Financial Performance and Growth of Boeing 7E7 Project: Report

VerifiedAdded on 2020/07/22

|12

|3664

|40

Report

AI Summary

This report delves into the financial analysis of Boeing's 7E7 project, examining the international finance and decision-making processes involved. It begins with an introduction to international finance and the context of the 7E7 project, highlighting the challenges faced by Boeing in launching the project. The report calculates the required rate of return using IRR and other financial metrics, evaluates the Capital Asset Pricing Model (CAPM) and its limitations in estimating the cost of capital, and demonstrates its use in calculating the cost of equity. It also addresses the use of Beta in assessing project risk, determines the cost of debt, and explores commercial risk components. The report further calculates the weighted average cost of debt and assesses capital structure weights. It then critiques the use of WACC and identifies situations where the project would be attractive, followed by a discussion of sensitivity analysis. The report concludes with a final evaluation of the project and references relevant financial literature.

International Finance &

Decision Making

Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a. Launching of 7E7 project...................................................................................................1

QUESTION 2...................................................................................................................................2

a) Required rate of return with IRRs from the Boeing 7E7...................................................2

b) Critical evaluation of CAPM model that does not directly estimate cost of capital..........2

c) Use of CAPM to calculate cost of equity ..........................................................................2

d) Use of Beta.........................................................................................................................3

e) Boeing cost of debts...........................................................................................................3

F): Commercial risk components...........................................................................................4

g): Discuss not simple use of CAPM to estimate cost of debt...............................................4

H): Calculate a weighted average of debt ..............................................................................4

I): Capital structure weight ....................................................................................................5

QUESTION 3...................................................................................................................................5

a) Judgement against WACC.................................................................................................5

b) Situation in which project can be attractive.......................................................................6

c) Sensitivity analysis.............................................................................................................6

QUESTION 4...................................................................................................................................7

Is it board approve the 7E7 ....................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a. Launching of 7E7 project...................................................................................................1

QUESTION 2...................................................................................................................................2

a) Required rate of return with IRRs from the Boeing 7E7...................................................2

b) Critical evaluation of CAPM model that does not directly estimate cost of capital..........2

c) Use of CAPM to calculate cost of equity ..........................................................................2

d) Use of Beta.........................................................................................................................3

e) Boeing cost of debts...........................................................................................................3

F): Commercial risk components...........................................................................................4

g): Discuss not simple use of CAPM to estimate cost of debt...............................................4

H): Calculate a weighted average of debt ..............................................................................4

I): Capital structure weight ....................................................................................................5

QUESTION 3...................................................................................................................................5

a) Judgement against WACC.................................................................................................5

b) Situation in which project can be attractive.......................................................................6

c) Sensitivity analysis.............................................................................................................6

QUESTION 4...................................................................................................................................7

Is it board approve the 7E7 ....................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

International finance is said to be the branch of economics that is associated with the

monetary and macroeconomic relation among two or more countries. Financial decisions are

linked with cross border complexities. They need to make choice about raising capital,

investment, risk management and other necessary aspects which involve international

consideration (Bayne and Woolcock, 2011). In this project report, information about 7E7 project

which is planned by Boeing is discussed. Financial analysis for Boeing 7E7 is done by using IRR

and other sources. Various tools and techniques are used to discuss the financial performance

and chances of future growth of Boeing.

QUESTION 1

a. Launching of 7E7 project

Boeing is associated with designing plenty of attractive and economic air planes that

meet with customers’ needs and wants. Because in the news over the last six months depressed

the market for aircraft. UK went to war against spasms of international terrorism in Iraq that

offered shocking news and deadly illness known as SARS. It results in global travel warnings.

The reason of this, airlines profits were goes on declining stage in coming generation. Thus, at

that point of time, 7E7 could not be launched as it was difficult to get buyers as the market was

down. Profitability cannot be recover according to the expected target. The situation prevail at

that time was incredible in which to launch a huge new airframe project.

It has been seen that Boeing has not introduced any commercial aircraft since its success

of 777 in 1994. So, they are planning to design two new commercial aircraft programs that can

help customers to fly 15% to 20% faster than any other aircraft. But after two years of

development, Boeing customers are not been able to pay a premium price for a faster ride. It

make company to go into financial falloff. After looking into this, they have decided to introduce

7E7 which can regain the commercial sales and control losses of company. This was the perfect

time to launch its project in order to control their sales as well as retain their customers.

1

International finance is said to be the branch of economics that is associated with the

monetary and macroeconomic relation among two or more countries. Financial decisions are

linked with cross border complexities. They need to make choice about raising capital,

investment, risk management and other necessary aspects which involve international

consideration (Bayne and Woolcock, 2011). In this project report, information about 7E7 project

which is planned by Boeing is discussed. Financial analysis for Boeing 7E7 is done by using IRR

and other sources. Various tools and techniques are used to discuss the financial performance

and chances of future growth of Boeing.

QUESTION 1

a. Launching of 7E7 project

Boeing is associated with designing plenty of attractive and economic air planes that

meet with customers’ needs and wants. Because in the news over the last six months depressed

the market for aircraft. UK went to war against spasms of international terrorism in Iraq that

offered shocking news and deadly illness known as SARS. It results in global travel warnings.

The reason of this, airlines profits were goes on declining stage in coming generation. Thus, at

that point of time, 7E7 could not be launched as it was difficult to get buyers as the market was

down. Profitability cannot be recover according to the expected target. The situation prevail at

that time was incredible in which to launch a huge new airframe project.

It has been seen that Boeing has not introduced any commercial aircraft since its success

of 777 in 1994. So, they are planning to design two new commercial aircraft programs that can

help customers to fly 15% to 20% faster than any other aircraft. But after two years of

development, Boeing customers are not been able to pay a premium price for a faster ride. It

make company to go into financial falloff. After looking into this, they have decided to introduce

7E7 which can regain the commercial sales and control losses of company. This was the perfect

time to launch its project in order to control their sales as well as retain their customers.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 2

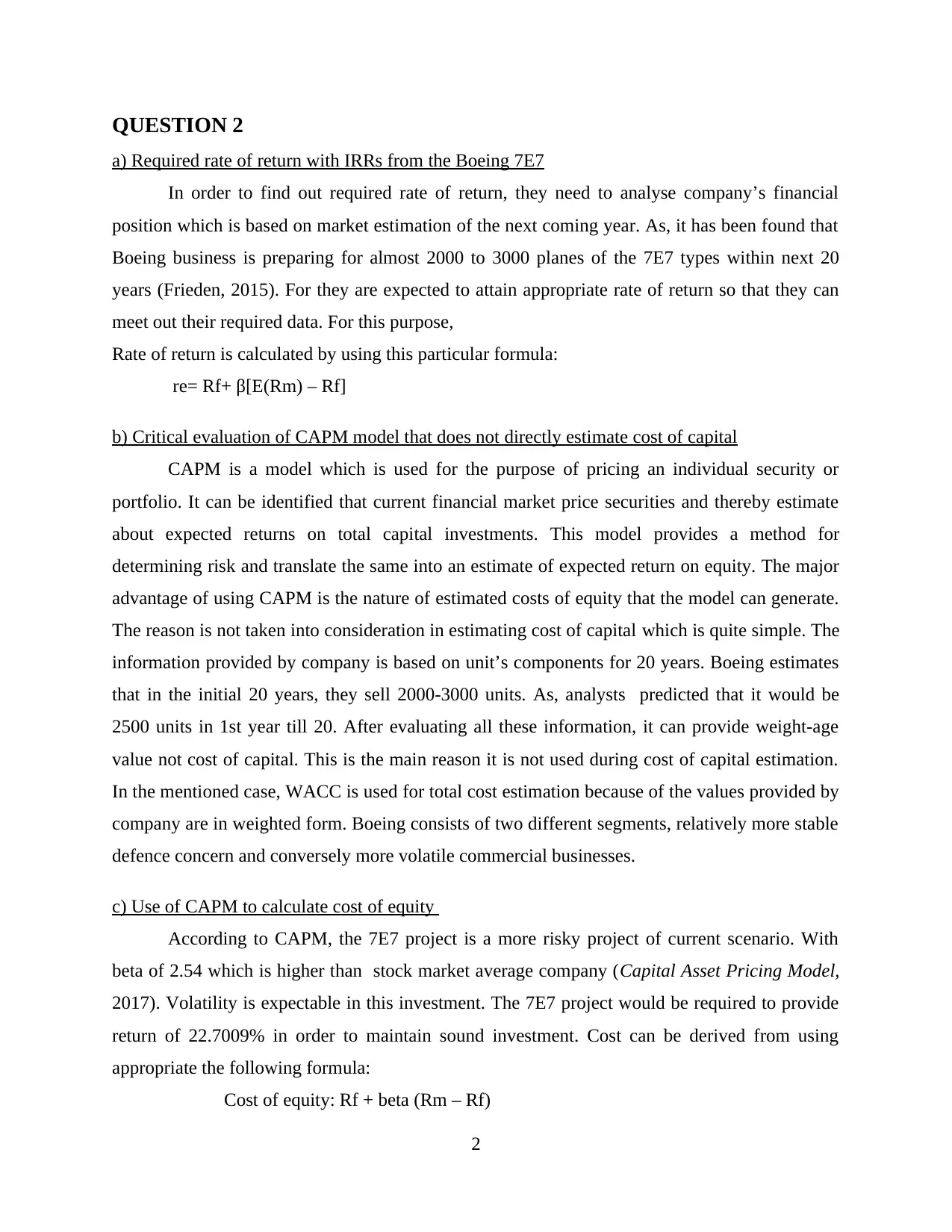

a) Required rate of return with IRRs from the Boeing 7E7

In order to find out required rate of return, they need to analyse company’s financial

position which is based on market estimation of the next coming year. As, it has been found that

Boeing business is preparing for almost 2000 to 3000 planes of the 7E7 types within next 20

years (Frieden, 2015). For they are expected to attain appropriate rate of return so that they can

meet out their required data. For this purpose,

Rate of return is calculated by using this particular formula:

re= Rf+ β[E(Rm) – Rf]

b) Critical evaluation of CAPM model that does not directly estimate cost of capital

CAPM is a model which is used for the purpose of pricing an individual security or

portfolio. It can be identified that current financial market price securities and thereby estimate

about expected returns on total capital investments. This model provides a method for

determining risk and translate the same into an estimate of expected return on equity. The major

advantage of using CAPM is the nature of estimated costs of equity that the model can generate.

The reason is not taken into consideration in estimating cost of capital which is quite simple. The

information provided by company is based on unit’s components for 20 years. Boeing estimates

that in the initial 20 years, they sell 2000-3000 units. As, analysts predicted that it would be

2500 units in 1st year till 20. After evaluating all these information, it can provide weight-age

value not cost of capital. This is the main reason it is not used during cost of capital estimation.

In the mentioned case, WACC is used for total cost estimation because of the values provided by

company are in weighted form. Boeing consists of two different segments, relatively more stable

defence concern and conversely more volatile commercial businesses.

c) Use of CAPM to calculate cost of equity

According to CAPM, the 7E7 project is a more risky project of current scenario. With

beta of 2.54 which is higher than stock market average company (Capital Asset Pricing Model,

2017). Volatility is expectable in this investment. The 7E7 project would be required to provide

return of 22.7009% in order to maintain sound investment. Cost can be derived from using

appropriate the following formula:

Cost of equity: Rf + beta (Rm – Rf)

2

a) Required rate of return with IRRs from the Boeing 7E7

In order to find out required rate of return, they need to analyse company’s financial

position which is based on market estimation of the next coming year. As, it has been found that

Boeing business is preparing for almost 2000 to 3000 planes of the 7E7 types within next 20

years (Frieden, 2015). For they are expected to attain appropriate rate of return so that they can

meet out their required data. For this purpose,

Rate of return is calculated by using this particular formula:

re= Rf+ β[E(Rm) – Rf]

b) Critical evaluation of CAPM model that does not directly estimate cost of capital

CAPM is a model which is used for the purpose of pricing an individual security or

portfolio. It can be identified that current financial market price securities and thereby estimate

about expected returns on total capital investments. This model provides a method for

determining risk and translate the same into an estimate of expected return on equity. The major

advantage of using CAPM is the nature of estimated costs of equity that the model can generate.

The reason is not taken into consideration in estimating cost of capital which is quite simple. The

information provided by company is based on unit’s components for 20 years. Boeing estimates

that in the initial 20 years, they sell 2000-3000 units. As, analysts predicted that it would be

2500 units in 1st year till 20. After evaluating all these information, it can provide weight-age

value not cost of capital. This is the main reason it is not used during cost of capital estimation.

In the mentioned case, WACC is used for total cost estimation because of the values provided by

company are in weighted form. Boeing consists of two different segments, relatively more stable

defence concern and conversely more volatile commercial businesses.

c) Use of CAPM to calculate cost of equity

According to CAPM, the 7E7 project is a more risky project of current scenario. With

beta of 2.54 which is higher than stock market average company (Capital Asset Pricing Model,

2017). Volatility is expectable in this investment. The 7E7 project would be required to provide

return of 22.7009% in order to maintain sound investment. Cost can be derived from using

appropriate the following formula:

Cost of equity: Rf + beta (Rm – Rf)

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

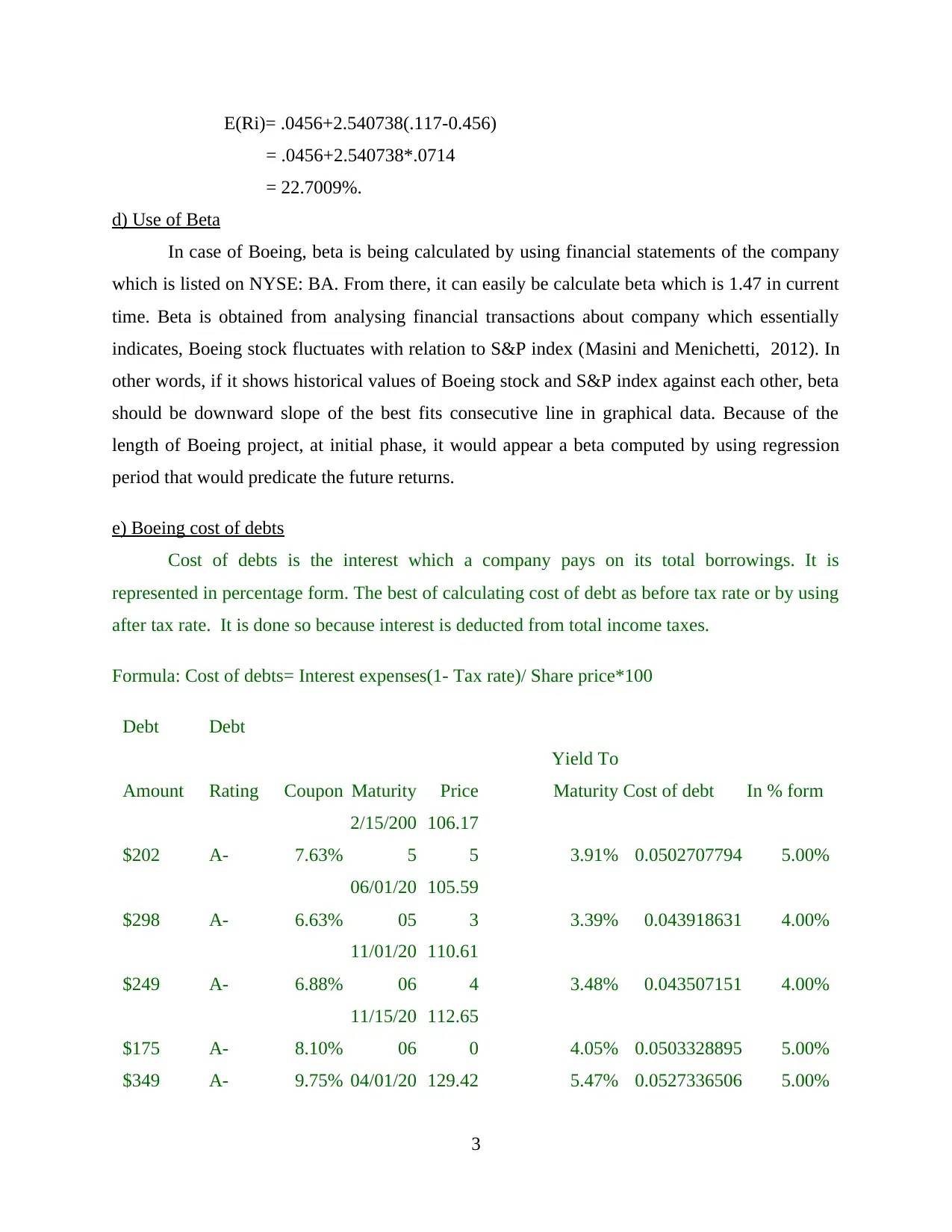

E(Ri)= .0456+2.540738(.117-0.456)

= .0456+2.540738*.0714

= 22.7009%.

d) Use of Beta

In case of Boeing, beta is being calculated by using financial statements of the company

which is listed on NYSE: BA. From there, it can easily be calculate beta which is 1.47 in current

time. Beta is obtained from analysing financial transactions about company which essentially

indicates, Boeing stock fluctuates with relation to S&P index (Masini and Menichetti, 2012). In

other words, if it shows historical values of Boeing stock and S&P index against each other, beta

should be downward slope of the best fits consecutive line in graphical data. Because of the

length of Boeing project, at initial phase, it would appear a beta computed by using regression

period that would predicate the future returns.

e) Boeing cost of debts

Cost of debts is the interest which a company pays on its total borrowings. It is

represented in percentage form. The best of calculating cost of debt as before tax rate or by using

after tax rate. It is done so because interest is deducted from total income taxes.

Formula: Cost of debts= Interest expenses(1- Tax rate)/ Share price*100

Debt Debt

Amount Rating Coupon Maturity Price

Yield To

Maturity Cost of debt In % form

$202 A- 7.63%

2/15/200

5

106.17

5 3.91% 0.0502707794 5.00%

$298 A- 6.63%

06/01/20

05

105.59

3 3.39% 0.043918631 4.00%

$249 A- 6.88%

11/01/20

06

110.61

4 3.48% 0.043507151 4.00%

$175 A- 8.10%

11/15/20

06

112.65

0 4.05% 0.0503328895 5.00%

$349 A- 9.75% 04/01/20 129.42 5.47% 0.0527336506 5.00%

3

= .0456+2.540738*.0714

= 22.7009%.

d) Use of Beta

In case of Boeing, beta is being calculated by using financial statements of the company

which is listed on NYSE: BA. From there, it can easily be calculate beta which is 1.47 in current

time. Beta is obtained from analysing financial transactions about company which essentially

indicates, Boeing stock fluctuates with relation to S&P index (Masini and Menichetti, 2012). In

other words, if it shows historical values of Boeing stock and S&P index against each other, beta

should be downward slope of the best fits consecutive line in graphical data. Because of the

length of Boeing project, at initial phase, it would appear a beta computed by using regression

period that would predicate the future returns.

e) Boeing cost of debts

Cost of debts is the interest which a company pays on its total borrowings. It is

represented in percentage form. The best of calculating cost of debt as before tax rate or by using

after tax rate. It is done so because interest is deducted from total income taxes.

Formula: Cost of debts= Interest expenses(1- Tax rate)/ Share price*100

Debt Debt

Amount Rating Coupon Maturity Price

Yield To

Maturity Cost of debt In % form

$202 A- 7.63%

2/15/200

5

106.17

5 3.91% 0.0502707794 5.00%

$298 A- 6.63%

06/01/20

05

105.59

3 3.39% 0.043918631 4.00%

$249 A- 6.88%

11/01/20

06

110.61

4 3.48% 0.043507151 4.00%

$175 A- 8.10%

11/15/20

06

112.65

0 4.05% 0.0503328895 5.00%

$349 A- 9.75% 04/01/20 129.42 5.47% 0.0527336506 5.00%

3

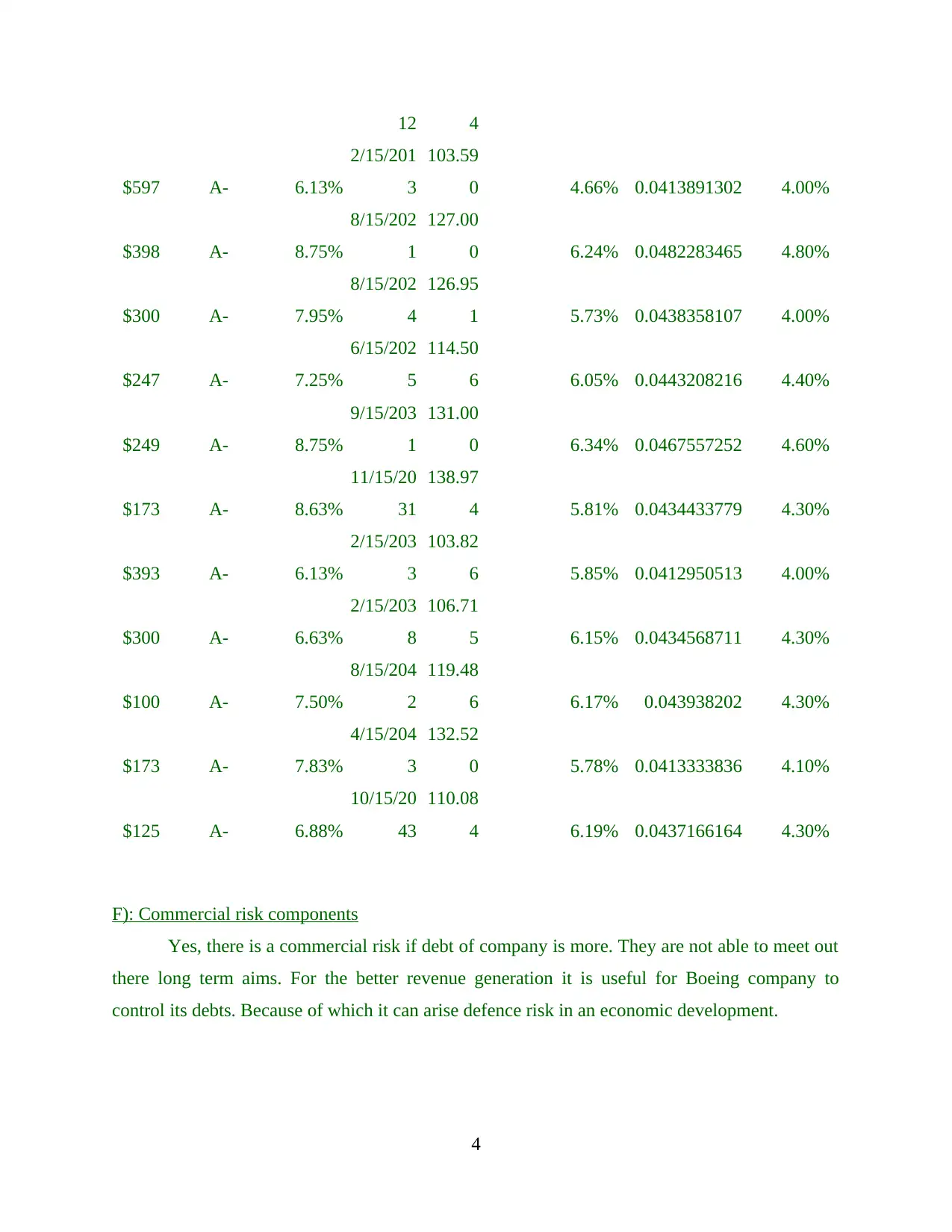

12 4

$597 A- 6.13%

2/15/201

3

103.59

0 4.66% 0.0413891302 4.00%

$398 A- 8.75%

8/15/202

1

127.00

0 6.24% 0.0482283465 4.80%

$300 A- 7.95%

8/15/202

4

126.95

1 5.73% 0.0438358107 4.00%

$247 A- 7.25%

6/15/202

5

114.50

6 6.05% 0.0443208216 4.40%

$249 A- 8.75%

9/15/203

1

131.00

0 6.34% 0.0467557252 4.60%

$173 A- 8.63%

11/15/20

31

138.97

4 5.81% 0.0434433779 4.30%

$393 A- 6.13%

2/15/203

3

103.82

6 5.85% 0.0412950513 4.00%

$300 A- 6.63%

2/15/203

8

106.71

5 6.15% 0.0434568711 4.30%

$100 A- 7.50%

8/15/204

2

119.48

6 6.17% 0.043938202 4.30%

$173 A- 7.83%

4/15/204

3

132.52

0 5.78% 0.0413333836 4.10%

$125 A- 6.88%

10/15/20

43

110.08

4 6.19% 0.0437166164 4.30%

F): Commercial risk components

Yes, there is a commercial risk if debt of company is more. They are not able to meet out

there long term aims. For the better revenue generation it is useful for Boeing company to

control its debts. Because of which it can arise defence risk in an economic development.

4

$597 A- 6.13%

2/15/201

3

103.59

0 4.66% 0.0413891302 4.00%

$398 A- 8.75%

8/15/202

1

127.00

0 6.24% 0.0482283465 4.80%

$300 A- 7.95%

8/15/202

4

126.95

1 5.73% 0.0438358107 4.00%

$247 A- 7.25%

6/15/202

5

114.50

6 6.05% 0.0443208216 4.40%

$249 A- 8.75%

9/15/203

1

131.00

0 6.34% 0.0467557252 4.60%

$173 A- 8.63%

11/15/20

31

138.97

4 5.81% 0.0434433779 4.30%

$393 A- 6.13%

2/15/203

3

103.82

6 5.85% 0.0412950513 4.00%

$300 A- 6.63%

2/15/203

8

106.71

5 6.15% 0.0434568711 4.30%

$100 A- 7.50%

8/15/204

2

119.48

6 6.17% 0.043938202 4.30%

$173 A- 7.83%

4/15/204

3

132.52

0 5.78% 0.0413333836 4.10%

$125 A- 6.88%

10/15/20

43

110.08

4 6.19% 0.0437166164 4.30%

F): Commercial risk components

Yes, there is a commercial risk if debt of company is more. They are not able to meet out

there long term aims. For the better revenue generation it is useful for Boeing company to

control its debts. Because of which it can arise defence risk in an economic development.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

g): Discuss not simple use of CAPM to estimate cost of debt

CAPM is tool which is used for calculating cost of equity not debt of the company which

are carried by an organisation. If they want to determine exact debts then WACC methods can be

more useful in evaluating more correct solution for cost of debt. These are based on market

capitalisation rate and systematic risk associated with it.

H): Calculate a weighted average of debt

The WACC is the rate through which a company is estimated to pay on an average to all

its securities to finance its assets.

Formula= WACC: Total cost of debt / no of observation*100

70.10

% Total cost of debt

0.04 4.30%

I): Capital structure weight

It a company finance which is based on overall operations and growth through using

various sources of capital. Debts comes in the way of issuing bond and long term payable.

While, equity is divided into common stock or retained earning.

QUESTION 3

a) Judgement against WACC

Weighted average cost of capital is the rate that a company is projected to pay on average

to all its security holders to finance its assets. WACC is more similarly related to as of firm's

total cost of capital. Every source of capital consists of common stock, preferred stock, bonds

and any other long term debts. In order to calculate company's it can be used under the

mentioned formula:

WACC = Wd rd (1- t) + We* r e

Where:

Wd = Proportion of debt in a market - value capital structure

rd = Pre-tax cost of debt capital

t = Marginal effective corporate tax rate

We = Proportion of equity in a market - value capital structure

re = Cost of equity capital

5

CAPM is tool which is used for calculating cost of equity not debt of the company which

are carried by an organisation. If they want to determine exact debts then WACC methods can be

more useful in evaluating more correct solution for cost of debt. These are based on market

capitalisation rate and systematic risk associated with it.

H): Calculate a weighted average of debt

The WACC is the rate through which a company is estimated to pay on an average to all

its securities to finance its assets.

Formula= WACC: Total cost of debt / no of observation*100

70.10

% Total cost of debt

0.04 4.30%

I): Capital structure weight

It a company finance which is based on overall operations and growth through using

various sources of capital. Debts comes in the way of issuing bond and long term payable.

While, equity is divided into common stock or retained earning.

QUESTION 3

a) Judgement against WACC

Weighted average cost of capital is the rate that a company is projected to pay on average

to all its security holders to finance its assets. WACC is more similarly related to as of firm's

total cost of capital. Every source of capital consists of common stock, preferred stock, bonds

and any other long term debts. In order to calculate company's it can be used under the

mentioned formula:

WACC = Wd rd (1- t) + We* r e

Where:

Wd = Proportion of debt in a market - value capital structure

rd = Pre-tax cost of debt capital

t = Marginal effective corporate tax rate

We = Proportion of equity in a market - value capital structure

re = Cost of equity capital

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

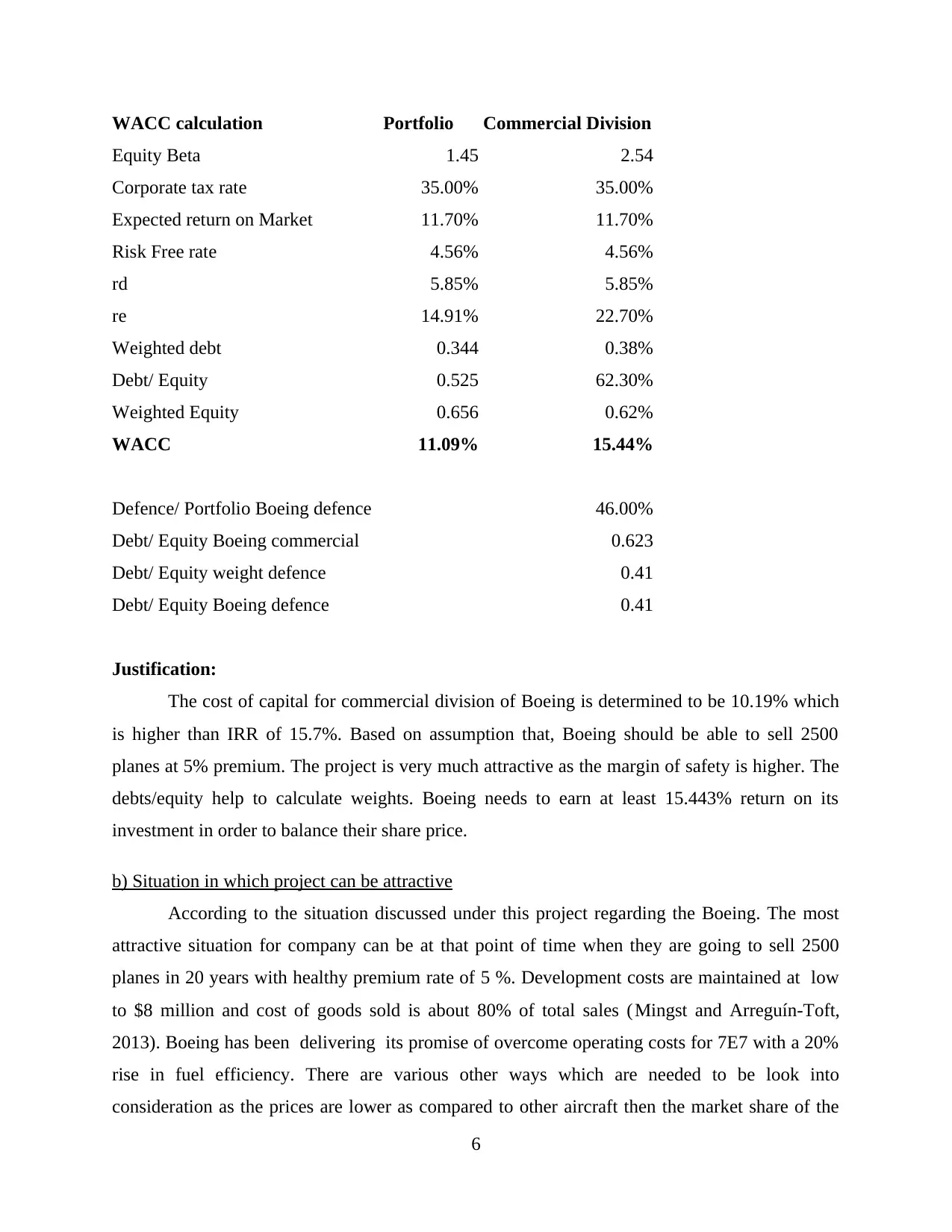

WACC calculation Portfolio Commercial Division

Equity Beta 1.45 2.54

Corporate tax rate 35.00% 35.00%

Expected return on Market 11.70% 11.70%

Risk Free rate 4.56% 4.56%

rd 5.85% 5.85%

re 14.91% 22.70%

Weighted debt 0.344 0.38%

Debt/ Equity 0.525 62.30%

Weighted Equity 0.656 0.62%

WACC 11.09% 15.44%

Defence/ Portfolio Boeing defence 46.00%

Debt/ Equity Boeing commercial 0.623

Debt/ Equity weight defence 0.41

Debt/ Equity Boeing defence 0.41

Justification:

The cost of capital for commercial division of Boeing is determined to be 10.19% which

is higher than IRR of 15.7%. Based on assumption that, Boeing should be able to sell 2500

planes at 5% premium. The project is very much attractive as the margin of safety is higher. The

debts/equity help to calculate weights. Boeing needs to earn at least 15.443% return on its

investment in order to balance their share price.

b) Situation in which project can be attractive

According to the situation discussed under this project regarding the Boeing. The most

attractive situation for company can be at that point of time when they are going to sell 2500

planes in 20 years with healthy premium rate of 5 %. Development costs are maintained at low

to $8 million and cost of goods sold is about 80% of total sales (Mingst and Arreguín-Toft,

2013). Boeing has been delivering its promise of overcome operating costs for 7E7 with a 20%

rise in fuel efficiency. There are various other ways which are needed to be look into

consideration as the prices are lower as compared to other aircraft then the market share of the

6

Equity Beta 1.45 2.54

Corporate tax rate 35.00% 35.00%

Expected return on Market 11.70% 11.70%

Risk Free rate 4.56% 4.56%

rd 5.85% 5.85%

re 14.91% 22.70%

Weighted debt 0.344 0.38%

Debt/ Equity 0.525 62.30%

Weighted Equity 0.656 0.62%

WACC 11.09% 15.44%

Defence/ Portfolio Boeing defence 46.00%

Debt/ Equity Boeing commercial 0.623

Debt/ Equity weight defence 0.41

Debt/ Equity Boeing defence 0.41

Justification:

The cost of capital for commercial division of Boeing is determined to be 10.19% which

is higher than IRR of 15.7%. Based on assumption that, Boeing should be able to sell 2500

planes at 5% premium. The project is very much attractive as the margin of safety is higher. The

debts/equity help to calculate weights. Boeing needs to earn at least 15.443% return on its

investment in order to balance their share price.

b) Situation in which project can be attractive

According to the situation discussed under this project regarding the Boeing. The most

attractive situation for company can be at that point of time when they are going to sell 2500

planes in 20 years with healthy premium rate of 5 %. Development costs are maintained at low

to $8 million and cost of goods sold is about 80% of total sales (Mingst and Arreguín-Toft,

2013). Boeing has been delivering its promise of overcome operating costs for 7E7 with a 20%

rise in fuel efficiency. There are various other ways which are needed to be look into

consideration as the prices are lower as compared to other aircraft then the market share of the

6

company will automatically be rise. The main chance of getting maximum advantages is when,

Boeing could sell more than enough planes in an allotted period of time above a certain period of

time. The interest rate of return provides project a net present value of zero which is about 15.4%

as per the evaluation. It will help to increase the wealth of shareholders that is invested in this

project.

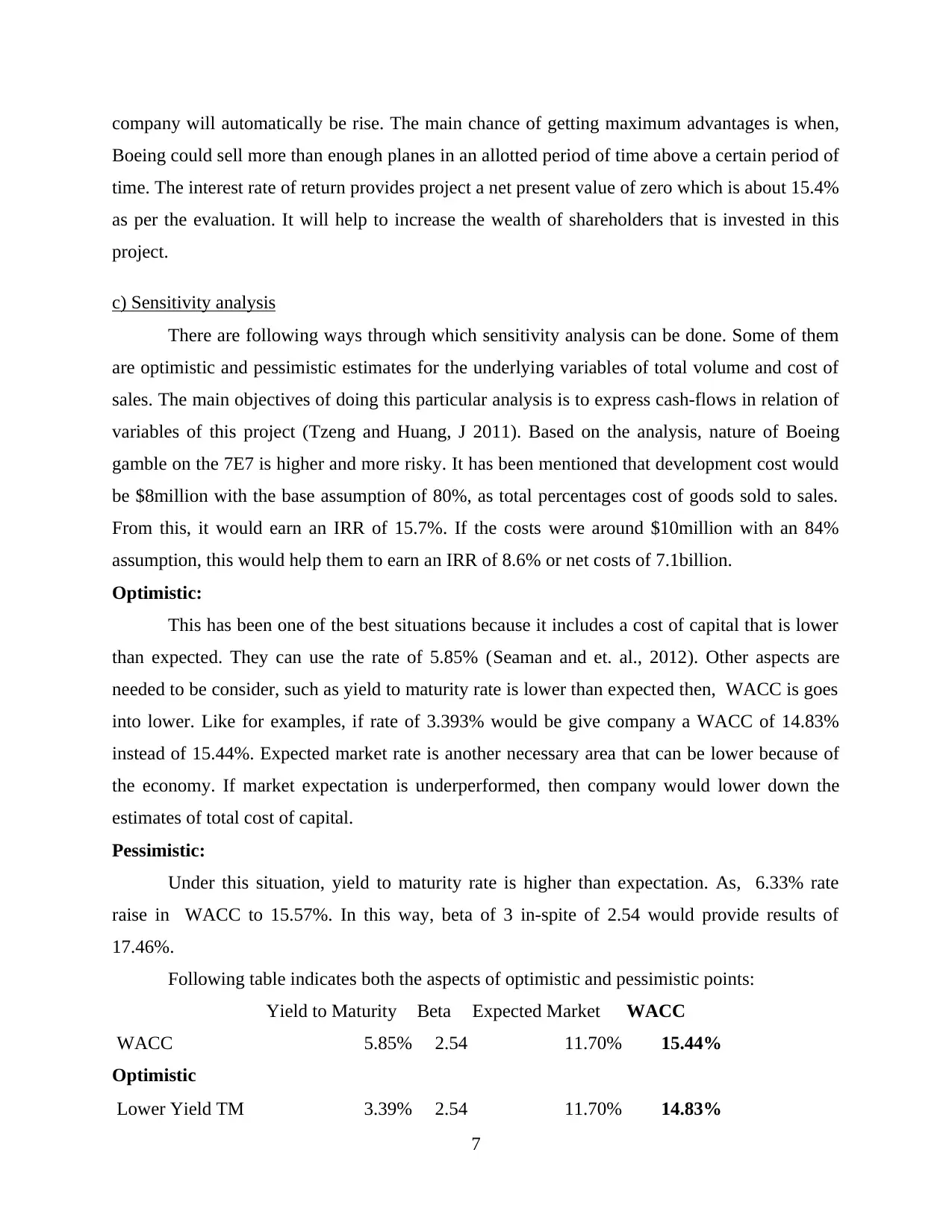

c) Sensitivity analysis

There are following ways through which sensitivity analysis can be done. Some of them

are optimistic and pessimistic estimates for the underlying variables of total volume and cost of

sales. The main objectives of doing this particular analysis is to express cash-flows in relation of

variables of this project (Tzeng and Huang, J 2011). Based on the analysis, nature of Boeing

gamble on the 7E7 is higher and more risky. It has been mentioned that development cost would

be $8million with the base assumption of 80%, as total percentages cost of goods sold to sales.

From this, it would earn an IRR of 15.7%. If the costs were around $10million with an 84%

assumption, this would help them to earn an IRR of 8.6% or net costs of 7.1billion.

Optimistic:

This has been one of the best situations because it includes a cost of capital that is lower

than expected. They can use the rate of 5.85% (Seaman and et. al., 2012). Other aspects are

needed to be consider, such as yield to maturity rate is lower than expected then, WACC is goes

into lower. Like for examples, if rate of 3.393% would be give company a WACC of 14.83%

instead of 15.44%. Expected market rate is another necessary area that can be lower because of

the economy. If market expectation is underperformed, then company would lower down the

estimates of total cost of capital.

Pessimistic:

Under this situation, yield to maturity rate is higher than expectation. As, 6.33% rate

raise in WACC to 15.57%. In this way, beta of 3 in-spite of 2.54 would provide results of

17.46%.

Following table indicates both the aspects of optimistic and pessimistic points:

Yield to Maturity Beta Expected Market WACC

WACC 5.85% 2.54 11.70% 15.44%

Optimistic

Lower Yield TM 3.39% 2.54 11.70% 14.83%

7

Boeing could sell more than enough planes in an allotted period of time above a certain period of

time. The interest rate of return provides project a net present value of zero which is about 15.4%

as per the evaluation. It will help to increase the wealth of shareholders that is invested in this

project.

c) Sensitivity analysis

There are following ways through which sensitivity analysis can be done. Some of them

are optimistic and pessimistic estimates for the underlying variables of total volume and cost of

sales. The main objectives of doing this particular analysis is to express cash-flows in relation of

variables of this project (Tzeng and Huang, J 2011). Based on the analysis, nature of Boeing

gamble on the 7E7 is higher and more risky. It has been mentioned that development cost would

be $8million with the base assumption of 80%, as total percentages cost of goods sold to sales.

From this, it would earn an IRR of 15.7%. If the costs were around $10million with an 84%

assumption, this would help them to earn an IRR of 8.6% or net costs of 7.1billion.

Optimistic:

This has been one of the best situations because it includes a cost of capital that is lower

than expected. They can use the rate of 5.85% (Seaman and et. al., 2012). Other aspects are

needed to be consider, such as yield to maturity rate is lower than expected then, WACC is goes

into lower. Like for examples, if rate of 3.393% would be give company a WACC of 14.83%

instead of 15.44%. Expected market rate is another necessary area that can be lower because of

the economy. If market expectation is underperformed, then company would lower down the

estimates of total cost of capital.

Pessimistic:

Under this situation, yield to maturity rate is higher than expectation. As, 6.33% rate

raise in WACC to 15.57%. In this way, beta of 3 in-spite of 2.54 would provide results of

17.46%.

Following table indicates both the aspects of optimistic and pessimistic points:

Yield to Maturity Beta Expected Market WACC

WACC 5.85% 2.54 11.70% 15.44%

Optimistic

Lower Yield TM 3.39% 2.54 11.70% 14.83%

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

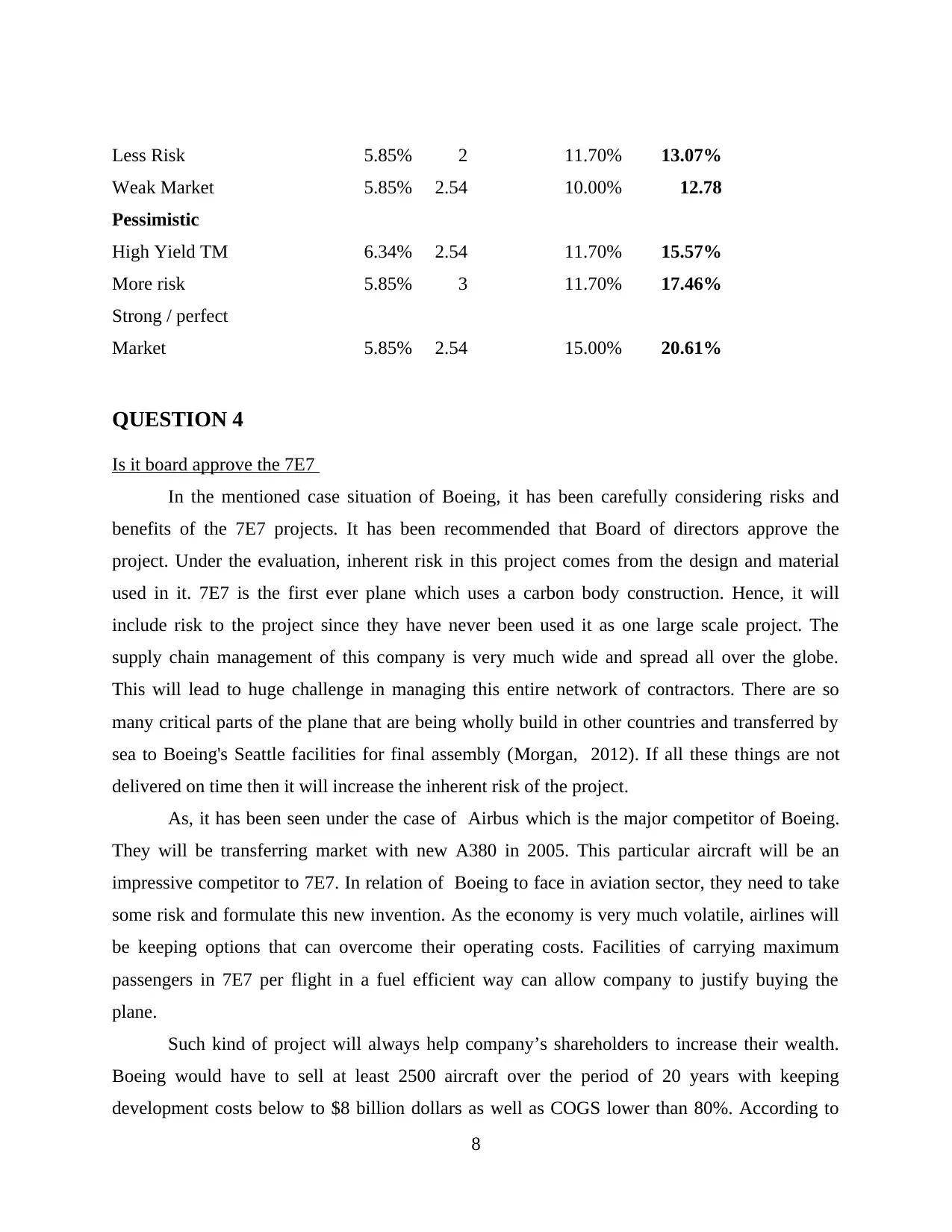

Less Risk 5.85% 2 11.70% 13.07%

Weak Market 5.85% 2.54 10.00% 12.78

Pessimistic

High Yield TM 6.34% 2.54 11.70% 15.57%

More risk 5.85% 3 11.70% 17.46%

Strong / perfect

Market 5.85% 2.54 15.00% 20.61%

QUESTION 4

Is it board approve the 7E7

In the mentioned case situation of Boeing, it has been carefully considering risks and

benefits of the 7E7 projects. It has been recommended that Board of directors approve the

project. Under the evaluation, inherent risk in this project comes from the design and material

used in it. 7E7 is the first ever plane which uses a carbon body construction. Hence, it will

include risk to the project since they have never been used it as one large scale project. The

supply chain management of this company is very much wide and spread all over the globe.

This will lead to huge challenge in managing this entire network of contractors. There are so

many critical parts of the plane that are being wholly build in other countries and transferred by

sea to Boeing's Seattle facilities for final assembly (Morgan, 2012). If all these things are not

delivered on time then it will increase the inherent risk of the project.

As, it has been seen under the case of Airbus which is the major competitor of Boeing.

They will be transferring market with new A380 in 2005. This particular aircraft will be an

impressive competitor to 7E7. In relation of Boeing to face in aviation sector, they need to take

some risk and formulate this new invention. As the economy is very much volatile, airlines will

be keeping options that can overcome their operating costs. Facilities of carrying maximum

passengers in 7E7 per flight in a fuel efficient way can allow company to justify buying the

plane.

Such kind of project will always help company’s shareholders to increase their wealth.

Boeing would have to sell at least 2500 aircraft over the period of 20 years with keeping

development costs below to $8 billion dollars as well as COGS lower than 80%. According to

8

Weak Market 5.85% 2.54 10.00% 12.78

Pessimistic

High Yield TM 6.34% 2.54 11.70% 15.57%

More risk 5.85% 3 11.70% 17.46%

Strong / perfect

Market 5.85% 2.54 15.00% 20.61%

QUESTION 4

Is it board approve the 7E7

In the mentioned case situation of Boeing, it has been carefully considering risks and

benefits of the 7E7 projects. It has been recommended that Board of directors approve the

project. Under the evaluation, inherent risk in this project comes from the design and material

used in it. 7E7 is the first ever plane which uses a carbon body construction. Hence, it will

include risk to the project since they have never been used it as one large scale project. The

supply chain management of this company is very much wide and spread all over the globe.

This will lead to huge challenge in managing this entire network of contractors. There are so

many critical parts of the plane that are being wholly build in other countries and transferred by

sea to Boeing's Seattle facilities for final assembly (Morgan, 2012). If all these things are not

delivered on time then it will increase the inherent risk of the project.

As, it has been seen under the case of Airbus which is the major competitor of Boeing.

They will be transferring market with new A380 in 2005. This particular aircraft will be an

impressive competitor to 7E7. In relation of Boeing to face in aviation sector, they need to take

some risk and formulate this new invention. As the economy is very much volatile, airlines will

be keeping options that can overcome their operating costs. Facilities of carrying maximum

passengers in 7E7 per flight in a fuel efficient way can allow company to justify buying the

plane.

Such kind of project will always help company’s shareholders to increase their wealth.

Boeing would have to sell at least 2500 aircraft over the period of 20 years with keeping

development costs below to $8 billion dollars as well as COGS lower than 80%. According to

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the equity market risk premium, it should be equal to the total return expected by investors on the

particular market portfolio (Brealey and et. al., 2012). The WACC is calculated as 15.44%. In

order to increase shareholder’s value, the IRR must be equal to WACC. In order to reach at that

level, they need to sell around 2500 airlines in time period of 20 years. The overall financial

evaluation incurred in this report indicates that there is a positive chance of increasing

shareholder’s wealth. There are some other risks which are included in above that should be

taken into consideration. But on balance the reasons to move forward with the project exceed

those against it.

CONCLUSION

From the above report, it has been concluded that international finance is an important

aspect of any business organisation. It helps in taking necessary decisions regarding future

growth and sustainability of firm. Under this project, financial analysis of Boeing 7E7 project is

discussed in effective manner to entered into the market. Various financial tools is been used for

the purpose of analysing company performance which is more beneficial for them to increase its

productivity. Cost of capital, CAPM model and WACC is been explained clearly under this

project. The complete project is prepared and put in front of board of director for the future

approval.

9

particular market portfolio (Brealey and et. al., 2012). The WACC is calculated as 15.44%. In

order to increase shareholder’s value, the IRR must be equal to WACC. In order to reach at that

level, they need to sell around 2500 airlines in time period of 20 years. The overall financial

evaluation incurred in this report indicates that there is a positive chance of increasing

shareholder’s wealth. There are some other risks which are included in above that should be

taken into consideration. But on balance the reasons to move forward with the project exceed

those against it.

CONCLUSION

From the above report, it has been concluded that international finance is an important

aspect of any business organisation. It helps in taking necessary decisions regarding future

growth and sustainability of firm. Under this project, financial analysis of Boeing 7E7 project is

discussed in effective manner to entered into the market. Various financial tools is been used for

the purpose of analysing company performance which is more beneficial for them to increase its

productivity. Cost of capital, CAPM model and WACC is been explained clearly under this

project. The complete project is prepared and put in front of board of director for the future

approval.

9

REFERENCES

Books and Journals

Bayne, N. and Woolcock, S. eds., 2011. The new economic diplomacy: decision-making and

negotiation in international economic relations. Ashgate Publishing, Ltd..

Brealey, R. A and et. al., 2012. Principles of corporate finance. Tata McGraw-Hill Education.

Frieden, J., 2015. Banking on the world: the politics of American international finance.

Routledge.

Masini, A. and Menichetti, E., 2012. The impact of behavioural factors in the renewable energy

investment decision making process: Conceptual framework and empirical findings.

Energy Policy. 40. pp.28-38.

Mingst, K. A. and Arreguín-Toft, I. M., 2013. Essentials of International Relations: Sixth

International Student Edition. WW Norton & Company.

Morgan, R. K., 2012. Environmental impact assessment: the state of the art. Impact Assessment

and Project Appraisal. 30(1). pp.5-14.

Seaman, C and et. al., 2012, June. Using technical debt data in decision making: Potential

decision approaches. In Proceedings of the Third International Workshop on Managing

Technical Debt (pp. 45-48). IEEE Press.

Tzeng, G. H. and Huang, J. J., 2011. Multiple attribute decision making: methods and

applications. CRC press.

Online

Capital Asset Pricing Model. 2017. [Online]. Available through:

<http://www.investinganswers.com/financial-dictionary/stock-valuation/capital-asset-

pricing-model-capm-1125>.

10

Books and Journals

Bayne, N. and Woolcock, S. eds., 2011. The new economic diplomacy: decision-making and

negotiation in international economic relations. Ashgate Publishing, Ltd..

Brealey, R. A and et. al., 2012. Principles of corporate finance. Tata McGraw-Hill Education.

Frieden, J., 2015. Banking on the world: the politics of American international finance.

Routledge.

Masini, A. and Menichetti, E., 2012. The impact of behavioural factors in the renewable energy

investment decision making process: Conceptual framework and empirical findings.

Energy Policy. 40. pp.28-38.

Mingst, K. A. and Arreguín-Toft, I. M., 2013. Essentials of International Relations: Sixth

International Student Edition. WW Norton & Company.

Morgan, R. K., 2012. Environmental impact assessment: the state of the art. Impact Assessment

and Project Appraisal. 30(1). pp.5-14.

Seaman, C and et. al., 2012, June. Using technical debt data in decision making: Potential

decision approaches. In Proceedings of the Third International Workshop on Managing

Technical Debt (pp. 45-48). IEEE Press.

Tzeng, G. H. and Huang, J. J., 2011. Multiple attribute decision making: methods and

applications. CRC press.

Online

Capital Asset Pricing Model. 2017. [Online]. Available through:

<http://www.investinganswers.com/financial-dictionary/stock-valuation/capital-asset-

pricing-model-capm-1125>.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.