Business Valuation: Prospective Analysis of Blackmores Limited

VerifiedAdded on 2023/06/04

|25

|7176

|146

Report

AI Summary

This report provides a comprehensive business valuation and financial analysis of Blackmores Limited, an Australian health products company. It includes forecasting of sales growth, asset turnover ratio, and profit margin for the next five years (2019-2023) using historical data and market trends. The report applies various valuation models, including the Dividend Discount Model, Residual Income Model, Residual Operating Income Model, and Free Cash Flow Model, to estimate the firm's share value. A sensitivity analysis is performed on key forecasting assumptions using the Residual Operating Income Model to assess potential opportunities and challenges for Blackmores. The analysis concludes with management consulting decisions, offering specific remedies for identified concerns.

Running Head: Business valuation and analysis

1

Project Report: Business valuation and analysis

1

Project Report: Business valuation and analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business valuation and analysis 2

Contents

Introduction:.....................................................................................................................4

Forecasting:.......................................................................................................................4

Sales growth:................................................................................................................4

Asset turnover ratio forecast (ATO forecast):..............................................................7

PM:...............................................................................................................................8

Free cash flow and Net dividend payout ratio forecasting:........................................10

Cost of debt:................................................................................................................11

Cost of equity:.............................................................................................................12

Valuation:.......................................................................................................................13

Dividend discount model:...........................................................................................14

Residual income model:.............................................................................................15

Residual operating income model:.............................................................................15

Free cash flow model:.................................................................................................16

Sensitivity analysis:........................................................................................................16

Sales growth:..............................................................................................................16

ATO:...........................................................................................................................17

PM:.............................................................................................................................17

Net dividend payout ratio:..........................................................................................18

Cost of debt:................................................................................................................18

Cost of equity and WACC:.........................................................................................18

Management consulting decisions:.................................................................................19

Opportunities..............................................................................................................19

Contents

Introduction:.....................................................................................................................4

Forecasting:.......................................................................................................................4

Sales growth:................................................................................................................4

Asset turnover ratio forecast (ATO forecast):..............................................................7

PM:...............................................................................................................................8

Free cash flow and Net dividend payout ratio forecasting:........................................10

Cost of debt:................................................................................................................11

Cost of equity:.............................................................................................................12

Valuation:.......................................................................................................................13

Dividend discount model:...........................................................................................14

Residual income model:.............................................................................................15

Residual operating income model:.............................................................................15

Free cash flow model:.................................................................................................16

Sensitivity analysis:........................................................................................................16

Sales growth:..............................................................................................................16

ATO:...........................................................................................................................17

PM:.............................................................................................................................17

Net dividend payout ratio:..........................................................................................18

Cost of debt:................................................................................................................18

Cost of equity and WACC:.........................................................................................18

Management consulting decisions:.................................................................................19

Opportunities..............................................................................................................19

Business valuation and analysis 3

Challenges...................................................................................................................19

Conclusion:.....................................................................................................................20

References:.....................................................................................................................21

Appendix.........................................................................................................................22

Challenges...................................................................................................................19

Conclusion:.....................................................................................................................20

References:.....................................................................................................................21

Appendix.........................................................................................................................22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business valuation and analysis 4

Introduction:

The report has been prepared on Blackmore limited. The future forecasting, valuation,

sensitivity analysis, management consulting decision etc models have been applied on the

company to measure the future performance and current capital market performance of the

business. Blackmore limited is an Australian company which offers health products such as

herbal supplements and vitamins. The company has started its operations in the year of 1930

and from that time, it has expanded its business into overseas market. The prospective

analysis has been done on the company along with the other financial models to measure the

future performance of the company. the main objectives of the report is to evaluate the

overall market performance and the future forecasting of the company in order to make a

better investment decision in the company.

Forecasting:

Forecasting analysis is a financial analysis model which is used by the financial analyst

or financial manager of an organization in concern to evaluate the future performance &

position of an organization. In the case of Blackmore limited, a forecasting process has been

done on the company for the next 5 years from 2019 to 2023. The historical data of the

company has been taken into the context to calculate the future changes in the business. The

other factors have also been taken into the context to measure the company’s overall financial

performance in next 5 years.

Sales growth:

In order to forecast the sales growth, sales price and the quality of the products of the

company, the forecasting application has been applied on the business. In order to evaluate

the past sales growth of the business, it has been found that the sales growth of the company

has been influenced with the industry, GDP; inflation rate etc. on the basis of calculations,

sales growth rate of the business was higher in 2016. The revenue of the Blackmore limited

was $ 717,211 thousand. The reasons behind this expansion are china market which has boost

up the overall sales of the company.

Though, in the year of 2017 and 2018, a decrement has been seen in the sales growth of

the business because of the sales pattern of the business. However, the sales price and product

Introduction:

The report has been prepared on Blackmore limited. The future forecasting, valuation,

sensitivity analysis, management consulting decision etc models have been applied on the

company to measure the future performance and current capital market performance of the

business. Blackmore limited is an Australian company which offers health products such as

herbal supplements and vitamins. The company has started its operations in the year of 1930

and from that time, it has expanded its business into overseas market. The prospective

analysis has been done on the company along with the other financial models to measure the

future performance of the company. the main objectives of the report is to evaluate the

overall market performance and the future forecasting of the company in order to make a

better investment decision in the company.

Forecasting:

Forecasting analysis is a financial analysis model which is used by the financial analyst

or financial manager of an organization in concern to evaluate the future performance &

position of an organization. In the case of Blackmore limited, a forecasting process has been

done on the company for the next 5 years from 2019 to 2023. The historical data of the

company has been taken into the context to calculate the future changes in the business. The

other factors have also been taken into the context to measure the company’s overall financial

performance in next 5 years.

Sales growth:

In order to forecast the sales growth, sales price and the quality of the products of the

company, the forecasting application has been applied on the business. In order to evaluate

the past sales growth of the business, it has been found that the sales growth of the company

has been influenced with the industry, GDP; inflation rate etc. on the basis of calculations,

sales growth rate of the business was higher in 2016. The revenue of the Blackmore limited

was $ 717,211 thousand. The reasons behind this expansion are china market which has boost

up the overall sales of the company.

Though, in the year of 2017 and 2018, a decrement has been seen in the sales growth of

the business because of the sales pattern of the business. However, the sales price and product

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business valuation and analysis 5

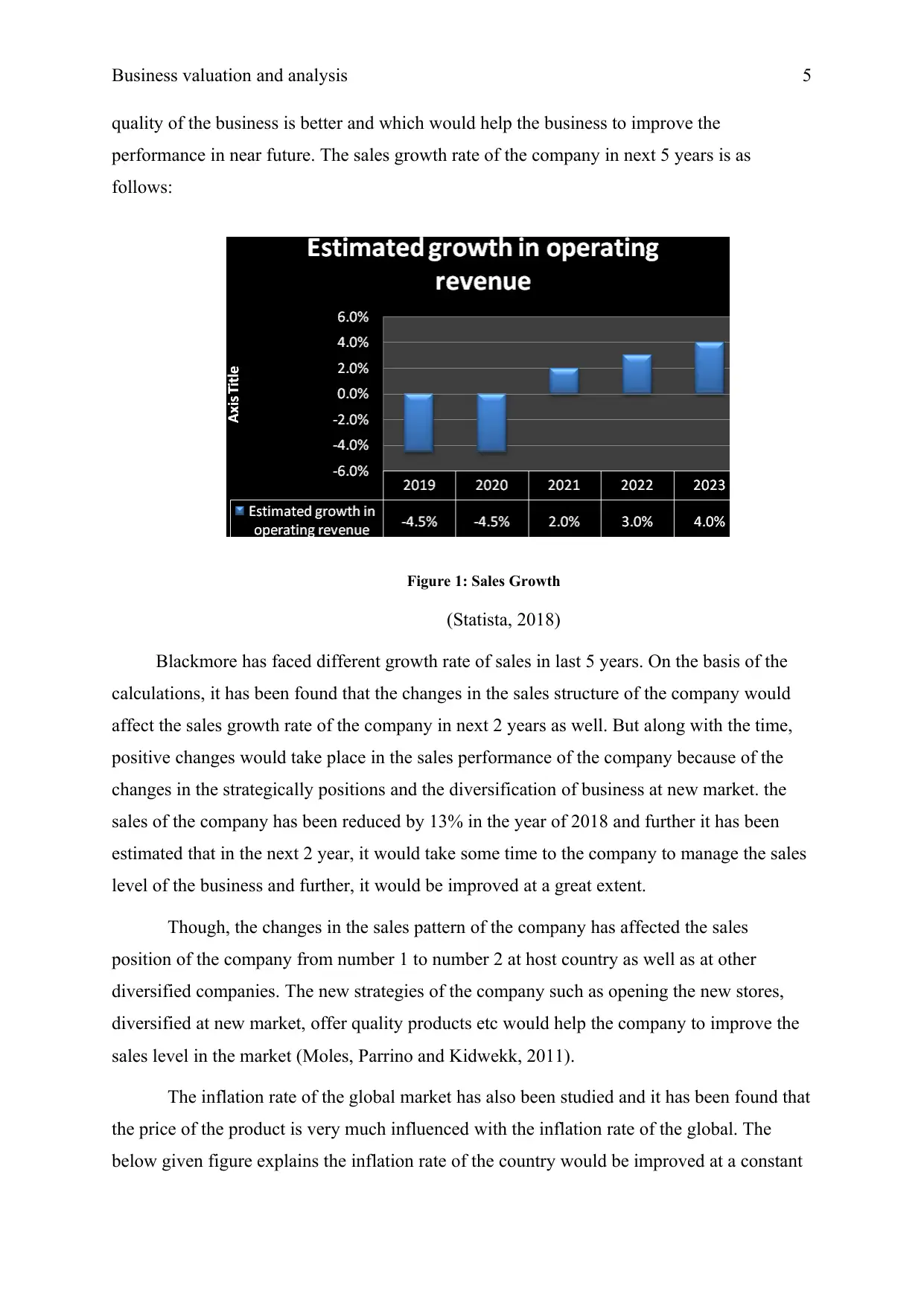

quality of the business is better and which would help the business to improve the

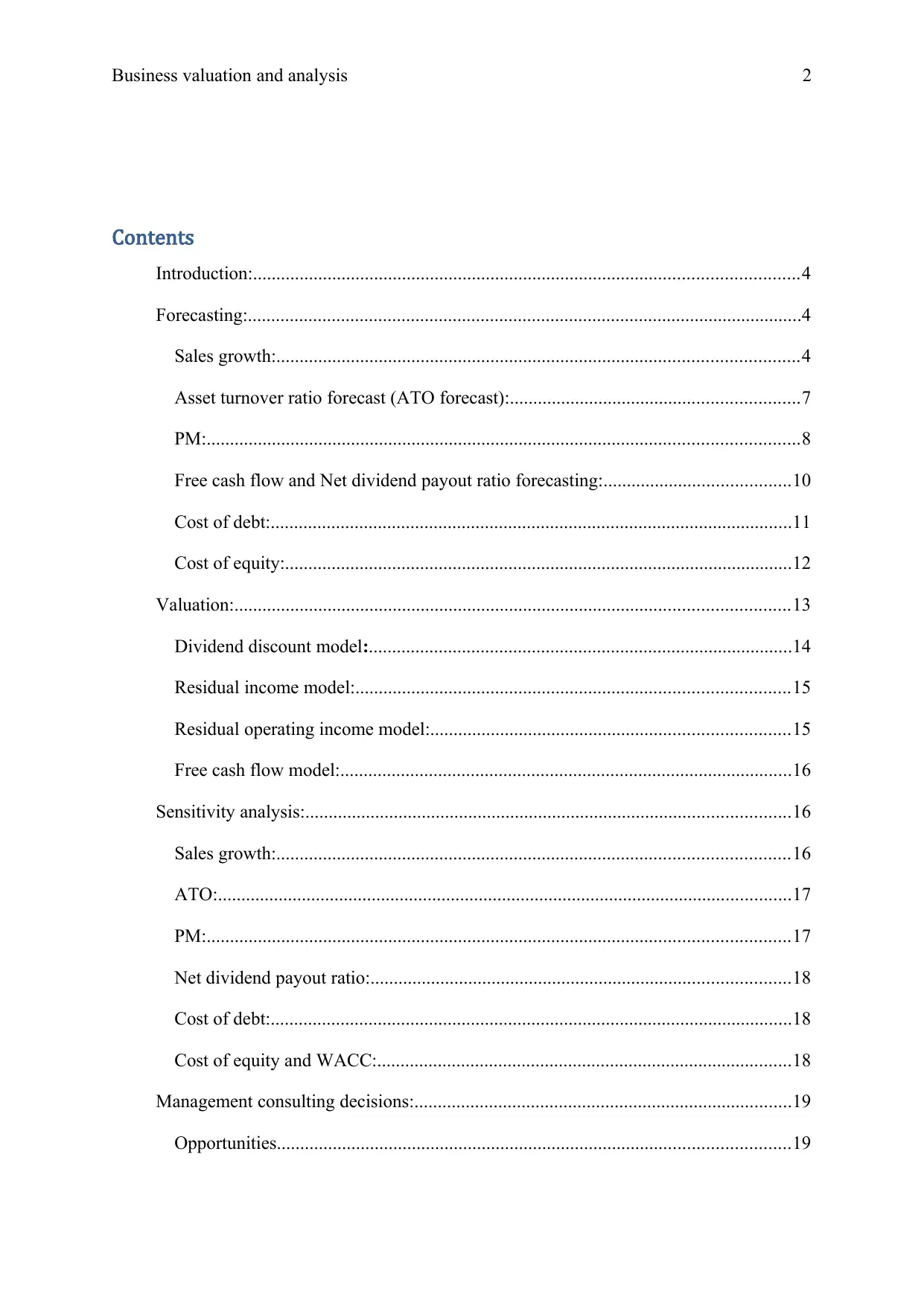

performance in near future. The sales growth rate of the company in next 5 years is as

follows:

Figure 1: Sales Growth

(Statista, 2018)

Blackmore has faced different growth rate of sales in last 5 years. On the basis of the

calculations, it has been found that the changes in the sales structure of the company would

affect the sales growth rate of the company in next 2 years as well. But along with the time,

positive changes would take place in the sales performance of the company because of the

changes in the strategically positions and the diversification of business at new market. the

sales of the company has been reduced by 13% in the year of 2018 and further it has been

estimated that in the next 2 year, it would take some time to the company to manage the sales

level of the business and further, it would be improved at a great extent.

Though, the changes in the sales pattern of the company has affected the sales

position of the company from number 1 to number 2 at host country as well as at other

diversified companies. The new strategies of the company such as opening the new stores,

diversified at new market, offer quality products etc would help the company to improve the

sales level in the market (Moles, Parrino and Kidwekk, 2011).

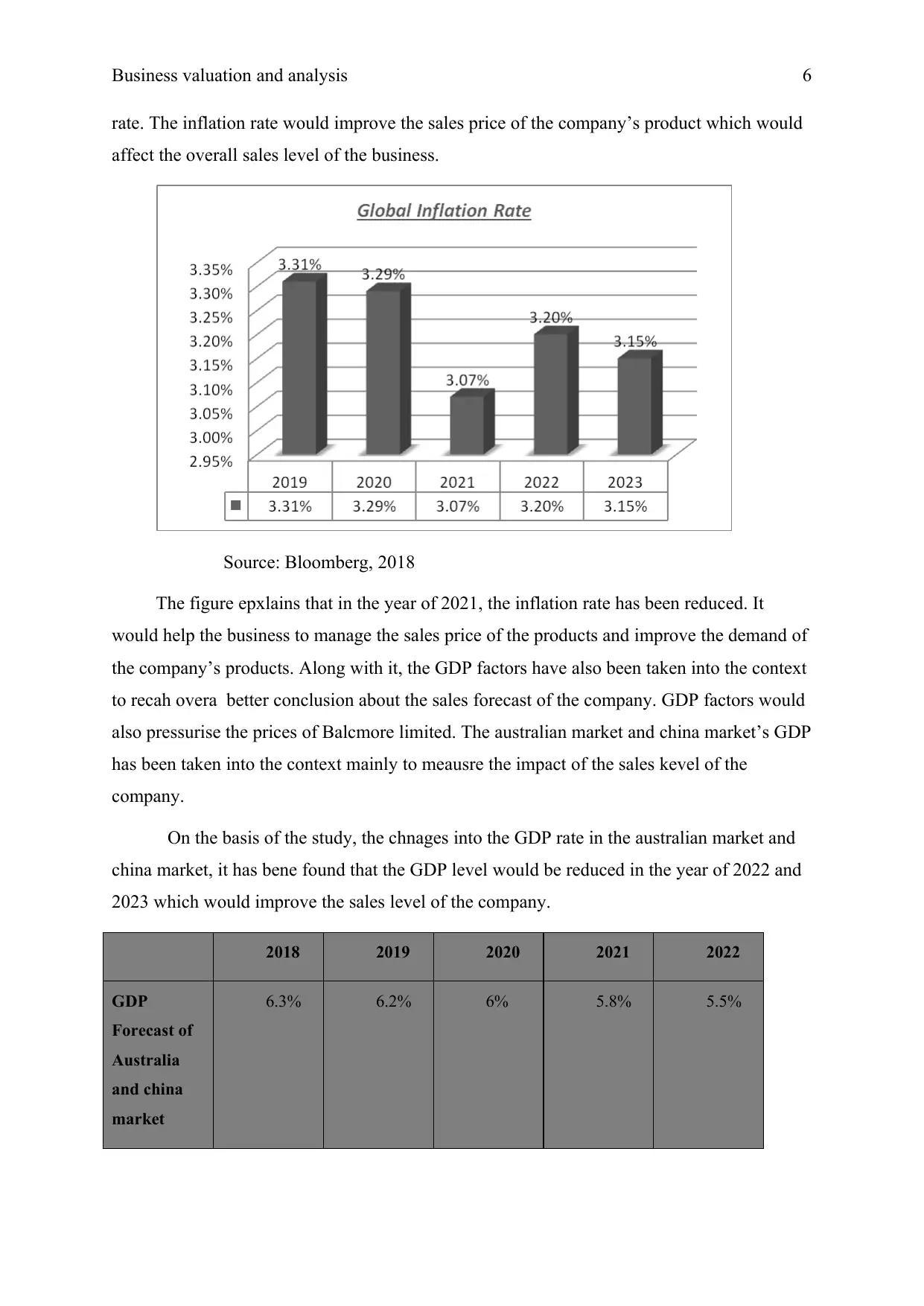

The inflation rate of the global market has also been studied and it has been found that

the price of the product is very much influenced with the inflation rate of the global. The

below given figure explains the inflation rate of the country would be improved at a constant

quality of the business is better and which would help the business to improve the

performance in near future. The sales growth rate of the company in next 5 years is as

follows:

Figure 1: Sales Growth

(Statista, 2018)

Blackmore has faced different growth rate of sales in last 5 years. On the basis of the

calculations, it has been found that the changes in the sales structure of the company would

affect the sales growth rate of the company in next 2 years as well. But along with the time,

positive changes would take place in the sales performance of the company because of the

changes in the strategically positions and the diversification of business at new market. the

sales of the company has been reduced by 13% in the year of 2018 and further it has been

estimated that in the next 2 year, it would take some time to the company to manage the sales

level of the business and further, it would be improved at a great extent.

Though, the changes in the sales pattern of the company has affected the sales

position of the company from number 1 to number 2 at host country as well as at other

diversified companies. The new strategies of the company such as opening the new stores,

diversified at new market, offer quality products etc would help the company to improve the

sales level in the market (Moles, Parrino and Kidwekk, 2011).

The inflation rate of the global market has also been studied and it has been found that

the price of the product is very much influenced with the inflation rate of the global. The

below given figure explains the inflation rate of the country would be improved at a constant

Business valuation and analysis 6

rate. The inflation rate would improve the sales price of the company’s product which would

affect the overall sales level of the business.

Source: Bloomberg, 2018

The figure epxlains that in the year of 2021, the inflation rate has been reduced. It

would help the business to manage the sales price of the products and improve the demand of

the company’s products. Along with it, the GDP factors have also been taken into the context

to recah overa better conclusion about the sales forecast of the company. GDP factors would

also pressurise the prices of Balcmore limited. The australian market and china market’s GDP

has been taken into the context mainly to meausre the impact of the sales kevel of the

company.

On the basis of the study, the chnages into the GDP rate in the australian market and

china market, it has bene found that the GDP level would be reduced in the year of 2022 and

2023 which would improve the sales level of the company.

2018 2019 2020 2021 2022

GDP

Forecast of

Australia

and china

market

6.3% 6.2% 6% 5.8% 5.5%

rate. The inflation rate would improve the sales price of the company’s product which would

affect the overall sales level of the business.

Source: Bloomberg, 2018

The figure epxlains that in the year of 2021, the inflation rate has been reduced. It

would help the business to manage the sales price of the products and improve the demand of

the company’s products. Along with it, the GDP factors have also been taken into the context

to recah overa better conclusion about the sales forecast of the company. GDP factors would

also pressurise the prices of Balcmore limited. The australian market and china market’s GDP

has been taken into the context mainly to meausre the impact of the sales kevel of the

company.

On the basis of the study, the chnages into the GDP rate in the australian market and

china market, it has bene found that the GDP level would be reduced in the year of 2022 and

2023 which would improve the sales level of the company.

2018 2019 2020 2021 2022

GDP

Forecast of

Australia

and china

market

6.3% 6.2% 6% 5.8% 5.5%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business valuation and analysis 7

The other factors such as population rate, industry growth rate etc has been taken into

the concern. The population rate of the country is expected to be decreased because of the

low fertility rate as well as the industry growth rate would be expected to be improved in near

future which would lead to the business towards better performance. On the basis of the

overall study on the sales growth rate, it has been measured that the overall performance of

sales would be improved in the year of 2021, 2022 and 2023. The diversification and other

strategies would help the business to achieve the level.

Asset turnover ratio forecast (ATO forecast):

In order to forecast the asset turnover ratio, efficiency level and the past figures,

performance of the assets have been measured. The forecasting application has been applied

on the business to identify the overall performance in near future. In order to evaluate the

ATO ratio of the business, it has been found that the level of asset depends on the demand of

the products of the business. On the basis of calculations, asset turnover forecast of the

company was higher in the year of 2016. The ATO ratio of the company was 2.92. The

reasons behind this expansion are the better management of the assets in order to expand the

sales level in the china market (Madura, 2014).

Though, in the year of 2017 and 2018, a decrement has been seen in the ATO ratio of

the business because of the decrement in the sales level of the business. However, the few

changes into the strategically performance and the resources level would make the changes in

the overall performance of the business. The ATO forecast of the company in next 5 years is

as follows:

The other factors such as population rate, industry growth rate etc has been taken into

the concern. The population rate of the country is expected to be decreased because of the

low fertility rate as well as the industry growth rate would be expected to be improved in near

future which would lead to the business towards better performance. On the basis of the

overall study on the sales growth rate, it has been measured that the overall performance of

sales would be improved in the year of 2021, 2022 and 2023. The diversification and other

strategies would help the business to achieve the level.

Asset turnover ratio forecast (ATO forecast):

In order to forecast the asset turnover ratio, efficiency level and the past figures,

performance of the assets have been measured. The forecasting application has been applied

on the business to identify the overall performance in near future. In order to evaluate the

ATO ratio of the business, it has been found that the level of asset depends on the demand of

the products of the business. On the basis of calculations, asset turnover forecast of the

company was higher in the year of 2016. The ATO ratio of the company was 2.92. The

reasons behind this expansion are the better management of the assets in order to expand the

sales level in the china market (Madura, 2014).

Though, in the year of 2017 and 2018, a decrement has been seen in the ATO ratio of

the business because of the decrement in the sales level of the business. However, the few

changes into the strategically performance and the resources level would make the changes in

the overall performance of the business. The ATO forecast of the company in next 5 years is

as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business valuation and analysis 8

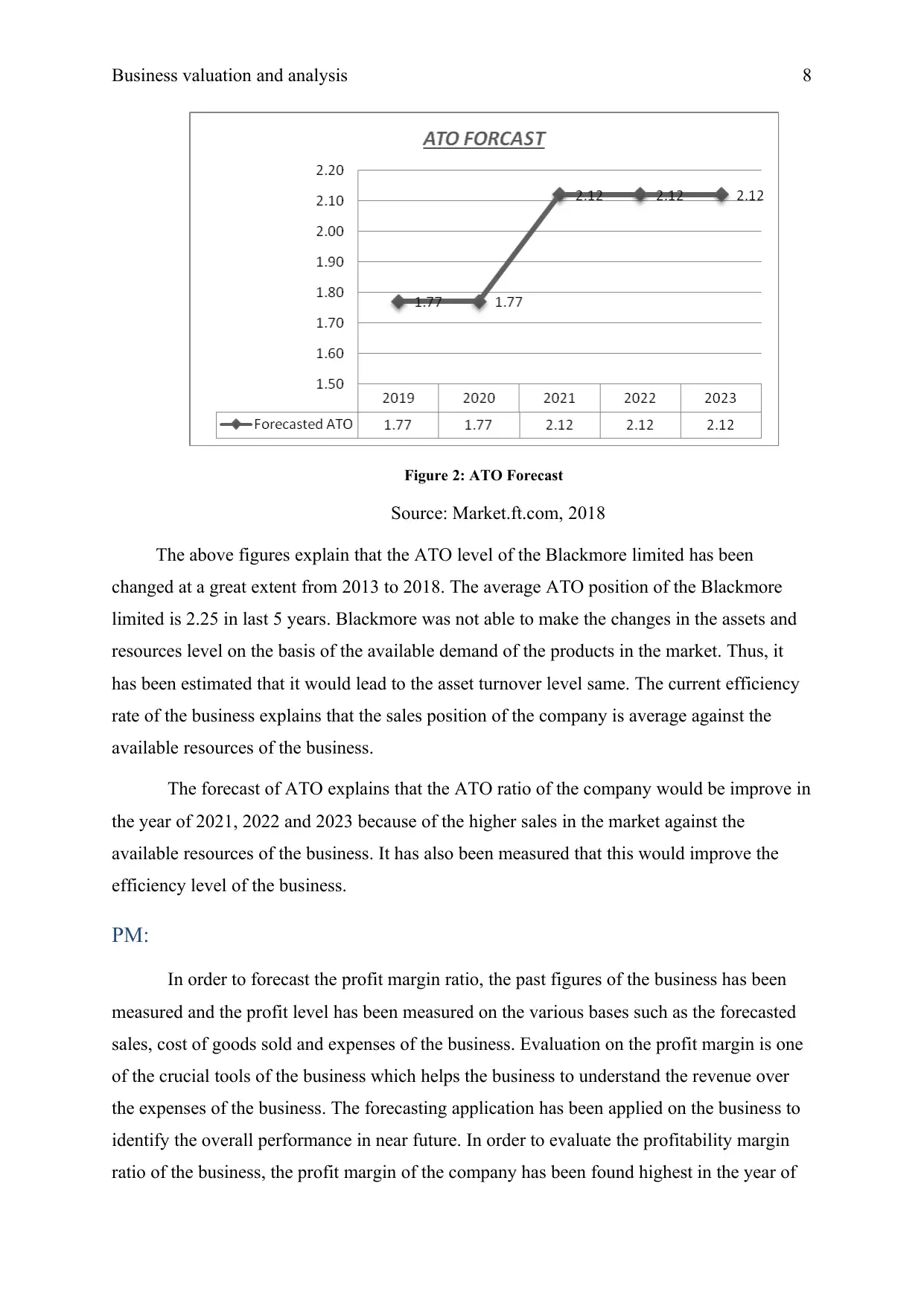

Figure 2: ATO Forecast

Source: Market.ft.com, 2018

The above figures explain that the ATO level of the Blackmore limited has been

changed at a great extent from 2013 to 2018. The average ATO position of the Blackmore

limited is 2.25 in last 5 years. Blackmore was not able to make the changes in the assets and

resources level on the basis of the available demand of the products in the market. Thus, it

has been estimated that it would lead to the asset turnover level same. The current efficiency

rate of the business explains that the sales position of the company is average against the

available resources of the business.

The forecast of ATO explains that the ATO ratio of the company would be improve in

the year of 2021, 2022 and 2023 because of the higher sales in the market against the

available resources of the business. It has also been measured that this would improve the

efficiency level of the business.

PM:

In order to forecast the profit margin ratio, the past figures of the business has been

measured and the profit level has been measured on the various bases such as the forecasted

sales, cost of goods sold and expenses of the business. Evaluation on the profit margin is one

of the crucial tools of the business which helps the business to understand the revenue over

the expenses of the business. The forecasting application has been applied on the business to

identify the overall performance in near future. In order to evaluate the profitability margin

ratio of the business, the profit margin of the company has been found highest in the year of

Figure 2: ATO Forecast

Source: Market.ft.com, 2018

The above figures explain that the ATO level of the Blackmore limited has been

changed at a great extent from 2013 to 2018. The average ATO position of the Blackmore

limited is 2.25 in last 5 years. Blackmore was not able to make the changes in the assets and

resources level on the basis of the available demand of the products in the market. Thus, it

has been estimated that it would lead to the asset turnover level same. The current efficiency

rate of the business explains that the sales position of the company is average against the

available resources of the business.

The forecast of ATO explains that the ATO ratio of the company would be improve in

the year of 2021, 2022 and 2023 because of the higher sales in the market against the

available resources of the business. It has also been measured that this would improve the

efficiency level of the business.

PM:

In order to forecast the profit margin ratio, the past figures of the business has been

measured and the profit level has been measured on the various bases such as the forecasted

sales, cost of goods sold and expenses of the business. Evaluation on the profit margin is one

of the crucial tools of the business which helps the business to understand the revenue over

the expenses of the business. The forecasting application has been applied on the business to

identify the overall performance in near future. In order to evaluate the profitability margin

ratio of the business, the profit margin of the company has been found highest in the year of

Business valuation and analysis 9

2016. The PM ratio of the company was 101,287 thousands and the increment rate in profit

margin is 107%. The reasons behind this expansion are the higher sales turnover of the

business and the better management of the expenses of the company (Blackmore.com.au,

2018).

Though, in the year of 2017 and 2018, a decrement has been seen in the PM ratio of the

business because of the decrement in the sales level of the business. However, the few

changes into the strategically performance and the resources level would make the changes in

the overall performance of the business. The Pm forecast of the company in next 5 years is as

follows:

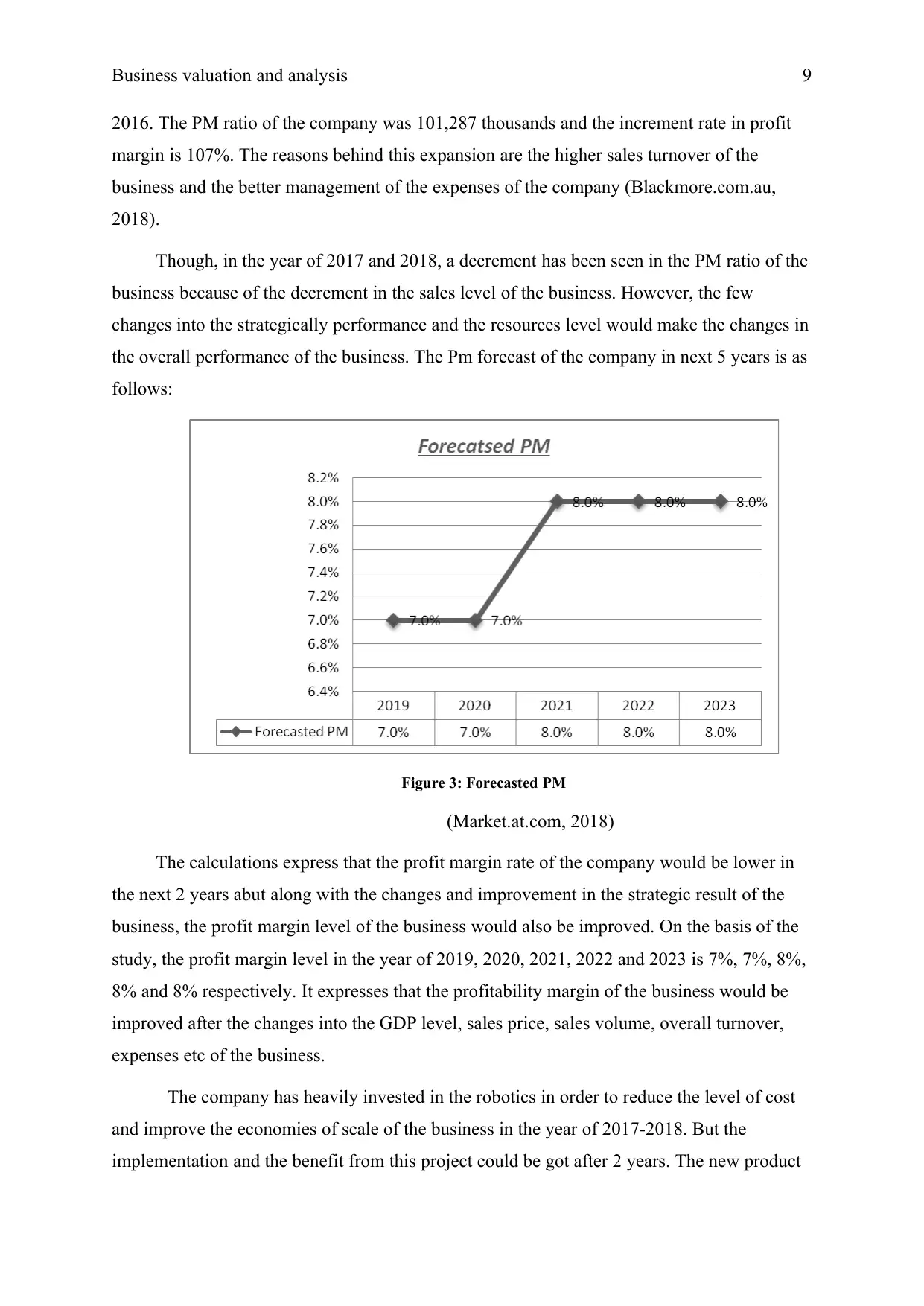

Figure 3: Forecasted PM

(Market.at.com, 2018)

The calculations express that the profit margin rate of the company would be lower in

the next 2 years abut along with the changes and improvement in the strategic result of the

business, the profit margin level of the business would also be improved. On the basis of the

study, the profit margin level in the year of 2019, 2020, 2021, 2022 and 2023 is 7%, 7%, 8%,

8% and 8% respectively. It expresses that the profitability margin of the business would be

improved after the changes into the GDP level, sales price, sales volume, overall turnover,

expenses etc of the business.

The company has heavily invested in the robotics in order to reduce the level of cost

and improve the economies of scale of the business in the year of 2017-2018. But the

implementation and the benefit from this project could be got after 2 years. The new product

2016. The PM ratio of the company was 101,287 thousands and the increment rate in profit

margin is 107%. The reasons behind this expansion are the higher sales turnover of the

business and the better management of the expenses of the company (Blackmore.com.au,

2018).

Though, in the year of 2017 and 2018, a decrement has been seen in the PM ratio of the

business because of the decrement in the sales level of the business. However, the few

changes into the strategically performance and the resources level would make the changes in

the overall performance of the business. The Pm forecast of the company in next 5 years is as

follows:

Figure 3: Forecasted PM

(Market.at.com, 2018)

The calculations express that the profit margin rate of the company would be lower in

the next 2 years abut along with the changes and improvement in the strategic result of the

business, the profit margin level of the business would also be improved. On the basis of the

study, the profit margin level in the year of 2019, 2020, 2021, 2022 and 2023 is 7%, 7%, 8%,

8% and 8% respectively. It expresses that the profitability margin of the business would be

improved after the changes into the GDP level, sales price, sales volume, overall turnover,

expenses etc of the business.

The company has heavily invested in the robotics in order to reduce the level of cost

and improve the economies of scale of the business in the year of 2017-2018. But the

implementation and the benefit from this project could be got after 2 years. The new product

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business valuation and analysis 10

launch of the company, infant baby formula would also improve the profitability level of the

business. Further, it has been found that the demand in the industry is continuously improving

which would improve the profit margin of Blackmore limited.

In the profitability trend of the company, the profit margin of the Blackmore limited has

been reduced in the year of 2017 and 2018. The negative trend has come into the profitability

margin of the business because of the shield increment in the sales level and profitability

level of the company in the year of 2016. The forecasting level explains that in next 5 years,

the highest profit margin growth rate of the company would be 8% only because of the lower

demand of the products and various GDP, inflation rate, political factors etc in the business

(Higgins, 2012).

However, the international market diversification could help the business to improve

the sales and the profit margin level of the business. The previous data of the company

represent that around $ 312 million sales of the company id from Asian market only. So a

conversion rate would help the company to reduce the overall expenses and improve the

profitability margin of the business. It has been estimated that the AUD conversion rate slows

at reduced rate on the basis of the USD rate. However, in case of Chinese currency, Yuan, it

has been found that the reduced rate of Yuan is higher. The changes and the implementation

of conversion rate in the business would improve the overall performance of the business.

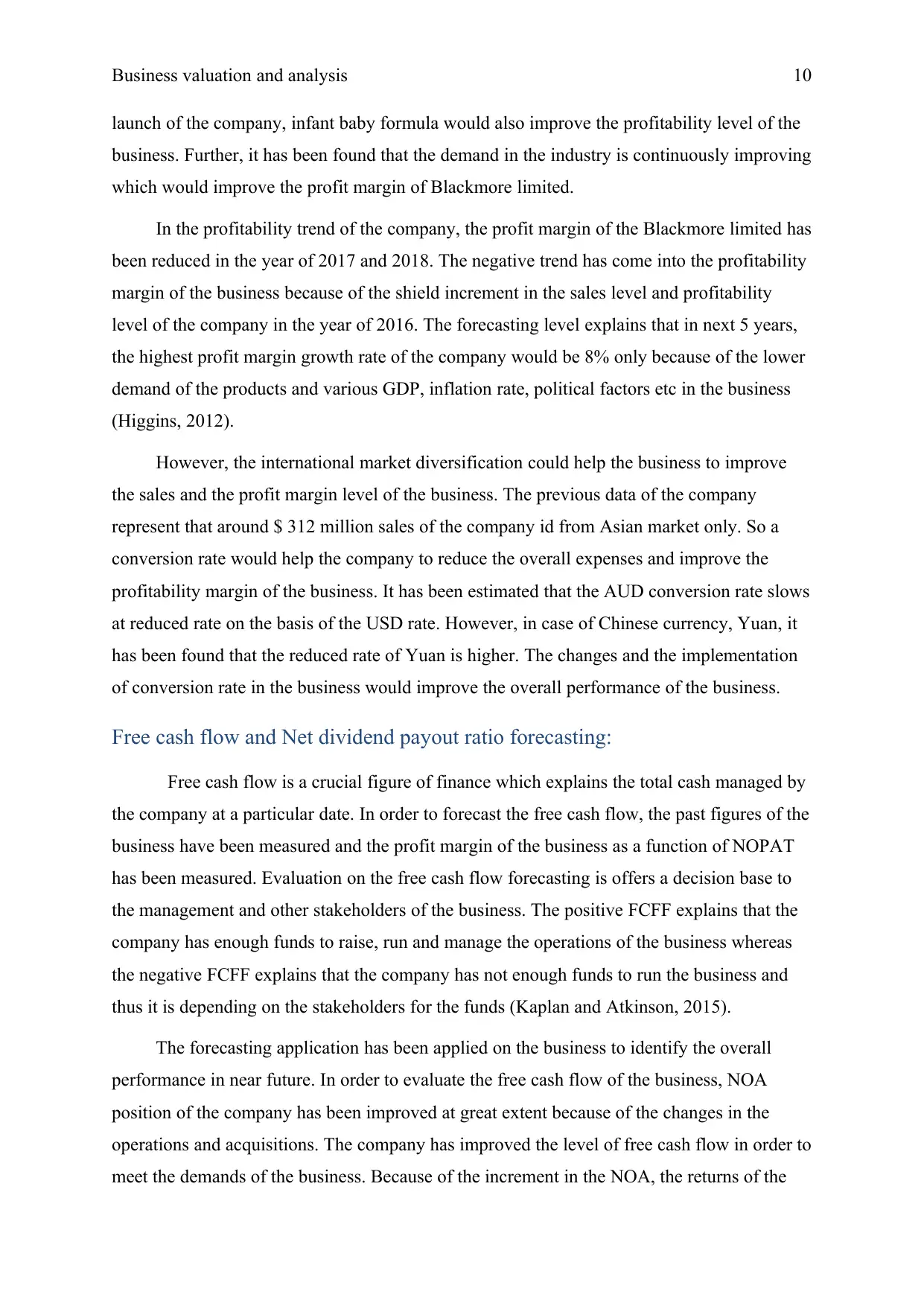

Free cash flow and Net dividend payout ratio forecasting:

Free cash flow is a crucial figure of finance which explains the total cash managed by

the company at a particular date. In order to forecast the free cash flow, the past figures of the

business have been measured and the profit margin of the business as a function of NOPAT

has been measured. Evaluation on the free cash flow forecasting is offers a decision base to

the management and other stakeholders of the business. The positive FCFF explains that the

company has enough funds to raise, run and manage the operations of the business whereas

the negative FCFF explains that the company has not enough funds to run the business and

thus it is depending on the stakeholders for the funds (Kaplan and Atkinson, 2015).

The forecasting application has been applied on the business to identify the overall

performance in near future. In order to evaluate the free cash flow of the business, NOA

position of the company has been improved at great extent because of the changes in the

operations and acquisitions. The company has improved the level of free cash flow in order to

meet the demands of the business. Because of the increment in the NOA, the returns of the

launch of the company, infant baby formula would also improve the profitability level of the

business. Further, it has been found that the demand in the industry is continuously improving

which would improve the profit margin of Blackmore limited.

In the profitability trend of the company, the profit margin of the Blackmore limited has

been reduced in the year of 2017 and 2018. The negative trend has come into the profitability

margin of the business because of the shield increment in the sales level and profitability

level of the company in the year of 2016. The forecasting level explains that in next 5 years,

the highest profit margin growth rate of the company would be 8% only because of the lower

demand of the products and various GDP, inflation rate, political factors etc in the business

(Higgins, 2012).

However, the international market diversification could help the business to improve

the sales and the profit margin level of the business. The previous data of the company

represent that around $ 312 million sales of the company id from Asian market only. So a

conversion rate would help the company to reduce the overall expenses and improve the

profitability margin of the business. It has been estimated that the AUD conversion rate slows

at reduced rate on the basis of the USD rate. However, in case of Chinese currency, Yuan, it

has been found that the reduced rate of Yuan is higher. The changes and the implementation

of conversion rate in the business would improve the overall performance of the business.

Free cash flow and Net dividend payout ratio forecasting:

Free cash flow is a crucial figure of finance which explains the total cash managed by

the company at a particular date. In order to forecast the free cash flow, the past figures of the

business have been measured and the profit margin of the business as a function of NOPAT

has been measured. Evaluation on the free cash flow forecasting is offers a decision base to

the management and other stakeholders of the business. The positive FCFF explains that the

company has enough funds to raise, run and manage the operations of the business whereas

the negative FCFF explains that the company has not enough funds to run the business and

thus it is depending on the stakeholders for the funds (Kaplan and Atkinson, 2015).

The forecasting application has been applied on the business to identify the overall

performance in near future. In order to evaluate the free cash flow of the business, NOA

position of the company has been improved at great extent because of the changes in the

operations and acquisitions. The company has improved the level of free cash flow in order to

meet the demands of the business. Because of the increment in the NOA, the returns of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business valuation and analysis 11

company have been improved as well the FCF level of the company represents about the

better cash management.

2019 2020 2021 2022 2023

Calculated FCFs (‘000) -15,436 56,362 94,186 41,638 40,577

Forecasted net dividend

payout 58.00% 58.00% 58.00% 58.00% 58.00%

(Statista, 2018)

On the basis of the estimated level of FCFF of the business, it has been found that the

main issues with FCF level of the business are dividend payout. The forecasting process

briefs about the dividend payout ratio of the company which would be 58%. In the year of

2019, it has been estimated that the FCF of the company would be lower because of the huge

impact on the sales level. From the historic dividend payout, it has been found that the free

cash flow of the company would be $ -15,436,000 in the year of 2019. But along with the

time and the changes into the sales turnover and credit policies of the business would

improve the overall free cash flow level of the business.

In the year of 2020, 2021, 2022 and 2023, it has been estimated that the cash level of

the business would be improved along with the same %. It has been estimated that in the year

of 2021, the free cash flow level of the business would at highest because of the demand of

the market and in order to manage the liquidity ratio of the business. The company is

managing the positive cash flow, in order to improve the liquidity position and maintain the

sudden demand of the stakeholders of the company.

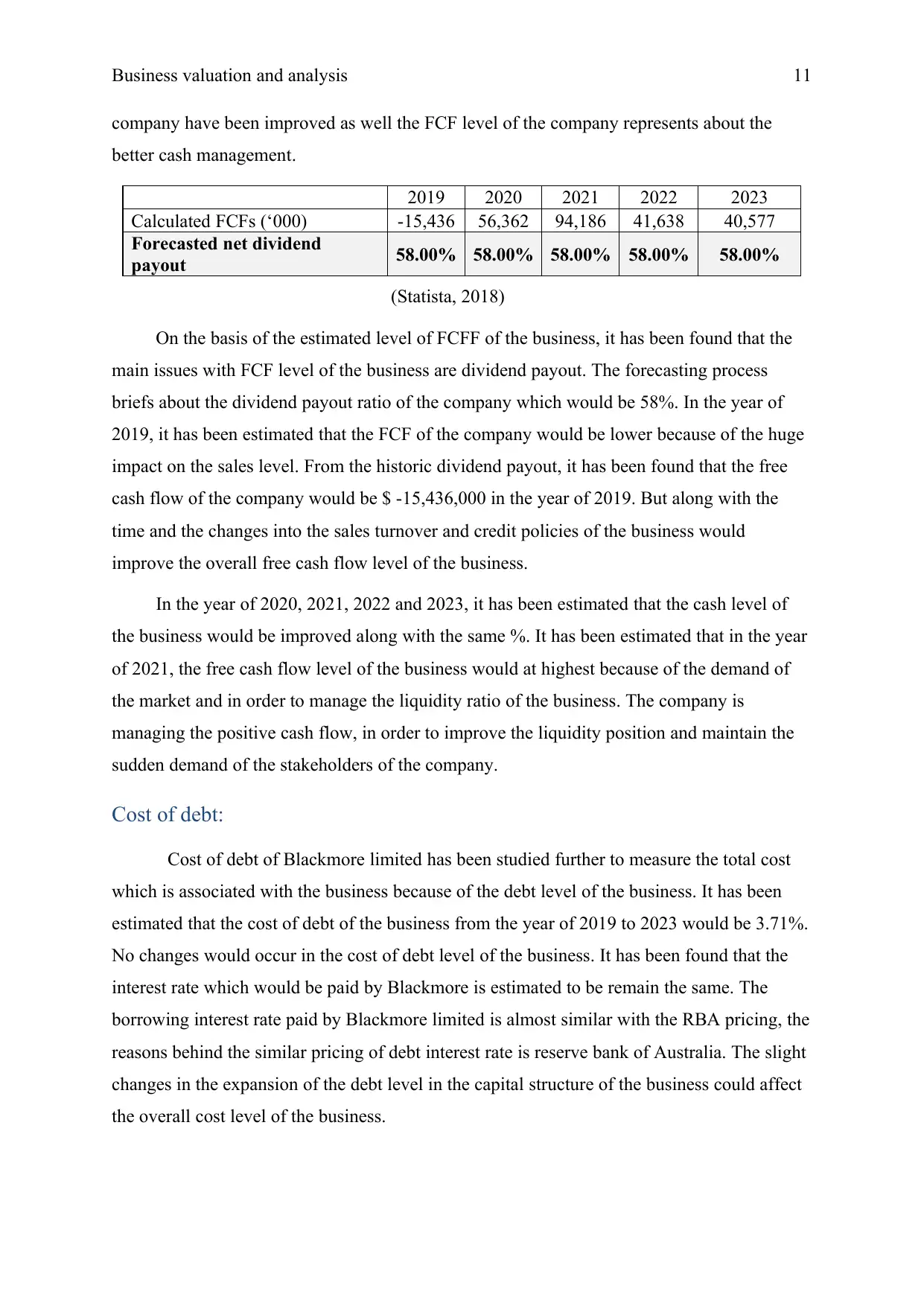

Cost of debt:

Cost of debt of Blackmore limited has been studied further to measure the total cost

which is associated with the business because of the debt level of the business. It has been

estimated that the cost of debt of the business from the year of 2019 to 2023 would be 3.71%.

No changes would occur in the cost of debt level of the business. It has been found that the

interest rate which would be paid by Blackmore is estimated to be remain the same. The

borrowing interest rate paid by Blackmore limited is almost similar with the RBA pricing, the

reasons behind the similar pricing of debt interest rate is reserve bank of Australia. The slight

changes in the expansion of the debt level in the capital structure of the business could affect

the overall cost level of the business.

company have been improved as well the FCF level of the company represents about the

better cash management.

2019 2020 2021 2022 2023

Calculated FCFs (‘000) -15,436 56,362 94,186 41,638 40,577

Forecasted net dividend

payout 58.00% 58.00% 58.00% 58.00% 58.00%

(Statista, 2018)

On the basis of the estimated level of FCFF of the business, it has been found that the

main issues with FCF level of the business are dividend payout. The forecasting process

briefs about the dividend payout ratio of the company which would be 58%. In the year of

2019, it has been estimated that the FCF of the company would be lower because of the huge

impact on the sales level. From the historic dividend payout, it has been found that the free

cash flow of the company would be $ -15,436,000 in the year of 2019. But along with the

time and the changes into the sales turnover and credit policies of the business would

improve the overall free cash flow level of the business.

In the year of 2020, 2021, 2022 and 2023, it has been estimated that the cash level of

the business would be improved along with the same %. It has been estimated that in the year

of 2021, the free cash flow level of the business would at highest because of the demand of

the market and in order to manage the liquidity ratio of the business. The company is

managing the positive cash flow, in order to improve the liquidity position and maintain the

sudden demand of the stakeholders of the company.

Cost of debt:

Cost of debt of Blackmore limited has been studied further to measure the total cost

which is associated with the business because of the debt level of the business. It has been

estimated that the cost of debt of the business from the year of 2019 to 2023 would be 3.71%.

No changes would occur in the cost of debt level of the business. It has been found that the

interest rate which would be paid by Blackmore is estimated to be remain the same. The

borrowing interest rate paid by Blackmore limited is almost similar with the RBA pricing, the

reasons behind the similar pricing of debt interest rate is reserve bank of Australia. The slight

changes in the expansion of the debt level in the capital structure of the business could affect

the overall cost level of the business.

Business valuation and analysis 12

2019 2020 2021 2022 2023

Forecasted cost of debt

after tax 3.77% 3.77% 3.77% 3.77% 3.77%

(Bloomberg, 2018)

It expresses that the level of the cost of the debt would be similar in all the next 5 years

and it would not affect the level of cost of debt of the company.

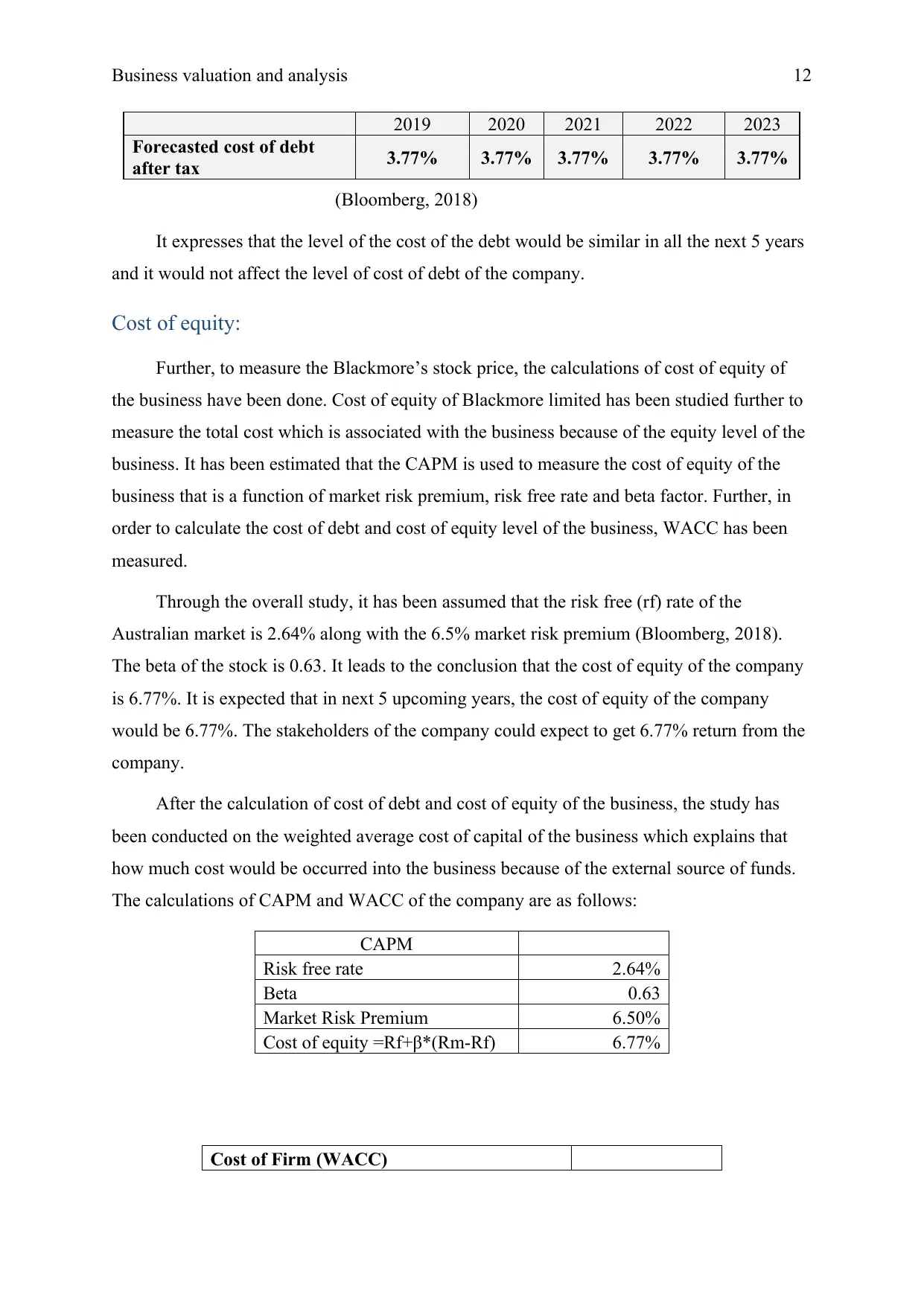

Cost of equity:

Further, to measure the Blackmore’s stock price, the calculations of cost of equity of

the business have been done. Cost of equity of Blackmore limited has been studied further to

measure the total cost which is associated with the business because of the equity level of the

business. It has been estimated that the CAPM is used to measure the cost of equity of the

business that is a function of market risk premium, risk free rate and beta factor. Further, in

order to calculate the cost of debt and cost of equity level of the business, WACC has been

measured.

Through the overall study, it has been assumed that the risk free (rf) rate of the

Australian market is 2.64% along with the 6.5% market risk premium (Bloomberg, 2018).

The beta of the stock is 0.63. It leads to the conclusion that the cost of equity of the company

is 6.77%. It is expected that in next 5 upcoming years, the cost of equity of the company

would be 6.77%. The stakeholders of the company could expect to get 6.77% return from the

company.

After the calculation of cost of debt and cost of equity of the business, the study has

been conducted on the weighted average cost of capital of the business which explains that

how much cost would be occurred into the business because of the external source of funds.

The calculations of CAPM and WACC of the company are as follows:

CAPM

Risk free rate 2.64%

Βeta 0.63

Market Risk Premium 6.50%

Cost of equity =Rf+β*(Rm-Rf) 6.77%

Cost of Firm (WACC)

2019 2020 2021 2022 2023

Forecasted cost of debt

after tax 3.77% 3.77% 3.77% 3.77% 3.77%

(Bloomberg, 2018)

It expresses that the level of the cost of the debt would be similar in all the next 5 years

and it would not affect the level of cost of debt of the company.

Cost of equity:

Further, to measure the Blackmore’s stock price, the calculations of cost of equity of

the business have been done. Cost of equity of Blackmore limited has been studied further to

measure the total cost which is associated with the business because of the equity level of the

business. It has been estimated that the CAPM is used to measure the cost of equity of the

business that is a function of market risk premium, risk free rate and beta factor. Further, in

order to calculate the cost of debt and cost of equity level of the business, WACC has been

measured.

Through the overall study, it has been assumed that the risk free (rf) rate of the

Australian market is 2.64% along with the 6.5% market risk premium (Bloomberg, 2018).

The beta of the stock is 0.63. It leads to the conclusion that the cost of equity of the company

is 6.77%. It is expected that in next 5 upcoming years, the cost of equity of the company

would be 6.77%. The stakeholders of the company could expect to get 6.77% return from the

company.

After the calculation of cost of debt and cost of equity of the business, the study has

been conducted on the weighted average cost of capital of the business which explains that

how much cost would be occurred into the business because of the external source of funds.

The calculations of CAPM and WACC of the company are as follows:

CAPM

Risk free rate 2.64%

Βeta 0.63

Market Risk Premium 6.50%

Cost of equity =Rf+β*(Rm-Rf) 6.77%

Cost of Firm (WACC)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.