Final Year Project: Blockchain and Cross-Border Payments Industry

VerifiedAdded on 2021/03/03

|43

|14347

|225

Project

AI Summary

This final year project investigates the transformative potential of blockchain technology within the cross-border payments industry. The research, conducted by Sameer Ahmed at Cass Business School, analyzes the inefficiencies of the current payment systems and explores how blockchain can offer a more viable and efficient solution. The project utilizes questionnaires to gather data from financial institutions that have adopted blockchain, providing insights into the technology's impact on speed, cost, and security. The findings suggest that blockchain is more efficient than existing technologies in the cross-border payments sector and is on track for mass adoption. The paper covers the current systems for cross-border payments, the role of blockchain, the adoption of blockchain in financial institutions, and provides recommendations for future researchers. It includes an introduction, literature review, research methodology, data analysis, and conclusion, offering a comprehensive overview of the topic.

Final Year Project

1

Blockchain and the Cross-Border Payments

Industry

Name: Sameer Ahmed

Supervisor: Dr Li Cunningham

"I certify that I have complied with the guidelines on plagiarism

outlined in the Course Handbook in the production of this dissertation and

that it is my own, unaided work".

Signature……………… …………………………………………………………………….

Cass Business School

BSc(Hons) in Business Management

Student ID: 160016163

1

Blockchain and the Cross-Border Payments

Industry

Name: Sameer Ahmed

Supervisor: Dr Li Cunningham

"I certify that I have complied with the guidelines on plagiarism

outlined in the Course Handbook in the production of this dissertation and

that it is my own, unaided work".

Signature……………… …………………………………………………………………….

Cass Business School

BSc(Hons) in Business Management

Student ID: 160016163

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Final Year Project

2

Acknowledgment

Firstly, I would like to thank Almighty God for providing me the strength and guidance to partake

and complete such an endeavor.

Next, I would like to acknowledge my supervisor Dr. Li Cunningham for her constant help and

support. This task would not have been possible without her guidance and efforts. Her constant

guidance kept me on track and helped me produce a well-rounded and well researched academic

paper.

I would also like to acknowledge my Parents. They have provided me constant support and

encouragement throughout the time line of this research paper.

Furthermore, I would like to thank my University, Cass Business School. The university has

provided me with an invaluable set of skills and experience that has greatly helped me in

completing this research paper.

Lastly, I would like to give credit to the banks and financial institutions that helped me in the

research for this paper. These institutions provided invaluable data without which this research

paper would not have been possible.

2

Acknowledgment

Firstly, I would like to thank Almighty God for providing me the strength and guidance to partake

and complete such an endeavor.

Next, I would like to acknowledge my supervisor Dr. Li Cunningham for her constant help and

support. This task would not have been possible without her guidance and efforts. Her constant

guidance kept me on track and helped me produce a well-rounded and well researched academic

paper.

I would also like to acknowledge my Parents. They have provided me constant support and

encouragement throughout the time line of this research paper.

Furthermore, I would like to thank my University, Cass Business School. The university has

provided me with an invaluable set of skills and experience that has greatly helped me in

completing this research paper.

Lastly, I would like to give credit to the banks and financial institutions that helped me in the

research for this paper. These institutions provided invaluable data without which this research

paper would not have been possible.

Final Year Project

3

Abstract

This research paper provides an insight into the concept of blockchain and how it is revolutionizing

the cross border payments industry. This research paper thus sets out to investigate whether a

disruptive technology like blockchain proves to be a more viable and efficient solution to the ever

growing issues faced by the payments industry. Blockchain technology has the potential to

revolutionize the payments industry. While people expect a lot from the technology, the real world

benefits are still not clear. However, the technology is undergoing mass adoption by major

companies because of which its benefits are becoming clearer day by day.

The research method used for this research paper is questionnaires. A number of people from

companies in the banking and finance industry that have adopted Blockchain were chosen to fill

out the questionnaires. This gave the researcher a good overall view about whether Blockchain has

helped or made improvements in the Cross border payments and settlements category.

After a thorough analysis of the authors research findings and an in-depth view of the existing

literature the author has concluded that blockchain technology is overall more efficient than

existing technology in the cross border payments sector and is on track to mass adoption.

3

Abstract

This research paper provides an insight into the concept of blockchain and how it is revolutionizing

the cross border payments industry. This research paper thus sets out to investigate whether a

disruptive technology like blockchain proves to be a more viable and efficient solution to the ever

growing issues faced by the payments industry. Blockchain technology has the potential to

revolutionize the payments industry. While people expect a lot from the technology, the real world

benefits are still not clear. However, the technology is undergoing mass adoption by major

companies because of which its benefits are becoming clearer day by day.

The research method used for this research paper is questionnaires. A number of people from

companies in the banking and finance industry that have adopted Blockchain were chosen to fill

out the questionnaires. This gave the researcher a good overall view about whether Blockchain has

helped or made improvements in the Cross border payments and settlements category.

After a thorough analysis of the authors research findings and an in-depth view of the existing

literature the author has concluded that blockchain technology is overall more efficient than

existing technology in the cross border payments sector and is on track to mass adoption.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Final Year Project

4

Table of Contents

1.0 Introduction..................................................................................................................... 5

2.0 Literature Review............................................................................................................. 8

2.1 The Cross Border Payments Industry .........................................................................................9

2.2 Problems with the current system .......................................................................................... 10

2.3 History of Blockchain .............................................................................................................. 11

2.4 Concept of Blockchain technology ........................................................................................... 12

2.5 Adoption of Blockchain in the Payments Industry .................................................................... 14

2.5a Adoption by Financial Bodies ............................................................................................. 16

2.5b Adoption in UK.................................................................................................................. 17

2.5c Adoption in China .............................................................................................................. 17

2.5d Adoption in America ......................................................................................................... 17

3.0 Methodology and Research Question ............................................................................. 18

3.1 Research Objectives ............................................................................................................... 19

3.2 Research Methodology ........................................................................................................... 19

3.3 Limitations ............................................................................................................................. 20

.3.4 Deductive research vs Inductive Research .............................................................................. 21

3.5 Pilot Study.............................................................................................................................. 21

3.6 Alternative Methods .............................................................................................................. 21

3.7 Research ........................................................................................................................ 22

3.7a Limitations ........................................................................................................................... 22

3.8 Sample........................................................................................................................... 23

3.9 Ethical Considerations ............................................................................................................ 25

4

Table of Contents

1.0 Introduction..................................................................................................................... 5

2.0 Literature Review............................................................................................................. 8

2.1 The Cross Border Payments Industry .........................................................................................9

2.2 Problems with the current system .......................................................................................... 10

2.3 History of Blockchain .............................................................................................................. 11

2.4 Concept of Blockchain technology ........................................................................................... 12

2.5 Adoption of Blockchain in the Payments Industry .................................................................... 14

2.5a Adoption by Financial Bodies ............................................................................................. 16

2.5b Adoption in UK.................................................................................................................. 17

2.5c Adoption in China .............................................................................................................. 17

2.5d Adoption in America ......................................................................................................... 17

3.0 Methodology and Research Question ............................................................................. 18

3.1 Research Objectives ............................................................................................................... 19

3.2 Research Methodology ........................................................................................................... 19

3.3 Limitations ............................................................................................................................. 20

.3.4 Deductive research vs Inductive Research .............................................................................. 21

3.5 Pilot Study.............................................................................................................................. 21

3.6 Alternative Methods .............................................................................................................. 21

3.7 Research ........................................................................................................................ 22

3.7a Limitations ........................................................................................................................... 22

3.8 Sample........................................................................................................................... 23

3.9 Ethical Considerations ............................................................................................................ 25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Final Year Project

5

4.0 Introduction to Data Analysis ......................................................................................... 25

4.1 Data Analysis.......................................................................................................................... 26

4.2 Data Analysis- Questionnaires ................................................................................................ 26

5.0 General Discussion ......................................................................................................... 33

6.0 Conclusion ..................................................................................................................... 34

6.1 Summary of Results ................................................................................................................ 34

6.2 Initial Objectives: ................................................................................................................... 35

6.3 Future of Blockchain: .............................................................................................................. 35

6.4 Implications: .......................................................................................................................... 36

6.5 Recommendations for future researchers: .............................................................................. 37

References .......................................................................................................................... 38

Appendix ............................................................................................................................. 41

5

4.0 Introduction to Data Analysis ......................................................................................... 25

4.1 Data Analysis.......................................................................................................................... 26

4.2 Data Analysis- Questionnaires ................................................................................................ 26

5.0 General Discussion ......................................................................................................... 33

6.0 Conclusion ..................................................................................................................... 34

6.1 Summary of Results ................................................................................................................ 34

6.2 Initial Objectives: ................................................................................................................... 35

6.3 Future of Blockchain: .............................................................................................................. 35

6.4 Implications: .......................................................................................................................... 36

6.5 Recommendations for future researchers: .............................................................................. 37

References .......................................................................................................................... 38

Appendix ............................................................................................................................. 41

Final Year Project

6

1.0 Introduction

Every industry goes through technological advancements and innovation. One such industry that

has not experienced major innovation is the payments industry. In today’s world of digitization,

cross border payments are still slow, costly and prone to security risks. Major companies have

been investigating distributed ledger technology for quite some time now. When Bitcoin emerged

in 2008, majority of people believed it would bring about a revolution in the financial world.

However, as time passed by, its weakness as a currency became apparent because of which the

focus shifted to its underlying technology, Blockchain. Blockchain is a disruptive technology that

is slowly taking over. Blockchain is revolutionizing processes in a number of industries. Its

technology can be applied to fields such as Data sharing, Digital IDs, Supply Chain, Payment

processing, etc. Also, Blockchain is viable for many industries such as auditing, gambling, and

authentication for events or luxury goods (Fanning & Centers, 2016).

One of the most notable areas where Blockchain technology is becoming the standard is the

gigantic payment’s industry. Experts predict that blockchain could save financial institutes at least

$20 billion annually in costs (Fanning & Centers, 2016). This makes further exploration into the

potential of Blockchain crucial for companies and governments alike.

This paper focuses on the application of blockchain in the cross border payments industry.

Blockchain in simplified terms is a distributed ledger in which the members taking part in the

network share transaction information between the parties.

The technology is a means of attaining a low cost way of sending payments that not only cuts

down the need for third party verification but also proves to be very secure. Thus, Blockchain is a

means of sending payments without the need for third party verification. Along with this

Blockchain technology results in only a fraction of the fees being charged as compared to the fees

charged by existing institutions using other technology. Blockchain aims to shift the world to a

cashless system. Today, trillions of dollars’ exchanges hands around the world via an antiquated

and outdated system of slow payments and added fees. The current system used for cross border

payments is ineffective, expensive and highly fragmented.

If a person employed in New York wants to send money to his family in London. He might have

to pay a $35 flat wire transfer fee. Moreover, he will be required to pay additional fees amounting

6

1.0 Introduction

Every industry goes through technological advancements and innovation. One such industry that

has not experienced major innovation is the payments industry. In today’s world of digitization,

cross border payments are still slow, costly and prone to security risks. Major companies have

been investigating distributed ledger technology for quite some time now. When Bitcoin emerged

in 2008, majority of people believed it would bring about a revolution in the financial world.

However, as time passed by, its weakness as a currency became apparent because of which the

focus shifted to its underlying technology, Blockchain. Blockchain is a disruptive technology that

is slowly taking over. Blockchain is revolutionizing processes in a number of industries. Its

technology can be applied to fields such as Data sharing, Digital IDs, Supply Chain, Payment

processing, etc. Also, Blockchain is viable for many industries such as auditing, gambling, and

authentication for events or luxury goods (Fanning & Centers, 2016).

One of the most notable areas where Blockchain technology is becoming the standard is the

gigantic payment’s industry. Experts predict that blockchain could save financial institutes at least

$20 billion annually in costs (Fanning & Centers, 2016). This makes further exploration into the

potential of Blockchain crucial for companies and governments alike.

This paper focuses on the application of blockchain in the cross border payments industry.

Blockchain in simplified terms is a distributed ledger in which the members taking part in the

network share transaction information between the parties.

The technology is a means of attaining a low cost way of sending payments that not only cuts

down the need for third party verification but also proves to be very secure. Thus, Blockchain is a

means of sending payments without the need for third party verification. Along with this

Blockchain technology results in only a fraction of the fees being charged as compared to the fees

charged by existing institutions using other technology. Blockchain aims to shift the world to a

cashless system. Today, trillions of dollars’ exchanges hands around the world via an antiquated

and outdated system of slow payments and added fees. The current system used for cross border

payments is ineffective, expensive and highly fragmented.

If a person employed in New York wants to send money to his family in London. He might have

to pay a $35 flat wire transfer fee. Moreover, he will be required to pay additional fees amounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Final Year Project

7

up to 7.4%. The bank chosen to transfer the money gets a cut, the person is also charged an

exchange fee. It will take the recipient bank several days to register the transaction. This way the

payments business proves to be very profitable for banks leaving them with no incentive to reduce

their fees.

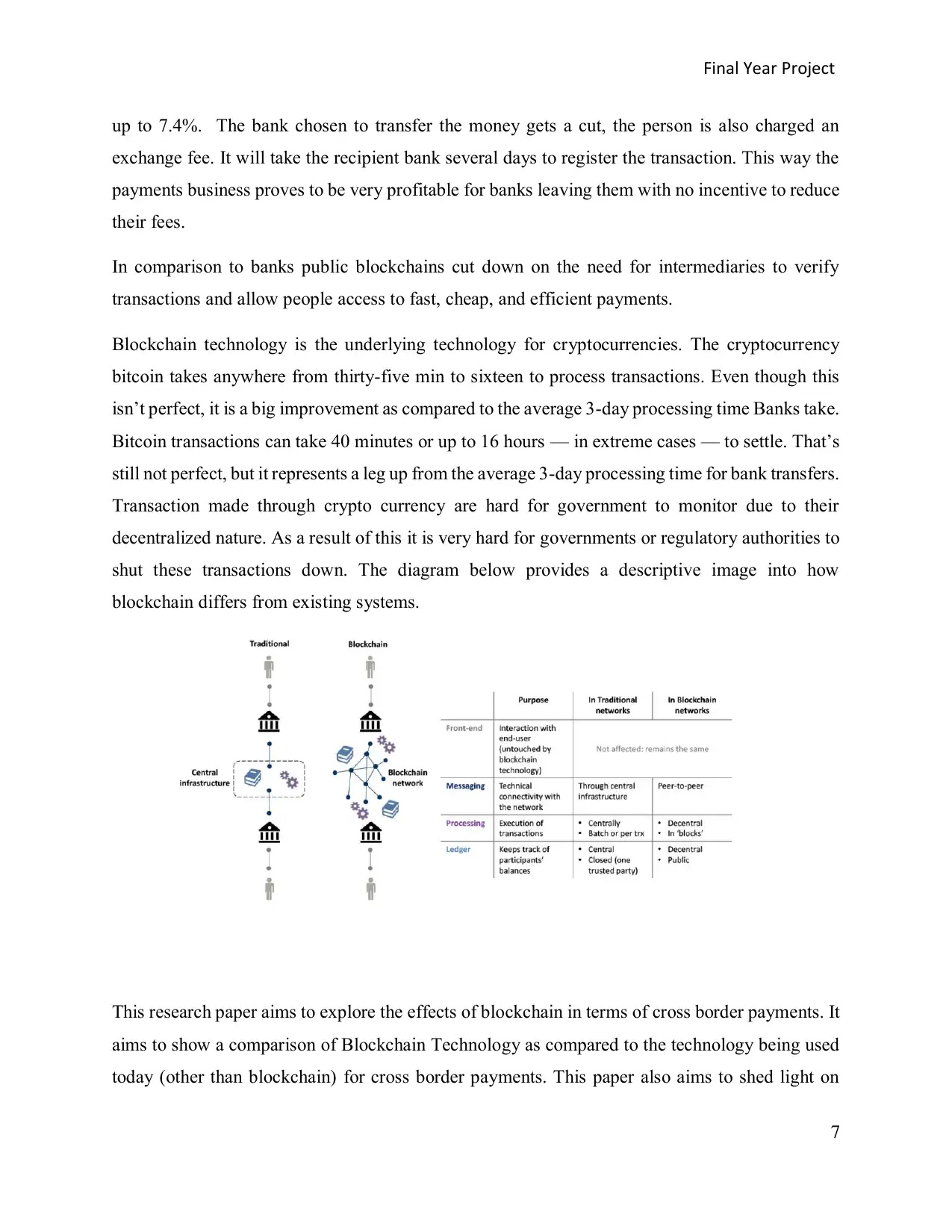

In comparison to banks public blockchains cut down on the need for intermediaries to verify

transactions and allow people access to fast, cheap, and efficient payments.

Blockchain technology is the underlying technology for cryptocurrencies. The cryptocurrency

bitcoin takes anywhere from thirty-five min to sixteen to process transactions. Even though this

isn’t perfect, it is a big improvement as compared to the average 3-day processing time Banks take.

Bitcoin transactions can take 40 minutes or up to 16 hours — in extreme cases — to settle. That’s

still not perfect, but it represents a leg up from the average 3-day processing time for bank transfers.

Transaction made through crypto currency are hard for government to monitor due to their

decentralized nature. As a result of this it is very hard for governments or regulatory authorities to

shut these transactions down. The diagram below provides a descriptive image into how

blockchain differs from existing systems.

This research paper aims to explore the effects of blockchain in terms of cross border payments. It

aims to show a comparison of Blockchain Technology as compared to the technology being used

today (other than blockchain) for cross border payments. This paper also aims to shed light on

7

up to 7.4%. The bank chosen to transfer the money gets a cut, the person is also charged an

exchange fee. It will take the recipient bank several days to register the transaction. This way the

payments business proves to be very profitable for banks leaving them with no incentive to reduce

their fees.

In comparison to banks public blockchains cut down on the need for intermediaries to verify

transactions and allow people access to fast, cheap, and efficient payments.

Blockchain technology is the underlying technology for cryptocurrencies. The cryptocurrency

bitcoin takes anywhere from thirty-five min to sixteen to process transactions. Even though this

isn’t perfect, it is a big improvement as compared to the average 3-day processing time Banks take.

Bitcoin transactions can take 40 minutes or up to 16 hours — in extreme cases — to settle. That’s

still not perfect, but it represents a leg up from the average 3-day processing time for bank transfers.

Transaction made through crypto currency are hard for government to monitor due to their

decentralized nature. As a result of this it is very hard for governments or regulatory authorities to

shut these transactions down. The diagram below provides a descriptive image into how

blockchain differs from existing systems.

This research paper aims to explore the effects of blockchain in terms of cross border payments. It

aims to show a comparison of Blockchain Technology as compared to the technology being used

today (other than blockchain) for cross border payments. This paper also aims to shed light on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Final Year Project

8

adoption of blockchain in financial institutions for cross border payments around the world. The

following points have been covered in this dissertation:

- The current systems for cross border payments and its inherent issues

- The role of blockchain in cross border payments

- Wether or not Blockchain technology is helping revoloutionize the Cross Border

Payments Industry

- An analysis based on findings collected through primary research from a hundred

particpants belonging to nine large scale financial institutions

- A brief look into the future of blockchain

This dissertation has been sanctioned into four parts, mainly the ‘Introduction’, ‘Literature

Review’, ‘Research methodology’ and ‘Data Analysis’. Recommendations and implications of the

research has also been added after the conclusion. While introduction defines the concept of

Blockchain, the literature review gives a comprehensive look at the History, concept and adoption

of Blockchain technology. The research methodology explains a step by step approach taken by

the author to conduct primary research for this dissertation. The data anlysis provides an indepth

research and discussion based on the findings of the primary research conducted. Lastly, the

conclusion overall view of the findings and the results that have been achieved after analysing the

findings.

2.0 Literature Review

This section provides an in-depth look into the available literature on blockchain and the payments

industry. This section will shed some light onto the existing literature found on the payments

industry and the current systems used for cross border payments. The section follows a step by

step procedure in explaining the cross border payment industry, issues with the current system, the

history of blockchain, the concept of blockchain and adoption of blockchain technology.

8

adoption of blockchain in financial institutions for cross border payments around the world. The

following points have been covered in this dissertation:

- The current systems for cross border payments and its inherent issues

- The role of blockchain in cross border payments

- Wether or not Blockchain technology is helping revoloutionize the Cross Border

Payments Industry

- An analysis based on findings collected through primary research from a hundred

particpants belonging to nine large scale financial institutions

- A brief look into the future of blockchain

This dissertation has been sanctioned into four parts, mainly the ‘Introduction’, ‘Literature

Review’, ‘Research methodology’ and ‘Data Analysis’. Recommendations and implications of the

research has also been added after the conclusion. While introduction defines the concept of

Blockchain, the literature review gives a comprehensive look at the History, concept and adoption

of Blockchain technology. The research methodology explains a step by step approach taken by

the author to conduct primary research for this dissertation. The data anlysis provides an indepth

research and discussion based on the findings of the primary research conducted. Lastly, the

conclusion overall view of the findings and the results that have been achieved after analysing the

findings.

2.0 Literature Review

This section provides an in-depth look into the available literature on blockchain and the payments

industry. This section will shed some light onto the existing literature found on the payments

industry and the current systems used for cross border payments. The section follows a step by

step procedure in explaining the cross border payment industry, issues with the current system, the

history of blockchain, the concept of blockchain and adoption of blockchain technology.

Final Year Project

9

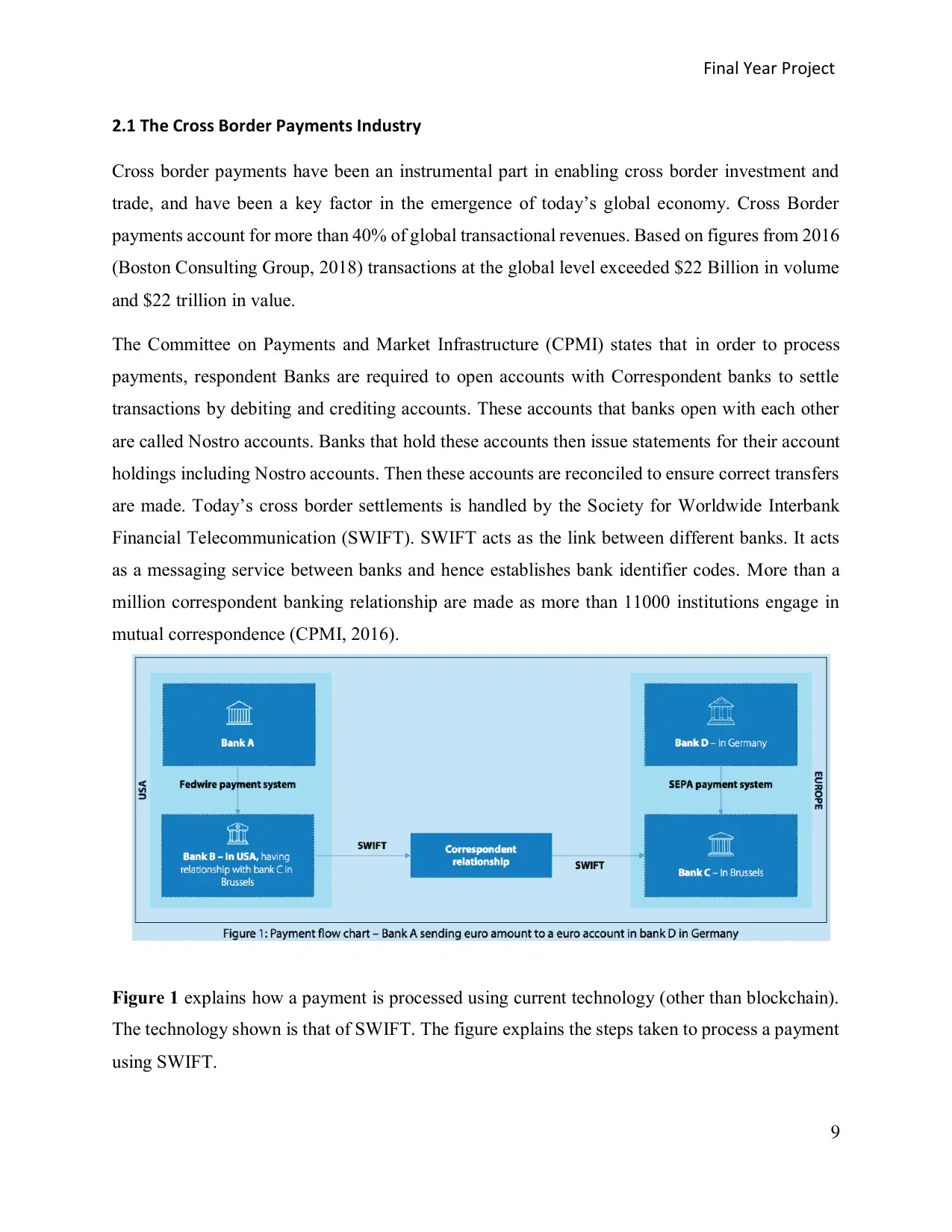

2.1 The Cross Border Payments Industry

Cross border payments have been an instrumental part in enabling cross border investment and

trade, and have been a key factor in the emergence of today’s global economy. Cross Border

payments account for more than 40% of global transactional revenues. Based on figures from 2016

(Boston Consulting Group, 2018) transactions at the global level exceeded $22 Billion in volume

and $22 trillion in value.

The Committee on Payments and Market Infrastructure (CPMI) states that in order to process

payments, respondent Banks are required to open accounts with Correspondent banks to settle

transactions by debiting and crediting accounts. These accounts that banks open with each other

are called Nostro accounts. Banks that hold these accounts then issue statements for their account

holdings including Nostro accounts. Then these accounts are reconciled to ensure correct transfers

are made. Today’s cross border settlements is handled by the Society for Worldwide Interbank

Financial Telecommunication (SWIFT). SWIFT acts as the link between different banks. It acts

as a messaging service between banks and hence establishes bank identifier codes. More than a

million correspondent banking relationship are made as more than 11000 institutions engage in

mutual correspondence (CPMI, 2016).

Figure 1 explains how a payment is processed using current technology (other than blockchain).

The technology shown is that of SWIFT. The figure explains the steps taken to process a payment

using SWIFT.

9

2.1 The Cross Border Payments Industry

Cross border payments have been an instrumental part in enabling cross border investment and

trade, and have been a key factor in the emergence of today’s global economy. Cross Border

payments account for more than 40% of global transactional revenues. Based on figures from 2016

(Boston Consulting Group, 2018) transactions at the global level exceeded $22 Billion in volume

and $22 trillion in value.

The Committee on Payments and Market Infrastructure (CPMI) states that in order to process

payments, respondent Banks are required to open accounts with Correspondent banks to settle

transactions by debiting and crediting accounts. These accounts that banks open with each other

are called Nostro accounts. Banks that hold these accounts then issue statements for their account

holdings including Nostro accounts. Then these accounts are reconciled to ensure correct transfers

are made. Today’s cross border settlements is handled by the Society for Worldwide Interbank

Financial Telecommunication (SWIFT). SWIFT acts as the link between different banks. It acts

as a messaging service between banks and hence establishes bank identifier codes. More than a

million correspondent banking relationship are made as more than 11000 institutions engage in

mutual correspondence (CPMI, 2016).

Figure 1 explains how a payment is processed using current technology (other than blockchain).

The technology shown is that of SWIFT. The figure explains the steps taken to process a payment

using SWIFT.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Final Year Project

10

2.2 Problems with the current system

The current system is full of inefficiencies and flaws which makes way for disruptive technologies

and innovations to come in. Due to these inherent flaws in the system institutions and governments

are trying to find alternative methods to improve the efficiency of their cross border transactions.

Blockchain technology does not encounter these problems and therefore provides increased

efficiency and on demand liquidity in cross border payments. Some of the main flaws are as

follows:

• Need for Intermediary Authority:

A big hurdle for the industry, as well as for regulators, is the sustained decrease in

correspondent banking relationships which result in lengthening of payment chains and

increasing reliance on fewer correspondent banks (FSB, 2017). Due to tightening

regulatory requirements (AML and CTF) by key jurisdictions, such as the Europe and

US, 75% of global bank providers have reduced their correspondent banking

relationships (IMF, 2017) or left this business altogether.

• High Costs: High costs are a huge problem for the current payment processing system.

This rises due to multiple banks being involved, each charging a fees. In a report by

Mckinsey&company mentioned that the average cost of a transaction amounts to $25-

30. These high costs are a major problem for companies settling billions of dollars in

payments across borders.

• Long settlement times: According to a survey, 64% of treasurers stated that they

prefer real-time payments tracking, while 42% were in favor of instant payments.

Blockchain is able to provide both of these qualities through the use of Distributed

Ledgre Technology (DLT).

• Security issues: Due to the considerable number of intermediaries involved the

chances of fraud or a hack increase. Just in 2016, the world’s biggest payment settler

Swift, experienced a mass scale hack in its system.

10

2.2 Problems with the current system

The current system is full of inefficiencies and flaws which makes way for disruptive technologies

and innovations to come in. Due to these inherent flaws in the system institutions and governments

are trying to find alternative methods to improve the efficiency of their cross border transactions.

Blockchain technology does not encounter these problems and therefore provides increased

efficiency and on demand liquidity in cross border payments. Some of the main flaws are as

follows:

• Need for Intermediary Authority:

A big hurdle for the industry, as well as for regulators, is the sustained decrease in

correspondent banking relationships which result in lengthening of payment chains and

increasing reliance on fewer correspondent banks (FSB, 2017). Due to tightening

regulatory requirements (AML and CTF) by key jurisdictions, such as the Europe and

US, 75% of global bank providers have reduced their correspondent banking

relationships (IMF, 2017) or left this business altogether.

• High Costs: High costs are a huge problem for the current payment processing system.

This rises due to multiple banks being involved, each charging a fees. In a report by

Mckinsey&company mentioned that the average cost of a transaction amounts to $25-

30. These high costs are a major problem for companies settling billions of dollars in

payments across borders.

• Long settlement times: According to a survey, 64% of treasurers stated that they

prefer real-time payments tracking, while 42% were in favor of instant payments.

Blockchain is able to provide both of these qualities through the use of Distributed

Ledgre Technology (DLT).

• Security issues: Due to the considerable number of intermediaries involved the

chances of fraud or a hack increase. Just in 2016, the world’s biggest payment settler

Swift, experienced a mass scale hack in its system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Final Year Project

11

2.3 History of Blockchain

Milton Friedman, a Nobel prize winning economist (1999) said,

“the one thing that’s missing is a reliable e-cash, whereby on the internet you can transfer funds from

A to B without A knowing B or B knowing A”.

Digital payments are similar to payments processed through digital means, for example, the

transactions between a cash register and an electronic wallet or through digital money. (Staykova,

K.S., and Dalsgaard, J, 2015). The Cryptographic Mailing List published a report titled, “Bitcoin:

A Peer-to-Peer Electronic Cash System”. The report focuses mainly on a digital currency that does

not require the use of a mediator or a third party. This is evident from the beginning sentence of

the document: “A purely peer-to-peer version of electronic cash would allow online payments to

be sent directly from one party to another without going through a financial institution”

(Nakamoto, 2008).

However, this was not the first time in history that digital payments were mentioned, as in 1970

David Chaum in two publications introduced the concept of a digital currency. After the report a

small amount of institutions made several attempts to introduce digital currencies like e-gold and

e-cash. (Frisby, 2014).

Nakamoto (2008) introduced Blockchain technology was mainly to bypass intermediaries or third

partys such as financial institutions by allowing the participants to conduct peer-to-peer

transactions directly. To accomplish this, Nakamoto developed a peer-to-peer distributed ledger.

By using this distributed ledger, the payee and the payer can exchange and correspond directly

over the network, using consensus mechanisms and encryption (Guo & Liang, 2016; Tsai, Blower,

Zhu, & Yu, 2016; Zhu & Zhou, 2016) to render these transactions to be immune to tampering as

any change to the historical data record is traceable and detectable by the blockchain network

nodes that are participating (B. Lee & Lee, 2017; Tapscott & Tapscott, 2017). The transactions

based on the distributed ledger allow for transaction to be processed quickly and seamlessly, while

also minimizing the potential drawbacks of a trust based model.

11

2.3 History of Blockchain

Milton Friedman, a Nobel prize winning economist (1999) said,

“the one thing that’s missing is a reliable e-cash, whereby on the internet you can transfer funds from

A to B without A knowing B or B knowing A”.

Digital payments are similar to payments processed through digital means, for example, the

transactions between a cash register and an electronic wallet or through digital money. (Staykova,

K.S., and Dalsgaard, J, 2015). The Cryptographic Mailing List published a report titled, “Bitcoin:

A Peer-to-Peer Electronic Cash System”. The report focuses mainly on a digital currency that does

not require the use of a mediator or a third party. This is evident from the beginning sentence of

the document: “A purely peer-to-peer version of electronic cash would allow online payments to

be sent directly from one party to another without going through a financial institution”

(Nakamoto, 2008).

However, this was not the first time in history that digital payments were mentioned, as in 1970

David Chaum in two publications introduced the concept of a digital currency. After the report a

small amount of institutions made several attempts to introduce digital currencies like e-gold and

e-cash. (Frisby, 2014).

Nakamoto (2008) introduced Blockchain technology was mainly to bypass intermediaries or third

partys such as financial institutions by allowing the participants to conduct peer-to-peer

transactions directly. To accomplish this, Nakamoto developed a peer-to-peer distributed ledger.

By using this distributed ledger, the payee and the payer can exchange and correspond directly

over the network, using consensus mechanisms and encryption (Guo & Liang, 2016; Tsai, Blower,

Zhu, & Yu, 2016; Zhu & Zhou, 2016) to render these transactions to be immune to tampering as

any change to the historical data record is traceable and detectable by the blockchain network

nodes that are participating (B. Lee & Lee, 2017; Tapscott & Tapscott, 2017). The transactions

based on the distributed ledger allow for transaction to be processed quickly and seamlessly, while

also minimizing the potential drawbacks of a trust based model.

Final Year Project

12

2.4 Concept of Blockchain technology

In layman’s terms, blockchain is a trusted, public and shared ledger (The Economist, 2016b), on a

peer-to-peer network which implies that it is run by thousands of participants, however, no one

controls it (The Economist, 2015). This makes blockchain different from existing technologies as

it acts as a shared ledger. As the blockchain is available to all the participants, it makes it public in

nature (The Economist, 2016b). Blockchain acts as a truly trusted ledger as the information that is

processed through blockchain is tamperproof as the system will quickly be able to detect if anyone

attempts to tamper with it (The Economist, 2015). These characteristics allow blockchain to

process huge amounts of information without any third party or middleman in between. For

example, assume Jordan transfers $10 to Linda. The network in the blockchain is aware of Linda’s

ownership of $10 as the transaction is distributed to each participant. While Linda will be able to

transfer $10 or less to another party, the network will automatically reject a proposal to transfer

$12 as it is more than what Linda owns.

A trusted entity records all holdings and transactions when it comes to centralized networks; only

through this can participants reach an agreement/consensus on relevant facts, in particular the

participants holdings (McAfee, 2014). In many countries, security accounts for all the market

participants that invest in securities is maintained by a central security depository. All disposition

and acquisitions that take place are recorder in that register and each balance recorded is retrievable

(J Lollike & N. & Malone, S, 2016). Decentralized networks operate in a way that different records

together provide information on holdings and transactions. The comprehensive information is not

held by any single record. For instance, in some jurisdictions, transactions and holdings of end

investors are not recorder rather holdings of bankers and brokers are. The assumption is that these

banks to and brokers will make entries in their own ledger according identity of investors to whom

the securities belong to.

“As a solution for currency, blockchain is essential. As a solution to sharing information across

disparate parties, blockchain is truly revolutionary” (Price, 2017). It is crucial to understand that

payments done through blockchain are settled almost instantly. The key reason for this is that there

is no financial intermediary. This not only reduces settlement times by a huge margin rather also

result in minimal fees. This is because in a transaction carried out by using blockchain technology

there network management, nostro-vostro liquidity, compliance or FX costs.

12

2.4 Concept of Blockchain technology

In layman’s terms, blockchain is a trusted, public and shared ledger (The Economist, 2016b), on a

peer-to-peer network which implies that it is run by thousands of participants, however, no one

controls it (The Economist, 2015). This makes blockchain different from existing technologies as

it acts as a shared ledger. As the blockchain is available to all the participants, it makes it public in

nature (The Economist, 2016b). Blockchain acts as a truly trusted ledger as the information that is

processed through blockchain is tamperproof as the system will quickly be able to detect if anyone

attempts to tamper with it (The Economist, 2015). These characteristics allow blockchain to

process huge amounts of information without any third party or middleman in between. For

example, assume Jordan transfers $10 to Linda. The network in the blockchain is aware of Linda’s

ownership of $10 as the transaction is distributed to each participant. While Linda will be able to

transfer $10 or less to another party, the network will automatically reject a proposal to transfer

$12 as it is more than what Linda owns.

A trusted entity records all holdings and transactions when it comes to centralized networks; only

through this can participants reach an agreement/consensus on relevant facts, in particular the

participants holdings (McAfee, 2014). In many countries, security accounts for all the market

participants that invest in securities is maintained by a central security depository. All disposition

and acquisitions that take place are recorder in that register and each balance recorded is retrievable

(J Lollike & N. & Malone, S, 2016). Decentralized networks operate in a way that different records

together provide information on holdings and transactions. The comprehensive information is not

held by any single record. For instance, in some jurisdictions, transactions and holdings of end

investors are not recorder rather holdings of bankers and brokers are. The assumption is that these

banks to and brokers will make entries in their own ledger according identity of investors to whom

the securities belong to.

“As a solution for currency, blockchain is essential. As a solution to sharing information across

disparate parties, blockchain is truly revolutionary” (Price, 2017). It is crucial to understand that

payments done through blockchain are settled almost instantly. The key reason for this is that there

is no financial intermediary. This not only reduces settlement times by a huge margin rather also

result in minimal fees. This is because in a transaction carried out by using blockchain technology

there network management, nostro-vostro liquidity, compliance or FX costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 43

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.