Audit Report: Business Risks, Internal Controls for Big Machine Ltd

VerifiedAdded on 2021/05/30

|13

|2837

|50

Report

AI Summary

This report provides a comprehensive analysis of the audit conducted for Big Machine Ltd (BML), a company offering lease services for heavy mining machinery. The report begins with an assessment of financial ratios, including accounts receivable, machinery finance liabilities, plant and equipment, and lease income, highlighting industry benchmarks and identifying potential business risks. It then delves into the company's internal controls, evaluating control processes, risk reduction strategies, and the examination of controls. The report also addresses weaknesses in the internal control mechanisms, specifically for contract payroll, and discusses the business risks that threaten the company. The analysis includes an evaluation of audit steps, audit risks, and mitigation strategies. The report emphasizes the importance of internal control functions within the framework to effectively address problematic scenarios.

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmqwertyuiopasdfghjklzxcv

bnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmrtyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

AUDIT

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmqwertyuiopasdfghjklzxcv

bnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmrtyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

AUDIT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BML

Executive summary

Audit techniques and processes are very pivotal as it assists in creating a path for companies

to progress further. Besides, it is vital for companies to pursue a powerful internal control

function within their framework so that they can cater to problematic scenarios effectively.

This report intends to shed light on Big Machine Ltd (BML) that offers lease services

associated to heavy mining machineries to the gold mines. Moreover, this report starts with

the assessment part wherein computation of ratios has been facilitated. In other words, four

different accounts are disclosed by the audit partner that is again followed by a table wherein

audit steps, audit risk, and evaluation part to decrease risks have been discussed. Further, the

ratios are assessed to depict the business risks posing a threat to the company. Nevertheless,

in the other segment, internal control measures are emphasized wherein control processes,

risk deduction, and examination of control is highlighted through a table. Lastly, the

weaknesses of such mechanism for contract payroll is discussed.

2

Executive summary

Audit techniques and processes are very pivotal as it assists in creating a path for companies

to progress further. Besides, it is vital for companies to pursue a powerful internal control

function within their framework so that they can cater to problematic scenarios effectively.

This report intends to shed light on Big Machine Ltd (BML) that offers lease services

associated to heavy mining machineries to the gold mines. Moreover, this report starts with

the assessment part wherein computation of ratios has been facilitated. In other words, four

different accounts are disclosed by the audit partner that is again followed by a table wherein

audit steps, audit risk, and evaluation part to decrease risks have been discussed. Further, the

ratios are assessed to depict the business risks posing a threat to the company. Nevertheless,

in the other segment, internal control measures are emphasized wherein control processes,

risk deduction, and examination of control is highlighted through a table. Lastly, the

weaknesses of such mechanism for contract payroll is discussed.

2

BML

Contents

1. Planning of audit in BML................................................................................................................3

1B. Business risks that pose a threat to the company...........................................................................7

2a. Recognition of internal controls......................................................................................................7

2B. Weaknesses in the internal control for contract payroll.................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

3

Contents

1. Planning of audit in BML................................................................................................................3

1B. Business risks that pose a threat to the company...........................................................................7

2a. Recognition of internal controls......................................................................................................7

2B. Weaknesses in the internal control for contract payroll.................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BML

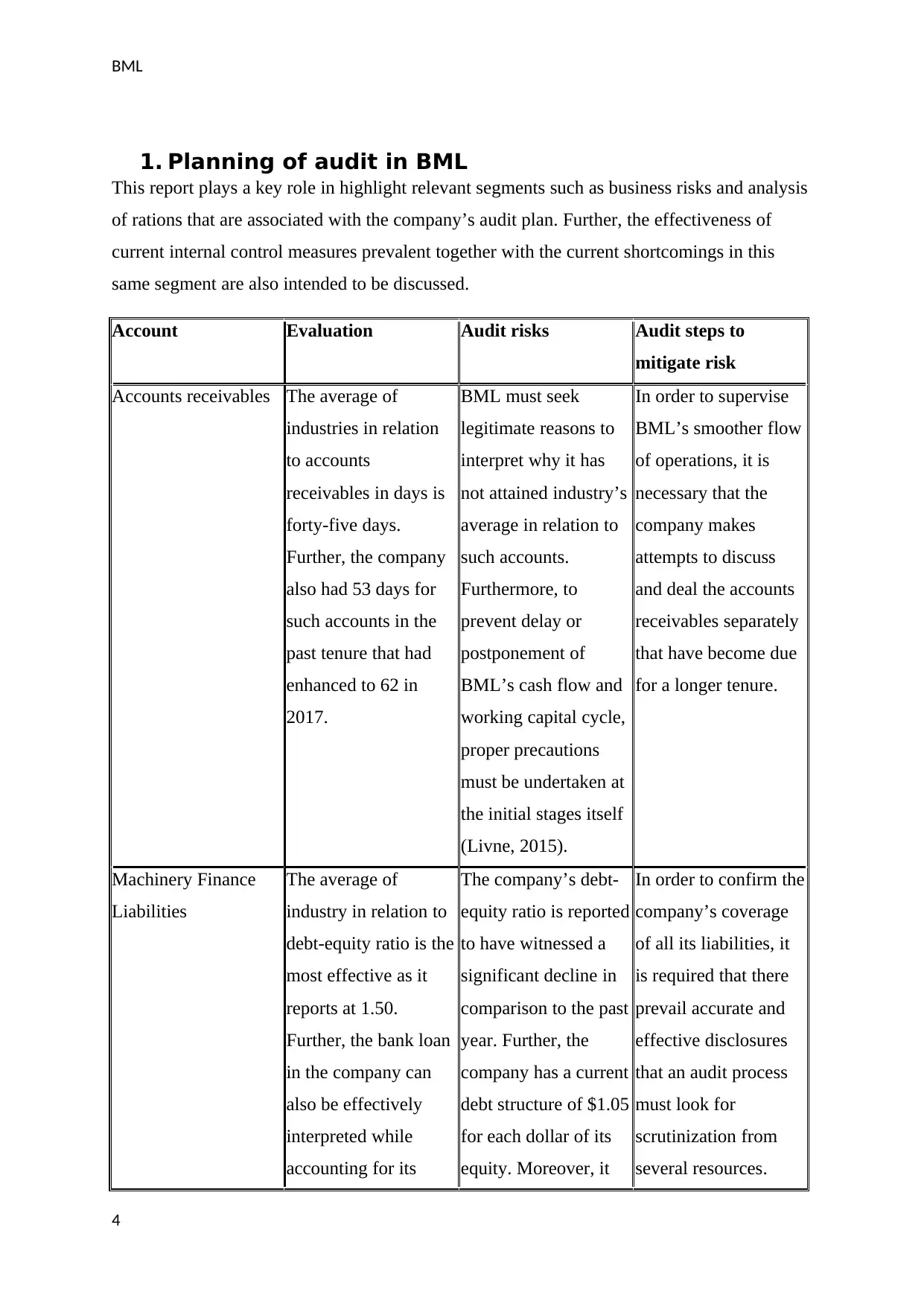

1. Planning of audit in BML

This report plays a key role in highlight relevant segments such as business risks and analysis

of rations that are associated with the company’s audit plan. Further, the effectiveness of

current internal control measures prevalent together with the current shortcomings in this

same segment are also intended to be discussed.

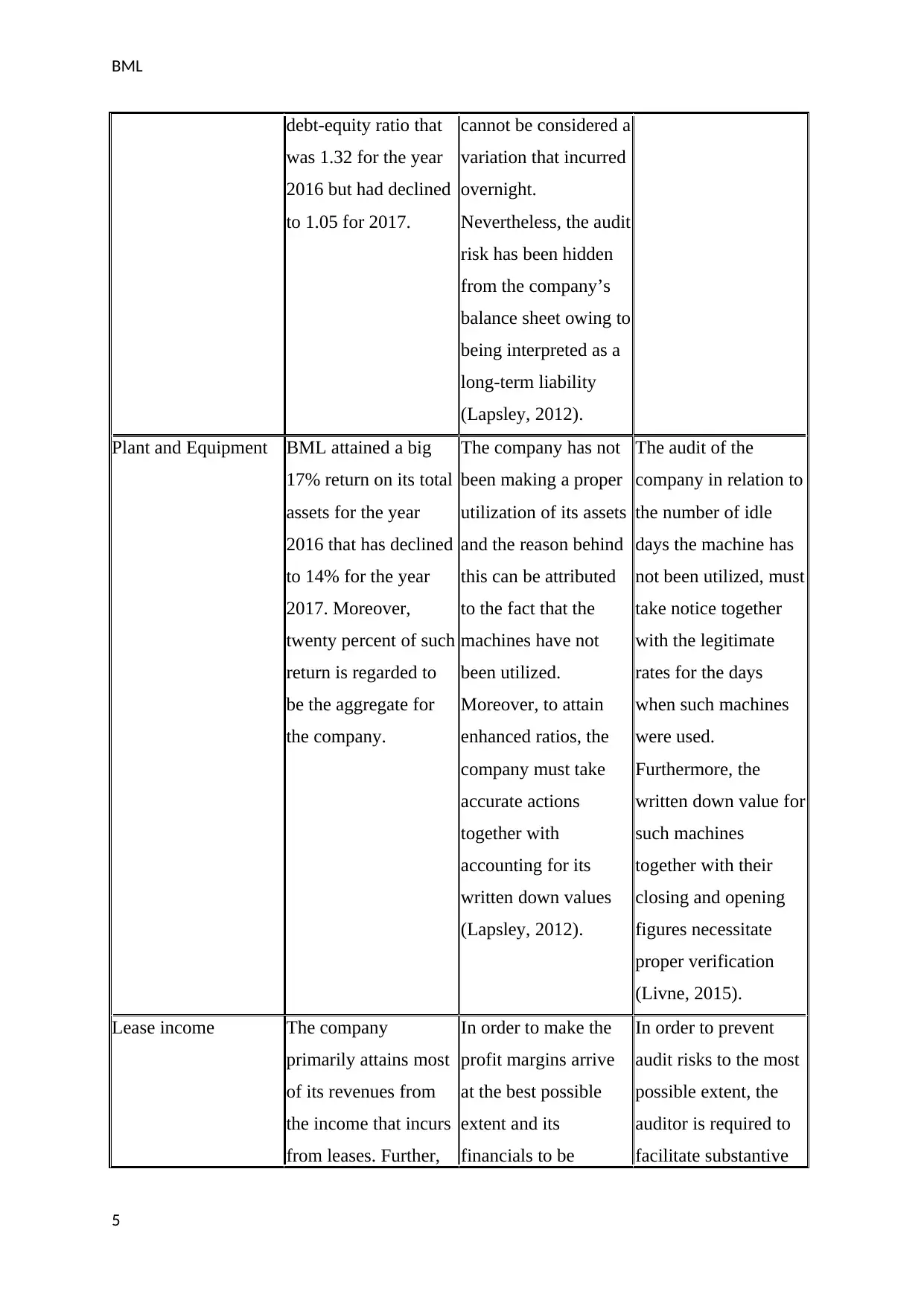

Account Evaluation Audit risks Audit steps to

mitigate risk

Accounts receivables The average of

industries in relation

to accounts

receivables in days is

forty-five days.

Further, the company

also had 53 days for

such accounts in the

past tenure that had

enhanced to 62 in

2017.

BML must seek

legitimate reasons to

interpret why it has

not attained industry’s

average in relation to

such accounts.

Furthermore, to

prevent delay or

postponement of

BML’s cash flow and

working capital cycle,

proper precautions

must be undertaken at

the initial stages itself

(Livne, 2015).

In order to supervise

BML’s smoother flow

of operations, it is

necessary that the

company makes

attempts to discuss

and deal the accounts

receivables separately

that have become due

for a longer tenure.

Machinery Finance

Liabilities

The average of

industry in relation to

debt-equity ratio is the

most effective as it

reports at 1.50.

Further, the bank loan

in the company can

also be effectively

interpreted while

accounting for its

The company’s debt-

equity ratio is reported

to have witnessed a

significant decline in

comparison to the past

year. Further, the

company has a current

debt structure of $1.05

for each dollar of its

equity. Moreover, it

In order to confirm the

company’s coverage

of all its liabilities, it

is required that there

prevail accurate and

effective disclosures

that an audit process

must look for

scrutinization from

several resources.

4

1. Planning of audit in BML

This report plays a key role in highlight relevant segments such as business risks and analysis

of rations that are associated with the company’s audit plan. Further, the effectiveness of

current internal control measures prevalent together with the current shortcomings in this

same segment are also intended to be discussed.

Account Evaluation Audit risks Audit steps to

mitigate risk

Accounts receivables The average of

industries in relation

to accounts

receivables in days is

forty-five days.

Further, the company

also had 53 days for

such accounts in the

past tenure that had

enhanced to 62 in

2017.

BML must seek

legitimate reasons to

interpret why it has

not attained industry’s

average in relation to

such accounts.

Furthermore, to

prevent delay or

postponement of

BML’s cash flow and

working capital cycle,

proper precautions

must be undertaken at

the initial stages itself

(Livne, 2015).

In order to supervise

BML’s smoother flow

of operations, it is

necessary that the

company makes

attempts to discuss

and deal the accounts

receivables separately

that have become due

for a longer tenure.

Machinery Finance

Liabilities

The average of

industry in relation to

debt-equity ratio is the

most effective as it

reports at 1.50.

Further, the bank loan

in the company can

also be effectively

interpreted while

accounting for its

The company’s debt-

equity ratio is reported

to have witnessed a

significant decline in

comparison to the past

year. Further, the

company has a current

debt structure of $1.05

for each dollar of its

equity. Moreover, it

In order to confirm the

company’s coverage

of all its liabilities, it

is required that there

prevail accurate and

effective disclosures

that an audit process

must look for

scrutinization from

several resources.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BML

debt-equity ratio that

was 1.32 for the year

2016 but had declined

to 1.05 for 2017.

cannot be considered a

variation that incurred

overnight.

Nevertheless, the audit

risk has been hidden

from the company’s

balance sheet owing to

being interpreted as a

long-term liability

(Lapsley, 2012).

Plant and Equipment BML attained a big

17% return on its total

assets for the year

2016 that has declined

to 14% for the year

2017. Moreover,

twenty percent of such

return is regarded to

be the aggregate for

the company.

The company has not

been making a proper

utilization of its assets

and the reason behind

this can be attributed

to the fact that the

machines have not

been utilized.

Moreover, to attain

enhanced ratios, the

company must take

accurate actions

together with

accounting for its

written down values

(Lapsley, 2012).

The audit of the

company in relation to

the number of idle

days the machine has

not been utilized, must

take notice together

with the legitimate

rates for the days

when such machines

were used.

Furthermore, the

written down value for

such machines

together with their

closing and opening

figures necessitate

proper verification

(Livne, 2015).

Lease income The company

primarily attains most

of its revenues from

the income that incurs

from leases. Further,

In order to make the

profit margins arrive

at the best possible

extent and its

financials to be

In order to prevent

audit risks to the most

possible extent, the

auditor is required to

facilitate substantive

5

debt-equity ratio that

was 1.32 for the year

2016 but had declined

to 1.05 for 2017.

cannot be considered a

variation that incurred

overnight.

Nevertheless, the audit

risk has been hidden

from the company’s

balance sheet owing to

being interpreted as a

long-term liability

(Lapsley, 2012).

Plant and Equipment BML attained a big

17% return on its total

assets for the year

2016 that has declined

to 14% for the year

2017. Moreover,

twenty percent of such

return is regarded to

be the aggregate for

the company.

The company has not

been making a proper

utilization of its assets

and the reason behind

this can be attributed

to the fact that the

machines have not

been utilized.

Moreover, to attain

enhanced ratios, the

company must take

accurate actions

together with

accounting for its

written down values

(Lapsley, 2012).

The audit of the

company in relation to

the number of idle

days the machine has

not been utilized, must

take notice together

with the legitimate

rates for the days

when such machines

were used.

Furthermore, the

written down value for

such machines

together with their

closing and opening

figures necessitate

proper verification

(Livne, 2015).

Lease income The company

primarily attains most

of its revenues from

the income that incurs

from leases. Further,

In order to make the

profit margins arrive

at the best possible

extent and its

financials to be

In order to prevent

audit risks to the most

possible extent, the

auditor is required to

facilitate substantive

5

BML

the margin on such

lease for the past

tenure was twelve

percent that declined

to eight percent in the

present year. One of

the biggest reasons in

relation to the same

can be attributed to the

fact is the diminishing

capability for

employment of older

machines. Further, the

operation and

installation of new

machineries are also

needed that can

facilitate in incurring

additional

expenditures for

yielding lesser returns.

favourable in the eyes

of others, the company

may depict few of its

revenue expenses as a

part of its revenue

expenditure. Further,

this can be regarded as

the audit risk that is

associated with the

scenario (Kaplan,

2011).

audit processes to

distinguish capital

expenses from the

revenue expenses.

The enhancement in the machine employment that were newly installed accounted to the

decline in the company’s net profit margin by four percent. In contrast to this, the gross

margin was not influenced, thereby indicating that there is no variation in the company’s

direct expense.

In comparison to the last year, the company had achieved lower times of interest in the

present year that is also a lesser figure when compared with the industry average. Therefore,

to surpass or avoid this scenario and attain proper returns, BML must effectively concentrate

on enhancing or developing the employment of its resources that have been kept idle

(Hoffelder, 2012).

6

the margin on such

lease for the past

tenure was twelve

percent that declined

to eight percent in the

present year. One of

the biggest reasons in

relation to the same

can be attributed to the

fact is the diminishing

capability for

employment of older

machines. Further, the

operation and

installation of new

machineries are also

needed that can

facilitate in incurring

additional

expenditures for

yielding lesser returns.

favourable in the eyes

of others, the company

may depict few of its

revenue expenses as a

part of its revenue

expenditure. Further,

this can be regarded as

the audit risk that is

associated with the

scenario (Kaplan,

2011).

audit processes to

distinguish capital

expenses from the

revenue expenses.

The enhancement in the machine employment that were newly installed accounted to the

decline in the company’s net profit margin by four percent. In contrast to this, the gross

margin was not influenced, thereby indicating that there is no variation in the company’s

direct expense.

In comparison to the last year, the company had achieved lower times of interest in the

present year that is also a lesser figure when compared with the industry average. Therefore,

to surpass or avoid this scenario and attain proper returns, BML must effectively concentrate

on enhancing or developing the employment of its resources that have been kept idle

(Hoffelder, 2012).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BML

Further, the industry average in relation to return on equity have reported at 26%. Besides,

the return on equity for the company have declined to 15% from 22% that was in the previous

year. Nonetheless, the enhanced shareholding due to the issues that are made to the public

and the decline in profits can be attributed to the causes of decline in return on equity

(Matthew,2015).

BML pursues a favourable and acceptable current ratio and quick ratio that is closer to the

industry average. Furthermore, taking into account the financial performance of the company,

it can be said that the company must make proper amendments for future developments.

Besides, the machines having no use must be disposed or sold off by the company so that

funds can be realized in relation to the same (Geoffrey et. al, 2016).

7

Further, the industry average in relation to return on equity have reported at 26%. Besides,

the return on equity for the company have declined to 15% from 22% that was in the previous

year. Nonetheless, the enhanced shareholding due to the issues that are made to the public

and the decline in profits can be attributed to the causes of decline in return on equity

(Matthew,2015).

BML pursues a favourable and acceptable current ratio and quick ratio that is closer to the

industry average. Furthermore, taking into account the financial performance of the company,

it can be said that the company must make proper amendments for future developments.

Besides, the machines having no use must be disposed or sold off by the company so that

funds can be realized in relation to the same (Geoffrey et. al, 2016).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BML

1B. Business risks that pose a threat to the company

In order to encounter the situation of present industrialization standards, the employment of

machines that are automatic, and disposal of outdated machines are needed. Such machines

must be computerized in nature and to follow such trend, the company has been interested in

purchasing and installing automated and updated machineries that has facilitated in

enhancing the requirement of massive resources (Manoharan, 2011).

The business risks posing a threat to the company are as follows:

1. If it is considered that the company has kept several of its machines idle and

unemployed for a longer period of time in its yard or warehouse, there must be a

decline in the company’s net realizable amount in relation to such machineries.

Therefore, the books of accounts of the company must acknowledge such necessary

and depreciation write-offs (Gay & Simnet, 2015).

2. The operations of the company are also influenced by the usual fluctuations in the

metal market. Further, the prices of coal have also increased due to the decline in iron

ores and gold. Besides, to encounter such fluctuations in the market, the company

must make required necessary alterations in its mode of affairs and framework.

3. In order to tackle emergence of fraudulent affairs, it is needed for the contracted

personnel, employees, and accountant to be accustomed and updated with the newly

machinery systems installed (Gay & Simnet, 2015). Moreover, regular knowledge

must be facilitated through updating and training to the employees, staff, and

accountants so that they are updated properly. Therefore, not accounting for such

steps can pose a threat to the company.

4. The business risk of enhanced and modern technology advancements is a major

concern for the company because what may be trending in such technology today may

become outdated and old in the future taking into account the speed at which

developments are being made.

2a. Recognition of internal controls

Control Risk alleviated Test of control

Approval of exact working

time- It is needed that the

contract manager must

It can be witnessed that the

employees have reported

working hours that were

It is needed that the auditors

evaluate on what basis the

approval of working hours has

8

1B. Business risks that pose a threat to the company

In order to encounter the situation of present industrialization standards, the employment of

machines that are automatic, and disposal of outdated machines are needed. Such machines

must be computerized in nature and to follow such trend, the company has been interested in

purchasing and installing automated and updated machineries that has facilitated in

enhancing the requirement of massive resources (Manoharan, 2011).

The business risks posing a threat to the company are as follows:

1. If it is considered that the company has kept several of its machines idle and

unemployed for a longer period of time in its yard or warehouse, there must be a

decline in the company’s net realizable amount in relation to such machineries.

Therefore, the books of accounts of the company must acknowledge such necessary

and depreciation write-offs (Gay & Simnet, 2015).

2. The operations of the company are also influenced by the usual fluctuations in the

metal market. Further, the prices of coal have also increased due to the decline in iron

ores and gold. Besides, to encounter such fluctuations in the market, the company

must make required necessary alterations in its mode of affairs and framework.

3. In order to tackle emergence of fraudulent affairs, it is needed for the contracted

personnel, employees, and accountant to be accustomed and updated with the newly

machinery systems installed (Gay & Simnet, 2015). Moreover, regular knowledge

must be facilitated through updating and training to the employees, staff, and

accountants so that they are updated properly. Therefore, not accounting for such

steps can pose a threat to the company.

4. The business risk of enhanced and modern technology advancements is a major

concern for the company because what may be trending in such technology today may

become outdated and old in the future taking into account the speed at which

developments are being made.

2a. Recognition of internal controls

Control Risk alleviated Test of control

Approval of exact working

time- It is needed that the

contract manager must

It can be witnessed that the

employees have reported

working hours that were

It is needed that the auditors

evaluate on what basis the

approval of working hours has

8

BML

compare the actual working

hours of employees with the

hours that are entered by him

so that he can approve prior to

the initiation of payment

processes (Fazal, 2013).

untrue and were also approved

and verified by the contract

managers, thereby proving

that the manager is

questionable and accountable

for the frauds on the part of

employees.

been conducted by the

contract managers through

day-to-day timely records that

are maintained by the

manager for such time

reflected by the employee

(Fazal, 2013).

Recruiting new personnel-

The information from hard

copies and authorized revenue

tax declaration must be

verified by the payroll clerk.

It is the responsibility of

employees to monitor and

double check the information

filled by payroll clerks and

accountants to prevent

mistakes. The information

offered by the clerk passes

through various stages, so it is

easy for contract managers,

employees, and payroll clerks

to double check the

information (Elder et. al,

2010).

The information from the hard

copies and authenticated

declaration of income tax

filled by the payroll clerk

must also be verified by the

auditor of the company. This

can be undertaken by

comparing specific details that

are filled by such clerk and

accountants with the

supporting documents (Elder

et. al, 2010).

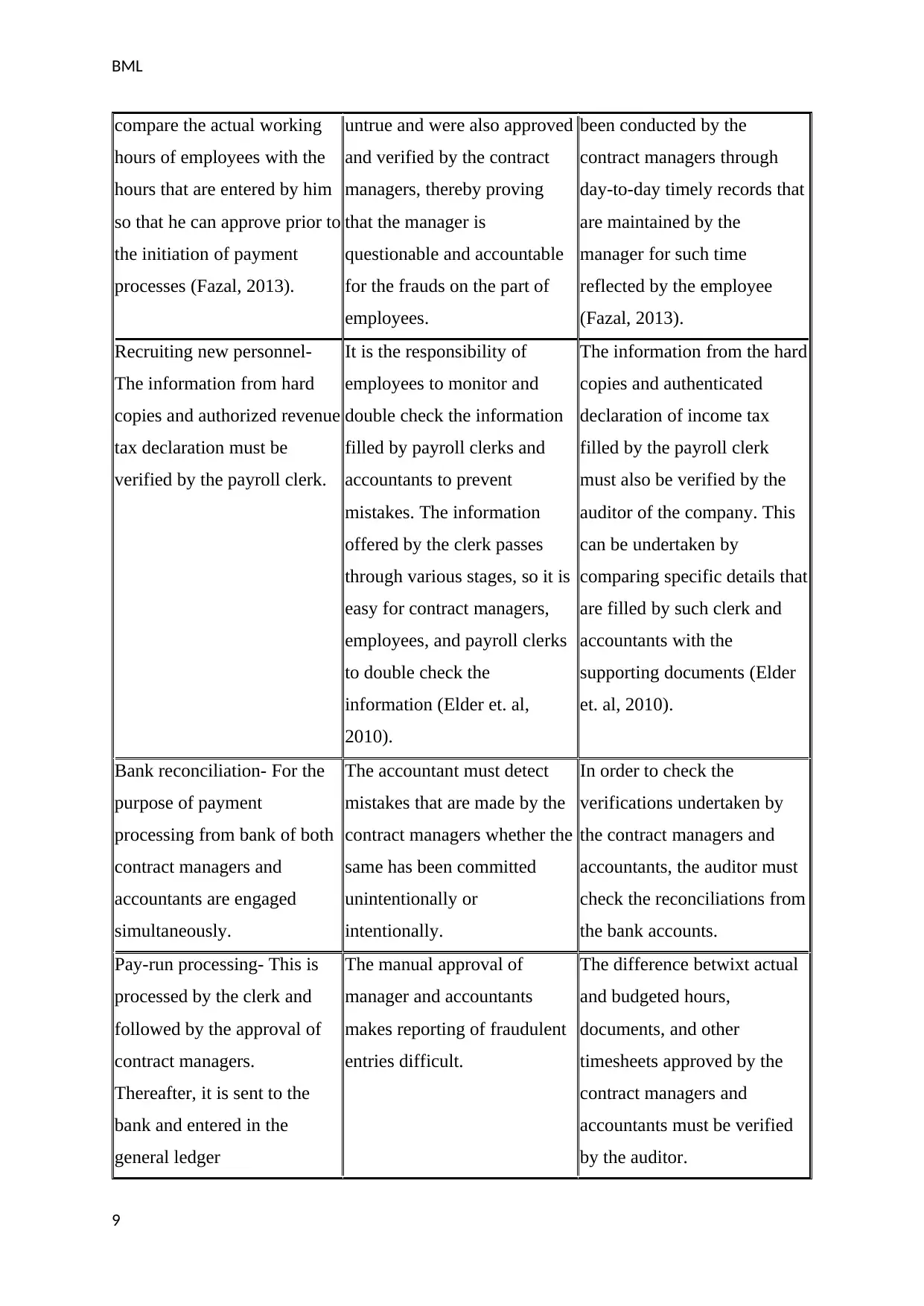

Bank reconciliation- For the

purpose of payment

processing from bank of both

contract managers and

accountants are engaged

simultaneously.

The accountant must detect

mistakes that are made by the

contract managers whether the

same has been committed

unintentionally or

intentionally.

In order to check the

verifications undertaken by

the contract managers and

accountants, the auditor must

check the reconciliations from

the bank accounts.

Pay-run processing- This is

processed by the clerk and

followed by the approval of

contract managers.

Thereafter, it is sent to the

bank and entered in the

general ledger

The manual approval of

manager and accountants

makes reporting of fraudulent

entries difficult.

The difference betwixt actual

and budgeted hours,

documents, and other

timesheets approved by the

contract managers and

accountants must be verified

by the auditor.

9

compare the actual working

hours of employees with the

hours that are entered by him

so that he can approve prior to

the initiation of payment

processes (Fazal, 2013).

untrue and were also approved

and verified by the contract

managers, thereby proving

that the manager is

questionable and accountable

for the frauds on the part of

employees.

been conducted by the

contract managers through

day-to-day timely records that

are maintained by the

manager for such time

reflected by the employee

(Fazal, 2013).

Recruiting new personnel-

The information from hard

copies and authorized revenue

tax declaration must be

verified by the payroll clerk.

It is the responsibility of

employees to monitor and

double check the information

filled by payroll clerks and

accountants to prevent

mistakes. The information

offered by the clerk passes

through various stages, so it is

easy for contract managers,

employees, and payroll clerks

to double check the

information (Elder et. al,

2010).

The information from the hard

copies and authenticated

declaration of income tax

filled by the payroll clerk

must also be verified by the

auditor of the company. This

can be undertaken by

comparing specific details that

are filled by such clerk and

accountants with the

supporting documents (Elder

et. al, 2010).

Bank reconciliation- For the

purpose of payment

processing from bank of both

contract managers and

accountants are engaged

simultaneously.

The accountant must detect

mistakes that are made by the

contract managers whether the

same has been committed

unintentionally or

intentionally.

In order to check the

verifications undertaken by

the contract managers and

accountants, the auditor must

check the reconciliations from

the bank accounts.

Pay-run processing- This is

processed by the clerk and

followed by the approval of

contract managers.

Thereafter, it is sent to the

bank and entered in the

general ledger

The manual approval of

manager and accountants

makes reporting of fraudulent

entries difficult.

The difference betwixt actual

and budgeted hours,

documents, and other

timesheets approved by the

contract managers and

accountants must be verified

by the auditor.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BML

2B. Weaknesses in the internal control for contract

payroll

The reason behind the usage of internal control is to enhance effectiveness and decrease the

emergence of frauds. If an employee is operating overtime, then they must be liable to attain

a wage for such particular time that is marked by documentation and analysis and

verification. Such kind of risk emerges when this documentation is missing or failed to be

recorded by the management (Baldwin, 2010). If the time duration of such overtime is

terminated, then the ending time is also relevant for the assessment of amount that the

employees are liable to attain. Besides, most of the opening gaps are associated with the

internal control mechanisms.

The loopholes that prevail in the internal controls are:

1. It can be seen that the contract manager can control the information associated to

working hours has access to the salary website of the company. Further, no

verification system is present that can check the stored data. It is relevant for the

company to allow verification of records and data by the accountant but not allowing

to any other person (Cappelleto, 2010).

2. It is usual for an employee to join the company and therefore, payroll clerk is

responsible to set a password and username. This is simple and accurate but it can be

feasible that false entries are made here, thereby resulting in fraud and another

loophole in internal control.

3. For the employees’ working hours, they are to enter their respective timing

themselves that are approved and verified by the contract managers. If the employee

has connection with the manager, false entries can easily be made, and the accountant

may fail to verify the same. It may also happen that the contract manager overlooks a

false record by mistake and this can facilitate in becoming a boon to the employee,

thereby resulting in another loophole of internal control mechanism (Merchant, 2012).

10

2B. Weaknesses in the internal control for contract

payroll

The reason behind the usage of internal control is to enhance effectiveness and decrease the

emergence of frauds. If an employee is operating overtime, then they must be liable to attain

a wage for such particular time that is marked by documentation and analysis and

verification. Such kind of risk emerges when this documentation is missing or failed to be

recorded by the management (Baldwin, 2010). If the time duration of such overtime is

terminated, then the ending time is also relevant for the assessment of amount that the

employees are liable to attain. Besides, most of the opening gaps are associated with the

internal control mechanisms.

The loopholes that prevail in the internal controls are:

1. It can be seen that the contract manager can control the information associated to

working hours has access to the salary website of the company. Further, no

verification system is present that can check the stored data. It is relevant for the

company to allow verification of records and data by the accountant but not allowing

to any other person (Cappelleto, 2010).

2. It is usual for an employee to join the company and therefore, payroll clerk is

responsible to set a password and username. This is simple and accurate but it can be

feasible that false entries are made here, thereby resulting in fraud and another

loophole in internal control.

3. For the employees’ working hours, they are to enter their respective timing

themselves that are approved and verified by the contract managers. If the employee

has connection with the manager, false entries can easily be made, and the accountant

may fail to verify the same. It may also happen that the contract manager overlooks a

false record by mistake and this can facilitate in becoming a boon to the employee,

thereby resulting in another loophole of internal control mechanism (Merchant, 2012).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BML

Conclusion

Considering the previously mentioned scenario and analysis, the several standards of re-

evaluation including data verification by more than one individual must be established by the

company so that it can easily pave a path for mitigating or avoiding such loopholes and

frauds. Besides, an efficient risk management plan must collaborate with the mechanisms of

internal control so that it can assist in eliminating risks, thereby facilitating in smooth flow of

operations. Moreover, it is the obligation of auditors to report significant threats so that it

cannot influence the company and its activities. Nevertheless, various structural changes are

needed in the internal control mechanisms so that the path towards fraud and risks can be

terminated.

11

Conclusion

Considering the previously mentioned scenario and analysis, the several standards of re-

evaluation including data verification by more than one individual must be established by the

company so that it can easily pave a path for mitigating or avoiding such loopholes and

frauds. Besides, an efficient risk management plan must collaborate with the mechanisms of

internal control so that it can assist in eliminating risks, thereby facilitating in smooth flow of

operations. Moreover, it is the obligation of auditors to report significant threats so that it

cannot influence the company and its activities. Nevertheless, various structural changes are

needed in the internal control mechanisms so that the path towards fraud and risks can be

terminated.

11

BML

References

Baldwin, S. (2010). Doing a content audit or inventory. Pearson Press.

Cappelleto, G. (2010) Challenges Facing Accounting Education in Australia. AFAANZ,

Melbourne

Elder, J. R., Beasley S. M., and Arens A. A. (2010). Auditing and Assurance Services. Person

Education, New Jersey: USA

Fazal, H. (2013, May 13). What is Intimidation threat in auditing?.Retrieved from:

http://pakaccountants.com/what-is-intimidation-threat-in-auditing/

Gay, G., and Simnet, R. (2015). Auditing and Assurance Services. McGraw Hill

Geoffrey D. B., Joleen K., K. K.S., and David A. W. (2016). Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors.

Accounting Horizons, 30(1), 143-156. https://doi.org/10.2308/acch-51309

Hoffelder, K. (2012). New Audit Standard Encourages More Talking. Harvard Press.

Kaplan, R.S. (2011). Accounting scholarship that advances professional knowledge and

practice. The Accounting Review, 86(2), 367–383.

https://doi.org/10.2308/accr.00000031

Lapsley, I. (2012). Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management, 9(3), pp. 291-292.

https://doi.org/10.1111/1468-0408.00081

Livne, G. (2015, May 12). Threats to Auditor Independence and Possible Remedies. Retrieved

from: http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full

Manoharan, T.N. (2011). Financial Statement Fraud and Corporate Governance. The

George Washington University.

Matthew, S. E. (2015). Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review, 90(2), 495-527. https://doi.org/10.2308/accr-

50871

Merchant, K. A. (2012). Making Management Accounting Research More Useful. Pacific

Accounting Review, 24(3), 1-34. https://doi.org/10.1108/01140581211283904

12

References

Baldwin, S. (2010). Doing a content audit or inventory. Pearson Press.

Cappelleto, G. (2010) Challenges Facing Accounting Education in Australia. AFAANZ,

Melbourne

Elder, J. R., Beasley S. M., and Arens A. A. (2010). Auditing and Assurance Services. Person

Education, New Jersey: USA

Fazal, H. (2013, May 13). What is Intimidation threat in auditing?.Retrieved from:

http://pakaccountants.com/what-is-intimidation-threat-in-auditing/

Gay, G., and Simnet, R. (2015). Auditing and Assurance Services. McGraw Hill

Geoffrey D. B., Joleen K., K. K.S., and David A. W. (2016). Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors.

Accounting Horizons, 30(1), 143-156. https://doi.org/10.2308/acch-51309

Hoffelder, K. (2012). New Audit Standard Encourages More Talking. Harvard Press.

Kaplan, R.S. (2011). Accounting scholarship that advances professional knowledge and

practice. The Accounting Review, 86(2), 367–383.

https://doi.org/10.2308/accr.00000031

Lapsley, I. (2012). Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management, 9(3), pp. 291-292.

https://doi.org/10.1111/1468-0408.00081

Livne, G. (2015, May 12). Threats to Auditor Independence and Possible Remedies. Retrieved

from: http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full

Manoharan, T.N. (2011). Financial Statement Fraud and Corporate Governance. The

George Washington University.

Matthew, S. E. (2015). Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review, 90(2), 495-527. https://doi.org/10.2308/accr-

50871

Merchant, K. A. (2012). Making Management Accounting Research More Useful. Pacific

Accounting Review, 24(3), 1-34. https://doi.org/10.1108/01140581211283904

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.