BIZ201 Accounting for Decision Making: Capital Budgeting Analysis

VerifiedAdded on 2023/06/04

|9

|1698

|394

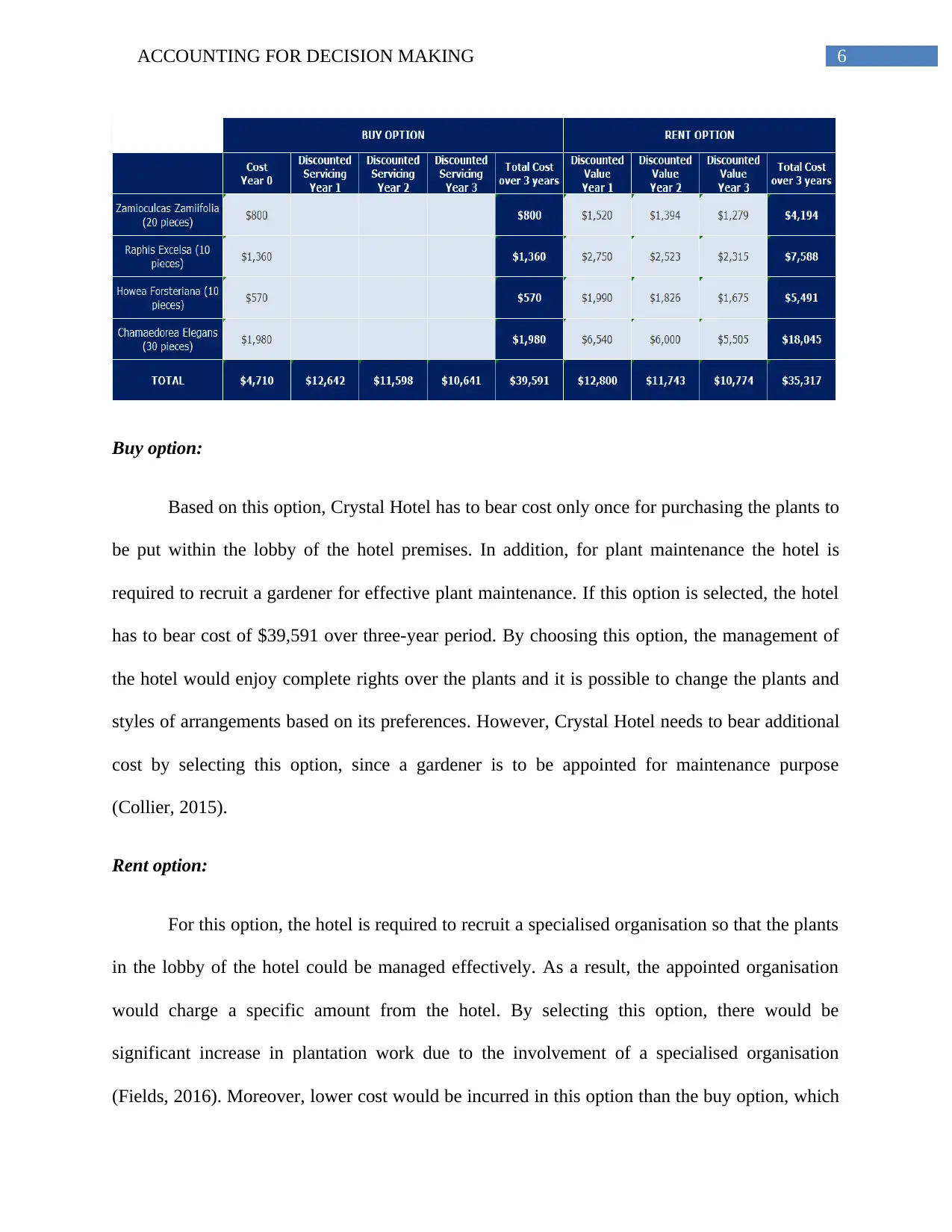

Case Study

AI Summary

This case study assesses Crystal Hotel's investment decisions, focusing on the sales and marketing department and the functions and event department. The sales and marketing department evaluates the options of buying versus renting equipment for a wellness center project, concluding that renting is more cost-effective. For promotional activities, a budget of $14,800 is allocated across various advertising channels. The functions and event department analyzes options for enhancing the hotel lobby with plantation work, comparing recruiting a specialized organization to hiring a gardener, recommending the rental option for cost minimization. The analysis uses costing and capital budgeting techniques to advise the hotel's management on optimal financial strategies. Desklib provides students with access to a wealth of solved assignments and past papers.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.