Detailed Analysis of Binomial Tree and Option Pricing for MMAF514

VerifiedAdded on 2022/11/09

|6

|1125

|97

Homework Assignment

AI Summary

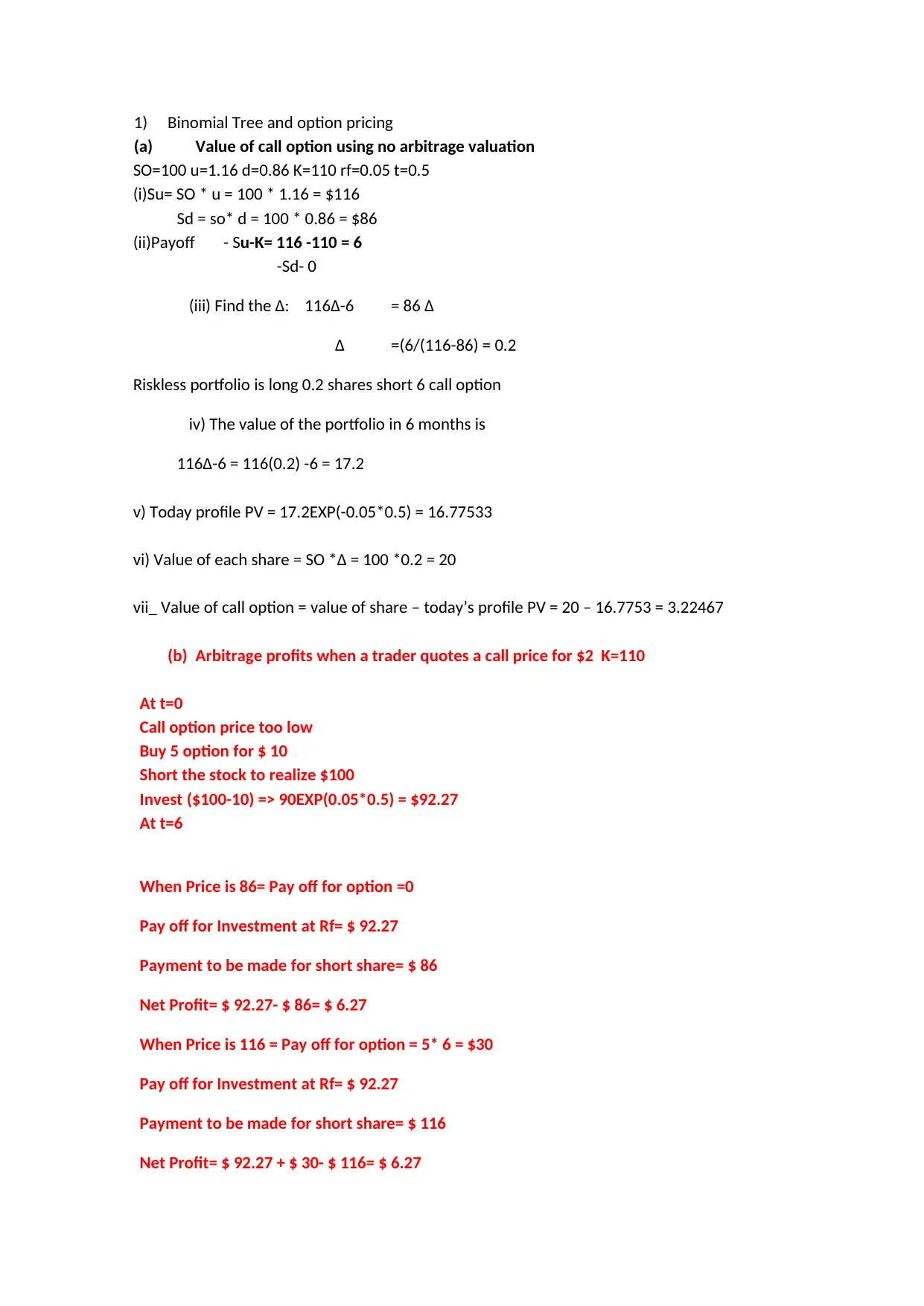

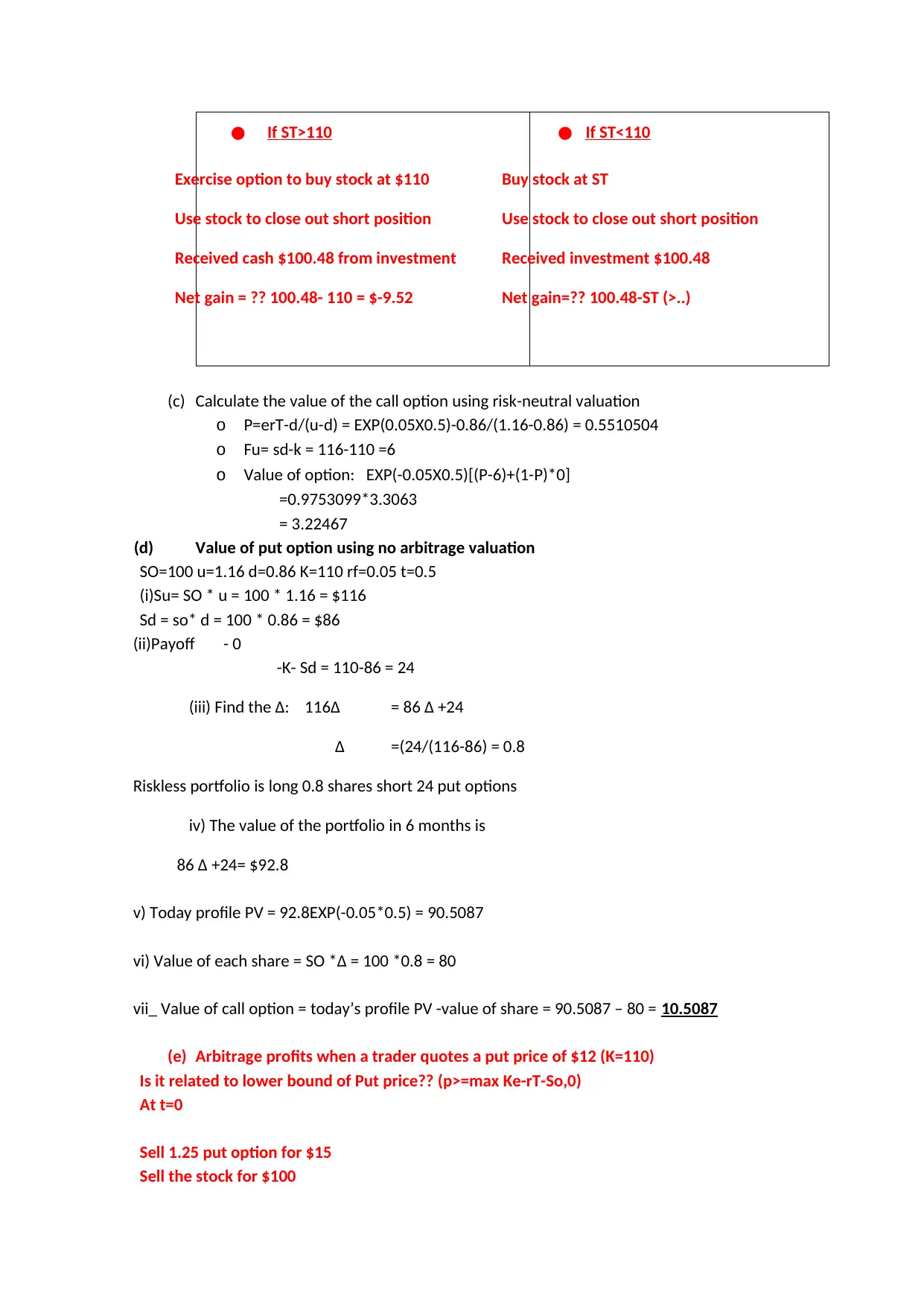

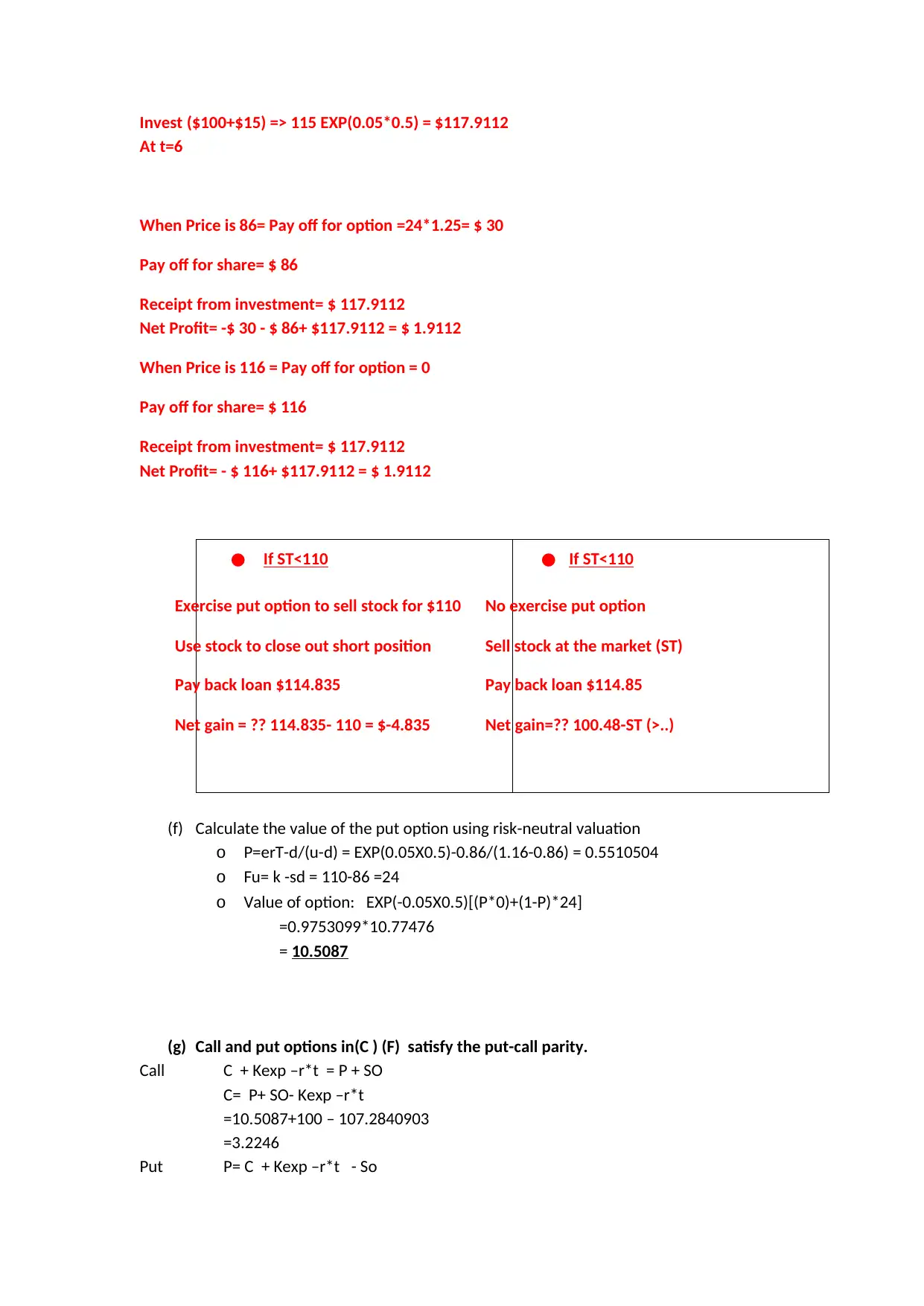

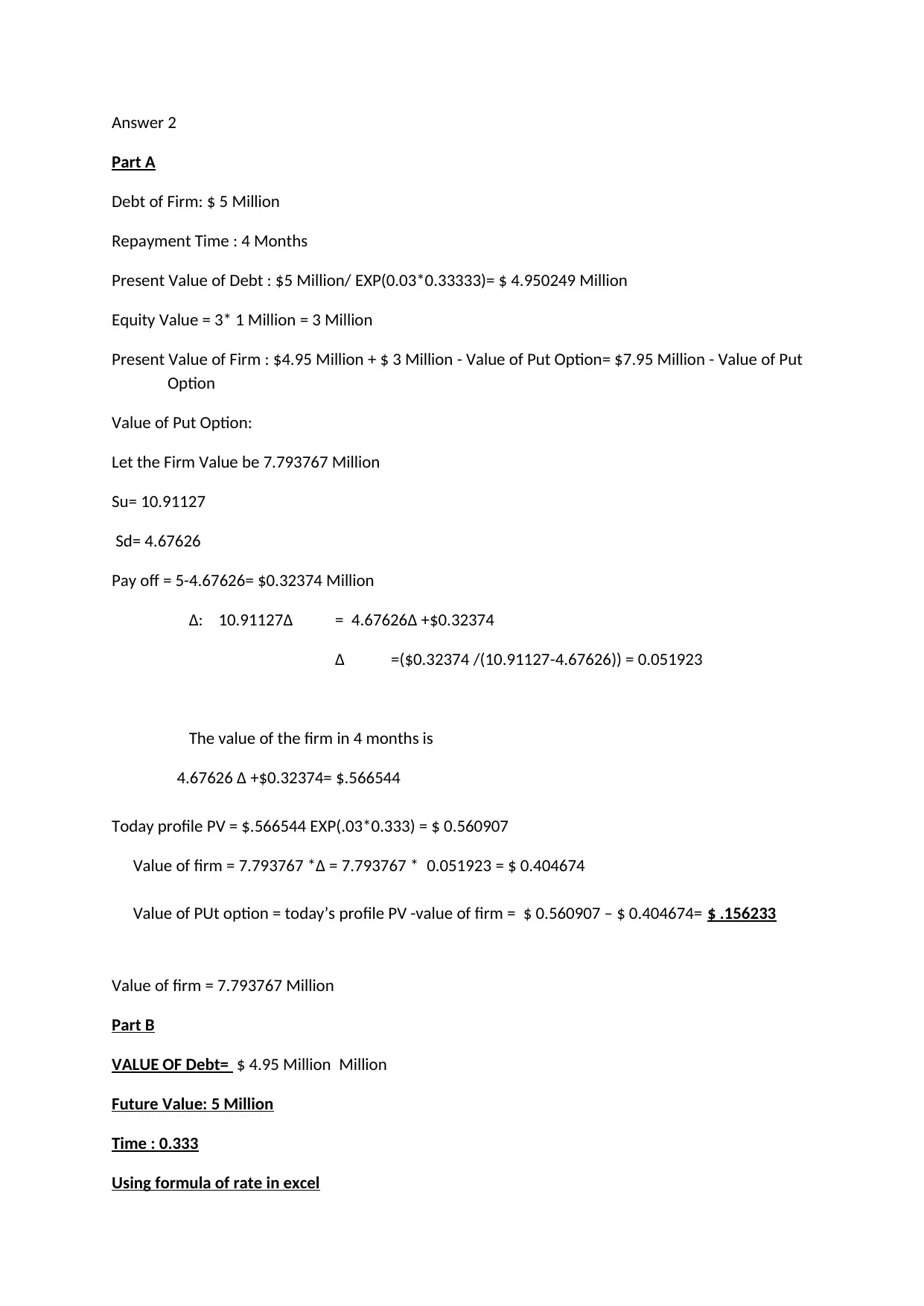

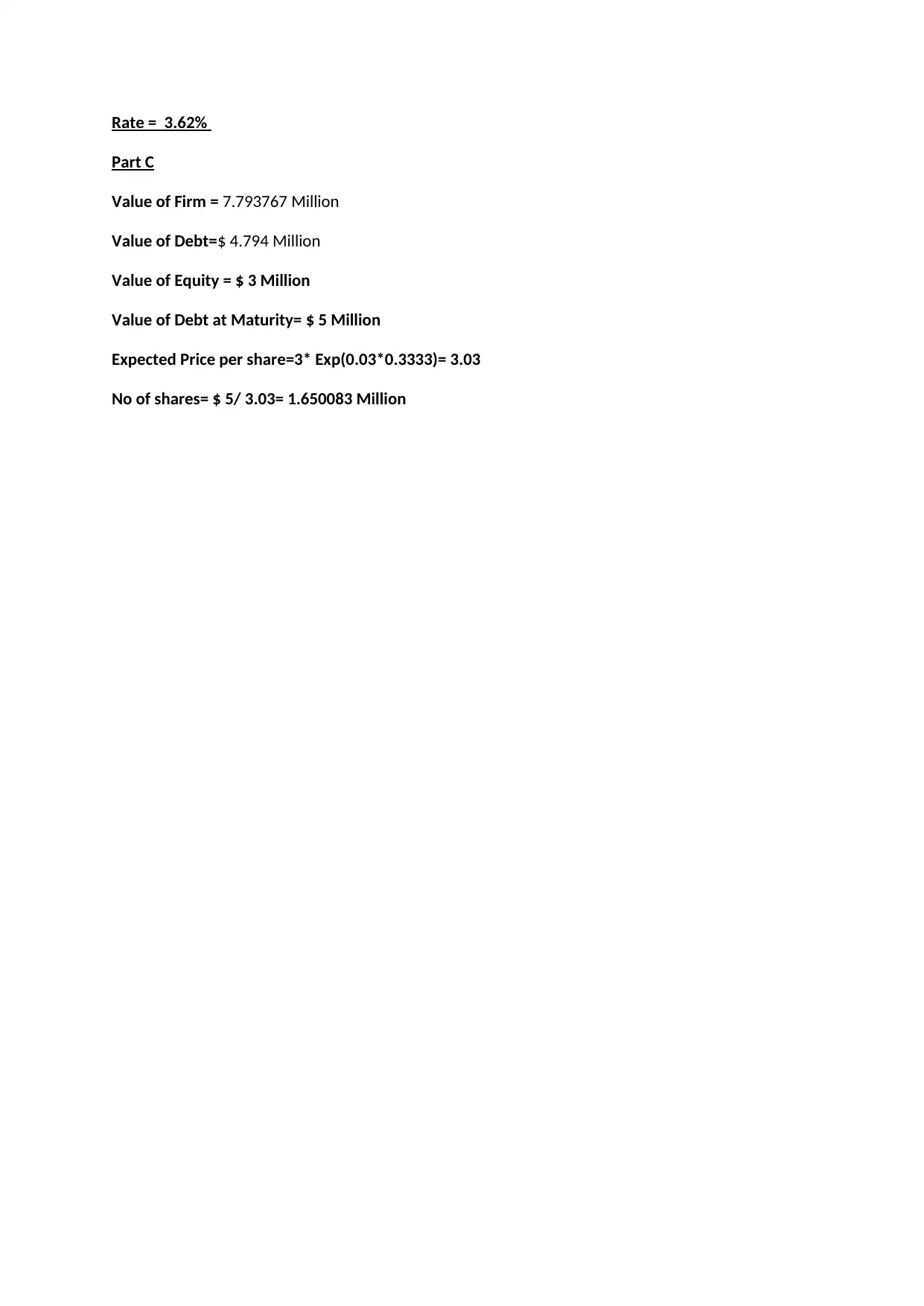

This document presents a comprehensive solution to an assignment focused on binomial tree option pricing. It begins by calculating the value of a call option using no-arbitrage valuation and demonstrates how to profit from arbitrage when a call option is mispriced. The solution then calculates the call option value using risk-neutral valuation. Following this, the document calculates the value of a put option using no-arbitrage valuation and illustrates arbitrage opportunities arising from mispriced put options. The put option value is also calculated using risk-neutral valuation. Finally, the solution demonstrates that the values of call and put options satisfy put-call parity. The assignment also includes the analysis of a firm's debt and equity, and the calculation of the yield to maturity and the value of a put option related to the firm's debt structure.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.