BMS512 - Financial Performance Analysis of R plc Using Ratios

VerifiedAdded on 2023/06/15

|7

|1362

|280

Report

AI Summary

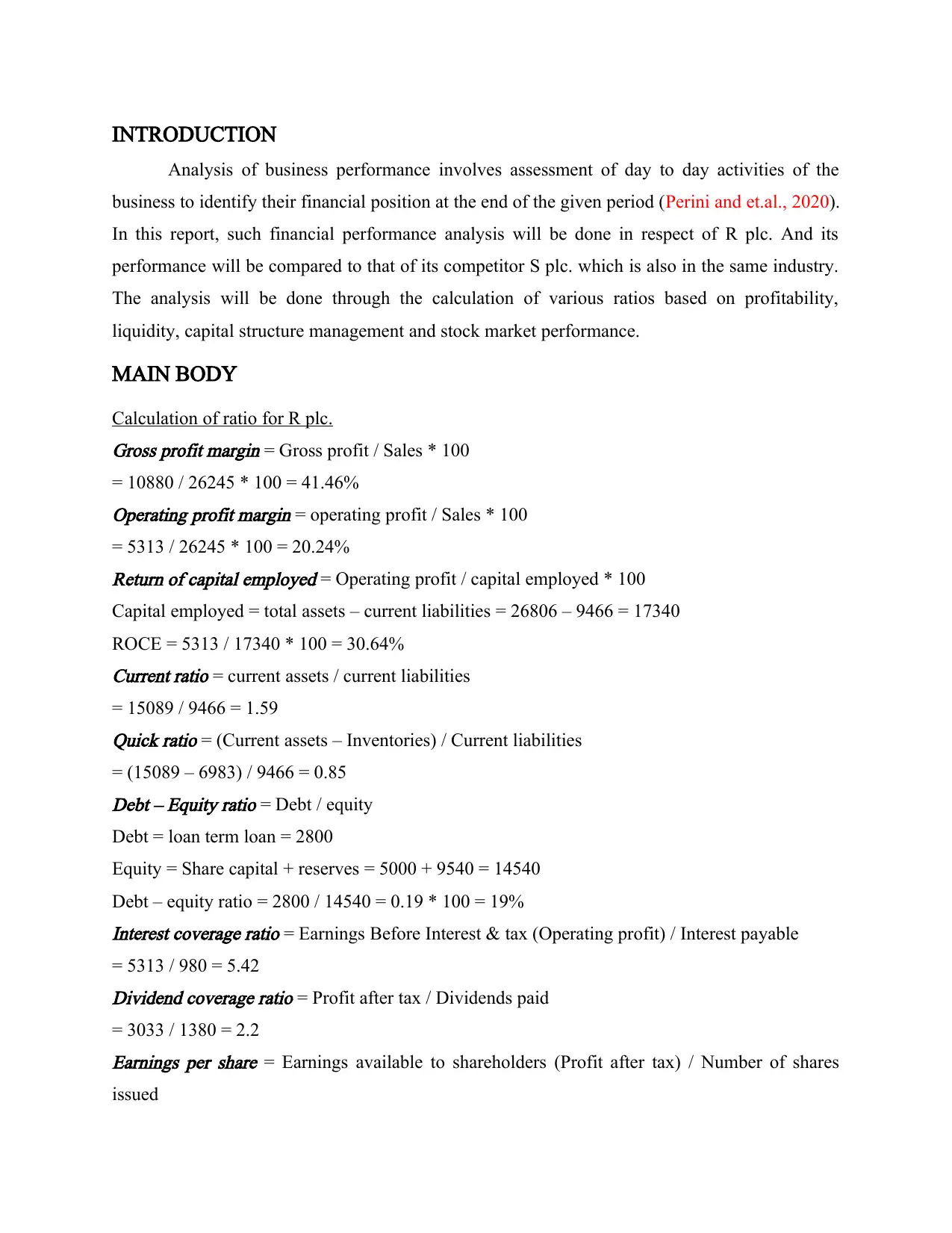

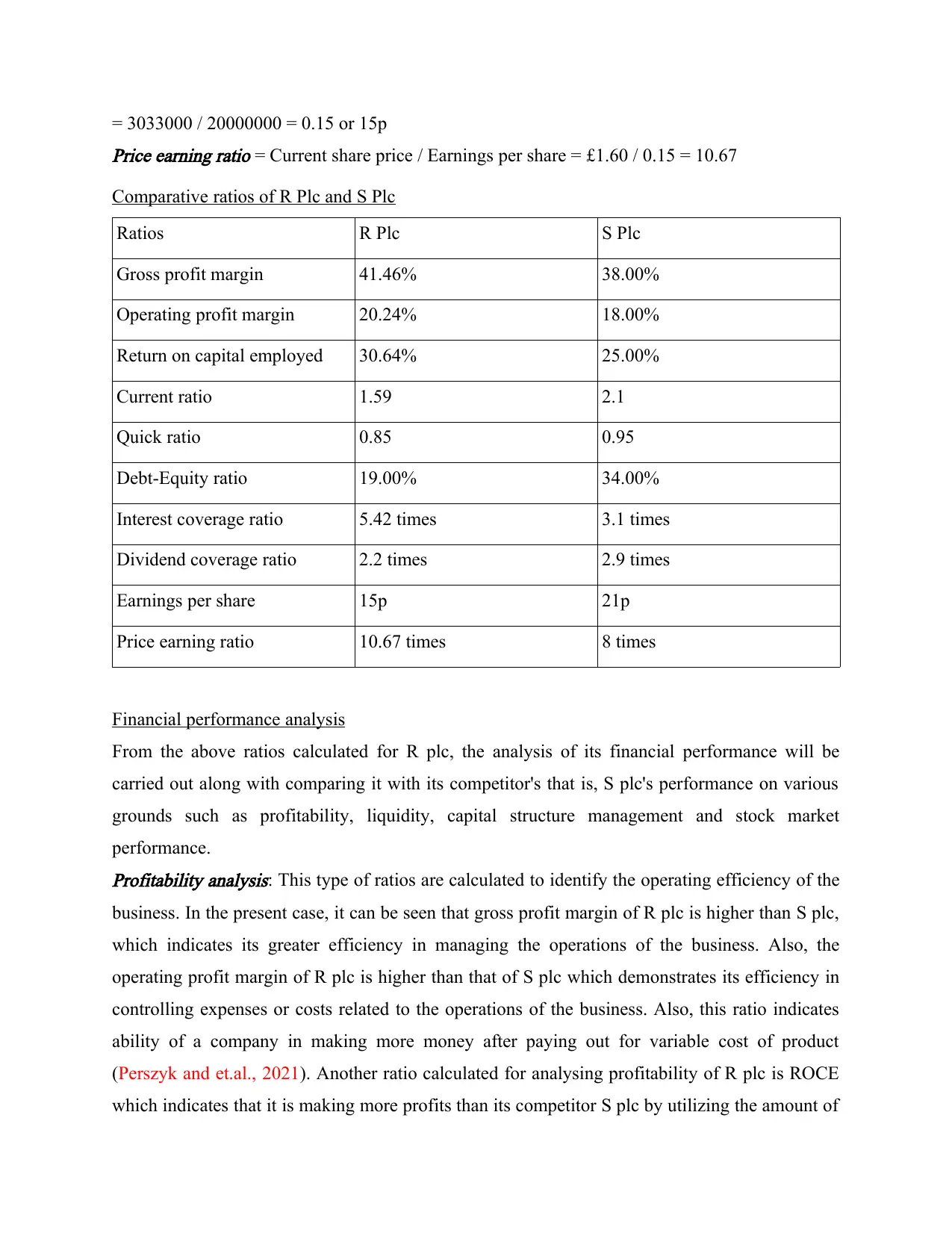

This report provides a comprehensive financial performance analysis of R plc, utilizing various financial ratios related to profitability, liquidity, capital structure management, and stock market performance. The analysis includes a comparison with R plc's competitor, S plc, highlighting key differences in gross profit margin, operating profit margin, return on capital employed (ROCE), current ratio, quick ratio, debt-equity ratio, interest coverage ratio, dividend coverage ratio, earnings per share (EPS), and price-earnings (P/E) ratio. The findings indicate that R plc outperforms S plc in profitability and capital structure management but lags in liquidity, suggesting areas for improvement. The report concludes that while R plc demonstrates strong financial health overall, attention should be given to enhancing its liquidity position to meet short-term obligations more effectively. Desklib offers a range of study tools and resources for students seeking similar financial analysis reports and solved assignments.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.