BM414 Financial Decision Making: Analysis of SKANSKA Plc's Finance

VerifiedAdded on 2023/06/18

|13

|3865

|265

Report

AI Summary

This assignment provides a comprehensive analysis of financial decision-making within SKANSKA Plc, focusing on the application of management accounting techniques and financial ratios. It evaluates the role of accounting and finance functions in the company's operations, highlighting the use of financial planning, statement analysis, standard costing, budgetary control, and cash flow statements. The report includes a critical analysis of these techniques, acknowledging their benefits and limitations. Furthermore, it calculates and interprets key financial ratios such as Return on Capital Employed (ROCE), net profit margin, current ratio, and debtor/creditor days, assessing SKANSKA Plc's financial performance and efficiency. Desklib is your go-to resource for similar solved assignments and past papers.

Financial Decision-Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK-1............................................................................................................................................3

INTRODUCTION...........................................................................................................................3

Techniques of management accounting.......................................................................................4

Critical Analysis...........................................................................................................................5

CONCLUSION................................................................................................................................6

TASK-2............................................................................................................................................7

Calculation of ratios.....................................................................................................................7

Accounting ratios and their importance.......................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

TASK-1............................................................................................................................................3

INTRODUCTION...........................................................................................................................3

Techniques of management accounting.......................................................................................4

Critical Analysis...........................................................................................................................5

CONCLUSION................................................................................................................................6

TASK-2............................................................................................................................................7

Calculation of ratios.....................................................................................................................7

Accounting ratios and their importance.......................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

TASK-1

INTRODUCTION

The financial decision making is a crucial decision that are taken by the financial

managers of the company about the financing mix of the company. In other words it can be said

it is a decision making which focuses on the allocation and borrowing of funds which are

required for the investment decision of the company. Accounting ratios are a tool which is used

in analysing the financial statement of the company and identifying the financial position of the

company thus helping the company in making financial decision regarding the allocation and

borrowing of funds.

Accounting function plays a very vital role in running a company. Its helps the company

in evaluating the performance of the company, it also ensures statutory compliance. And it is

also very useful in creating budgets and future projection and also finds out if there are any

deviations or not. Similarly finance function are the lifeblood of any business. It involves

acquiring and utilisation of funds which are necessary for smooth functioning of an organisation.

It helps in identifying the need of finance, the sources from the company can acquire the funds

and compares the different sources of finance and analysing the risk involved.

SKANSKA Plc, was establishes in 1887. it started with a modest beginning, based in s

small fishing village in Sweden more than 125 years ago. It is now one of the world's leading

project development and constructing groups. It is operating in selected markets like Europe and

the U.S. It is also listed on the Stockholm stock exchange. Its headquarter is situated in Sweden's

capital city. Its purpose it to contribute to a sustainable future for its customers and communities.

It employs around 32000 people. In 2019, its revenue was SEK 176.8 billion and its operating

income was SEK 7.8 billion (Skanska UK in brief., 2021).

Management Accounting

Management accounting is a process which analyses the operations and the costs of the

business and prepares a financial record which helps the decision making process and also helps

in achieving the future goals (Abdusalomova, 2019). It helps management in devising new plans

and policy, making decision, and controlling and monitoring the overall performance of the

company.

INTRODUCTION

The financial decision making is a crucial decision that are taken by the financial

managers of the company about the financing mix of the company. In other words it can be said

it is a decision making which focuses on the allocation and borrowing of funds which are

required for the investment decision of the company. Accounting ratios are a tool which is used

in analysing the financial statement of the company and identifying the financial position of the

company thus helping the company in making financial decision regarding the allocation and

borrowing of funds.

Accounting function plays a very vital role in running a company. Its helps the company

in evaluating the performance of the company, it also ensures statutory compliance. And it is

also very useful in creating budgets and future projection and also finds out if there are any

deviations or not. Similarly finance function are the lifeblood of any business. It involves

acquiring and utilisation of funds which are necessary for smooth functioning of an organisation.

It helps in identifying the need of finance, the sources from the company can acquire the funds

and compares the different sources of finance and analysing the risk involved.

SKANSKA Plc, was establishes in 1887. it started with a modest beginning, based in s

small fishing village in Sweden more than 125 years ago. It is now one of the world's leading

project development and constructing groups. It is operating in selected markets like Europe and

the U.S. It is also listed on the Stockholm stock exchange. Its headquarter is situated in Sweden's

capital city. Its purpose it to contribute to a sustainable future for its customers and communities.

It employs around 32000 people. In 2019, its revenue was SEK 176.8 billion and its operating

income was SEK 7.8 billion (Skanska UK in brief., 2021).

Management Accounting

Management accounting is a process which analyses the operations and the costs of the

business and prepares a financial record which helps the decision making process and also helps

in achieving the future goals (Abdusalomova, 2019). It helps management in devising new plans

and policy, making decision, and controlling and monitoring the overall performance of the

company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Techniques of management accounting

There are various techniques of management accounting:

Financial Planning

Financial planing is considered one of the best tool for achieving the objectives of

business (Alexander, 2018). It is an act of planning in advance about the financial activities

which are necessary for achieving the primary objectives of the company. It helps SKANSKA

Plc in formulating financial policies and develop procedures to achieve the objectives of the

company. Also, it helps to determines the short and long term objectives of the SKANSKA Plc.

Analysis of Financial Statement

Analysis of financial statement is a process of analysing the organisation's financial

statement for the purpose of decision making. This analysis is used by internal and external

stakeholders to analyse the performance of the business. Financial reports are prepared by

SKANSKA Plc on monthly, quarterly and annually and are used internally for the management

of business. This technique is used by SKANSKA Plc to compare the trend analysis, financial

statements, cash fund flow statement for decision making purposes.

Standard Costing

Standard costing is a method of estimating the expense of the production processes

(Berger, 2011). It compares the standard cost and the actual cost and finds out the difference

which is known as the variance. This allows SKANSKA Plc to improve its cost control as they

are more aware of their spending habits and can strive to achieve to for no variance.

Budgetary Control

Budgetary control is a method of determining actual results with the budgetary figures for

the business for the future and standards are then compared to the budgeted figures for

calculating the variances (Guo, 2018). Budgetary control is one of the most important techniques

of directing business operation which is used by SKANSKA Plc which helps in achieving

satisfactory return on investment.

Fund Flow Statement

It is a statement which is prepared to analyse the changes in the financial position of the

organisation between its two balance sheets. It includes the inflow as well as outflow of funds,

the sources of funds and its application for a particular period. It helps SKANSKA Plc in

There are various techniques of management accounting:

Financial Planning

Financial planing is considered one of the best tool for achieving the objectives of

business (Alexander, 2018). It is an act of planning in advance about the financial activities

which are necessary for achieving the primary objectives of the company. It helps SKANSKA

Plc in formulating financial policies and develop procedures to achieve the objectives of the

company. Also, it helps to determines the short and long term objectives of the SKANSKA Plc.

Analysis of Financial Statement

Analysis of financial statement is a process of analysing the organisation's financial

statement for the purpose of decision making. This analysis is used by internal and external

stakeholders to analyse the performance of the business. Financial reports are prepared by

SKANSKA Plc on monthly, quarterly and annually and are used internally for the management

of business. This technique is used by SKANSKA Plc to compare the trend analysis, financial

statements, cash fund flow statement for decision making purposes.

Standard Costing

Standard costing is a method of estimating the expense of the production processes

(Berger, 2011). It compares the standard cost and the actual cost and finds out the difference

which is known as the variance. This allows SKANSKA Plc to improve its cost control as they

are more aware of their spending habits and can strive to achieve to for no variance.

Budgetary Control

Budgetary control is a method of determining actual results with the budgetary figures for

the business for the future and standards are then compared to the budgeted figures for

calculating the variances (Guo, 2018). Budgetary control is one of the most important techniques

of directing business operation which is used by SKANSKA Plc which helps in achieving

satisfactory return on investment.

Fund Flow Statement

It is a statement which is prepared to analyse the changes in the financial position of the

organisation between its two balance sheets. It includes the inflow as well as outflow of funds,

the sources of funds and its application for a particular period. It helps SKANSKA Plc in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

identifying the liquidity strain despite generating profits as shown in the profit and loss statement

of the company.

Cash Flow Statement

It is a financial statement which shows the entry and exit of the amount of cash and cash

equivalents of a company (Maheshwari, 2021). It measures how well the company generates its

cash to pay the debts and thus, maintaining its cash position. It helps SKANSKA Plc in verifying

the capital cash balance of the company and maintaining its cash position..

Decision Making

Decision making is a process of choosing the best course of action from various

alternatives for the purpose of achieving the objectives of the company (Abubakar, and et.al.,

2019). It plays a vital role in the successful running of the company. It helps the management of

SKANSKA Plc to choose the best alternative techniques of marginal costing, capital budgeting

etc. which helps them to maximise profits.

Critical Analysis

Management accounting techniques are the process of accumulation, identification,

analysis, measurement, preparation, communication and interpretation of information that helps

in achieving the objectives of the company. It helps management of the company to perform all

the functions such as planning, organising, directing, staffing and controlling (Oyewo, 2021). It

also helps the executives to execute plans and helps in measurement of the performance of the

company.

Management accounting techniques plays a very vital role in SKANSKA Plc in

efficiently performing its function such as planning controlling and decision making. With the

use of the technique of financial planing the company is able to plan in advance the financial

activities which are necessary for achieving the objectives of the company. SKANSKA Plc with

the help of this technique is formulating policies and procedures to achieve the long term and

short term objectives of the company. It serves the company with vital source of information for

future planning and the historical data captured by these techniques of accounting shows the

growth of the company which is helpful in forecasting the future. Also, the analysis of various

financial statements has helped the company in effective decision making by comparing the cash

flow funds, trend analysis and statements. It helps SKANKSA Plc in applying various analytical

of the company.

Cash Flow Statement

It is a financial statement which shows the entry and exit of the amount of cash and cash

equivalents of a company (Maheshwari, 2021). It measures how well the company generates its

cash to pay the debts and thus, maintaining its cash position. It helps SKANSKA Plc in verifying

the capital cash balance of the company and maintaining its cash position..

Decision Making

Decision making is a process of choosing the best course of action from various

alternatives for the purpose of achieving the objectives of the company (Abubakar, and et.al.,

2019). It plays a vital role in the successful running of the company. It helps the management of

SKANSKA Plc to choose the best alternative techniques of marginal costing, capital budgeting

etc. which helps them to maximise profits.

Critical Analysis

Management accounting techniques are the process of accumulation, identification,

analysis, measurement, preparation, communication and interpretation of information that helps

in achieving the objectives of the company. It helps management of the company to perform all

the functions such as planning, organising, directing, staffing and controlling (Oyewo, 2021). It

also helps the executives to execute plans and helps in measurement of the performance of the

company.

Management accounting techniques plays a very vital role in SKANSKA Plc in

efficiently performing its function such as planning controlling and decision making. With the

use of the technique of financial planing the company is able to plan in advance the financial

activities which are necessary for achieving the objectives of the company. SKANSKA Plc with

the help of this technique is formulating policies and procedures to achieve the long term and

short term objectives of the company. It serves the company with vital source of information for

future planning and the historical data captured by these techniques of accounting shows the

growth of the company which is helpful in forecasting the future. Also, the analysis of various

financial statements has helped the company in effective decision making by comparing the cash

flow funds, trend analysis and statements. It helps SKANKSA Plc in applying various analytical

information regarding different alternatives which makes it easy for the management of the

company in decision making. That is by using standard costing it measures the actual cost with

the set standards and finds out the deviation which helps the company in measuring and

monitoring the actual performance and taking corrective actions to make sure that the goals and

objectives of the company are achieved. With the proper analysis of the cash flow statement. it

has helped in enhancing the profitability and liquidity position of the company and has also

helped SKANSKA Plc in maintaining the capital cash balance of the company.

However it can be critically analysed that using of such management accounting

techniques and installation of such system in very costly. Also it can be critiqued that the

decision made by the management may be misleading as these decision are based on the

management techniques and these techniques take into consideration the past records which is

provided by the cost and financial accounting such as standard costing. And if the past data is

not accurate and it limits the dependence of the management of the company for future decision

making. There are also possibility of manipulation and personal bias from data collection to

stage of interpretation in management accounting of the company. And which will result in loss

of objectivity and validity. It can be critically evaluated that it only takes into consideration in

quantifiable variables and there are various issues which cannot be expressed in monetary terms.

Hence, such problems cannot be interpreted by the company for the future.

CONCLUSION

From the above task it can be concluded that financial decision making is a very crucial

decision which is taken by the management about the financing mix of the company. Accounting

and finance functions also plays a very vital role in the smooth functioning of SKANSKA plc. It

evaluates the performance of the company and ensures statutory compliance. Also, it can be

concluded that there are various management techniques that are used by the companies such as

financial planning, analysis of financial statements, standard costing and budgetary control. And

with the use of all these techniques of management accounting it helps SKANSKA Plc to

accumulate, measure, identify, interpret the data which helps in fulfilling the objectives of the

company. Also, these techniques helps the company in performing its function such as planning,

controlling, directing and decision making. However, it can be understood from the critical

evaluation that using of such techniques can be costlier. Also, it is based on past records so it

company in decision making. That is by using standard costing it measures the actual cost with

the set standards and finds out the deviation which helps the company in measuring and

monitoring the actual performance and taking corrective actions to make sure that the goals and

objectives of the company are achieved. With the proper analysis of the cash flow statement. it

has helped in enhancing the profitability and liquidity position of the company and has also

helped SKANSKA Plc in maintaining the capital cash balance of the company.

However it can be critically analysed that using of such management accounting

techniques and installation of such system in very costly. Also it can be critiqued that the

decision made by the management may be misleading as these decision are based on the

management techniques and these techniques take into consideration the past records which is

provided by the cost and financial accounting such as standard costing. And if the past data is

not accurate and it limits the dependence of the management of the company for future decision

making. There are also possibility of manipulation and personal bias from data collection to

stage of interpretation in management accounting of the company. And which will result in loss

of objectivity and validity. It can be critically evaluated that it only takes into consideration in

quantifiable variables and there are various issues which cannot be expressed in monetary terms.

Hence, such problems cannot be interpreted by the company for the future.

CONCLUSION

From the above task it can be concluded that financial decision making is a very crucial

decision which is taken by the management about the financing mix of the company. Accounting

and finance functions also plays a very vital role in the smooth functioning of SKANSKA plc. It

evaluates the performance of the company and ensures statutory compliance. Also, it can be

concluded that there are various management techniques that are used by the companies such as

financial planning, analysis of financial statements, standard costing and budgetary control. And

with the use of all these techniques of management accounting it helps SKANSKA Plc to

accumulate, measure, identify, interpret the data which helps in fulfilling the objectives of the

company. Also, these techniques helps the company in performing its function such as planning,

controlling, directing and decision making. However, it can be understood from the critical

evaluation that using of such techniques can be costlier. Also, it is based on past records so it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

can mislead the decision making process. And there are every possible chances of manipulation

and personal bias which may hinder the management accounting process.

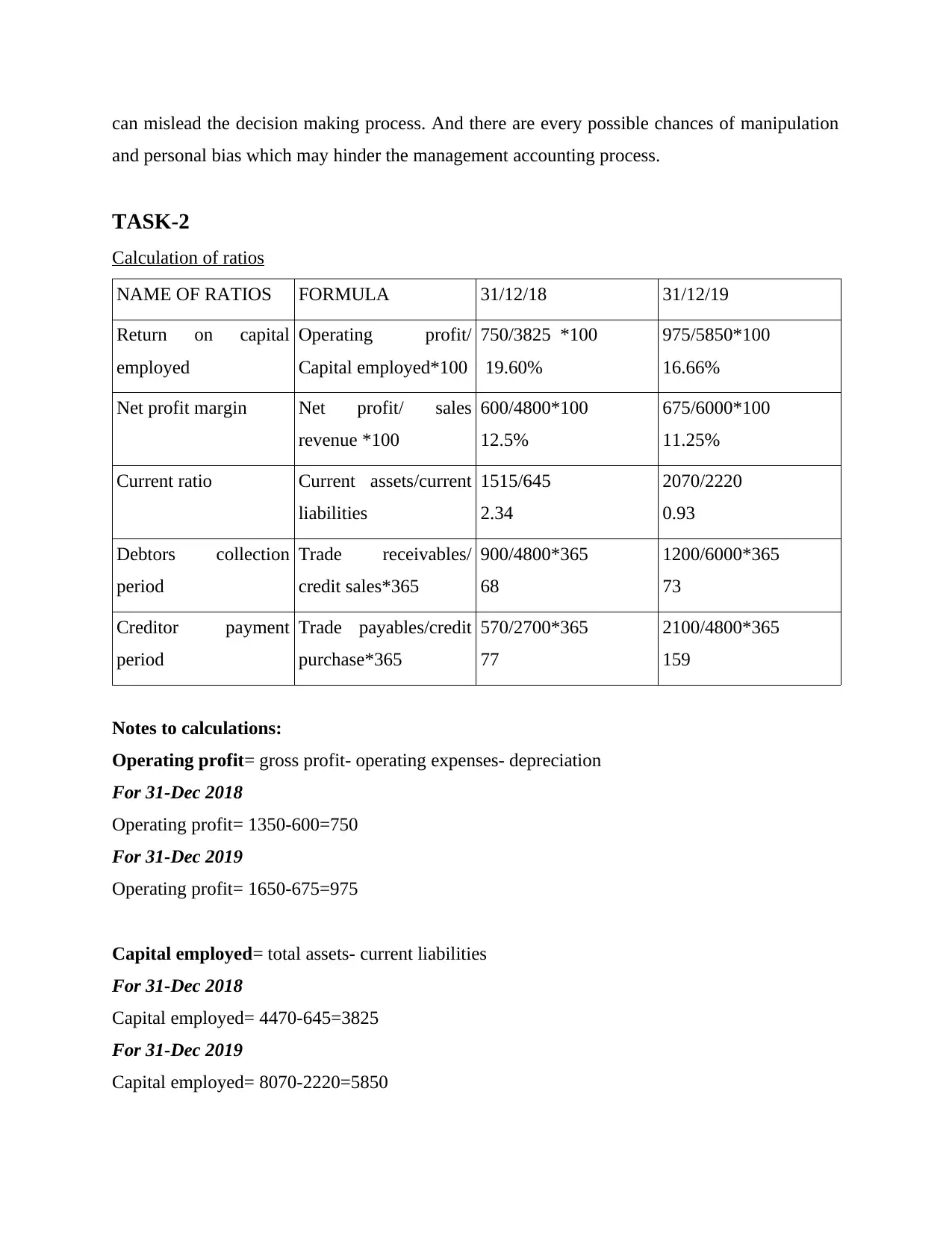

TASK-2

Calculation of ratios

NAME OF RATIOS FORMULA 31/12/18 31/12/19

Return on capital

employed

Operating profit/

Capital employed*100

750/3825 *100

19.60%

975/5850*100

16.66%

Net profit margin Net profit/ sales

revenue *100

600/4800*100

12.5%

675/6000*100

11.25%

Current ratio Current assets/current

liabilities

1515/645

2.34

2070/2220

0.93

Debtors collection

period

Trade receivables/

credit sales*365

900/4800*365

68

1200/6000*365

73

Creditor payment

period

Trade payables/credit

purchase*365

570/2700*365

77

2100/4800*365

159

Notes to calculations:

Operating profit= gross profit- operating expenses- depreciation

For 31-Dec 2018

Operating profit= 1350-600=750

For 31-Dec 2019

Operating profit= 1650-675=975

Capital employed= total assets- current liabilities

For 31-Dec 2018

Capital employed= 4470-645=3825

For 31-Dec 2019

Capital employed= 8070-2220=5850

and personal bias which may hinder the management accounting process.

TASK-2

Calculation of ratios

NAME OF RATIOS FORMULA 31/12/18 31/12/19

Return on capital

employed

Operating profit/

Capital employed*100

750/3825 *100

19.60%

975/5850*100

16.66%

Net profit margin Net profit/ sales

revenue *100

600/4800*100

12.5%

675/6000*100

11.25%

Current ratio Current assets/current

liabilities

1515/645

2.34

2070/2220

0.93

Debtors collection

period

Trade receivables/

credit sales*365

900/4800*365

68

1200/6000*365

73

Creditor payment

period

Trade payables/credit

purchase*365

570/2700*365

77

2100/4800*365

159

Notes to calculations:

Operating profit= gross profit- operating expenses- depreciation

For 31-Dec 2018

Operating profit= 1350-600=750

For 31-Dec 2019

Operating profit= 1650-675=975

Capital employed= total assets- current liabilities

For 31-Dec 2018

Capital employed= 4470-645=3825

For 31-Dec 2019

Capital employed= 8070-2220=5850

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting ratios and their importance

Accounting ratios is a tool which is used for analysing the financial statement of

company by comparing two financial data. It a tool which is used by creditors. Stakeholders to

understand the strength, financial position of the company (Kasasbeh, 2021). The role of

accounting ratios is very significant in business as it helps to find out the efficiency of

management, rate of profit etc. it provides with valuable information in a simple form so that it

could be easily understood by the creditors, investors and shareholders. It helps in decision

making and formulating plans by comparing the past financial performance of the company.

There are various ratios which helps in identifying the financial position of the company:

Return on capital employed

Return on capital employed is a profitability ratio which shows that how a company is

using its capital to produce profits efficiently (Singh, S. and Das, S., 2018). It is one of the most

suitable profitability ratios which is commonly used by investors to identify whether they should

invest in the company or not. A higher rate of capital employed is always favourable as it shows

more profits are being generated and it shows efficient use of capital employed. Return on capital

employed is useful in measuring the financial efficiency as it measures the profitability of the

company after measuring the capital used to create that level of profitability

From the above calculation of the ROCE for the SKANSKA Plc it can be seen that it has

a declining rate of ROCE that is in 2018 the ROCE was 19.60% but in 2019 it came down to

16.66% which indicates that the companies profit generation has been decreased by 3%. Also, it

shows that SKANSKA Plc is not efficiently using its capital employed. One of the major reason

in the decline of ROCE of the company is that cost of expenses is increasing and the sales is not

increasing to that level. So to improve ROCE, SKANSKA Plc can sell out its outdated machines

and lower the total assets base of the company which will help in improving the ROCE as

removing unnecessary assets allows less capital to be employed for same amount of production.

Also, they can start paying off debt which will help in reducing liabilites and result in increasing

capital employed.

Net profit margin

Net profit margin is a ratio which shows that how much net profit is generated as to the

percentage of revenue received (Nariswari,2020). It helps the investors and the shareholders to

Accounting ratios is a tool which is used for analysing the financial statement of

company by comparing two financial data. It a tool which is used by creditors. Stakeholders to

understand the strength, financial position of the company (Kasasbeh, 2021). The role of

accounting ratios is very significant in business as it helps to find out the efficiency of

management, rate of profit etc. it provides with valuable information in a simple form so that it

could be easily understood by the creditors, investors and shareholders. It helps in decision

making and formulating plans by comparing the past financial performance of the company.

There are various ratios which helps in identifying the financial position of the company:

Return on capital employed

Return on capital employed is a profitability ratio which shows that how a company is

using its capital to produce profits efficiently (Singh, S. and Das, S., 2018). It is one of the most

suitable profitability ratios which is commonly used by investors to identify whether they should

invest in the company or not. A higher rate of capital employed is always favourable as it shows

more profits are being generated and it shows efficient use of capital employed. Return on capital

employed is useful in measuring the financial efficiency as it measures the profitability of the

company after measuring the capital used to create that level of profitability

From the above calculation of the ROCE for the SKANSKA Plc it can be seen that it has

a declining rate of ROCE that is in 2018 the ROCE was 19.60% but in 2019 it came down to

16.66% which indicates that the companies profit generation has been decreased by 3%. Also, it

shows that SKANSKA Plc is not efficiently using its capital employed. One of the major reason

in the decline of ROCE of the company is that cost of expenses is increasing and the sales is not

increasing to that level. So to improve ROCE, SKANSKA Plc can sell out its outdated machines

and lower the total assets base of the company which will help in improving the ROCE as

removing unnecessary assets allows less capital to be employed for same amount of production.

Also, they can start paying off debt which will help in reducing liabilites and result in increasing

capital employed.

Net profit margin

Net profit margin is a ratio which shows that how much net profit is generated as to the

percentage of revenue received (Nariswari,2020). It helps the investors and the shareholders to

identify the company financial position that is whether the company is generating profits which

are enough to cover the operating and overhead costs of the company. It is one of the most

important tool which is used to identify the company's financial health that is by tracking the

increase and decrease in the ratio the company can identify whether the current practices are

effective or not.

From the above table it can be observed that the net profit margin of SKANSKA Plc is

declining that is in 2018 it was 12.5% and in 2019 it was 11.25%. So, a low net profit margin

shows that SKANSKA Plc has an ineffective cost structure that is high costs of expenses which

shows poor operational efficiency of the company. So to improve the net margin ratio

SKANSKA Plc should lower its operational costs which will automatically result in higher

profits as the cost of production will be reduced, it can increase its revenue by selling more

goods by increasing prices thus, generating higher profits. Also, they can reduce their costs and

increase their net margin for e.g. by finding cheap sources of raw material.

Current Ratio

Current ratios are the liquidity ratios that shows the ability of the company to pay the

short term obligation which are due in one year (Nuryani, 2020). It helps the investors in

analysing whether company is able to maximise its current assets so that it to satisfy the needs of

current debt and other liability. A higher current ratio is more favourable as it indicates that the

company can more easily make payments of its current debt. Current ratio is very important for

the company and the investor as it compares all the current assets of the company to its liability

and identify whether the company is able to pay its debt or not.

From the above table of calculation it can indicated that the SKANSKA Plc has a low

current ratio that in 2018 it was 2.34 and after that in 2019 it came down to 0.93. and a current

ratio which is less than 1 show that SKANSKA Plc have problems meeting its short term

obligations. It means that the company has no sufficient funds to pay its debt. Also, it can be

analysed that SKANSKA Plc is operating beyond its limit and it not utilising its resources

properly. So to have an ideal current ratio that is 2:1, SKANSKA Plc should delay any capital

purchase that requires any cash payments. Also, it can sell those capital assets which are not

generating any return to the company and use that cash to pay its current debts. Also, it can

reduce its personal drawings from the business.

Debtor collection period

are enough to cover the operating and overhead costs of the company. It is one of the most

important tool which is used to identify the company's financial health that is by tracking the

increase and decrease in the ratio the company can identify whether the current practices are

effective or not.

From the above table it can be observed that the net profit margin of SKANSKA Plc is

declining that is in 2018 it was 12.5% and in 2019 it was 11.25%. So, a low net profit margin

shows that SKANSKA Plc has an ineffective cost structure that is high costs of expenses which

shows poor operational efficiency of the company. So to improve the net margin ratio

SKANSKA Plc should lower its operational costs which will automatically result in higher

profits as the cost of production will be reduced, it can increase its revenue by selling more

goods by increasing prices thus, generating higher profits. Also, they can reduce their costs and

increase their net margin for e.g. by finding cheap sources of raw material.

Current Ratio

Current ratios are the liquidity ratios that shows the ability of the company to pay the

short term obligation which are due in one year (Nuryani, 2020). It helps the investors in

analysing whether company is able to maximise its current assets so that it to satisfy the needs of

current debt and other liability. A higher current ratio is more favourable as it indicates that the

company can more easily make payments of its current debt. Current ratio is very important for

the company and the investor as it compares all the current assets of the company to its liability

and identify whether the company is able to pay its debt or not.

From the above table of calculation it can indicated that the SKANSKA Plc has a low

current ratio that in 2018 it was 2.34 and after that in 2019 it came down to 0.93. and a current

ratio which is less than 1 show that SKANSKA Plc have problems meeting its short term

obligations. It means that the company has no sufficient funds to pay its debt. Also, it can be

analysed that SKANSKA Plc is operating beyond its limit and it not utilising its resources

properly. So to have an ideal current ratio that is 2:1, SKANSKA Plc should delay any capital

purchase that requires any cash payments. Also, it can sell those capital assets which are not

generating any return to the company and use that cash to pay its current debts. Also, it can

reduce its personal drawings from the business.

Debtor collection period

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The debtor collection period are the performance ratio that measures the efficiency of the

company that is it shows for how long the company's money it stuck with the customer credit

(Eforis, 2019). Calculating debtor collection period is very important for the company as its

helps the company in understanding how efficiently it is collecting the money that is needed to

cover its expenditure. It helps a company in maintaining a level of funds that helps the company

in paying its debt and gives the company an idea of when it is capable to make large purchases.

From the above table it can be observed that the debtor collection period of SKANSKA

Plc has increased that is in 2018 it was 68 days and now it has gone up to 73 days. An ideal time

for debtors collection should be 45 days. But from the above we can see SKANSKA Plc is not

even close to the ideal collection period. One of the major reason for the increasing debtor

collection period is the loose credit policy that is in order to increase the sales of the company,

the management of the company is granting more credit to its customers. So to improve its

debtor collection period SKANSKA Plc must have a tight credit policy that is it should be a little

strict towards its customer who pay on credit bases. And also it can send timely reminders when

the due date is near.

Creditor payment period

Creditors payment period is a ratio which measures the number of days a company takes

to pay to its creditors (Kasozi, 2017). It helps the company by providing better understanding of

whether the company is taking maximum advantage of the trade credits available or not. Credit

payment period should always be more in compared to debtor collection period so the company

can have higher return on investments. It helps the investors and creditors in analysing how

quickly company can pay its credit purchases.

From the above table of calculation it can be seen that the credit payment period of

SKANSKA Plc has bees increasing that is in 2018 it was 77 days and in 2019 it has increased

upto 159 days. So it can been seen that the company is taking full advantage of the trade credit

available to them and with a high credit period it will help the company it increasing its return on

investment.

CONCLUSION

From the above task it can be analysed that the financial position of SKANSKA Plc is not

favourable. By analysing different ratios it can be seen that the company is not using its capital

company that is it shows for how long the company's money it stuck with the customer credit

(Eforis, 2019). Calculating debtor collection period is very important for the company as its

helps the company in understanding how efficiently it is collecting the money that is needed to

cover its expenditure. It helps a company in maintaining a level of funds that helps the company

in paying its debt and gives the company an idea of when it is capable to make large purchases.

From the above table it can be observed that the debtor collection period of SKANSKA

Plc has increased that is in 2018 it was 68 days and now it has gone up to 73 days. An ideal time

for debtors collection should be 45 days. But from the above we can see SKANSKA Plc is not

even close to the ideal collection period. One of the major reason for the increasing debtor

collection period is the loose credit policy that is in order to increase the sales of the company,

the management of the company is granting more credit to its customers. So to improve its

debtor collection period SKANSKA Plc must have a tight credit policy that is it should be a little

strict towards its customer who pay on credit bases. And also it can send timely reminders when

the due date is near.

Creditor payment period

Creditors payment period is a ratio which measures the number of days a company takes

to pay to its creditors (Kasozi, 2017). It helps the company by providing better understanding of

whether the company is taking maximum advantage of the trade credits available or not. Credit

payment period should always be more in compared to debtor collection period so the company

can have higher return on investments. It helps the investors and creditors in analysing how

quickly company can pay its credit purchases.

From the above table of calculation it can be seen that the credit payment period of

SKANSKA Plc has bees increasing that is in 2018 it was 77 days and in 2019 it has increased

upto 159 days. So it can been seen that the company is taking full advantage of the trade credit

available to them and with a high credit period it will help the company it increasing its return on

investment.

CONCLUSION

From the above task it can be analysed that the financial position of SKANSKA Plc is not

favourable. By analysing different ratios it can be seen that the company is not using its capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

employed efficiently which has resulted in decrease return on capital employed. Also, the

ineffective cost structure of SKANSKA Plc has resulted in poor efficiency of operational costs

and all this has led to decline in net profit margin. So, it is recommended to investors that they

should not invest their money in SKANSKA Plc. As the company has low return on capital

employed and also its profitability ratios are decreasing resulting in decreasing profit generation.

And also, the company is not able to meet its short term obligation as it does not have enough

funds.

ineffective cost structure of SKANSKA Plc has resulted in poor efficiency of operational costs

and all this has led to decline in net profit margin. So, it is recommended to investors that they

should not invest their money in SKANSKA Plc. As the company has low return on capital

employed and also its profitability ratios are decreasing resulting in decreasing profit generation.

And also, the company is not able to meet its short term obligation as it does not have enough

funds.

REFERENCES

Books and journals

Alexander, J., 2018. Financial planning & analysis and performance management. John Wiley

& Sons.

Abdusalomova, N., 2019. PROBLEMS OF MANAGEMENT ACCOUNTING AND WAYS TO

SOLVE THEM. International Finance and Accounting, 2019(3). p.2.

Abubakar, and et.al., 2019. Knowledge management, decision-making style and organizational

performance. Journal of Innovation & Knowledge. 4(2). pp.104-114.

Berger, A., 2011. Standard Costing, Variance Analysis and Decision-Making. GRIN Verlag.

Eforis, C. and Pioleta, G., 2019. PENGARUH AVERAGE COLLECTION PERIOD,

INVENTORY TURNOVER IN DAYS, AVERAGE PAYMENT PERIOD, DEBT

RATIO, STRUKTUR ASET DAN UKURAN PERUSAHAAN TERHADAP

PROFITABILITAS PERUSAHAAN (STUDI PADA PERUSAHAAN

MANUFAKTUR SEKTOR INDUSTRI BARANG KONSUMSI YANG TERDAFTAR

DI. Ultima Management: Jurnal Ilmu Manajemen. 11(2). pp.164-188.

Guo, X. and Yang, Q., 2018. On the Integration of IT system with the budgetary control system:

insights from the case of Wanhua chemical. Wireless Personal

Communications. 102(4). pp.3687-3697.

Kasasbeh, F.I., 2021. Impact of financing decisions ratios on firm accounting-based performance:

evidence from Jordan listed companies. Future Business Journal, 7(1), pp.1-10.

Kasozi, J., 2017. The effect of working capital management on profitability: A case of listed

manufacturing firms in South Africa. Investment management and financial

innovations. 14(2). pp.336-346.

Maheshwari, S.N., Maheshwari, S.K. and Maheshwari, M.S.K., 2021. Principles of Management

Accounting. Sultan Chand & Sons.

Nariswari, T.N. and Nugraha, N.M., 2020. Profit Growth: Impact of Net Profit Margin, Gross

Profit Margin and Total Assests Turnover. International Journal of Finance & Banking

Studies (2147-4486). 9(4). pp.87-96.

Nuryani, Y. and Sunarsi, D., 2020. The Effect of Current Ratio and Debt to Equity Ratio on

Deviding Growth. JASa (Jurnal Akuntansi, Audit dan Sistem Informasi

Akuntansi). 4(2). pp.304-312.

1

Books and journals

Alexander, J., 2018. Financial planning & analysis and performance management. John Wiley

& Sons.

Abdusalomova, N., 2019. PROBLEMS OF MANAGEMENT ACCOUNTING AND WAYS TO

SOLVE THEM. International Finance and Accounting, 2019(3). p.2.

Abubakar, and et.al., 2019. Knowledge management, decision-making style and organizational

performance. Journal of Innovation & Knowledge. 4(2). pp.104-114.

Berger, A., 2011. Standard Costing, Variance Analysis and Decision-Making. GRIN Verlag.

Eforis, C. and Pioleta, G., 2019. PENGARUH AVERAGE COLLECTION PERIOD,

INVENTORY TURNOVER IN DAYS, AVERAGE PAYMENT PERIOD, DEBT

RATIO, STRUKTUR ASET DAN UKURAN PERUSAHAAN TERHADAP

PROFITABILITAS PERUSAHAAN (STUDI PADA PERUSAHAAN

MANUFAKTUR SEKTOR INDUSTRI BARANG KONSUMSI YANG TERDAFTAR

DI. Ultima Management: Jurnal Ilmu Manajemen. 11(2). pp.164-188.

Guo, X. and Yang, Q., 2018. On the Integration of IT system with the budgetary control system:

insights from the case of Wanhua chemical. Wireless Personal

Communications. 102(4). pp.3687-3697.

Kasasbeh, F.I., 2021. Impact of financing decisions ratios on firm accounting-based performance:

evidence from Jordan listed companies. Future Business Journal, 7(1), pp.1-10.

Kasozi, J., 2017. The effect of working capital management on profitability: A case of listed

manufacturing firms in South Africa. Investment management and financial

innovations. 14(2). pp.336-346.

Maheshwari, S.N., Maheshwari, S.K. and Maheshwari, M.S.K., 2021. Principles of Management

Accounting. Sultan Chand & Sons.

Nariswari, T.N. and Nugraha, N.M., 2020. Profit Growth: Impact of Net Profit Margin, Gross

Profit Margin and Total Assests Turnover. International Journal of Finance & Banking

Studies (2147-4486). 9(4). pp.87-96.

Nuryani, Y. and Sunarsi, D., 2020. The Effect of Current Ratio and Debt to Equity Ratio on

Deviding Growth. JASa (Jurnal Akuntansi, Audit dan Sistem Informasi

Akuntansi). 4(2). pp.304-312.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.