8006FMGT - BHP Group Financial Report: Ratio, CCC & Funding

VerifiedAdded on 2022/10/18

|14

|2892

|10

Report

AI Summary

This report provides a financial analysis of BHP Group, focusing on capital structure and profitability ratios over five years. The analysis reveals a deterioration in capital structure ratios due to increased debt and a decline in profitability ratios reflecting weaker business performance. Compared to competitor RIO TINTO, BHP's financial ratios appear weaker. The cash conversion cycle (CCC) improved from 9.32 days to -18.59 days, driven by increased payable days, generally viewed positively. Furthermore, the report explores debt and equity funding options, favoring low-cost debt financing based on BHP's current capital structure, and analyzes the impact of rumors on bond prices and ordinary share value using the Gordon Growth Model.

Running Head: Finance Management

8006FMGT – Finance Management

NAME

STUDENT ID

TITLE OF REPORT

8006FMGT – Finance Management

NAME

STUDENT ID

TITLE OF REPORT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance Management

Executive summary

This report performed the financial analysis of BHP Group. The ratio analysis is done using

the capital structure and profitability ratios for the last five years. All the major capital

structure ratios have deteriorated as the debt portion of the balance sheet has increased

over this period. Also the profitability ratios have deteriorated as the company’s business

performance went down. In comparison to its competitor RIO TINTO, the financial ratios of

BHP were weaker. The report also performed the calculation of the cash conversion cycle of

BHP and it found that the CCC has declined from 9.32 days to -18.59 days due to the

increase in days of payables. This is generally taken as a positive for the firm. The document

also performed analysis of debt and equity funding and it found that the low cost debt

financing is preferable for BHP depending upon the current capital structure.

Page 2

Executive summary

This report performed the financial analysis of BHP Group. The ratio analysis is done using

the capital structure and profitability ratios for the last five years. All the major capital

structure ratios have deteriorated as the debt portion of the balance sheet has increased

over this period. Also the profitability ratios have deteriorated as the company’s business

performance went down. In comparison to its competitor RIO TINTO, the financial ratios of

BHP were weaker. The report also performed the calculation of the cash conversion cycle of

BHP and it found that the CCC has declined from 9.32 days to -18.59 days due to the

increase in days of payables. This is generally taken as a positive for the firm. The document

also performed analysis of debt and equity funding and it found that the low cost debt

financing is preferable for BHP depending upon the current capital structure.

Page 2

Finance Management

Table of Contents

Executive summary............................................................................................................... 2

1. Introduction................................................................................................................... 4

2. Financial Ratio Analysis.................................................................................................5

2.1 Capital Structure Ratios Analysis............................................................................ 6

2.2 Profitability Ratios Analysis.................................................................................... 6

2.3 Areas for improvement for BHP and appropriate actions......................................7

2.4 BHP comparison with RIO TINTO............................................................................7

3. Cash conversion cycle of BHP........................................................................................9

4. Analysis of debt and equity funding............................................................................ 10

4.1 Price of the bond before and after the rumour and the expected change in the

price of the bond............................................................................................................. 10

4.2 Value of the ordinary share..................................................................................11

4.3 Relationship between the coupon interest rate and yield to maturity and the

market value of a bond...................................................................................................11

4.4 Funding decision between equity and debt on the basis of BHP’s current capital

structure......................................................................................................................... 12

5. Conclusion................................................................................................................... 13

References.......................................................................................................................... 14

Page 3

Table of Contents

Executive summary............................................................................................................... 2

1. Introduction................................................................................................................... 4

2. Financial Ratio Analysis.................................................................................................5

2.1 Capital Structure Ratios Analysis............................................................................ 6

2.2 Profitability Ratios Analysis.................................................................................... 6

2.3 Areas for improvement for BHP and appropriate actions......................................7

2.4 BHP comparison with RIO TINTO............................................................................7

3. Cash conversion cycle of BHP........................................................................................9

4. Analysis of debt and equity funding............................................................................ 10

4.1 Price of the bond before and after the rumour and the expected change in the

price of the bond............................................................................................................. 10

4.2 Value of the ordinary share..................................................................................11

4.3 Relationship between the coupon interest rate and yield to maturity and the

market value of a bond...................................................................................................11

4.4 Funding decision between equity and debt on the basis of BHP’s current capital

structure......................................................................................................................... 12

5. Conclusion................................................................................................................... 13

References.......................................................................................................................... 14

Page 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance Management

1. Introduction

The report performs the financial analysis of BHP, a global resources company based in

Australia. To perform the ratio analysis it uses profitability and capital structure ratios like

net profit margin, return on assets, return on equity, debt to equity ratio, debt ratio, equity

ratio and debt coverage ratio. Trend analysis of these ratios is used to determine the

deterioration or strengthening of BHP’s business. These ratios are also compared with its

competitor RIO TINTO. Then the cash conversion cycle of BHP is analysed over last five years

to check if there is any change in it. Then the report analyses the different kind of funding

available to the firm. The price of the bond is measured before and after the change in YTM

due to the rumour. The value of ordinary share is also determined using Gordon growth

model. Then the current capital structure of BHP is analysed to decide between the debt

and equity funding.

Page 4

1. Introduction

The report performs the financial analysis of BHP, a global resources company based in

Australia. To perform the ratio analysis it uses profitability and capital structure ratios like

net profit margin, return on assets, return on equity, debt to equity ratio, debt ratio, equity

ratio and debt coverage ratio. Trend analysis of these ratios is used to determine the

deterioration or strengthening of BHP’s business. These ratios are also compared with its

competitor RIO TINTO. Then the cash conversion cycle of BHP is analysed over last five years

to check if there is any change in it. Then the report analyses the different kind of funding

available to the firm. The price of the bond is measured before and after the change in YTM

due to the rumour. The value of ordinary share is also determined using Gordon growth

model. Then the current capital structure of BHP is analysed to decide between the debt

and equity funding.

Page 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance Management

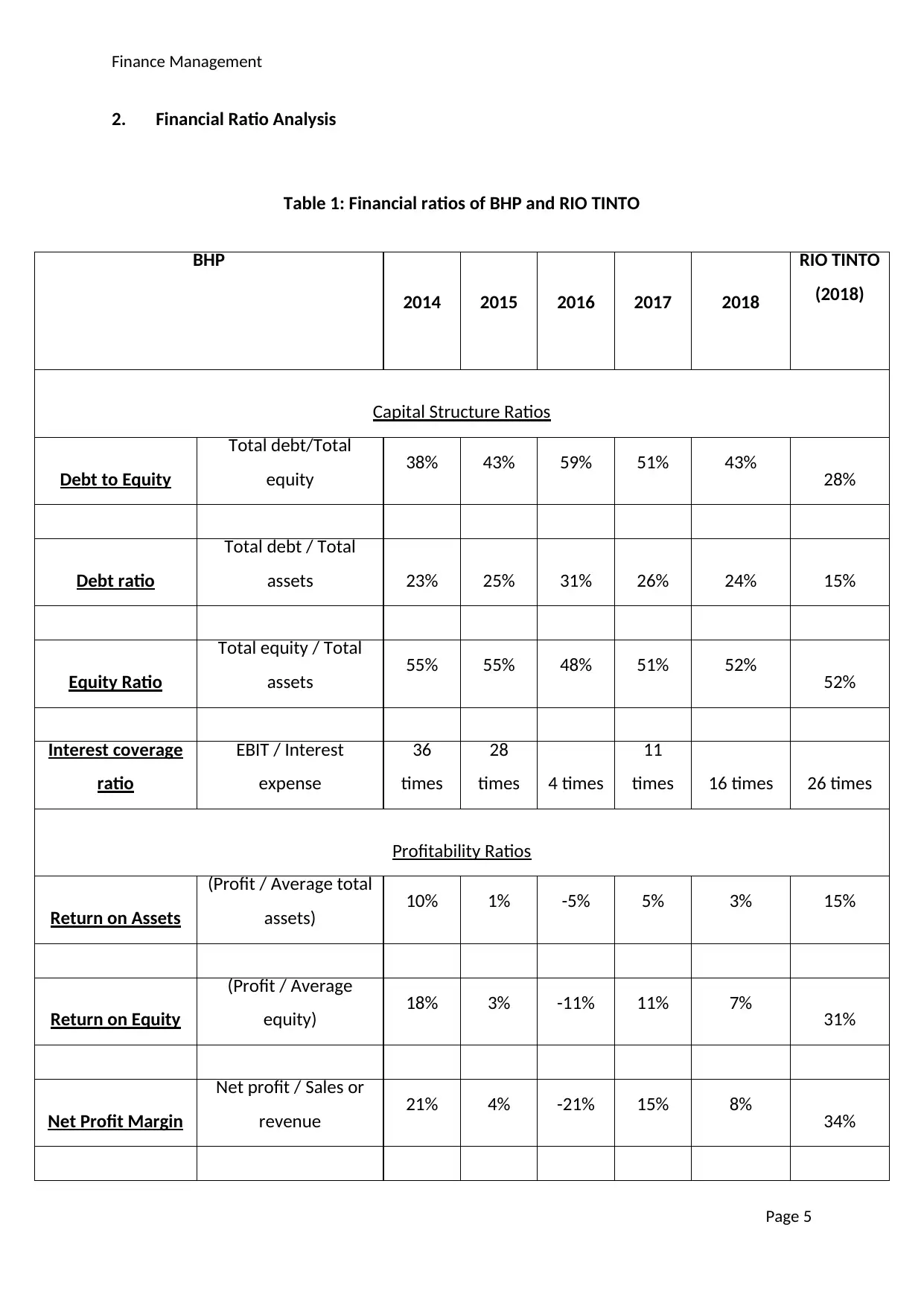

2. Financial Ratio Analysis

Table 1: Financial ratios of BHP and RIO TINTO

Page 5

BHP

2014 2015 2016 2017 2018

RIO TINTO

(2018)

Capital Structure Ratios

Debt to Equity

Total debt/Total

equity 38% 43% 59% 51% 43% 28%

Debt ratio

Total debt / Total

assets 23% 25% 31% 26% 24% 15%

Equity Ratio

Total equity / Total

assets 55% 55% 48% 51% 52% 52%

Interest coverage

ratio

EBIT / Interest

expense

36

times

28

times 4 times

11

times 16 times 26 times

Profitability Ratios

Return on Assets

(Profit / Average total

assets) 10% 1% -5% 5% 3% 15%

Return on Equity

(Profit / Average

equity) 18% 3% -11% 11% 7% 31%

Net Profit Margin

Net profit / Sales or

revenue 21% 4% -21% 15% 8% 34%

2. Financial Ratio Analysis

Table 1: Financial ratios of BHP and RIO TINTO

Page 5

BHP

2014 2015 2016 2017 2018

RIO TINTO

(2018)

Capital Structure Ratios

Debt to Equity

Total debt/Total

equity 38% 43% 59% 51% 43% 28%

Debt ratio

Total debt / Total

assets 23% 25% 31% 26% 24% 15%

Equity Ratio

Total equity / Total

assets 55% 55% 48% 51% 52% 52%

Interest coverage

ratio

EBIT / Interest

expense

36

times

28

times 4 times

11

times 16 times 26 times

Profitability Ratios

Return on Assets

(Profit / Average total

assets) 10% 1% -5% 5% 3% 15%

Return on Equity

(Profit / Average

equity) 18% 3% -11% 11% 7% 31%

Net Profit Margin

Net profit / Sales or

revenue 21% 4% -21% 15% 8% 34%

Finance Management

Source: Morningstar, (n.d.).

2.1 Capital Structure Ratios Analysis

The trend analysis of various capital structure ratios shows that BHP condition has

deteriorated a little in terms of capital structure. Debt to equity ratio tells about the overall

capital structure of the firm that is debt in proportion to the equity (Atrill and McLaney,

2019). BHP's debt to equity ratio has increased from 38% in 2014 to 43% in 2018. BHP

maybe using debt for making the capital investments for its business expansion as it is a

cheap source of funds but the raising value of debt in the capital structure can put

additional pressure on the firm's performance particularly in bad times. Debt ratio increased

in this time period but this increase was little as the asset base of the firm has also been

expanding. The equity ratio of BHP has decreased from 55% in 2014 to 52% in 2018 as the

firm might have been using debt financing for its capital investments. This decreases the

firm's ownership of these assets and can create financial problems. The interest coverage

ratio of BHP has declined drastically from 36 times in 2014 to 16 times in 2018. This ratio

measures the ability of the firm to meet its interest obligations using its operating income.

The declining interest coverage ratio can create major issues for BHP as it may find it

difficult to pay interest obligations from its core business operations, which can make the

company insolvent.

2.2 Profitability Ratios Analysis

The trend analysis of probability ratios shows that the profitability of BHP deteriorated from

2014 to 2018. Return on Assets decreased from 10% in 2014 to 3% in 2018. So, the firm's

ability to generated profits from its assets has decreased. Similarly its return on equity

decreased from 18% to 7% in 2018. It tells that BHP was not able to produce good returns

for its equity holders. Net profit margin considers all the incomes and expenses of the firm

and measures how much proportion of the total revenues is represented by its bottom line.

This ratio decreased a lot from 21% in 2014 to 8% in 2018 and the ratio remained quite

volatile during this period. Gross profit margin tells about the profit firm is generating from

Page 6

Gross Profit

Margin

Gross profit / Sales or

revenue 52% 46% 39% 56% 61% 50%

Source: Morningstar, (n.d.).

2.1 Capital Structure Ratios Analysis

The trend analysis of various capital structure ratios shows that BHP condition has

deteriorated a little in terms of capital structure. Debt to equity ratio tells about the overall

capital structure of the firm that is debt in proportion to the equity (Atrill and McLaney,

2019). BHP's debt to equity ratio has increased from 38% in 2014 to 43% in 2018. BHP

maybe using debt for making the capital investments for its business expansion as it is a

cheap source of funds but the raising value of debt in the capital structure can put

additional pressure on the firm's performance particularly in bad times. Debt ratio increased

in this time period but this increase was little as the asset base of the firm has also been

expanding. The equity ratio of BHP has decreased from 55% in 2014 to 52% in 2018 as the

firm might have been using debt financing for its capital investments. This decreases the

firm's ownership of these assets and can create financial problems. The interest coverage

ratio of BHP has declined drastically from 36 times in 2014 to 16 times in 2018. This ratio

measures the ability of the firm to meet its interest obligations using its operating income.

The declining interest coverage ratio can create major issues for BHP as it may find it

difficult to pay interest obligations from its core business operations, which can make the

company insolvent.

2.2 Profitability Ratios Analysis

The trend analysis of probability ratios shows that the profitability of BHP deteriorated from

2014 to 2018. Return on Assets decreased from 10% in 2014 to 3% in 2018. So, the firm's

ability to generated profits from its assets has decreased. Similarly its return on equity

decreased from 18% to 7% in 2018. It tells that BHP was not able to produce good returns

for its equity holders. Net profit margin considers all the incomes and expenses of the firm

and measures how much proportion of the total revenues is represented by its bottom line.

This ratio decreased a lot from 21% in 2014 to 8% in 2018 and the ratio remained quite

volatile during this period. Gross profit margin tells about the profit firm is generating from

Page 6

Gross Profit

Margin

Gross profit / Sales or

revenue 52% 46% 39% 56% 61% 50%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance Management

its core business operations. It only considers the direct costs related to the revenues so it is

not affected by the other operating and non-operating activities. This ratio actually

improved over this period which shows that the firm's core operations have been

improving. It can be noticed from the overall trend analysis of profitability ratios that the

firm's core operations have improved but the net profits deteriorated. This can be because

of some short term non-operating costs arising because of losses on discontinued

operations.

2.3 Areas for improvement for BHP and appropriate actions

BHP's capital structure ratios have deteriorated but they are still in an acceptable range. The

change in one capital ratio that is most worrying is the fall in interest coverage ratio. This

can be due to the falling profitability of the firm's overall operations. If the BHP's business

does not improve in the coming time and it keeps on taking more debt, the firm can become

insolvent. So, the firm should try to make it business more sustainable by cutting off

unnecessary costs and focusing on its core business, which is still moving in the right

direction.

2.4 BHP comparison with RIO TINTO

The overall financial health and the business performance of BHP are weaker in comparison

to its competitor RIO TINTO. Almost all the capital structure ratios of BHP are higher that

RIO TINTO, which shows that BHP has taken more financial leverage. Higher proportion of

debt in the capital structure of BHP can be due to its business strategy of using low cost

debt funding for expanding its business but the issue is that its interest coverage ratio of 16

times is quite lower than RIO TINTO's ratio of 26 times. So, BHP's operating profits are not

increasing in proportion to the increasing interest costs. This can result it huge financial

problems in future. All the profitability ratios of BHP are lower than RIO TINTO except the

gross profit margins. That tells that BHP's overall profits are going down in spite of strong

core operations. Therefore, BHP needs to improve its overall business operations to make

the firm sustainable and profitable.

2.5 Relationship between capital structure and profitability ratios

Page 7

its core business operations. It only considers the direct costs related to the revenues so it is

not affected by the other operating and non-operating activities. This ratio actually

improved over this period which shows that the firm's core operations have been

improving. It can be noticed from the overall trend analysis of profitability ratios that the

firm's core operations have improved but the net profits deteriorated. This can be because

of some short term non-operating costs arising because of losses on discontinued

operations.

2.3 Areas for improvement for BHP and appropriate actions

BHP's capital structure ratios have deteriorated but they are still in an acceptable range. The

change in one capital ratio that is most worrying is the fall in interest coverage ratio. This

can be due to the falling profitability of the firm's overall operations. If the BHP's business

does not improve in the coming time and it keeps on taking more debt, the firm can become

insolvent. So, the firm should try to make it business more sustainable by cutting off

unnecessary costs and focusing on its core business, which is still moving in the right

direction.

2.4 BHP comparison with RIO TINTO

The overall financial health and the business performance of BHP are weaker in comparison

to its competitor RIO TINTO. Almost all the capital structure ratios of BHP are higher that

RIO TINTO, which shows that BHP has taken more financial leverage. Higher proportion of

debt in the capital structure of BHP can be due to its business strategy of using low cost

debt funding for expanding its business but the issue is that its interest coverage ratio of 16

times is quite lower than RIO TINTO's ratio of 26 times. So, BHP's operating profits are not

increasing in proportion to the increasing interest costs. This can result it huge financial

problems in future. All the profitability ratios of BHP are lower than RIO TINTO except the

gross profit margins. That tells that BHP's overall profits are going down in spite of strong

core operations. Therefore, BHP needs to improve its overall business operations to make

the firm sustainable and profitable.

2.5 Relationship between capital structure and profitability ratios

Page 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance Management

A negative relationship between the capital structure ratios and profitability ratios can be

identified from the trend analysis of these ratios. As the capital structure ratios increased

from 2014 to 2018 that means the proportion of debt increased during this period. This

provide the firm with the low cost debt capital for making capital investments but the firm

was not able to use these investments efficiently as the profitability ratios decreased. The

decrease in the profitability can also be due to the increase in fixed interest costs that

creates pressure on the firm. The financial risk of the firm increases with the increase in

debt because the firm needs to make fixed payments in spite of the business conditions. If

the return generated from these debt investments is not in line with the undertaken risk,

then the profitability of the firm will reduce.

3. Cash conversion cycle of BHP

Page 8

A negative relationship between the capital structure ratios and profitability ratios can be

identified from the trend analysis of these ratios. As the capital structure ratios increased

from 2014 to 2018 that means the proportion of debt increased during this period. This

provide the firm with the low cost debt capital for making capital investments but the firm

was not able to use these investments efficiently as the profitability ratios decreased. The

decrease in the profitability can also be due to the increase in fixed interest costs that

creates pressure on the firm. The financial risk of the firm increases with the increase in

debt because the firm needs to make fixed payments in spite of the business conditions. If

the return generated from these debt investments is not in line with the undertaken risk,

then the profitability of the firm will reduce.

3. Cash conversion cycle of BHP

Page 8

Finance Management

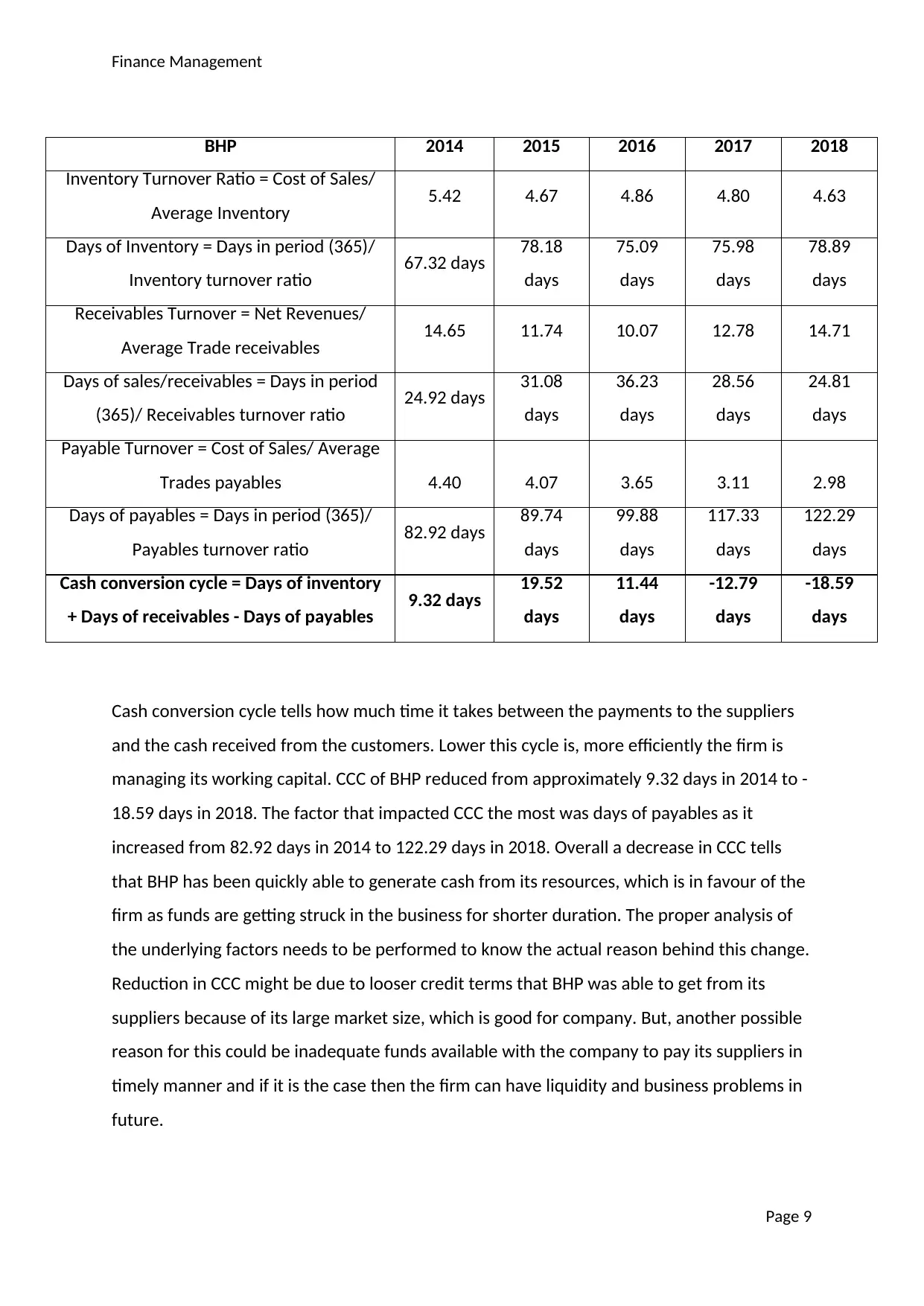

Cash conversion cycle tells how much time it takes between the payments to the suppliers

and the cash received from the customers. Lower this cycle is, more efficiently the firm is

managing its working capital. CCC of BHP reduced from approximately 9.32 days in 2014 to -

18.59 days in 2018. The factor that impacted CCC the most was days of payables as it

increased from 82.92 days in 2014 to 122.29 days in 2018. Overall a decrease in CCC tells

that BHP has been quickly able to generate cash from its resources, which is in favour of the

firm as funds are getting struck in the business for shorter duration. The proper analysis of

the underlying factors needs to be performed to know the actual reason behind this change.

Reduction in CCC might be due to looser credit terms that BHP was able to get from its

suppliers because of its large market size, which is good for company. But, another possible

reason for this could be inadequate funds available with the company to pay its suppliers in

timely manner and if it is the case then the firm can have liquidity and business problems in

future.

Page 9

BHP 2014 2015 2016 2017 2018

Inventory Turnover Ratio = Cost of Sales/

Average Inventory 5.42 4.67 4.86 4.80 4.63

Days of Inventory = Days in period (365)/

Inventory turnover ratio 67.32 days 78.18

days

75.09

days

75.98

days

78.89

days

Receivables Turnover = Net Revenues/

Average Trade receivables 14.65 11.74 10.07 12.78 14.71

Days of sales/receivables = Days in period

(365)/ Receivables turnover ratio 24.92 days 31.08

days

36.23

days

28.56

days

24.81

days

Payable Turnover = Cost of Sales/ Average

Trades payables 4.40 4.07 3.65 3.11 2.98

Days of payables = Days in period (365)/

Payables turnover ratio 82.92 days 89.74

days

99.88

days

117.33

days

122.29

days

Cash conversion cycle = Days of inventory

+ Days of receivables - Days of payables 9.32 days 19.52

days

11.44

days

-12.79

days

-18.59

days

Cash conversion cycle tells how much time it takes between the payments to the suppliers

and the cash received from the customers. Lower this cycle is, more efficiently the firm is

managing its working capital. CCC of BHP reduced from approximately 9.32 days in 2014 to -

18.59 days in 2018. The factor that impacted CCC the most was days of payables as it

increased from 82.92 days in 2014 to 122.29 days in 2018. Overall a decrease in CCC tells

that BHP has been quickly able to generate cash from its resources, which is in favour of the

firm as funds are getting struck in the business for shorter duration. The proper analysis of

the underlying factors needs to be performed to know the actual reason behind this change.

Reduction in CCC might be due to looser credit terms that BHP was able to get from its

suppliers because of its large market size, which is good for company. But, another possible

reason for this could be inadequate funds available with the company to pay its suppliers in

timely manner and if it is the case then the firm can have liquidity and business problems in

future.

Page 9

BHP 2014 2015 2016 2017 2018

Inventory Turnover Ratio = Cost of Sales/

Average Inventory 5.42 4.67 4.86 4.80 4.63

Days of Inventory = Days in period (365)/

Inventory turnover ratio 67.32 days 78.18

days

75.09

days

75.98

days

78.89

days

Receivables Turnover = Net Revenues/

Average Trade receivables 14.65 11.74 10.07 12.78 14.71

Days of sales/receivables = Days in period

(365)/ Receivables turnover ratio 24.92 days 31.08

days

36.23

days

28.56

days

24.81

days

Payable Turnover = Cost of Sales/ Average

Trades payables 4.40 4.07 3.65 3.11 2.98

Days of payables = Days in period (365)/

Payables turnover ratio 82.92 days 89.74

days

99.88

days

117.33

days

122.29

days

Cash conversion cycle = Days of inventory

+ Days of receivables - Days of payables 9.32 days 19.52

days

11.44

days

-12.79

days

-18.59

days

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance Management

4. Analysis of debt and equity funding

4.1 Price of the bond before and after the rumour and the expected change in the price

of the bond

BOND

Face-value $1,000.00

Annual Coupon Rate 14%

Interest/Coupon frequency Semi-annually

Semi-annual interest rate 7%

Semi-annual coupon payment $70.00

Starting YTM (current) (per annum) 12%

Semi-annual YTM 6%

Maturity Time (years) 10

Semi-annual periods 20

Price of the bond

$1,114.70

New YTM 15%

Semi-annual

7

.5%

Price of the bond according to the new YTM

$949.03

Expected Change in price = (new price-old

price)/ old price -14.86%

Page 10

4. Analysis of debt and equity funding

4.1 Price of the bond before and after the rumour and the expected change in the price

of the bond

BOND

Face-value $1,000.00

Annual Coupon Rate 14%

Interest/Coupon frequency Semi-annually

Semi-annual interest rate 7%

Semi-annual coupon payment $70.00

Starting YTM (current) (per annum) 12%

Semi-annual YTM 6%

Maturity Time (years) 10

Semi-annual periods 20

Price of the bond

$1,114.70

New YTM 15%

Semi-annual

7

.5%

Price of the bond according to the new YTM

$949.03

Expected Change in price = (new price-old

price)/ old price -14.86%

Page 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance Management

YTM increases after the rumour that the credit rating of the firm will decrease because the

future cash-flows will appear more risky in the present term. So, the investors now need

higher return for taking this increased risk. This will result in the decrease in the bond price

by 14.86% because the future payments from the bond will now be discounted at higher

rate.

4.2 Value of the ordinary share

Ordinary Stock

Current Dividend $1.20

Future constant growth 8%

Required rate of return 15%

Value according to the Gordon growth model = (Current Dividend * (1+Growth

Rate))/(Required Return-Growth Rate) = $18.51

4.3 Relationship between the coupon interest rate and yield to maturity and the

market value of a bond

If YTM is less than the coupon rate then the Market-Value of the bond is greater than the

Face-Value of the bond (Premium bond) as the periodic rate used to discount the future

values is less than the rate according to which the periodic payments are calculated. If YTM

is equal to the coupon rate then the market value of the bond is equal to the face value of

the bond (Par bond). If YTM is greater than the coupon rate then the market value of the

bond is less than the face value of the bond (Discount bond) as the periodic rate used to

discount the future values is higher than the rate according to which the periodic payments

are calculated.

Page 11

In the case of the above bond:

Before rumour, YTM of 12% p.a. < annual coupon rate of 14%. So, the market value of

the bond of $1114.70 > face value of the bond of $1000. (Premium Bond)

YTM increases after the rumour that the credit rating of the firm will decrease because the

future cash-flows will appear more risky in the present term. So, the investors now need

higher return for taking this increased risk. This will result in the decrease in the bond price

by 14.86% because the future payments from the bond will now be discounted at higher

rate.

4.2 Value of the ordinary share

Ordinary Stock

Current Dividend $1.20

Future constant growth 8%

Required rate of return 15%

Value according to the Gordon growth model = (Current Dividend * (1+Growth

Rate))/(Required Return-Growth Rate) = $18.51

4.3 Relationship between the coupon interest rate and yield to maturity and the

market value of a bond

If YTM is less than the coupon rate then the Market-Value of the bond is greater than the

Face-Value of the bond (Premium bond) as the periodic rate used to discount the future

values is less than the rate according to which the periodic payments are calculated. If YTM

is equal to the coupon rate then the market value of the bond is equal to the face value of

the bond (Par bond). If YTM is greater than the coupon rate then the market value of the

bond is less than the face value of the bond (Discount bond) as the periodic rate used to

discount the future values is higher than the rate according to which the periodic payments

are calculated.

Page 11

In the case of the above bond:

Before rumour, YTM of 12% p.a. < annual coupon rate of 14%. So, the market value of

the bond of $1114.70 > face value of the bond of $1000. (Premium Bond)

Finance Management

4.4 Funding decision between equity and debt on the basis of BHP’s current capital

structure

The debt funding provides cheap source of equity for the companies as compared to the

equity funding as there is lower risk for the capital providers because of the fixed payments

and collateral. Here, after tax cost of debt of the company is 9.8% which is lower than

required return of equity of 15%. The company's Debt to equity ratio is approximately 43%.

So, the company can easily issue more debt without negatively affecting its gearing position

and so it will not pose much financial leverage risk. Therefore, it makes sense for BHP to

choose debt funding over equity funding.

Page 12

After rumour, YTM of 15% p.a. > annual coupon rate of 14%. So, the market value of

the bond of $949.03 < face value of the bond of $1000. (Discount Bond)

After tax cost of debt (using Australian corporate tax rate of 30%) 9.80%

Cost of equity 15%

4.4 Funding decision between equity and debt on the basis of BHP’s current capital

structure

The debt funding provides cheap source of equity for the companies as compared to the

equity funding as there is lower risk for the capital providers because of the fixed payments

and collateral. Here, after tax cost of debt of the company is 9.8% which is lower than

required return of equity of 15%. The company's Debt to equity ratio is approximately 43%.

So, the company can easily issue more debt without negatively affecting its gearing position

and so it will not pose much financial leverage risk. Therefore, it makes sense for BHP to

choose debt funding over equity funding.

Page 12

After rumour, YTM of 15% p.a. > annual coupon rate of 14%. So, the market value of

the bond of $949.03 < face value of the bond of $1000. (Discount Bond)

After tax cost of debt (using Australian corporate tax rate of 30%) 9.80%

Cost of equity 15%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.