Impact of Gender Diversity on ASX Company Board Performance

VerifiedAdded on 2023/06/03

|10

|1783

|477

Report

AI Summary

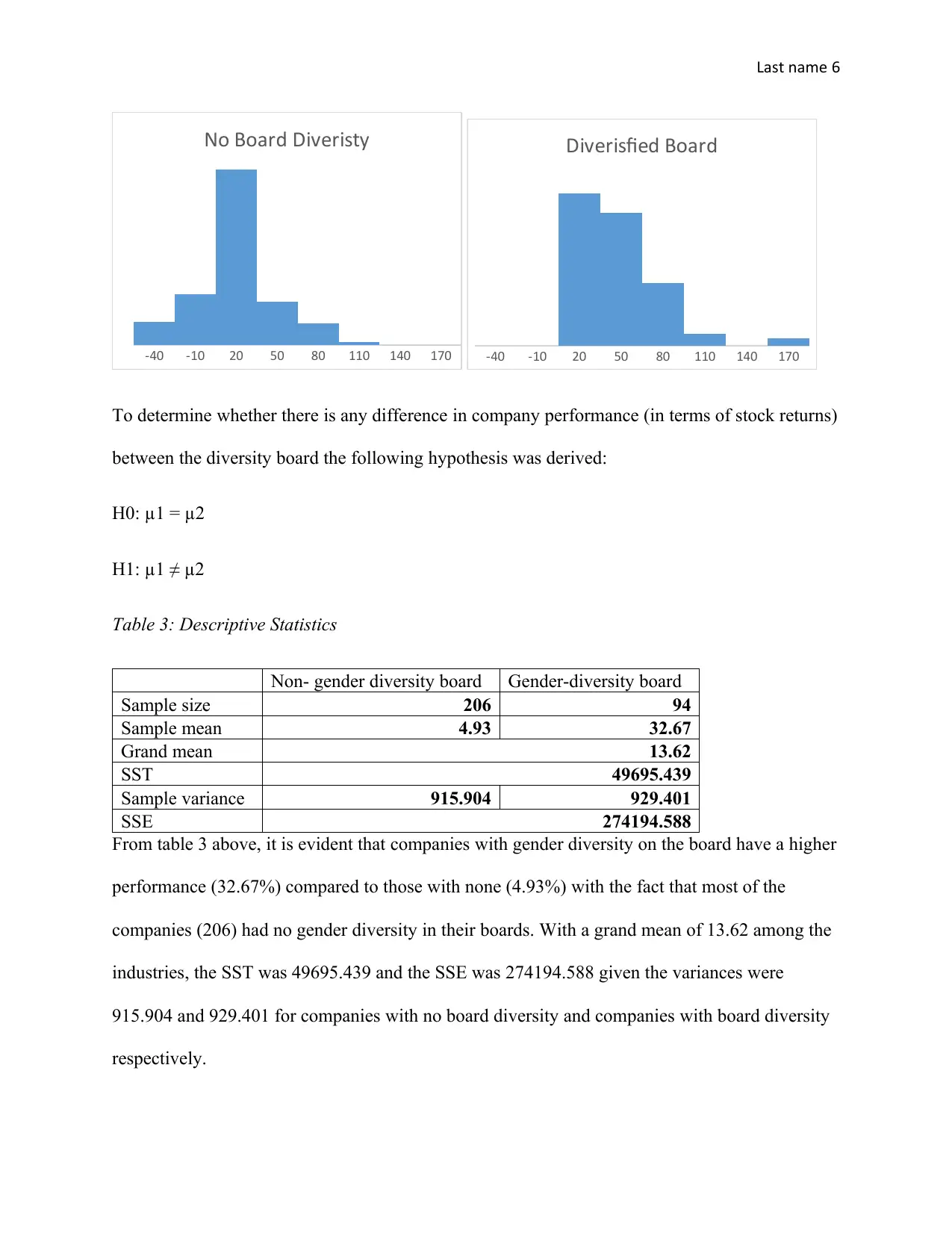

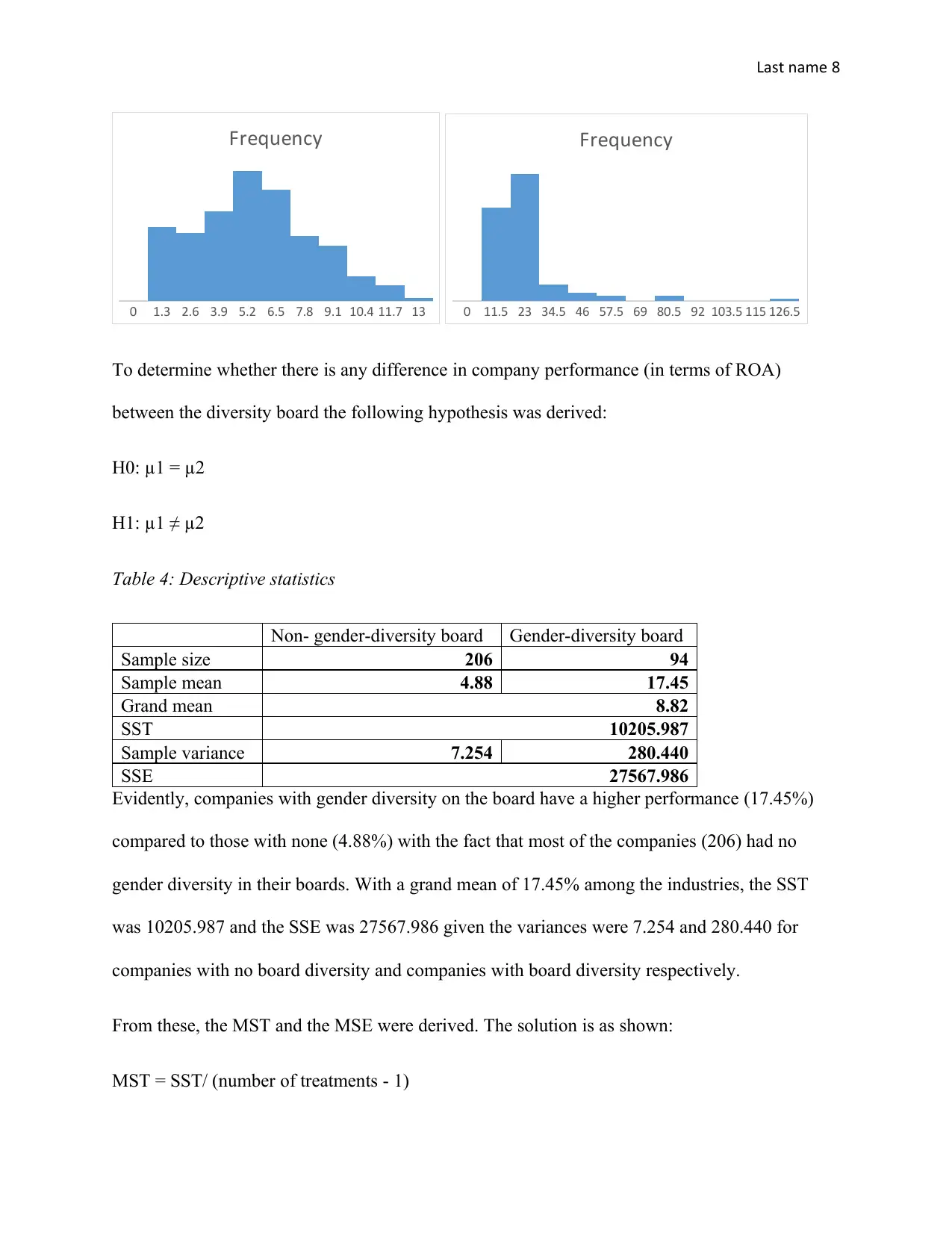

This report investigates the perceived value of female participation on company boards by analyzing the relationship between gender diversity and financial performance metrics. The study focuses on companies listed on the ASX, examining data from three industry sectors: Consumer Staples, Energy, and Health Care. The research employs statistical analyses, including chi-square and ANOVA tests, to determine if board representation based on gender is dependent on industry sectors and if there are any differences in stock market returns among the industry sectors. Furthermore, the study assesses whether companies with gender-diverse boards outperform those with non-gender-diverse boards in terms of stock market returns and return on assets (ROA). The findings reveal that the industry sectors exhibit varying stock market returns and that company performance, measured by both stock returns and ROA, does not significantly differ between companies with gender-diverse boards and those without. The study also concludes that board representation is not dependent on industry sectors, suggesting that female participation on company boards is perceived as not being valuable, based on the data analyzed.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.