Research Proposal: Board Responsibility and Carbon Emission Reduction

VerifiedAdded on 2023/06/06

|16

|3387

|440

Project

AI Summary

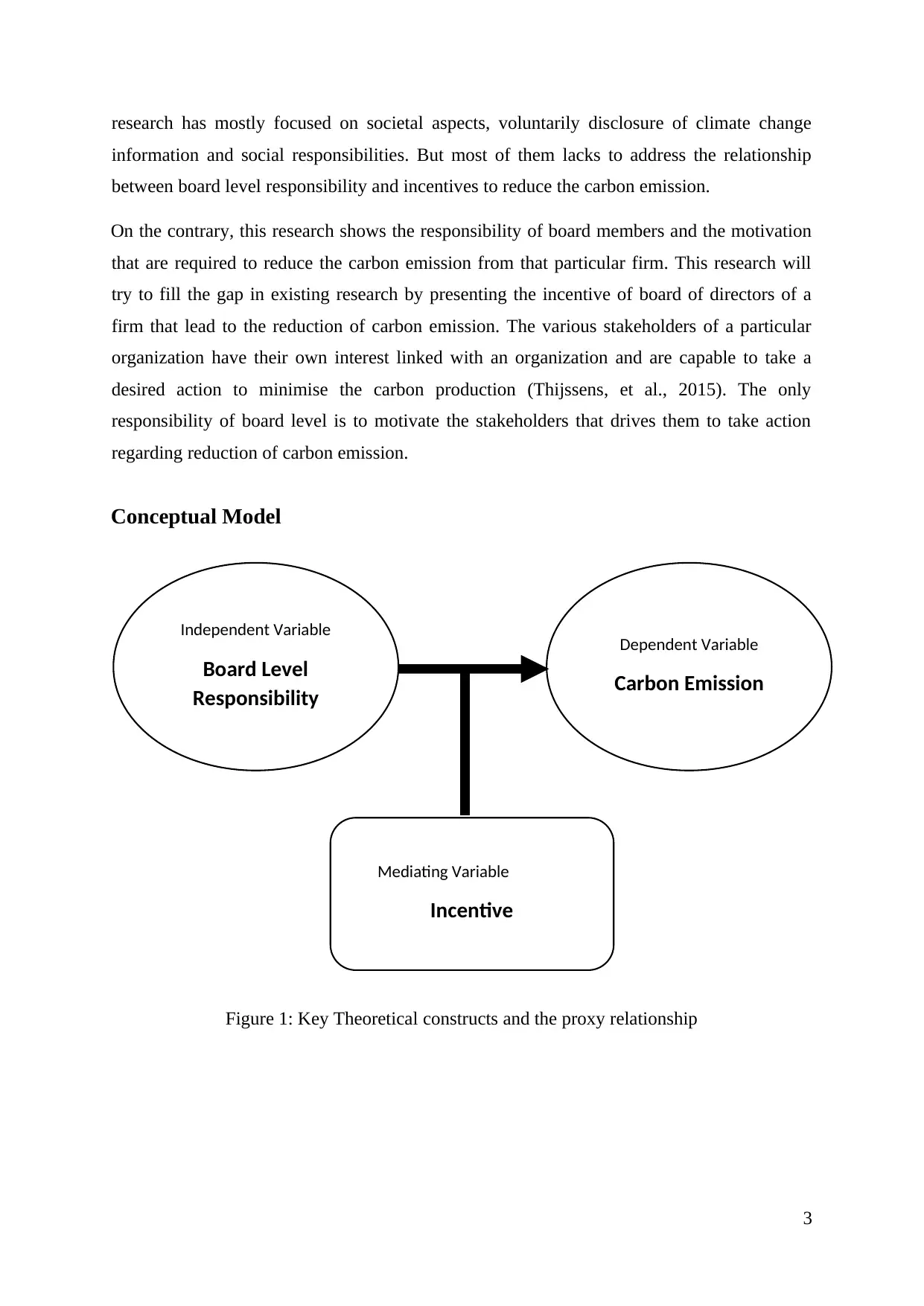

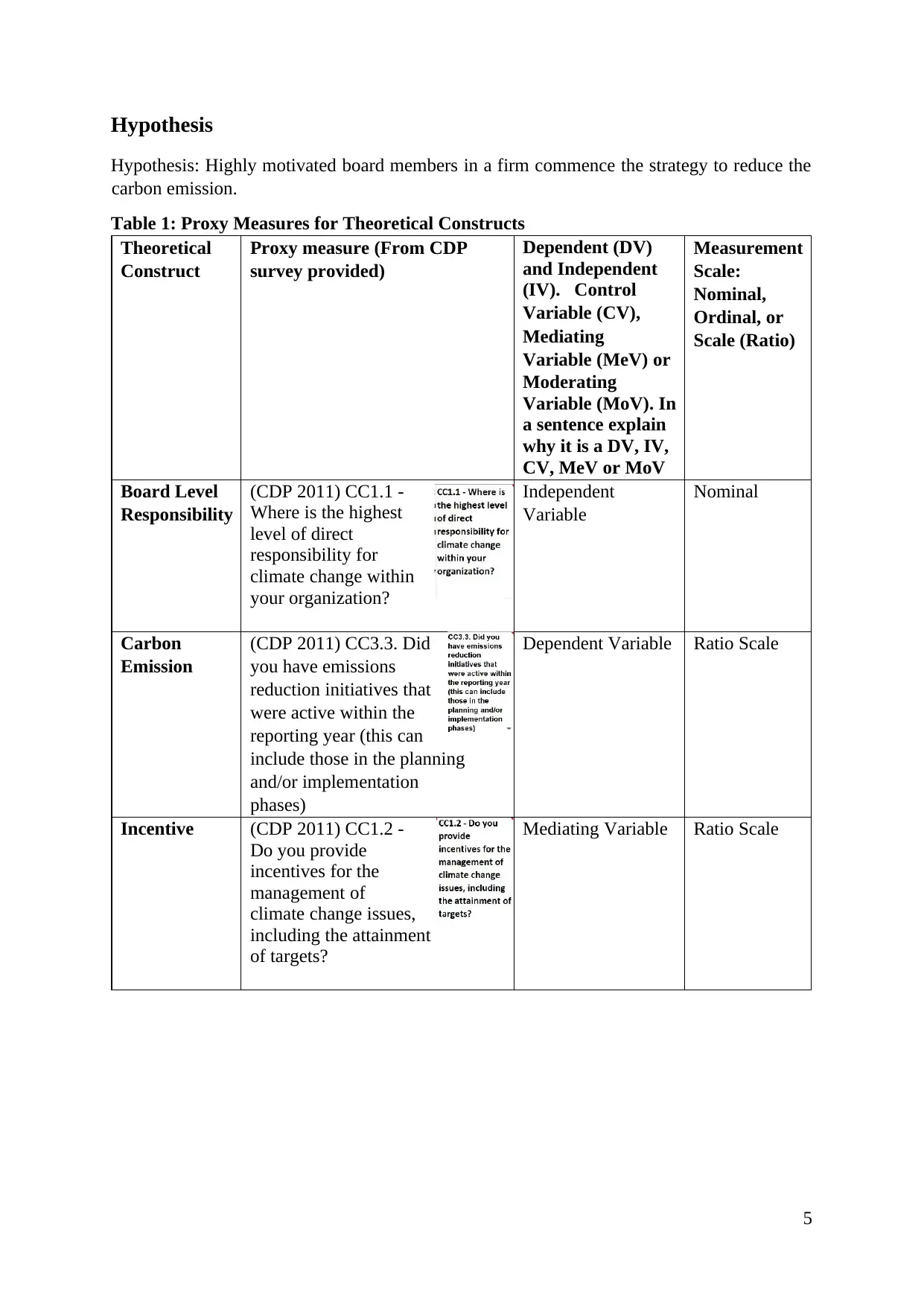

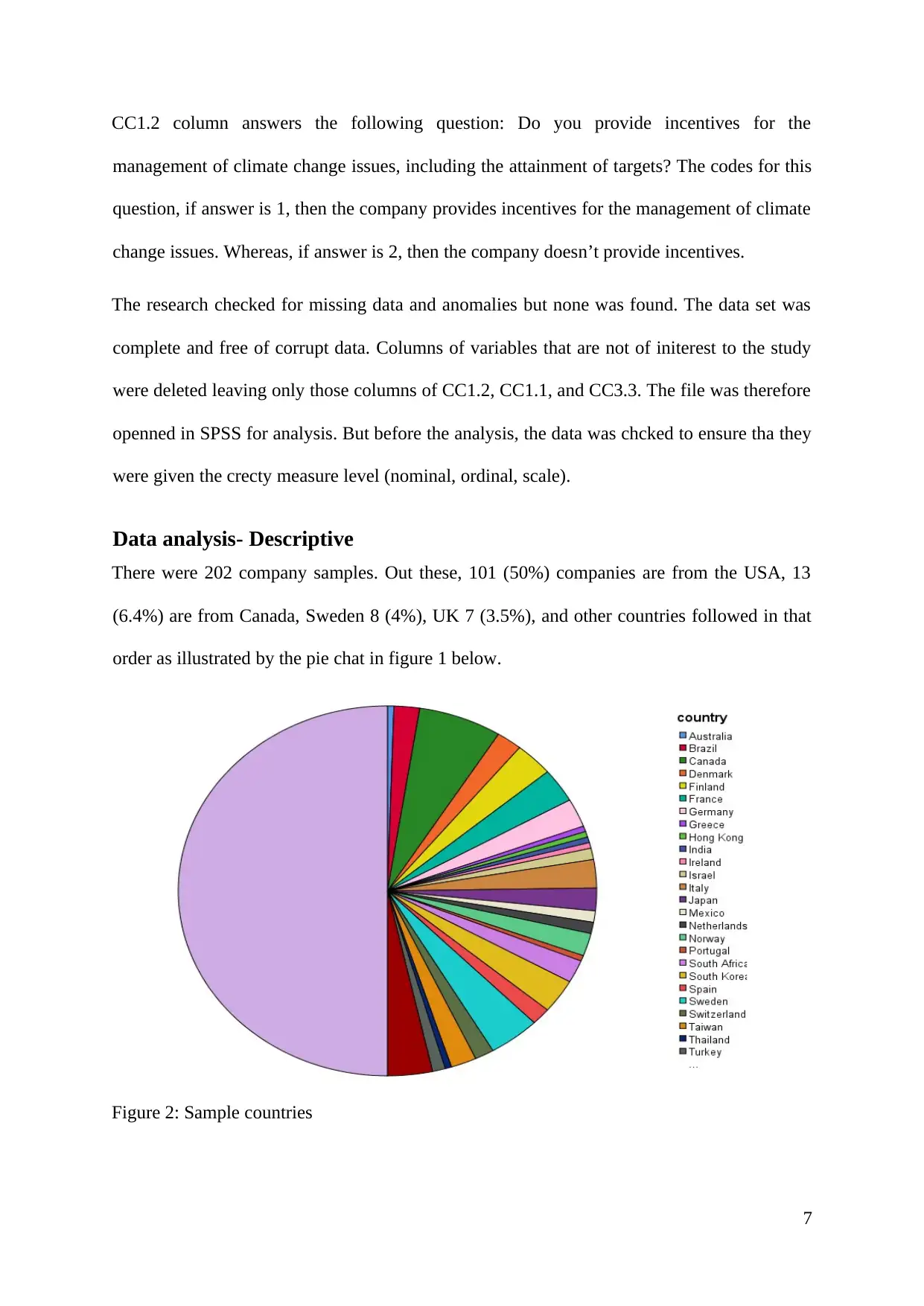

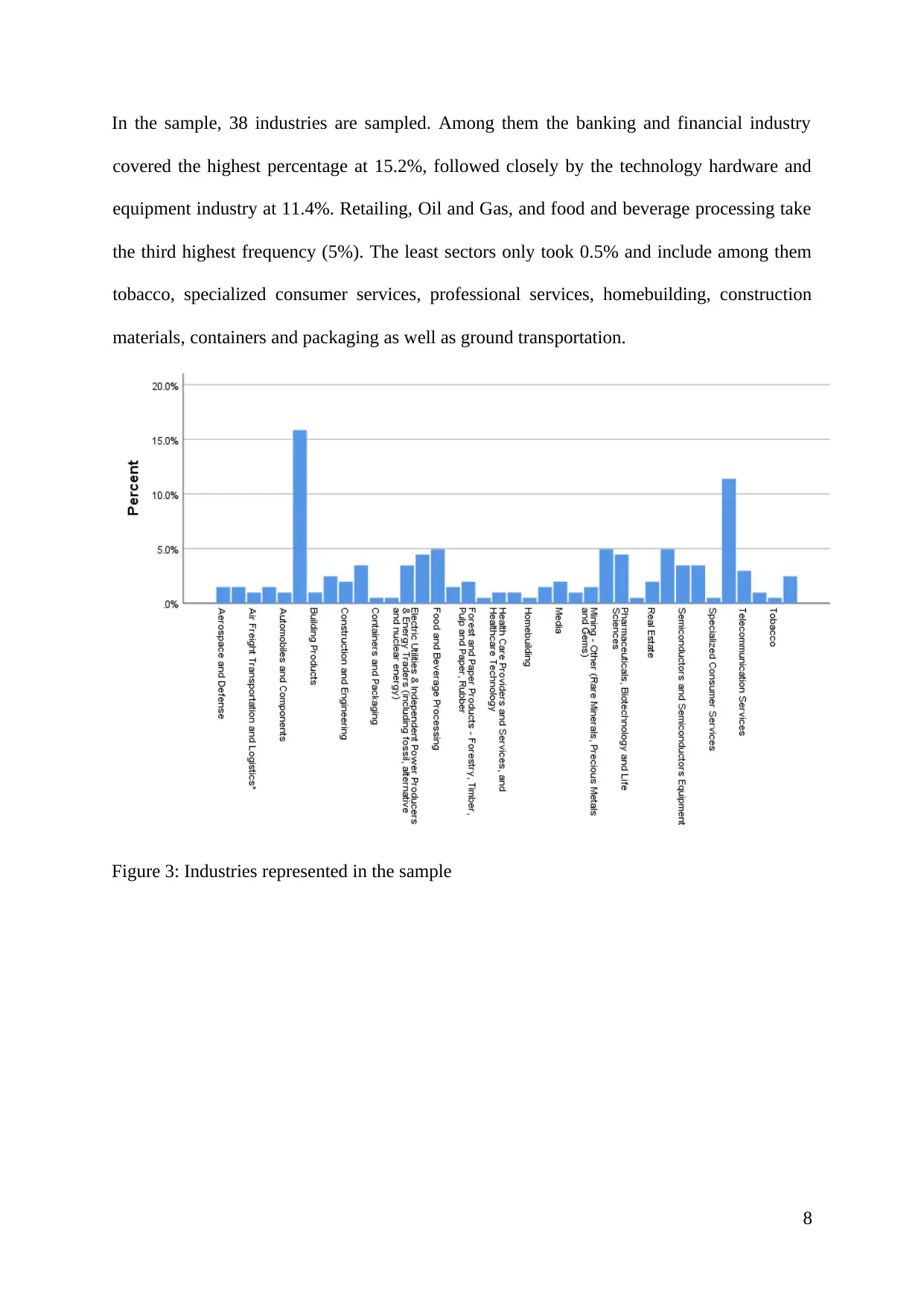

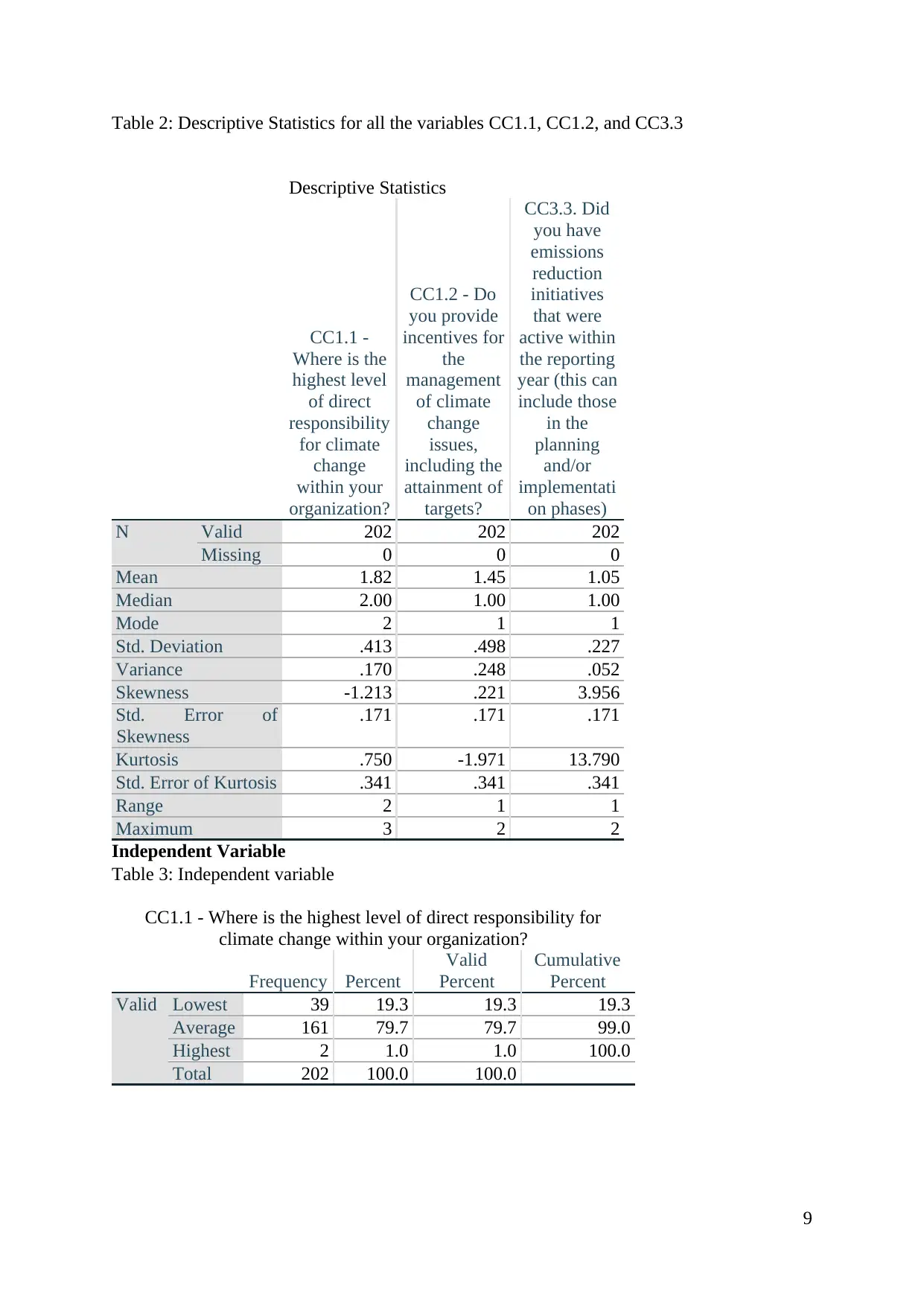

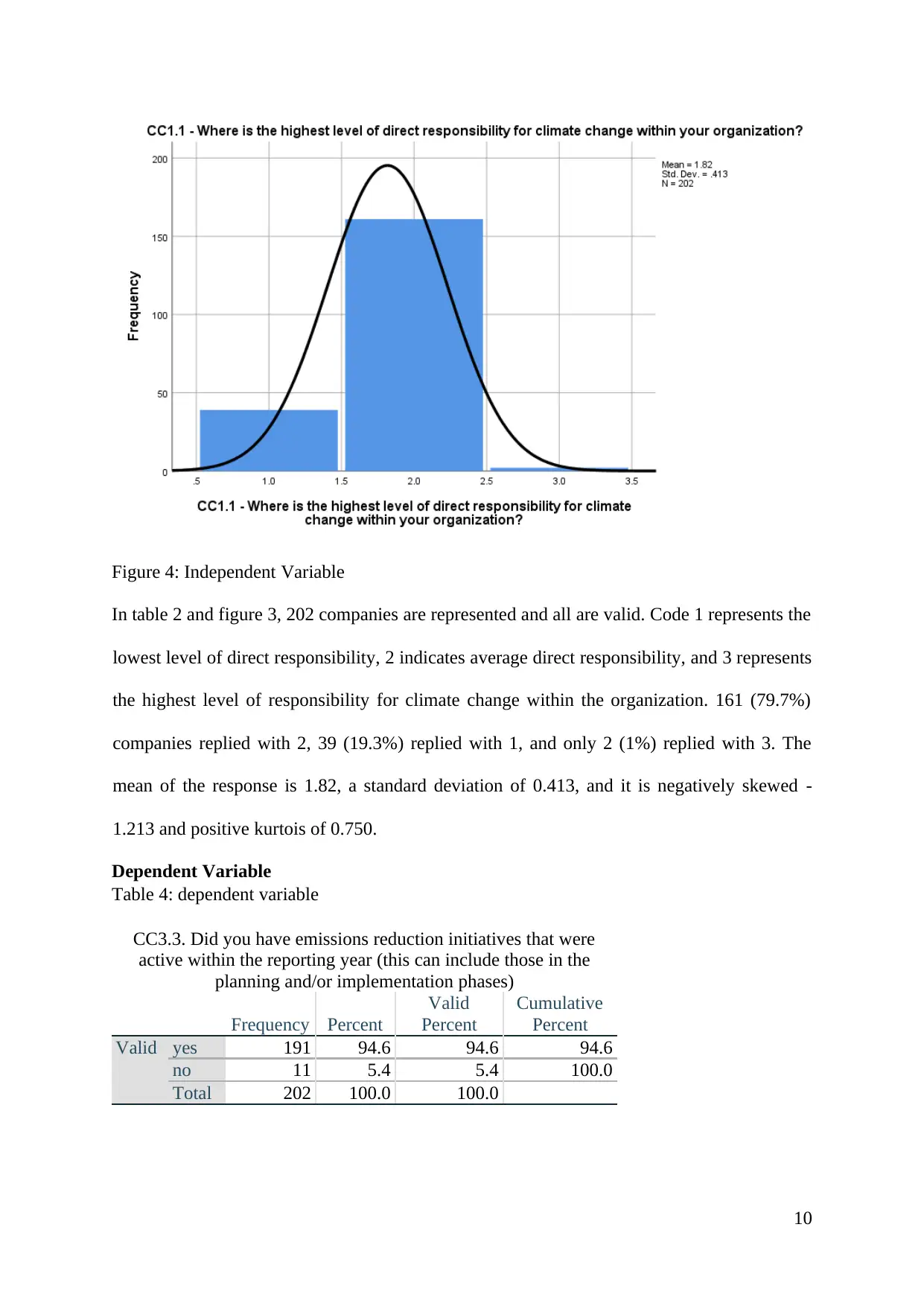

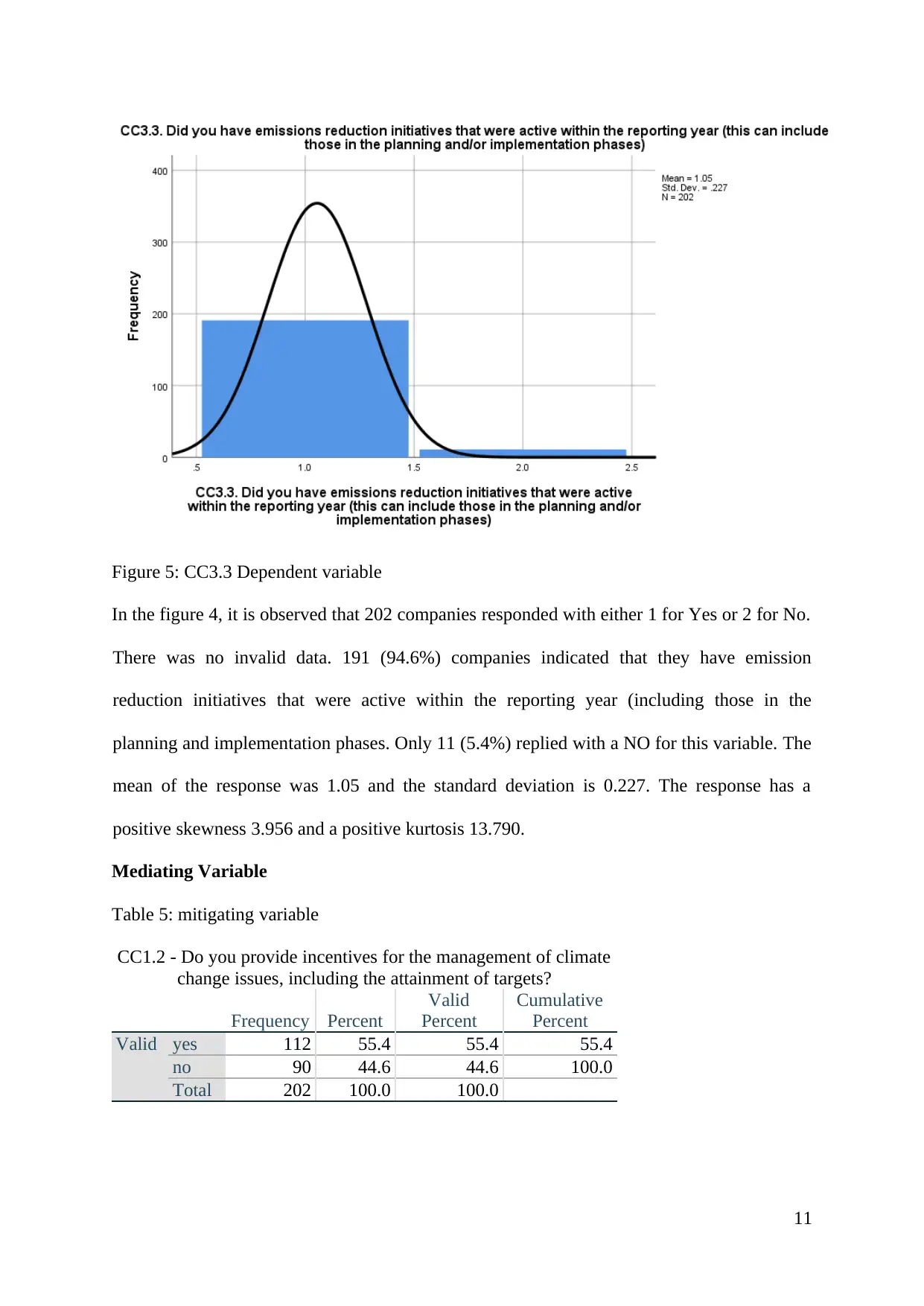

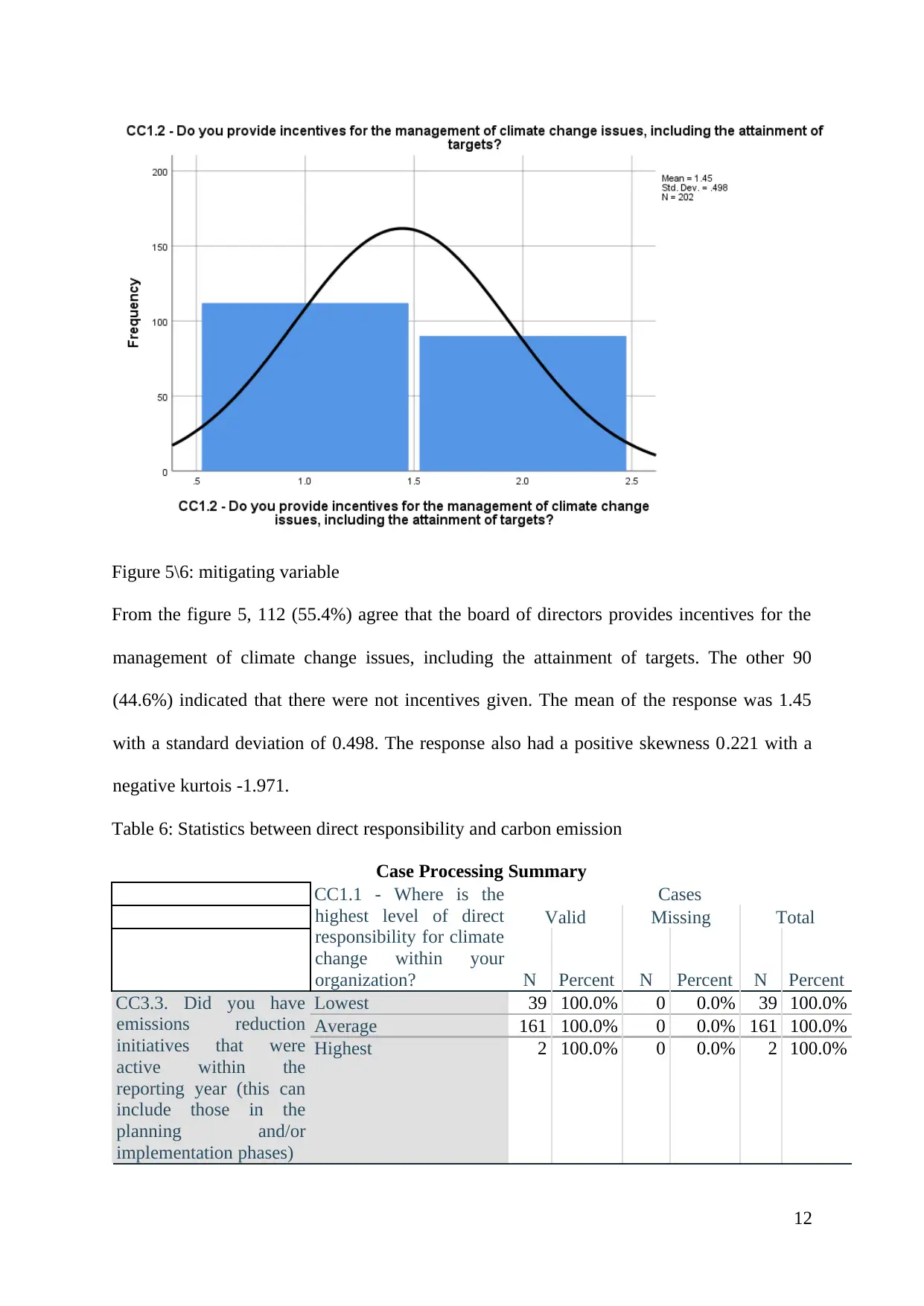

This research proposal investigates the relationship between board-level responsibility for climate change and carbon emission reduction, grounded in stakeholder theory. The study aims to determine if board-level accountability leads to reduced carbon emissions, exploring the mediating role of incentives. The literature review highlights the growing importance of environmental governance and the stakeholder theory's relevance in aligning business practices with societal values. The practical motivation stems from stakeholder pressure for improved organizational environmental performance. The research employs a quantitative approach, utilizing data from the Carbon Disclosure Project (CDP) survey, with a sample of 202 companies across various industries. The research employs descriptive statistics to analyze the data. Findings indicate a strong emphasis on emission reduction initiatives and the importance of incentives. The research concludes with an analysis of the independent, dependent, and mediating variables, including board level responsibility, carbon emission, and incentives respectively. The methodology involves the use of proxy measures from CDP, with nominal and ratio scales, to assess the relationship between the variables, and the data analysis reveals the distribution across industries and the level of responsibility within organizations.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.