Financial Analysis of Boeing 7E7 Project: A Comprehensive Report

VerifiedAdded on 2020/09/08

|13

|3396

|142

Report

AI Summary

This report provides a comprehensive financial analysis of Boeing's 7E7 project, examining various aspects of financial decision-making. The analysis begins with the rationale behind the project's launch, considering factors such as market competition and technological advancements. It then delves into determining the appropriate rate of return using WACC, exploring the cost of capital without CAPM, and applying CAPM to analyze the cost of equity, considering risk-free rates and beta. The report also assesses the cost of debt, the relationship between debt and commercial/defense risks, and the application of CAPM in determining debt costs. Furthermore, it evaluates the project's attractiveness using metrics like ARR, NPV, and payback period, including sensitivity analysis. The report concludes with a discussion on the project's value and its implications for Boeing's financial strategies, offering recommendations for effective financial execution and competition with rivals like Airbus.

International financial &

decision making

decision making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Reasons fort Boeing contemplating for launch of 7E7 project..............................................1

QUESTION 2...................................................................................................................................1

A. Determining the appropriate rate of return for the prospective IRR from Boeing 7E7

project.....................................................................................................................................1

B. To determine the cost of capital without using capital assets pricing model....................2

C. Implicating the use of capital assets pricing model to analyse cost of equity with risk free

rate and beta rate.....................................................................................................................2

D. Application of Capital assets pricing model on risk free rate and risk- premium.............3

E. Analysing the cost of debt for Boeing...............................................................................3

F. Relationship of debt with commercial and defence risk....................................................3

G. Analysing the use of CAPM in terms of determining the cost of debts............................4

H. To analyse the length of project the estimation belongs to weighted average debt and long

terms debts..............................................................................................................................4

I. Determine the capital structure weights to be use...............................................................4

QUESTION 3...................................................................................................................................5

A. Judgement relevant with WACC and the attractiveness of the project Boeing 7E7.........5

B. Economically attractiveness of the project under several conditions................................5

C. Sensitivity analysis in relation with the Boeing's gamble.................................................6

QUESTION 4...................................................................................................................................6

Valuable the project 7E7 for the board...................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDIX......................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Reasons fort Boeing contemplating for launch of 7E7 project..............................................1

QUESTION 2...................................................................................................................................1

A. Determining the appropriate rate of return for the prospective IRR from Boeing 7E7

project.....................................................................................................................................1

B. To determine the cost of capital without using capital assets pricing model....................2

C. Implicating the use of capital assets pricing model to analyse cost of equity with risk free

rate and beta rate.....................................................................................................................2

D. Application of Capital assets pricing model on risk free rate and risk- premium.............3

E. Analysing the cost of debt for Boeing...............................................................................3

F. Relationship of debt with commercial and defence risk....................................................3

G. Analysing the use of CAPM in terms of determining the cost of debts............................4

H. To analyse the length of project the estimation belongs to weighted average debt and long

terms debts..............................................................................................................................4

I. Determine the capital structure weights to be use...............................................................4

QUESTION 3...................................................................................................................................5

A. Judgement relevant with WACC and the attractiveness of the project Boeing 7E7.........5

B. Economically attractiveness of the project under several conditions................................5

C. Sensitivity analysis in relation with the Boeing's gamble.................................................6

QUESTION 4...................................................................................................................................6

Valuable the project 7E7 for the board...................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDIX......................................................................................................................................9

INTRODUCTION

Financial decision is the prime requirement of the business which will be fruitful for the

business in terms of making the adequate operational activities in the long run. In the present

report there has been discussion based on Boeing's 7E7 project. Therefore, this will be fruitful

for the manages in terms of having the adequate financial execution and the suggests relevant

with the cost of capital, debts and equity. The advices will be presented to the managers as to

make proper increment in the operations of business as well as the launch of these aircraft project

to compete with competitors like Airbus.

QUESTION 1

Reasons fort Boeing contemplating for launch of 7E7 project

In consideration with the increment in the competitors and technology there is need to

have an up gradation in the operations and designs of the aircraft. Boeing has planned to launch

the 7E7 project which will be consists of various new features and design. In respect to such

planning they decided to launch an aircraft with having two different configurations such as

reducing the cabin altitude as well as increasing the cabin's Humidity. On the other side, while

considering the increment in the terrorist activities there will be huge risks which are relevant

with the problems which are being faced by an aviation industry and need to have strong security

systems (Dutta and Nezlobin, 2017). Other than this, the main obstacle in the operations of the

business is presented by rivalries such as Airbus is giving the tough competition to Boeing.

Therefore, it can be said that this is not a time to have a launch of this project in spite of this,

they must make strong plans and have increment in the technology.

QUESTION 2

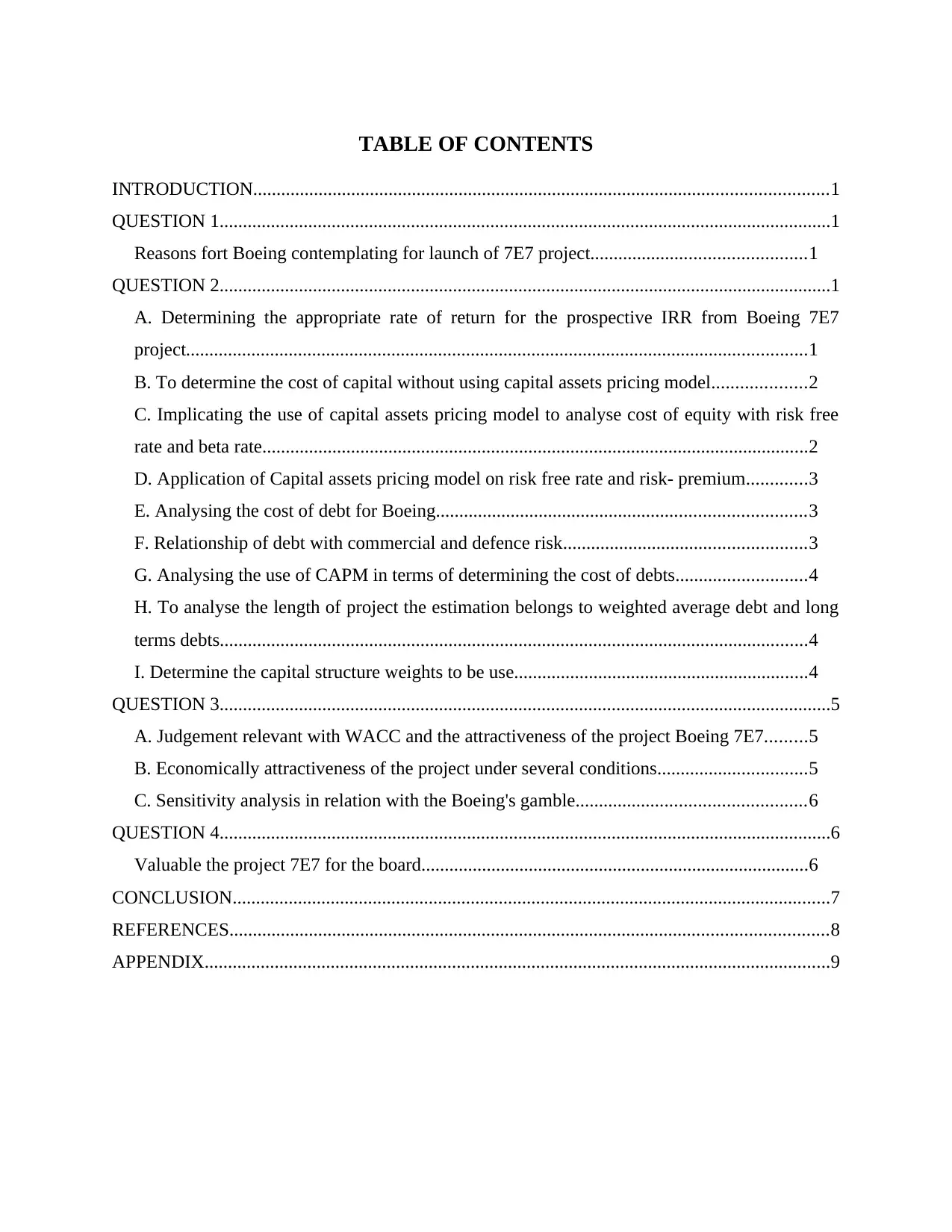

A. Determining the appropriate rate of return for the prospective IRR from Boeing 7E7 project

1

Financial decision is the prime requirement of the business which will be fruitful for the

business in terms of making the adequate operational activities in the long run. In the present

report there has been discussion based on Boeing's 7E7 project. Therefore, this will be fruitful

for the manages in terms of having the adequate financial execution and the suggests relevant

with the cost of capital, debts and equity. The advices will be presented to the managers as to

make proper increment in the operations of business as well as the launch of these aircraft project

to compete with competitors like Airbus.

QUESTION 1

Reasons fort Boeing contemplating for launch of 7E7 project

In consideration with the increment in the competitors and technology there is need to

have an up gradation in the operations and designs of the aircraft. Boeing has planned to launch

the 7E7 project which will be consists of various new features and design. In respect to such

planning they decided to launch an aircraft with having two different configurations such as

reducing the cabin altitude as well as increasing the cabin's Humidity. On the other side, while

considering the increment in the terrorist activities there will be huge risks which are relevant

with the problems which are being faced by an aviation industry and need to have strong security

systems (Dutta and Nezlobin, 2017). Other than this, the main obstacle in the operations of the

business is presented by rivalries such as Airbus is giving the tough competition to Boeing.

Therefore, it can be said that this is not a time to have a launch of this project in spite of this,

they must make strong plans and have increment in the technology.

QUESTION 2

A. Determining the appropriate rate of return for the prospective IRR from Boeing 7E7 project

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In order to analyse the adequate rate of return which is aimed at reducing the costs of

production, there has been measurement of WACC is presented. The current WACC is 2.76%

which is comparatively lower than the 3.39% of WACC which indicates that the Cost of capital

is adequate (Creedy and Gemmell, 2017). Therefore, it includes the measurements for the

elements such as debt amount for 4328, equity amount at 7696 etc. the rates of various taxes

were also been mentioned such as cost of debt before tax is 8%, cost of equity art 3% and the

corporate tax of 35%. Therefore, the weighted debts is for 36% and weighted equity is for 64%

were measured.

B. To determine the cost of capital without using capital assets pricing model

In consideration with determining the cost of capital there has been implementation or

influences of various components which are useful in measuring it. Therefore, in this project

there is not any use of such components so it will not be possible in terms of measuring the cost

of capital. There will not be implication of CAPM in terms of computing the cost of capital while

WACC will be useful as it includes the same elements such as Corporate tax cost of debts etc.

thus, it can be said that with using the CAPM this not possible to analyse the cost of capital

(Biørn, 2017).

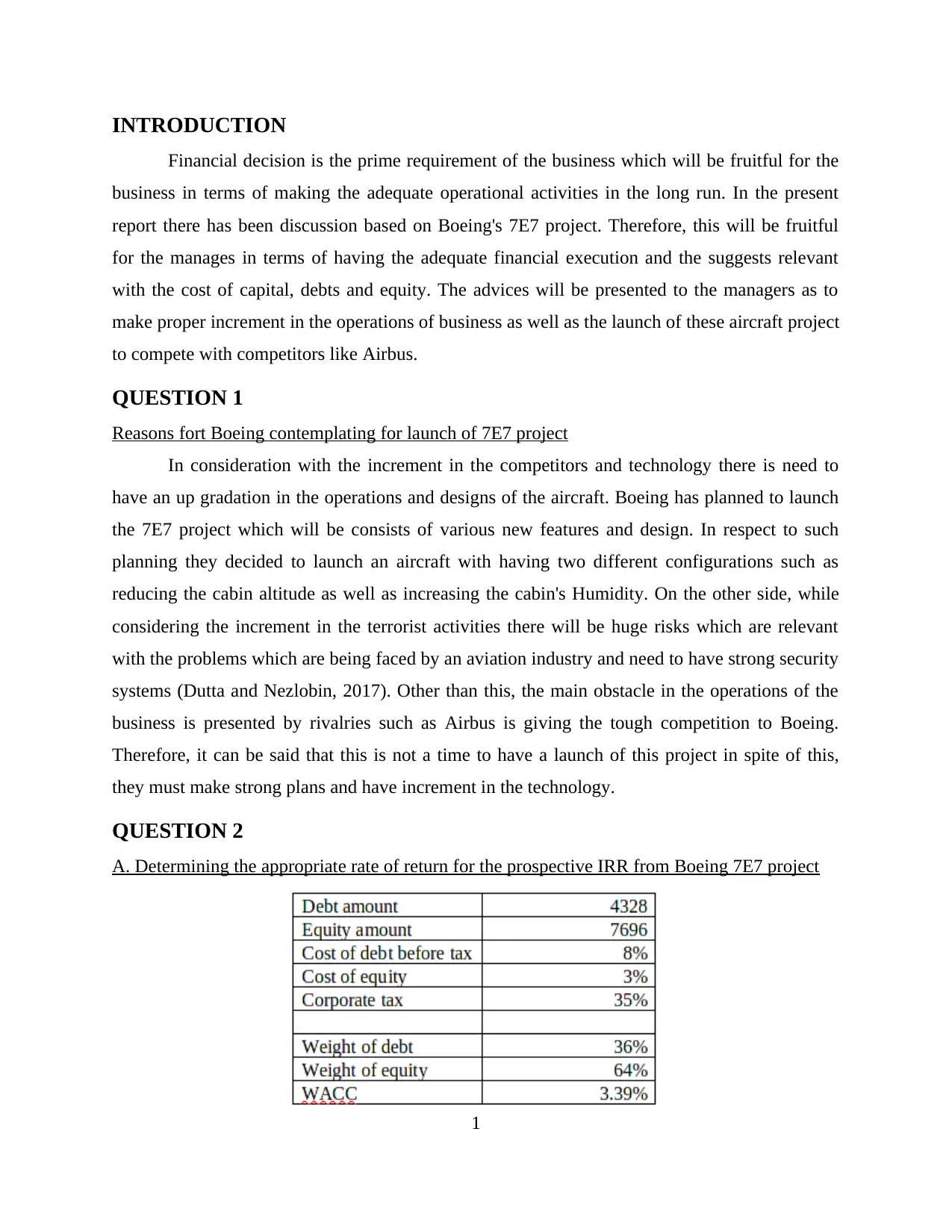

C. Implicating the use of capital assets pricing model to analyse cost of equity with risk free rate

and beta rate

Interpretation: In terms of identifying the cost of equity the capital asset pricing method

is the very useful method. Therefore, due to implications of this method the cost equity was

measured at 3% which is adequate and appropriate. Thus, it indicates that to launch this project

the firm will require less capital as well as they have the risk free rate for 0.85%. There has been

measurement for the beta on the basis of 60 days of share trading which are highly volatile in

nature so the 3-6 month of the period is to be considered while measuring it (Levi and Welch,

2017).

2

production, there has been measurement of WACC is presented. The current WACC is 2.76%

which is comparatively lower than the 3.39% of WACC which indicates that the Cost of capital

is adequate (Creedy and Gemmell, 2017). Therefore, it includes the measurements for the

elements such as debt amount for 4328, equity amount at 7696 etc. the rates of various taxes

were also been mentioned such as cost of debt before tax is 8%, cost of equity art 3% and the

corporate tax of 35%. Therefore, the weighted debts is for 36% and weighted equity is for 64%

were measured.

B. To determine the cost of capital without using capital assets pricing model

In consideration with determining the cost of capital there has been implementation or

influences of various components which are useful in measuring it. Therefore, in this project

there is not any use of such components so it will not be possible in terms of measuring the cost

of capital. There will not be implication of CAPM in terms of computing the cost of capital while

WACC will be useful as it includes the same elements such as Corporate tax cost of debts etc.

thus, it can be said that with using the CAPM this not possible to analyse the cost of capital

(Biørn, 2017).

C. Implicating the use of capital assets pricing model to analyse cost of equity with risk free rate

and beta rate

Interpretation: In terms of identifying the cost of equity the capital asset pricing method

is the very useful method. Therefore, due to implications of this method the cost equity was

measured at 3% which is adequate and appropriate. Thus, it indicates that to launch this project

the firm will require less capital as well as they have the risk free rate for 0.85%. There has been

measurement for the beta on the basis of 60 days of share trading which are highly volatile in

nature so the 3-6 month of the period is to be considered while measuring it (Levi and Welch,

2017).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D. Application of Capital assets pricing model on risk free rate and risk- premium

Risk free rate: This is the factor and a rate which an investor expected from the

investments he has made for specific time. Therefore, it will be known as the investment from

the zero risks and have the favourable returns in the coming time. Here, the 0.85% of the risk has

been estimated for the short term investment in the project which shows that there is no variation

between market return and the risk free rate (Olson and Pagano, 2017).

Risk Premium: This is the component which considers the risk free rate of return will be

considers to the risk premium. Therefore, it can be said that it is and profitable compensation for

the investors over the amount of capital they have invested in the project. Here, the risk premium

is 1.15% which is being computed as to deduct the market return for 2%. However, it is because

of the market environment is not healthy for the business as well as it will not facilitate the risk

free returns to the investors (López Prol and Steininger, 2017).

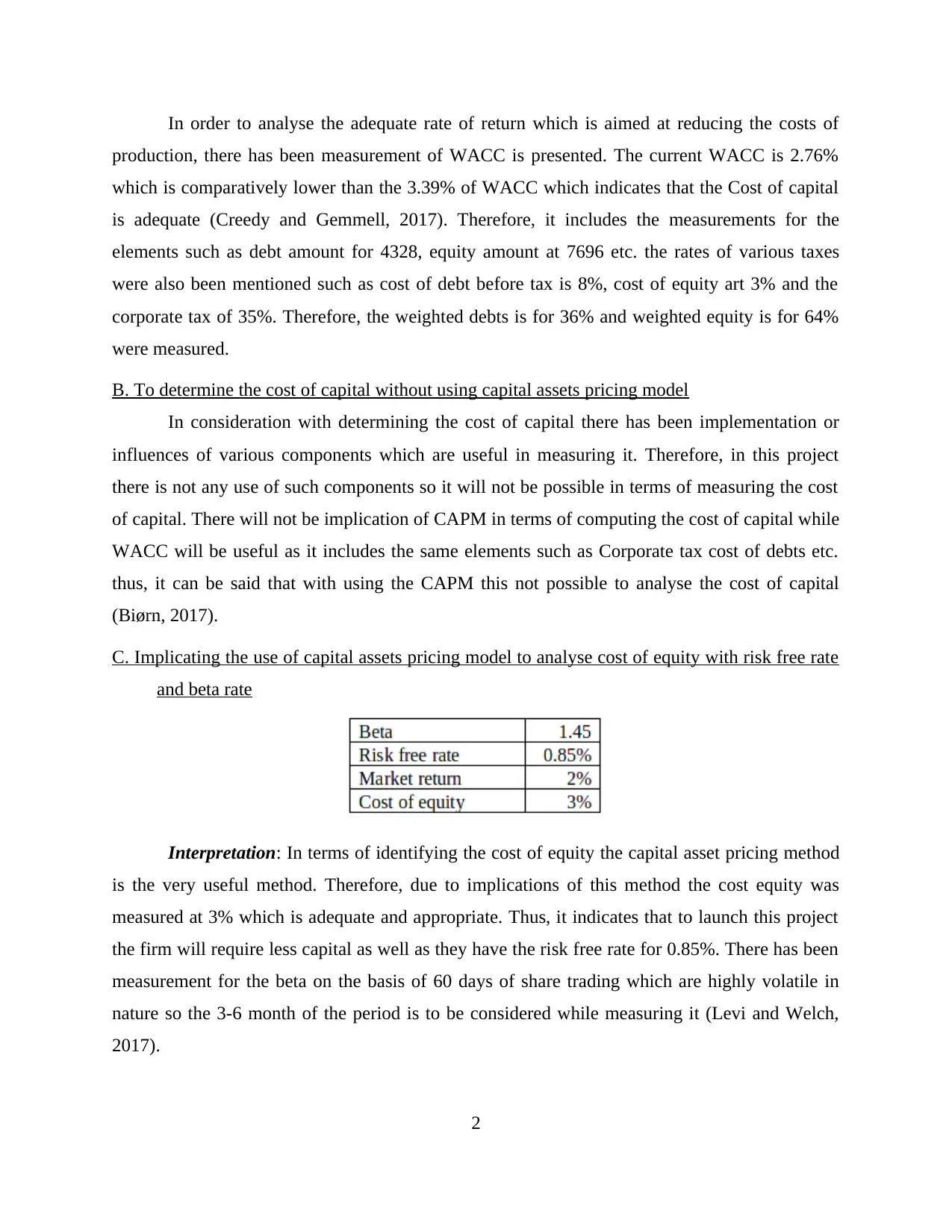

E. Analysing the cost of debt for Boeing

Interpretation: the aim behind measuring the cost of debt which helps in analysing the

rate of interest a firm will pay over its borrowings and withdraws. This is to be considers as per

the income taxes to be paid by firm so there is two outcomes were mentioned such as Cost of

debt after tax and before tax. The cost of debt before tax is 7.59% while deducting the corporate

tax for 35% the cost of debt after tax will be analysed as 5%. However, there has been use of

debts systematic approach which helps in presenting Boeing's cost of debt.

F. Relationship of debt with commercial and defence risk

In accordance with analysing the relationship between debts and commercial risk. There

has been a strong boding between them. The debts cannot be paid by a firm without considering

the commercial risks. Thus, it can be said that Boeing need to take necessary steps as well as

plan strategies to control the debts risk (Borello and et.al., 2017). Therefore, in this regard the

firm usually make exceeding payments to the shareholders or investors which will be helpful in

the long run as if the firm will have any financial crisis they will have enough amount of money

to make the adequate payments to their creditors. However, in accordance with having the long

3

Risk free rate: This is the factor and a rate which an investor expected from the

investments he has made for specific time. Therefore, it will be known as the investment from

the zero risks and have the favourable returns in the coming time. Here, the 0.85% of the risk has

been estimated for the short term investment in the project which shows that there is no variation

between market return and the risk free rate (Olson and Pagano, 2017).

Risk Premium: This is the component which considers the risk free rate of return will be

considers to the risk premium. Therefore, it can be said that it is and profitable compensation for

the investors over the amount of capital they have invested in the project. Here, the risk premium

is 1.15% which is being computed as to deduct the market return for 2%. However, it is because

of the market environment is not healthy for the business as well as it will not facilitate the risk

free returns to the investors (López Prol and Steininger, 2017).

E. Analysing the cost of debt for Boeing

Interpretation: the aim behind measuring the cost of debt which helps in analysing the

rate of interest a firm will pay over its borrowings and withdraws. This is to be considers as per

the income taxes to be paid by firm so there is two outcomes were mentioned such as Cost of

debt after tax and before tax. The cost of debt before tax is 7.59% while deducting the corporate

tax for 35% the cost of debt after tax will be analysed as 5%. However, there has been use of

debts systematic approach which helps in presenting Boeing's cost of debt.

F. Relationship of debt with commercial and defence risk

In accordance with analysing the relationship between debts and commercial risk. There

has been a strong boding between them. The debts cannot be paid by a firm without considering

the commercial risks. Thus, it can be said that Boeing need to take necessary steps as well as

plan strategies to control the debts risk (Borello and et.al., 2017). Therefore, in this regard the

firm usually make exceeding payments to the shareholders or investors which will be helpful in

the long run as if the firm will have any financial crisis they will have enough amount of money

to make the adequate payments to their creditors. However, in accordance with having the long

3

term benefits there is need to have the proper execution of the current business operations and

make strategic plan to control the debt risks. On the pother side, while considering the defence

risk which will be beneficial for the Boeing in terms of preventing the aircraft from terrorism.

G. Analysing the use of CAPM in terms of determining the cost of debts

To analyse the cost debts there will be use of CAPM method which will require the

returns over investments which must be as long as the systematic risk of the investment.

Therefore, it can be said that, to measure such component there is need to have implication of the

equity beta as to analyse the return over equity (Using CAPM to determine the cost of debt,

2012). Therefore, if the debt beta is not zero then capital assets pricing model will be used to

determine the cost of debt such as:

However, in this case there is no such components are available so it will not been

calculated for Boeing.

H. To analyse the length of project the estimation belongs to weighted average debt and long

terms debts

In order to meet the length of project there is need to have the proper analysis of WACC

which will be beneficial for the firm in having the adequate returns for the long period.

Therefore, while referring to the situation there are requirements to have acquiring a loan that

will be beneficial in terms of analysing the WACC. Thus, while measuring the cash flows of the

project there is only long term debts were considered by professionals which do not bring the

adequate return over the invested money (Sanusi and Dada, 2017). There is need to consider all

the short term as well as long terms investment that will be beneficial in terms of analysing the

adequate return to be obtained by firm at the period of maturity. However, it can be said that if

Boeing mention all the investments in to accounts than it will be fruitful for them to measure the

outcomes they will go to have the time of completion of project.

I. Determine the capital structure weights to be use

In the current situation of Boeing the capital structure is not balanced as they have the

debt for 36% while equity is of 64%. Therefore, it can be said that to balance these ratios there is

4

make strategic plan to control the debt risks. On the pother side, while considering the defence

risk which will be beneficial for the Boeing in terms of preventing the aircraft from terrorism.

G. Analysing the use of CAPM in terms of determining the cost of debts

To analyse the cost debts there will be use of CAPM method which will require the

returns over investments which must be as long as the systematic risk of the investment.

Therefore, it can be said that, to measure such component there is need to have implication of the

equity beta as to analyse the return over equity (Using CAPM to determine the cost of debt,

2012). Therefore, if the debt beta is not zero then capital assets pricing model will be used to

determine the cost of debt such as:

However, in this case there is no such components are available so it will not been

calculated for Boeing.

H. To analyse the length of project the estimation belongs to weighted average debt and long

terms debts

In order to meet the length of project there is need to have the proper analysis of WACC

which will be beneficial for the firm in having the adequate returns for the long period.

Therefore, while referring to the situation there are requirements to have acquiring a loan that

will be beneficial in terms of analysing the WACC. Thus, while measuring the cash flows of the

project there is only long term debts were considered by professionals which do not bring the

adequate return over the invested money (Sanusi and Dada, 2017). There is need to consider all

the short term as well as long terms investment that will be beneficial in terms of analysing the

adequate return to be obtained by firm at the period of maturity. However, it can be said that if

Boeing mention all the investments in to accounts than it will be fruitful for them to measure the

outcomes they will go to have the time of completion of project.

I. Determine the capital structure weights to be use

In the current situation of Boeing the capital structure is not balanced as they have the

debt for 36% while equity is of 64%. Therefore, it can be said that to balance these ratios there is

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

need to have proper execution in the business which will help the professionals to raise the debts.

The idle capital structure would be balanced as if the ratios of both the elements will reach to 50-

50%,. Thus, in these regards there is need to have proper operational planing in the organisation

which will help them in managing such ratios (Afrin and et.al., 2017). It will be beneficial for

them in enchaining the operational performance of the business as well as have the adequate

control over the debts of the entity.

QUESTION 3

A. Judgement relevant with WACC and the attractiveness of the project Boeing 7E7

In accordance with the measurement relevant with WACC there has been analysis made

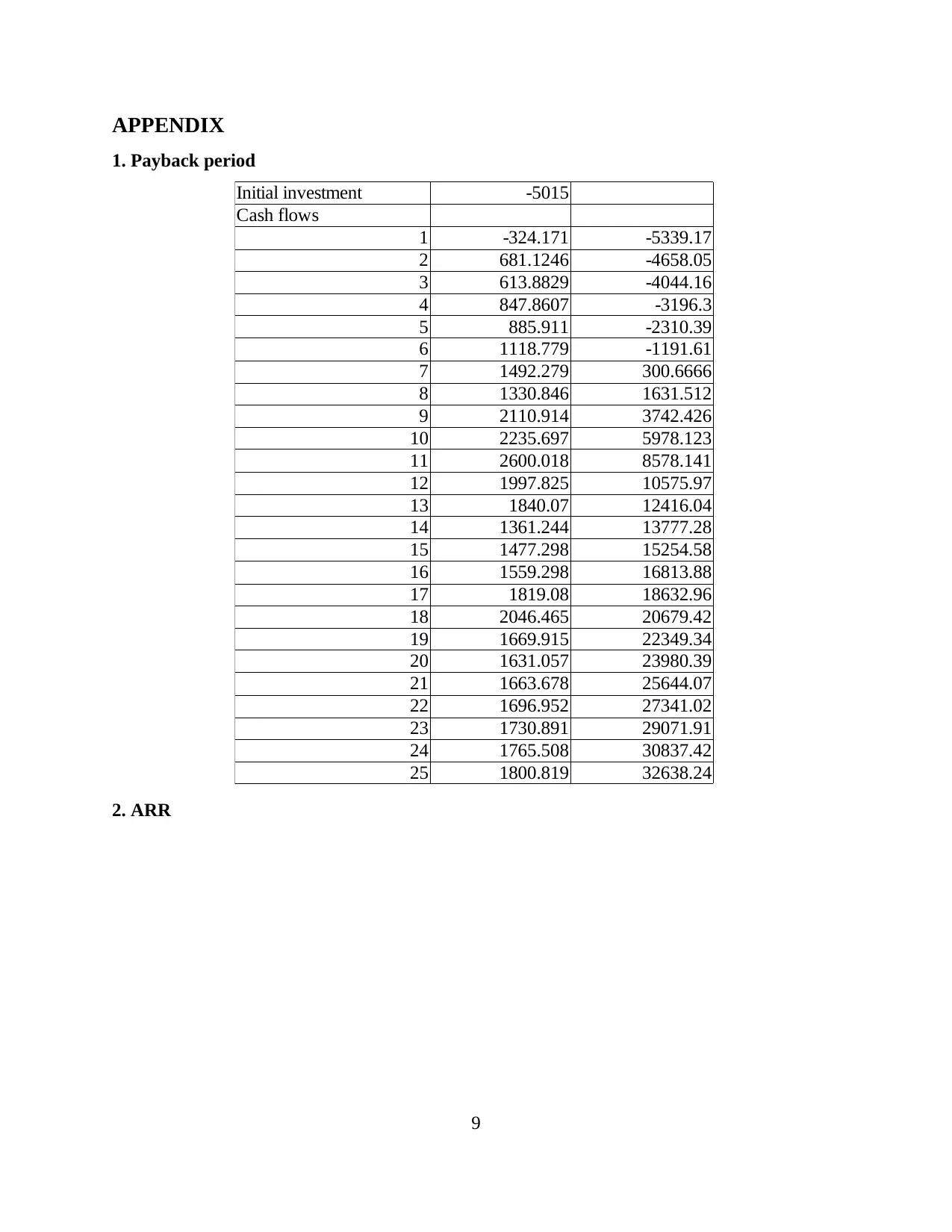

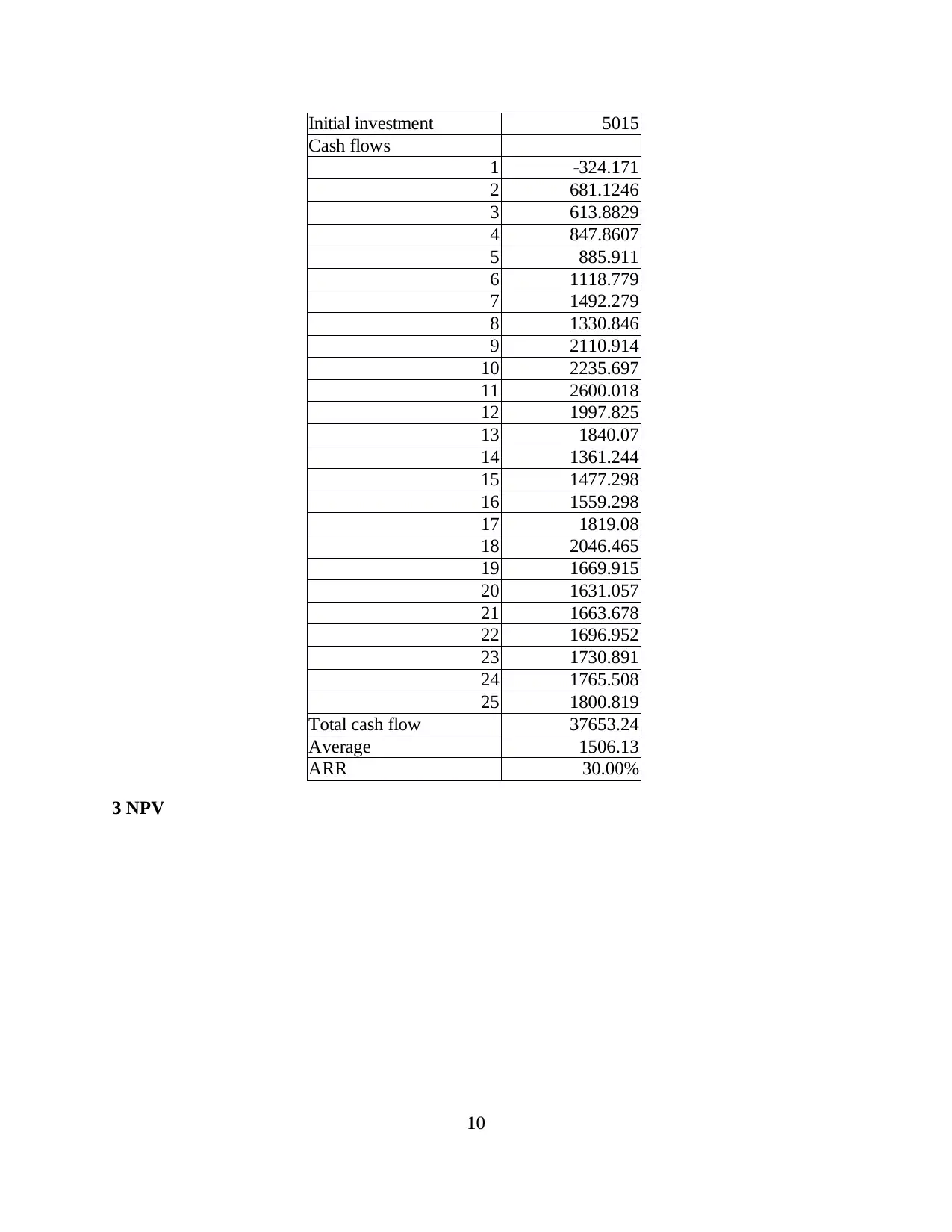

over the ARR, payback and NPV value of the firm. Thus, in these regards it can be said that the

expected life of the project is 6 years which is comparatively lower than the project life for 25

years. In accordance with the annual cash flows of the project the ARR is being estimated as

30%. Therefore, it can be said that that ARR is appropriately measured as it indicates that this

project will be beneficial for Boeing in terms of having the profitable returns. These results are

being shown in the appendix of this project. In terms of identifying the NPV of the project which

represents the present value of the forecasted cash flow (Ong and et.al., 2017). Thus, the NPV is

18547.91 which is reflecting the positive balance as well as better than the initial investments.

Thus, it can be said that the project will be fruitful for the business in the long run and it must be

launched.

B. Economically attractiveness of the project under several conditions

In terms with the profitability of project 7E7 of Boeing, there has been various

circumstances which reflects the fruitfulness of this project. The cost of capital is appropriate as

it indicates that there will be less requirement of funds to meet the operations of business. The

project will have less capital expenditure so the firm do not ned to depend over the shareholders

or investors to make the adequate capital investments in the launch of 7E7. On the other side, the

payback period of the invested capital is to be expected at 6 years, ARR at 30% as well as NPV

as 18547.91. Therefore, it can be said that the project is being very profitable for the business as

it will not reflect any losses and it must be operated (Dutta and Nezlobin, 2017).

5

The idle capital structure would be balanced as if the ratios of both the elements will reach to 50-

50%,. Thus, in these regards there is need to have proper operational planing in the organisation

which will help them in managing such ratios (Afrin and et.al., 2017). It will be beneficial for

them in enchaining the operational performance of the business as well as have the adequate

control over the debts of the entity.

QUESTION 3

A. Judgement relevant with WACC and the attractiveness of the project Boeing 7E7

In accordance with the measurement relevant with WACC there has been analysis made

over the ARR, payback and NPV value of the firm. Thus, in these regards it can be said that the

expected life of the project is 6 years which is comparatively lower than the project life for 25

years. In accordance with the annual cash flows of the project the ARR is being estimated as

30%. Therefore, it can be said that that ARR is appropriately measured as it indicates that this

project will be beneficial for Boeing in terms of having the profitable returns. These results are

being shown in the appendix of this project. In terms of identifying the NPV of the project which

represents the present value of the forecasted cash flow (Ong and et.al., 2017). Thus, the NPV is

18547.91 which is reflecting the positive balance as well as better than the initial investments.

Thus, it can be said that the project will be fruitful for the business in the long run and it must be

launched.

B. Economically attractiveness of the project under several conditions

In terms with the profitability of project 7E7 of Boeing, there has been various

circumstances which reflects the fruitfulness of this project. The cost of capital is appropriate as

it indicates that there will be less requirement of funds to meet the operations of business. The

project will have less capital expenditure so the firm do not ned to depend over the shareholders

or investors to make the adequate capital investments in the launch of 7E7. On the other side, the

payback period of the invested capital is to be expected at 6 years, ARR at 30% as well as NPV

as 18547.91. Therefore, it can be said that the project is being very profitable for the business as

it will not reflect any losses and it must be operated (Dutta and Nezlobin, 2017).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

C. Sensitivity analysis in relation with the Boeing's gamble

To analyse the profitability of the project the sensitivity analysis will reflect the 3

different discounting factors of the operations. Therefore, in these regards the cost of capital and

equity to be considered for estimating the discounting factor at 3.39% of rate. Thus, the

measurements will belong to the cash flow of 25 years at the initial investments of 5015 which

reflect the NPV of 18547.91. It reflects the positive balance for the project as well as the

estimation reflects that this project will be beneficial and it will be helpful for the entity to have

fruitful gains for the long run. There has been changes in the discounting factor which is rated at

2% for the same 25 years the NPV has been measured as 28347.98. Thereafter, the NPV of

21775.26 will be measured at the discounting rate of 4% were measured. Therefore, it can be

said that, the project will be beneficial for the entity as the professionals in the firm make

adequate planning in terms of reducing the expenses or costs of operations (Creedy and

Gemmell, 2017). There has favourable outcomes on the said of each transactions and thus, it can

assume that the project will be profitable for the business as well as it will bring the fruitful

returns.

QUESTION 4

Valuable the project 7E7 for the board

The project 7E7 will be beneficial and profitable for Boeing as per the measurement has

been made over the cost of capital and costs of equity. Therefore, in accordance with the costs of

capital it if 3.39% which is current lower at 2.76% so it can be said that, comparatively the cost

of capital is lower and the business will be beneficial as if they are having the profitable returns

over their expenses In relation with the payback period it has been analysed that the firm will

become able to recover the amount of capital invested in the project which will be within 6 years.

It indicates that the project is profitable for entity as it helps in meeting the amount of

investments within less time. Thereafter, the cost of equity was measured at 1.15% which is also

favourable for the industrial operations. There is need to make increment in the debts of the firm

which will help them in having balance capital structure (Biørn, 2017). However, in accordance

with the ARR and NPV which also reflect the most favourable outcomes from this project. The

NPV has been measured with the help of using the different discounting factors such as 3.39%,

2% and 4% and all presents the positive results. Thus, it can e said that the managers in firm

6

To analyse the profitability of the project the sensitivity analysis will reflect the 3

different discounting factors of the operations. Therefore, in these regards the cost of capital and

equity to be considered for estimating the discounting factor at 3.39% of rate. Thus, the

measurements will belong to the cash flow of 25 years at the initial investments of 5015 which

reflect the NPV of 18547.91. It reflects the positive balance for the project as well as the

estimation reflects that this project will be beneficial and it will be helpful for the entity to have

fruitful gains for the long run. There has been changes in the discounting factor which is rated at

2% for the same 25 years the NPV has been measured as 28347.98. Thereafter, the NPV of

21775.26 will be measured at the discounting rate of 4% were measured. Therefore, it can be

said that, the project will be beneficial for the entity as the professionals in the firm make

adequate planning in terms of reducing the expenses or costs of operations (Creedy and

Gemmell, 2017). There has favourable outcomes on the said of each transactions and thus, it can

assume that the project will be profitable for the business as well as it will bring the fruitful

returns.

QUESTION 4

Valuable the project 7E7 for the board

The project 7E7 will be beneficial and profitable for Boeing as per the measurement has

been made over the cost of capital and costs of equity. Therefore, in accordance with the costs of

capital it if 3.39% which is current lower at 2.76% so it can be said that, comparatively the cost

of capital is lower and the business will be beneficial as if they are having the profitable returns

over their expenses In relation with the payback period it has been analysed that the firm will

become able to recover the amount of capital invested in the project which will be within 6 years.

It indicates that the project is profitable for entity as it helps in meeting the amount of

investments within less time. Thereafter, the cost of equity was measured at 1.15% which is also

favourable for the industrial operations. There is need to make increment in the debts of the firm

which will help them in having balance capital structure (Biørn, 2017). However, in accordance

with the ARR and NPV which also reflect the most favourable outcomes from this project. The

NPV has been measured with the help of using the different discounting factors such as 3.39%,

2% and 4% and all presents the positive results. Thus, it can e said that the managers in firm

6

must launch this project as it will be fruitful for them in the long run as well as it is facilitating

them the adequate results (Levi and Welch, 2017). Moreover, it will be suggested to the

professionals in the firm that they must have proper execution over the costs and expenses to be

made which will be fruitful for them in the long run as well as enhances the performance of

entity.

CONCLUSION

On the basis of this study it can be said that, the project 7E7 for Boeing will be fruitful as

it reselect the adequate balances as well as make the appropriate changes in the operations of the

business. However, it will be helpful for the business in terms of various analysis such as cost of

debt, equity and capitals. In accordance with the profitably of the projects the analysis has been

made at determining the payback period, ARR and NPV for the estimated 25 years. Thus, this all

factors reflects favourable outcomes and the project must be operated.

7

them the adequate results (Levi and Welch, 2017). Moreover, it will be suggested to the

professionals in the firm that they must have proper execution over the costs and expenses to be

made which will be fruitful for them in the long run as well as enhances the performance of

entity.

CONCLUSION

On the basis of this study it can be said that, the project 7E7 for Boeing will be fruitful as

it reselect the adequate balances as well as make the appropriate changes in the operations of the

business. However, it will be helpful for the business in terms of various analysis such as cost of

debt, equity and capitals. In accordance with the profitably of the projects the analysis has been

made at determining the payback period, ARR and NPV for the estimated 25 years. Thus, this all

factors reflects favourable outcomes and the project must be operated.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Afrin, H. and et.al., 2017. Profitability analysis and gender division of labour in duck rearing: a

case of Kishoreganj district in Bangladesh. Progressive Agriculture. 27(4). pp.482-489.

Biørn, E., 2017. Taxation, technology, and the user cost of capital (Vol. 182). Elsevier.

Borello, D. and et.al., 2017. Modeling and Experimental Study of a Small Scale Olive Pomace

Gasifier for Cogeneration: Energy and Profitability Analysis. Energies. 10(12). p.1930.

Creedy, J. and Gemmell, N., 2017. Taxation and the user cost of capital. Journal of Economic

Surveys. 31(1). pp.201-225.

Dutta, S. and Nezlobin, A., 2017. Information disclosure, firm growth, and the cost of capital.

Journal of Financial Economics. 123(2). pp.415-431.

Levi, Y. and Welch, I., 2017. Best Practice for Cost-of-Capital Estimates. Journal of Financial

and Quantitative Analysis. 52(2). pp.427-463.

López Prol, J. and Steininger, K. W., 2017. Photovoltaic self-consumption regulation in Spain:

Profitability analysis and alternative regulation schemes. Energy Policy. 108(C). pp.742-

754.

Olson, G. T. and Pagano, M. S., 2017. The Empirical Average Cost of Capital: A New Approach

to Estimating the Cost of Corporate Funds. Journal of Applied Corporate Finance. 29(3).

pp.101-110.

Ong, J. B. and et.al., 2017. Groupon and Groupon Now: Participating Firm’s Profitability

Analysis. Computational Economics, pp.1-16.

Sanusi, M. M. and Dada, O. D., 2017. PROFITABILITY ANALYSIS OF MARKETING

TOMATO IN ODEDA LOCAL GOVERNMENT AREA OF OGUN STATE, NIGERIA.

Ife Journal of Agriculture. 28(2). pp.91-101.

Online

Using CAPM to determine the cost of debt. 2012. [Online]. Available through

:<http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Cost%20of%20Debt.aspx>.

8

Books and Journals

Afrin, H. and et.al., 2017. Profitability analysis and gender division of labour in duck rearing: a

case of Kishoreganj district in Bangladesh. Progressive Agriculture. 27(4). pp.482-489.

Biørn, E., 2017. Taxation, technology, and the user cost of capital (Vol. 182). Elsevier.

Borello, D. and et.al., 2017. Modeling and Experimental Study of a Small Scale Olive Pomace

Gasifier for Cogeneration: Energy and Profitability Analysis. Energies. 10(12). p.1930.

Creedy, J. and Gemmell, N., 2017. Taxation and the user cost of capital. Journal of Economic

Surveys. 31(1). pp.201-225.

Dutta, S. and Nezlobin, A., 2017. Information disclosure, firm growth, and the cost of capital.

Journal of Financial Economics. 123(2). pp.415-431.

Levi, Y. and Welch, I., 2017. Best Practice for Cost-of-Capital Estimates. Journal of Financial

and Quantitative Analysis. 52(2). pp.427-463.

López Prol, J. and Steininger, K. W., 2017. Photovoltaic self-consumption regulation in Spain:

Profitability analysis and alternative regulation schemes. Energy Policy. 108(C). pp.742-

754.

Olson, G. T. and Pagano, M. S., 2017. The Empirical Average Cost of Capital: A New Approach

to Estimating the Cost of Corporate Funds. Journal of Applied Corporate Finance. 29(3).

pp.101-110.

Ong, J. B. and et.al., 2017. Groupon and Groupon Now: Participating Firm’s Profitability

Analysis. Computational Economics, pp.1-16.

Sanusi, M. M. and Dada, O. D., 2017. PROFITABILITY ANALYSIS OF MARKETING

TOMATO IN ODEDA LOCAL GOVERNMENT AREA OF OGUN STATE, NIGERIA.

Ife Journal of Agriculture. 28(2). pp.91-101.

Online

Using CAPM to determine the cost of debt. 2012. [Online]. Available through

:<http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Cost%20of%20Debt.aspx>.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

1. Payback period

Initial investment -5015

Cash flows

1 -324.171 -5339.17

2 681.1246 -4658.05

3 613.8829 -4044.16

4 847.8607 -3196.3

5 885.911 -2310.39

6 1118.779 -1191.61

7 1492.279 300.6666

8 1330.846 1631.512

9 2110.914 3742.426

10 2235.697 5978.123

11 2600.018 8578.141

12 1997.825 10575.97

13 1840.07 12416.04

14 1361.244 13777.28

15 1477.298 15254.58

16 1559.298 16813.88

17 1819.08 18632.96

18 2046.465 20679.42

19 1669.915 22349.34

20 1631.057 23980.39

21 1663.678 25644.07

22 1696.952 27341.02

23 1730.891 29071.91

24 1765.508 30837.42

25 1800.819 32638.24

2. ARR

9

1. Payback period

Initial investment -5015

Cash flows

1 -324.171 -5339.17

2 681.1246 -4658.05

3 613.8829 -4044.16

4 847.8607 -3196.3

5 885.911 -2310.39

6 1118.779 -1191.61

7 1492.279 300.6666

8 1330.846 1631.512

9 2110.914 3742.426

10 2235.697 5978.123

11 2600.018 8578.141

12 1997.825 10575.97

13 1840.07 12416.04

14 1361.244 13777.28

15 1477.298 15254.58

16 1559.298 16813.88

17 1819.08 18632.96

18 2046.465 20679.42

19 1669.915 22349.34

20 1631.057 23980.39

21 1663.678 25644.07

22 1696.952 27341.02

23 1730.891 29071.91

24 1765.508 30837.42

25 1800.819 32638.24

2. ARR

9

Initial investment 5015

Cash flows

1 -324.171

2 681.1246

3 613.8829

4 847.8607

5 885.911

6 1118.779

7 1492.279

8 1330.846

9 2110.914

10 2235.697

11 2600.018

12 1997.825

13 1840.07

14 1361.244

15 1477.298

16 1559.298

17 1819.08

18 2046.465

19 1669.915

20 1631.057

21 1663.678

22 1696.952

23 1730.891

24 1765.508

25 1800.819

Total cash flow 37653.24

Average 1506.13

ARR 30.00%

3 NPV

10

Cash flows

1 -324.171

2 681.1246

3 613.8829

4 847.8607

5 885.911

6 1118.779

7 1492.279

8 1330.846

9 2110.914

10 2235.697

11 2600.018

12 1997.825

13 1840.07

14 1361.244

15 1477.298

16 1559.298

17 1819.08

18 2046.465

19 1669.915

20 1631.057

21 1663.678

22 1696.952

23 1730.891

24 1765.508

25 1800.819

Total cash flow 37653.24

Average 1506.13

ARR 30.00%

3 NPV

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.