Billabong Limited Financial Health: Detailed Ratio Analysis Report

VerifiedAdded on 2023/06/11

|5

|1246

|421

Report

AI Summary

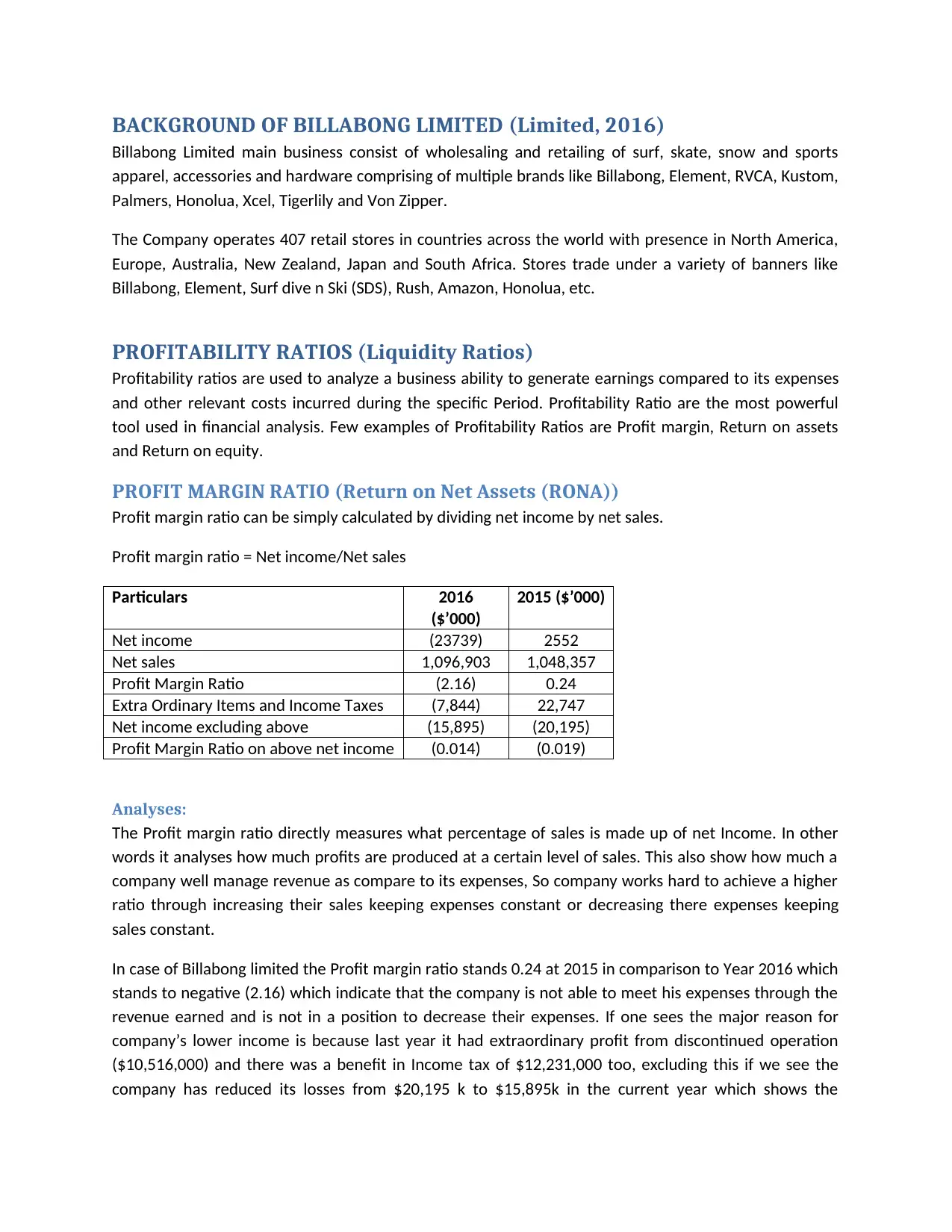

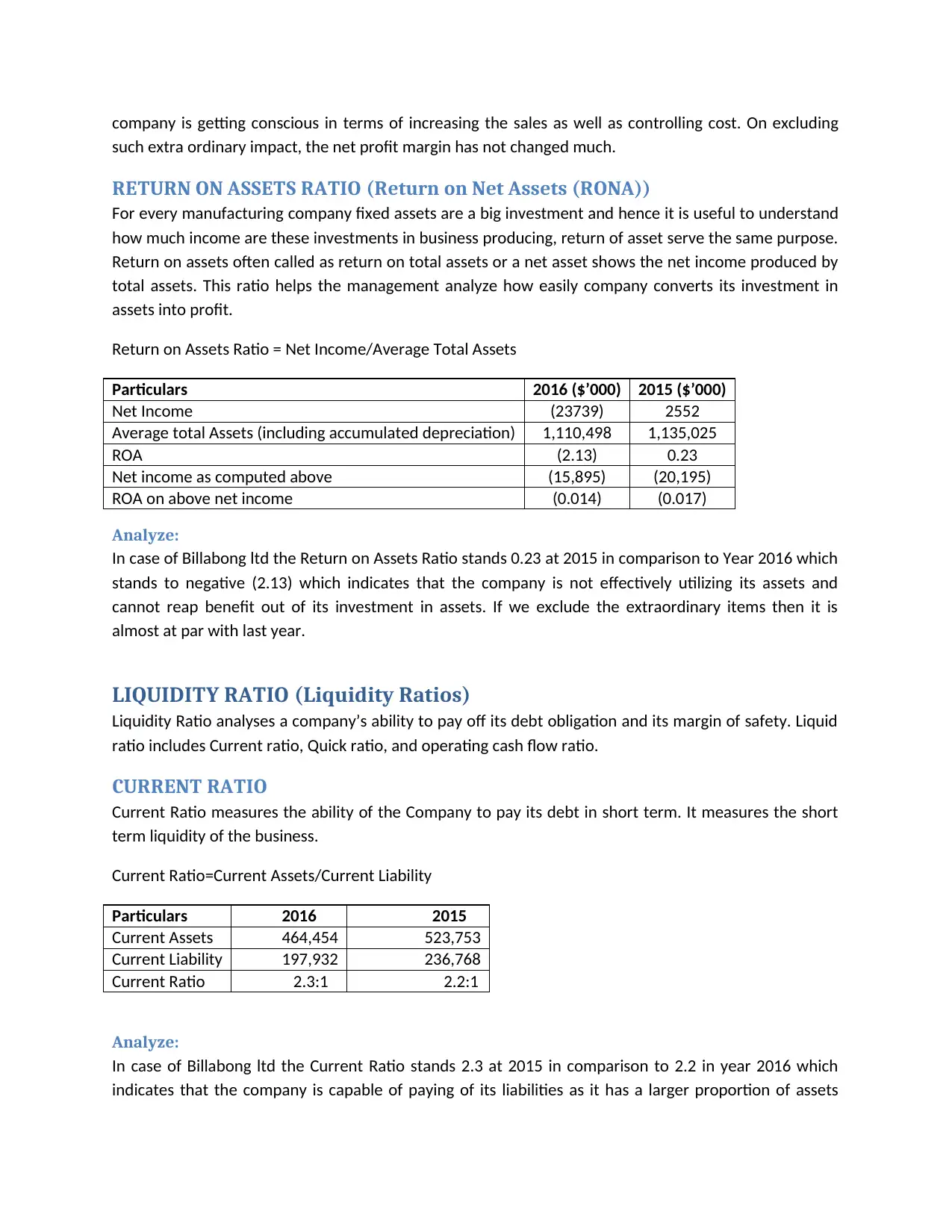

This report provides a comprehensive financial ratio analysis of Billabong Limited, focusing on profitability and liquidity. It examines key ratios such as profit margin, return on assets, current ratio, and quick ratio, comparing the company's performance in 2015 and 2016. The analysis reveals a decline in profitability and return on assets in 2016, attributed to the absence of extraordinary profits from discontinued operations and income tax benefits. Despite this, the company has reduced its losses, indicating improved cost control and sales strategies. The liquidity ratios, including current and quick ratios, suggest that Billabong Limited is capable of meeting its short-term obligations, with a slightly improved current ratio in 2016. The report references Billabong Limited's financial report and other sources to support its findings.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.