International Finance and Decision Making: Boeing 7E7 Project Analysis

VerifiedAdded on 2020/06/04

|12

|3598

|47

Report

AI Summary

This report delves into the financial analysis of Boeing's 7E7 project, examining the application of various financial tools and techniques. It begins with an introduction to the importance of finance in business operations, particularly for large-scale projects. The report explores the rationale behind the 7E7 project, including its objectives and the market conditions at the time of its proposed launch. It then calculates and analyzes key financial metrics, such as the Internal Rate of Return (IRR), Cost of Equity (using CAPM), Cost of Debt, and Weighted Average Cost of Capital (WACC). The analysis considers the impact of debt levels on business risk and evaluates the project's financial viability under different scenarios. The report also includes a sensitivity analysis to assess the project's resilience to changes in key variables like development costs and sales volume. The conclusion summarizes the financial implications and provides recommendations based on the findings.

INTERNATIONAL

FINANCE AND DECISION

MAKING

FINANCE AND DECISION

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Launching of 7E7 projects:....................................................................................................1

Question 2........................................................................................................................................2

A)............................................................................................................................................2

B)............................................................................................................................................2

C)............................................................................................................................................2

D)............................................................................................................................................2

E)............................................................................................................................................3

F).............................................................................................................................................4

G)............................................................................................................................................4

H)............................................................................................................................................4

I).............................................................................................................................................5

Question 3........................................................................................................................................5

a).............................................................................................................................................5

b).............................................................................................................................................6

C)............................................................................................................................................6

QUESTION 4...................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Launching of 7E7 projects:....................................................................................................1

Question 2........................................................................................................................................2

A)............................................................................................................................................2

B)............................................................................................................................................2

C)............................................................................................................................................2

D)............................................................................................................................................2

E)............................................................................................................................................3

F).............................................................................................................................................4

G)............................................................................................................................................4

H)............................................................................................................................................4

I).............................................................................................................................................5

Question 3........................................................................................................................................5

a).............................................................................................................................................5

b).............................................................................................................................................6

C)............................................................................................................................................6

QUESTION 4...................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Finance is one of the most crucial thing in a business which is used by each organisation

for smoothly running their business operations. There are certain things which are used by the

firm for making business operations in a sustainable manner. This is the report which is linked

with information about 7E7 project which is planned by Boeing. By using capital appraisal tools,

Boeing uses 7E7 projects (Beugelsdijk and Frijns, 2010). Diverse tools and techniques are

implemented to elaborate financial performance and chances of future growth of Boeing.

Question 1

Launching of 7E7 projects:

Boeing was planning to launch 7E7 project. First, it did not launch new aircraft for a long

time. Emerging a new product could assist Boeing rebuilt commercial aircraft market back from

its topmost rival Airbus. It had 57 more commercial aircraft orders from Boeing. Second, main

aim of Boeing was to reduce the production cost and also to make product efficiently. Beside

this, Boeing 7E7 could likewise enhance long and short distance flexibility of planes to satiate

more consumers' requirements and to allay their concern about aging fleet of mid-range planes

after 9/11 attack. Apart from that, adopting the long term business cycle, air travels consistently

make great connection with GDP by an annual growing rate of 5.1%. Henceforth, this is worth

emerging the commercial airline business (Bayne and Woolcock, 2011).

At this time, there is no need to launch the 7E7 projects. Because, this is not the right

time for launching. Firstly, there are technological problems or issues that can led to higher risk

of failure and need vast amount of initial investment. Developing a plane with diverse

wingspans. This has been developed after the plane crash in 2001, which implements of

composite materials continue to carries risk. What is more, Iraq war, SARS, and international

terrorism emergence in international travel threats. The actual market demand was estimated to

be the worst during these years.

Question 2

A).

The calculated internal rate of return is relied on the this report as 15.66%, henceforth,

there is a need to have at least 15.7% required rate of return. If the net present value is nil then,

1

Finance is one of the most crucial thing in a business which is used by each organisation

for smoothly running their business operations. There are certain things which are used by the

firm for making business operations in a sustainable manner. This is the report which is linked

with information about 7E7 project which is planned by Boeing. By using capital appraisal tools,

Boeing uses 7E7 projects (Beugelsdijk and Frijns, 2010). Diverse tools and techniques are

implemented to elaborate financial performance and chances of future growth of Boeing.

Question 1

Launching of 7E7 projects:

Boeing was planning to launch 7E7 project. First, it did not launch new aircraft for a long

time. Emerging a new product could assist Boeing rebuilt commercial aircraft market back from

its topmost rival Airbus. It had 57 more commercial aircraft orders from Boeing. Second, main

aim of Boeing was to reduce the production cost and also to make product efficiently. Beside

this, Boeing 7E7 could likewise enhance long and short distance flexibility of planes to satiate

more consumers' requirements and to allay their concern about aging fleet of mid-range planes

after 9/11 attack. Apart from that, adopting the long term business cycle, air travels consistently

make great connection with GDP by an annual growing rate of 5.1%. Henceforth, this is worth

emerging the commercial airline business (Bayne and Woolcock, 2011).

At this time, there is no need to launch the 7E7 projects. Because, this is not the right

time for launching. Firstly, there are technological problems or issues that can led to higher risk

of failure and need vast amount of initial investment. Developing a plane with diverse

wingspans. This has been developed after the plane crash in 2001, which implements of

composite materials continue to carries risk. What is more, Iraq war, SARS, and international

terrorism emergence in international travel threats. The actual market demand was estimated to

be the worst during these years.

Question 2

A).

The calculated internal rate of return is relied on the this report as 15.66%, henceforth,

there is a need to have at least 15.7% required rate of return. If the net present value is nil then,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the project is considered after caution. On the other hand, if net present value is higher than the

zero, then the project is required to be adopted by the firm.

B).

Capital-asset-pricing-model is implemented by using an individual scrutiny or portfolio.

This is determined that the existing market price securities and henceforth, forecast about the

expected return on the aggregate capital investments. This model renders a tool for identifying

risk and translate it into forecast of expected return on the equity. The most crucial thing for

using CAPM is to forecast the require rate of on an individual equity. But this is not quite simple

to estimate the required rate of return. Boeing forecasts that in the initial 20 years, they are

predicting to sell 2000-3000 units of 7E7 projects. After assessing all these information, this can

be rendered that it would sale at-least of 2000 planes. But after analysing all these information,

there is a need to adopt the weighted average cost of capital as this covers all the aspects which

are related to the all product. Henceforth, WACC is used to calculate the total cost. Boeing

comprised of two separate segments which is more stable defence concern and conversely

higher volatile commercial businesses ( Beugelsdijk and Frijns, 2010).

C).

As per the capital asset pricing method, the cost of Equity is calculated by using these formula.

Rf+Beta* Market risk premium. Hence, cost of equity= 1.05%+1.43*2.75%=4.98%.

During this case, 74 year equity market risk premium was estimated to be 2.75%. beta of

the company was calculated to be the 1.43, which is based on the Bloomberg forecast for the

firm. This beta reflects how the Boeing stock is much riskier than the market.

D).

Equity market risk premium is the return which is generated over the risk free rate of

return. This return compensate the investors for bearing more risk on the equity market than the

risk free rate of return (Elango and et. al., 2010). Henceforth, to calculate this, this consider the

expected rate of return and subtract the risk free rate as follows:

EMRP is calculated by using: Expected rate of return- risk free rate of return=(Dividend Yield+

Growth rate of dividends)-Rf=(2.74%+1.06%)-1.05%=2.75%, where dividend earn and growth

rate of dividends is obtained from financial ratio and data of the firm. Rf is the APY of 3-months

Treasury Bill.

2

zero, then the project is required to be adopted by the firm.

B).

Capital-asset-pricing-model is implemented by using an individual scrutiny or portfolio.

This is determined that the existing market price securities and henceforth, forecast about the

expected return on the aggregate capital investments. This model renders a tool for identifying

risk and translate it into forecast of expected return on the equity. The most crucial thing for

using CAPM is to forecast the require rate of on an individual equity. But this is not quite simple

to estimate the required rate of return. Boeing forecasts that in the initial 20 years, they are

predicting to sell 2000-3000 units of 7E7 projects. After assessing all these information, this can

be rendered that it would sale at-least of 2000 planes. But after analysing all these information,

there is a need to adopt the weighted average cost of capital as this covers all the aspects which

are related to the all product. Henceforth, WACC is used to calculate the total cost. Boeing

comprised of two separate segments which is more stable defence concern and conversely

higher volatile commercial businesses ( Beugelsdijk and Frijns, 2010).

C).

As per the capital asset pricing method, the cost of Equity is calculated by using these formula.

Rf+Beta* Market risk premium. Hence, cost of equity= 1.05%+1.43*2.75%=4.98%.

During this case, 74 year equity market risk premium was estimated to be 2.75%. beta of

the company was calculated to be the 1.43, which is based on the Bloomberg forecast for the

firm. This beta reflects how the Boeing stock is much riskier than the market.

D).

Equity market risk premium is the return which is generated over the risk free rate of

return. This return compensate the investors for bearing more risk on the equity market than the

risk free rate of return (Elango and et. al., 2010). Henceforth, to calculate this, this consider the

expected rate of return and subtract the risk free rate as follows:

EMRP is calculated by using: Expected rate of return- risk free rate of return=(Dividend Yield+

Growth rate of dividends)-Rf=(2.74%+1.06%)-1.05%=2.75%, where dividend earn and growth

rate of dividends is obtained from financial ratio and data of the firm. Rf is the APY of 3-months

Treasury Bill.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

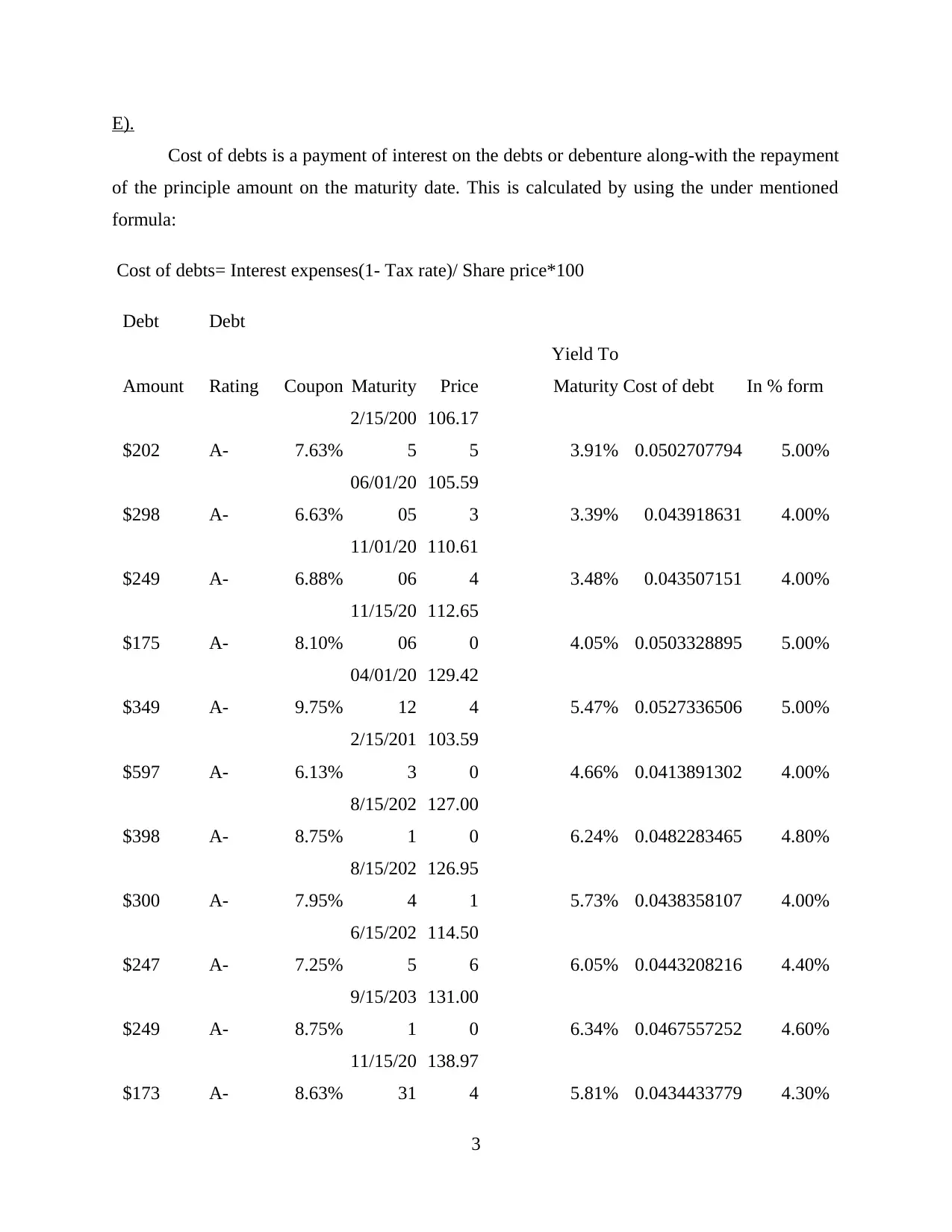

E).

Cost of debts is a payment of interest on the debts or debenture along-with the repayment

of the principle amount on the maturity date. This is calculated by using the under mentioned

formula:

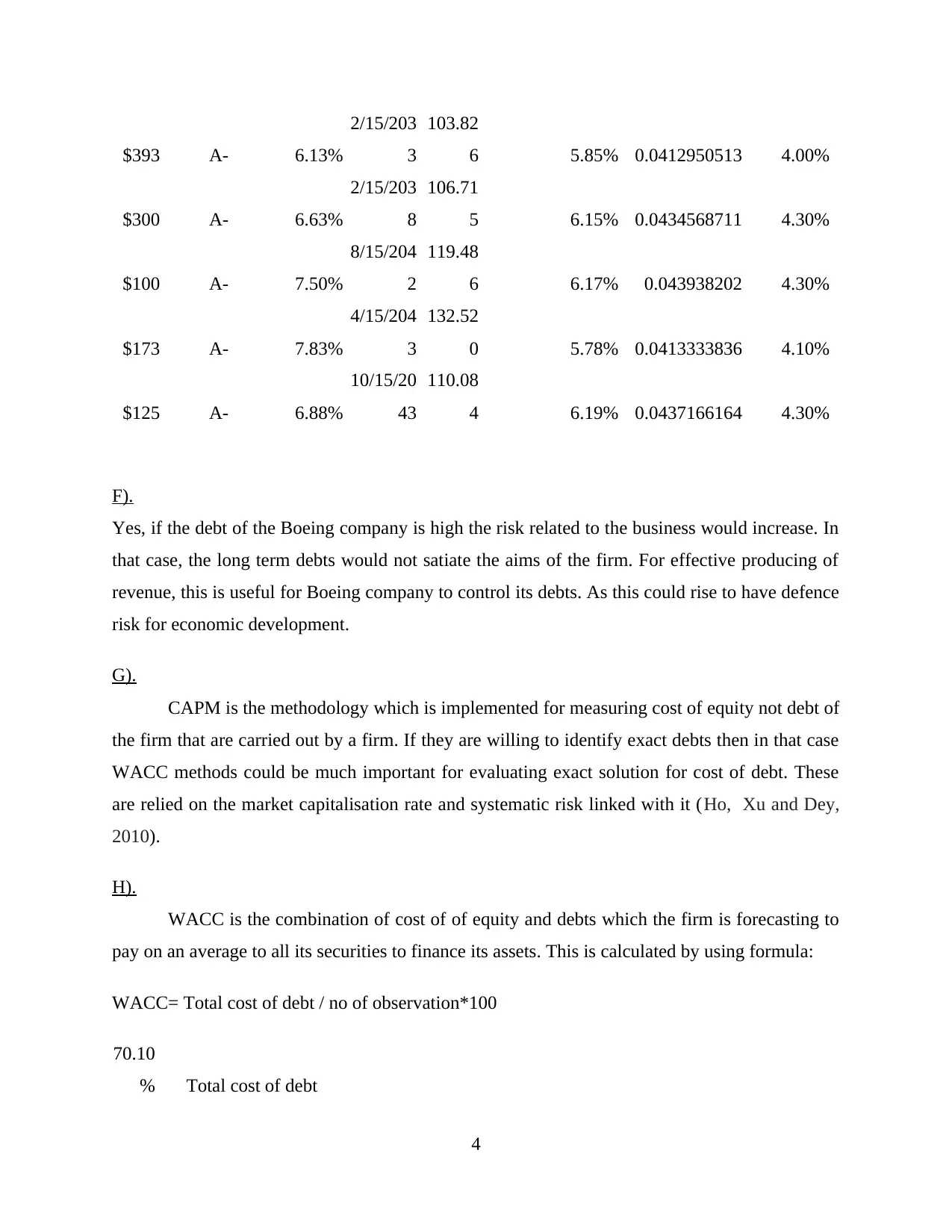

Cost of debts= Interest expenses(1- Tax rate)/ Share price*100

Debt Debt

Amount Rating Coupon Maturity Price

Yield To

Maturity Cost of debt In % form

$202 A- 7.63%

2/15/200

5

106.17

5 3.91% 0.0502707794 5.00%

$298 A- 6.63%

06/01/20

05

105.59

3 3.39% 0.043918631 4.00%

$249 A- 6.88%

11/01/20

06

110.61

4 3.48% 0.043507151 4.00%

$175 A- 8.10%

11/15/20

06

112.65

0 4.05% 0.0503328895 5.00%

$349 A- 9.75%

04/01/20

12

129.42

4 5.47% 0.0527336506 5.00%

$597 A- 6.13%

2/15/201

3

103.59

0 4.66% 0.0413891302 4.00%

$398 A- 8.75%

8/15/202

1

127.00

0 6.24% 0.0482283465 4.80%

$300 A- 7.95%

8/15/202

4

126.95

1 5.73% 0.0438358107 4.00%

$247 A- 7.25%

6/15/202

5

114.50

6 6.05% 0.0443208216 4.40%

$249 A- 8.75%

9/15/203

1

131.00

0 6.34% 0.0467557252 4.60%

$173 A- 8.63%

11/15/20

31

138.97

4 5.81% 0.0434433779 4.30%

3

Cost of debts is a payment of interest on the debts or debenture along-with the repayment

of the principle amount on the maturity date. This is calculated by using the under mentioned

formula:

Cost of debts= Interest expenses(1- Tax rate)/ Share price*100

Debt Debt

Amount Rating Coupon Maturity Price

Yield To

Maturity Cost of debt In % form

$202 A- 7.63%

2/15/200

5

106.17

5 3.91% 0.0502707794 5.00%

$298 A- 6.63%

06/01/20

05

105.59

3 3.39% 0.043918631 4.00%

$249 A- 6.88%

11/01/20

06

110.61

4 3.48% 0.043507151 4.00%

$175 A- 8.10%

11/15/20

06

112.65

0 4.05% 0.0503328895 5.00%

$349 A- 9.75%

04/01/20

12

129.42

4 5.47% 0.0527336506 5.00%

$597 A- 6.13%

2/15/201

3

103.59

0 4.66% 0.0413891302 4.00%

$398 A- 8.75%

8/15/202

1

127.00

0 6.24% 0.0482283465 4.80%

$300 A- 7.95%

8/15/202

4

126.95

1 5.73% 0.0438358107 4.00%

$247 A- 7.25%

6/15/202

5

114.50

6 6.05% 0.0443208216 4.40%

$249 A- 8.75%

9/15/203

1

131.00

0 6.34% 0.0467557252 4.60%

$173 A- 8.63%

11/15/20

31

138.97

4 5.81% 0.0434433779 4.30%

3

$393 A- 6.13%

2/15/203

3

103.82

6 5.85% 0.0412950513 4.00%

$300 A- 6.63%

2/15/203

8

106.71

5 6.15% 0.0434568711 4.30%

$100 A- 7.50%

8/15/204

2

119.48

6 6.17% 0.043938202 4.30%

$173 A- 7.83%

4/15/204

3

132.52

0 5.78% 0.0413333836 4.10%

$125 A- 6.88%

10/15/20

43

110.08

4 6.19% 0.0437166164 4.30%

F).

Yes, if the debt of the Boeing company is high the risk related to the business would increase. In

that case, the long term debts would not satiate the aims of the firm. For effective producing of

revenue, this is useful for Boeing company to control its debts. As this could rise to have defence

risk for economic development.

G).

CAPM is the methodology which is implemented for measuring cost of equity not debt of

the firm that are carried out by a firm. If they are willing to identify exact debts then in that case

WACC methods could be much important for evaluating exact solution for cost of debt. These

are relied on the market capitalisation rate and systematic risk linked with it (Ho, Xu and Dey,

2010).

H).

WACC is the combination of cost of of equity and debts which the firm is forecasting to

pay on an average to all its securities to finance its assets. This is calculated by using formula:

WACC= Total cost of debt / no of observation*100

70.10

% Total cost of debt

4

2/15/203

3

103.82

6 5.85% 0.0412950513 4.00%

$300 A- 6.63%

2/15/203

8

106.71

5 6.15% 0.0434568711 4.30%

$100 A- 7.50%

8/15/204

2

119.48

6 6.17% 0.043938202 4.30%

$173 A- 7.83%

4/15/204

3

132.52

0 5.78% 0.0413333836 4.10%

$125 A- 6.88%

10/15/20

43

110.08

4 6.19% 0.0437166164 4.30%

F).

Yes, if the debt of the Boeing company is high the risk related to the business would increase. In

that case, the long term debts would not satiate the aims of the firm. For effective producing of

revenue, this is useful for Boeing company to control its debts. As this could rise to have defence

risk for economic development.

G).

CAPM is the methodology which is implemented for measuring cost of equity not debt of

the firm that are carried out by a firm. If they are willing to identify exact debts then in that case

WACC methods could be much important for evaluating exact solution for cost of debt. These

are relied on the market capitalisation rate and systematic risk linked with it (Ho, Xu and Dey,

2010).

H).

WACC is the combination of cost of of equity and debts which the firm is forecasting to

pay on an average to all its securities to finance its assets. This is calculated by using formula:

WACC= Total cost of debt / no of observation*100

70.10

% Total cost of debt

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0.04 4.30%

I).

In this scenario, each company is trying to opt the tool under which both equity and debts

comprised. Combination of both capital structure would adopt by the firm in order to gain the

sustainability (Masini and Menichetti, 2012).

Question 3

a).

Weighted average cost of capital is the rate which an organisation is forecasted to pay on

average to all its stockholders to finance it assets. WACC is mostly concerned to firm's total cost

of capital. Each source of capital comprises of equity, preferred stock, bonds and any other long

term debts. For calculating WACC, company can use this formula:

WACC = Wd rd (1- t) + We* r e

Where:

Wd = Proportion of debt in a market - value capital structure

rd = Pre-tax cost of debt capital

t = Marginal effective corporate tax rate

We = Proportion of equity in a market - value capital structure.

Re= Cost of equity capital

WACC calculation Portfolio Commercial Division

Equity Beta 1.45 2.54

Corporate tax rate 35.00% 35.00%

Expected return on Market 11.70% 11.70%

Risk Free rate 4.56% 4.56%

rd 5.85% 5.85%

re 14.91% 22.70%

Weighted debt 0.344 0.38%

Debt/ Equity 0.525 62.30%

Weighted Equity 0.656 0.62%

5

I).

In this scenario, each company is trying to opt the tool under which both equity and debts

comprised. Combination of both capital structure would adopt by the firm in order to gain the

sustainability (Masini and Menichetti, 2012).

Question 3

a).

Weighted average cost of capital is the rate which an organisation is forecasted to pay on

average to all its stockholders to finance it assets. WACC is mostly concerned to firm's total cost

of capital. Each source of capital comprises of equity, preferred stock, bonds and any other long

term debts. For calculating WACC, company can use this formula:

WACC = Wd rd (1- t) + We* r e

Where:

Wd = Proportion of debt in a market - value capital structure

rd = Pre-tax cost of debt capital

t = Marginal effective corporate tax rate

We = Proportion of equity in a market - value capital structure.

Re= Cost of equity capital

WACC calculation Portfolio Commercial Division

Equity Beta 1.45 2.54

Corporate tax rate 35.00% 35.00%

Expected return on Market 11.70% 11.70%

Risk Free rate 4.56% 4.56%

rd 5.85% 5.85%

re 14.91% 22.70%

Weighted debt 0.344 0.38%

Debt/ Equity 0.525 62.30%

Weighted Equity 0.656 0.62%

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

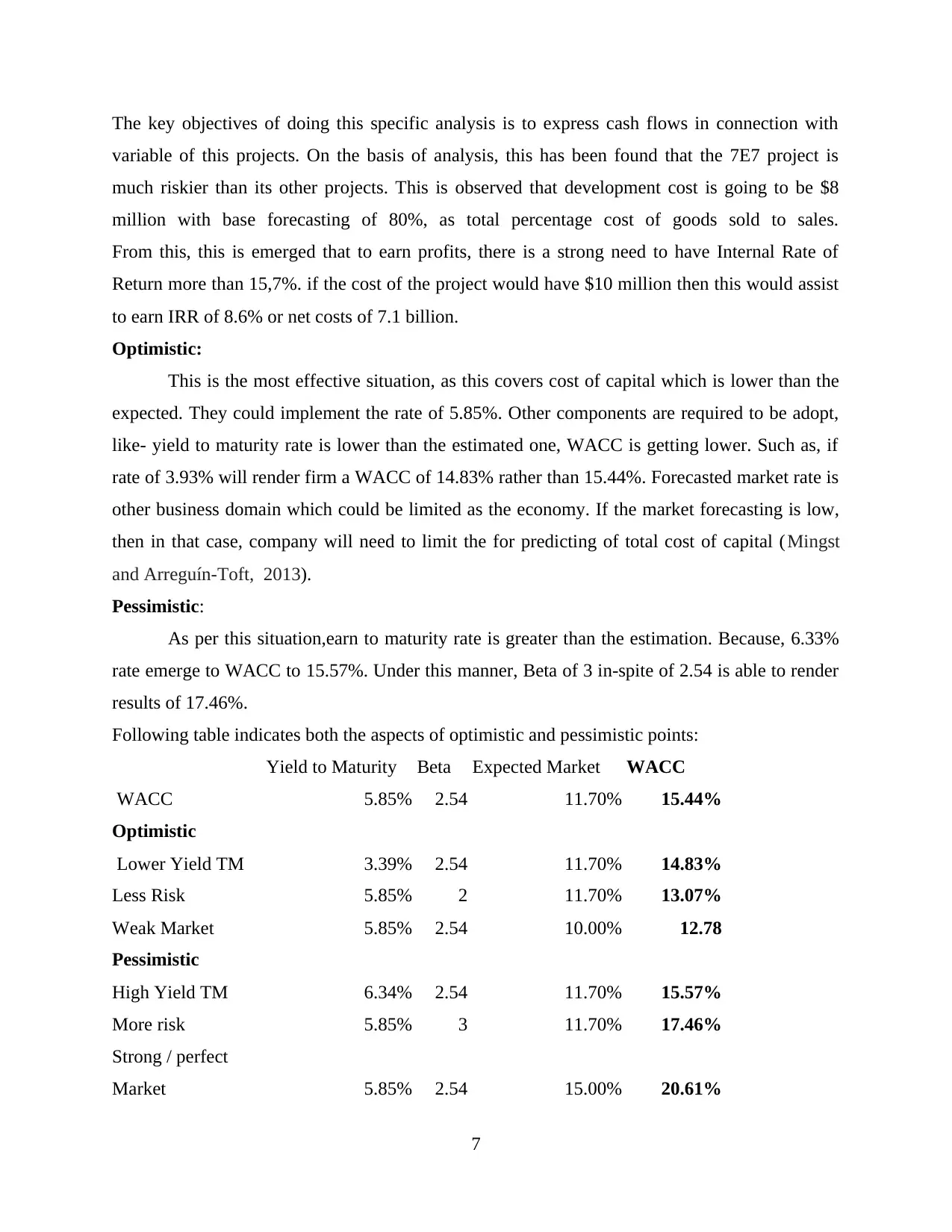

WACC 11.09% 15.44%

Defence/ Portfolio Boeing defence 46.00%

Debt/ Equity Boeing commercial 0.623

Debt/ Equity weight defence 0.41

Debt/ Equity Boeing defence 0.41

Justification:

The cost of capital for commercial department of Boeing is identified to be 10.19% that is

more than IRR of 15.7%. based on the hypothesis, Boeing must be able to offer 2500 planes at

5% premium. This is lucrative because of higher margin of safety. The debt/ equity assist to

measure weights. Boeing requires to earn minimum of 15.443% return on its investment for

balancing their share price.

b).

As per the case scenario elaborated under this project related to the 7E7 project regarding

Boeing. The most lucrative condition for organisation could be that point of time when firm will

sell 2500 planes in 20 years with a great premium rate of 5%. Development costs are stay low to

$8 million and cost of products offered is about 80% of total sales. Boeing is ensuring to deliver

its promise to overcome operational expenses for 7E7 with 20% rise in fuel efficient manner.

There are other ways that are required to be seen into consideration as prices are minimum as

compared to other planes. In that case, market share of the company would automatically be rise.

The most effective plan of getting optimum advantages is when , Boeing is able to sale more

commercial aircraft within the allotted time period. The internal rate of return renders project a

net present value of zero that is 15.4% according to the assessment. This would assist to enhance

the income of shareholders which is going to invest under this project (Maxwell, Jeffrey and

Lévesque, 2011).

C).

There are so many methods via which sensitivity analysis is done. Few of them are

optimistic and pessimistic estimates for underlying components of total volume and cost of sales.

6

Defence/ Portfolio Boeing defence 46.00%

Debt/ Equity Boeing commercial 0.623

Debt/ Equity weight defence 0.41

Debt/ Equity Boeing defence 0.41

Justification:

The cost of capital for commercial department of Boeing is identified to be 10.19% that is

more than IRR of 15.7%. based on the hypothesis, Boeing must be able to offer 2500 planes at

5% premium. This is lucrative because of higher margin of safety. The debt/ equity assist to

measure weights. Boeing requires to earn minimum of 15.443% return on its investment for

balancing their share price.

b).

As per the case scenario elaborated under this project related to the 7E7 project regarding

Boeing. The most lucrative condition for organisation could be that point of time when firm will

sell 2500 planes in 20 years with a great premium rate of 5%. Development costs are stay low to

$8 million and cost of products offered is about 80% of total sales. Boeing is ensuring to deliver

its promise to overcome operational expenses for 7E7 with 20% rise in fuel efficient manner.

There are other ways that are required to be seen into consideration as prices are minimum as

compared to other planes. In that case, market share of the company would automatically be rise.

The most effective plan of getting optimum advantages is when , Boeing is able to sale more

commercial aircraft within the allotted time period. The internal rate of return renders project a

net present value of zero that is 15.4% according to the assessment. This would assist to enhance

the income of shareholders which is going to invest under this project (Maxwell, Jeffrey and

Lévesque, 2011).

C).

There are so many methods via which sensitivity analysis is done. Few of them are

optimistic and pessimistic estimates for underlying components of total volume and cost of sales.

6

The key objectives of doing this specific analysis is to express cash flows in connection with

variable of this projects. On the basis of analysis, this has been found that the 7E7 project is

much riskier than its other projects. This is observed that development cost is going to be $8

million with base forecasting of 80%, as total percentage cost of goods sold to sales.

From this, this is emerged that to earn profits, there is a strong need to have Internal Rate of

Return more than 15,7%. if the cost of the project would have $10 million then this would assist

to earn IRR of 8.6% or net costs of 7.1 billion.

Optimistic:

This is the most effective situation, as this covers cost of capital which is lower than the

expected. They could implement the rate of 5.85%. Other components are required to be adopt,

like- yield to maturity rate is lower than the estimated one, WACC is getting lower. Such as, if

rate of 3.93% will render firm a WACC of 14.83% rather than 15.44%. Forecasted market rate is

other business domain which could be limited as the economy. If the market forecasting is low,

then in that case, company will need to limit the for predicting of total cost of capital (Mingst

and Arreguín-Toft, 2013).

Pessimistic:

As per this situation,earn to maturity rate is greater than the estimation. Because, 6.33%

rate emerge to WACC to 15.57%. Under this manner, Beta of 3 in-spite of 2.54 is able to render

results of 17.46%.

Following table indicates both the aspects of optimistic and pessimistic points:

Yield to Maturity Beta Expected Market WACC

WACC 5.85% 2.54 11.70% 15.44%

Optimistic

Lower Yield TM 3.39% 2.54 11.70% 14.83%

Less Risk 5.85% 2 11.70% 13.07%

Weak Market 5.85% 2.54 10.00% 12.78

Pessimistic

High Yield TM 6.34% 2.54 11.70% 15.57%

More risk 5.85% 3 11.70% 17.46%

Strong / perfect

Market 5.85% 2.54 15.00% 20.61%

7

variable of this projects. On the basis of analysis, this has been found that the 7E7 project is

much riskier than its other projects. This is observed that development cost is going to be $8

million with base forecasting of 80%, as total percentage cost of goods sold to sales.

From this, this is emerged that to earn profits, there is a strong need to have Internal Rate of

Return more than 15,7%. if the cost of the project would have $10 million then this would assist

to earn IRR of 8.6% or net costs of 7.1 billion.

Optimistic:

This is the most effective situation, as this covers cost of capital which is lower than the

expected. They could implement the rate of 5.85%. Other components are required to be adopt,

like- yield to maturity rate is lower than the estimated one, WACC is getting lower. Such as, if

rate of 3.93% will render firm a WACC of 14.83% rather than 15.44%. Forecasted market rate is

other business domain which could be limited as the economy. If the market forecasting is low,

then in that case, company will need to limit the for predicting of total cost of capital (Mingst

and Arreguín-Toft, 2013).

Pessimistic:

As per this situation,earn to maturity rate is greater than the estimation. Because, 6.33%

rate emerge to WACC to 15.57%. Under this manner, Beta of 3 in-spite of 2.54 is able to render

results of 17.46%.

Following table indicates both the aspects of optimistic and pessimistic points:

Yield to Maturity Beta Expected Market WACC

WACC 5.85% 2.54 11.70% 15.44%

Optimistic

Lower Yield TM 3.39% 2.54 11.70% 14.83%

Less Risk 5.85% 2 11.70% 13.07%

Weak Market 5.85% 2.54 10.00% 12.78

Pessimistic

High Yield TM 6.34% 2.54 11.70% 15.57%

More risk 5.85% 3 11.70% 17.46%

Strong / perfect

Market 5.85% 2.54 15.00% 20.61%

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 4

Before approval of the Boeing 7E7, it is important consider the risk and benefits which

are associated with 7E7. This helps the board to make their decisions regarding the approval of

this project of Boeing 7E7. For this purpose, evaluation of 7E7 s conducted and the risk can be

determined with their design and materials which used in it. To make the body of 7E7 , first time

carbon body construction is used. Use of such technique in preparation of the body is considered

as risks as it is never used in the large scale in never before. Boeing has large supply chain

system which is spread in all over the world. Due to having large network, it is difficult to

manage all the contractors effectively. This will reduce the ability of Boeing regarding

operations of their functions. There are many major parts of plane are prepared in other countries

which increases the cost of operations and lots of difficulties are faced during during its

transmission for final assembly. Sea route is adopt by Boeing to transfer the important parts of

plane for it final production which also consumes large time. If all important parts are not

delivered as per time specification then this will increase the operational cost and increases the

risks associated with Boeing 7E7 (Morgan, 2012).

Airbus is the major competitor which affects the business activities of Boeing. The new

plane of A380 which is launched by Airbus in 2005 transformed the market. This will be the

biggest competitor of the 7E7. The major benefits which are derive from the 7E7 is it provides

the facility of carrying maximum number of passengers. In aviation sector, airline always find

out the new planes which are more efficient and provides large number of benefits to improve

their profitability. This provides the opportunity to the new airlines to saves their cost by

carrying large number of passengers in one and takes the advantage of fuel efficient.

This projects provides the large number of opportunities regarding increase the wealth of

their shareholders. To reduce their COGS less than 80% and maintain the development cost up to

$8 billion dollars the Boeing is need to sell 2500 aircraft in around more than 20 years. It is

important to increase the shareholders value the IRR should be equal to WACC and the WACC

of Boeing is calculated as 15.44%. This project provide the large number of opportunities to

boing to increase the wealth of their shareholders and derive the large number of other benefits

improves their profitability (Nielsen and Nielsen, 2011).

8

Before approval of the Boeing 7E7, it is important consider the risk and benefits which

are associated with 7E7. This helps the board to make their decisions regarding the approval of

this project of Boeing 7E7. For this purpose, evaluation of 7E7 s conducted and the risk can be

determined with their design and materials which used in it. To make the body of 7E7 , first time

carbon body construction is used. Use of such technique in preparation of the body is considered

as risks as it is never used in the large scale in never before. Boeing has large supply chain

system which is spread in all over the world. Due to having large network, it is difficult to

manage all the contractors effectively. This will reduce the ability of Boeing regarding

operations of their functions. There are many major parts of plane are prepared in other countries

which increases the cost of operations and lots of difficulties are faced during during its

transmission for final assembly. Sea route is adopt by Boeing to transfer the important parts of

plane for it final production which also consumes large time. If all important parts are not

delivered as per time specification then this will increase the operational cost and increases the

risks associated with Boeing 7E7 (Morgan, 2012).

Airbus is the major competitor which affects the business activities of Boeing. The new

plane of A380 which is launched by Airbus in 2005 transformed the market. This will be the

biggest competitor of the 7E7. The major benefits which are derive from the 7E7 is it provides

the facility of carrying maximum number of passengers. In aviation sector, airline always find

out the new planes which are more efficient and provides large number of benefits to improve

their profitability. This provides the opportunity to the new airlines to saves their cost by

carrying large number of passengers in one and takes the advantage of fuel efficient.

This projects provides the large number of opportunities regarding increase the wealth of

their shareholders. To reduce their COGS less than 80% and maintain the development cost up to

$8 billion dollars the Boeing is need to sell 2500 aircraft in around more than 20 years. It is

important to increase the shareholders value the IRR should be equal to WACC and the WACC

of Boeing is calculated as 15.44%. This project provide the large number of opportunities to

boing to increase the wealth of their shareholders and derive the large number of other benefits

improves their profitability (Nielsen and Nielsen, 2011).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

It has been concluded from the above report that, internation finance has large number of

importance in providence of funding to the different operations of company. This helps the

management of company to improves their decision making regarding different aspects. Such

international financing resources helps in allocation of the financial resources in their different

functions which helps in growth and sustainable performance of Boeing. Financial analysis helps

the Boeing 7E7 to find out the new ways to enter into new market. Different financial tools like

cost of capital and WACC are clearly defined.

9

It has been concluded from the above report that, internation finance has large number of

importance in providence of funding to the different operations of company. This helps the

management of company to improves their decision making regarding different aspects. Such

international financing resources helps in allocation of the financial resources in their different

functions which helps in growth and sustainable performance of Boeing. Financial analysis helps

the Boeing 7E7 to find out the new ways to enter into new market. Different financial tools like

cost of capital and WACC are clearly defined.

9

REFERENCES

Books and Journals

Bayne, N. and Woolcock, S. eds., 2011. The new economic diplomacy: decision-making and

negotiation in international economic relations. Ashgate Publishing, Ltd..

Beugelsdijk, S. and Frijns, B., 2010. A cultural explanation of the foreign bias in international

asset allocation. Journal of Banking & Finance. 34(9). pp.2121-2131.

Elango, B. and et. al., 2010. Organizational ethics, individual ethics, and ethical intentions in

international decision-making. Journal of Business Ethics. 97(4). pp.543-561.

Ho, W., Xu, X. and Dey, P.K., 2010. Multi-criteria decision making approaches for supplier

evaluation and selection: A literature review. European Journal of operational

research. 202(1). pp.16-24.

Masini, A. and Menichetti, E., 2012. The impact of behavioural factors in the renewable energy

investment decision making process: Conceptual framework and empirical findings.

Energy Policy. 40. pp.28-38.

Maxwell, A.L., Jeffrey, S.A. and Lévesque, M., 2011. Business angel early stage decision

making. Journal of Business Venturing. 26(2). pp.212-225.

Mingst, K.A. and Arreguín-Toft, I.M., 2013. Essentials of International Relations: Sixth

International Student Edition. WW Norton & Company.

Morgan, R.K., 2012. Environmental impact assessment: the state of the art. Impact Assessment

and Project Appraisal. 30(1). pp.5-14.

Nielsen, B.B. and Nielsen, S., 2011. The role of top management team international orientation

in international strategic decision-making: The choice of foreign entry mode. Journal of

World Business. 46(2). pp.185-193.

Sanayei, A., Mousavi, S.F. and Yazdankhah, A., 2010. Group decision making process for

supplier selection with VIKOR under fuzzy environment. Expert Systems with

Applications. 37(1). pp.24-30.

Xu, Z., 2010. A method based on distance measure for interval-valued intuitionistic fuzzy group

decision making. Information sciences. 180(1). pp.181-190.

Ye, J., 2013. Multicriteria decision-making method using the correlation coefficient under

single-valued neutrosophic environment. International Journal of General Systems.

42(4). pp.386-394.

Online:

Financial decision making 2017 [Online]. Available through:

<https://www.aaltoee.com/programs/financial-decision-making>

10

Books and Journals

Bayne, N. and Woolcock, S. eds., 2011. The new economic diplomacy: decision-making and

negotiation in international economic relations. Ashgate Publishing, Ltd..

Beugelsdijk, S. and Frijns, B., 2010. A cultural explanation of the foreign bias in international

asset allocation. Journal of Banking & Finance. 34(9). pp.2121-2131.

Elango, B. and et. al., 2010. Organizational ethics, individual ethics, and ethical intentions in

international decision-making. Journal of Business Ethics. 97(4). pp.543-561.

Ho, W., Xu, X. and Dey, P.K., 2010. Multi-criteria decision making approaches for supplier

evaluation and selection: A literature review. European Journal of operational

research. 202(1). pp.16-24.

Masini, A. and Menichetti, E., 2012. The impact of behavioural factors in the renewable energy

investment decision making process: Conceptual framework and empirical findings.

Energy Policy. 40. pp.28-38.

Maxwell, A.L., Jeffrey, S.A. and Lévesque, M., 2011. Business angel early stage decision

making. Journal of Business Venturing. 26(2). pp.212-225.

Mingst, K.A. and Arreguín-Toft, I.M., 2013. Essentials of International Relations: Sixth

International Student Edition. WW Norton & Company.

Morgan, R.K., 2012. Environmental impact assessment: the state of the art. Impact Assessment

and Project Appraisal. 30(1). pp.5-14.

Nielsen, B.B. and Nielsen, S., 2011. The role of top management team international orientation

in international strategic decision-making: The choice of foreign entry mode. Journal of

World Business. 46(2). pp.185-193.

Sanayei, A., Mousavi, S.F. and Yazdankhah, A., 2010. Group decision making process for

supplier selection with VIKOR under fuzzy environment. Expert Systems with

Applications. 37(1). pp.24-30.

Xu, Z., 2010. A method based on distance measure for interval-valued intuitionistic fuzzy group

decision making. Information sciences. 180(1). pp.181-190.

Ye, J., 2013. Multicriteria decision-making method using the correlation coefficient under

single-valued neutrosophic environment. International Journal of General Systems.

42(4). pp.386-394.

Online:

Financial decision making 2017 [Online]. Available through:

<https://www.aaltoee.com/programs/financial-decision-making>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.