BMP6015 Financial Reporting: Risk Management Strategies at Tesco PLC

VerifiedAdded on 2023/06/18

|10

|2317

|226

Report

AI Summary

This report provides an analysis of risk management at Tesco PLC within the context of financial reporting. It reviews real-world examples and academic models, considering the motivations behind the adoption of risk management strategies and their reported benefits and outcomes. The report also includes a critical appraisal of the current business environment in relation to risk management, highlighting both internal and external hazards. It concludes that while Tesco had risk management procedures in place, the company failed to adequately detect and manage fraudulent transactions, emphasizing the need for improved compensatory mechanisms and responses to potential risks. The document is available on Desklib, a platform offering a wealth of study resources for students.

BSc (Hons) Business Management (Finance)

BMP6015

Financial Reporting for Management

Assessment 1

Individual Report (Article review)

BMP6015

Financial Reporting for Management

Assessment 1

Individual Report (Article review)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION................................................................................................................................3

PART 1..............................................................................................................................................3

Review of real-world (and published) example, relating to text-book techniques and

academic models considering aspects and the motivation behind the adoption and reported

benefits and outcomes................................................................................................................3

PART 2..............................................................................................................................................6

A critical appraisal of the current business environment in relation to the topic of choice.......6

CONCLUSION...................................................................................................................................7

REFERENCES.....................................................................................................................................8

INTRODUCTION................................................................................................................................3

PART 1..............................................................................................................................................3

Review of real-world (and published) example, relating to text-book techniques and

academic models considering aspects and the motivation behind the adoption and reported

benefits and outcomes................................................................................................................3

PART 2..............................................................................................................................................6

A critical appraisal of the current business environment in relation to the topic of choice.......6

CONCLUSION...................................................................................................................................7

REFERENCES.....................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial reporting is more than just using financial records and accounting records to

present data. Non-monetary as well as monetary information is included in financial reporting. If

accounting information comprises critical information, the rationale for its existence is expressed

through timetables and explanatory comments, provided data is accurate and understandable.

The primary goal of reporting data is to guarantee that everyone who uses it (internally or

externally) may make an educated choice tailored to the needs (Sander and et.al, 2020). To

prepare this report selected topic is “Risk Management”. Every organisation applied this term as

per their requirement and select different risk management strategy to effectively run their

business in a proper manner. Along with selecting a real world example and compare in current

business environment in present economy.

PART 1

Review of real-world (and published) example, relating to text-book techniques and academic

models considering aspects and the motivation behind the adoption and reported benefits

and outcomes.

Creating a risk management team may obstruct risk control because workers are more

vulnerable to the risk than with the customer, therefore we're just focused with the customer and

what might go incorrect. One of the reasons of successful organizations is risk assessment;

employees utilize it without recognizing it since it is part of their duties. They must take

responsibility for their acts.

The primary goal of risk management is to ensure about strategy goals after that apply

appropriate strategy. Enterprise Risk Management (ERM) a wide ranging approaches to

managing risk, and the balanced scorecard, a frequently used strategy implementation

mechanism. Tesco plc, one of the UK's large stores, has been used as a example study to

demonstrate how ERM may be integrated into an organization's strategic management system

(Sun, Bi and Yin, 2020).

Financial reporting is more than just using financial records and accounting records to

present data. Non-monetary as well as monetary information is included in financial reporting. If

accounting information comprises critical information, the rationale for its existence is expressed

through timetables and explanatory comments, provided data is accurate and understandable.

The primary goal of reporting data is to guarantee that everyone who uses it (internally or

externally) may make an educated choice tailored to the needs (Sander and et.al, 2020). To

prepare this report selected topic is “Risk Management”. Every organisation applied this term as

per their requirement and select different risk management strategy to effectively run their

business in a proper manner. Along with selecting a real world example and compare in current

business environment in present economy.

PART 1

Review of real-world (and published) example, relating to text-book techniques and academic

models considering aspects and the motivation behind the adoption and reported benefits

and outcomes.

Creating a risk management team may obstruct risk control because workers are more

vulnerable to the risk than with the customer, therefore we're just focused with the customer and

what might go incorrect. One of the reasons of successful organizations is risk assessment;

employees utilize it without recognizing it since it is part of their duties. They must take

responsibility for their acts.

The primary goal of risk management is to ensure about strategy goals after that apply

appropriate strategy. Enterprise Risk Management (ERM) a wide ranging approaches to

managing risk, and the balanced scorecard, a frequently used strategy implementation

mechanism. Tesco plc, one of the UK's large stores, has been used as a example study to

demonstrate how ERM may be integrated into an organization's strategic management system

(Sun, Bi and Yin, 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

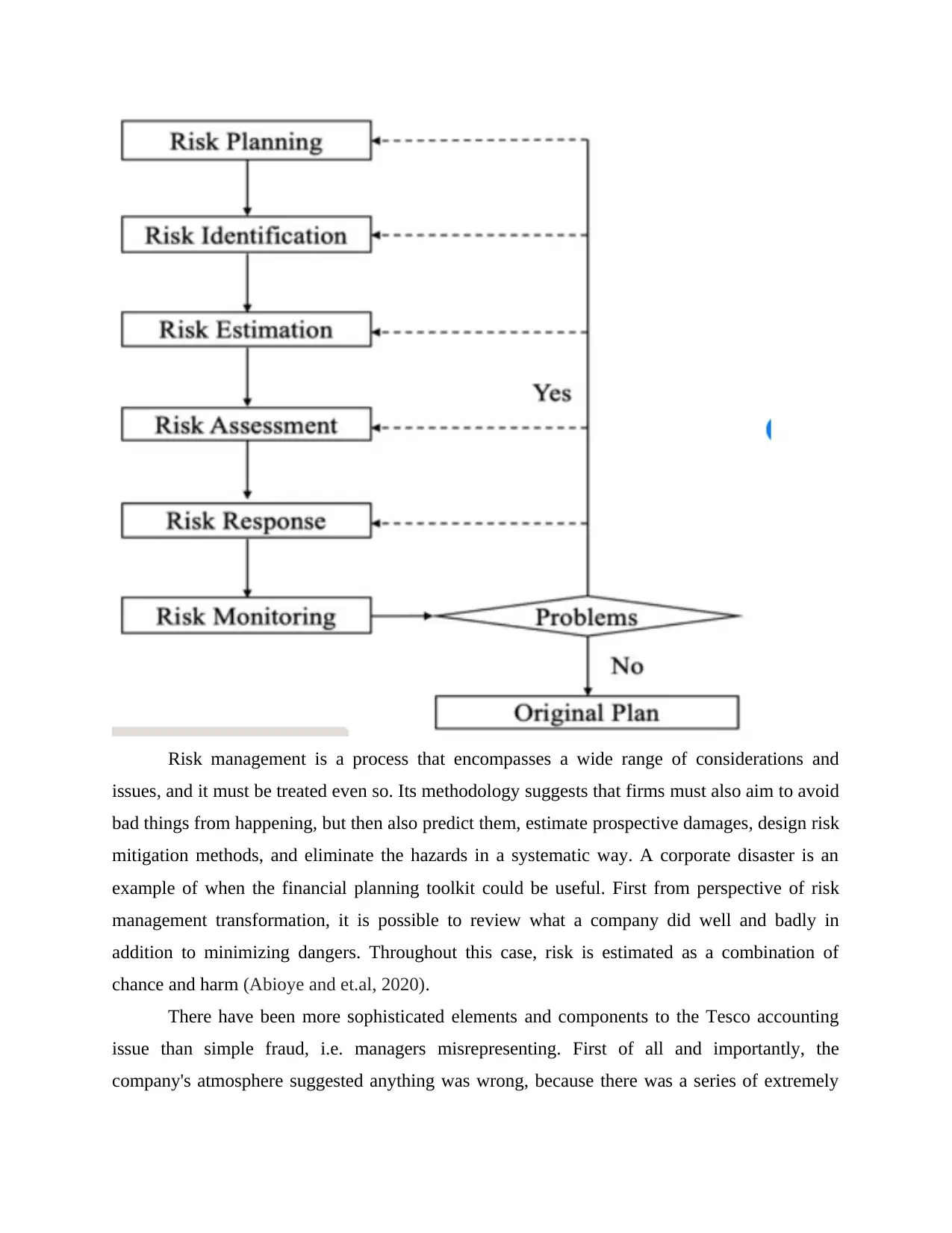

Risk management is a process that encompasses a wide range of considerations and

issues, and it must be treated even so. Its methodology suggests that firms must also aim to avoid

bad things from happening, but then also predict them, estimate prospective damages, design risk

mitigation methods, and eliminate the hazards in a systematic way. A corporate disaster is an

example of when the financial planning toolkit could be useful. First from perspective of risk

management transformation, it is possible to review what a company did well and badly in

addition to minimizing dangers. Throughout this case, risk is estimated as a combination of

chance and harm (Abioye and et.al, 2020).

There have been more sophisticated elements and components to the Tesco accounting

issue than simple fraud, i.e. managers misrepresenting. First of all and importantly, the

company's atmosphere suggested anything was wrong, because there was a series of extremely

issues, and it must be treated even so. Its methodology suggests that firms must also aim to avoid

bad things from happening, but then also predict them, estimate prospective damages, design risk

mitigation methods, and eliminate the hazards in a systematic way. A corporate disaster is an

example of when the financial planning toolkit could be useful. First from perspective of risk

management transformation, it is possible to review what a company did well and badly in

addition to minimizing dangers. Throughout this case, risk is estimated as a combination of

chance and harm (Abioye and et.al, 2020).

There have been more sophisticated elements and components to the Tesco accounting

issue than simple fraud, i.e. managers misrepresenting. First of all and importantly, the

company's atmosphere suggested anything was wrong, because there was a series of extremely

quiet resignations since the scandal broke in September 2014. As is now obvious, many Tesco

workers chose to resign because they felt forced by the grossly misrepresenting processes and

were willing to leave the firm rather than participate in what they thought to be illegal behavior.

Very importantly, the approaching disaster was anticipated not just by failures, but also from the

telecoms firm's responses (Ullah and et.al, 2021).

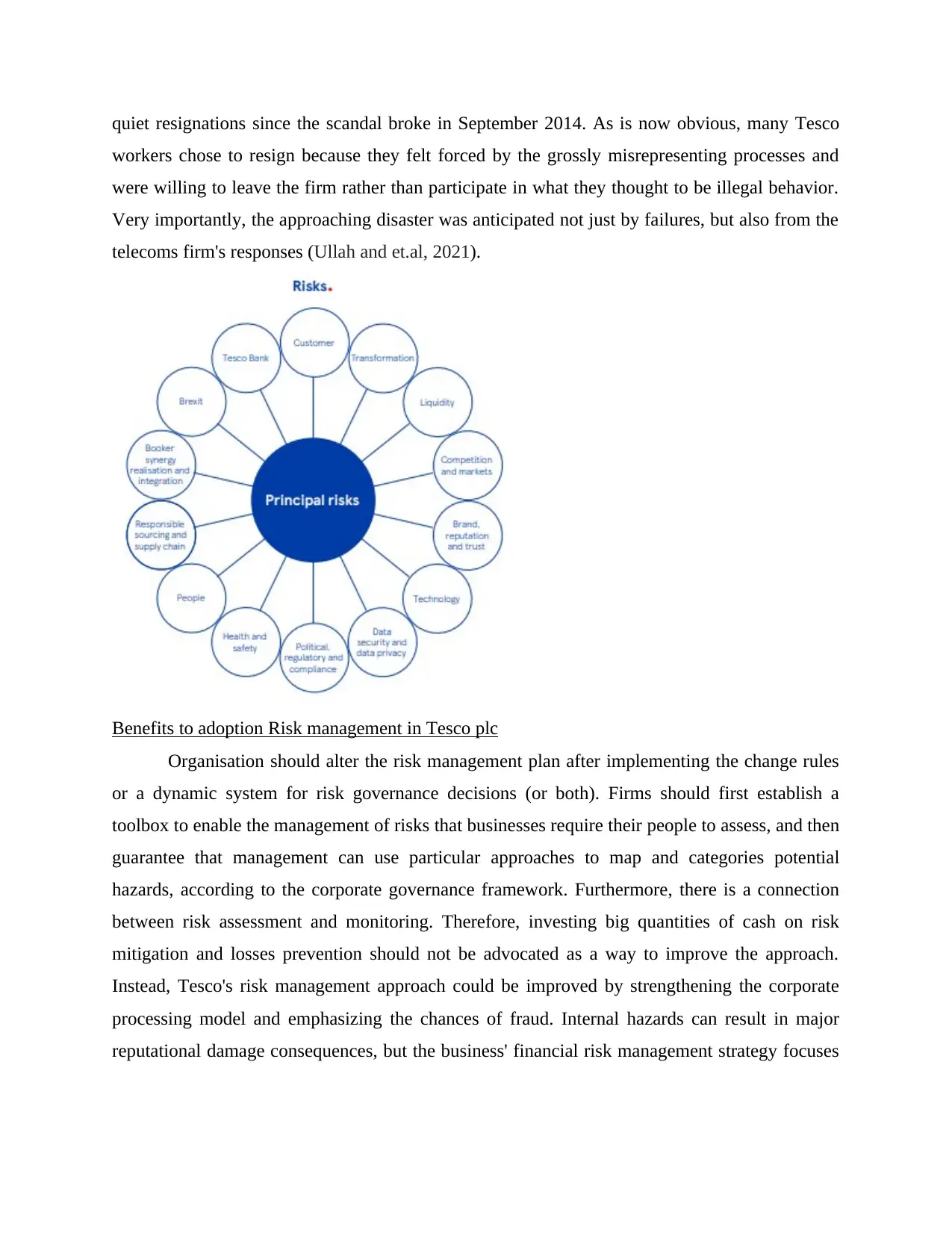

Benefits to adoption Risk management in Tesco plc

Organisation should alter the risk management plan after implementing the change rules

or a dynamic system for risk governance decisions (or both). Firms should first establish a

toolbox to enable the management of risks that businesses require their people to assess, and then

guarantee that management can use particular approaches to map and categories potential

hazards, according to the corporate governance framework. Furthermore, there is a connection

between risk assessment and monitoring. Therefore, investing big quantities of cash on risk

mitigation and losses prevention should not be advocated as a way to improve the approach.

Instead, Tesco's risk management approach could be improved by strengthening the corporate

processing model and emphasizing the chances of fraud. Internal hazards can result in major

reputational damage consequences, but the business' financial risk management strategy focuses

workers chose to resign because they felt forced by the grossly misrepresenting processes and

were willing to leave the firm rather than participate in what they thought to be illegal behavior.

Very importantly, the approaching disaster was anticipated not just by failures, but also from the

telecoms firm's responses (Ullah and et.al, 2021).

Benefits to adoption Risk management in Tesco plc

Organisation should alter the risk management plan after implementing the change rules

or a dynamic system for risk governance decisions (or both). Firms should first establish a

toolbox to enable the management of risks that businesses require their people to assess, and then

guarantee that management can use particular approaches to map and categories potential

hazards, according to the corporate governance framework. Furthermore, there is a connection

between risk assessment and monitoring. Therefore, investing big quantities of cash on risk

mitigation and losses prevention should not be advocated as a way to improve the approach.

Instead, Tesco's risk management approach could be improved by strengthening the corporate

processing model and emphasizing the chances of fraud. Internal hazards can result in major

reputational damage consequences, but the business' financial risk management strategy focuses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

more on mitigating external threats. Updating the processes that recognize and report unlawful

internal practices should improve the risk management plan (Naseem and et.al, 2020).

Motivation to apply risk management in Tesco

Customers will receive dependable assistance from a renowned organisation that

manages risk well.

Whenever risks are visible and the risk management process is properly explained and

disclosed, the interest rate demanded by shareholders will be lower.

Whenever methods, permissions, restrictions, desired returns, and incentive criteria are

properly established and articulated, employee motivation improves.

The trust of regulatory authority in the person's decision to regulate the risks connected

with its operations strengthens collaboration with the government even more.

Outcomes

It is vital to outline the major features of Tesco's risk management strategy after

commenting on each component of the risk assessment cycle. First of all and foremost, cost and

benefit assessment is a critical characteristic of effective risk management. This study is made up

of a series of interrelated measurements and activities, such as avoidance, division, integration,

and transference, to name a few. To minimize risk, an organisation should compute the overall

possible liability and then implement the practices necessary to not only prevent bad situations or

considerations that are probable to occur in bad results, but also to disseminate positions,

features, and assets in such a way that the probability of loss is reduced. Tesco has implemented

a variety of regulation initiatives to limit the spread of fraud. Nevertheless, in the example at

hand, the instruments were found to be insufficiently accurate, and fraudulent activities had been

established in the organisation for a long time until they were discovered.

PART 2

A critical appraisal of the current business environment in relation to the topic of choice.

Internally and externally types of hazards might both exist. Vulnerabilities are those that

the administration does not have direct control over. Political difficulties, currency values, and

borrowing costs are just a few examples. Internal risks, on the other extreme, encompass things

like non-compliance and data infiltration. Absent risk management, a company's future goals will

internal practices should improve the risk management plan (Naseem and et.al, 2020).

Motivation to apply risk management in Tesco

Customers will receive dependable assistance from a renowned organisation that

manages risk well.

Whenever risks are visible and the risk management process is properly explained and

disclosed, the interest rate demanded by shareholders will be lower.

Whenever methods, permissions, restrictions, desired returns, and incentive criteria are

properly established and articulated, employee motivation improves.

The trust of regulatory authority in the person's decision to regulate the risks connected

with its operations strengthens collaboration with the government even more.

Outcomes

It is vital to outline the major features of Tesco's risk management strategy after

commenting on each component of the risk assessment cycle. First of all and foremost, cost and

benefit assessment is a critical characteristic of effective risk management. This study is made up

of a series of interrelated measurements and activities, such as avoidance, division, integration,

and transference, to name a few. To minimize risk, an organisation should compute the overall

possible liability and then implement the practices necessary to not only prevent bad situations or

considerations that are probable to occur in bad results, but also to disseminate positions,

features, and assets in such a way that the probability of loss is reduced. Tesco has implemented

a variety of regulation initiatives to limit the spread of fraud. Nevertheless, in the example at

hand, the instruments were found to be insufficiently accurate, and fraudulent activities had been

established in the organisation for a long time until they were discovered.

PART 2

A critical appraisal of the current business environment in relation to the topic of choice.

Internally and externally types of hazards might both exist. Vulnerabilities are those that

the administration does not have direct control over. Political difficulties, currency values, and

borrowing costs are just a few examples. Internal risks, on the other extreme, encompass things

like non-compliance and data infiltration. Absent risk management, a company's future goals will

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be impossible to establish. If a corporation sets goals without considering the dangers, it's likely

that they'll lose focus if one of these hazards manifests itself. Many businesses have introduced

risk management divisions to their workforce in recent times (Ramanpong and et.al, 2020).

It is the responsibility of this committee to manage hazards, design strategies to minimize

such uncertainties, execute out the few strategies, and motivate all business personnel to join in

all of these measures. While large companies face more hazards, their approaches should be

more complicated. Furthermore, the risk management team is responsible for assessing all risks

and determining whether ones are critical to the firm's earnings. The main threats were those that

had the ability to harm the company, so they should be prioritized. The ultimate objective of the

risk is to guarantee that the organization must take only certain risks that will enable it achieve

its major objectives while keeping most of the other risks in check. (Atanga, 2020).

Companies will come to grasp those risks needed to be controlled after they obtained a

fresh perspective on what hazards may imply to their activities in terms of damages. While it is

evident that all of our activities carry some level of risk, it is also apparent that risk cannot be

managed in the same manner for all occurrences. Problems can't be dealt with only on the basis

of logic, disregarding the diverse risks of loss associated with different environments. The

unpredictability of current state of the economy has had a huge influence over how firms operate

presently. Businesses which used to function smoothly based on projections and forecasts are

increasingly refusing to make strong corporate choices. Risk management has become a major

concern for businesses. Risk is the key complicated issue in any organization. As a consequence,

companies are constantly concentrating on recognizing and mitigating the risks until they have a

detrimental influence on their business. Companies will be able to execute more confident

lengthy financial choices if they have the risk appetite. Their awareness of the challenges they

face will give them with a number of options for coping with unforeseen challenges (Wakefield,

2020).

Modern enterprises are exposed to a wide range of hazards and threats. Historically,

organizations managed their key risks by having each department manage its own company.

Indeed, many multinational corporations have coped with expansion by delegating increasing

amounts of authority to heads of various divisions, leaving the CEO and other senior executives

out of the day-to-day activities. This method, however, can lead to an error and risk

magnification or misrecognition when firms develop and take on additional divisions or

that they'll lose focus if one of these hazards manifests itself. Many businesses have introduced

risk management divisions to their workforce in recent times (Ramanpong and et.al, 2020).

It is the responsibility of this committee to manage hazards, design strategies to minimize

such uncertainties, execute out the few strategies, and motivate all business personnel to join in

all of these measures. While large companies face more hazards, their approaches should be

more complicated. Furthermore, the risk management team is responsible for assessing all risks

and determining whether ones are critical to the firm's earnings. The main threats were those that

had the ability to harm the company, so they should be prioritized. The ultimate objective of the

risk is to guarantee that the organization must take only certain risks that will enable it achieve

its major objectives while keeping most of the other risks in check. (Atanga, 2020).

Companies will come to grasp those risks needed to be controlled after they obtained a

fresh perspective on what hazards may imply to their activities in terms of damages. While it is

evident that all of our activities carry some level of risk, it is also apparent that risk cannot be

managed in the same manner for all occurrences. Problems can't be dealt with only on the basis

of logic, disregarding the diverse risks of loss associated with different environments. The

unpredictability of current state of the economy has had a huge influence over how firms operate

presently. Businesses which used to function smoothly based on projections and forecasts are

increasingly refusing to make strong corporate choices. Risk management has become a major

concern for businesses. Risk is the key complicated issue in any organization. As a consequence,

companies are constantly concentrating on recognizing and mitigating the risks until they have a

detrimental influence on their business. Companies will be able to execute more confident

lengthy financial choices if they have the risk appetite. Their awareness of the challenges they

face will give them with a number of options for coping with unforeseen challenges (Wakefield,

2020).

Modern enterprises are exposed to a wide range of hazards and threats. Historically,

organizations managed their key risks by having each department manage its own company.

Indeed, many multinational corporations have coped with expansion by delegating increasing

amounts of authority to heads of various divisions, leaving the CEO and other senior executives

out of the day-to-day activities. This method, however, can lead to an error and risk

magnification or misrecognition when firms develop and take on additional divisions or

economic sectors. Every department of a company is it's own "silo" in this instance. They can't

observe other units' risk exposures, how their risk exposures connect with those other

organizations, or how varied exposure times between components connect overall. As a result,

whereas a line manager may perceive possible risk, he or she may not understand (or be capable

of understanding) the implications of that danger to other elements of the organisation.

CONCLUSION

As per the above report it has been concluded that Tesco seems to have failed to detect

fraudulent transactions while also identifying and assessing their risks; at the same time, the

scandal broke so before the accounting hole reached 0.5 percent of annual sales, demonstrating

that risk management procedures were in place. Whereas if damages caused by the hazard had

been effectively investigated and managed, the business would have responded to symptoms of

dishonesty even before dark matter emerged. In addition, feedback would have improved

company procedures, judgments and examination plans. The company's main issue is that it

didn't respond adequately to the looming pensions. In the future, greater compensatory

mechanisms would need to be built and deployed.

observe other units' risk exposures, how their risk exposures connect with those other

organizations, or how varied exposure times between components connect overall. As a result,

whereas a line manager may perceive possible risk, he or she may not understand (or be capable

of understanding) the implications of that danger to other elements of the organisation.

CONCLUSION

As per the above report it has been concluded that Tesco seems to have failed to detect

fraudulent transactions while also identifying and assessing their risks; at the same time, the

scandal broke so before the accounting hole reached 0.5 percent of annual sales, demonstrating

that risk management procedures were in place. Whereas if damages caused by the hazard had

been effectively investigated and managed, the business would have responded to symptoms of

dishonesty even before dark matter emerged. In addition, feedback would have improved

company procedures, judgments and examination plans. The company's main issue is that it

didn't respond adequately to the looming pensions. In the future, greater compensatory

mechanisms would need to be built and deployed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journal

Abioye, T. E. and et.al, 2020. Toward ontology‐based risk management framework for software

projects: An empirical study. Journal of Software: Evolution and Process. 32(12).

p.e2269.

Atanga, R. A., 2020. The role of local community leaders in flood disaster risk management

strategy making in Accra. International journal of disaster risk reduction. 43. p.101358.

Naseem, T. and et.al, 2020. Corporate social responsibility engagement and firm performance in

Asia Pacific: The role of enterprise risk management. Corporate Social Responsibility

and Environmental Management. 27(2). pp.501-513.

Ramanpong, J. and et.al, 2020. Risk management in suburban forest recreation areas: A

retrospective analysis of illness cases. Urban Forestry & Urban Greening. 53. p.126710.

Sander, L. and et.al, 2020. Suicide risk management in research on internet-based interventions

for depression: A synthesis of the current state and recommendations for future

research. Journal of affective disorders. 263. pp.676-683.

Sun, Y., Bi, K. and Yin, S., 2020. Measuring and integrating risk management into green

innovation practices for green manufacturing under the global value

chain. Sustainability. 12(2). p.545.

Wakefield, S., 2020. Making nature into infrastructure: the construction of oysters as a risk

management solution in New York City. Environment and Planning E: Nature and

Space. 3(3). pp.761-785.

Ullah, F. and et.al, 2021. Risk management in sustainable smart cities governance: A TOE

framework. Technological Forecasting and Social Change. 167. p.120743.

Online

Risk management at Tesco Plc, 2008. [Online]. Available through;<

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1358776>

Woods, Margaret, Linking Risk Management to Strategic Controls: A Case Study of Tesco Plc

(February 1, 2008). International Journal of Risk Assessment and Management, Vol. 7,

No. 8, pp. 1074-1088, 2008, Available at SSRN: https://ssrn.com/abstract=1358776

Accounting Scandal in Tesco Plc, 2017. [Online]. Available through; <

https://ivypanda.com/essays/tesco-accounting-scandal-risk-management/>

Books and Journal

Abioye, T. E. and et.al, 2020. Toward ontology‐based risk management framework for software

projects: An empirical study. Journal of Software: Evolution and Process. 32(12).

p.e2269.

Atanga, R. A., 2020. The role of local community leaders in flood disaster risk management

strategy making in Accra. International journal of disaster risk reduction. 43. p.101358.

Naseem, T. and et.al, 2020. Corporate social responsibility engagement and firm performance in

Asia Pacific: The role of enterprise risk management. Corporate Social Responsibility

and Environmental Management. 27(2). pp.501-513.

Ramanpong, J. and et.al, 2020. Risk management in suburban forest recreation areas: A

retrospective analysis of illness cases. Urban Forestry & Urban Greening. 53. p.126710.

Sander, L. and et.al, 2020. Suicide risk management in research on internet-based interventions

for depression: A synthesis of the current state and recommendations for future

research. Journal of affective disorders. 263. pp.676-683.

Sun, Y., Bi, K. and Yin, S., 2020. Measuring and integrating risk management into green

innovation practices for green manufacturing under the global value

chain. Sustainability. 12(2). p.545.

Wakefield, S., 2020. Making nature into infrastructure: the construction of oysters as a risk

management solution in New York City. Environment and Planning E: Nature and

Space. 3(3). pp.761-785.

Ullah, F. and et.al, 2021. Risk management in sustainable smart cities governance: A TOE

framework. Technological Forecasting and Social Change. 167. p.120743.

Online

Risk management at Tesco Plc, 2008. [Online]. Available through;<

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1358776>

Woods, Margaret, Linking Risk Management to Strategic Controls: A Case Study of Tesco Plc

(February 1, 2008). International Journal of Risk Assessment and Management, Vol. 7,

No. 8, pp. 1074-1088, 2008, Available at SSRN: https://ssrn.com/abstract=1358776

Accounting Scandal in Tesco Plc, 2017. [Online]. Available through; <

https://ivypanda.com/essays/tesco-accounting-scandal-risk-management/>

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.