Comprehensive Auditing Report on Biotechnology Ltd's Financials

VerifiedAdded on 2021/06/14

|10

|1688

|105

Report

AI Summary

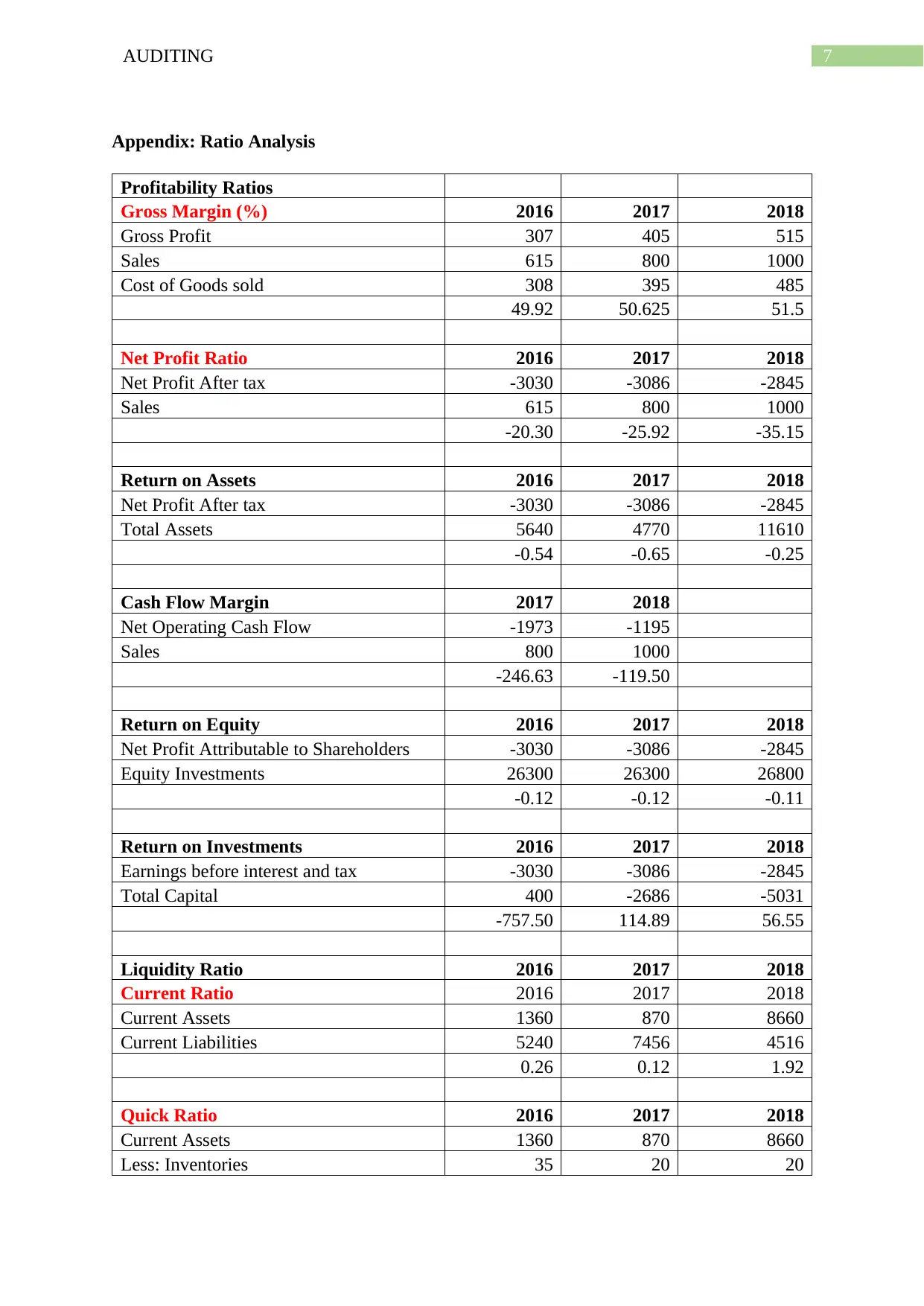

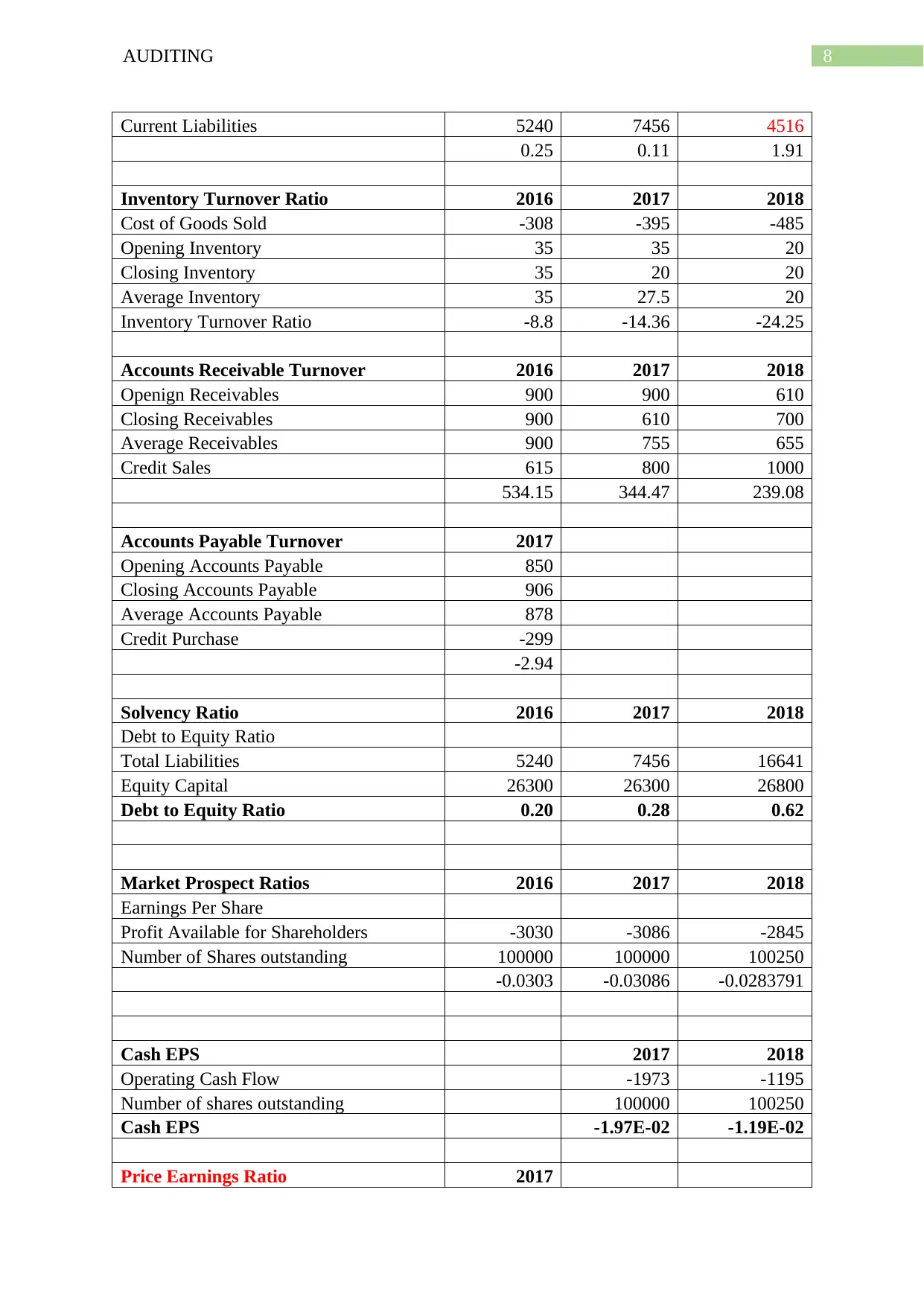

This report provides a detailed financial audit of Biotechnology Ltd, encompassing an analytical review of its financial statements and an assessment of its ability to continue as a going concern. The analysis utilizes ratio analysis, including gross margin, net profit margin, cash flow margin, liquidity ratios (current and quick ratios), solvency ratios (debt to equity), and market performance ratios. The report highlights Biotechnology Ltd's challenges, such as negative net profit margins, declining cash flow, and potential difficulties in meeting short and long-term debt obligations. The assessment of going concern reveals significant doubts about the company's ability to continue operations, primarily due to the failure of a cash injection deal and the resulting decline in share prices. The report concludes that Biotechnology Ltd lacks the capacity to operate as a going concern, given its financial instability and external factors impacting its business. The report includes references to relevant accounting standards and literature and an appendix with detailed ratio analysis data.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.