Bluescope Steel Limited: Auditing and Ethics Report Analysis, 2018

VerifiedAdded on 2023/02/01

|9

|2893

|54

Report

AI Summary

This report provides a comprehensive analysis of the auditing and ethics of Bluescope Steel Limited. It begins with background information on the company, followed by a discussion and analysis of key areas, including the quantification of materiality levels based on financial data. The report reviews notes and disclosures from the company's annual accounts and performs an analytical review using ratio analysis, assessing liquidity, profitability, solvency, and efficiency ratios. It also examines relevant audit assertions and procedures. Furthermore, the report analyzes the company's cash flow statement, identifying major contributors to cash flow, and reviews the audit report issued by Ernst & Young, highlighting critical audit matters. The analysis covers the period ending June 30, 2018, and is presented in a report format, fulfilling the requirements of an auditing and ethics assignment for CQUniversity Australia.

Student’s Name

UNIVERSITY NAME Australia

AUDITING AND ETHICS IN

AUSTRALIA

UNIVERSITY NAME Australia

AUDITING AND ETHICS IN

AUSTRALIA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Background..................................................................................................................................................2

Discussion and Analysis...............................................................................................................................3

Introduction to the company...................................................................................................................3

Section 1: Quantification of Materiality Level.........................................................................................3

Review of draft notes and disclosures.....................................................................................................3

Section 2: Analytical Review, Assertions and Audit procedures..............................................................4

Assertions and the audit procedures.......................................................................................................5

Section 3: Cash flow analysis...................................................................................................................5

Analysis of Audit report of the company.................................................................................................6

Conclusion...................................................................................................................................................7

References...................................................................................................................................................7

Background..................................................................................................................................................2

Discussion and Analysis...............................................................................................................................3

Introduction to the company...................................................................................................................3

Section 1: Quantification of Materiality Level.........................................................................................3

Review of draft notes and disclosures.....................................................................................................3

Section 2: Analytical Review, Assertions and Audit procedures..............................................................4

Assertions and the audit procedures.......................................................................................................5

Section 3: Cash flow analysis...................................................................................................................5

Analysis of Audit report of the company.................................................................................................6

Conclusion...................................................................................................................................................7

References...................................................................................................................................................7

Background

The financial analysis has been done for one of the reputed companies in Australia named Bluescope

Steel Limited Company. The report was made with the purpose of aiding the audit of company and

materiality has been calculated to help the auditor ascertain the significant accounts using the

quantitative estimate of the materiality. The notes and the disclosures shown in the annual accounts of

the company have also been studied to check the critical issues from perspective of audit. Furthermore

the analytical review was being performed using the ratio analysis of the company and the trend and

variance was analyzed for last 4 years. The relevant audit assertions together with the audit procedures

to be applied were also recommended. Towards the end, the cash flow statement of the company has

been analyzed to find the major and least contributor to the cash flow of the company and also the

audit report was reviewed to check if there are any critical accounts that have been highlighted.

The financial analysis has been done for one of the reputed companies in Australia named Bluescope

Steel Limited Company. The report was made with the purpose of aiding the audit of company and

materiality has been calculated to help the auditor ascertain the significant accounts using the

quantitative estimate of the materiality. The notes and the disclosures shown in the annual accounts of

the company have also been studied to check the critical issues from perspective of audit. Furthermore

the analytical review was being performed using the ratio analysis of the company and the trend and

variance was analyzed for last 4 years. The relevant audit assertions together with the audit procedures

to be applied were also recommended. Towards the end, the cash flow statement of the company has

been analyzed to find the major and least contributor to the cash flow of the company and also the

audit report was reviewed to check if there are any critical accounts that have been highlighted.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

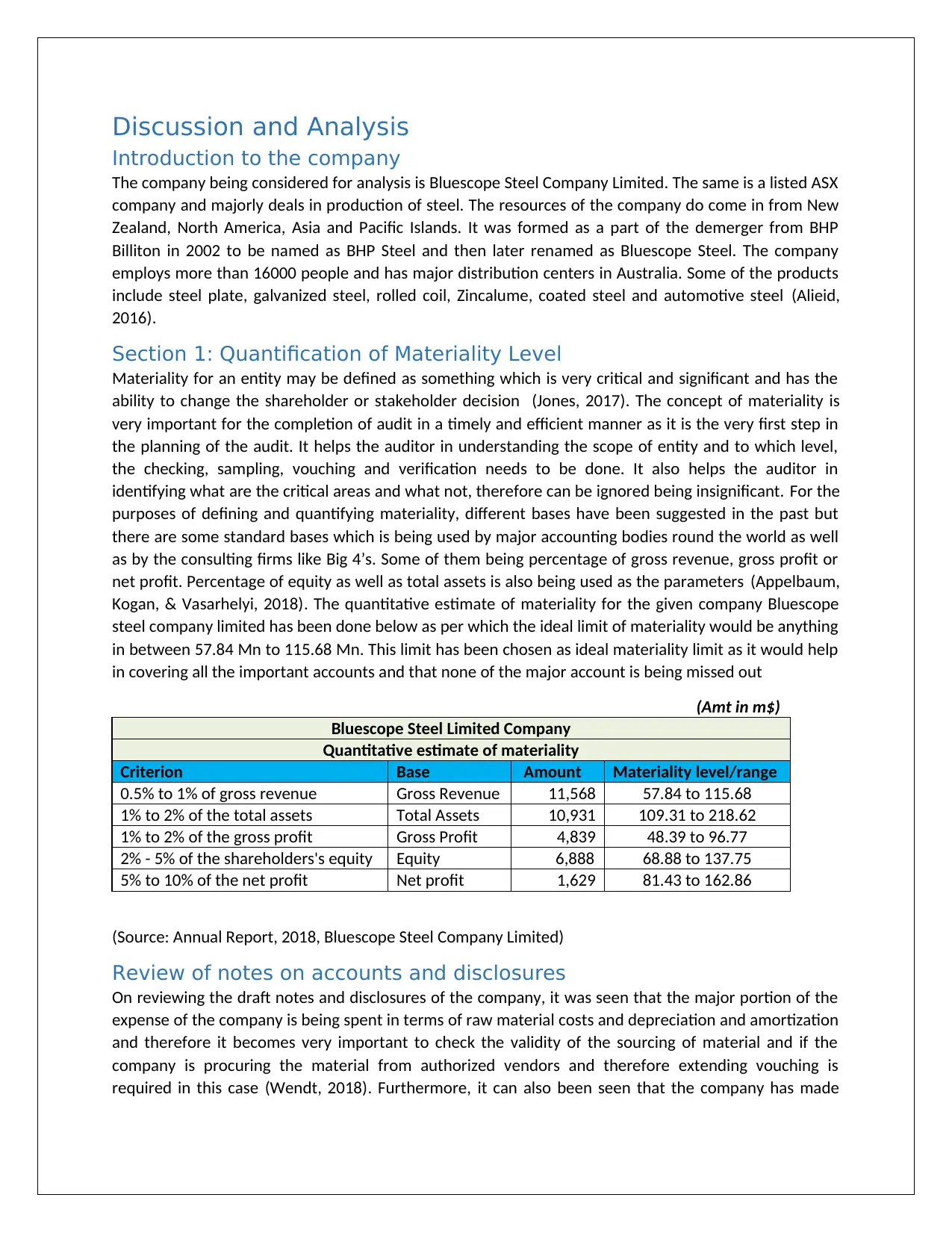

Discussion and Analysis

Introduction to the company

The company being considered for analysis is Bluescope Steel Company Limited. The same is a listed ASX

company and majorly deals in production of steel. The resources of the company do come in from New

Zealand, North America, Asia and Pacific Islands. It was formed as a part of the demerger from BHP

Billiton in 2002 to be named as BHP Steel and then later renamed as Bluescope Steel. The company

employs more than 16000 people and has major distribution centers in Australia. Some of the products

include steel plate, galvanized steel, rolled coil, Zincalume, coated steel and automotive steel (Alieid,

2016).

Section 1: Quantification of Materiality Level

Materiality for an entity may be defined as something which is very critical and significant and has the

ability to change the shareholder or stakeholder decision (Jones, 2017). The concept of materiality is

very important for the completion of audit in a timely and efficient manner as it is the very first step in

the planning of the audit. It helps the auditor in understanding the scope of entity and to which level,

the checking, sampling, vouching and verification needs to be done. It also helps the auditor in

identifying what are the critical areas and what not, therefore can be ignored being insignificant. For the

purposes of defining and quantifying materiality, different bases have been suggested in the past but

there are some standard bases which is being used by major accounting bodies round the world as well

as by the consulting firms like Big 4’s. Some of them being percentage of gross revenue, gross profit or

net profit. Percentage of equity as well as total assets is also being used as the parameters (Appelbaum,

Kogan, & Vasarhelyi, 2018). The quantitative estimate of materiality for the given company Bluescope

steel company limited has been done below as per which the ideal limit of materiality would be anything

in between 57.84 Mn to 115.68 Mn. This limit has been chosen as ideal materiality limit as it would help

in covering all the important accounts and that none of the major account is being missed out

(Amt in m$)

Bluescope Steel Limited Company

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 11,568 57.84 to 115.68

1% to 2% of the total assets Total Assets 10,931 109.31 to 218.62

1% to 2% of the gross profit Gross Profit 4,839 48.39 to 96.77

2% - 5% of the shareholders's equity Equity 6,888 68.88 to 137.75

5% to 10% of the net profit Net profit 1,629 81.43 to 162.86

(Source: Annual Report, 2018, Bluescope Steel Company Limited)

Review of notes on accounts and disclosures

On reviewing the draft notes and disclosures of the company, it was seen that the major portion of the

expense of the company is being spent in terms of raw material costs and depreciation and amortization

and therefore it becomes very important to check the validity of the sourcing of material and if the

company is procuring the material from authorized vendors and therefore extending vouching is

required in this case (Wendt, 2018). Furthermore, it can also been seen that the company has made

Introduction to the company

The company being considered for analysis is Bluescope Steel Company Limited. The same is a listed ASX

company and majorly deals in production of steel. The resources of the company do come in from New

Zealand, North America, Asia and Pacific Islands. It was formed as a part of the demerger from BHP

Billiton in 2002 to be named as BHP Steel and then later renamed as Bluescope Steel. The company

employs more than 16000 people and has major distribution centers in Australia. Some of the products

include steel plate, galvanized steel, rolled coil, Zincalume, coated steel and automotive steel (Alieid,

2016).

Section 1: Quantification of Materiality Level

Materiality for an entity may be defined as something which is very critical and significant and has the

ability to change the shareholder or stakeholder decision (Jones, 2017). The concept of materiality is

very important for the completion of audit in a timely and efficient manner as it is the very first step in

the planning of the audit. It helps the auditor in understanding the scope of entity and to which level,

the checking, sampling, vouching and verification needs to be done. It also helps the auditor in

identifying what are the critical areas and what not, therefore can be ignored being insignificant. For the

purposes of defining and quantifying materiality, different bases have been suggested in the past but

there are some standard bases which is being used by major accounting bodies round the world as well

as by the consulting firms like Big 4’s. Some of them being percentage of gross revenue, gross profit or

net profit. Percentage of equity as well as total assets is also being used as the parameters (Appelbaum,

Kogan, & Vasarhelyi, 2018). The quantitative estimate of materiality for the given company Bluescope

steel company limited has been done below as per which the ideal limit of materiality would be anything

in between 57.84 Mn to 115.68 Mn. This limit has been chosen as ideal materiality limit as it would help

in covering all the important accounts and that none of the major account is being missed out

(Amt in m$)

Bluescope Steel Limited Company

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 11,568 57.84 to 115.68

1% to 2% of the total assets Total Assets 10,931 109.31 to 218.62

1% to 2% of the gross profit Gross Profit 4,839 48.39 to 96.77

2% - 5% of the shareholders's equity Equity 6,888 68.88 to 137.75

5% to 10% of the net profit Net profit 1,629 81.43 to 162.86

(Source: Annual Report, 2018, Bluescope Steel Company Limited)

Review of notes on accounts and disclosures

On reviewing the draft notes and disclosures of the company, it was seen that the major portion of the

expense of the company is being spent in terms of raw material costs and depreciation and amortization

and therefore it becomes very important to check the validity of the sourcing of material and if the

company is procuring the material from authorized vendors and therefore extending vouching is

required in this case (Wendt, 2018). Furthermore, it can also been seen that the company has made

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

substantial addition to the current assets like inventory and cash balance as well as in PPE and in order

to validate the same, verification of the items is critical to audit. The auditor also needs to check into the

provisions for its completeness like in case of receivables, payables, restructuring costs, product claims,

worker’s compensation, carbon emissions, etc. The auditors also needs to look into the valuation of

goodwill and its impairment considering the significant movements over the year (Gooley, 2016). The

company has also disclosed a couple of contingent liabilities like that of liability on account of failure to

sale NZIS, guarantees given by the company for worker’s compensation, regulatory and taxation

contingencies and the prior year contingent liability on account of legal proceeding by South32 against

Bluescope Steel. All these contingencies needs to be reviewed extensively to check if any of them has

been materialized (Oberoi, 2018).

Section 2: Analytical Review, Assertions and Audit procedures

The analytical review of the company has been shown below. The same has been done using key ratios

for the years 2015 to 2018.

Bluescope Steel Company Limited > Ratios Analysis

Name of the ratio Formulas 2018 2017 2016 2015

Part A: Liquidity Ratios

Current Ratio or Working

Capital Ratio Current Assets / Current Liabilities 1.72 1.58 1.40 1.59

Quick ratio or Acid test ratio (Current Assets - Inventory) / Current

Liabilities 0.98 0.90 0.79 0.84

Cash flow Ratio Net cash flow from operating activities /

Current Liabilities 0.44 0.46 0.42 0.27

Name of the ratio Formulas 2018 2017 2016 2015

Part B: Profitability Ratios

Return on Equity Profit available to owners / Average

Equity *100

23.65

% 13.97% 8.35% 3.74%

Return on Assets Profit (loss) / Average total assets *100 14.90

% 8.08% 4.55% 2.25%

Gross Profit Margin Gross Profit / Sales Revenue *100 41.98

% 43.93% 45.52

% 43.36%

Profit Margin Profit (loss) / Sales Revenue *100 14.13

% 7.33% 4.52% 2.07%

Cash Flow to Sales Cash Flow from operating activities /

Sales Revenue *100 9.90% 10.73% 10.34

% 6.31%

Name of the ratio Formulas 2018 2017 2016 2015

Part C: Solvency Ratios

Debt Equity Ratio Debt/Equity 0.59 0.73 0.84 0.66

Debt to Asset Ratio Debt/Total Assets 0.37 0.42 0.46 0.40

Interest Service coverage

ratio EBIT/Interest cost 13.32 11.46 5.75 3.89

Name of the ratio Formulas 2018 2017 2016 2015

to validate the same, verification of the items is critical to audit. The auditor also needs to check into the

provisions for its completeness like in case of receivables, payables, restructuring costs, product claims,

worker’s compensation, carbon emissions, etc. The auditors also needs to look into the valuation of

goodwill and its impairment considering the significant movements over the year (Gooley, 2016). The

company has also disclosed a couple of contingent liabilities like that of liability on account of failure to

sale NZIS, guarantees given by the company for worker’s compensation, regulatory and taxation

contingencies and the prior year contingent liability on account of legal proceeding by South32 against

Bluescope Steel. All these contingencies needs to be reviewed extensively to check if any of them has

been materialized (Oberoi, 2018).

Section 2: Analytical Review, Assertions and Audit procedures

The analytical review of the company has been shown below. The same has been done using key ratios

for the years 2015 to 2018.

Bluescope Steel Company Limited > Ratios Analysis

Name of the ratio Formulas 2018 2017 2016 2015

Part A: Liquidity Ratios

Current Ratio or Working

Capital Ratio Current Assets / Current Liabilities 1.72 1.58 1.40 1.59

Quick ratio or Acid test ratio (Current Assets - Inventory) / Current

Liabilities 0.98 0.90 0.79 0.84

Cash flow Ratio Net cash flow from operating activities /

Current Liabilities 0.44 0.46 0.42 0.27

Name of the ratio Formulas 2018 2017 2016 2015

Part B: Profitability Ratios

Return on Equity Profit available to owners / Average

Equity *100

23.65

% 13.97% 8.35% 3.74%

Return on Assets Profit (loss) / Average total assets *100 14.90

% 8.08% 4.55% 2.25%

Gross Profit Margin Gross Profit / Sales Revenue *100 41.98

% 43.93% 45.52

% 43.36%

Profit Margin Profit (loss) / Sales Revenue *100 14.13

% 7.33% 4.52% 2.07%

Cash Flow to Sales Cash Flow from operating activities /

Sales Revenue *100 9.90% 10.73% 10.34

% 6.31%

Name of the ratio Formulas 2018 2017 2016 2015

Part C: Solvency Ratios

Debt Equity Ratio Debt/Equity 0.59 0.73 0.84 0.66

Debt to Asset Ratio Debt/Total Assets 0.37 0.42 0.46 0.40

Interest Service coverage

ratio EBIT/Interest cost 13.32 11.46 5.75 3.89

Name of the ratio Formulas 2018 2017 2016 2015

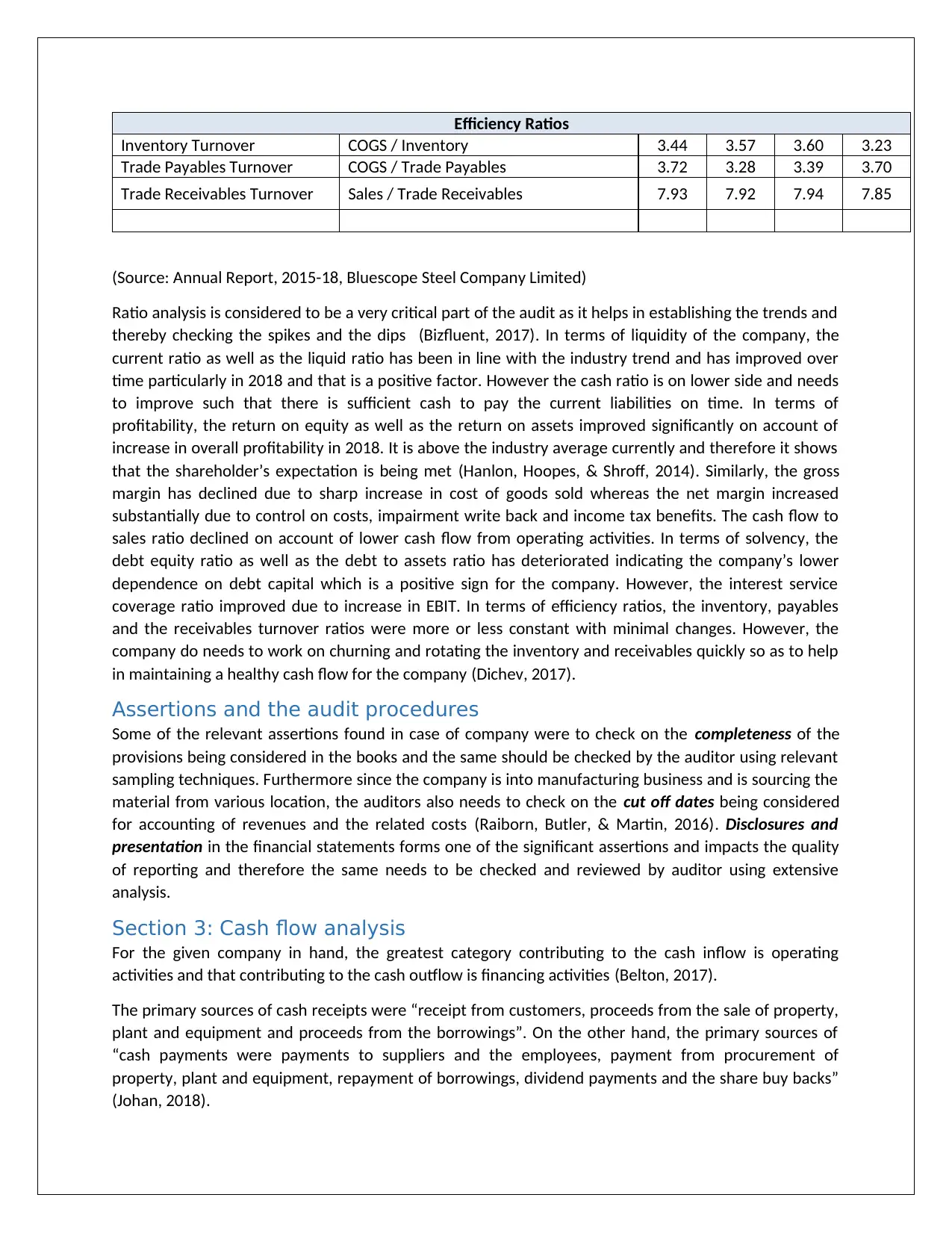

Efficiency Ratios

Inventory Turnover COGS / Inventory 3.44 3.57 3.60 3.23

Trade Payables Turnover COGS / Trade Payables 3.72 3.28 3.39 3.70

Trade Receivables Turnover Sales / Trade Receivables 7.93 7.92 7.94 7.85

(Source: Annual Report, 2015-18, Bluescope Steel Company Limited)

Ratio analysis is considered to be a very critical part of the audit as it helps in establishing the trends and

thereby checking the spikes and the dips (Bizfluent, 2017). In terms of liquidity of the company, the

current ratio as well as the liquid ratio has been in line with the industry trend and has improved over

time particularly in 2018 and that is a positive factor. However the cash ratio is on lower side and needs

to improve such that there is sufficient cash to pay the current liabilities on time. In terms of

profitability, the return on equity as well as the return on assets improved significantly on account of

increase in overall profitability in 2018. It is above the industry average currently and therefore it shows

that the shareholder’s expectation is being met (Hanlon, Hoopes, & Shroff, 2014). Similarly, the gross

margin has declined due to sharp increase in cost of goods sold whereas the net margin increased

substantially due to control on costs, impairment write back and income tax benefits. The cash flow to

sales ratio declined on account of lower cash flow from operating activities. In terms of solvency, the

debt equity ratio as well as the debt to assets ratio has deteriorated indicating the company’s lower

dependence on debt capital which is a positive sign for the company. However, the interest service

coverage ratio improved due to increase in EBIT. In terms of efficiency ratios, the inventory, payables

and the receivables turnover ratios were more or less constant with minimal changes. However, the

company do needs to work on churning and rotating the inventory and receivables quickly so as to help

in maintaining a healthy cash flow for the company (Dichev, 2017).

Assertions and the audit procedures

Some of the relevant assertions found in case of company were to check on the completeness of the

provisions being considered in the books and the same should be checked by the auditor using relevant

sampling techniques. Furthermore since the company is into manufacturing business and is sourcing the

material from various location, the auditors also needs to check on the cut off dates being considered

for accounting of revenues and the related costs (Raiborn, Butler, & Martin, 2016). Disclosures and

presentation in the financial statements forms one of the significant assertions and impacts the quality

of reporting and therefore the same needs to be checked and reviewed by auditor using extensive

analysis.

Section 3: Cash flow analysis

For the given company in hand, the greatest category contributing to the cash inflow is operating

activities and that contributing to the cash outflow is financing activities (Belton, 2017).

The primary sources of cash receipts were “receipt from customers, proceeds from the sale of property,

plant and equipment and proceeds from the borrowings”. On the other hand, the primary sources of

“cash payments were payments to suppliers and the employees, payment from procurement of

property, plant and equipment, repayment of borrowings, dividend payments and the share buy backs”

(Johan, 2018).

Inventory Turnover COGS / Inventory 3.44 3.57 3.60 3.23

Trade Payables Turnover COGS / Trade Payables 3.72 3.28 3.39 3.70

Trade Receivables Turnover Sales / Trade Receivables 7.93 7.92 7.94 7.85

(Source: Annual Report, 2015-18, Bluescope Steel Company Limited)

Ratio analysis is considered to be a very critical part of the audit as it helps in establishing the trends and

thereby checking the spikes and the dips (Bizfluent, 2017). In terms of liquidity of the company, the

current ratio as well as the liquid ratio has been in line with the industry trend and has improved over

time particularly in 2018 and that is a positive factor. However the cash ratio is on lower side and needs

to improve such that there is sufficient cash to pay the current liabilities on time. In terms of

profitability, the return on equity as well as the return on assets improved significantly on account of

increase in overall profitability in 2018. It is above the industry average currently and therefore it shows

that the shareholder’s expectation is being met (Hanlon, Hoopes, & Shroff, 2014). Similarly, the gross

margin has declined due to sharp increase in cost of goods sold whereas the net margin increased

substantially due to control on costs, impairment write back and income tax benefits. The cash flow to

sales ratio declined on account of lower cash flow from operating activities. In terms of solvency, the

debt equity ratio as well as the debt to assets ratio has deteriorated indicating the company’s lower

dependence on debt capital which is a positive sign for the company. However, the interest service

coverage ratio improved due to increase in EBIT. In terms of efficiency ratios, the inventory, payables

and the receivables turnover ratios were more or less constant with minimal changes. However, the

company do needs to work on churning and rotating the inventory and receivables quickly so as to help

in maintaining a healthy cash flow for the company (Dichev, 2017).

Assertions and the audit procedures

Some of the relevant assertions found in case of company were to check on the completeness of the

provisions being considered in the books and the same should be checked by the auditor using relevant

sampling techniques. Furthermore since the company is into manufacturing business and is sourcing the

material from various location, the auditors also needs to check on the cut off dates being considered

for accounting of revenues and the related costs (Raiborn, Butler, & Martin, 2016). Disclosures and

presentation in the financial statements forms one of the significant assertions and impacts the quality

of reporting and therefore the same needs to be checked and reviewed by auditor using extensive

analysis.

Section 3: Cash flow analysis

For the given company in hand, the greatest category contributing to the cash inflow is operating

activities and that contributing to the cash outflow is financing activities (Belton, 2017).

The primary sources of cash receipts were “receipt from customers, proceeds from the sale of property,

plant and equipment and proceeds from the borrowings”. On the other hand, the primary sources of

“cash payments were payments to suppliers and the employees, payment from procurement of

property, plant and equipment, repayment of borrowings, dividend payments and the share buy backs”

(Johan, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

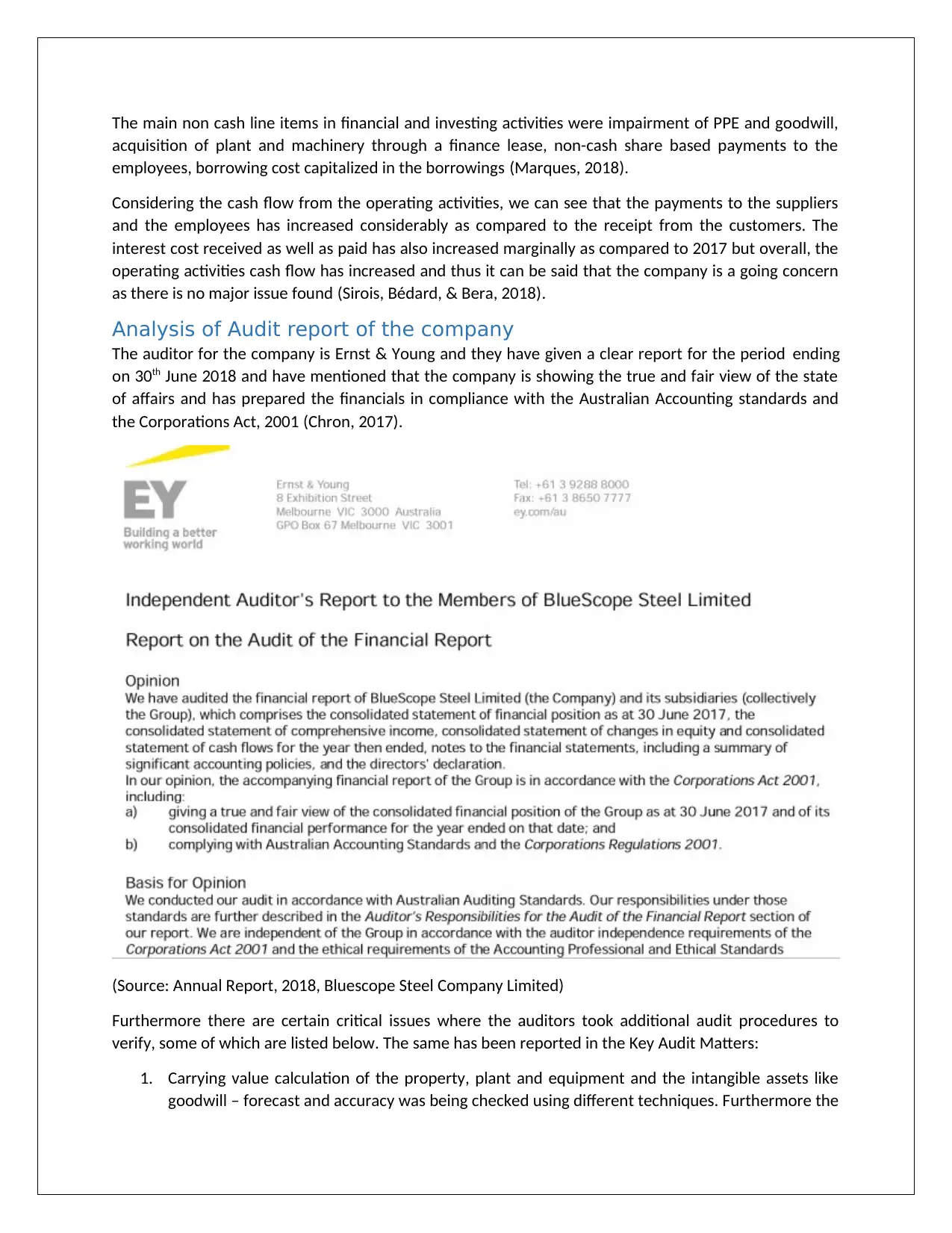

The main non cash line items in financial and investing activities were impairment of PPE and goodwill,

acquisition of plant and machinery through a finance lease, non-cash share based payments to the

employees, borrowing cost capitalized in the borrowings (Marques, 2018).

Considering the cash flow from the operating activities, we can see that the payments to the suppliers

and the employees has increased considerably as compared to the receipt from the customers. The

interest cost received as well as paid has also increased marginally as compared to 2017 but overall, the

operating activities cash flow has increased and thus it can be said that the company is a going concern

as there is no major issue found (Sirois, Bédard, & Bera, 2018).

Analysis of Audit report of the company

The auditor for the company is Ernst & Young and they have given a clear report for the period ending

on 30th June 2018 and have mentioned that the company is showing the true and fair view of the state

of affairs and has prepared the financials in compliance with the Australian Accounting standards and

the Corporations Act, 2001 (Chron, 2017).

(Source: Annual Report, 2018, Bluescope Steel Company Limited)

Furthermore there are certain critical issues where the auditors took additional audit procedures to

verify, some of which are listed below. The same has been reported in the Key Audit Matters:

1. Carrying value calculation of the property, plant and equipment and the intangible assets like

goodwill – forecast and accuracy was being checked using different techniques. Furthermore the

acquisition of plant and machinery through a finance lease, non-cash share based payments to the

employees, borrowing cost capitalized in the borrowings (Marques, 2018).

Considering the cash flow from the operating activities, we can see that the payments to the suppliers

and the employees has increased considerably as compared to the receipt from the customers. The

interest cost received as well as paid has also increased marginally as compared to 2017 but overall, the

operating activities cash flow has increased and thus it can be said that the company is a going concern

as there is no major issue found (Sirois, Bédard, & Bera, 2018).

Analysis of Audit report of the company

The auditor for the company is Ernst & Young and they have given a clear report for the period ending

on 30th June 2018 and have mentioned that the company is showing the true and fair view of the state

of affairs and has prepared the financials in compliance with the Australian Accounting standards and

the Corporations Act, 2001 (Chron, 2017).

(Source: Annual Report, 2018, Bluescope Steel Company Limited)

Furthermore there are certain critical issues where the auditors took additional audit procedures to

verify, some of which are listed below. The same has been reported in the Key Audit Matters:

1. Carrying value calculation of the property, plant and equipment and the intangible assets like

goodwill – forecast and accuracy was being checked using different techniques. Furthermore the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

calculation of impairment was also being reviewed (Buchanan, Cao, Liljeblom, & Weihrich,

2017).

2. Accounting for taxes – the company witnessed significant tax movements and therefore the

auditors checked on the estimates and assumptions in this regard.

Conclusion

Extensive discussion and analysis was being conducted on the annual report and based on the results of

the analytical review and cash flow analysis, it can be said that the company is a going concern. The

company has improved significantly in terms of profitability, solvency and liquidity but still needs to

improve in terms of efficiency ratios. The audit report and the cash flow statement was also being

reviewed and analyzed.

References

Annual Report, 2018, Bluescope Steel Company Limited

Annual Report, 2017, Bluescope Steel Company Limited

Annual Report, 2016, Bluescope Steel Company Limited

Annual Report, 2015, Bluescope Steel Company Limited

Alieid, E. E. (2016). The Role of Accounting Information Systems in Making Investment Decisions.

Internal Auditing & Risk Management, 11(2), 233-242.

Appelbaum, D., Kogan, A., & Vasarhelyi, M. (2018). Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics. . Journal of

Accounting Literature, 40(1), 83-101.

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance (Vol. 2). London:

Macat International ltd.

Bizfluent. (2017). Advantages & Disadvantages of Internal Control. Retrieved december 07, 2017, from

https://bizfluent.com/info-8064250-advantages-disadvantages-internal-control.html

Buchanan, B., Cao, C., Liljeblom, E., & Weihrich, S. (2017). Taxation and Dividend Policy: The Muting

Effect of Agency Issues and Shareholder Conflicts. Journal of Corporate Finance, 42, 179-197.

Chron. (2017). five-common-features-internal-control-system-business. Retrieved december 07, 2017,

from http://smallbusiness.chron.com/five-common-features-internal-control-system-business-

430.html

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. doi:https://doi.org/10.1080/00014788.2017.1299620

Gooley, J. (2016). Principles of Australian Contract Law (2 ed.). Australia: Lexis Nexis.

Hanlon, M., Hoopes, L., & Shroff, N. (2014). The effect of tax authority monitoring and enforcement on

financial reporting quality. The Journal of the American Taxation Association, 137-170.

2017).

2. Accounting for taxes – the company witnessed significant tax movements and therefore the

auditors checked on the estimates and assumptions in this regard.

Conclusion

Extensive discussion and analysis was being conducted on the annual report and based on the results of

the analytical review and cash flow analysis, it can be said that the company is a going concern. The

company has improved significantly in terms of profitability, solvency and liquidity but still needs to

improve in terms of efficiency ratios. The audit report and the cash flow statement was also being

reviewed and analyzed.

References

Annual Report, 2018, Bluescope Steel Company Limited

Annual Report, 2017, Bluescope Steel Company Limited

Annual Report, 2016, Bluescope Steel Company Limited

Annual Report, 2015, Bluescope Steel Company Limited

Alieid, E. E. (2016). The Role of Accounting Information Systems in Making Investment Decisions.

Internal Auditing & Risk Management, 11(2), 233-242.

Appelbaum, D., Kogan, A., & Vasarhelyi, M. (2018). Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics. . Journal of

Accounting Literature, 40(1), 83-101.

Belton, P. (2017). Competitive Strategy: Creating and Sustaining Superior Performance (Vol. 2). London:

Macat International ltd.

Bizfluent. (2017). Advantages & Disadvantages of Internal Control. Retrieved december 07, 2017, from

https://bizfluent.com/info-8064250-advantages-disadvantages-internal-control.html

Buchanan, B., Cao, C., Liljeblom, E., & Weihrich, S. (2017). Taxation and Dividend Policy: The Muting

Effect of Agency Issues and Shareholder Conflicts. Journal of Corporate Finance, 42, 179-197.

Chron. (2017). five-common-features-internal-control-system-business. Retrieved december 07, 2017,

from http://smallbusiness.chron.com/five-common-features-internal-control-system-business-

430.html

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632. doi:https://doi.org/10.1080/00014788.2017.1299620

Gooley, J. (2016). Principles of Australian Contract Law (2 ed.). Australia: Lexis Nexis.

Hanlon, M., Hoopes, L., & Shroff, N. (2014). The effect of tax authority monitoring and enforcement on

financial reporting quality. The Journal of the American Taxation Association, 137-170.

Johan, S. (2018). The Relationship Between Economic Value Added, Market Value Added And Return On

Cost Of Capital In Measuring Corporate Performance. Jurnal Manajemen Bisnis dan

Kewirausahaan, 3(1), 121-134.

Jones, P. (2017). Statistical Sampling and Risk Analysis in Auditing. NY: Routledge.

Marques, R. P. (2018). Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, 820-830.

Oberoi, J. (2018). Interest rate risk management and the mix of fixed and floating rate debt. Journal of

Banking and Finance, 86(3), 70-86.

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

Sirois, L., Bédard, J., & Bera, P. (2018). The informational value of key audit matters in the auditor's

report: evidence from an Eye-tracking study. Accounting Horizons., 32(2), 141-162.

Wendt, K. (2018). Positive Impact Investing: A Sustainable Bridge between Strategy, Innovation, Change

and Learning (first ed.). Switzerland: Springer.

Cost Of Capital In Measuring Corporate Performance. Jurnal Manajemen Bisnis dan

Kewirausahaan, 3(1), 121-134.

Jones, P. (2017). Statistical Sampling and Risk Analysis in Auditing. NY: Routledge.

Marques, R. P. (2018). Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, 820-830.

Oberoi, J. (2018). Interest rate risk management and the mix of fixed and floating rate debt. Journal of

Banking and Finance, 86(3), 70-86.

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

Sirois, L., Bédard, J., & Bera, P. (2018). The informational value of key audit matters in the auditor's

report: evidence from an Eye-tracking study. Accounting Horizons., 32(2), 141-162.

Wendt, K. (2018). Positive Impact Investing: A Sustainable Bridge between Strategy, Innovation, Change

and Learning (first ed.). Switzerland: Springer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.