Boeing 7E7 Project: International Finance and Decision Making

VerifiedAdded on 2020/06/06

|11

|3635

|27

Project

AI Summary

This project is a comprehensive financial analysis of Boeing's 7E7 project, exploring international finance and decision-making processes. It begins with an introduction to international finance and decision-making, followed by an analysis of Boeing's rationale for launching the 7E7. The project delves into the calculation of the required rate of return using IRR, the reasons for not directly using the Capital Asset Pricing Model (CAPM) to estimate the firm's cost of capital, and the application of CAPM to estimate the cost of equity, including beta analysis and risk-free rate considerations. It then determines the appropriate time to use CAPM, the types of risk premium and risk-free rates used, and calculates Boeing's cost of debt, considering commercial and defense risks. The project also examines the weighted average capital structure of Boeing and assesses the attractiveness of the 7E7 project based on the Weighted Average Cost of Capital (WACC), including sensitivity analysis. The analysis concludes with a discussion of the board's approval for the project and overall conclusions, supported by relevant references.

International Finance

&

Decision Making

&

Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Launch of 7E7 project.................................................................................................................1

QUESTION 2...................................................................................................................................2

a) Appropriate required rate of return to evaluate prospective IRRs from the Boeing 7E7.......2

b) Reason for not using Capital Assets Pricing Model to estimate the firm's cost of capital

directly.........................................................................................................................................2

c) Capital Asset Pricing Model to estimate the cost of equity. Analyses of Beta and risk-free

rate...............................................................................................................................................2

d) Appropriate time for using Capital Asset Pricing Model, type of risk-premium and risk-free

rate used in this scenario.............................................................................................................3

e. Boeing's Cost of Debt..............................................................................................................4

f. Commercial and defence risks.................................................................................................4

g. Reason for not using CAPM to estimate cost of debt.............................................................4

h. Weighted average of all debt and long-term debt, which method is to be considered for

calculation of Cost of debts.........................................................................................................5

i. Weighted average Capital structure of Boeing........................................................................5

Question 3........................................................................................................................................6

a. Determination of attractiveness of Boeing 7E7 project on the basis of WACC.....................6

b. Circumstances for the economical attractiveness of this project............................................6

c. Sensitivity analysis..................................................................................................................6

Question 4........................................................................................................................................7

Approval of Board for the Project...............................................................................................7

CONCLUSION................................................................................................................................8

.........................................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Launch of 7E7 project.................................................................................................................1

QUESTION 2...................................................................................................................................2

a) Appropriate required rate of return to evaluate prospective IRRs from the Boeing 7E7.......2

b) Reason for not using Capital Assets Pricing Model to estimate the firm's cost of capital

directly.........................................................................................................................................2

c) Capital Asset Pricing Model to estimate the cost of equity. Analyses of Beta and risk-free

rate...............................................................................................................................................2

d) Appropriate time for using Capital Asset Pricing Model, type of risk-premium and risk-free

rate used in this scenario.............................................................................................................3

e. Boeing's Cost of Debt..............................................................................................................4

f. Commercial and defence risks.................................................................................................4

g. Reason for not using CAPM to estimate cost of debt.............................................................4

h. Weighted average of all debt and long-term debt, which method is to be considered for

calculation of Cost of debts.........................................................................................................5

i. Weighted average Capital structure of Boeing........................................................................5

Question 3........................................................................................................................................6

a. Determination of attractiveness of Boeing 7E7 project on the basis of WACC.....................6

b. Circumstances for the economical attractiveness of this project............................................6

c. Sensitivity analysis..................................................................................................................6

Question 4........................................................................................................................................7

Approval of Board for the Project...............................................................................................7

CONCLUSION................................................................................................................................8

.........................................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

International finance is the part of financial economics which is broadly concerned with

monetary and macroeconomics interlinked between more than two countries. Decision making is

a process of selecting the best alternatives among various options available with a company

(Bayne and Woolcock, 2011). International finance and decision making together means a

judgement in selecting the best global project by a company. In the given assignment, case study

of Boeing reflects its decision making process to evaluate launch of 7E7 project. Boeing's main

competitor is Airbus and so company wants to launch an aircraft which is cheap and reduces

operating costs as well as fulfil the demand of current market which is flexibility in travelling

long and short term routes.

QUESTION 1

Launch of 7E7 project

Boeing is planning to launch 7E7 project because of various reasons which are given as below:

To replace mid-size planes

To create mid-size planes that can travel long distances

To reduce fuel price by 20%

To become safe from the issue of being copy of this design by Airbus

To lower down operating costs

This product is meeting with the requirements of customers.

It can compete with Airbus's short distance planes.

Yes, this is the right time to launch such a plane because it will fulfil the demand of its

customers which is providing plane having low operating costs and that are flexible to cover long

and short distances. As the biggest competitor of Boeing that is Airbus has already launched

A300/310, family which is capable to flexibly serve short, medium and long range routes. So,

Boeing is required to compete with Airbus to recover its market share in Commercial- Aircraft

Industry. Due to decrease in customer’s demand from 527 planes to 381, Boeing's earnings is

going down. Hence, to increase in customer’s demand, Boeing needs to launch 7E7 project.

International finance is the part of financial economics which is broadly concerned with

monetary and macroeconomics interlinked between more than two countries. Decision making is

a process of selecting the best alternatives among various options available with a company

(Bayne and Woolcock, 2011). International finance and decision making together means a

judgement in selecting the best global project by a company. In the given assignment, case study

of Boeing reflects its decision making process to evaluate launch of 7E7 project. Boeing's main

competitor is Airbus and so company wants to launch an aircraft which is cheap and reduces

operating costs as well as fulfil the demand of current market which is flexibility in travelling

long and short term routes.

QUESTION 1

Launch of 7E7 project

Boeing is planning to launch 7E7 project because of various reasons which are given as below:

To replace mid-size planes

To create mid-size planes that can travel long distances

To reduce fuel price by 20%

To become safe from the issue of being copy of this design by Airbus

To lower down operating costs

This product is meeting with the requirements of customers.

It can compete with Airbus's short distance planes.

Yes, this is the right time to launch such a plane because it will fulfil the demand of its

customers which is providing plane having low operating costs and that are flexible to cover long

and short distances. As the biggest competitor of Boeing that is Airbus has already launched

A300/310, family which is capable to flexibly serve short, medium and long range routes. So,

Boeing is required to compete with Airbus to recover its market share in Commercial- Aircraft

Industry. Due to decrease in customer’s demand from 527 planes to 381, Boeing's earnings is

going down. Hence, to increase in customer’s demand, Boeing needs to launch 7E7 project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 2

a) Appropriate required rate of return to evaluate prospective IRRs from the Boeing 7E7

On the basis of above case scenario, the observed IRR is 15.7% but it is also given that

IRR is sensitive to selling of units which means IRR will be increased with growth in sales unit

and it will decrease with decline in revenue by 11%. Hence, by taking average of 11% for 5

years, the required rate of return should be at least 17.9%. At this IRR, company’s NPV of this

project will be greater than 0. Therefore, 3 possible scenarios can be presented by taking NPV or

Net present Value as a base:

NPV > 0: At this scenario, project of 7E7 should be undertaken by Boeing. But

company should also be considered about other alternatives which are available in the

market.

NPV = 0: At this stage, company might not lose anything but it will not gain anything as

well. But this scenario is risky as due to high volatility in the market, NPV might go

negative.

NPV < 0: It is a clear choice that company should obviously ignore such an alternatives

and the project.

b) Reason for not using Capital Assets Pricing Model to estimate the firm's cost of capital

directly

Cost of capital includes the cost of debt + cost of equity. Capital Assets Pricing Model is

only useful for calculating cost of equity and risk on required rate of returns. Hence, CAPM can't

be used to directly estimate cost of capital (Mingst and Arreguín-Toft, 2013). It can only be

useful to estimate the cost of equity and later, this value could be used in WACC or Weighted

Average Cost of Capital method to estimate cost of the capital structure of Boeing.

c) Capital Asset Pricing Model to estimate the cost of equity. Analyses of Beta and risk-free rate

According to CAPM or Cost Asset Pricing Model concept, cost of Equity = Rf + Beta *

EMRP (Tzeng and Huang, 2011). In this, Rf is risk free rate, Beta is volatility of risk and EMRP

is Equity Market Risk Premium. Risk free rate is based on 3 months US Treasury bill or T-Bill,

Beta is identified from the financial reports of Boeing (Yahoo finance). This report indicates the

fluctuations in Boeing's stock as compared to S&P Index. EMRP is calculated in “d” part of

Question 2.

a) Appropriate required rate of return to evaluate prospective IRRs from the Boeing 7E7

On the basis of above case scenario, the observed IRR is 15.7% but it is also given that

IRR is sensitive to selling of units which means IRR will be increased with growth in sales unit

and it will decrease with decline in revenue by 11%. Hence, by taking average of 11% for 5

years, the required rate of return should be at least 17.9%. At this IRR, company’s NPV of this

project will be greater than 0. Therefore, 3 possible scenarios can be presented by taking NPV or

Net present Value as a base:

NPV > 0: At this scenario, project of 7E7 should be undertaken by Boeing. But

company should also be considered about other alternatives which are available in the

market.

NPV = 0: At this stage, company might not lose anything but it will not gain anything as

well. But this scenario is risky as due to high volatility in the market, NPV might go

negative.

NPV < 0: It is a clear choice that company should obviously ignore such an alternatives

and the project.

b) Reason for not using Capital Assets Pricing Model to estimate the firm's cost of capital

directly

Cost of capital includes the cost of debt + cost of equity. Capital Assets Pricing Model is

only useful for calculating cost of equity and risk on required rate of returns. Hence, CAPM can't

be used to directly estimate cost of capital (Mingst and Arreguín-Toft, 2013). It can only be

useful to estimate the cost of equity and later, this value could be used in WACC or Weighted

Average Cost of Capital method to estimate cost of the capital structure of Boeing.

c) Capital Asset Pricing Model to estimate the cost of equity. Analyses of Beta and risk-free rate

According to CAPM or Cost Asset Pricing Model concept, cost of Equity = Rf + Beta *

EMRP (Tzeng and Huang, 2011). In this, Rf is risk free rate, Beta is volatility of risk and EMRP

is Equity Market Risk Premium. Risk free rate is based on 3 months US Treasury bill or T-Bill,

Beta is identified from the financial reports of Boeing (Yahoo finance). This report indicates the

fluctuations in Boeing's stock as compared to S&P Index. EMRP is calculated in “d” part of

Question 2.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hence, the calculation of Cost of Equity through Capital Asset Pricing Model is done as

below:

Cost of Equity = Rf + Beta * EMRP

= 0.85% + 1.43 * 3.71%

= 6.15%

The result 6.15% indicates that Boeing is paying 6.15% of net profit after tax as a

dividend to its shareholders or investors.

Beta analysis is done by referring stock of Boeing:NYSE:BA. From here Beta is

calculated with the help of excel sheet, in which value of Boeing's and S&P Index's closing price

for whole month was taken, the value of Beta is 1.43 till 1st December, 2017. Beta is obtained

from financial reports which shows how the stock of Boeing's fluctuates with respect to S&P

Index. In a graph, beta is a slope of the best fit straight line.

d) Appropriate time for using Capital Asset Pricing Model, type of risk-premium and risk-free

rate used in this scenario

Capital Asset Pricing Model is useful for only those companies which have raised their

money by issuing shares and that are registered in stock market. It is commonly used to find the

cost of equity (Hopwood, Unerman and Fries, 2010). It is also referred by investors to get an idea

of free floating rate and match it with their required rate of return to get information of risk

premium.

Risk-premium or equity market risk premium is the excess return over its risk-free rate

provided by company to their investors (Brealey, Allen and Mohanty, 2012). This return is

treated as a reward to its shareholders for taking relatively high risk by purchasing equity of

Boeing. Risk premium is used on the basis of calculation in which expected rate of return is

subtracted by risk-free rate.

Risk free is used by taking 3 month’s T-Bills backed by US government which is 0.85%.

Hence, below is the calculation of EMRP:

EMRP = Expected rate of return – Risk-free rate

= (Dividend Yield + Growth rate of dividends) - Risk-free rate

= 4.56% - 0.85% = 3.71%.

Here, Dividend Yield is given in the scenario.

below:

Cost of Equity = Rf + Beta * EMRP

= 0.85% + 1.43 * 3.71%

= 6.15%

The result 6.15% indicates that Boeing is paying 6.15% of net profit after tax as a

dividend to its shareholders or investors.

Beta analysis is done by referring stock of Boeing:NYSE:BA. From here Beta is

calculated with the help of excel sheet, in which value of Boeing's and S&P Index's closing price

for whole month was taken, the value of Beta is 1.43 till 1st December, 2017. Beta is obtained

from financial reports which shows how the stock of Boeing's fluctuates with respect to S&P

Index. In a graph, beta is a slope of the best fit straight line.

d) Appropriate time for using Capital Asset Pricing Model, type of risk-premium and risk-free

rate used in this scenario

Capital Asset Pricing Model is useful for only those companies which have raised their

money by issuing shares and that are registered in stock market. It is commonly used to find the

cost of equity (Hopwood, Unerman and Fries, 2010). It is also referred by investors to get an idea

of free floating rate and match it with their required rate of return to get information of risk

premium.

Risk-premium or equity market risk premium is the excess return over its risk-free rate

provided by company to their investors (Brealey, Allen and Mohanty, 2012). This return is

treated as a reward to its shareholders for taking relatively high risk by purchasing equity of

Boeing. Risk premium is used on the basis of calculation in which expected rate of return is

subtracted by risk-free rate.

Risk free is used by taking 3 month’s T-Bills backed by US government which is 0.85%.

Hence, below is the calculation of EMRP:

EMRP = Expected rate of return – Risk-free rate

= (Dividend Yield + Growth rate of dividends) - Risk-free rate

= 4.56% - 0.85% = 3.71%.

Here, Dividend Yield is given in the scenario.

e. Boeing's Cost of Debt

Cost of Debt is generally based on the cost of company's bonds. Bond's are usually long-

term debt of a company and comes under long-term loans. In this scenario, Boeing has issued 30

years treasury bills @4.56%. So, its Yield of bond is 4.56%. As in raising capital through debt

sources usually get a benefit in tax, so Boeing only requires to pay 65% of interest out of 4.56%.

Below is the calculation of Cost of Debt:

Cost of Debt = Yield of Bond (1 – Cooperative tax)

= 4.56% (1 - .35)

= 2.964%

Interpretation: Cost of debt is reduced to 2.964%, due to benefit in tax which is 35% (as

given in scenario).

f. Commercial and defence risks

Commercial refers to providing services to public through domestic and international

flights (Acharya, 2010). While defence raises its income from army or particular government of

that nation by selling armed jet fighters to them.

Debt is subject to commercial and defence risk. Because these risks effects the rate of

debt or yield of bond in market. For example, if chances of success of launching Boeing's new

project which is 7E7 is very low or it is pertaining to high risk, than company requires to pay

high yield on their treasury bills. On the other hand if the risk of failure is low, than company can

manage to raise debts at lower interest margin. Both commercial and defence sectors are its

income source and risks of failure in both field would effect interest rate on debts.

Yes, it is recommended to the company to back out from commercial risk components,

for getting debt at reducing rate. But it can't be deny the concept that, more risks more return.

Hence, company should focus on effective portfolio by adding different projects.

g. Reason for not using CAPM to estimate cost of debt

Cost Asset Pricing Model is not using to estimate cost of debt, because CAPM is useful

only to determine cost of equity and required rate of return for a company. The formulae of

estimating CAPM is Rf + Beta * (Expected rate – Rf). Hence, cost of debt includes taxation rate,

to analyse actual cost of yield paid on treasury bonds (Papadopoulos and Heslop, 2014). As cost

of equity and debt's motives is different from each other, therefore CAPM can't used to estimate

Cost of Debt is generally based on the cost of company's bonds. Bond's are usually long-

term debt of a company and comes under long-term loans. In this scenario, Boeing has issued 30

years treasury bills @4.56%. So, its Yield of bond is 4.56%. As in raising capital through debt

sources usually get a benefit in tax, so Boeing only requires to pay 65% of interest out of 4.56%.

Below is the calculation of Cost of Debt:

Cost of Debt = Yield of Bond (1 – Cooperative tax)

= 4.56% (1 - .35)

= 2.964%

Interpretation: Cost of debt is reduced to 2.964%, due to benefit in tax which is 35% (as

given in scenario).

f. Commercial and defence risks

Commercial refers to providing services to public through domestic and international

flights (Acharya, 2010). While defence raises its income from army or particular government of

that nation by selling armed jet fighters to them.

Debt is subject to commercial and defence risk. Because these risks effects the rate of

debt or yield of bond in market. For example, if chances of success of launching Boeing's new

project which is 7E7 is very low or it is pertaining to high risk, than company requires to pay

high yield on their treasury bills. On the other hand if the risk of failure is low, than company can

manage to raise debts at lower interest margin. Both commercial and defence sectors are its

income source and risks of failure in both field would effect interest rate on debts.

Yes, it is recommended to the company to back out from commercial risk components,

for getting debt at reducing rate. But it can't be deny the concept that, more risks more return.

Hence, company should focus on effective portfolio by adding different projects.

g. Reason for not using CAPM to estimate cost of debt

Cost Asset Pricing Model is not using to estimate cost of debt, because CAPM is useful

only to determine cost of equity and required rate of return for a company. The formulae of

estimating CAPM is Rf + Beta * (Expected rate – Rf). Hence, cost of debt includes taxation rate,

to analyse actual cost of yield paid on treasury bonds (Papadopoulos and Heslop, 2014). As cost

of equity and debt's motives is different from each other, therefore CAPM can't used to estimate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost of debt. The another reason could be factors like free float rate and risk-premium. These

factors are irrelevant at the time of estimating cost of debts and doesn't effects the value of debt.

h. Weighted average of all debt and long-term debt, which method is to be considered for

calculation of Cost of debts

Weighted average of all debt includes, total liabilities which consists of long-term and

short-term liabilities. While calculating weighted average of long-term debt consists of only

long term liabilities (Gal, Stewart and Hanne, 2013). As per financing concerns, weighted

average of long-term liabilities should be considered for calculation of cost of debts. Some of the

reasons for not using average of all debts are; All debts or liabilities includes short-term debts

also, in which Accounts payable indicates those funds which is owned by creditors or suppliers.

These liabilities are not permitted to get tax benefit, because company doesn't have to pay any

regular interest expenses to their creditors. These short-term liabilities are to be paid within a

year and long term has to be paid for long time. So, average of both types would get irrelevant

result, due no interest payment on short-term liabilities.

i. Weighted average Capital structure of Boeing

WACC is average of cost of equity and debt taken by the company. The Weighted

Average Cost of Capital of Boeing is given below:

WACC = Wdrd(1 – t) + Were

Where:

Wd = Proportion of debt in a market

rd = Pre tax cost of debt capital

t = Marginal effective corporate tax rate

We = Proportion of equity in a market

re = Cost of equity capital

Putting the value in the above formulae, the following value will be obtained:

WACC = 0.10 * 0.456(1 - 0.35) + 0.90 * 0.0615

= 0.02964 + 0.05535

= 0.08499 or 8.5%

Interpretation: The above result indicates that total cost of capital, which is paid by

business for raising capital is 8.5% of capital. Out of 100% capital, 10% is raises through bonds

and 90% is raised through equity. Thus the ratio is .1 is to .9 which Debt/Equity.

factors are irrelevant at the time of estimating cost of debts and doesn't effects the value of debt.

h. Weighted average of all debt and long-term debt, which method is to be considered for

calculation of Cost of debts

Weighted average of all debt includes, total liabilities which consists of long-term and

short-term liabilities. While calculating weighted average of long-term debt consists of only

long term liabilities (Gal, Stewart and Hanne, 2013). As per financing concerns, weighted

average of long-term liabilities should be considered for calculation of cost of debts. Some of the

reasons for not using average of all debts are; All debts or liabilities includes short-term debts

also, in which Accounts payable indicates those funds which is owned by creditors or suppliers.

These liabilities are not permitted to get tax benefit, because company doesn't have to pay any

regular interest expenses to their creditors. These short-term liabilities are to be paid within a

year and long term has to be paid for long time. So, average of both types would get irrelevant

result, due no interest payment on short-term liabilities.

i. Weighted average Capital structure of Boeing

WACC is average of cost of equity and debt taken by the company. The Weighted

Average Cost of Capital of Boeing is given below:

WACC = Wdrd(1 – t) + Were

Where:

Wd = Proportion of debt in a market

rd = Pre tax cost of debt capital

t = Marginal effective corporate tax rate

We = Proportion of equity in a market

re = Cost of equity capital

Putting the value in the above formulae, the following value will be obtained:

WACC = 0.10 * 0.456(1 - 0.35) + 0.90 * 0.0615

= 0.02964 + 0.05535

= 0.08499 or 8.5%

Interpretation: The above result indicates that total cost of capital, which is paid by

business for raising capital is 8.5% of capital. Out of 100% capital, 10% is raises through bonds

and 90% is raised through equity. Thus the ratio is .1 is to .9 which Debt/Equity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3

a. Determination of attractiveness of Boeing 7E7 project on the basis of WACC

In the previous question, the value of WACC found is 8.5% of capital raised. Interest on

bonds is mandatory to pay by Boeing regardless of profit or loss in companies financial

statements. This makes debt funds riskier for a company and only suitable for only those firms

which is able to earn regular income. Hence the mixture of both type of funds is good for

financial health of a company.

As the value of WACC is below average which indicates that, this project is out of

potential risks and this makes project attractive for investors to invest their funds into this project

(Frieden, 2015). Hence, it is recommended to board of Boeing, that it should adopt this particular

project. As this project is feasible and profitable for the company.

b. Circumstances for the economical attractiveness of this project

This project will be economically attractive, if Boeing is able to sell maximum planes in

available time at certain price. The internal rate of return at which the value of NPV is zero is

15.4%. This indicates that company has to sell minimum 2,500 7E7 products within 20 years to

increase funds value of shareholders. Hence, below are two market analysis of Boeing, which is

also a circumstances for its economical feasibility:

Market Demand: The US airline industries has recorded less number of passengers in

previous years. It is not easy to achieve projected sales figures in this market atmosphere.

The factors which has affected demand are cost and advance technologies (Silveira, Kim

and Langa, 2010). In a weak economy, people try to travel only to local destinations

instead of abroad.

Market Share: Boeing's biggest rival is Airbus, which would give toughest competition

to new product 7E7. But lower operating share offer by Boeing company through

launching this new project, might increase the future market share of the company. The

another critical success factor of 7E7 might be expandable wing engineering.

c. Sensitivity analysis

Sensitivity analysis also known as variance analysis, in which results are measured on the

basis of optimistic and pessimistic estimates (Merigó and Casanovas, 2010). Where optimistic

a. Determination of attractiveness of Boeing 7E7 project on the basis of WACC

In the previous question, the value of WACC found is 8.5% of capital raised. Interest on

bonds is mandatory to pay by Boeing regardless of profit or loss in companies financial

statements. This makes debt funds riskier for a company and only suitable for only those firms

which is able to earn regular income. Hence the mixture of both type of funds is good for

financial health of a company.

As the value of WACC is below average which indicates that, this project is out of

potential risks and this makes project attractive for investors to invest their funds into this project

(Frieden, 2015). Hence, it is recommended to board of Boeing, that it should adopt this particular

project. As this project is feasible and profitable for the company.

b. Circumstances for the economical attractiveness of this project

This project will be economically attractive, if Boeing is able to sell maximum planes in

available time at certain price. The internal rate of return at which the value of NPV is zero is

15.4%. This indicates that company has to sell minimum 2,500 7E7 products within 20 years to

increase funds value of shareholders. Hence, below are two market analysis of Boeing, which is

also a circumstances for its economical feasibility:

Market Demand: The US airline industries has recorded less number of passengers in

previous years. It is not easy to achieve projected sales figures in this market atmosphere.

The factors which has affected demand are cost and advance technologies (Silveira, Kim

and Langa, 2010). In a weak economy, people try to travel only to local destinations

instead of abroad.

Market Share: Boeing's biggest rival is Airbus, which would give toughest competition

to new product 7E7. But lower operating share offer by Boeing company through

launching this new project, might increase the future market share of the company. The

another critical success factor of 7E7 might be expandable wing engineering.

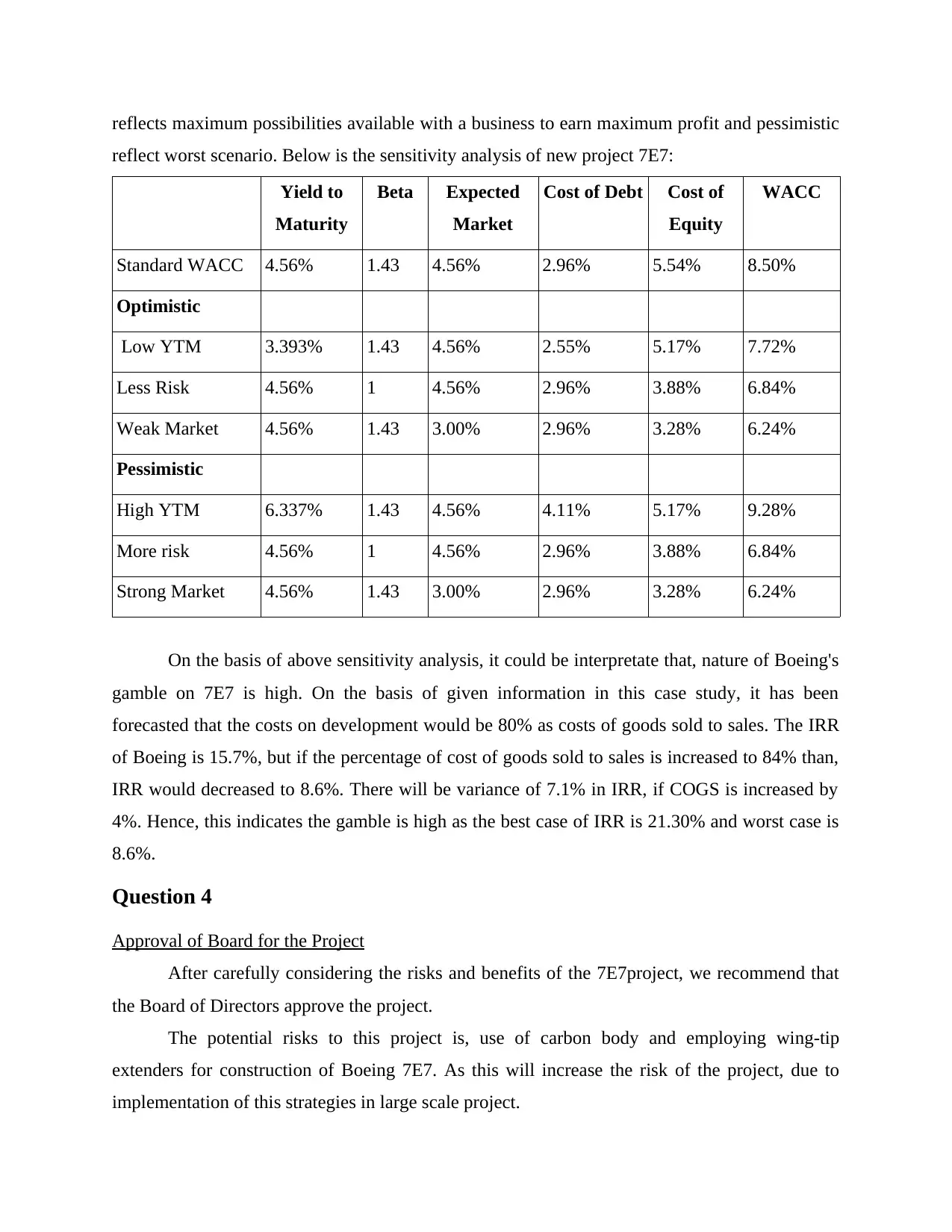

c. Sensitivity analysis

Sensitivity analysis also known as variance analysis, in which results are measured on the

basis of optimistic and pessimistic estimates (Merigó and Casanovas, 2010). Where optimistic

reflects maximum possibilities available with a business to earn maximum profit and pessimistic

reflect worst scenario. Below is the sensitivity analysis of new project 7E7:

Yield to

Maturity

Beta Expected

Market

Cost of Debt Cost of

Equity

WACC

Standard WACC 4.56% 1.43 4.56% 2.96% 5.54% 8.50%

Optimistic

Low YTM 3.393% 1.43 4.56% 2.55% 5.17% 7.72%

Less Risk 4.56% 1 4.56% 2.96% 3.88% 6.84%

Weak Market 4.56% 1.43 3.00% 2.96% 3.28% 6.24%

Pessimistic

High YTM 6.337% 1.43 4.56% 4.11% 5.17% 9.28%

More risk 4.56% 1 4.56% 2.96% 3.88% 6.84%

Strong Market 4.56% 1.43 3.00% 2.96% 3.28% 6.24%

On the basis of above sensitivity analysis, it could be interpretate that, nature of Boeing's

gamble on 7E7 is high. On the basis of given information in this case study, it has been

forecasted that the costs on development would be 80% as costs of goods sold to sales. The IRR

of Boeing is 15.7%, but if the percentage of cost of goods sold to sales is increased to 84% than,

IRR would decreased to 8.6%. There will be variance of 7.1% in IRR, if COGS is increased by

4%. Hence, this indicates the gamble is high as the best case of IRR is 21.30% and worst case is

8.6%.

Question 4

Approval of Board for the Project

After carefully considering the risks and benefits of the 7E7project, we recommend that

the Board of Directors approve the project.

The potential risks to this project is, use of carbon body and employing wing-tip

extenders for construction of Boeing 7E7. As this will increase the risk of the project, due to

implementation of this strategies in large scale project.

reflect worst scenario. Below is the sensitivity analysis of new project 7E7:

Yield to

Maturity

Beta Expected

Market

Cost of Debt Cost of

Equity

WACC

Standard WACC 4.56% 1.43 4.56% 2.96% 5.54% 8.50%

Optimistic

Low YTM 3.393% 1.43 4.56% 2.55% 5.17% 7.72%

Less Risk 4.56% 1 4.56% 2.96% 3.88% 6.84%

Weak Market 4.56% 1.43 3.00% 2.96% 3.28% 6.24%

Pessimistic

High YTM 6.337% 1.43 4.56% 4.11% 5.17% 9.28%

More risk 4.56% 1 4.56% 2.96% 3.88% 6.84%

Strong Market 4.56% 1.43 3.00% 2.96% 3.28% 6.24%

On the basis of above sensitivity analysis, it could be interpretate that, nature of Boeing's

gamble on 7E7 is high. On the basis of given information in this case study, it has been

forecasted that the costs on development would be 80% as costs of goods sold to sales. The IRR

of Boeing is 15.7%, but if the percentage of cost of goods sold to sales is increased to 84% than,

IRR would decreased to 8.6%. There will be variance of 7.1% in IRR, if COGS is increased by

4%. Hence, this indicates the gamble is high as the best case of IRR is 21.30% and worst case is

8.6%.

Question 4

Approval of Board for the Project

After carefully considering the risks and benefits of the 7E7project, we recommend that

the Board of Directors approve the project.

The potential risks to this project is, use of carbon body and employing wing-tip

extenders for construction of Boeing 7E7. As this will increase the risk of the project, due to

implementation of this strategies in large scale project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Airbus is a big rival of Boeing, they have already launched A380 plane, which is best

replacement to 7E7. This indicates that, in case Boeing is not covering up new innovation plans

in its new project like fuel efficiency and other attributes of long haul airliner than they might

lose huge market shares. Therefore Boeing has to take some risks to safe themselves from

loosing huge market share through launching this new project. 7E7 project has another

opportunities to get green flag from airline industries to purchase this new plane because more

passengers can sit in this plane. This new featured plane is getting attractive versatility through

its expandable wings.

This new project has huge growth chances, due to large availability of supply chain

across the world. The parts of Boeing is manufactured by other countries, this would help

company in construct this new plane at lower cost.

CONCLUSION

After analysing whole assignment and critical analysis of new project of Boeing which is

7E7, it can be concluded that, there is a very good opportunities for the company that this project

will increase the wealth of the shareholders. There are other risks mentioned above that must be

considered but on balance the reasons to go forward with the project outweigh those against it.

replacement to 7E7. This indicates that, in case Boeing is not covering up new innovation plans

in its new project like fuel efficiency and other attributes of long haul airliner than they might

lose huge market shares. Therefore Boeing has to take some risks to safe themselves from

loosing huge market share through launching this new project. 7E7 project has another

opportunities to get green flag from airline industries to purchase this new plane because more

passengers can sit in this plane. This new featured plane is getting attractive versatility through

its expandable wings.

This new project has huge growth chances, due to large availability of supply chain

across the world. The parts of Boeing is manufactured by other countries, this would help

company in construct this new plane at lower cost.

CONCLUSION

After analysing whole assignment and critical analysis of new project of Boeing which is

7E7, it can be concluded that, there is a very good opportunities for the company that this project

will increase the wealth of the shareholders. There are other risks mentioned above that must be

considered but on balance the reasons to go forward with the project outweigh those against it.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Acharya, V. V., and et. al., 2010. Regulating Wall Street: The Dodd-Frank Act and the new

architecture of global finance (Vol. 608). John Wiley & Sons.

Bayne, N. and Woolcock, S. eds., 2011. The new economic diplomacy: decision-making and

negotiation in international economic relations. Ashgate Publishing, Ltd..

Brealey, R. A., Myers, S. C., Allen, F. and Mohanty, P., 2012. Principles of corporate finance.

Tata McGraw-Hill Education.

Frieden, J., 2015. Banking on the world: the politics of American international finance.

Routledge.

Gal, T., Stewart, T. and Hanne, T. eds., 2013. Multicriteria decision making: advances in MCDM

models, algorithms, theory, and applications (Vol. 21). Springer Science & Business

Media.

Hopwood, A. G., Unerman, J. and Fries, J., 2010. Accounting for sustainability: Practical

insights. Earthscan.

Merigó, J. M. and Casanovas, M., 2010. Fuzzy Generalized Hybrid Aggregation Operators and

its Application in Fuzzy Decision Making. International Journal of Fuzzy

Systems. 12(1).

Mingst, K. A. and Arreguín-Toft, I. M., 2013. Essentials of International Relations: Sixth

International Student Edition. WW Norton & Company.

Papadopoulos, N. and Heslop, L. A., 2014. Product-country images: Impact and role in

international marketing. Routledge.

Silveira, M. J., Kim, S. Y. and Langa, K. M., 2010. Advance directives and outcomes of

surrogate decision making before death. New England Journal of Medicine. 362(13).

pp.1211-1218.

Tzeng, G. H. and Huang, J. J., 2011. Multiple attribute decision making: methods and

applications. CRC press.

Online

Yahoo finance, 2017. [Online]. Available

through<https://uk.finance.yahoo.com/quote/BA/financials?p=BA>.

Books and Journals

Acharya, V. V., and et. al., 2010. Regulating Wall Street: The Dodd-Frank Act and the new

architecture of global finance (Vol. 608). John Wiley & Sons.

Bayne, N. and Woolcock, S. eds., 2011. The new economic diplomacy: decision-making and

negotiation in international economic relations. Ashgate Publishing, Ltd..

Brealey, R. A., Myers, S. C., Allen, F. and Mohanty, P., 2012. Principles of corporate finance.

Tata McGraw-Hill Education.

Frieden, J., 2015. Banking on the world: the politics of American international finance.

Routledge.

Gal, T., Stewart, T. and Hanne, T. eds., 2013. Multicriteria decision making: advances in MCDM

models, algorithms, theory, and applications (Vol. 21). Springer Science & Business

Media.

Hopwood, A. G., Unerman, J. and Fries, J., 2010. Accounting for sustainability: Practical

insights. Earthscan.

Merigó, J. M. and Casanovas, M., 2010. Fuzzy Generalized Hybrid Aggregation Operators and

its Application in Fuzzy Decision Making. International Journal of Fuzzy

Systems. 12(1).

Mingst, K. A. and Arreguín-Toft, I. M., 2013. Essentials of International Relations: Sixth

International Student Edition. WW Norton & Company.

Papadopoulos, N. and Heslop, L. A., 2014. Product-country images: Impact and role in

international marketing. Routledge.

Silveira, M. J., Kim, S. Y. and Langa, K. M., 2010. Advance directives and outcomes of

surrogate decision making before death. New England Journal of Medicine. 362(13).

pp.1211-1218.

Tzeng, G. H. and Huang, J. J., 2011. Multiple attribute decision making: methods and

applications. CRC press.

Online

Yahoo finance, 2017. [Online]. Available

through<https://uk.finance.yahoo.com/quote/BA/financials?p=BA>.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.