Management Accounting Report: Systems and Methods for Bizdaq

VerifiedAdded on 2020/07/23

|18

|6183

|28

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and methods, specifically tailored for Bizdaq, a sales management company based in London. The report begins by introducing management accounting and its significance in providing financial information for decision-making and performance enhancement. It then delves into various management accounting systems, including inventory management, cost accounting, job costing, and price optimization, outlining their applications and benefits for Bizdaq. Furthermore, the report explores different methods of management accounting reporting, such as budget reports, accounts receivable aging reports, job cost reports, inventory and manufacturing reports, and income statement reports. Each method is explained with its relevance to Bizdaq's operations. The report also includes a discussion on the differences between income statements prepared using marginal and absorption costing, along with the advantages and disadvantages of planning tools used for budgetary control. Finally, it addresses the adoption of management accounting systems in responding to financial troubles. The report concludes by summarizing the key findings and emphasizing the importance of management accounting in achieving organizational goals.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting system.............................................................................................1

P2 Method of management accounting reporting........................................................................4

TASK 2............................................................................................................................................7

P3 Difference between income statement made through marginal and absorption costing........7

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of planning tools which are used for budgetary control.....11

P5 Adopting management accounting systems for responding financial troubles....................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting system.............................................................................................1

P2 Method of management accounting reporting........................................................................4

TASK 2............................................................................................................................................7

P3 Difference between income statement made through marginal and absorption costing........7

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of planning tools which are used for budgetary control.....11

P5 Adopting management accounting systems for responding financial troubles....................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is stated to be the process which is concerned with various

regulations related to accounting data. It is a very effective tool for managers to get all the

monetary information and take decisions. it is a field that provides provisions to the company for

all the transactions (financial and non-financial) and aid managers in formally informing higher

authorities. Managerial accounting is completely focused on boosting the revenues of company

by enhancing efficiency and finding new avenues to get investment (Ahmad and Mohamed

Zabri, 2012). In the beginning of industrial age, companies were highly mismanaged which

forced them to close down even in late 80’s they were not able to cope up with the

mismanagement of funds. This is when management accounting came as it provided vision to

companies as how they can strategically manage their monetary assets and use them properly.

This report is based on Bizdaq which is a sales management company. They are based in

London and was founded in 2015. The company has a staff of 14 individuals with an annual

turnover of 1 million pound. It contracts with other firms as to manage their sales and other

operations. This project will state about different types of management accounting system that

are needed by company to manage itself (Aminbakhsh, Gunduz and Sonmez, 2013). Income

statement will be prepared while using absorption and marginal costing. As well as difference

between them will be stated. Other aspects like planning tools and integration of managerial

accounting system will be described in the end.

TASK 1

P1 Management accounting system

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting system

This description is based on the concepts and ways management accounting systems are used by

organisation. Different types of accounting systems will be discussed in the following report,

such as, inventory management system, Expense optimisation, Job costing and cost accounting

system.

Management accounting system:

It is a system that is concerned with boosting financial knowledge so that decision making

1

Management accounting is stated to be the process which is concerned with various

regulations related to accounting data. It is a very effective tool for managers to get all the

monetary information and take decisions. it is a field that provides provisions to the company for

all the transactions (financial and non-financial) and aid managers in formally informing higher

authorities. Managerial accounting is completely focused on boosting the revenues of company

by enhancing efficiency and finding new avenues to get investment (Ahmad and Mohamed

Zabri, 2012). In the beginning of industrial age, companies were highly mismanaged which

forced them to close down even in late 80’s they were not able to cope up with the

mismanagement of funds. This is when management accounting came as it provided vision to

companies as how they can strategically manage their monetary assets and use them properly.

This report is based on Bizdaq which is a sales management company. They are based in

London and was founded in 2015. The company has a staff of 14 individuals with an annual

turnover of 1 million pound. It contracts with other firms as to manage their sales and other

operations. This project will state about different types of management accounting system that

are needed by company to manage itself (Aminbakhsh, Gunduz and Sonmez, 2013). Income

statement will be prepared while using absorption and marginal costing. As well as difference

between them will be stated. Other aspects like planning tools and integration of managerial

accounting system will be described in the end.

TASK 1

P1 Management accounting system

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting system

This description is based on the concepts and ways management accounting systems are used by

organisation. Different types of accounting systems will be discussed in the following report,

such as, inventory management system, Expense optimisation, Job costing and cost accounting

system.

Management accounting system:

It is a system that is concerned with boosting financial knowledge so that decision making

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

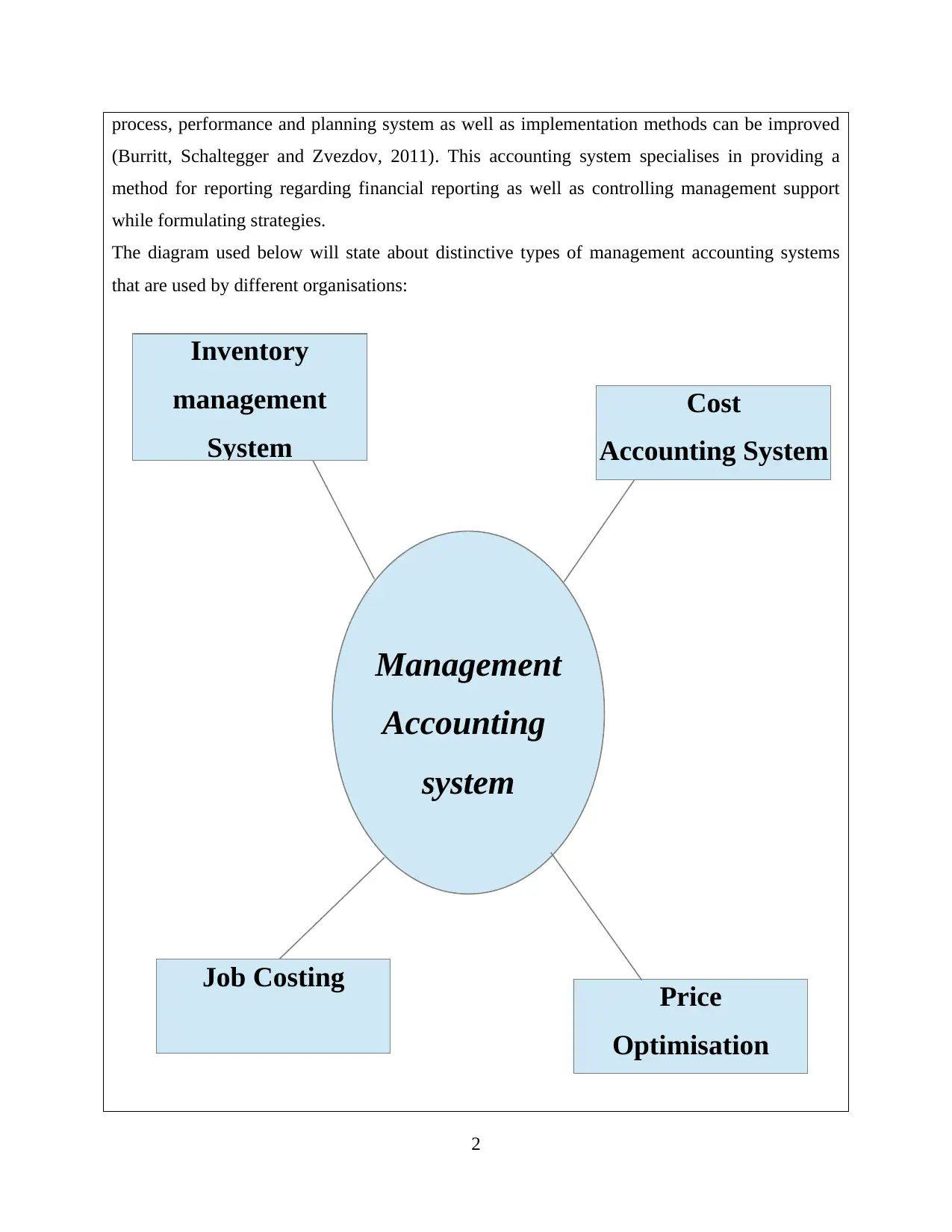

process, performance and planning system as well as implementation methods can be improved

(Burritt, Schaltegger and Zvezdov, 2011). This accounting system specialises in providing a

method for reporting regarding financial reporting as well as controlling management support

while formulating strategies.

The diagram used below will state about distinctive types of management accounting systems

that are used by different organisations:

2

Management

Accounting

system

Price

Optimisation

Job Costing

Cost

Accounting System

Inventory

management

System

(Burritt, Schaltegger and Zvezdov, 2011). This accounting system specialises in providing a

method for reporting regarding financial reporting as well as controlling management support

while formulating strategies.

The diagram used below will state about distinctive types of management accounting systems

that are used by different organisations:

2

Management

Accounting

system

Price

Optimisation

Job Costing

Cost

Accounting System

Inventory

management

System

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

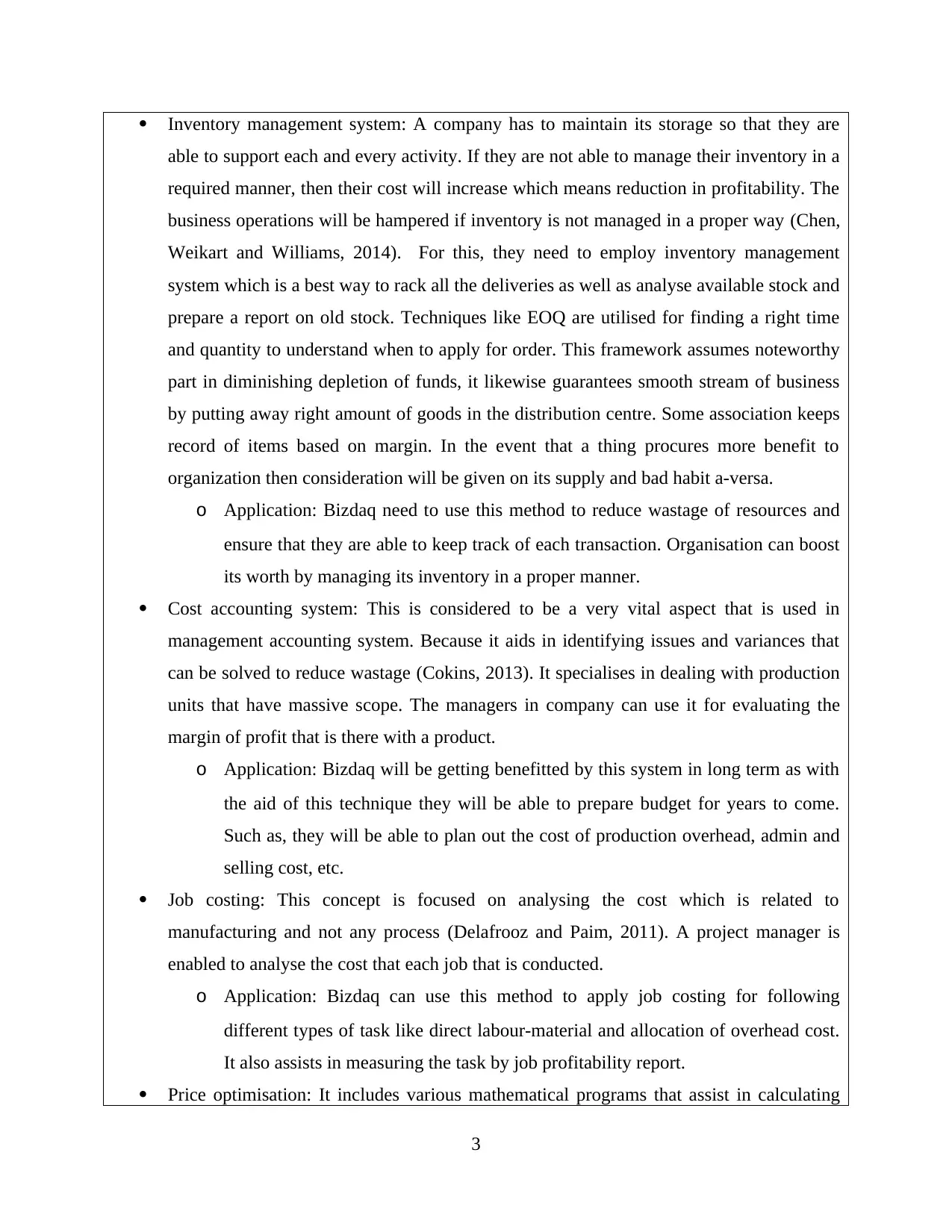

Inventory management system: A company has to maintain its storage so that they are

able to support each and every activity. If they are not able to manage their inventory in a

required manner, then their cost will increase which means reduction in profitability. The

business operations will be hampered if inventory is not managed in a proper way (Chen,

Weikart and Williams, 2014). For this, they need to employ inventory management

system which is a best way to rack all the deliveries as well as analyse available stock and

prepare a report on old stock. Techniques like EOQ are utilised for finding a right time

and quantity to understand when to apply for order. This framework assumes noteworthy

part in diminishing depletion of funds, it likewise guarantees smooth stream of business

by putting away right amount of goods in the distribution centre. Some association keeps

record of items based on margin. In the event that a thing procures more benefit to

organization then consideration will be given on its supply and bad habit a-versa.

o Application: Bizdaq need to use this method to reduce wastage of resources and

ensure that they are able to keep track of each transaction. Organisation can boost

its worth by managing its inventory in a proper manner.

Cost accounting system: This is considered to be a very vital aspect that is used in

management accounting system. Because it aids in identifying issues and variances that

can be solved to reduce wastage (Cokins, 2013). It specialises in dealing with production

units that have massive scope. The managers in company can use it for evaluating the

margin of profit that is there with a product.

o Application: Bizdaq will be getting benefitted by this system in long term as with

the aid of this technique they will be able to prepare budget for years to come.

Such as, they will be able to plan out the cost of production overhead, admin and

selling cost, etc.

Job costing: This concept is focused on analysing the cost which is related to

manufacturing and not any process (Delafrooz and Paim, 2011). A project manager is

enabled to analyse the cost that each job that is conducted.

o Application: Bizdaq can use this method to apply job costing for following

different types of task like direct labour-material and allocation of overhead cost.

It also assists in measuring the task by job profitability report.

Price optimisation: It includes various mathematical programs that assist in calculating

3

able to support each and every activity. If they are not able to manage their inventory in a

required manner, then their cost will increase which means reduction in profitability. The

business operations will be hampered if inventory is not managed in a proper way (Chen,

Weikart and Williams, 2014). For this, they need to employ inventory management

system which is a best way to rack all the deliveries as well as analyse available stock and

prepare a report on old stock. Techniques like EOQ are utilised for finding a right time

and quantity to understand when to apply for order. This framework assumes noteworthy

part in diminishing depletion of funds, it likewise guarantees smooth stream of business

by putting away right amount of goods in the distribution centre. Some association keeps

record of items based on margin. In the event that a thing procures more benefit to

organization then consideration will be given on its supply and bad habit a-versa.

o Application: Bizdaq need to use this method to reduce wastage of resources and

ensure that they are able to keep track of each transaction. Organisation can boost

its worth by managing its inventory in a proper manner.

Cost accounting system: This is considered to be a very vital aspect that is used in

management accounting system. Because it aids in identifying issues and variances that

can be solved to reduce wastage (Cokins, 2013). It specialises in dealing with production

units that have massive scope. The managers in company can use it for evaluating the

margin of profit that is there with a product.

o Application: Bizdaq will be getting benefitted by this system in long term as with

the aid of this technique they will be able to prepare budget for years to come.

Such as, they will be able to plan out the cost of production overhead, admin and

selling cost, etc.

Job costing: This concept is focused on analysing the cost which is related to

manufacturing and not any process (Delafrooz and Paim, 2011). A project manager is

enabled to analyse the cost that each job that is conducted.

o Application: Bizdaq can use this method to apply job costing for following

different types of task like direct labour-material and allocation of overhead cost.

It also assists in measuring the task by job profitability report.

Price optimisation: It includes various mathematical programs that assist in calculating

3

the prices at a distinctive demand levels. It assists in identifying the best optimum cost of

product by combining data with existing information related to pricing (Ekbatani and

Sangeladji, 2011). The small companies face a very difficult situation as they are not able

to set right and optimum pricing. But this system will enable them to do so in more

effective manner.

o Application: This technique will aid Bizdaq as they will be able to identify best

solutions for setting a price which brings in more profits for company and isn’t

too bad for market.

P2 Method of management accounting reporting

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting system

This report will be focused on identifying various management accounting method of reporting.

This will aid Bizdaq in taking good decisions as they will be aware about organisation and its

activities.

Management report

Accounting reports are very vital for companies who wants to attain a better market picture

and way in which organisation is making its move. A properly structured description is required

to make sure that management is able to understand how well company is doing in market

(Foster, Hart and Lewis, 2011). There are various types of reports that are prepared to ensure that

business is able to analyse and protect its interest by identifying issues before hand.

A management accounting report will assist business in identifying variances and issues,

that will be sorted out by strategically making changes in the system. These type of projects are

very different from financial accounting report, as it is primarily concerned for preparing them to

inform all type of stakeholders (Fullerton, Kennedy and Widener, 2014). For Bizdaq the

management accounting reports will assist in forecasting future, which will be considered to take

right decisions. as well as it will be used to determine the required rate of return to the company.

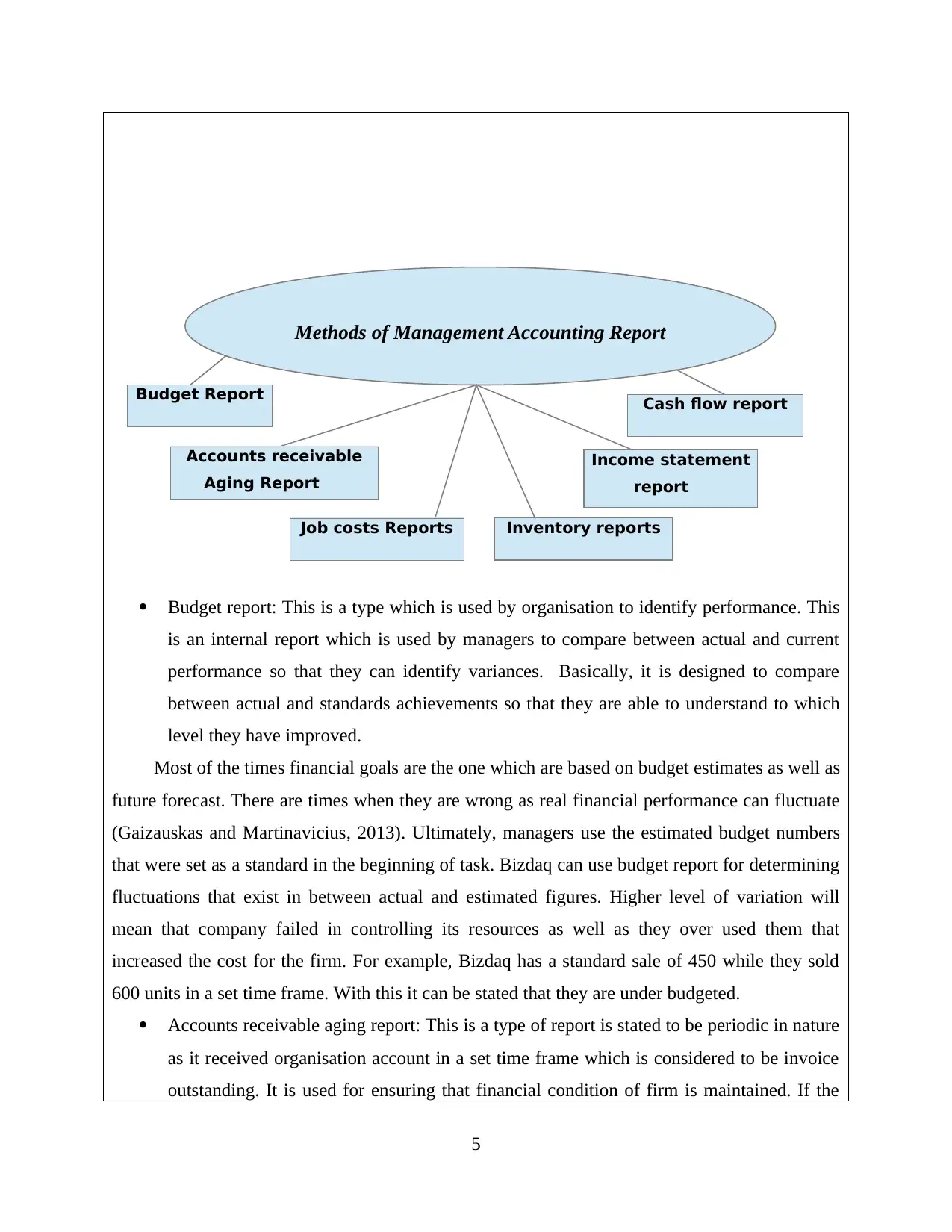

The diagram below will state about different methods which are used for making management

accounting reports:

4

product by combining data with existing information related to pricing (Ekbatani and

Sangeladji, 2011). The small companies face a very difficult situation as they are not able

to set right and optimum pricing. But this system will enable them to do so in more

effective manner.

o Application: This technique will aid Bizdaq as they will be able to identify best

solutions for setting a price which brings in more profits for company and isn’t

too bad for market.

P2 Method of management accounting reporting

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting system

This report will be focused on identifying various management accounting method of reporting.

This will aid Bizdaq in taking good decisions as they will be aware about organisation and its

activities.

Management report

Accounting reports are very vital for companies who wants to attain a better market picture

and way in which organisation is making its move. A properly structured description is required

to make sure that management is able to understand how well company is doing in market

(Foster, Hart and Lewis, 2011). There are various types of reports that are prepared to ensure that

business is able to analyse and protect its interest by identifying issues before hand.

A management accounting report will assist business in identifying variances and issues,

that will be sorted out by strategically making changes in the system. These type of projects are

very different from financial accounting report, as it is primarily concerned for preparing them to

inform all type of stakeholders (Fullerton, Kennedy and Widener, 2014). For Bizdaq the

management accounting reports will assist in forecasting future, which will be considered to take

right decisions. as well as it will be used to determine the required rate of return to the company.

The diagram below will state about different methods which are used for making management

accounting reports:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budget report: This is a type which is used by organisation to identify performance. This

is an internal report which is used by managers to compare between actual and current

performance so that they can identify variances. Basically, it is designed to compare

between actual and standards achievements so that they are able to understand to which

level they have improved.

Most of the times financial goals are the one which are based on budget estimates as well as

future forecast. There are times when they are wrong as real financial performance can fluctuate

(Gaizauskas and Martinavicius, 2013). Ultimately, managers use the estimated budget numbers

that were set as a standard in the beginning of task. Bizdaq can use budget report for determining

fluctuations that exist in between actual and estimated figures. Higher level of variation will

mean that company failed in controlling its resources as well as they over used them that

increased the cost for the firm. For example, Bizdaq has a standard sale of 450 while they sold

600 units in a set time frame. With this it can be stated that they are under budgeted.

Accounts receivable aging report: This is a type of report is stated to be periodic in nature

as it received organisation account in a set time frame which is considered to be invoice

outstanding. It is used for ensuring that financial condition of firm is maintained. If the

5

Methods of Management Accounting Report

Inventory reports

Budget Report

Job costs Reports

Cash flow report

Income statement

report

Accounts receivable

Aging Report

is an internal report which is used by managers to compare between actual and current

performance so that they can identify variances. Basically, it is designed to compare

between actual and standards achievements so that they are able to understand to which

level they have improved.

Most of the times financial goals are the one which are based on budget estimates as well as

future forecast. There are times when they are wrong as real financial performance can fluctuate

(Gaizauskas and Martinavicius, 2013). Ultimately, managers use the estimated budget numbers

that were set as a standard in the beginning of task. Bizdaq can use budget report for determining

fluctuations that exist in between actual and estimated figures. Higher level of variation will

mean that company failed in controlling its resources as well as they over used them that

increased the cost for the firm. For example, Bizdaq has a standard sale of 450 while they sold

600 units in a set time frame. With this it can be stated that they are under budgeted.

Accounts receivable aging report: This is a type of report is stated to be periodic in nature

as it received organisation account in a set time frame which is considered to be invoice

outstanding. It is used for ensuring that financial condition of firm is maintained. If the

5

Methods of Management Accounting Report

Inventory reports

Budget Report

Job costs Reports

Cash flow report

Income statement

report

Accounts receivable

Aging Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

figures in report state that their slow movement in acquisition than the organisation needs

to focus more on practice of sales.

This approach can be used by Bizdaq as to recognize the balance amount that is required for

allowance for doubtful accounts. They can prepare a/c receivables for the aging report via sorting

out unpaid sales invoices to the consumers and as per the stated dates in ledger.

Job cost reports: This is a very vital method that allows company in specifying the cost

that is there for an individual or a task that is concerned with the organisation (Higgins,

2012). This is mostly used in construction organisations but is used everywhere as to

allocate cost for various projects that will be undertaken by company.

A task can be concerned with serving a specified consumer this can involve manufacturing

products as well as prepare same types of units to complete the job. Bizdaq can use this

technique for developing a category where various business activities will get required funds.

Inventory and manufacturing reports: This is a report which is made up of 3 different

stages. Such as manufacturing, wholesaling and retailing. It is an inclusion of sum of

sales that are parted for three different stages (Hirth, 2013). They are mainly prepared to

track movement of items as well as assist managers in maintaining the storage and make

the process more visible.

Bizdaq can use these reports to make sure that they are able to grab all opportunities to

consolidate all activities. They enable in setting a cycle which can be followed to refill stocks in

a set time period.

Income statement reports: These are the type of reports that are used by financial officers

for making sure that they are able to measure total profit which is earned in a financial

year (Lambert and Sponem, 2012). It allows managers in knowing the present

performance by comparing it with historical income statements of company.

Bizdaq can use this technique for measuring organisation profitability in a set period of time.

Company has to understand as to what are the outstanding expenses of firm, arrears of

employees, payments that are due and also the one which is received are recorded in reports.

Conclusion

After analysing it briefly it is understood that Bizdaq need to evaluate all the features of the

reports so that they can adapt to the best ones and boost their own efficiency in informing various

parties. Also, there are different reasons and purposes because of which reports are prepared.

6

to focus more on practice of sales.

This approach can be used by Bizdaq as to recognize the balance amount that is required for

allowance for doubtful accounts. They can prepare a/c receivables for the aging report via sorting

out unpaid sales invoices to the consumers and as per the stated dates in ledger.

Job cost reports: This is a very vital method that allows company in specifying the cost

that is there for an individual or a task that is concerned with the organisation (Higgins,

2012). This is mostly used in construction organisations but is used everywhere as to

allocate cost for various projects that will be undertaken by company.

A task can be concerned with serving a specified consumer this can involve manufacturing

products as well as prepare same types of units to complete the job. Bizdaq can use this

technique for developing a category where various business activities will get required funds.

Inventory and manufacturing reports: This is a report which is made up of 3 different

stages. Such as manufacturing, wholesaling and retailing. It is an inclusion of sum of

sales that are parted for three different stages (Hirth, 2013). They are mainly prepared to

track movement of items as well as assist managers in maintaining the storage and make

the process more visible.

Bizdaq can use these reports to make sure that they are able to grab all opportunities to

consolidate all activities. They enable in setting a cycle which can be followed to refill stocks in

a set time period.

Income statement reports: These are the type of reports that are used by financial officers

for making sure that they are able to measure total profit which is earned in a financial

year (Lambert and Sponem, 2012). It allows managers in knowing the present

performance by comparing it with historical income statements of company.

Bizdaq can use this technique for measuring organisation profitability in a set period of time.

Company has to understand as to what are the outstanding expenses of firm, arrears of

employees, payments that are due and also the one which is received are recorded in reports.

Conclusion

After analysing it briefly it is understood that Bizdaq need to evaluate all the features of the

reports so that they can adapt to the best ones and boost their own efficiency in informing various

parties. Also, there are different reasons and purposes because of which reports are prepared.

6

Such as cash activities, cash flow, inventory statement as well as other reporting techniques will

be used. For example, budget reports will be forecasting about estimate. As well as income

statement will assist in knowing as how much earning company is going to have and what

amount it has to reinvest as to expand further more.

M1 Benefits of management accounting

Without any objectives manager cannot use the techniques which can influence the

performance organization. Management uses the management accounting information so that

transactions can be recorded in a proper manner. This leads to effective and efficient results of

the company. Thus managers can take relevant decisions through the financial statements so that

good results can be determined.

TASK 2

P3 Difference between income statement made through marginal and absorption costing

Income statements are the document which are prepared by the company to state about its

revenue that it has earned in a time frame with a level of expenditure done by them. in

management accounting, various techniques can be used to prepare income statements that are

also known as profit and loss a/c (Langevin and Mendoza, 2013). the two method which are

used are stated to be marginal method of costing and the other one is absorption technique. To

understand them in a proper manner, they are stated below:

Marginal Costing: It is focused on the additional expenditure that has been made by

company for producing an extra unit. In this technique, the fixed cost is stated to be on the basis

of period and variable cost is treated in a usual manner. This approach charges direct material,

labour as well as overhead at the time of incurring. For Bizdaq, if they can reduce the variability

in their expenditure than they will be able to reduce the pricing of packages that are sold by

them. In its contrast, selling and administration cost as well as fixed expenses will be charged

when they will be incurred.

Absorption costing: This technique is very unique and different. No matter if the cost of

product is fixed or variable, it will be associated with the units that are sold by firm. It is a

traditional method of calculating the cost of item also known as full costing method (Lavia

López and Hiebl, 2014). The prime benefits of utilising this approach is that it covers all the

aspects and expenses that a are made by organisation. In this method, there are no variations in

7

be used. For example, budget reports will be forecasting about estimate. As well as income

statement will assist in knowing as how much earning company is going to have and what

amount it has to reinvest as to expand further more.

M1 Benefits of management accounting

Without any objectives manager cannot use the techniques which can influence the

performance organization. Management uses the management accounting information so that

transactions can be recorded in a proper manner. This leads to effective and efficient results of

the company. Thus managers can take relevant decisions through the financial statements so that

good results can be determined.

TASK 2

P3 Difference between income statement made through marginal and absorption costing

Income statements are the document which are prepared by the company to state about its

revenue that it has earned in a time frame with a level of expenditure done by them. in

management accounting, various techniques can be used to prepare income statements that are

also known as profit and loss a/c (Langevin and Mendoza, 2013). the two method which are

used are stated to be marginal method of costing and the other one is absorption technique. To

understand them in a proper manner, they are stated below:

Marginal Costing: It is focused on the additional expenditure that has been made by

company for producing an extra unit. In this technique, the fixed cost is stated to be on the basis

of period and variable cost is treated in a usual manner. This approach charges direct material,

labour as well as overhead at the time of incurring. For Bizdaq, if they can reduce the variability

in their expenditure than they will be able to reduce the pricing of packages that are sold by

them. In its contrast, selling and administration cost as well as fixed expenses will be charged

when they will be incurred.

Absorption costing: This technique is very unique and different. No matter if the cost of

product is fixed or variable, it will be associated with the units that are sold by firm. It is a

traditional method of calculating the cost of item also known as full costing method (Lavia

López and Hiebl, 2014). The prime benefits of utilising this approach is that it covers all the

aspects and expenses that a are made by organisation. In this method, there are no variations in

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the fixed cost. Some of the main type of expense are not taken into consideration such as selling

and distribution cost at the time when income statement is being prepared.

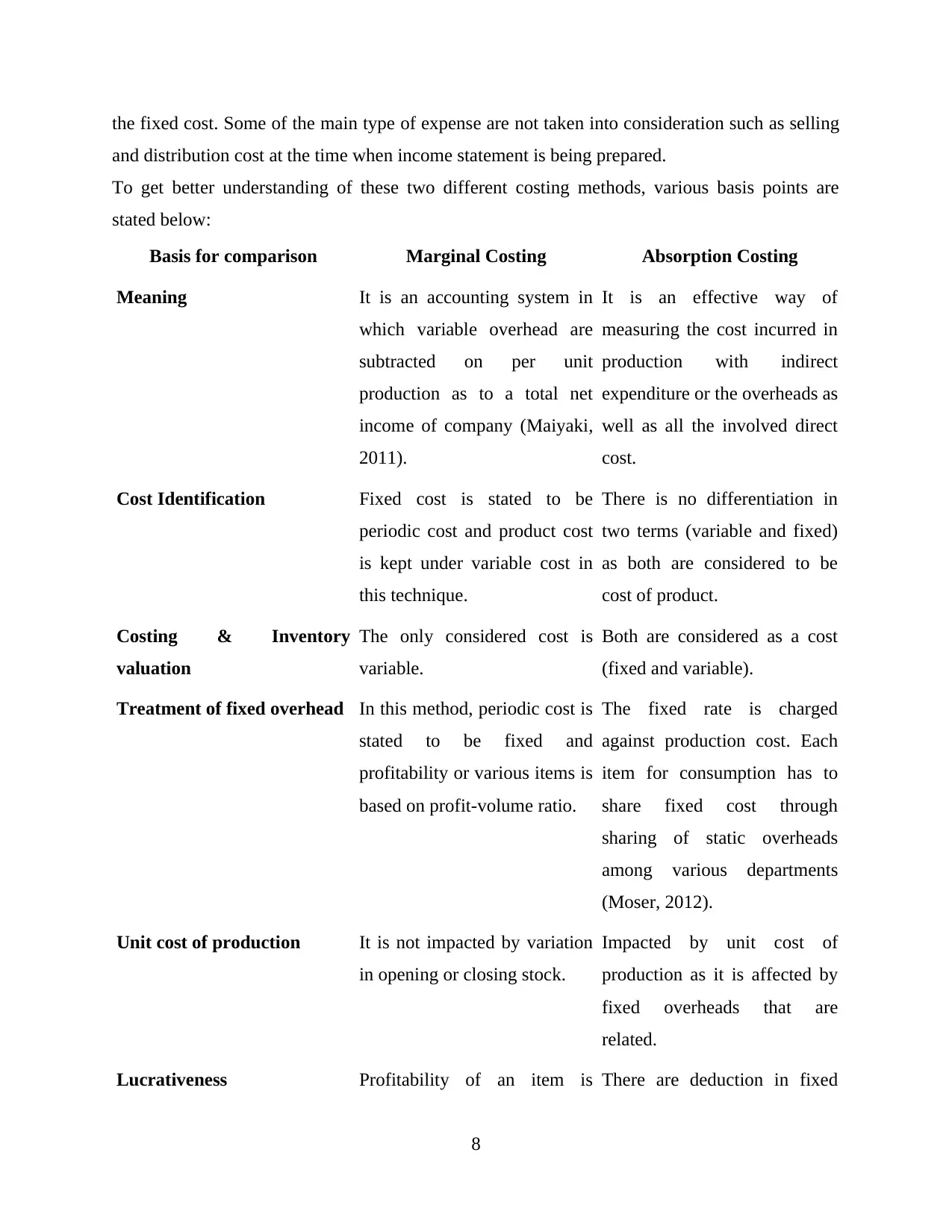

To get better understanding of these two different costing methods, various basis points are

stated below:

Basis for comparison Marginal Costing Absorption Costing

Meaning It is an accounting system in

which variable overhead are

subtracted on per unit

production as to a total net

income of company (Maiyaki,

2011).

It is an effective way of

measuring the cost incurred in

production with indirect

expenditure or the overheads as

well as all the involved direct

cost.

Cost Identification Fixed cost is stated to be

periodic cost and product cost

is kept under variable cost in

this technique.

There is no differentiation in

two terms (variable and fixed)

as both are considered to be

cost of product.

Costing & Inventory

valuation

The only considered cost is

variable.

Both are considered as a cost

(fixed and variable).

Treatment of fixed overhead In this method, periodic cost is

stated to be fixed and

profitability or various items is

based on profit-volume ratio.

The fixed rate is charged

against production cost. Each

item for consumption has to

share fixed cost through

sharing of static overheads

among various departments

(Moser, 2012).

Unit cost of production It is not impacted by variation

in opening or closing stock.

Impacted by unit cost of

production as it is affected by

fixed overheads that are

related.

Lucrativeness Profitability of an item is There are deduction in fixed

8

and distribution cost at the time when income statement is being prepared.

To get better understanding of these two different costing methods, various basis points are

stated below:

Basis for comparison Marginal Costing Absorption Costing

Meaning It is an accounting system in

which variable overhead are

subtracted on per unit

production as to a total net

income of company (Maiyaki,

2011).

It is an effective way of

measuring the cost incurred in

production with indirect

expenditure or the overheads as

well as all the involved direct

cost.

Cost Identification Fixed cost is stated to be

periodic cost and product cost

is kept under variable cost in

this technique.

There is no differentiation in

two terms (variable and fixed)

as both are considered to be

cost of product.

Costing & Inventory

valuation

The only considered cost is

variable.

Both are considered as a cost

(fixed and variable).

Treatment of fixed overhead In this method, periodic cost is

stated to be fixed and

profitability or various items is

based on profit-volume ratio.

The fixed rate is charged

against production cost. Each

item for consumption has to

share fixed cost through

sharing of static overheads

among various departments

(Moser, 2012).

Unit cost of production It is not impacted by variation

in opening or closing stock.

Impacted by unit cost of

production as it is affected by

fixed overheads that are

related.

Lucrativeness Profitability of an item is There are deduction in fixed

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

calculated on the basis of cost-

volume analysis.

cost which impacts

profitability.

Categorization of Expenses Cost are segregated on the

basis of variability and fixed

nature as to identify

contribution and net profit

distinctly.

Various classification is there

as to find out gross profit,

selling and distribution cost to

determine net profit.

Cost Collection Cost is directly collected while

outlining the total contribution

of items.

Cost are measured in

customary way as to state that

data cost.

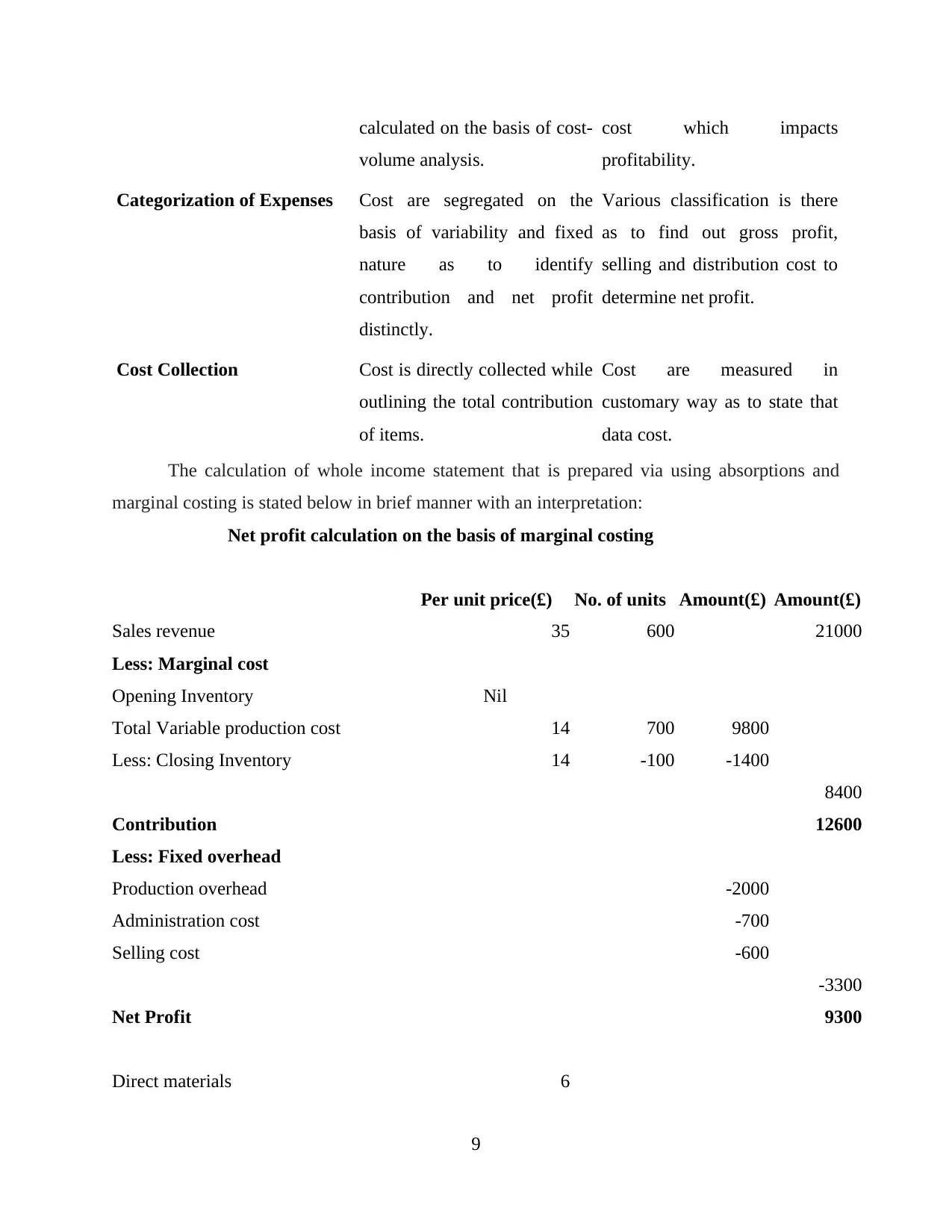

The calculation of whole income statement that is prepared via using absorptions and

marginal costing is stated below in brief manner with an interpretation:

Net profit calculation on the basis of marginal costing

Per unit price(£) No. of units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Marginal cost

Opening Inventory Nil

Total Variable production cost 14 700 9800

Less: Closing Inventory 14 -100 -1400

8400

Contribution 12600

Less: Fixed overhead

Production overhead -2000

Administration cost -700

Selling cost -600

-3300

Net Profit 9300

Direct materials 6

9

volume analysis.

cost which impacts

profitability.

Categorization of Expenses Cost are segregated on the

basis of variability and fixed

nature as to identify

contribution and net profit

distinctly.

Various classification is there

as to find out gross profit,

selling and distribution cost to

determine net profit.

Cost Collection Cost is directly collected while

outlining the total contribution

of items.

Cost are measured in

customary way as to state that

data cost.

The calculation of whole income statement that is prepared via using absorptions and

marginal costing is stated below in brief manner with an interpretation:

Net profit calculation on the basis of marginal costing

Per unit price(£) No. of units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Marginal cost

Opening Inventory Nil

Total Variable production cost 14 700 9800

Less: Closing Inventory 14 -100 -1400

8400

Contribution 12600

Less: Fixed overhead

Production overhead -2000

Administration cost -700

Selling cost -600

-3300

Net Profit 9300

Direct materials 6

9

Direct labour 5

Variable production Overhead 2

Variable sales overhead 1

Total Variable production cost 14

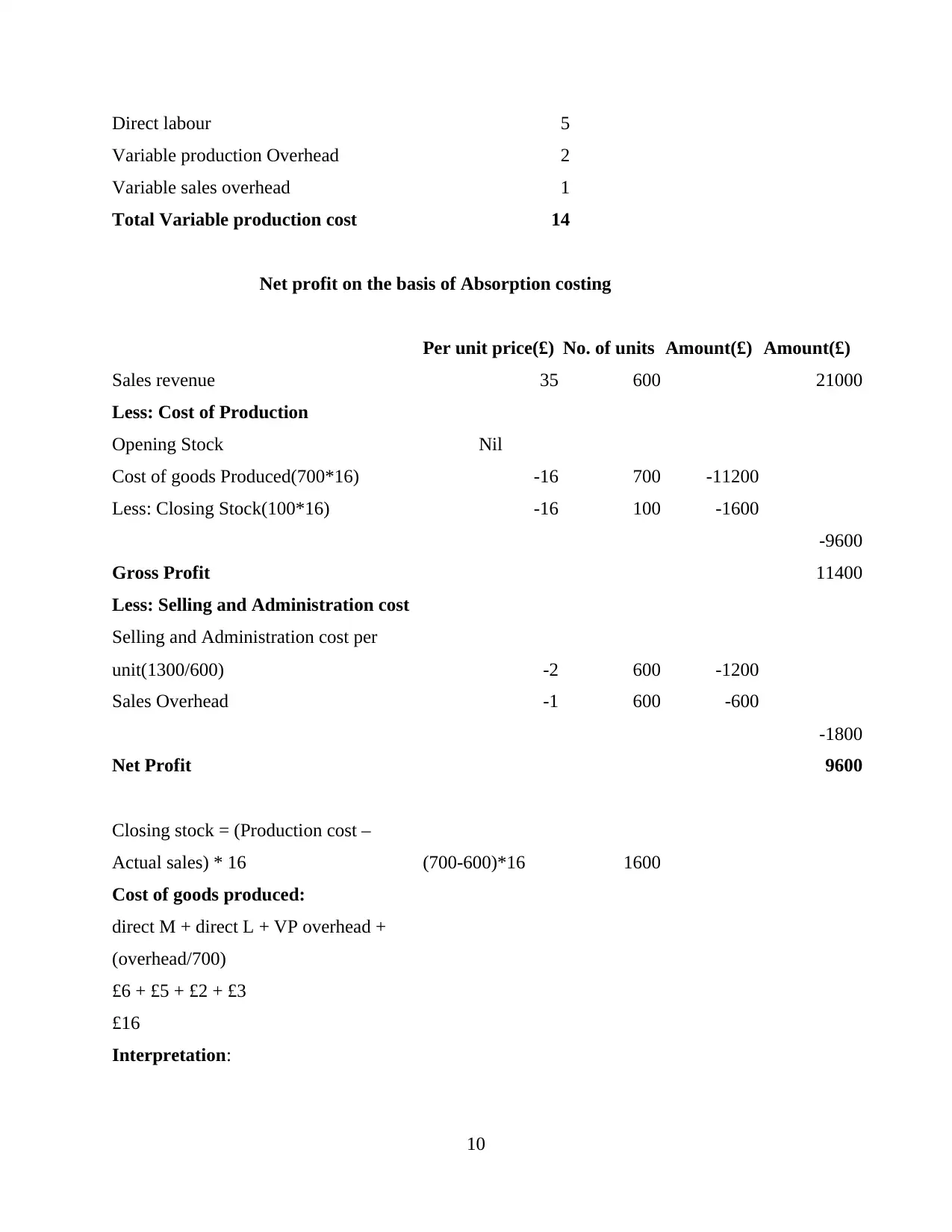

Net profit on the basis of Absorption costing

Per unit price(£) No. of units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Cost of Production

Opening Stock Nil

Cost of goods Produced(700*16) -16 700 -11200

Less: Closing Stock(100*16) -16 100 -1600

-9600

Gross Profit 11400

Less: Selling and Administration cost

Selling and Administration cost per

unit(1300/600) -2 600 -1200

Sales Overhead -1 600 -600

-1800

Net Profit 9600

Closing stock = (Production cost –

Actual sales) * 16 (700-600)*16 1600

Cost of goods produced:

direct M + direct L + VP overhead +

(overhead/700)

£6 + £5 + £2 + £3

£16

Interpretation:

10

Variable production Overhead 2

Variable sales overhead 1

Total Variable production cost 14

Net profit on the basis of Absorption costing

Per unit price(£) No. of units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Cost of Production

Opening Stock Nil

Cost of goods Produced(700*16) -16 700 -11200

Less: Closing Stock(100*16) -16 100 -1600

-9600

Gross Profit 11400

Less: Selling and Administration cost

Selling and Administration cost per

unit(1300/600) -2 600 -1200

Sales Overhead -1 600 -600

-1800

Net Profit 9600

Closing stock = (Production cost –

Actual sales) * 16 (700-600)*16 1600

Cost of goods produced:

direct M + direct L + VP overhead +

(overhead/700)

£6 + £5 + £2 + £3

£16

Interpretation:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.