Financial Derivatives: Black-Scholes Model Problems and Solutions

VerifiedAdded on 2022/08/13

|6

|546

|15

Homework Assignment

AI Summary

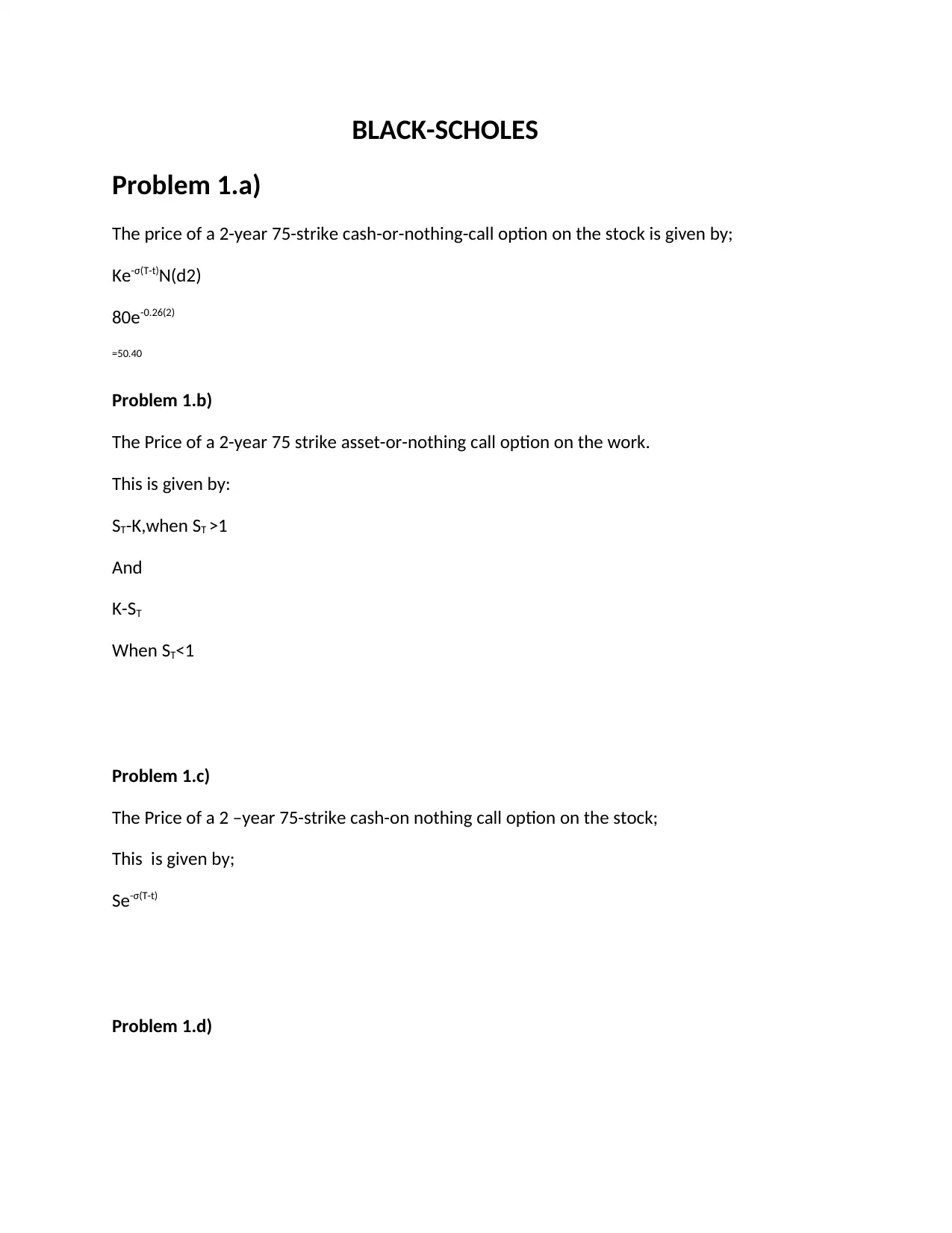

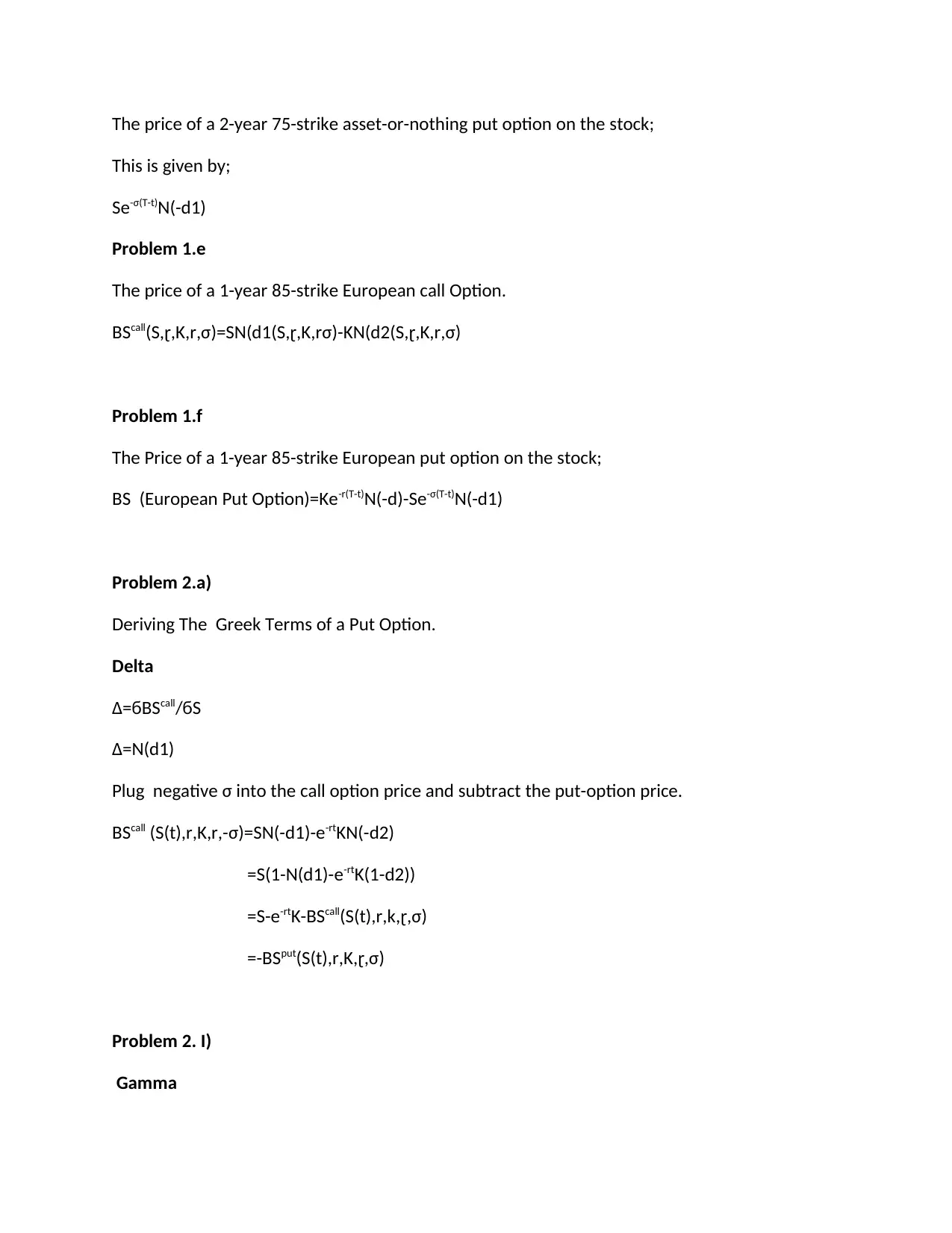

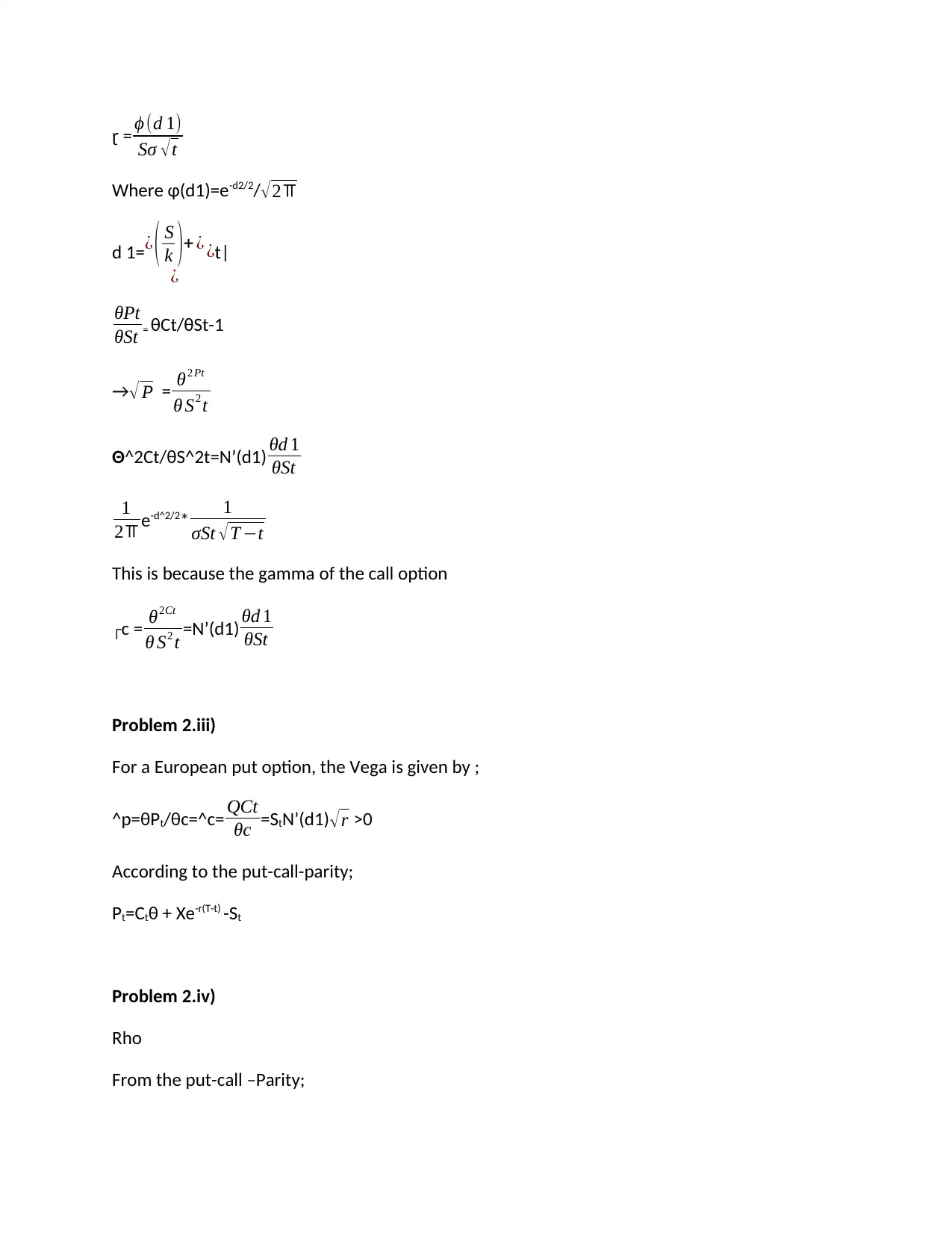

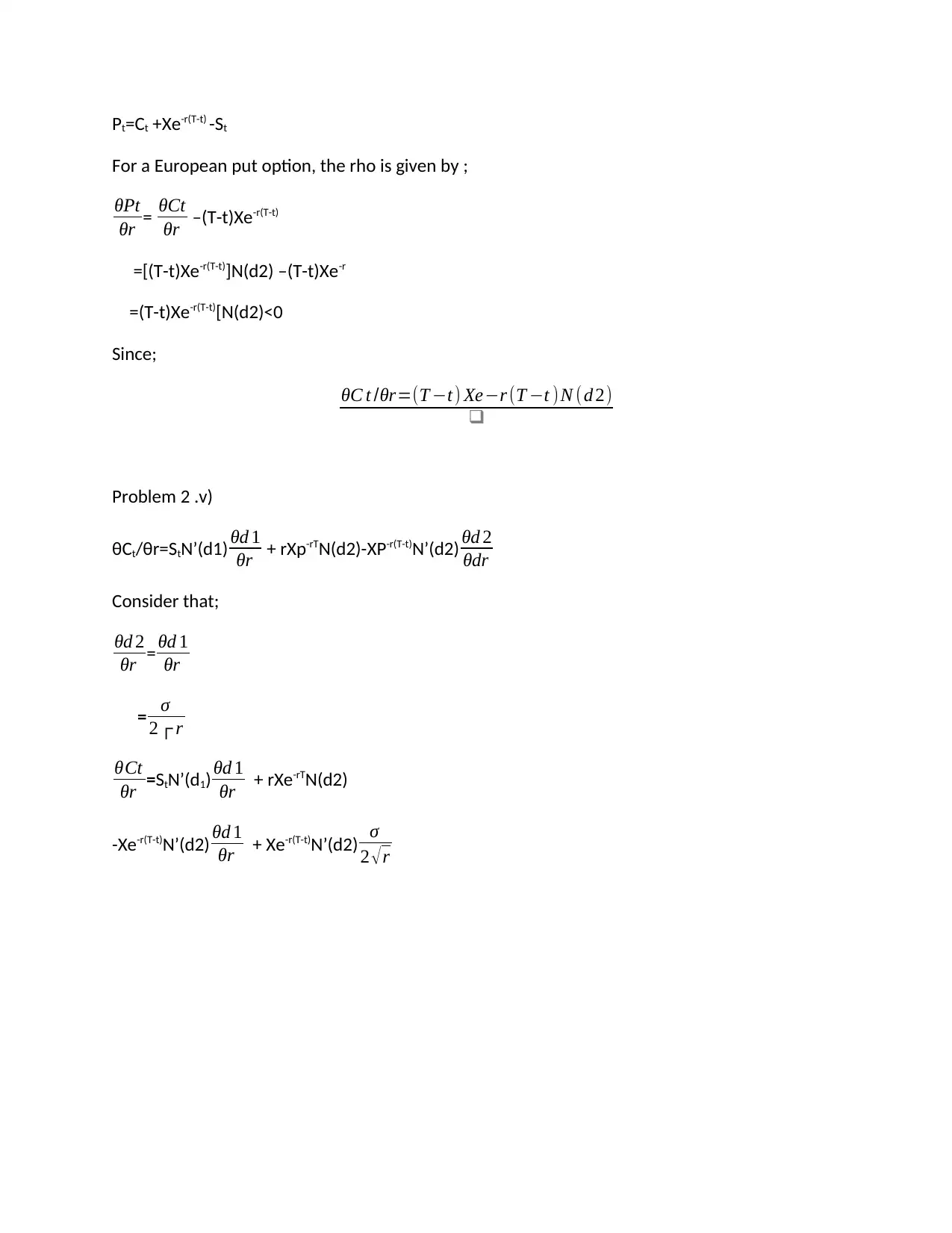

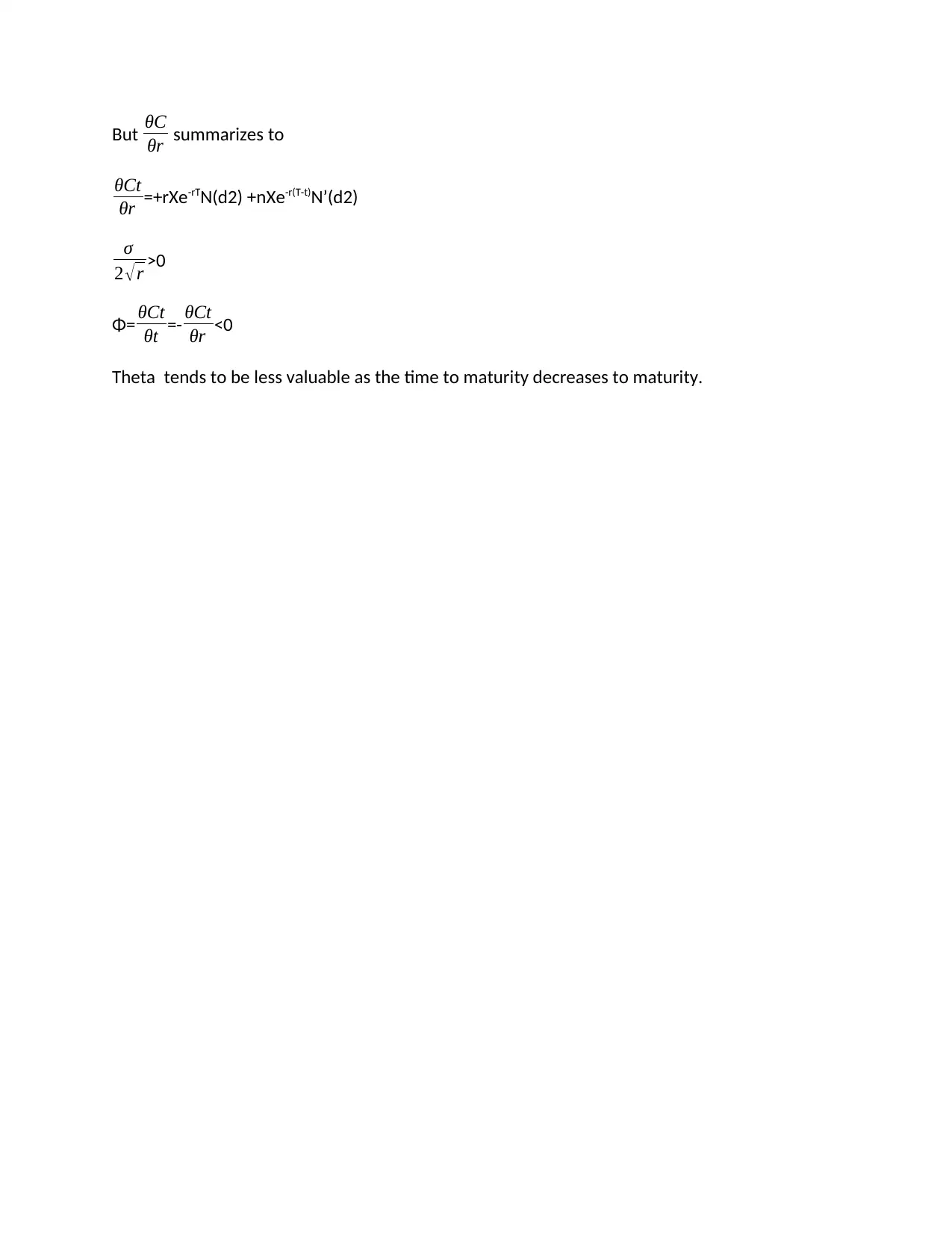

This document presents solutions to a series of problems related to the Black-Scholes option pricing model. The solutions cover various types of options, including cash-or-nothing call options, asset-or-nothing call and put options, and European call and put options. The solutions demonstrate the application of the Black-Scholes formula to calculate option prices under different scenarios. Furthermore, the assignment delves into the derivation of the Greek terms (delta, gamma, vega, rho, and theta) for a put option, explaining how each Greek measures the sensitivity of the option price to changes in underlying parameters such as the stock price, volatility, and time to maturity. The solutions provide a detailed breakdown of the formulas and calculations involved in determining the Greeks, offering insights into the risk management aspects of options trading.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.