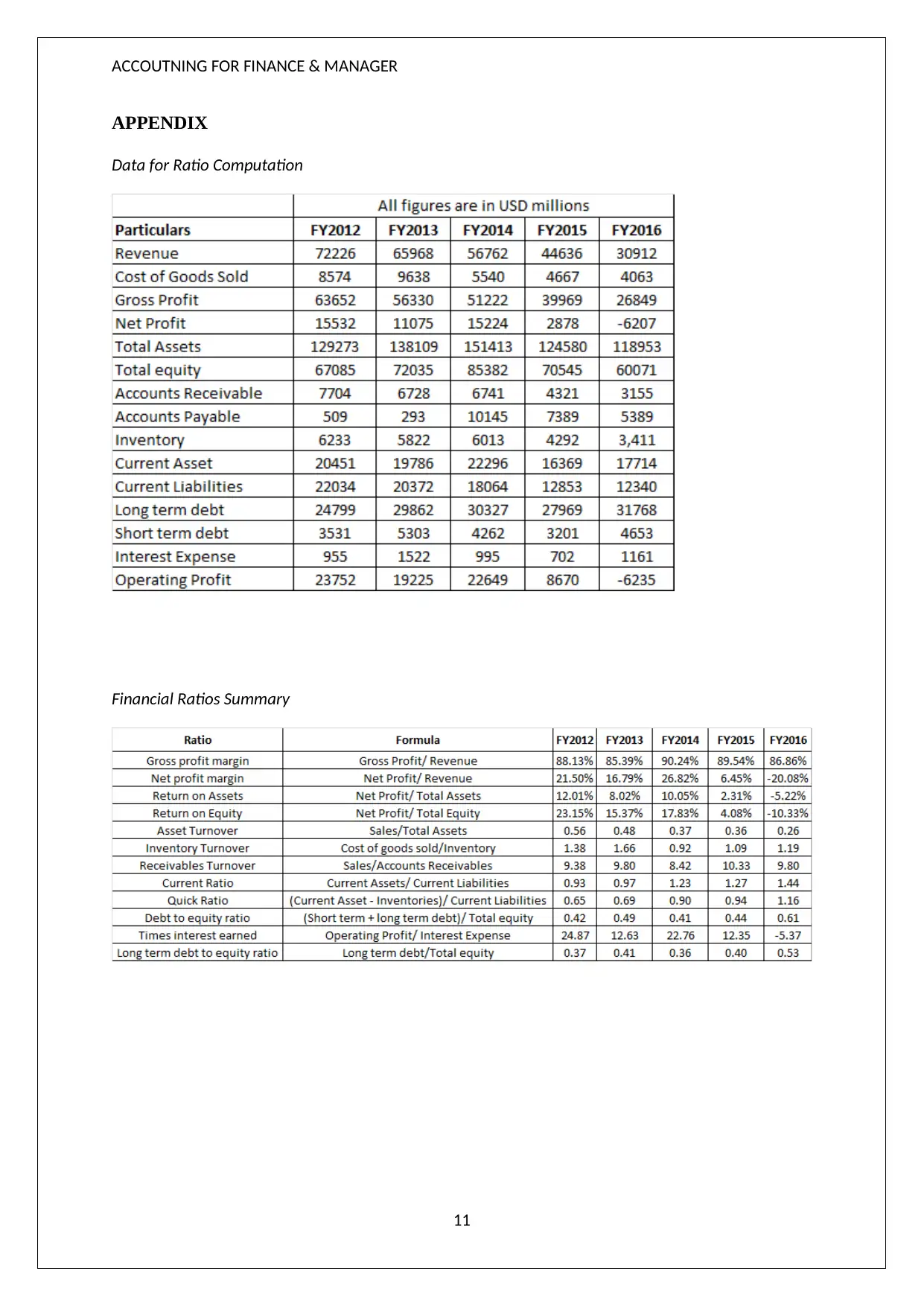

APPENDIX

Data for Ratio Computation

Financial Ratios Summary

11

APPENDIX

Data for Ratio Computation

Financial Ratios Summary

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.