ACCG224: Accounting Financial Analysis Report on Blackmores 2019

VerifiedAdded on 2022/12/15

|10

|1999

|177

Report

AI Summary

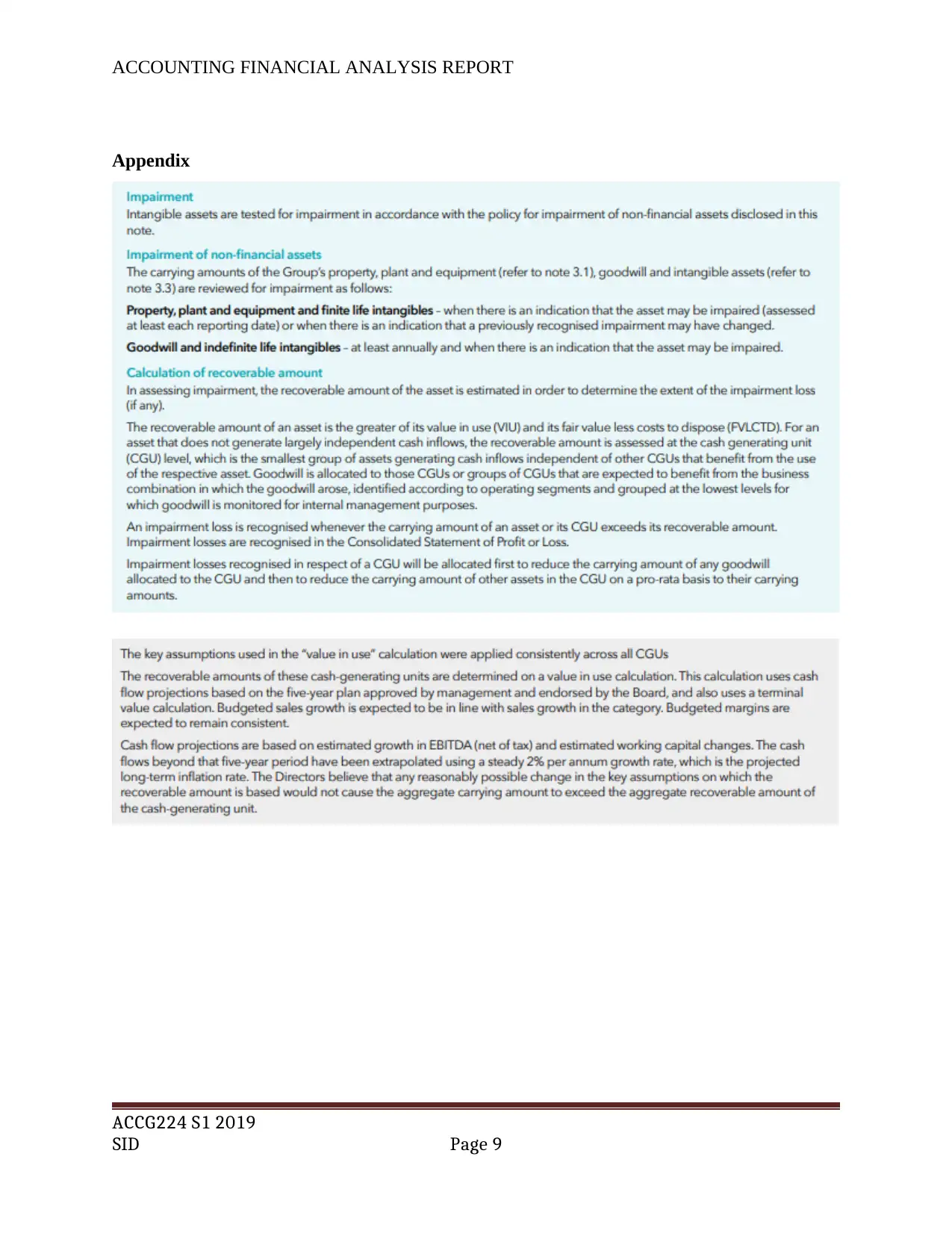

This report presents a financial analysis of Blackmores' annual report for the year ended June 30, 2018, focusing on the application of professional judgment in accounting, particularly concerning impairment testing. The report investigates the role of professional judgment, disclosures made by Blackmores for impairment of assets, and the valuation methods used, including the determination of the discount rate for cash flow analysis. The analysis reveals that while Blackmores generally complies with AASB standards in estimating cash flows, the use of a post-tax discount rate deviates from the standard's requirement for a pre-tax rate. The report concludes with recommendations for improved adherence to AASB standards, specifically regarding the discount rate and the provision of detailed breakdowns of impairment losses. The analysis covers key aspects such as recoverable amount, value in use (VIU), cash generating units (CGU), and the fundamental characteristics of financial reporting, including relevance and faithful representation.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.