Big Machine Limited Miller Yates Howarth Audit Report Analysis

VerifiedAdded on 2021/06/14

|15

|2832

|247

Report

AI Summary

This report is an audit and assurance services report for Big Machine Limited, analyzing financial statements, audit risks, and internal controls. The report examines key accounts like plant and equipment, accounts receivable, lease income, and financial liabilities, using ratio analysis and assessing the current internal control system. It identifies business risks such as strong competition, downtime in the mining industry, and weak internal systems. The report proposes internal control measures to mitigate risks and improve system efficiency, including detailed audit steps to reduce identified risks associated with each account. Furthermore, the report analyzes the company's financial health, evaluates the effectiveness of the internal control system, and lists weaknesses in the contract payroll system. This report provides valuable insights into the financial health and operational challenges faced by Big Machine Limited.

Big Machine Limited

Miller Yates Howarth

Audit Planning and Internal Control

2nd May, 2018

1

Miller Yates Howarth

Audit Planning and Internal Control

2nd May, 2018

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report has basically referenced to the audit and assurance services provided by an

auditor to a business organization. There are many parts of an audit and some part has been

covered in the below report. The report is for Big Machinery Limited whose audit has been

conducted and various things related to the audit has explained. There are different external

environment factors that affect the business operation of Big Machinery Limited. There are some

issues like strong competition, downtime in mining industry and weak internal system that the

company is facing. Various accounts related to audit has been demonstrated in the report and

steps are mentioned to reduce the same. There are four accounts that are considered- Plant and

equipment, machinery accounts receivable, lease income and financial liabilities. An analysis has

been done and for the same audit risk, ratio analysis and current internal control system has been

calculated in order to find out the results. This organization is facing business risk and this has

been concluded in this report. This report also includes proposed internal control measures that

can be easily implement and control the system to test them.

2

This report has basically referenced to the audit and assurance services provided by an

auditor to a business organization. There are many parts of an audit and some part has been

covered in the below report. The report is for Big Machinery Limited whose audit has been

conducted and various things related to the audit has explained. There are different external

environment factors that affect the business operation of Big Machinery Limited. There are some

issues like strong competition, downtime in mining industry and weak internal system that the

company is facing. Various accounts related to audit has been demonstrated in the report and

steps are mentioned to reduce the same. There are four accounts that are considered- Plant and

equipment, machinery accounts receivable, lease income and financial liabilities. An analysis has

been done and for the same audit risk, ratio analysis and current internal control system has been

calculated in order to find out the results. This organization is facing business risk and this has

been concluded in this report. This report also includes proposed internal control measures that

can be easily implement and control the system to test them.

2

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Question 1 A:...................................................................................................................................4

Question 1 B: Analyse the ratios and additional information to outline the business risks that

BML faces........................................................................................................................................4

Question 2 A:...................................................................................................................................5

Question 2 B: List and identify the weaknesses in internal control for contract payroll.................5

Conclusion.......................................................................................................................................6

References........................................................................................................................................7

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Question 1 A:...................................................................................................................................4

Question 1 B: Analyse the ratios and additional information to outline the business risks that

BML faces........................................................................................................................................4

Question 2 A:...................................................................................................................................5

Question 2 B: List and identify the weaknesses in internal control for contract payroll.................5

Conclusion.......................................................................................................................................6

References........................................................................................................................................7

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

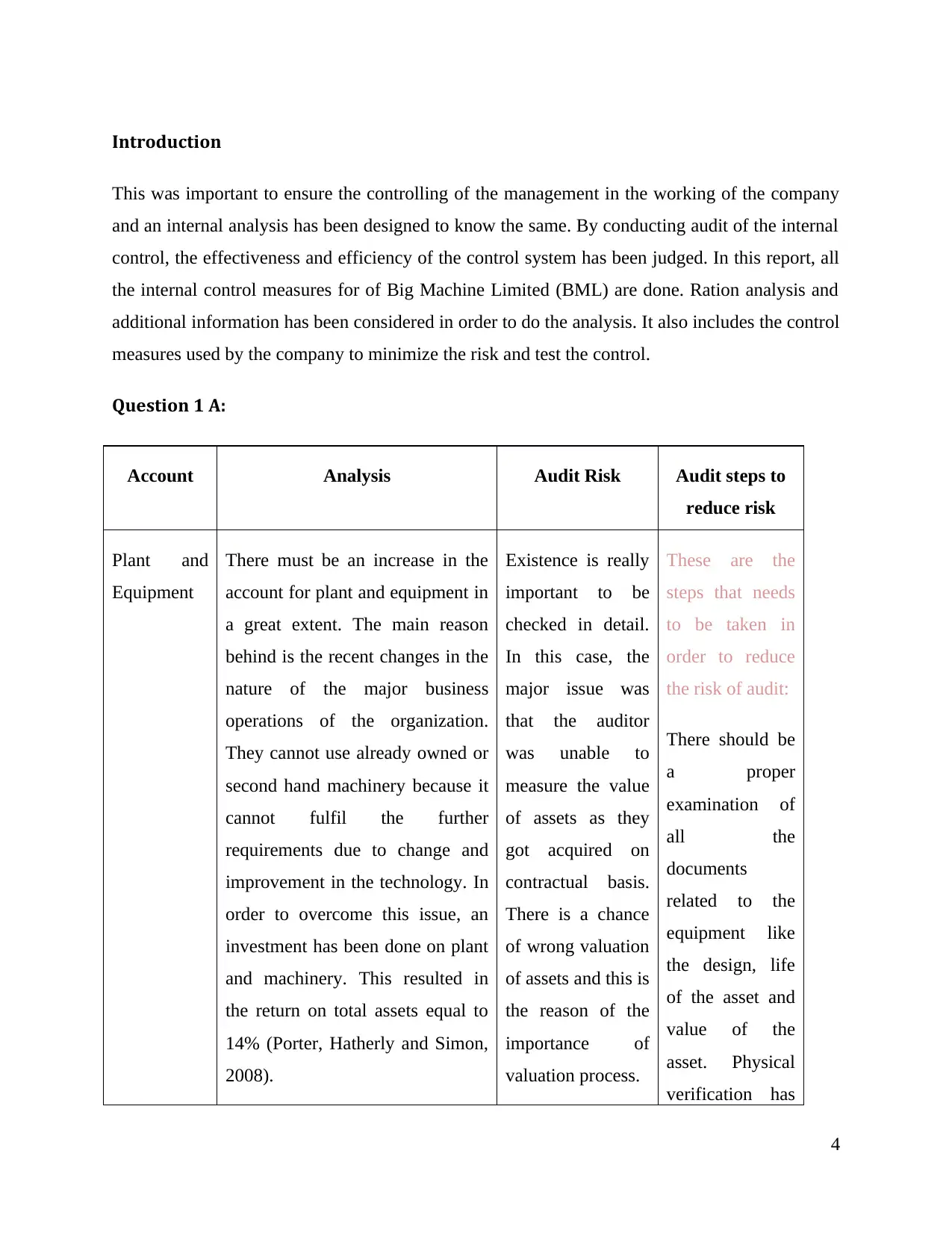

Introduction

This was important to ensure the controlling of the management in the working of the company

and an internal analysis has been designed to know the same. By conducting audit of the internal

control, the effectiveness and efficiency of the control system has been judged. In this report, all

the internal control measures for of Big Machine Limited (BML) are done. Ration analysis and

additional information has been considered in order to do the analysis. It also includes the control

measures used by the company to minimize the risk and test the control.

Question 1 A:

Account Analysis Audit Risk Audit steps to

reduce risk

Plant and

Equipment

There must be an increase in the

account for plant and equipment in

a great extent. The main reason

behind is the recent changes in the

nature of the major business

operations of the organization.

They cannot use already owned or

second hand machinery because it

cannot fulfil the further

requirements due to change and

improvement in the technology. In

order to overcome this issue, an

investment has been done on plant

and machinery. This resulted in

the return on total assets equal to

14% (Porter, Hatherly and Simon,

2008).

Existence is really

important to be

checked in detail.

In this case, the

major issue was

that the auditor

was unable to

measure the value

of assets as they

got acquired on

contractual basis.

There is a chance

of wrong valuation

of assets and this is

the reason of the

importance of

valuation process.

These are the

steps that needs

to be taken in

order to reduce

the risk of audit:

There should be

a proper

examination of

all the

documents

related to the

equipment like

the design, life

of the asset and

value of the

asset. Physical

verification has

4

This was important to ensure the controlling of the management in the working of the company

and an internal analysis has been designed to know the same. By conducting audit of the internal

control, the effectiveness and efficiency of the control system has been judged. In this report, all

the internal control measures for of Big Machine Limited (BML) are done. Ration analysis and

additional information has been considered in order to do the analysis. It also includes the control

measures used by the company to minimize the risk and test the control.

Question 1 A:

Account Analysis Audit Risk Audit steps to

reduce risk

Plant and

Equipment

There must be an increase in the

account for plant and equipment in

a great extent. The main reason

behind is the recent changes in the

nature of the major business

operations of the organization.

They cannot use already owned or

second hand machinery because it

cannot fulfil the further

requirements due to change and

improvement in the technology. In

order to overcome this issue, an

investment has been done on plant

and machinery. This resulted in

the return on total assets equal to

14% (Porter, Hatherly and Simon,

2008).

Existence is really

important to be

checked in detail.

In this case, the

major issue was

that the auditor

was unable to

measure the value

of assets as they

got acquired on

contractual basis.

There is a chance

of wrong valuation

of assets and this is

the reason of the

importance of

valuation process.

These are the

steps that needs

to be taken in

order to reduce

the risk of audit:

There should be

a proper

examination of

all the

documents

related to the

equipment like

the design, life

of the asset and

value of the

asset. Physical

verification has

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to be done for

the fixed assets

of the company

to check their

existence and

proper valuation

of the same.

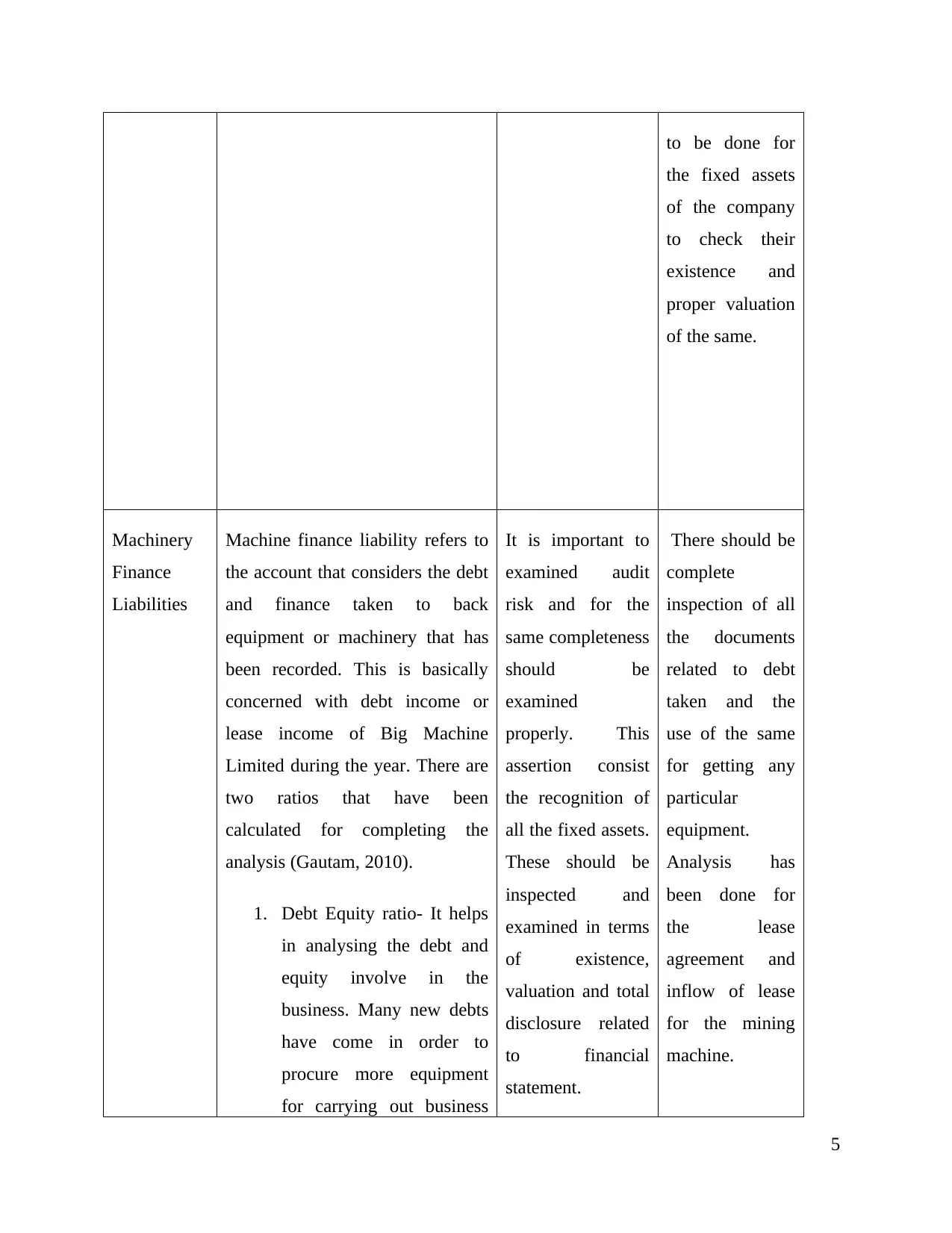

Machinery

Finance

Liabilities

Machine finance liability refers to

the account that considers the debt

and finance taken to back

equipment or machinery that has

been recorded. This is basically

concerned with debt income or

lease income of Big Machine

Limited during the year. There are

two ratios that have been

calculated for completing the

analysis (Gautam, 2010).

1. Debt Equity ratio- It helps

in analysing the debt and

equity involve in the

business. Many new debts

have come in order to

procure more equipment

for carrying out business

It is important to

examined audit

risk and for the

same completeness

should be

examined

properly. This

assertion consist

the recognition of

all the fixed assets.

These should be

inspected and

examined in terms

of existence,

valuation and total

disclosure related

to financial

statement.

There should be

complete

inspection of all

the documents

related to debt

taken and the

use of the same

for getting any

particular

equipment.

Analysis has

been done for

the lease

agreement and

inflow of lease

for the mining

machine.

5

the fixed assets

of the company

to check their

existence and

proper valuation

of the same.

Machinery

Finance

Liabilities

Machine finance liability refers to

the account that considers the debt

and finance taken to back

equipment or machinery that has

been recorded. This is basically

concerned with debt income or

lease income of Big Machine

Limited during the year. There are

two ratios that have been

calculated for completing the

analysis (Gautam, 2010).

1. Debt Equity ratio- It helps

in analysing the debt and

equity involve in the

business. Many new debts

have come in order to

procure more equipment

for carrying out business

It is important to

examined audit

risk and for the

same completeness

should be

examined

properly. This

assertion consist

the recognition of

all the fixed assets.

These should be

inspected and

examined in terms

of existence,

valuation and total

disclosure related

to financial

statement.

There should be

complete

inspection of all

the documents

related to debt

taken and the

use of the same

for getting any

particular

equipment.

Analysis has

been done for

the lease

agreement and

inflow of lease

for the mining

machine.

5

operations. So, there is a

change in debt equity ratio

but it is still according to

the expected level.

2. Profit/ Lease income ratio-

It is a ratio that helps in

analysing the part of lease

income in the overall profit

of Big Machine Limited.

There is an increase in

lease income for the

current year and it is

currently it should situate

at a higher level but it is

showing on a position of

moderate level (Apreda,.

2010).

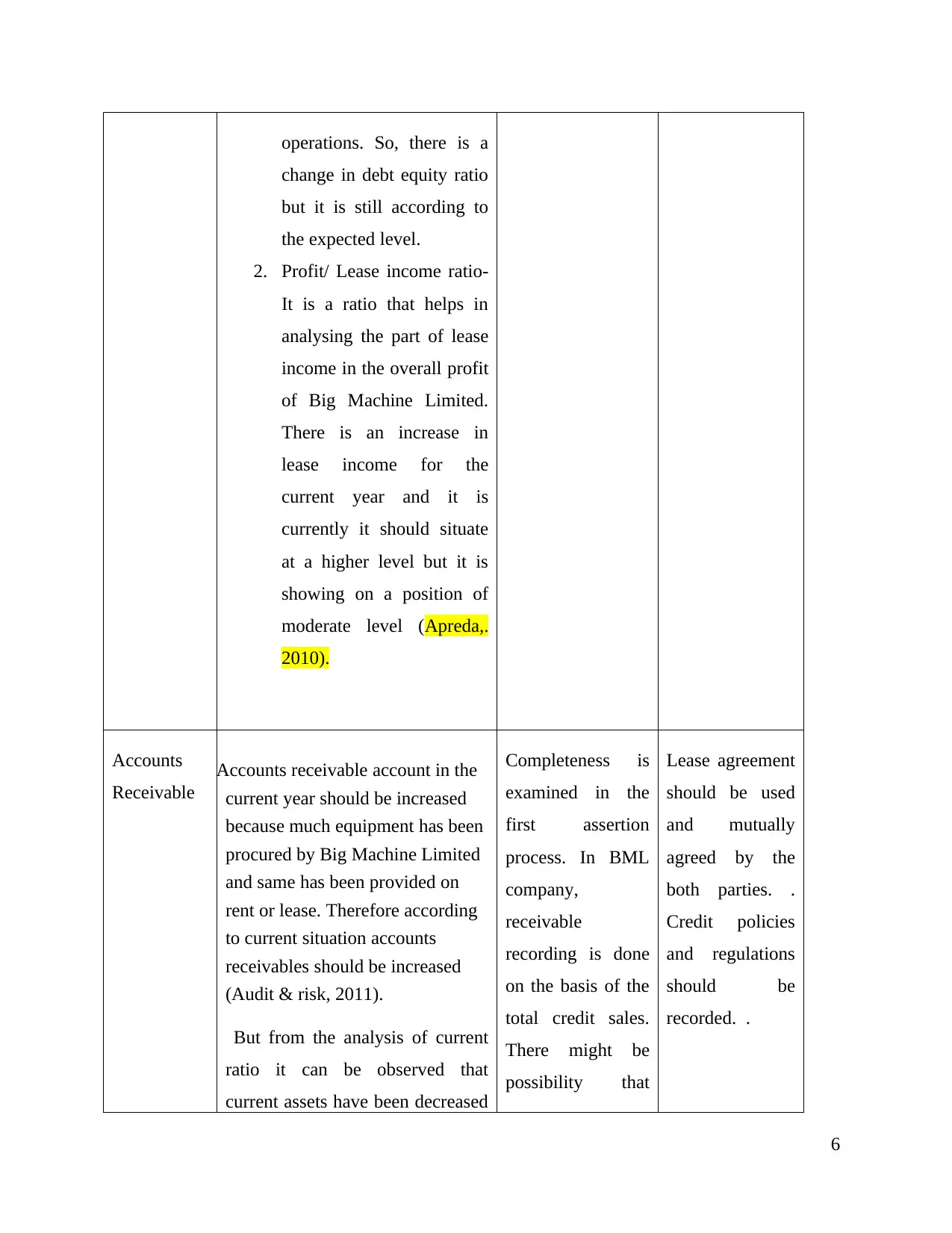

Accounts

Receivable

Accounts receivable account in the

current year should be increased

because much equipment has been

procured by Big Machine Limited

and same has been provided on

rent or lease. Therefore according

to current situation accounts

receivables should be increased

(Audit & risk, 2011).

But from the analysis of current

ratio it can be observed that

current assets have been decreased

Completeness is

examined in the

first assertion

process. In BML

company,

receivable

recording is done

on the basis of the

total credit sales.

There might be

possibility that

Lease agreement

should be used

and mutually

agreed by the

both parties. .

Credit policies

and regulations

should be

recorded. .

6

change in debt equity ratio

but it is still according to

the expected level.

2. Profit/ Lease income ratio-

It is a ratio that helps in

analysing the part of lease

income in the overall profit

of Big Machine Limited.

There is an increase in

lease income for the

current year and it is

currently it should situate

at a higher level but it is

showing on a position of

moderate level (Apreda,.

2010).

Accounts

Receivable

Accounts receivable account in the

current year should be increased

because much equipment has been

procured by Big Machine Limited

and same has been provided on

rent or lease. Therefore according

to current situation accounts

receivables should be increased

(Audit & risk, 2011).

But from the analysis of current

ratio it can be observed that

current assets have been decreased

Completeness is

examined in the

first assertion

process. In BML

company,

receivable

recording is done

on the basis of the

total credit sales.

There might be

possibility that

Lease agreement

should be used

and mutually

agreed by the

both parties. .

Credit policies

and regulations

should be

recorded. .

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as compared to last year. Therefor

there may be some misstatement in

accounts receivables account.

Current ratio includes accounts

receivables under current assets

part and according to changed

business operations current ratio

should be at higher side.

The lease agreement in the debtors

and BML should be based on the

entered contract. There is

possibility of the material mis-

statement in the recording of the

debts and other liabilities.

recording

procedure may

neglect the

transactions of the

receivables and

equipment sales.

Lease

income

Lease income is recorded as

capital revenue in the books of

accounts of the BML.

Recording of the lease income is

done as per the accounting rules

and regulation.

There should be a higher side of

the profits earned by lease income

but according to the ratios it is

showing low profits. So, there is a

possibility of a major misstatement

in this account (Elder, Beasley, &

Arenas, (2011).

Accuracy is the

main concern

while doing the

analysis and

auditing of

financial

statements. The

correctness of

lease income will

be checked under

this assertion

(Standover, 2017).

An analysis of

lease agreement

in a detailed way

has been done.

The amount

shown in lease

income should

be verified or a

cross checking

has been done

with the external

confirmation

team and lease

agreements.

Lease income

7

there may be some misstatement in

accounts receivables account.

Current ratio includes accounts

receivables under current assets

part and according to changed

business operations current ratio

should be at higher side.

The lease agreement in the debtors

and BML should be based on the

entered contract. There is

possibility of the material mis-

statement in the recording of the

debts and other liabilities.

recording

procedure may

neglect the

transactions of the

receivables and

equipment sales.

Lease

income

Lease income is recorded as

capital revenue in the books of

accounts of the BML.

Recording of the lease income is

done as per the accounting rules

and regulation.

There should be a higher side of

the profits earned by lease income

but according to the ratios it is

showing low profits. So, there is a

possibility of a major misstatement

in this account (Elder, Beasley, &

Arenas, (2011).

Accuracy is the

main concern

while doing the

analysis and

auditing of

financial

statements. The

correctness of

lease income will

be checked under

this assertion

(Standover, 2017).

An analysis of

lease agreement

in a detailed way

has been done.

The amount

shown in lease

income should

be verified or a

cross checking

has been done

with the external

confirmation

team and lease

agreements.

Lease income

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The gross margin of the company

has shown a static result if we

compare the same to the last year’s

figures. But there should be a

decline in the gross profit margin

according to the current scenario

of the business. Big Machine

Limited is facing so many issues

but still they are capable of

generating an appropriate profit is

not a realistic situation.

should be

calculated in

terms of the date

of receiving and

amount

mentioned in

lease agreement

(Developing an

audit trail,

2008).

Question 1 B: Analyse the ratios and additional information to outline the business

risks that BML faces.

After the completion of analysis regarding the actual position of Big Machine Limited, the ratios

has been calculated and some risks are determined that can interrupt the working of the

organization (Mainardi, 2011).

Return on Assets- It has been concluded that the overall return on total asset has decreased and

the reason for the same is the increase in fixed assets. Profits earned by using the same assets are

known as return on assets. There is a chance to maintain the returns normal the options for the

same were sale of fixed assets and hike in profits. These results are in the low business expansion

as well as low investments done by investors (Gay, & Simnett, 2015).

Downtime in mining industry- There is a downtime in the mining industry as per discussed and

this is the reason for the shutdown of many companies. There are strict implications of the

government in the mining industry and due to this many companies are going back from this

business (Demina, Larionova and Chinaeva, 2017).

8

has shown a static result if we

compare the same to the last year’s

figures. But there should be a

decline in the gross profit margin

according to the current scenario

of the business. Big Machine

Limited is facing so many issues

but still they are capable of

generating an appropriate profit is

not a realistic situation.

should be

calculated in

terms of the date

of receiving and

amount

mentioned in

lease agreement

(Developing an

audit trail,

2008).

Question 1 B: Analyse the ratios and additional information to outline the business

risks that BML faces.

After the completion of analysis regarding the actual position of Big Machine Limited, the ratios

has been calculated and some risks are determined that can interrupt the working of the

organization (Mainardi, 2011).

Return on Assets- It has been concluded that the overall return on total asset has decreased and

the reason for the same is the increase in fixed assets. Profits earned by using the same assets are

known as return on assets. There is a chance to maintain the returns normal the options for the

same were sale of fixed assets and hike in profits. These results are in the low business expansion

as well as low investments done by investors (Gay, & Simnett, 2015).

Downtime in mining industry- There is a downtime in the mining industry as per discussed and

this is the reason for the shutdown of many companies. There are strict implications of the

government in the mining industry and due to this many companies are going back from this

business (Demina, Larionova and Chinaeva, 2017).

8

Change in the metal market- there is a major change in the market of metal and this created an

impact on the business of BML. Due to the same, there was a drop in the rates of the metals. All

these fluctuations on the market and industry have impacted the business operation of BML.

Unstable receivables credit policy- It has been observed while analysing efficiency ratio that the

money taken by the debtors is more. It shows the low availability of cash in the business

organisation (O'Donnell, Arnold, & Sutton, (2010).

9

impact on the business of BML. Due to the same, there was a drop in the rates of the metals. All

these fluctuations on the market and industry have impacted the business operation of BML.

Unstable receivables credit policy- It has been observed while analysing efficiency ratio that the

money taken by the debtors is more. It shows the low availability of cash in the business

organisation (O'Donnell, Arnold, & Sutton, (2010).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

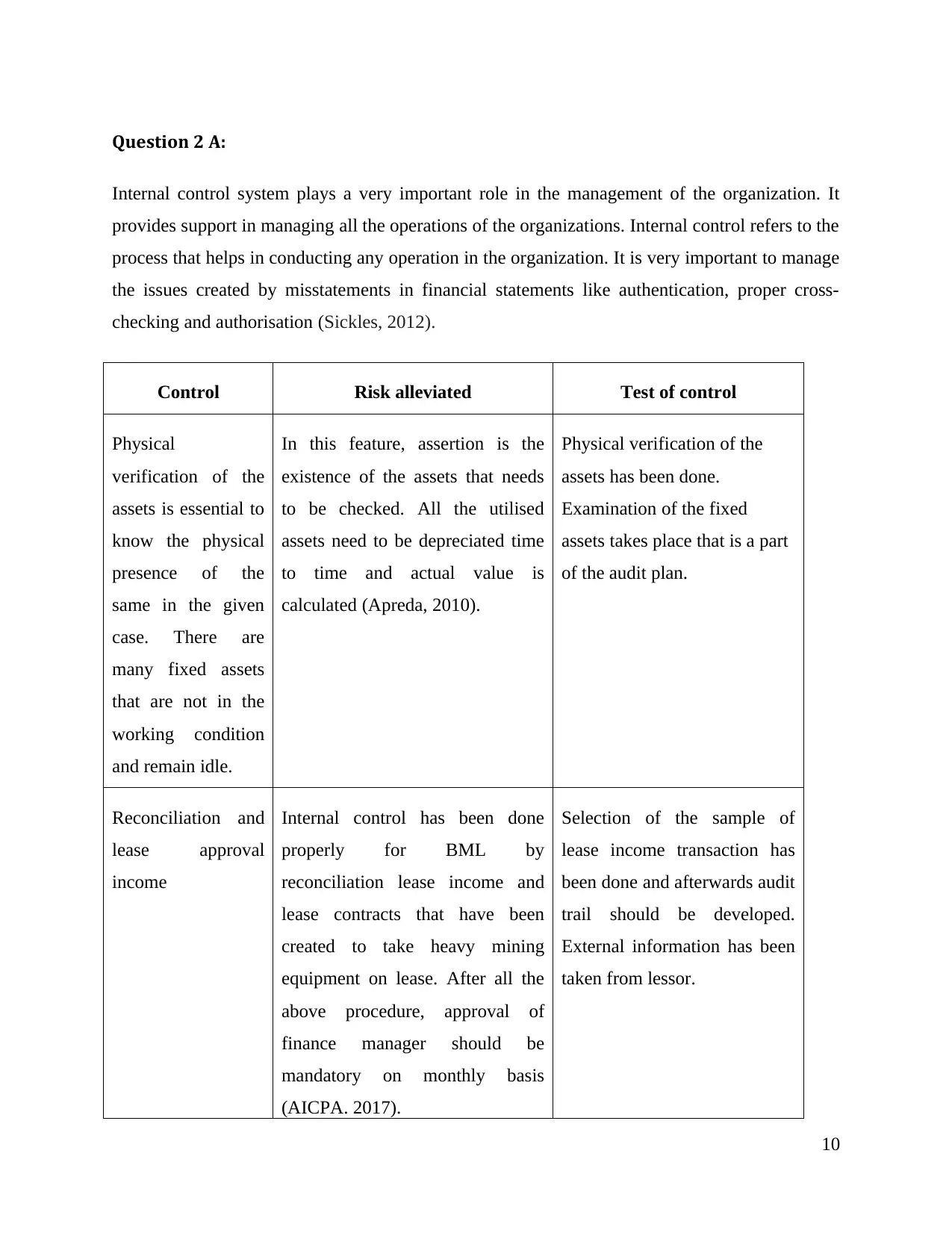

Question 2 A:

Internal control system plays a very important role in the management of the organization. It

provides support in managing all the operations of the organizations. Internal control refers to the

process that helps in conducting any operation in the organization. It is very important to manage

the issues created by misstatements in financial statements like authentication, proper cross-

checking and authorisation (Sickles, 2012).

Control Risk alleviated Test of control

Physical

verification of the

assets is essential to

know the physical

presence of the

same in the given

case. There are

many fixed assets

that are not in the

working condition

and remain idle.

In this feature, assertion is the

existence of the assets that needs

to be checked. All the utilised

assets need to be depreciated time

to time and actual value is

calculated (Apreda, 2010).

Physical verification of the

assets has been done.

Examination of the fixed

assets takes place that is a part

of the audit plan.

Reconciliation and

lease approval

income

Internal control has been done

properly for BML by

reconciliation lease income and

lease contracts that have been

created to take heavy mining

equipment on lease. After all the

above procedure, approval of

finance manager should be

mandatory on monthly basis

(AICPA. 2017).

Selection of the sample of

lease income transaction has

been done and afterwards audit

trail should be developed.

External information has been

taken from lessor.

10

Internal control system plays a very important role in the management of the organization. It

provides support in managing all the operations of the organizations. Internal control refers to the

process that helps in conducting any operation in the organization. It is very important to manage

the issues created by misstatements in financial statements like authentication, proper cross-

checking and authorisation (Sickles, 2012).

Control Risk alleviated Test of control

Physical

verification of the

assets is essential to

know the physical

presence of the

same in the given

case. There are

many fixed assets

that are not in the

working condition

and remain idle.

In this feature, assertion is the

existence of the assets that needs

to be checked. All the utilised

assets need to be depreciated time

to time and actual value is

calculated (Apreda, 2010).

Physical verification of the

assets has been done.

Examination of the fixed

assets takes place that is a part

of the audit plan.

Reconciliation and

lease approval

income

Internal control has been done

properly for BML by

reconciliation lease income and

lease contracts that have been

created to take heavy mining

equipment on lease. After all the

above procedure, approval of

finance manager should be

mandatory on monthly basis

(AICPA. 2017).

Selection of the sample of

lease income transaction has

been done and afterwards audit

trail should be developed.

External information has been

taken from lessor.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

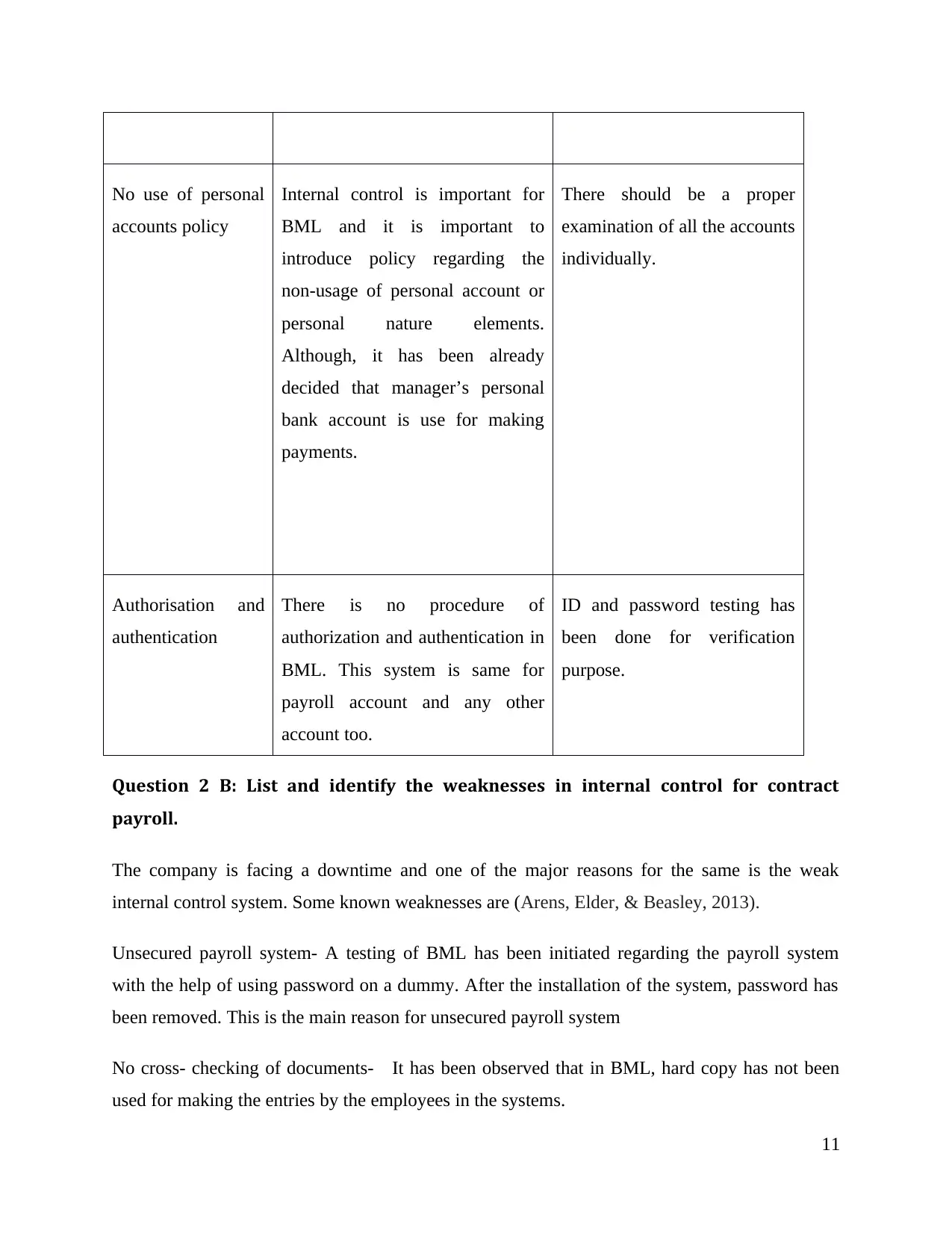

No use of personal

accounts policy

Internal control is important for

BML and it is important to

introduce policy regarding the

non-usage of personal account or

personal nature elements.

Although, it has been already

decided that manager’s personal

bank account is use for making

payments.

There should be a proper

examination of all the accounts

individually.

Authorisation and

authentication

There is no procedure of

authorization and authentication in

BML. This system is same for

payroll account and any other

account too.

ID and password testing has

been done for verification

purpose.

Question 2 B: List and identify the weaknesses in internal control for contract

payroll.

The company is facing a downtime and one of the major reasons for the same is the weak

internal control system. Some known weaknesses are (Arens, Elder, & Beasley, 2013).

Unsecured payroll system- A testing of BML has been initiated regarding the payroll system

with the help of using password on a dummy. After the installation of the system, password has

been removed. This is the main reason for unsecured payroll system

No cross- checking of documents- It has been observed that in BML, hard copy has not been

used for making the entries by the employees in the systems.

11

accounts policy

Internal control is important for

BML and it is important to

introduce policy regarding the

non-usage of personal account or

personal nature elements.

Although, it has been already

decided that manager’s personal

bank account is use for making

payments.

There should be a proper

examination of all the accounts

individually.

Authorisation and

authentication

There is no procedure of

authorization and authentication in

BML. This system is same for

payroll account and any other

account too.

ID and password testing has

been done for verification

purpose.

Question 2 B: List and identify the weaknesses in internal control for contract

payroll.

The company is facing a downtime and one of the major reasons for the same is the weak

internal control system. Some known weaknesses are (Arens, Elder, & Beasley, 2013).

Unsecured payroll system- A testing of BML has been initiated regarding the payroll system

with the help of using password on a dummy. After the installation of the system, password has

been removed. This is the main reason for unsecured payroll system

No cross- checking of documents- It has been observed that in BML, hard copy has not been

used for making the entries by the employees in the systems.

11

This is the reason for lacking in cross checking from the relevant source of information to the

wrong entries (Mohseni, 2014).

Wrong working hour entries by payroll employees- There is a fictitious system for the

employees, and this helps employees to enter working hours in the system according to them. It

was found that employees made false entries, when checking has been done (Dube, & Gulati,

2015).

Improper management of deduction and overtime- The system used by BML has not the capacity

to calculate the deduction for leaves and absenteeism. There are no proper rules and policies for

the employees who work overtime. So, controlling of working hours is very important (Messier,

Glover, & Prawitt, 2016).

12

wrong entries (Mohseni, 2014).

Wrong working hour entries by payroll employees- There is a fictitious system for the

employees, and this helps employees to enter working hours in the system according to them. It

was found that employees made false entries, when checking has been done (Dube, & Gulati,

2015).

Improper management of deduction and overtime- The system used by BML has not the capacity

to calculate the deduction for leaves and absenteeism. There are no proper rules and policies for

the employees who work overtime. So, controlling of working hours is very important (Messier,

Glover, & Prawitt, 2016).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.