Blackmores Ltd Financial Report Analysis Based on Conceptual Framework

VerifiedAdded on 2023/06/12

|12

|2247

|334

Report

AI Summary

This assignment provides a critical analysis of Blackmores Ltd, an ASX-listed company, focusing on the effectiveness of its financial reporting in relation to the conceptual framework. The report evaluates whether Blackmores Ltd's financial statements adhere to the objectives of the conceptual framework, including providing relevant information for stakeholders and accurately representing the company's financial performance. It examines the recognition criteria used for assets, liabilities, income, and expenses, and assesses the presence of fundamental and enhancing qualitative characteristics in the financial statements. The analysis also considers the company's compliance with Australian Accounting Standards Board (AASB) guidelines. The report concludes with recommendations for improving Blackmores Ltd's reporting framework, particularly regarding disclosure requirements and presentation of financial information.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of the Student:

Name of the University:

Author’s Note:

Contemporary Issues in Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The focus of this assignment is to critically analyse the annual reports of a company which is

listed in Australian Stock Exchange (ASX). The company which is selected for this assignment

is Blackmores ltd which has its business headquarters in Australia. The report will be analysing

the financial statements of the company and establish whether the financial statements are

prepared in accordance with conceptual framework of reporting. The report will be stating the

various objectives which the conceptual framework of accounting serves in today’s environment.

In addition, it will point out the recognition criteria of the company and also whether the

financial statements show Fundamental and Enhancing features in the financial statement. Lastly

the report will be ending with a section of recommendations.

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The focus of this assignment is to critically analyse the annual reports of a company which is

listed in Australian Stock Exchange (ASX). The company which is selected for this assignment

is Blackmores ltd which has its business headquarters in Australia. The report will be analysing

the financial statements of the company and establish whether the financial statements are

prepared in accordance with conceptual framework of reporting. The report will be stating the

various objectives which the conceptual framework of accounting serves in today’s environment.

In addition, it will point out the recognition criteria of the company and also whether the

financial statements show Fundamental and Enhancing features in the financial statement. Lastly

the report will be ending with a section of recommendations.

2

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Discussions......................................................................................................................................3

Objectives of Conceptual Framework.........................................................................................3

Recognizing Criteria........................................................................................................................7

Fundamental Qualitative Characteristics.....................................................................................8

Enhancing Qualitative Characteristics.........................................................................................9

Conclusion and Recommendations..................................................................................................9

Reference.......................................................................................................................................11

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Discussions......................................................................................................................................3

Objectives of Conceptual Framework.........................................................................................3

Recognizing Criteria........................................................................................................................7

Fundamental Qualitative Characteristics.....................................................................................8

Enhancing Qualitative Characteristics.........................................................................................9

Conclusion and Recommendations..................................................................................................9

Reference.......................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

Conceptual Framework may be defined as a system or ideas which are important so that

it can be used by different organization for the purpose of preparation of the annual reports of a

business by following the rules, regulations and guideline. The framework is useful to promote

comparability and consistency among the annual reports which are prepared by different

businesses and also annual reports which are prepared at different reporting dates (Díaz et al.

2015). Conceptual Framework provides the guidelines which are needed to be followed to ensure

that the financial statements of the company are represented in an effective manner. The

framework consists of various accounting standards which were issued by AASB, accounting

principles which are followed and accounting conventions. The conceptual framework should be

followed by each entity to ensure that the financial statements is displaying fair representation

(Libby 2017).

The company which is selected for this assignment is Blackmores ltd. The company is

engaged health supplement business in Australia. The company was first established in 1930 and

the company has its headquarter in Australia. The net profit which was generated by the business

after tax amounted to $ 58 million and the company has a global presence in most of the major

countries (Blackmores.com.au. 2018).

Discussions

Objectives of Conceptual Framework

As discussed above Conceptual Framework of reporting enables the users of the financial

statements to understand, compare and interpret the financial information which is provided in

the annual reports of the company. The objectives of conceptual framework are discussed below

in details:

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

Conceptual Framework may be defined as a system or ideas which are important so that

it can be used by different organization for the purpose of preparation of the annual reports of a

business by following the rules, regulations and guideline. The framework is useful to promote

comparability and consistency among the annual reports which are prepared by different

businesses and also annual reports which are prepared at different reporting dates (Díaz et al.

2015). Conceptual Framework provides the guidelines which are needed to be followed to ensure

that the financial statements of the company are represented in an effective manner. The

framework consists of various accounting standards which were issued by AASB, accounting

principles which are followed and accounting conventions. The conceptual framework should be

followed by each entity to ensure that the financial statements is displaying fair representation

(Libby 2017).

The company which is selected for this assignment is Blackmores ltd. The company is

engaged health supplement business in Australia. The company was first established in 1930 and

the company has its headquarter in Australia. The net profit which was generated by the business

after tax amounted to $ 58 million and the company has a global presence in most of the major

countries (Blackmores.com.au. 2018).

Discussions

Objectives of Conceptual Framework

As discussed above Conceptual Framework of reporting enables the users of the financial

statements to understand, compare and interpret the financial information which is provided in

the annual reports of the company. The objectives of conceptual framework are discussed below

in details:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CONTEMPORARY ISSUES IN ACCOUNTING

1. The purpose of Conceptual framework is to ensure that the annual reports of the company

contains all relevant and necessary information which can be of use to the users of the

financial accounts of the business. These users are mainly potential investors and

stakeholders of the business. The information which are presented in the financial

statements are used for taking decisions regarding future investments and present

holdings of the shares. The financial statements are also taken as performance report of

the company. In the case of Blackmores ltd, the annual reports of the company for the

year 2017 shows necessary information which can be used by the shareholders in order to

take decision regarding investments in the shares of the company or decision relating to

holding the ownership of shares of the company. The components of the financial

statements are effectively prepared which can provide the shareholders information

regarding the overall performance of the company and also regarding how the business is

utilizing the funds of the shareholders.

2. Another objective of Conceptual framework is to effectively assess the amount of cash

inflows which is generated by the business. The framework is also used to identify the

various sources through which company can generate future cash inflows for the business

and various resources which can be used by the business. As per the annual reports of

Blackmores ltd, the business has effectively anticipated certain expenses which the

business and will be implementing new standard which can improve the reporting process

of the business in 2018.

CONTEMPORARY ISSUES IN ACCOUNTING

1. The purpose of Conceptual framework is to ensure that the annual reports of the company

contains all relevant and necessary information which can be of use to the users of the

financial accounts of the business. These users are mainly potential investors and

stakeholders of the business. The information which are presented in the financial

statements are used for taking decisions regarding future investments and present

holdings of the shares. The financial statements are also taken as performance report of

the company. In the case of Blackmores ltd, the annual reports of the company for the

year 2017 shows necessary information which can be used by the shareholders in order to

take decision regarding investments in the shares of the company or decision relating to

holding the ownership of shares of the company. The components of the financial

statements are effectively prepared which can provide the shareholders information

regarding the overall performance of the company and also regarding how the business is

utilizing the funds of the shareholders.

2. Another objective of Conceptual framework is to effectively assess the amount of cash

inflows which is generated by the business. The framework is also used to identify the

various sources through which company can generate future cash inflows for the business

and various resources which can be used by the business. As per the annual reports of

Blackmores ltd, the business has effectively anticipated certain expenses which the

business and will be implementing new standard which can improve the reporting process

of the business in 2018.

5

CONTEMPORARY ISSUES IN ACCOUNTING

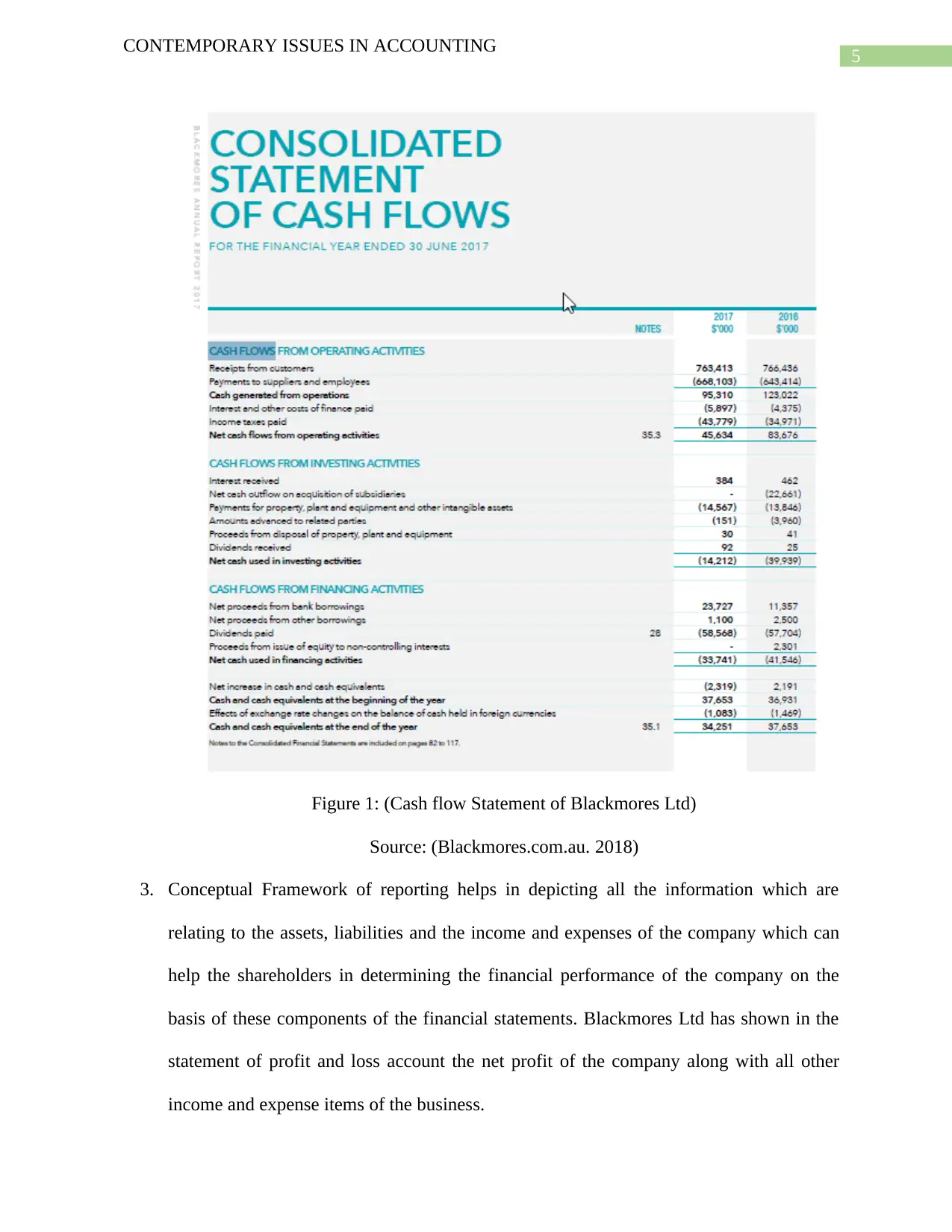

Figure 1: (Cash flow Statement of Blackmores Ltd)

Source: (Blackmores.com.au. 2018)

3. Conceptual Framework of reporting helps in depicting all the information which are

relating to the assets, liabilities and the income and expenses of the company which can

help the shareholders in determining the financial performance of the company on the

basis of these components of the financial statements. Blackmores Ltd has shown in the

statement of profit and loss account the net profit of the company along with all other

income and expense items of the business.

CONTEMPORARY ISSUES IN ACCOUNTING

Figure 1: (Cash flow Statement of Blackmores Ltd)

Source: (Blackmores.com.au. 2018)

3. Conceptual Framework of reporting helps in depicting all the information which are

relating to the assets, liabilities and the income and expenses of the company which can

help the shareholders in determining the financial performance of the company on the

basis of these components of the financial statements. Blackmores Ltd has shown in the

statement of profit and loss account the net profit of the company along with all other

income and expense items of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CONTEMPORARY ISSUES IN ACCOUNTING

Figure 2: (Profit and loss Account of Blackmores Ltd)

Source: (Blackmores.com.au. 2018)

Thus, from the above analysis of the objectives of the Conceptual framework it is clear that

the framework is very important for effective representation of the financial information of the

company in the annual reports which is prepared by the company. Such information are of

immense use to the stakeholders of the company.

CONTEMPORARY ISSUES IN ACCOUNTING

Figure 2: (Profit and loss Account of Blackmores Ltd)

Source: (Blackmores.com.au. 2018)

Thus, from the above analysis of the objectives of the Conceptual framework it is clear that

the framework is very important for effective representation of the financial information of the

company in the annual reports which is prepared by the company. Such information are of

immense use to the stakeholders of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CONTEMPORARY ISSUES IN ACCOUNTING

Recognizing Criteria

The recognition criteria of the reporting components needs to fairly represent the various

components of the financial statements which are to be recorded. Australian Accounting

Standard Board (AASB) is the board which issues standards related to accounting which set the

guidelines which are to be followed by businesses for treatment of certain items of the financial

statements and thereby ensuring that the annual reports are showing true and fair view (Ahmed,

Neel and Wang 2013). In addition to this, the conceptual framework also set a certain guideline

which is to be followed for recording and recognizing specific transactions of the business (Brief

and Peasnell 2013). The various components which are to be recognized are given below:

1. Assets: As per the general framework assets are to be subdivide into short-term assets and

long-term assets which are also known as current and non-current assets respectively.

Blackmores ltd have subdivided their assets as per the requirement of the framework. The

current assets of the company consist of cash and cash equivalents, inventory and debtors

which are commonly seen as an item of the current assets of the company. The non-

current assets of the company comprise of investment, property, plants and equipment

and deferred tax assets and intangible assets of the business.

2. Liabilities: The liabilities of the business are also sub divided into current and non-

current liabilities similarly as assets. The asset side total will always be equal to the

liability side total as per the matching principle of accounting. The current liabilities of

Blackmores ltd consist of trade payables, current tax liabilities and other current

liabilities of the business. The non-current liabilities of the business consist of interest

bearing liabilities and other liabilities as well.

CONTEMPORARY ISSUES IN ACCOUNTING

Recognizing Criteria

The recognition criteria of the reporting components needs to fairly represent the various

components of the financial statements which are to be recorded. Australian Accounting

Standard Board (AASB) is the board which issues standards related to accounting which set the

guidelines which are to be followed by businesses for treatment of certain items of the financial

statements and thereby ensuring that the annual reports are showing true and fair view (Ahmed,

Neel and Wang 2013). In addition to this, the conceptual framework also set a certain guideline

which is to be followed for recording and recognizing specific transactions of the business (Brief

and Peasnell 2013). The various components which are to be recognized are given below:

1. Assets: As per the general framework assets are to be subdivide into short-term assets and

long-term assets which are also known as current and non-current assets respectively.

Blackmores ltd have subdivided their assets as per the requirement of the framework. The

current assets of the company consist of cash and cash equivalents, inventory and debtors

which are commonly seen as an item of the current assets of the company. The non-

current assets of the company comprise of investment, property, plants and equipment

and deferred tax assets and intangible assets of the business.

2. Liabilities: The liabilities of the business are also sub divided into current and non-

current liabilities similarly as assets. The asset side total will always be equal to the

liability side total as per the matching principle of accounting. The current liabilities of

Blackmores ltd consist of trade payables, current tax liabilities and other current

liabilities of the business. The non-current liabilities of the business consist of interest

bearing liabilities and other liabilities as well.

8

CONTEMPORARY ISSUES IN ACCOUNTING

3. Income: The income of the company is recorded and shown in the profit and loss account

prepared by the company. The revenues are recognized by the company when the risks

and rewards associated with the product is transferred to third party.

4. Expenses: The expenses of the company are depicted in the profit and loss account of the

company. Some of these expenses are cash expenses while some are non-cash like

depreciation and impairment loss.

5. Equity: The equity of the company comprises of retained earnings which are generated

by the business and used for financing purpose of the business and also issued capital of

the business.

Fundamental Qualitative Characteristics

As per the financial statements of Blackmores ltd, the financial statements contain the

qualitative characteristics which are given below in details:

1. Relevance: This principle states that the annual reports of any business should include

information which are relevant and which can be used by the shareholders of the

company (Zhang and Andrew 2014). In the case of Blackmores ltd, all related AASB and

IAS standard which is relevant has been followed.

2. Faithful representation: In order to prove that the financial statements are showing true

and fair view, the financial statement are audited and independently investigated by an

independent and competent auditor (Beattie 2014). The auditors of the company are

Deloitte which is one of the big 4 auditing firms. The auditor of Blackmores ltd is of the

view that the financial statements are showing true and fair view and the company has

complied with all relevant accounting standards and principles.

CONTEMPORARY ISSUES IN ACCOUNTING

3. Income: The income of the company is recorded and shown in the profit and loss account

prepared by the company. The revenues are recognized by the company when the risks

and rewards associated with the product is transferred to third party.

4. Expenses: The expenses of the company are depicted in the profit and loss account of the

company. Some of these expenses are cash expenses while some are non-cash like

depreciation and impairment loss.

5. Equity: The equity of the company comprises of retained earnings which are generated

by the business and used for financing purpose of the business and also issued capital of

the business.

Fundamental Qualitative Characteristics

As per the financial statements of Blackmores ltd, the financial statements contain the

qualitative characteristics which are given below in details:

1. Relevance: This principle states that the annual reports of any business should include

information which are relevant and which can be used by the shareholders of the

company (Zhang and Andrew 2014). In the case of Blackmores ltd, all related AASB and

IAS standard which is relevant has been followed.

2. Faithful representation: In order to prove that the financial statements are showing true

and fair view, the financial statement are audited and independently investigated by an

independent and competent auditor (Beattie 2014). The auditors of the company are

Deloitte which is one of the big 4 auditing firms. The auditor of Blackmores ltd is of the

view that the financial statements are showing true and fair view and the company has

complied with all relevant accounting standards and principles.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CONTEMPORARY ISSUES IN ACCOUNTING

Enhancing Qualitative Characteristics

The Enhancing Qualitative features of the financial report of the Blackmores ltd are given

below in details:

1. Comparability: As per this principle the users of the financial statements are able to

compare the similarities and differences which arises between the results of the financial

statement of a company between two periods (Palea 2013).

2. Verifiability: This principle states that the financial statements should be verifiable by the

users of the financial statements of the company.

3. Timeliness: The principle states that financial information should be made available to

the shareholders of the company in a timely manner.

4. Understandability: The financial statements should be such that the users of the financial

statements are able to clearly understand the financial information. The information

should be properly classified, summarized and presented in a concise manner which can

promote understanding (Macve 2015).

Conclusion and Recommendations

Thus, from the analysis of the annual reports of Blackmores ltd it is clear that the

company follows conceptual framework of reporting as the company as recorded all the relevant

transaction which can help the users to gain understanding of the financial statements are shown

in the financial statement of the company. In addition to this, the financial statements also satisfy

the fundamental and Enhancing qualitative features of the financial statements. The financial

reports of the company also follow recognition criteria which enables the financial statements to

contain all relevant information which can be of use to the potential investors and stakeholders of

the business.

CONTEMPORARY ISSUES IN ACCOUNTING

Enhancing Qualitative Characteristics

The Enhancing Qualitative features of the financial report of the Blackmores ltd are given

below in details:

1. Comparability: As per this principle the users of the financial statements are able to

compare the similarities and differences which arises between the results of the financial

statement of a company between two periods (Palea 2013).

2. Verifiability: This principle states that the financial statements should be verifiable by the

users of the financial statements of the company.

3. Timeliness: The principle states that financial information should be made available to

the shareholders of the company in a timely manner.

4. Understandability: The financial statements should be such that the users of the financial

statements are able to clearly understand the financial information. The information

should be properly classified, summarized and presented in a concise manner which can

promote understanding (Macve 2015).

Conclusion and Recommendations

Thus, from the analysis of the annual reports of Blackmores ltd it is clear that the

company follows conceptual framework of reporting as the company as recorded all the relevant

transaction which can help the users to gain understanding of the financial statements are shown

in the financial statement of the company. In addition to this, the financial statements also satisfy

the fundamental and Enhancing qualitative features of the financial statements. The financial

reports of the company also follow recognition criteria which enables the financial statements to

contain all relevant information which can be of use to the potential investors and stakeholders of

the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CONTEMPORARY ISSUES IN ACCOUNTING

Recommendation

The recommendations which can be given to the company which can lead to further

improvement of the reporting framework is given below in points form:

1. The management needs to improve the disclosing requirement of Key audit matters

which relates to rebate of $ 143.5 million and the same need to be explained clearly in the

financial statements.

2. The financial statement of Blackmores ltd can be improved further with better

presentation of the financial information of the business.

CONTEMPORARY ISSUES IN ACCOUNTING

Recommendation

The recommendations which can be given to the company which can lead to further

improvement of the reporting framework is given below in points form:

1. The management needs to improve the disclosing requirement of Key audit matters

which relates to rebate of $ 143.5 million and the same need to be explained clearly in the

financial statements.

2. The financial statement of Blackmores ltd can be improved further with better

presentation of the financial information of the business.

11

CONTEMPORARY ISSUES IN ACCOUNTING

Reference

Ahmed, A.S., Neel, M. and Wang, D., 2013. Does mandatory adoption of IFRS improve

accounting quality? Preliminary evidence. Contemporary Accounting Research, 30(4), pp.1344-

1372.

Beattie, V., 2014. Accounting narratives and the narrative turn in accounting research: Issues,

theory, methodology, methods and a research framework. The British Accounting Review, 46(2),

pp.111-134.

Blackmores.com.au. (2018). Company information. [online] Available at:

https://www.blackmores.com.au/about-us/company-information [Accessed 20 Apr. 2018].

Brief, R.P. and Peasnell, K.V. eds., 2013. Clean surplus: A link between accounting and finance.

Routledge.

Díaz, S., Demissew, S., Carabias, J., Joly, C., Lonsdale, M., Ash, N., Larigauderie, A., Adhikari,

J.R., Arico, S., Báldi, A. and Bartuska, A., 2015. The IPBES Conceptual Framework—

connecting nature and people. Current Opinion in Environmental Sustainability, 14, pp.1-16.

Libby, R., 2017. Accounting and human information processing. In The Routledge Companion

to Behavioural Accounting Research (pp. 42-54). Routledge.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Palea, V., 2013. IAS/IFRS and financial reporting quality: lessons from the European

experience. China Journal of Accounting Research, 6(4), pp.247-263.

Zhang, Y. and Andrew, J., 2014. Financialisation and the conceptual framework. Critical

perspectives on accounting, 25(1), pp.17-26.

CONTEMPORARY ISSUES IN ACCOUNTING

Reference

Ahmed, A.S., Neel, M. and Wang, D., 2013. Does mandatory adoption of IFRS improve

accounting quality? Preliminary evidence. Contemporary Accounting Research, 30(4), pp.1344-

1372.

Beattie, V., 2014. Accounting narratives and the narrative turn in accounting research: Issues,

theory, methodology, methods and a research framework. The British Accounting Review, 46(2),

pp.111-134.

Blackmores.com.au. (2018). Company information. [online] Available at:

https://www.blackmores.com.au/about-us/company-information [Accessed 20 Apr. 2018].

Brief, R.P. and Peasnell, K.V. eds., 2013. Clean surplus: A link between accounting and finance.

Routledge.

Díaz, S., Demissew, S., Carabias, J., Joly, C., Lonsdale, M., Ash, N., Larigauderie, A., Adhikari,

J.R., Arico, S., Báldi, A. and Bartuska, A., 2015. The IPBES Conceptual Framework—

connecting nature and people. Current Opinion in Environmental Sustainability, 14, pp.1-16.

Libby, R., 2017. Accounting and human information processing. In The Routledge Companion

to Behavioural Accounting Research (pp. 42-54). Routledge.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Palea, V., 2013. IAS/IFRS and financial reporting quality: lessons from the European

experience. China Journal of Accounting Research, 6(4), pp.247-263.

Zhang, Y. and Andrew, J., 2014. Financialisation and the conceptual framework. Critical

perspectives on accounting, 25(1), pp.17-26.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.