Auditing Theory and Practice: BML Ltd. Risk and Control Analysis

VerifiedAdded on 2023/06/12

|14

|2999

|122

Case Study

AI Summary

This report provides a detailed analysis of BML Ltd., focusing on identifying weaknesses in its internal controls and recommending corrective measures. It examines financial ratios and additional information to determine the risks faced by the company, including obsolescence of plant and equipment, increased financial liabilities due to loans, and fluctuations in the metal market. The report also assesses the effectiveness of existing internal controls, proposes tests of control, and identifies weaknesses in contract payroll. Key business risks are confirmed through ratio analysis, highlighting discrepancies between audited and unaudited results and extended accounts receivable periods. Effective inventory and receivables management systems, along with accounting software, are recommended to mitigate these risks and improve financial reporting accuracy. Desklib offers more resources for students seeking similar solved assignments and past papers.

Running head: AUDITING THEORY AND PRACTICE

Auditing Theory and Practice

Name of the Student:

Name of the University:

Author Note:

Auditing Theory and Practice

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2AUDITING THEORY AND PRACTICE

Executive summary

In the p-resent report, detailed analysis of the various aspects of the business conducted by

BML Ltd. will be analysed. The purpose of this analysis is to determine the various

weaknesses in the internal control of the company and to determine the corrective measures

to be taken to check them. The primary job will be to analyse all of the information that is

being presented like the various financial ratios and the additional information

Executive summary

In the p-resent report, detailed analysis of the various aspects of the business conducted by

BML Ltd. will be analysed. The purpose of this analysis is to determine the various

weaknesses in the internal control of the company and to determine the corrective measures

to be taken to check them. The primary job will be to analyse all of the information that is

being presented like the various financial ratios and the additional information

3AUDITING THEORY AND PRACTICE

Table of Contents

Introduction:...............................................................................................................................3

Analysis of the ratios and the additional information as listed out by audit partner, Ms.

Leanne Hopkins:........................................................................................................................3

Analysis of the ratios and the additional information to determine the risks faced by the

company:....................................................................................................................................6

Internal controls that are effective, risks that they alleviate and the test of control to check

them............................................................................................................................................8

Identification of the weaknesses in the internal control for contract payroll:..........................10

Conclusion:..............................................................................................................................10

Reference List..........................................................................................................................12

Table of Contents

Introduction:...............................................................................................................................3

Analysis of the ratios and the additional information as listed out by audit partner, Ms.

Leanne Hopkins:........................................................................................................................3

Analysis of the ratios and the additional information to determine the risks faced by the

company:....................................................................................................................................6

Internal controls that are effective, risks that they alleviate and the test of control to check

them............................................................................................................................................8

Identification of the weaknesses in the internal control for contract payroll:..........................10

Conclusion:..............................................................................................................................10

Reference List..........................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4AUDITING THEORY AND PRACTICE

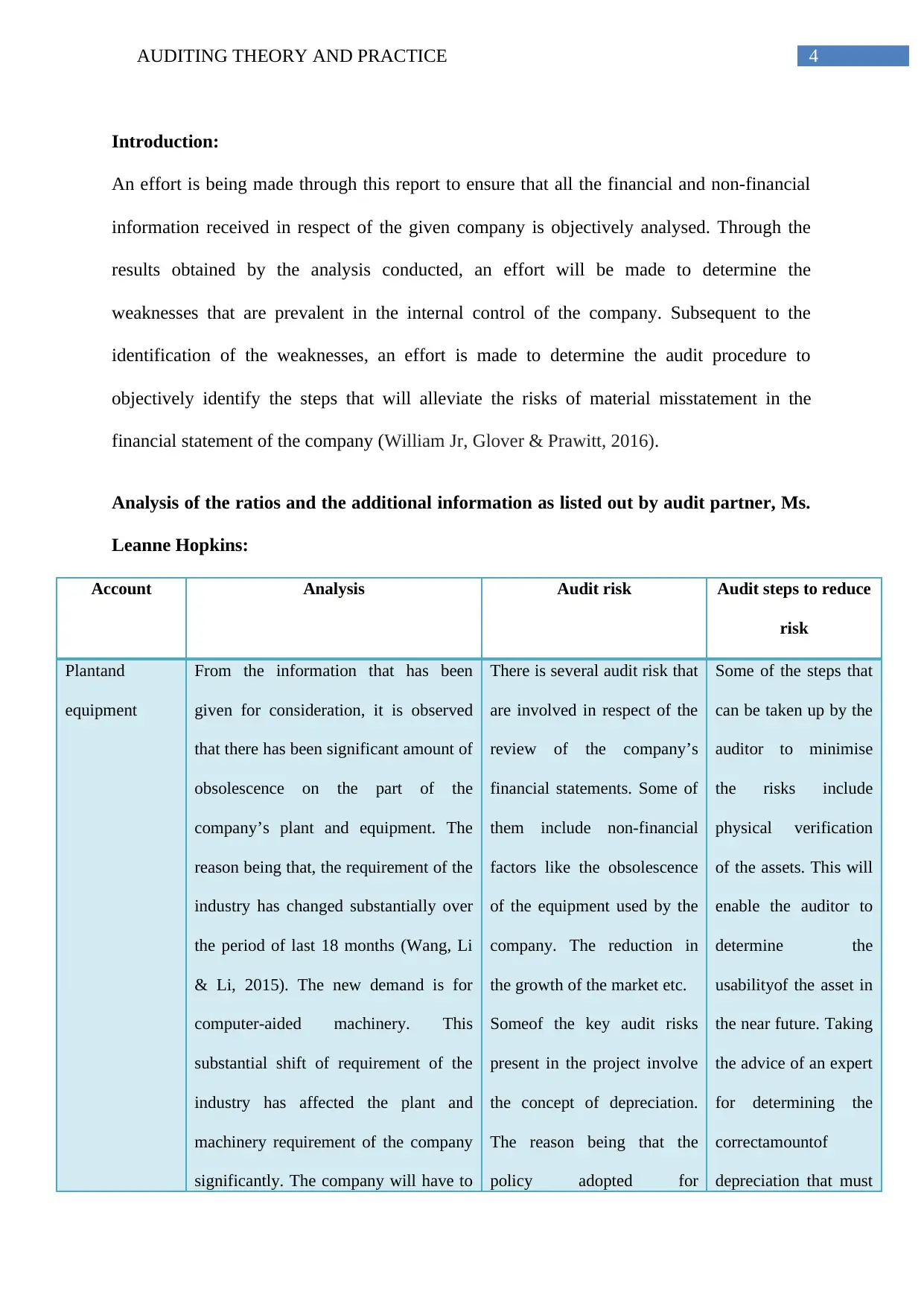

Introduction:

An effort is being made through this report to ensure that all the financial and non-financial

information received in respect of the given company is objectively analysed. Through the

results obtained by the analysis conducted, an effort will be made to determine the

weaknesses that are prevalent in the internal control of the company. Subsequent to the

identification of the weaknesses, an effort is made to determine the audit procedure to

objectively identify the steps that will alleviate the risks of material misstatement in the

financial statement of the company (William Jr, Glover & Prawitt, 2016).

Analysis of the ratios and the additional information as listed out by audit partner, Ms.

Leanne Hopkins:

Account Analysis Audit risk Audit steps to reduce

risk

Plantand

equipment

From the information that has been

given for consideration, it is observed

that there has been significant amount of

obsolescence on the part of the

company’s plant and equipment. The

reason being that, the requirement of the

industry has changed substantially over

the period of last 18 months (Wang, Li

& Li, 2015). The new demand is for

computer-aided machinery. This

substantial shift of requirement of the

industry has affected the plant and

machinery requirement of the company

significantly. The company will have to

There is several audit risk that

are involved in respect of the

review of the company’s

financial statements. Some of

them include non-financial

factors like the obsolescence

of the equipment used by the

company. The reduction in

the growth of the market etc.

Someof the key audit risks

present in the project involve

the concept of depreciation.

The reason being that the

policy adopted for

Some of the steps that

can be taken up by the

auditor to minimise

the risks include

physical verification

of the assets. This will

enable the auditor to

determine the

usabilityof the asset in

the near future. Taking

the advice of an expert

for determining the

correctamountof

depreciation that must

Introduction:

An effort is being made through this report to ensure that all the financial and non-financial

information received in respect of the given company is objectively analysed. Through the

results obtained by the analysis conducted, an effort will be made to determine the

weaknesses that are prevalent in the internal control of the company. Subsequent to the

identification of the weaknesses, an effort is made to determine the audit procedure to

objectively identify the steps that will alleviate the risks of material misstatement in the

financial statement of the company (William Jr, Glover & Prawitt, 2016).

Analysis of the ratios and the additional information as listed out by audit partner, Ms.

Leanne Hopkins:

Account Analysis Audit risk Audit steps to reduce

risk

Plantand

equipment

From the information that has been

given for consideration, it is observed

that there has been significant amount of

obsolescence on the part of the

company’s plant and equipment. The

reason being that, the requirement of the

industry has changed substantially over

the period of last 18 months (Wang, Li

& Li, 2015). The new demand is for

computer-aided machinery. This

substantial shift of requirement of the

industry has affected the plant and

machinery requirement of the company

significantly. The company will have to

There is several audit risk that

are involved in respect of the

review of the company’s

financial statements. Some of

them include non-financial

factors like the obsolescence

of the equipment used by the

company. The reduction in

the growth of the market etc.

Someof the key audit risks

present in the project involve

the concept of depreciation.

The reason being that the

policy adopted for

Some of the steps that

can be taken up by the

auditor to minimise

the risks include

physical verification

of the assets. This will

enable the auditor to

determine the

usabilityof the asset in

the near future. Taking

the advice of an expert

for determining the

correctamountof

depreciation that must

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5AUDITING THEORY AND PRACTICE

replace the majority percentage of its

stock with latest machinery. Failing to

do so will cost the company its client

and its future viability of operations.

After going through the warehouse of

the company, it is observed that the

stock of plant and equipment as kept

and manged by the company is lying

idle. This shows that the equipment

present in the stock of the company has

lost their power or ability to generate

any sort of revenue or profit for the

company. The investment of the

company on these assets has become

useless. In addition to this, the

depreciation of the machinery including

the method used for recognising the

same has to be reviewed by the

company to ensure that the depreciation

due to obsolescence is duel accounted

for by the company.

recognising depreciation at

the time of acquisition of the

machinery might have

changed over the period due

to the change of the

circumstances in the business

environment of the company.

Another significant aspect

corresponding to this account

includes the valuation of the

impact of the circumstances

on the recoverable amount of

the property, plant and

equipment.

be charged byte

company for the same.

Machinery

finance

liabilities

In the present case, the company has

taken immense loan to finance the latest

equipment. The machinery originally

purchased was financed by way of loans

too. This has led to immense finance

liabilities in respect of the assets

The audit risks that are

involved in reviewing these

include overlooking of the

present revenue generation

capability of the assets of the

company. The auditor might

There are several

methods or steps that

can be taken up by the

auditor to minimise

the risks this include:

a) Going

replace the majority percentage of its

stock with latest machinery. Failing to

do so will cost the company its client

and its future viability of operations.

After going through the warehouse of

the company, it is observed that the

stock of plant and equipment as kept

and manged by the company is lying

idle. This shows that the equipment

present in the stock of the company has

lost their power or ability to generate

any sort of revenue or profit for the

company. The investment of the

company on these assets has become

useless. In addition to this, the

depreciation of the machinery including

the method used for recognising the

same has to be reviewed by the

company to ensure that the depreciation

due to obsolescence is duel accounted

for by the company.

recognising depreciation at

the time of acquisition of the

machinery might have

changed over the period due

to the change of the

circumstances in the business

environment of the company.

Another significant aspect

corresponding to this account

includes the valuation of the

impact of the circumstances

on the recoverable amount of

the property, plant and

equipment.

be charged byte

company for the same.

Machinery

finance

liabilities

In the present case, the company has

taken immense loan to finance the latest

equipment. The machinery originally

purchased was financed by way of loans

too. This has led to immense finance

liabilities in respect of the assets

The audit risks that are

involved in reviewing these

include overlooking of the

present revenue generation

capability of the assets of the

company. The auditor might

There are several

methods or steps that

can be taken up by the

auditor to minimise

the risks this include:

a) Going

6AUDITING THEORY AND PRACTICE

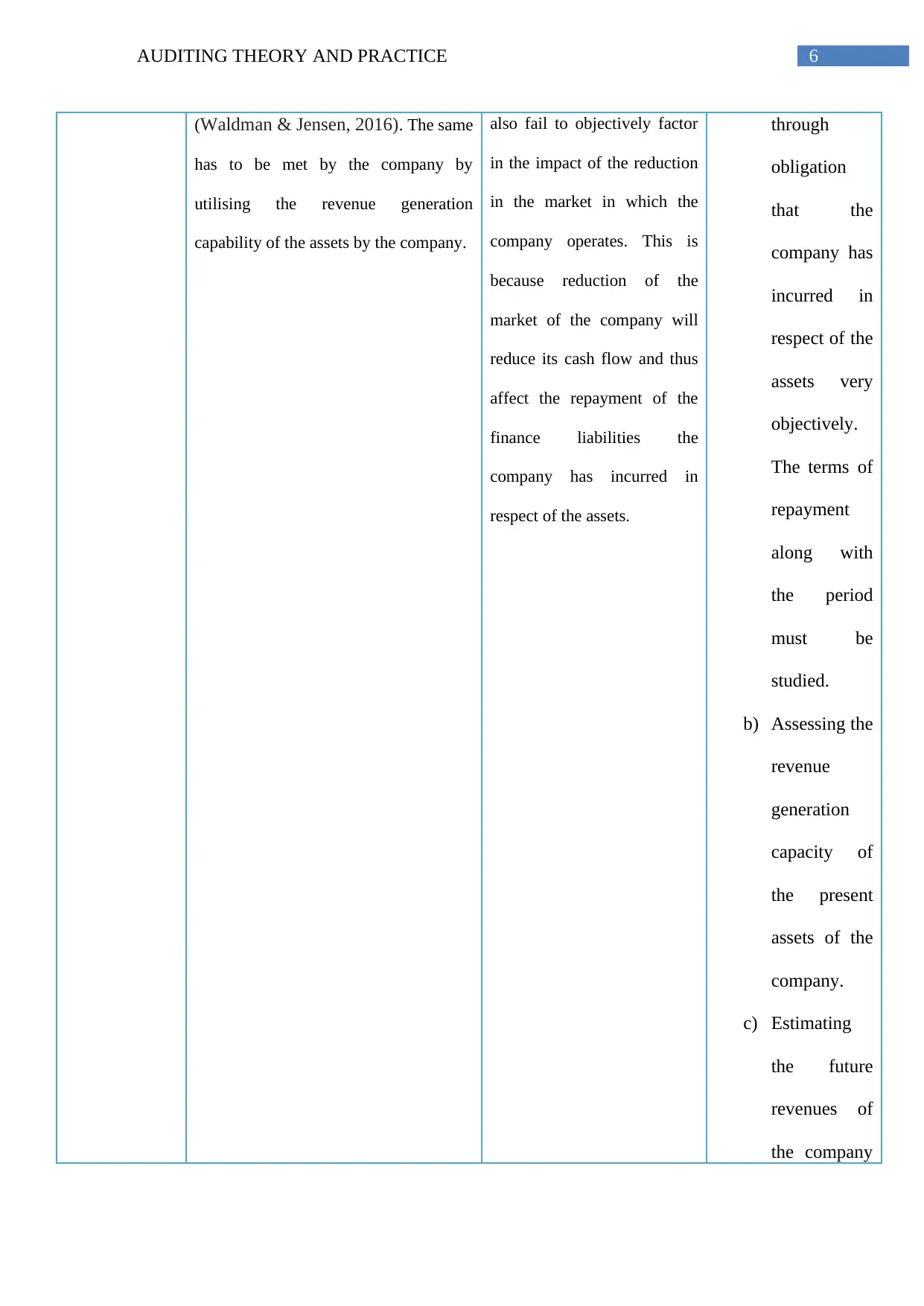

(Waldman & Jensen, 2016). The same

has to be met by the company by

utilising the revenue generation

capability of the assets by the company.

also fail to objectively factor

in the impact of the reduction

in the market in which the

company operates. This is

because reduction of the

market of the company will

reduce its cash flow and thus

affect the repayment of the

finance liabilities the

company has incurred in

respect of the assets.

through

obligation

that the

company has

incurred in

respect of the

assets very

objectively.

The terms of

repayment

along with

the period

must be

studied.

b) Assessing the

revenue

generation

capacity of

the present

assets of the

company.

c) Estimating

the future

revenues of

the company

(Waldman & Jensen, 2016). The same

has to be met by the company by

utilising the revenue generation

capability of the assets by the company.

also fail to objectively factor

in the impact of the reduction

in the market in which the

company operates. This is

because reduction of the

market of the company will

reduce its cash flow and thus

affect the repayment of the

finance liabilities the

company has incurred in

respect of the assets.

through

obligation

that the

company has

incurred in

respect of the

assets very

objectively.

The terms of

repayment

along with

the period

must be

studied.

b) Assessing the

revenue

generation

capacity of

the present

assets of the

company.

c) Estimating

the future

revenues of

the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7AUDITING THEORY AND PRACTICE

while

factoring in

the

Accounts

receivables

The account receivable so the company

have been –paying late payments to the

company. This has increased the days in

receivablesof the company above the

industry average.

There is a huge risk that the

amount shown by the

company as receivables

become will become bad debt.

The reason being the

substantial time taken up by

the debtors.

The auditor must ask

for debtor aging sheet

from the management

that will contain the

details of the debtors

and the delay they

have shown in

repayment.

Lease Income The company has been showing less

lease income in the unaudited

statements. There is also no relevant

data available for the lease income in

respect of the industry average.

There is a substantial risk in

respect of audit as there is no

parameter against which the

income can be measured.

The auditor must take

the suggestions from

the experts of the field

regarding the

sufficiency of the

lease income earned

by the company.

Analysis of the ratios and the additional information to determine the risks faced by the

company:

It is of utmost importance that the business risks faced by the company are properly discussed

because their respective implication affects the business in a multitude of ways. The business

risk is needed to be understood by the auditor in order to determine the areas of the

company’s financial statements that are most likely to contain material misstatements

while

factoring in

the

Accounts

receivables

The account receivable so the company

have been –paying late payments to the

company. This has increased the days in

receivablesof the company above the

industry average.

There is a huge risk that the

amount shown by the

company as receivables

become will become bad debt.

The reason being the

substantial time taken up by

the debtors.

The auditor must ask

for debtor aging sheet

from the management

that will contain the

details of the debtors

and the delay they

have shown in

repayment.

Lease Income The company has been showing less

lease income in the unaudited

statements. There is also no relevant

data available for the lease income in

respect of the industry average.

There is a substantial risk in

respect of audit as there is no

parameter against which the

income can be measured.

The auditor must take

the suggestions from

the experts of the field

regarding the

sufficiency of the

lease income earned

by the company.

Analysis of the ratios and the additional information to determine the risks faced by the

company:

It is of utmost importance that the business risks faced by the company are properly discussed

because their respective implication affects the business in a multitude of ways. The business

risk is needed to be understood by the auditor in order to determine the areas of the

company’s financial statements that are most likely to contain material misstatements

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8AUDITING THEORY AND PRACTICE

(Stewart & Shamdasani, 2014). This will increase the effectiveness and the efficiency of the

audit procedures applied by him.

Some of the business risks that are mentioned in the additional information are as follows:

a) The demand for the equipment owned by the company has decreased substantially

and there has been an increase in the demand for the computer operated machinery in

the market. This has rendered the costly old equipment’sof the company useless and

incapable of generating revenue in the future.

b) Due to the rising demand for the new machineries, the company had to increase its

borrowings for the purposeof acquiring tis new machineries.

c) There had been huge fluctuations in the metal market and it had effected the

operations of the company in the following manner:

i) The gold market has dropped around 24.95% since 2012.

ii) Iron ore market has dropped around 43.78% since the year 2012.

d) Due to increase in the demand of the new machinery, the company had to take huge

borrowings and thus it will have to bear higher financial obligations.

e) Along with the requirement of the new machineries, the company is facing the

requirement of new employees who are trained and skilled in operating these

machineries. As the workers of these machineries need to be more trained, they will

command higher salaries. This will increase the employee cost of the company

substantially.

The confirmation of the business risks identified in the additional information can be found in

the ratio analysis because of the following reasons:

a) The Return on Assets earned by the company is below the industry average.

(Stewart & Shamdasani, 2014). This will increase the effectiveness and the efficiency of the

audit procedures applied by him.

Some of the business risks that are mentioned in the additional information are as follows:

a) The demand for the equipment owned by the company has decreased substantially

and there has been an increase in the demand for the computer operated machinery in

the market. This has rendered the costly old equipment’sof the company useless and

incapable of generating revenue in the future.

b) Due to the rising demand for the new machineries, the company had to increase its

borrowings for the purposeof acquiring tis new machineries.

c) There had been huge fluctuations in the metal market and it had effected the

operations of the company in the following manner:

i) The gold market has dropped around 24.95% since 2012.

ii) Iron ore market has dropped around 43.78% since the year 2012.

d) Due to increase in the demand of the new machinery, the company had to take huge

borrowings and thus it will have to bear higher financial obligations.

e) Along with the requirement of the new machineries, the company is facing the

requirement of new employees who are trained and skilled in operating these

machineries. As the workers of these machineries need to be more trained, they will

command higher salaries. This will increase the employee cost of the company

substantially.

The confirmation of the business risks identified in the additional information can be found in

the ratio analysis because of the following reasons:

a) The Return on Assets earned by the company is below the industry average.

9AUDITING THEORY AND PRACTICE

b) The company is earning a reduced amount of Return on Equity corresponding to the

industry average.

c) The profit margin of the company is less than the industry average.

Some of the business risks that can be identified from the ratio analysis are as follows:

a) The difference between the audited and the unaudited financial ratios is substantially

high. This suggests that the company has been involving in many either intentional or

unintentional errors while reporting its annual results.

b) The days in account receivable of the company is significantly higher than that of the

industry average that suggests that the company is incurring additional opportunity

loss due to blocking of funds (Rezaee et al., 2018).

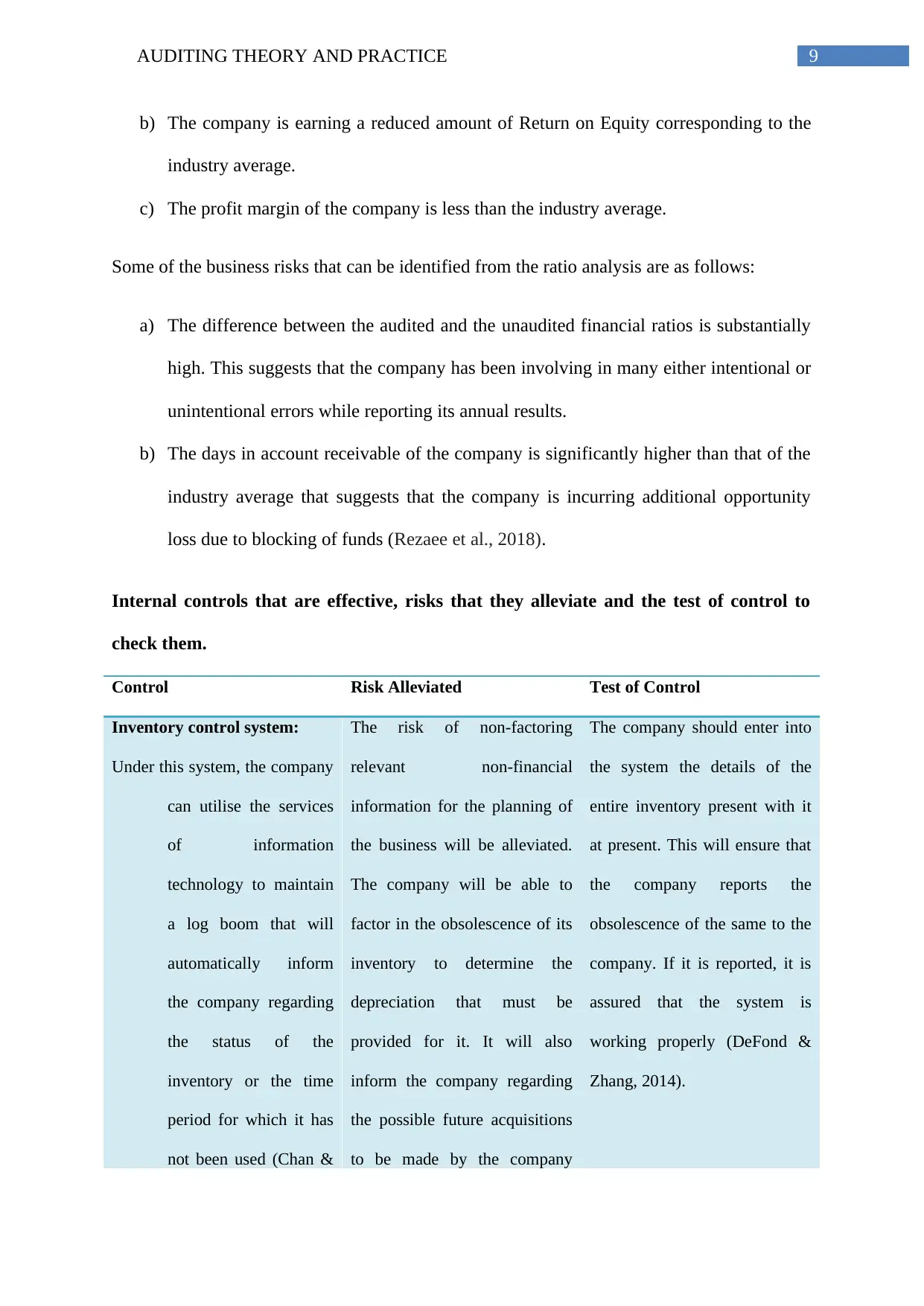

Internal controls that are effective, risks that they alleviate and the test of control to

check them.

Control Risk Alleviated Test of Control

Inventory control system:

Under this system, the company

can utilise the services

of information

technology to maintain

a log boom that will

automatically inform

the company regarding

the status of the

inventory or the time

period for which it has

not been used (Chan &

The risk of non-factoring

relevant non-financial

information for the planning of

the business will be alleviated.

The company will be able to

factor in the obsolescence of its

inventory to determine the

depreciation that must be

provided for it. It will also

inform the company regarding

the possible future acquisitions

to be made by the company

The company should enter into

the system the details of the

entire inventory present with it

at present. This will ensure that

the company reports the

obsolescence of the same to the

company. If it is reported, it is

assured that the system is

working properly (DeFond &

Zhang, 2014).

b) The company is earning a reduced amount of Return on Equity corresponding to the

industry average.

c) The profit margin of the company is less than the industry average.

Some of the business risks that can be identified from the ratio analysis are as follows:

a) The difference between the audited and the unaudited financial ratios is substantially

high. This suggests that the company has been involving in many either intentional or

unintentional errors while reporting its annual results.

b) The days in account receivable of the company is significantly higher than that of the

industry average that suggests that the company is incurring additional opportunity

loss due to blocking of funds (Rezaee et al., 2018).

Internal controls that are effective, risks that they alleviate and the test of control to

check them.

Control Risk Alleviated Test of Control

Inventory control system:

Under this system, the company

can utilise the services

of information

technology to maintain

a log boom that will

automatically inform

the company regarding

the status of the

inventory or the time

period for which it has

not been used (Chan &

The risk of non-factoring

relevant non-financial

information for the planning of

the business will be alleviated.

The company will be able to

factor in the obsolescence of its

inventory to determine the

depreciation that must be

provided for it. It will also

inform the company regarding

the possible future acquisitions

to be made by the company

The company should enter into

the system the details of the

entire inventory present with it

at present. This will ensure that

the company reports the

obsolescence of the same to the

company. If it is reported, it is

assured that the system is

working properly (DeFond &

Zhang, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10AUDITING THEORY AND PRACTICE

Vasarhelyi, 2018). (Collins, 2017).

Receivables management

softwares:

Under this, the company can

make us of software that

contains the details of the entire

debtors of the company. It will

automatically inform the

debtors when the payment will

be due from them.

Simultaneously the person

concerned with the management

of the receivables will be

informed regarding the

collection of the dues from the

debtors on time (Alles, Kogan

& Vasarhelyi, 2018).

Risk of bad debt will be

alleviated:

If the system is implemented by

the company, it will ensure that

the company is bake to reduce

its days in accounts receivables

and it will substantially reduce

the risk of bad debts.

The present debtors are paying

the company in a delayed time.

Hence, immediate application

of the system should inform the

management regarding the

debtors who are making

defaults in respect of among the

payments on time.

Use of effective and efficient

accounting softwares:

Presently the gap between the

audited and the unaudited

results of the company is

immense. This suggests that the

personnel’sof the company are

failing to make the records of

the company properly according

This will alleviate the risk of

faulty accounting recording

and treatment. This will

improve the efficiency of the

auditor too as he will be able

to focus on key performance

indicators of the company

rather than getting diverted

with small but numerous

The accounting software must

be equipped with all the latest

amendments that have been

brought about by the statute

recently.

Vasarhelyi, 2018). (Collins, 2017).

Receivables management

softwares:

Under this, the company can

make us of software that

contains the details of the entire

debtors of the company. It will

automatically inform the

debtors when the payment will

be due from them.

Simultaneously the person

concerned with the management

of the receivables will be

informed regarding the

collection of the dues from the

debtors on time (Alles, Kogan

& Vasarhelyi, 2018).

Risk of bad debt will be

alleviated:

If the system is implemented by

the company, it will ensure that

the company is bake to reduce

its days in accounts receivables

and it will substantially reduce

the risk of bad debts.

The present debtors are paying

the company in a delayed time.

Hence, immediate application

of the system should inform the

management regarding the

debtors who are making

defaults in respect of among the

payments on time.

Use of effective and efficient

accounting softwares:

Presently the gap between the

audited and the unaudited

results of the company is

immense. This suggests that the

personnel’sof the company are

failing to make the records of

the company properly according

This will alleviate the risk of

faulty accounting recording

and treatment. This will

improve the efficiency of the

auditor too as he will be able

to focus on key performance

indicators of the company

rather than getting diverted

with small but numerous

The accounting software must

be equipped with all the latest

amendments that have been

brought about by the statute

recently.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11AUDITING THEORY AND PRACTICE

to the statutory guidelines.

Hence, there is an immediate

requirement for its correction.

errors in the financial

statements of the company.

Identification of the weaknesses in the internal control for contract payroll:

Some of the weaknesses that the company experiences in the internal control of its contract

payroll are as follows:

a) The entry of the employee details by the payroll clerk is made using a hard copy

containing various sortsso details of the employee. The company must make sure that

it should maintain the soft copy of the details as well. The same should be attached

with the employee details in the system (Hayes, Wallage & Gortemaker, 2014). As

the clerk may claim to lose the hard copy.

b) The timing of the work hours are manually recorded and entered by the employee. It

is not possible for the contract’s manager to monitor each employee if his or her

numbers are significant (Freeman et al., 2017).

c) The entire system is automatic. In case of failure to change the amendments in the

regulatory requirements like that of the tax rate etc., the entire system along with the

corresponding information will give misleading results.

d) The bank log in details must not be present with the accountant. At least it must not

grant him the ability of processing of payments. This may result in manipulation of

funds by him.

e) The calculation of the regular payments and the payments regarding the

superannuation and other funds must be separate. As it will eliminate the risk of faulty

methods being used by the company for computation of the same. It will increase the

transference of the method employed by the company (Hargie, 2016).

to the statutory guidelines.

Hence, there is an immediate

requirement for its correction.

errors in the financial

statements of the company.

Identification of the weaknesses in the internal control for contract payroll:

Some of the weaknesses that the company experiences in the internal control of its contract

payroll are as follows:

a) The entry of the employee details by the payroll clerk is made using a hard copy

containing various sortsso details of the employee. The company must make sure that

it should maintain the soft copy of the details as well. The same should be attached

with the employee details in the system (Hayes, Wallage & Gortemaker, 2014). As

the clerk may claim to lose the hard copy.

b) The timing of the work hours are manually recorded and entered by the employee. It

is not possible for the contract’s manager to monitor each employee if his or her

numbers are significant (Freeman et al., 2017).

c) The entire system is automatic. In case of failure to change the amendments in the

regulatory requirements like that of the tax rate etc., the entire system along with the

corresponding information will give misleading results.

d) The bank log in details must not be present with the accountant. At least it must not

grant him the ability of processing of payments. This may result in manipulation of

funds by him.

e) The calculation of the regular payments and the payments regarding the

superannuation and other funds must be separate. As it will eliminate the risk of faulty

methods being used by the company for computation of the same. It will increase the

transference of the method employed by the company (Hargie, 2016).

12AUDITING THEORY AND PRACTICE

Conclusion:

After conducting the detailed analysis of the various aspects of the company, it was found

that there is substantial business risk present in the operations of the business. This includes

the obsolescence of the equipment of the company and the shrinking market. In addition to

this, it was seen that there were several weaknesses in the internal control of the company.

Those can be alleviated by optimal utilisation of the softwares by the company.

Conclusion:

After conducting the detailed analysis of the various aspects of the company, it was found

that there is substantial business risk present in the operations of the business. This includes

the obsolescence of the equipment of the company and the shrinking market. In addition to

this, it was seen that there were several weaknesses in the internal control of the company.

Those can be alleviated by optimal utilisation of the softwares by the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.