Financial Accounting and Reporting: BHP Impairment Analysis Report

VerifiedAdded on 2023/02/01

|12

|1207

|63

Report

AI Summary

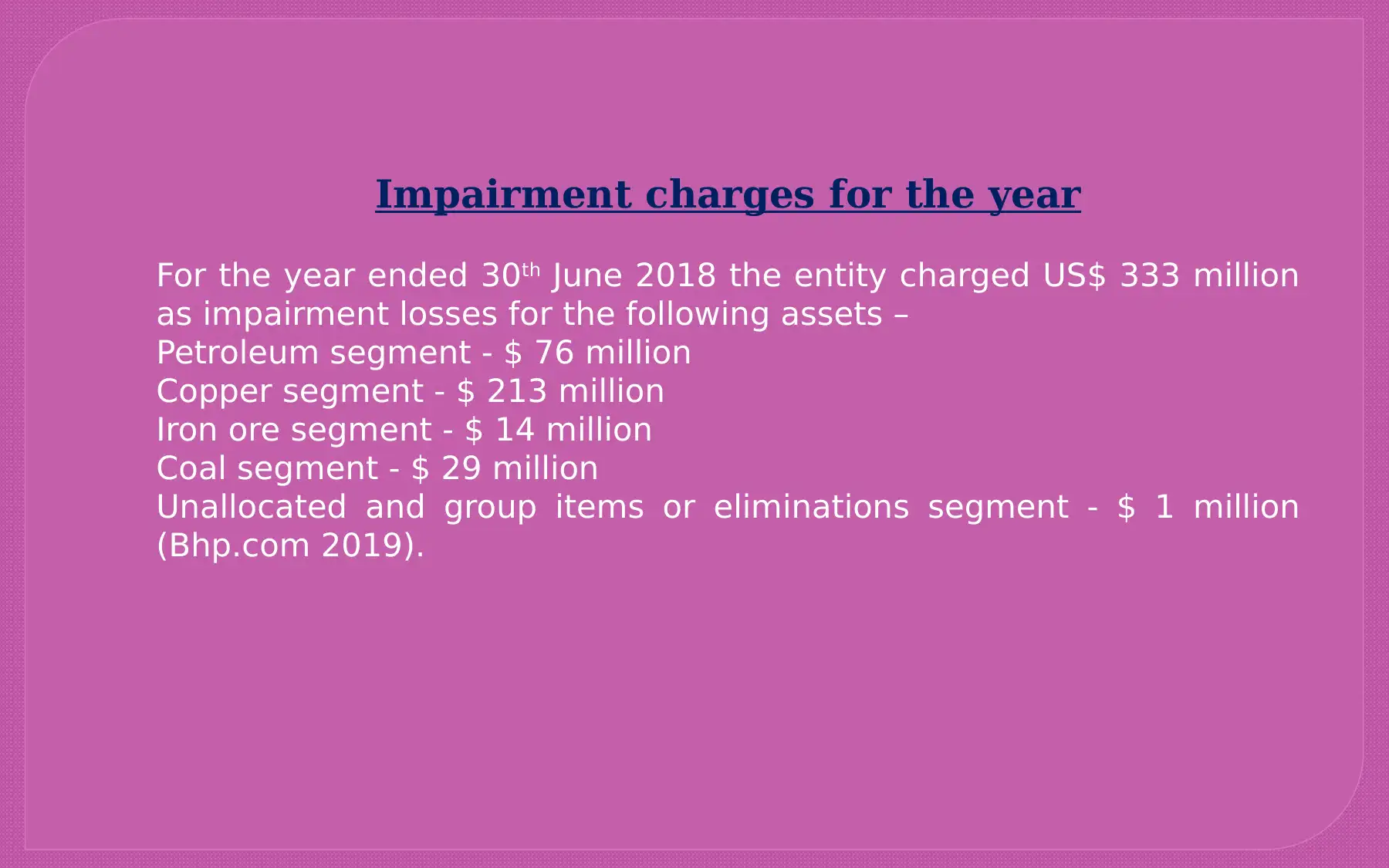

This report provides a detailed analysis of BHP's financial accounting practices, specifically focusing on impairment testing and the application of professional judgment. The report begins with an introduction to BHP, an ASX-listed entity, and its compliance with Australian and international accounting standards (IFRS). It then explores the crucial role of professional judgment in accounting, emphasizing its importance in ensuring regulatory compliance, building trust, and enabling informed decision-making by financial statement users. The report examines BHP's impairment disclosures, valuation methods (including fair value and value in use), and the key estimates and judgments involved in determining recoverable amounts. It highlights the impairment charges for the year ended June 30, 2018, across different segments. Furthermore, the report analyzes how BHP applies professional judgment in estimating cash flows and discount rates, as required by accounting standards. The report concludes by emphasizing that BHP complies with financial reporting requirements, providing relevant, faithfully presented, and complete information. The analysis references various sources to support its findings.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.