Financial Decision Making Report: BM 414 for Panini Limited Analysis

VerifiedAdded on 2023/06/10

|12

|3727

|69

Report

AI Summary

This report analyzes the financial decision-making processes of Panini Limited, a medium-sized bread manufacturing company. Task 1 explores the roles of accounting and finance departments, including financial accounting, management accounting, tax, auditing, investment, financing, dividend, and working capital functions. It also details the sources of finance available to the company, such as retained earnings, equity, and debt. Task 2 involves a comprehensive ratio analysis, calculating and interpreting eight key financial ratios: gross profit margin, operating profit margin, return on capital employed (ROCE), current ratio, quick ratio, inventory turnover, debtor’s collection period, and creditor’s collection period. The analysis includes comparisons between 2018 and 2019 figures, reasons for changes, and suggestions for improvement, providing insights into the company's financial performance and areas for potential enhancement.

BM 414 Financial Decision Making Report

Cover Page

Word count range: (2250-2750)

Cover Page

Word count range: (2250-2750)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Contents

Introduction...........................................................................................................................................3

TASK 1....................................................................................................................................................3

Part a: Accounting and Finance departments....................................................................................3

Part b: Sources of finance..................................................................................................................5

TASK 2....................................................................................................................................................6

Part a: Calculation of the 8 ratios below using the correct formulas.................................................6

Part b: Individual analysis of each ratio based on the numerical results from part a........................7

Conclusion...........................................................................................................................................10

References...........................................................................................................................................12

Contents

Introduction...........................................................................................................................................3

TASK 1....................................................................................................................................................3

Part a: Accounting and Finance departments....................................................................................3

Part b: Sources of finance..................................................................................................................5

TASK 2....................................................................................................................................................6

Part a: Calculation of the 8 ratios below using the correct formulas.................................................6

Part b: Individual analysis of each ratio based on the numerical results from part a........................7

Conclusion...........................................................................................................................................10

References...........................................................................................................................................12

Introduction

Financial decision making means outlining the monetary position of the business and

helping out the organisation in problem solving. It also helps in making critical decisions for

the benefit of the company (Boucher, Jasinski and Tokpavi, 2021). The report accompanies

the company Panini Limited which established its business operations in 2016 and is

recognised as a medium sized business. The firm deals in manufacturing of the bread for the

supermarket in United Kingdom. The report consists of two Tasks. In task 1, the functions,

duties, and roles of an organisation which is related to accounting and finance will be

explained. Also, the sources of financing that helps in serving the expansion purpose for the

company are elaborated. In Task 2, the monetary ratios of the company will be computed and

then the performance and profitability of the firm will be analysed through it.

TASK 1

Part a: Accounting and Finance departments

For each of the below two departments, you need to provide a brief

introduction, before you proceed to the analysis of each function.

The following two departments along with their functions should be covered:

1. Accounting department: This can be defined as the gathering and assembling of

information relating to financial transactions in one location. The development of a

company's financials and the recording of business-related transactions. It is usually

interpreted as a mechanism for keeping proper records and utilising the information in

connected areas. The primary function of bookkeeping is to examine the appearance

of employees who are employed by the company in a similar environment. As a

result, it is also useful for assessing the location and productivity of businesses and

economies. It assesses the reasons for cash input and outflow in specific companies

(Fauziah, 2020). It is also recognised that it serves as a tool for those who are

associated with the firm or who want to get involved with business in a competitive

environment.

a) Financial accounting function:

Examine important transactions: Panini Ltd is required to record linked

exchanges that would result in an unmistakable and evident effect

recorded thus far after considering the operation of related company

within business environment.

Examine the serviced performance: Accounting is beneficial for having

a suitable investigation of Panini ltd firm that would assist the business

in managing connected life cycle for a certain time frame span that

Financial decision making means outlining the monetary position of the business and

helping out the organisation in problem solving. It also helps in making critical decisions for

the benefit of the company (Boucher, Jasinski and Tokpavi, 2021). The report accompanies

the company Panini Limited which established its business operations in 2016 and is

recognised as a medium sized business. The firm deals in manufacturing of the bread for the

supermarket in United Kingdom. The report consists of two Tasks. In task 1, the functions,

duties, and roles of an organisation which is related to accounting and finance will be

explained. Also, the sources of financing that helps in serving the expansion purpose for the

company are elaborated. In Task 2, the monetary ratios of the company will be computed and

then the performance and profitability of the firm will be analysed through it.

TASK 1

Part a: Accounting and Finance departments

For each of the below two departments, you need to provide a brief

introduction, before you proceed to the analysis of each function.

The following two departments along with their functions should be covered:

1. Accounting department: This can be defined as the gathering and assembling of

information relating to financial transactions in one location. The development of a

company's financials and the recording of business-related transactions. It is usually

interpreted as a mechanism for keeping proper records and utilising the information in

connected areas. The primary function of bookkeeping is to examine the appearance

of employees who are employed by the company in a similar environment. As a

result, it is also useful for assessing the location and productivity of businesses and

economies. It assesses the reasons for cash input and outflow in specific companies

(Fauziah, 2020). It is also recognised that it serves as a tool for those who are

associated with the firm or who want to get involved with business in a competitive

environment.

a) Financial accounting function:

Examine important transactions: Panini Ltd is required to record linked

exchanges that would result in an unmistakable and evident effect

recorded thus far after considering the operation of related company

within business environment.

Examine the serviced performance: Accounting is beneficial for having

a suitable investigation of Panini ltd firm that would assist the business

in managing connected life cycle for a certain time frame span that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

would be beneficial in combating a serious climate in the not-too-

distant future.

b) Management accounting function:

Maintains track of connected spending and compensation: It keeps

track of what is donated and what is purchased by the organisation. It

would aid Panini in comprehending the reasons for the creation of

earnings and pay by relevant capability, as well as which activities

should be regulated to aid in the further development of expenses

incurred during the operation and operation of the firm (Grossmann,

Mooney and Dugan, 2019).

Accounting assists in more effective and appealing navigation by

selecting the greatest optional options available through Panini Ltd. It

is also beneficial in determining what best meets the needs and

requirements of a linked firm over a period of time, as well as which

methods would be most effective in reducing costs and maximising

benefits during that time.

c) Tax function: All organisations under the supervision of the Department of

Finance must pay taxes. It focuses on maintaining a positive relationship with

the state by disbursing PAYE to the right authorities, as well as ensuring that

tax payments are made in accordance with established procedures.

d) Auditing function: The company's finance section focuses on current assets.

The company's working capital must be successfully managed in order to

generate more revenue in regards to the quantity of money invested, which

puts a greater strain on the company's liquidity.

2. Finance department: It states that funds that are limited in nature should be

managed in such a way that they serve the intended purpose and aims. It concentrates

on areas that contribute to the generation of cash and income that can be employed in

the company's ongoing activities (Kapesa, Kufakunesu and Cheza, 2021).

a) Investment function: The investment function is used to make money or earn

interest over a set period of time. The interest rate and investment have an

inverse connection. By boosting the manufacturing and purchasing of capital

goods, the investment function leads to the highest level of income and

productivity.

distant future.

b) Management accounting function:

Maintains track of connected spending and compensation: It keeps

track of what is donated and what is purchased by the organisation. It

would aid Panini in comprehending the reasons for the creation of

earnings and pay by relevant capability, as well as which activities

should be regulated to aid in the further development of expenses

incurred during the operation and operation of the firm (Grossmann,

Mooney and Dugan, 2019).

Accounting assists in more effective and appealing navigation by

selecting the greatest optional options available through Panini Ltd. It

is also beneficial in determining what best meets the needs and

requirements of a linked firm over a period of time, as well as which

methods would be most effective in reducing costs and maximising

benefits during that time.

c) Tax function: All organisations under the supervision of the Department of

Finance must pay taxes. It focuses on maintaining a positive relationship with

the state by disbursing PAYE to the right authorities, as well as ensuring that

tax payments are made in accordance with established procedures.

d) Auditing function: The company's finance section focuses on current assets.

The company's working capital must be successfully managed in order to

generate more revenue in regards to the quantity of money invested, which

puts a greater strain on the company's liquidity.

2. Finance department: It states that funds that are limited in nature should be

managed in such a way that they serve the intended purpose and aims. It concentrates

on areas that contribute to the generation of cash and income that can be employed in

the company's ongoing activities (Kapesa, Kufakunesu and Cheza, 2021).

a) Investment function: The investment function is used to make money or earn

interest over a set period of time. The interest rate and investment have an

inverse connection. By boosting the manufacturing and purchasing of capital

goods, the investment function leads to the highest level of income and

productivity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) Financing function: This function assists in decision-making and is used to

manage the company's finances. It denotes the receipt and use of monies

designated for efficient operations. Finance is the most significant aspect of

every business because it supplies the funds.

c) Dividend function: This role assists in the cash dividends to the company's

shareholders. The quantity of the dividend is decided by the general meeting

of shareholders. Dividends are payments provided by a firm to its shareholders

in exchange for their investment (Killingsworth, Mehany and Kim, 2021).

d) Working capital function: Working capital is the amount of money that a

company requires to decide how much money it needs to pay its short-term

debt obligations. If a company has enough operating capital, it will be capable

of paying its vendors and workforce.

Part b: Sources of finance

There are various techniques to obtaining funds that businesses employ to generate

assets and use them in the growth and advancement of commercial operations. Panini Limited

expands its business by investing in central activities.

Retained Earnings: It is the purchase of a business that remains after the loan

repayments have been paid and the profit payment to the investors has been paid.

These resources are mostly used to expand the company's business operations and

create new transactions. After evaluating all of the external variables that can

influence the organization's development, the following instance organisation has

utilised those assets in employee creative exercises and ensuring the firm's stability. It

aids organisations in managing assets without claiming any credit or providing value

to the general public without jeopardising their ownership (Kizar, 2022).

Equity: It is a different type of funding source that the organisation uses to raise

funds. In the following scenario, the organisation can raise assets without using

market advancements. By placing these assets into business activity to increase deals,

value helps to produce new assets. A necessary payment to investors is not required of

an organisation. It also puts a demand on good performance because the

administration must make efforts to increase the wealth of the investors.

Debt: It is the least costly source of finance that the corporation uses to obtain assets

through credit facilitators. In the following scenario, an organisation can use this

manage the company's finances. It denotes the receipt and use of monies

designated for efficient operations. Finance is the most significant aspect of

every business because it supplies the funds.

c) Dividend function: This role assists in the cash dividends to the company's

shareholders. The quantity of the dividend is decided by the general meeting

of shareholders. Dividends are payments provided by a firm to its shareholders

in exchange for their investment (Killingsworth, Mehany and Kim, 2021).

d) Working capital function: Working capital is the amount of money that a

company requires to decide how much money it needs to pay its short-term

debt obligations. If a company has enough operating capital, it will be capable

of paying its vendors and workforce.

Part b: Sources of finance

There are various techniques to obtaining funds that businesses employ to generate

assets and use them in the growth and advancement of commercial operations. Panini Limited

expands its business by investing in central activities.

Retained Earnings: It is the purchase of a business that remains after the loan

repayments have been paid and the profit payment to the investors has been paid.

These resources are mostly used to expand the company's business operations and

create new transactions. After evaluating all of the external variables that can

influence the organization's development, the following instance organisation has

utilised those assets in employee creative exercises and ensuring the firm's stability. It

aids organisations in managing assets without claiming any credit or providing value

to the general public without jeopardising their ownership (Kizar, 2022).

Equity: It is a different type of funding source that the organisation uses to raise

funds. In the following scenario, the organisation can raise assets without using

market advancements. By placing these assets into business activity to increase deals,

value helps to produce new assets. A necessary payment to investors is not required of

an organisation. It also puts a demand on good performance because the

administration must make efforts to increase the wealth of the investors.

Debt: It is the least costly source of finance that the corporation uses to obtain assets

through credit facilitators. In the following scenario, an organisation can use this

source of assets, and the owners of the securities are compensated a certain sum at

regular intervals. When compared to other forms of protection, it is seen as superior.

TASK 2

Part a: Calculation of the 8 ratios below using the correct formulas

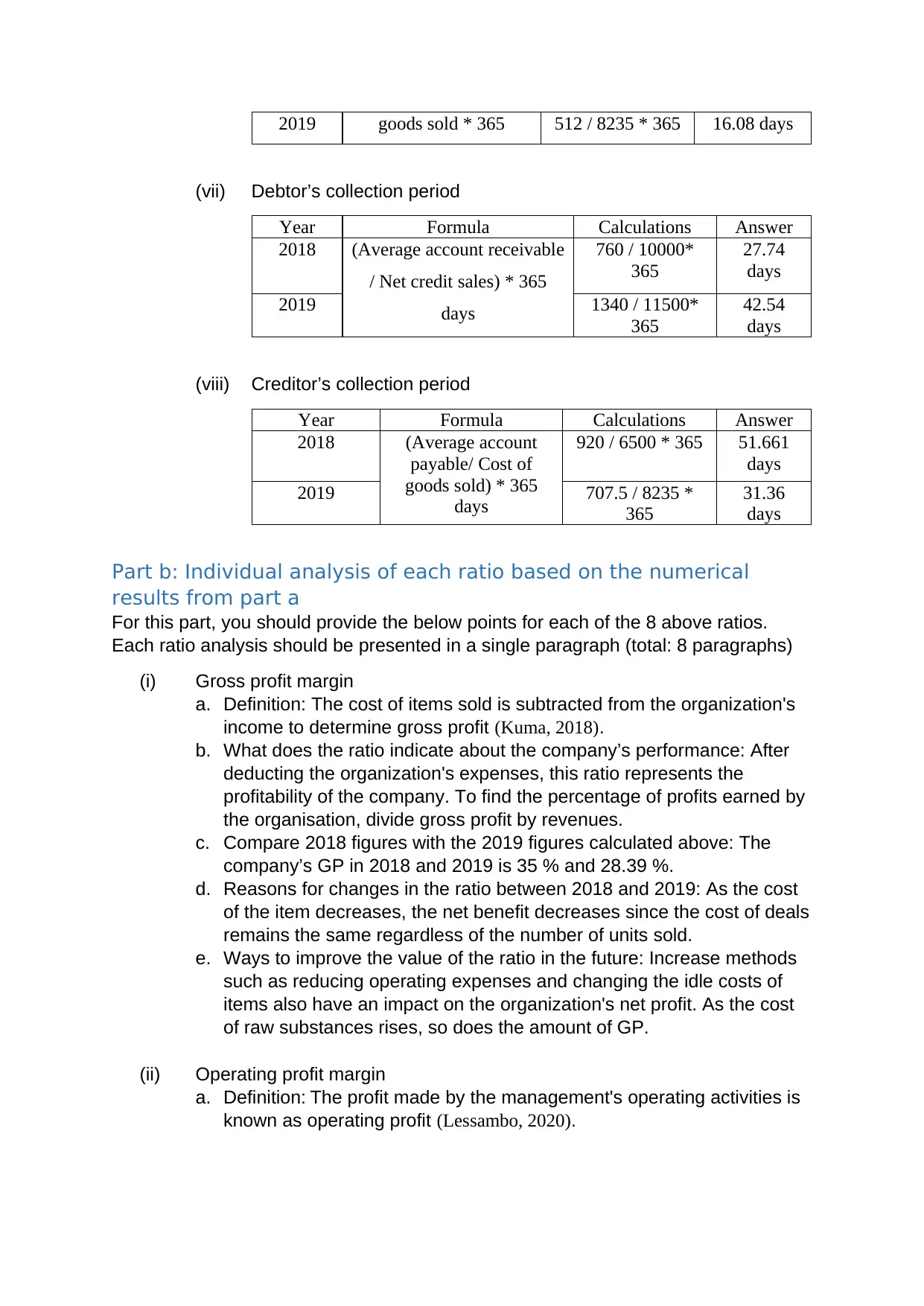

(i) Gross profit margin

Year Formula Calculations Answer

2018 Gross profit/ Net sales * 100 3500/10000 *

100

35%

2019 3265/ 11500 *

100

28.39%

(ii) Operating profit margin

Year Formula Calculations Answer

2018 Operating profit/ Net

sales * 100

2765 / 10000* 100 27.65%

2019 2305 / 11500* 100 20.04%

(iii) Return on capital employed (ROCE)

Year Formula Calculations Answer

2018 (Earnings before interest

and tax / Share equity +

Long term Liabilities) * 100

2765/ 8755 *

100

31.58%

2019 2305/ 10211*

100

22.57%

(iv) Current ratio

Year Formula Calculations Answer

2018 Current assets/ Current

liabilities

1175 / 970 1.211: 1

2019 2110 / 512 4.12: 1

(v) Quick ratio

Year Formula Calculations Answer

2018 Current assets – Inventory /

Current liabilities

1175 – 350/ 970 0.85: 1

2019 2110 – 675/ 512 2.80: 1

(vi) Inventory turnover days

Year Formula Calculations Answer

2018 Inventory / Cost of 350 / 6500 * 365 13.57 days

regular intervals. When compared to other forms of protection, it is seen as superior.

TASK 2

Part a: Calculation of the 8 ratios below using the correct formulas

(i) Gross profit margin

Year Formula Calculations Answer

2018 Gross profit/ Net sales * 100 3500/10000 *

100

35%

2019 3265/ 11500 *

100

28.39%

(ii) Operating profit margin

Year Formula Calculations Answer

2018 Operating profit/ Net

sales * 100

2765 / 10000* 100 27.65%

2019 2305 / 11500* 100 20.04%

(iii) Return on capital employed (ROCE)

Year Formula Calculations Answer

2018 (Earnings before interest

and tax / Share equity +

Long term Liabilities) * 100

2765/ 8755 *

100

31.58%

2019 2305/ 10211*

100

22.57%

(iv) Current ratio

Year Formula Calculations Answer

2018 Current assets/ Current

liabilities

1175 / 970 1.211: 1

2019 2110 / 512 4.12: 1

(v) Quick ratio

Year Formula Calculations Answer

2018 Current assets – Inventory /

Current liabilities

1175 – 350/ 970 0.85: 1

2019 2110 – 675/ 512 2.80: 1

(vi) Inventory turnover days

Year Formula Calculations Answer

2018 Inventory / Cost of 350 / 6500 * 365 13.57 days

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

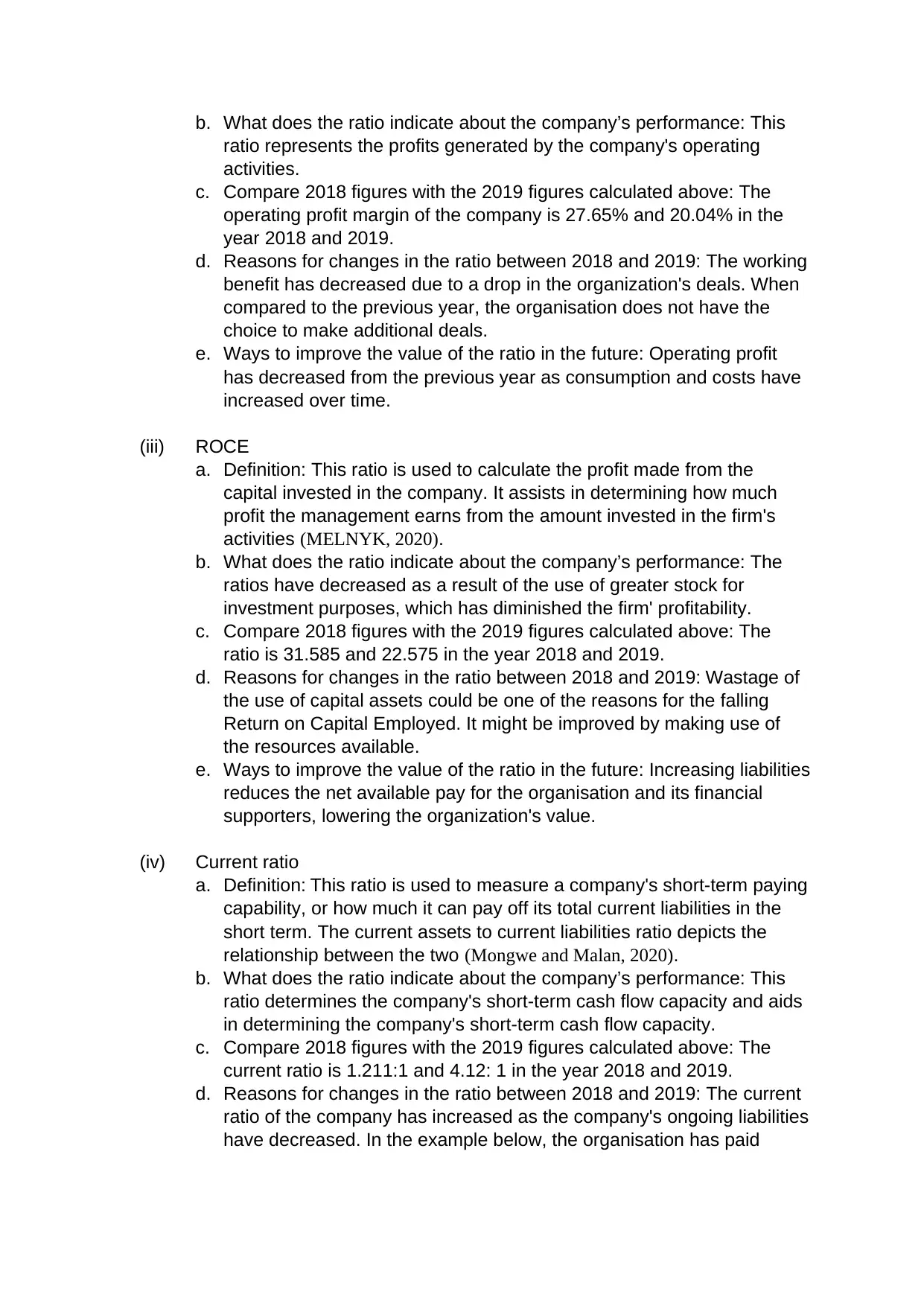

goods sold * 3652019 512 / 8235 * 365 16.08 days

(vii) Debtor’s collection period

Year Formula Calculations Answer

2018 (Average account receivable

/ Net credit sales) * 365

days

760 / 10000*

365

27.74

days

2019 1340 / 11500*

365

42.54

days

(viii) Creditor’s collection period

Year Formula Calculations Answer

2018 (Average account

payable/ Cost of

goods sold) * 365

days

920 / 6500 * 365 51.661

days

2019 707.5 / 8235 *

365

31.36

days

Part b: Individual analysis of each ratio based on the numerical

results from part a

For this part, you should provide the below points for each of the 8 above ratios.

Each ratio analysis should be presented in a single paragraph (total: 8 paragraphs)

(i) Gross profit margin

a. Definition: The cost of items sold is subtracted from the organization's

income to determine gross profit (Kuma, 2018).

b. What does the ratio indicate about the company’s performance: After

deducting the organization's expenses, this ratio represents the

profitability of the company. To find the percentage of profits earned by

the organisation, divide gross profit by revenues.

c. Compare 2018 figures with the 2019 figures calculated above: The

company’s GP in 2018 and 2019 is 35 % and 28.39 %.

d. Reasons for changes in the ratio between 2018 and 2019: As the cost

of the item decreases, the net benefit decreases since the cost of deals

remains the same regardless of the number of units sold.

e. Ways to improve the value of the ratio in the future: Increase methods

such as reducing operating expenses and changing the idle costs of

items also have an impact on the organization's net profit. As the cost

of raw substances rises, so does the amount of GP.

(ii) Operating profit margin

a. Definition: The profit made by the management's operating activities is

known as operating profit (Lessambo, 2020).

(vii) Debtor’s collection period

Year Formula Calculations Answer

2018 (Average account receivable

/ Net credit sales) * 365

days

760 / 10000*

365

27.74

days

2019 1340 / 11500*

365

42.54

days

(viii) Creditor’s collection period

Year Formula Calculations Answer

2018 (Average account

payable/ Cost of

goods sold) * 365

days

920 / 6500 * 365 51.661

days

2019 707.5 / 8235 *

365

31.36

days

Part b: Individual analysis of each ratio based on the numerical

results from part a

For this part, you should provide the below points for each of the 8 above ratios.

Each ratio analysis should be presented in a single paragraph (total: 8 paragraphs)

(i) Gross profit margin

a. Definition: The cost of items sold is subtracted from the organization's

income to determine gross profit (Kuma, 2018).

b. What does the ratio indicate about the company’s performance: After

deducting the organization's expenses, this ratio represents the

profitability of the company. To find the percentage of profits earned by

the organisation, divide gross profit by revenues.

c. Compare 2018 figures with the 2019 figures calculated above: The

company’s GP in 2018 and 2019 is 35 % and 28.39 %.

d. Reasons for changes in the ratio between 2018 and 2019: As the cost

of the item decreases, the net benefit decreases since the cost of deals

remains the same regardless of the number of units sold.

e. Ways to improve the value of the ratio in the future: Increase methods

such as reducing operating expenses and changing the idle costs of

items also have an impact on the organization's net profit. As the cost

of raw substances rises, so does the amount of GP.

(ii) Operating profit margin

a. Definition: The profit made by the management's operating activities is

known as operating profit (Lessambo, 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b. What does the ratio indicate about the company’s performance: This

ratio represents the profits generated by the company's operating

activities.

c. Compare 2018 figures with the 2019 figures calculated above: The

operating profit margin of the company is 27.65% and 20.04% in the

year 2018 and 2019.

d. Reasons for changes in the ratio between 2018 and 2019: The working

benefit has decreased due to a drop in the organization's deals. When

compared to the previous year, the organisation does not have the

choice to make additional deals.

e. Ways to improve the value of the ratio in the future: Operating profit

has decreased from the previous year as consumption and costs have

increased over time.

(iii) ROCE

a. Definition: This ratio is used to calculate the profit made from the

capital invested in the company. It assists in determining how much

profit the management earns from the amount invested in the firm's

activities (MELNYK, 2020).

b. What does the ratio indicate about the company’s performance: The

ratios have decreased as a result of the use of greater stock for

investment purposes, which has diminished the firm' profitability.

c. Compare 2018 figures with the 2019 figures calculated above: The

ratio is 31.585 and 22.575 in the year 2018 and 2019.

d. Reasons for changes in the ratio between 2018 and 2019: Wastage of

the use of capital assets could be one of the reasons for the falling

Return on Capital Employed. It might be improved by making use of

the resources available.

e. Ways to improve the value of the ratio in the future: Increasing liabilities

reduces the net available pay for the organisation and its financial

supporters, lowering the organization's value.

(iv) Current ratio

a. Definition: This ratio is used to measure a company's short-term paying

capability, or how much it can pay off its total current liabilities in the

short term. The current assets to current liabilities ratio depicts the

relationship between the two (Mongwe and Malan, 2020).

b. What does the ratio indicate about the company’s performance: This

ratio determines the company's short-term cash flow capacity and aids

in determining the company's short-term cash flow capacity.

c. Compare 2018 figures with the 2019 figures calculated above: The

current ratio is 1.211:1 and 4.12: 1 in the year 2018 and 2019.

d. Reasons for changes in the ratio between 2018 and 2019: The current

ratio of the company has increased as the company's ongoing liabilities

have decreased. In the example below, the organisation has paid

ratio represents the profits generated by the company's operating

activities.

c. Compare 2018 figures with the 2019 figures calculated above: The

operating profit margin of the company is 27.65% and 20.04% in the

year 2018 and 2019.

d. Reasons for changes in the ratio between 2018 and 2019: The working

benefit has decreased due to a drop in the organization's deals. When

compared to the previous year, the organisation does not have the

choice to make additional deals.

e. Ways to improve the value of the ratio in the future: Operating profit

has decreased from the previous year as consumption and costs have

increased over time.

(iii) ROCE

a. Definition: This ratio is used to calculate the profit made from the

capital invested in the company. It assists in determining how much

profit the management earns from the amount invested in the firm's

activities (MELNYK, 2020).

b. What does the ratio indicate about the company’s performance: The

ratios have decreased as a result of the use of greater stock for

investment purposes, which has diminished the firm' profitability.

c. Compare 2018 figures with the 2019 figures calculated above: The

ratio is 31.585 and 22.575 in the year 2018 and 2019.

d. Reasons for changes in the ratio between 2018 and 2019: Wastage of

the use of capital assets could be one of the reasons for the falling

Return on Capital Employed. It might be improved by making use of

the resources available.

e. Ways to improve the value of the ratio in the future: Increasing liabilities

reduces the net available pay for the organisation and its financial

supporters, lowering the organization's value.

(iv) Current ratio

a. Definition: This ratio is used to measure a company's short-term paying

capability, or how much it can pay off its total current liabilities in the

short term. The current assets to current liabilities ratio depicts the

relationship between the two (Mongwe and Malan, 2020).

b. What does the ratio indicate about the company’s performance: This

ratio determines the company's short-term cash flow capacity and aids

in determining the company's short-term cash flow capacity.

c. Compare 2018 figures with the 2019 figures calculated above: The

current ratio is 1.211:1 and 4.12: 1 in the year 2018 and 2019.

d. Reasons for changes in the ratio between 2018 and 2019: The current

ratio of the company has increased as the company's ongoing liabilities

have decreased. In the example below, the organisation has paid

current liabilities, reducing its liabilities and increasing the ongoing

ratio.

e. Ways to improve the value of the ratio in the future: Trade payables

and receivables management of the company has reduced its payables

while increasing its receivables, resulting in an increase in the current

ratio.

(v) Quick ratio

a. Definition: This ratio aids in analysing the company's liquidity condition.

By removing the company's anticipated expenses and inventory,

exiting liquidity is determined (Nadar and Wadhwa, 2019).

b. What does the ratio indicate about the company’s performance

c. Compare 2018 figures with the 2019 figures calculated above: the

quick ratio for both year 2018 and 2019 is 0.85: 1 and 2.80: 1.

d. Reasons for changes in the ratio between 2018 and 2019: sales

between companies have grown over time, resulting in an increase in

the fast ratio.

e. Ways to improve the value of the ratio in the future: During the last two

years, an increase in the organization's inventory has resulted in an

increase in the quick ratio.

(vi) Inventory turnover days

a. Definition: It assists in determining performance by dividing the

company's current assets and current liabilities.

b. What does the ratio indicate about the company’s performance: The

amount of times stock is spun in a year is determined by this ratio.It

aids in defining the sales that the company will be able to make in a

given period of time.

c. Compare 2018 figures with the 2019 figures calculated above: the

turnover ratio for both the years is 13.57 and 16.08 times.

d. Reasons for changes in the ratio between 2018 and 2019: A decrease

in the number of units sold or a growth in progress, both of which have

resulted in an increase in the turnover ratio.

e. Ways to improve the value of the ratio in the future: Because

executives are concerned with both excess and shortage deals, any

business should have the ability to regulate its outcome. As the cost of

purchasing unprocessed components per unit decreases, the company

may be able to obtain fresher resources for the same amount of

money, resulting in an increase in stock levels.

(vii) Debtor’s collection period

a. Definition: This ratio indicates how long it takes the company to figure

out how much money it owes to its debtors.

b. What does the ratio indicate about the company’s performance:

c. Compare 2018 figures with the 2019 figures calculated above: The

collection period by Panini ltd from its debtors is 27.74 and 42.54 days

in 2018 and 2019.

ratio.

e. Ways to improve the value of the ratio in the future: Trade payables

and receivables management of the company has reduced its payables

while increasing its receivables, resulting in an increase in the current

ratio.

(v) Quick ratio

a. Definition: This ratio aids in analysing the company's liquidity condition.

By removing the company's anticipated expenses and inventory,

exiting liquidity is determined (Nadar and Wadhwa, 2019).

b. What does the ratio indicate about the company’s performance

c. Compare 2018 figures with the 2019 figures calculated above: the

quick ratio for both year 2018 and 2019 is 0.85: 1 and 2.80: 1.

d. Reasons for changes in the ratio between 2018 and 2019: sales

between companies have grown over time, resulting in an increase in

the fast ratio.

e. Ways to improve the value of the ratio in the future: During the last two

years, an increase in the organization's inventory has resulted in an

increase in the quick ratio.

(vi) Inventory turnover days

a. Definition: It assists in determining performance by dividing the

company's current assets and current liabilities.

b. What does the ratio indicate about the company’s performance: The

amount of times stock is spun in a year is determined by this ratio.It

aids in defining the sales that the company will be able to make in a

given period of time.

c. Compare 2018 figures with the 2019 figures calculated above: the

turnover ratio for both the years is 13.57 and 16.08 times.

d. Reasons for changes in the ratio between 2018 and 2019: A decrease

in the number of units sold or a growth in progress, both of which have

resulted in an increase in the turnover ratio.

e. Ways to improve the value of the ratio in the future: Because

executives are concerned with both excess and shortage deals, any

business should have the ability to regulate its outcome. As the cost of

purchasing unprocessed components per unit decreases, the company

may be able to obtain fresher resources for the same amount of

money, resulting in an increase in stock levels.

(vii) Debtor’s collection period

a. Definition: This ratio indicates how long it takes the company to figure

out how much money it owes to its debtors.

b. What does the ratio indicate about the company’s performance:

c. Compare 2018 figures with the 2019 figures calculated above: The

collection period by Panini ltd from its debtors is 27.74 and 42.54 days

in 2018 and 2019.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

d. Reasons for changes in the ratio between 2018 and 2019: The Panini

group's efforts to collect money have dwindled, resulting in a longer

receivables collection period. As a result, conditions such as extending

receivables collection time have evolved.

e. Ways to improve the value of the ratio in the future: It is critical for any

business to correctly manage its credit strategy, as this will aid in

improving the instalment terms of assets obtained from the market,

allowing Panini ltd to flourish and grow in the economy.

(viii) Creditor’s collection period

a. Definition: This ratio defines the amount of time it takes management to

pay its creditors. The amount of days’ business costs to pay off its

debtors is likewise determined by this (Wellalage and Fernandez, 2019).

b. What does the ratio indicate about the company’s performance: This

ratio indicates that the time it takes to repay creditors has decreased,

implying that the amount will be paid more frequently.

c. Compare 2018 figures with the 2019 figures calculated above: The

collection time taken by the company in 2018 and 2019 is 51.6 and

31.6 days.

d. Reasons for changes in the ratio between 2018 and 2019: Late

payment to stock and material sellers and providers is one of several

aspects that contribute to Panini Ltd.'s dissolving payable repayment

period.

e. Ways to improve the value of the ratio in the future: the impact of a

shorter payment period is the deterioration of credit strategy and

financial situation. If Panini ltd should have an event that is more

dependent on expansion and development relatively soon, it is critical

for them to further develop their economic position and circumstances

in the ecosystem.

Conclusion

From the above-mentioned report, it is clear that finance and accounting will play an

important role in the organization's success. It has a variety of limitations, activities, and

commitments that have been chosen for more business creation over time. It also aids in

evaluating ongoing operations and anticipating future dangers. There are numerous extents

that are not totally fixed in stone that serve as a foundation for distinguishing current business

results from previous ones. It also serves as a guide for financial investors and management

to see if the organisation is progressing according to their expectations, and if not, what areas

need to be modified for better performance. It also aids in the evaluation and enhancement of

associations.

group's efforts to collect money have dwindled, resulting in a longer

receivables collection period. As a result, conditions such as extending

receivables collection time have evolved.

e. Ways to improve the value of the ratio in the future: It is critical for any

business to correctly manage its credit strategy, as this will aid in

improving the instalment terms of assets obtained from the market,

allowing Panini ltd to flourish and grow in the economy.

(viii) Creditor’s collection period

a. Definition: This ratio defines the amount of time it takes management to

pay its creditors. The amount of days’ business costs to pay off its

debtors is likewise determined by this (Wellalage and Fernandez, 2019).

b. What does the ratio indicate about the company’s performance: This

ratio indicates that the time it takes to repay creditors has decreased,

implying that the amount will be paid more frequently.

c. Compare 2018 figures with the 2019 figures calculated above: The

collection time taken by the company in 2018 and 2019 is 51.6 and

31.6 days.

d. Reasons for changes in the ratio between 2018 and 2019: Late

payment to stock and material sellers and providers is one of several

aspects that contribute to Panini Ltd.'s dissolving payable repayment

period.

e. Ways to improve the value of the ratio in the future: the impact of a

shorter payment period is the deterioration of credit strategy and

financial situation. If Panini ltd should have an event that is more

dependent on expansion and development relatively soon, it is critical

for them to further develop their economic position and circumstances

in the ecosystem.

Conclusion

From the above-mentioned report, it is clear that finance and accounting will play an

important role in the organization's success. It has a variety of limitations, activities, and

commitments that have been chosen for more business creation over time. It also aids in

evaluating ongoing operations and anticipating future dangers. There are numerous extents

that are not totally fixed in stone that serve as a foundation for distinguishing current business

results from previous ones. It also serves as a guide for financial investors and management

to see if the organisation is progressing according to their expectations, and if not, what areas

need to be modified for better performance. It also aids in the evaluation and enhancement of

associations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Boucher, C., Jasinski, A. and Tokpavi, S., 2021. Conditional Mean Reversion of Financial

Ratios and the Predictability of Returns. Available at SSRN 3983094.

Fauziah, N., 2020. The Effect of Financial Ratios, Market Return, and Macroeconomic

Factors (Doctoral dissertation, Sekolah Tinggi Manajemen IPMI).

Grossmann, A., Mooney, L. and Dugan, M., 2019. Inclusion fairness in accounting, finance,

and management: An investigation of A-star publications on the ABDC journal

list. Journal of Business Research, 95, pp.232-241.

Kapesa, T., Kufakunesu, F. and Cheza, A., 2021. Financing the ‘working of talents’

Ventures: The Role of Innovative Finance. In Matarenda/Talents in Zimbabwean

Pentecostalism (pp. 49-75). Brill.

Killingsworth, J., Mehany, M.H. and Kim, J., 2021. Using accounting ratios to measure

construction industry lag. Journal of Financial Management of Property and

Construction.

Kizar, N., 2022. The predictive content of financial ratios and macroeconomic factors for

stock return in the EU Stock Market.

Kuma, B., 2018. Insurance Industry and its Financial Ratios. International Journal of

Research in Social Sciences, 8(10), pp.588-592.

Lessambo, F.I., 2020. Commercial Bank’s Financial Ratios Analysis. In The US Banking

System (pp. 259-275). Palgrave Macmillan, Cham.

MELNYK, K., 2020. Institutional Aspects of Choice and Application of Audit

Procedures. Accounting & Finance/Oblik i Finansi, (89).

Mongwe, W.T. and Malan, K.M., 2020, December. The efficacy of financial ratios for fraud

detection using self organising maps. In 2020 IEEE Symposium Series on

Computational Intelligence (SSCI) (pp. 1100-1106). IEEE.

Nadar, D.S. and Wadhwa, B., 2019. Theoretical review of the role of financial

ratios. Available at SSRN 3472673.

Wellalage, N.H. and Fernandez, V., 2019. Innovation and SME finance: Evidence from

developing countries. International Review of Financial Analysis, 66, p.101370.

Boucher, C., Jasinski, A. and Tokpavi, S., 2021. Conditional Mean Reversion of Financial

Ratios and the Predictability of Returns. Available at SSRN 3983094.

Fauziah, N., 2020. The Effect of Financial Ratios, Market Return, and Macroeconomic

Factors (Doctoral dissertation, Sekolah Tinggi Manajemen IPMI).

Grossmann, A., Mooney, L. and Dugan, M., 2019. Inclusion fairness in accounting, finance,

and management: An investigation of A-star publications on the ABDC journal

list. Journal of Business Research, 95, pp.232-241.

Kapesa, T., Kufakunesu, F. and Cheza, A., 2021. Financing the ‘working of talents’

Ventures: The Role of Innovative Finance. In Matarenda/Talents in Zimbabwean

Pentecostalism (pp. 49-75). Brill.

Killingsworth, J., Mehany, M.H. and Kim, J., 2021. Using accounting ratios to measure

construction industry lag. Journal of Financial Management of Property and

Construction.

Kizar, N., 2022. The predictive content of financial ratios and macroeconomic factors for

stock return in the EU Stock Market.

Kuma, B., 2018. Insurance Industry and its Financial Ratios. International Journal of

Research in Social Sciences, 8(10), pp.588-592.

Lessambo, F.I., 2020. Commercial Bank’s Financial Ratios Analysis. In The US Banking

System (pp. 259-275). Palgrave Macmillan, Cham.

MELNYK, K., 2020. Institutional Aspects of Choice and Application of Audit

Procedures. Accounting & Finance/Oblik i Finansi, (89).

Mongwe, W.T. and Malan, K.M., 2020, December. The efficacy of financial ratios for fraud

detection using self organising maps. In 2020 IEEE Symposium Series on

Computational Intelligence (SSCI) (pp. 1100-1106). IEEE.

Nadar, D.S. and Wadhwa, B., 2019. Theoretical review of the role of financial

ratios. Available at SSRN 3472673.

Wellalage, N.H. and Fernandez, V., 2019. Innovation and SME finance: Evidence from

developing countries. International Review of Financial Analysis, 66, p.101370.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.