Analyzing Boeing & General Dynamics Stocks Using Statistics

VerifiedAdded on 2023/06/11

|14

|2481

|429

Report

AI Summary

This report provides a statistical analysis of Boeing (BA) and General Dynamics (GD) stock prices from July 2011 to July 2016, utilizing monthly adjusted closing prices obtained from Yahoo Finance. The analysis includes trend identification, return calculations, and summary statistics, along with Jarque-Bera tests to assess normality. A one-sample t-test evaluates if GD's average return differs from 2.8%, while an F-test compares the variances of BA and GD. An independent sample t-test determines if the average returns of both stocks are similar. The Capital Asset Pricing Model (CAPM) is applied to GD, calculating excess returns and market returns to assess risk, with a regression analysis providing a coefficient of determination. Desklib offers this and other solved assignments for students seeking study resources.

Running Head: STATISTICS FOR BUSINESS AND FINANCE

Statistics for Business and Finance

Name of the Student

Name of the University

Author Note

Statistics for Business and Finance

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1SFFBSTATISTICS FOR BUSINESS AND FINANCE

Table of Contents

Introduction......................................................................................................................................2

Task A..............................................................................................................................................2

Part 2................................................................................................................................................4

Part a............................................................................................................................................4

Part b............................................................................................................................................6

Part c............................................................................................................................................6

Part 3................................................................................................................................................7

Part 4................................................................................................................................................8

Part 5................................................................................................................................................8

Part 6................................................................................................................................................9

Part 7................................................................................................................................................9

Part a............................................................................................................................................9

Part b..........................................................................................................................................11

Part c..........................................................................................................................................11

Part d..........................................................................................................................................12

Part 8..............................................................................................................................................12

Part 9..............................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................2

Task A..............................................................................................................................................2

Part 2................................................................................................................................................4

Part a............................................................................................................................................4

Part b............................................................................................................................................6

Part c............................................................................................................................................6

Part 3................................................................................................................................................7

Part 4................................................................................................................................................8

Part 5................................................................................................................................................8

Part 6................................................................................................................................................9

Part 7................................................................................................................................................9

Part a............................................................................................................................................9

Part b..........................................................................................................................................11

Part c..........................................................................................................................................11

Part d..........................................................................................................................................12

Part 8..............................................................................................................................................12

Part 9..............................................................................................................................................12

2SFFBSTATISTICS FOR BUSINESS AND FINANCE

Introduction

In order to invest in stock one should be able to analyse the stocks. The decision to invest can be

taken can be taken after an analysis of the performance of the stock. The performance of a stock

can be evaluated from its returns. Here we have evaluated the stocks of Boeing (BA) and

General Dynamics (GD). The adjusted closing prices of the stock for the period 1st July 2011 to

1st July 2016 have been taken to compare the performance of the stocks (roll No 1 9552104). The

information on the stock prices have been collected from yahoo finance. Monthly data of the

stock prices have been taken into account. Further, for market portfolio S&P 500 and to calculate

excess return “interest rate on 10-year treasury note” have been used.

The decision to invest in a stock depends on performance of the stock.

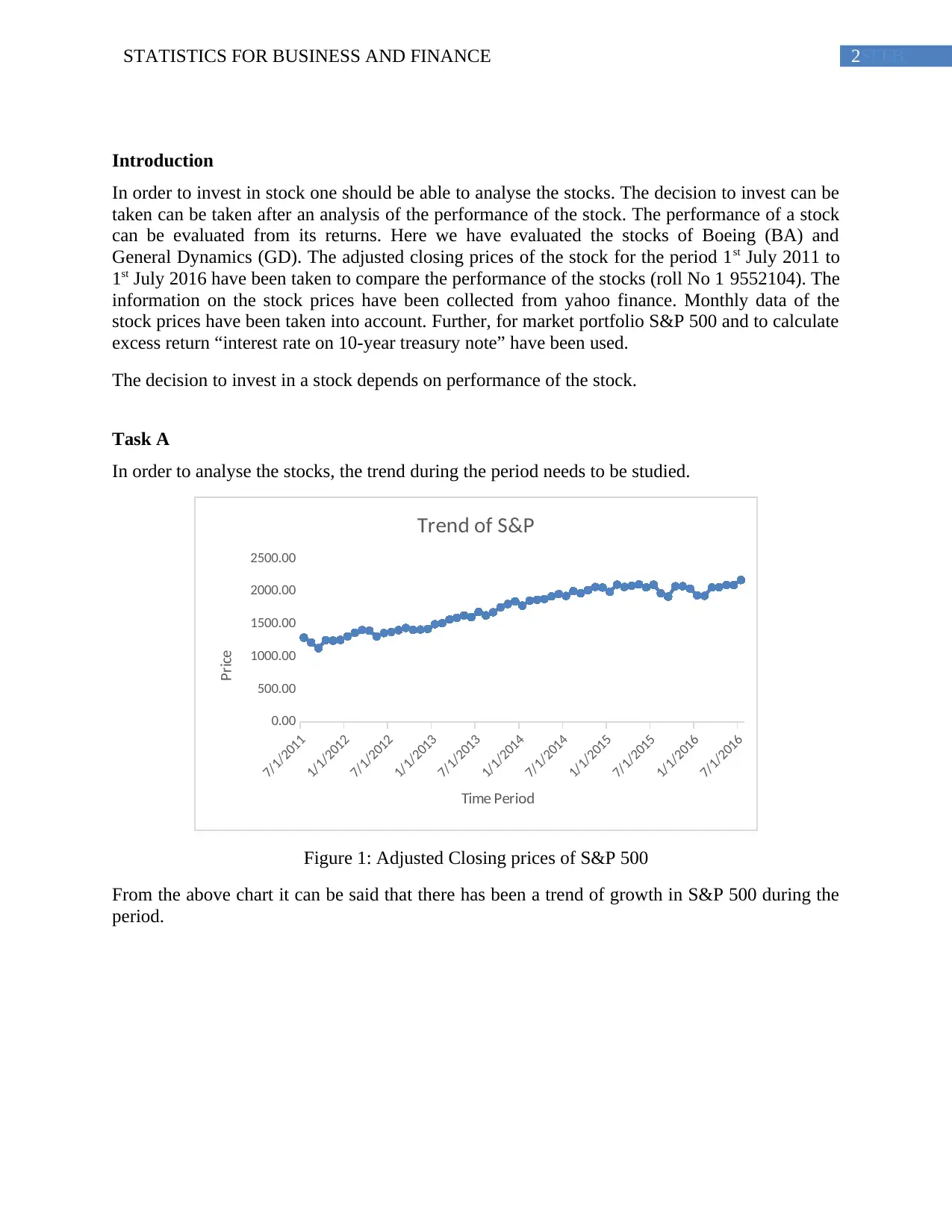

Task A

In order to analyse the stocks, the trend during the period needs to be studied.

7/1/2011

1/1/2012

7/1/2012

1/1/2013

7/1/2013

1/1/2014

7/1/2014

1/1/2015

7/1/2015

1/1/2016

7/1/2016

0.00

500.00

1000.00

1500.00

2000.00

2500.00

Trend of S&P

Time Period

Price

Figure 1: Adjusted Closing prices of S&P 500

From the above chart it can be said that there has been a trend of growth in S&P 500 during the

period.

Introduction

In order to invest in stock one should be able to analyse the stocks. The decision to invest can be

taken can be taken after an analysis of the performance of the stock. The performance of a stock

can be evaluated from its returns. Here we have evaluated the stocks of Boeing (BA) and

General Dynamics (GD). The adjusted closing prices of the stock for the period 1st July 2011 to

1st July 2016 have been taken to compare the performance of the stocks (roll No 1 9552104). The

information on the stock prices have been collected from yahoo finance. Monthly data of the

stock prices have been taken into account. Further, for market portfolio S&P 500 and to calculate

excess return “interest rate on 10-year treasury note” have been used.

The decision to invest in a stock depends on performance of the stock.

Task A

In order to analyse the stocks, the trend during the period needs to be studied.

7/1/2011

1/1/2012

7/1/2012

1/1/2013

7/1/2013

1/1/2014

7/1/2014

1/1/2015

7/1/2015

1/1/2016

7/1/2016

0.00

500.00

1000.00

1500.00

2000.00

2500.00

Trend of S&P

Time Period

Price

Figure 1: Adjusted Closing prices of S&P 500

From the above chart it can be said that there has been a trend of growth in S&P 500 during the

period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3SFFBSTATISTICS FOR BUSINESS AND FINANCE

7/1/2011

1/1/2012

7/1/2012

1/1/2013

7/1/2013

1/1/2014

7/1/2014

1/1/2015

7/1/2015

1/1/2016

7/1/2016

0

20

40

60

80

100

120

140

160

Trend of Boeing

Time Period

Period

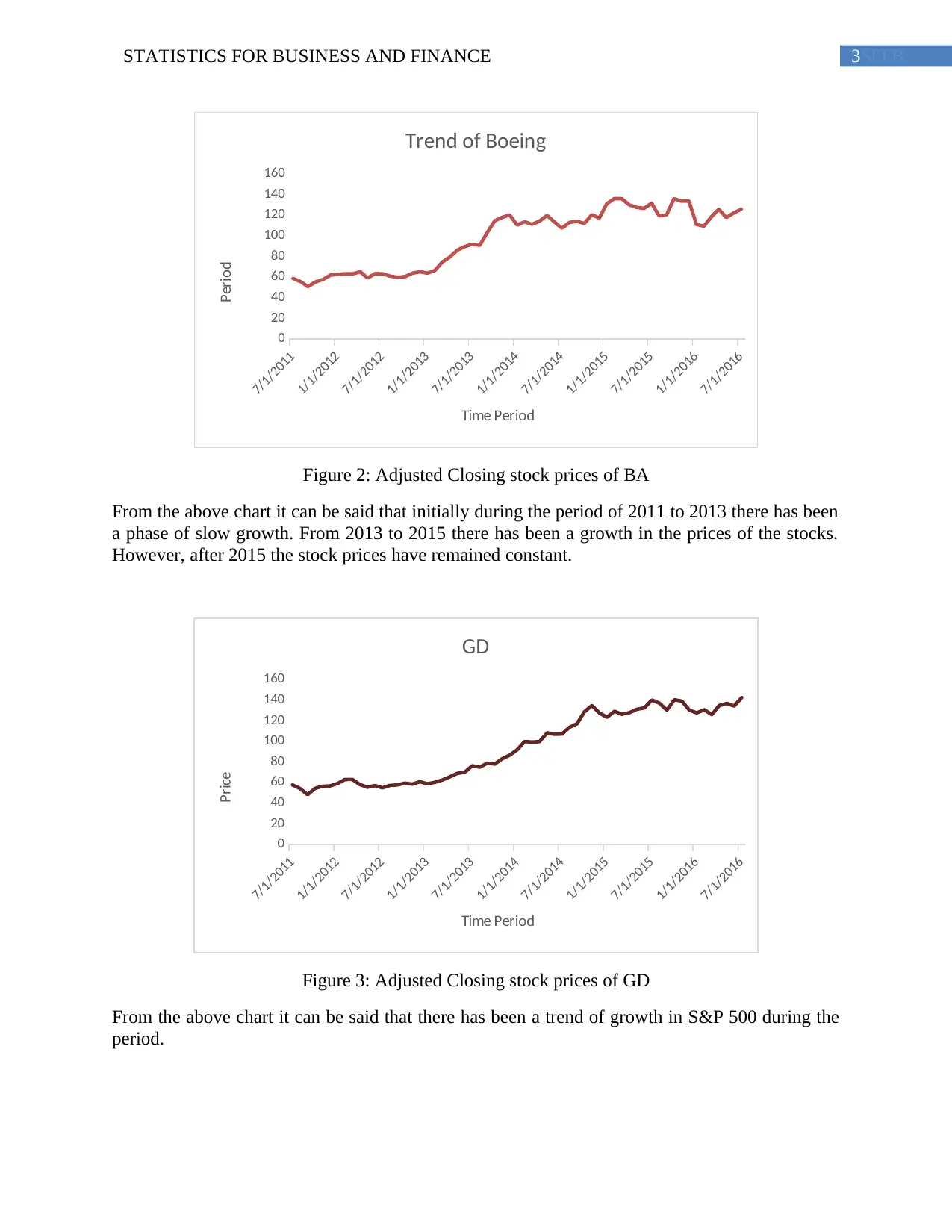

Figure 2: Adjusted Closing stock prices of BA

From the above chart it can be said that initially during the period of 2011 to 2013 there has been

a phase of slow growth. From 2013 to 2015 there has been a growth in the prices of the stocks.

However, after 2015 the stock prices have remained constant.

7/1/2011

1/1/2012

7/1/2012

1/1/2013

7/1/2013

1/1/2014

7/1/2014

1/1/2015

7/1/2015

1/1/2016

7/1/2016

0

20

40

60

80

100

120

140

160

GD

Time Period

Price

Figure 3: Adjusted Closing stock prices of GD

From the above chart it can be said that there has been a trend of growth in S&P 500 during the

period.

7/1/2011

1/1/2012

7/1/2012

1/1/2013

7/1/2013

1/1/2014

7/1/2014

1/1/2015

7/1/2015

1/1/2016

7/1/2016

0

20

40

60

80

100

120

140

160

Trend of Boeing

Time Period

Period

Figure 2: Adjusted Closing stock prices of BA

From the above chart it can be said that initially during the period of 2011 to 2013 there has been

a phase of slow growth. From 2013 to 2015 there has been a growth in the prices of the stocks.

However, after 2015 the stock prices have remained constant.

7/1/2011

1/1/2012

7/1/2012

1/1/2013

7/1/2013

1/1/2014

7/1/2014

1/1/2015

7/1/2015

1/1/2016

7/1/2016

0

20

40

60

80

100

120

140

160

GD

Time Period

Price

Figure 3: Adjusted Closing stock prices of GD

From the above chart it can be said that there has been a trend of growth in S&P 500 during the

period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4SFFBSTATISTICS FOR BUSINESS AND FINANCE

Part 2

Part a

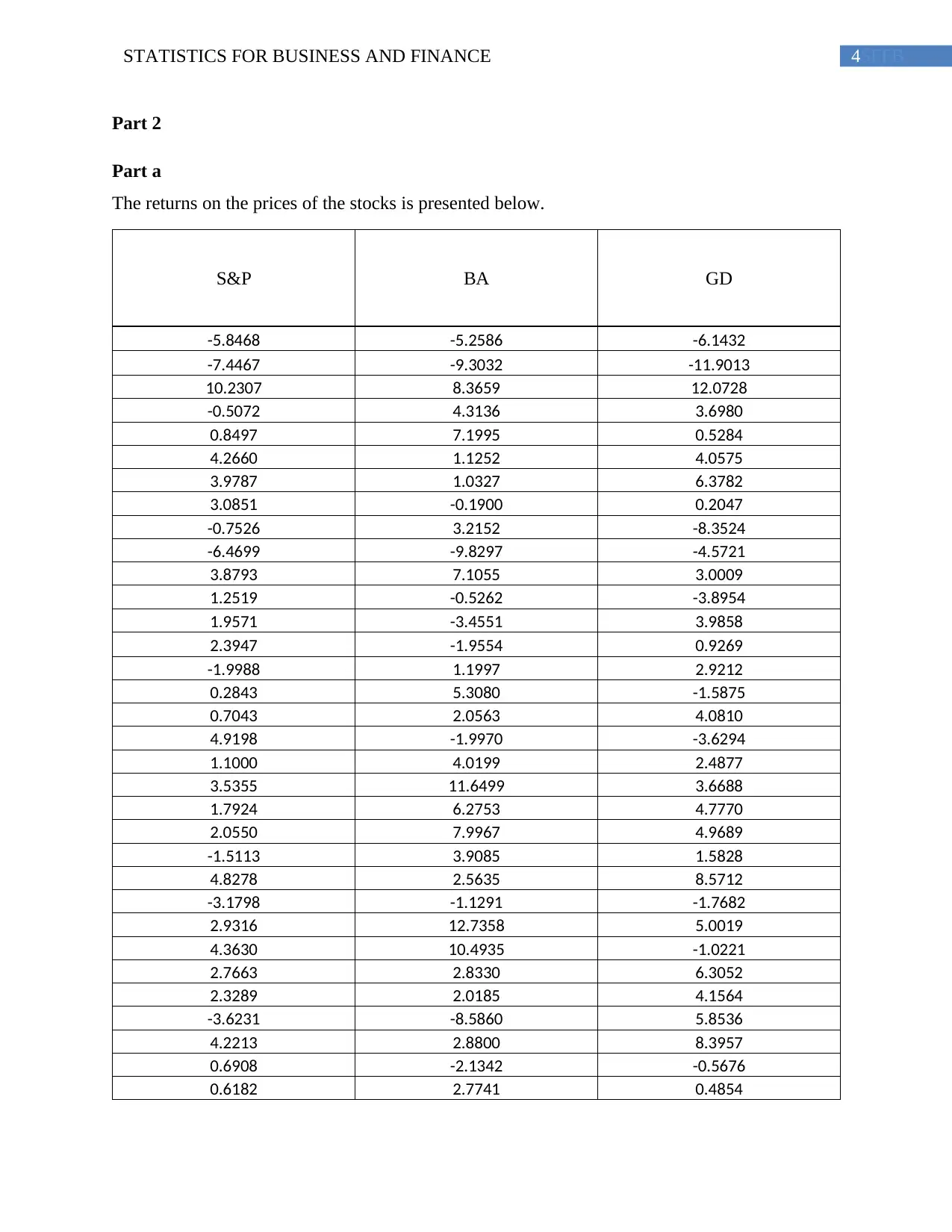

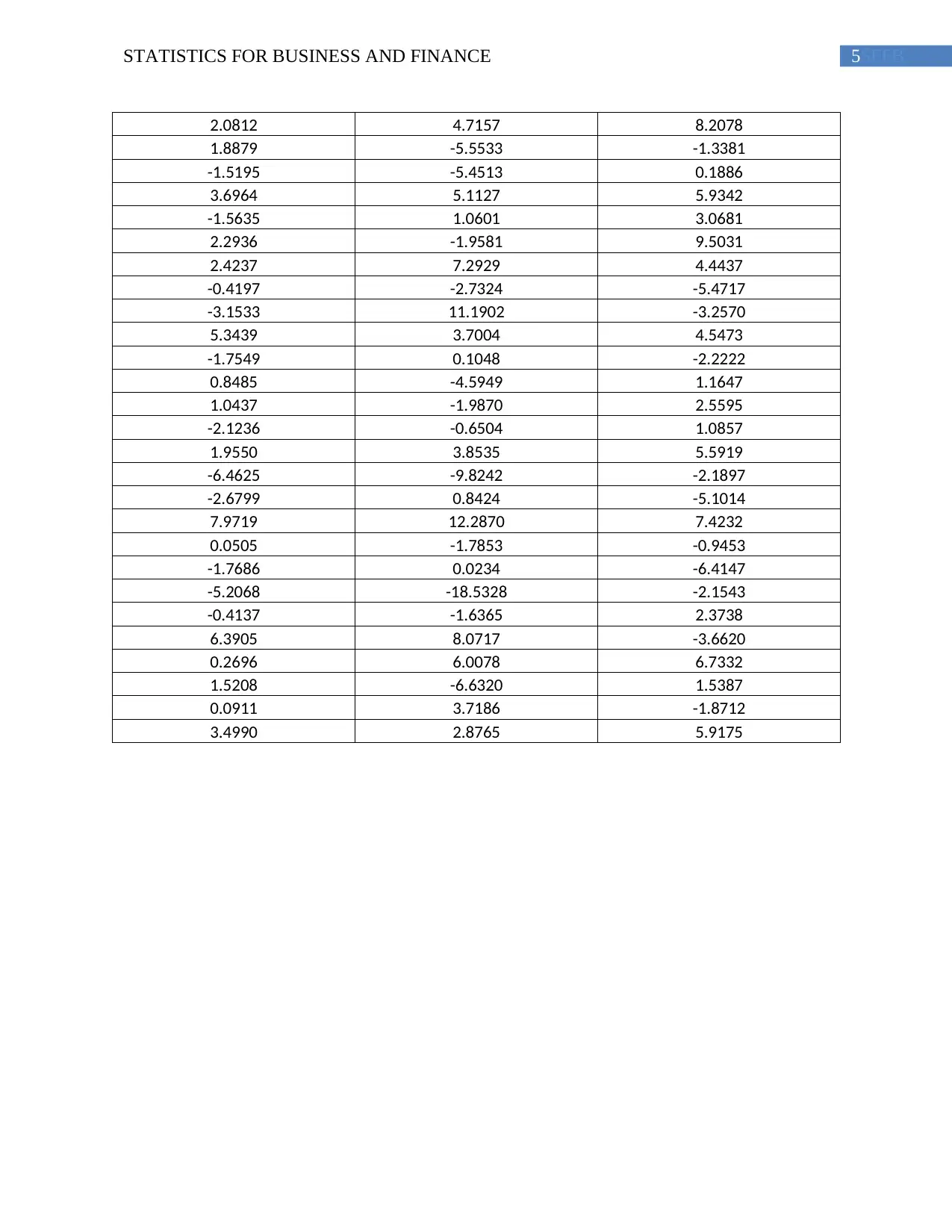

The returns on the prices of the stocks is presented below.

S&P BA GD

-5.8468 -5.2586 -6.1432

-7.4467 -9.3032 -11.9013

10.2307 8.3659 12.0728

-0.5072 4.3136 3.6980

0.8497 7.1995 0.5284

4.2660 1.1252 4.0575

3.9787 1.0327 6.3782

3.0851 -0.1900 0.2047

-0.7526 3.2152 -8.3524

-6.4699 -9.8297 -4.5721

3.8793 7.1055 3.0009

1.2519 -0.5262 -3.8954

1.9571 -3.4551 3.9858

2.3947 -1.9554 0.9269

-1.9988 1.1997 2.9212

0.2843 5.3080 -1.5875

0.7043 2.0563 4.0810

4.9198 -1.9970 -3.6294

1.1000 4.0199 2.4877

3.5355 11.6499 3.6688

1.7924 6.2753 4.7770

2.0550 7.9967 4.9689

-1.5113 3.9085 1.5828

4.8278 2.5635 8.5712

-3.1798 -1.1291 -1.7682

2.9316 12.7358 5.0019

4.3630 10.4935 -1.0221

2.7663 2.8330 6.3052

2.3289 2.0185 4.1564

-3.6231 -8.5860 5.8536

4.2213 2.8800 8.3957

0.6908 -2.1342 -0.5676

0.6182 2.7741 0.4854

Part 2

Part a

The returns on the prices of the stocks is presented below.

S&P BA GD

-5.8468 -5.2586 -6.1432

-7.4467 -9.3032 -11.9013

10.2307 8.3659 12.0728

-0.5072 4.3136 3.6980

0.8497 7.1995 0.5284

4.2660 1.1252 4.0575

3.9787 1.0327 6.3782

3.0851 -0.1900 0.2047

-0.7526 3.2152 -8.3524

-6.4699 -9.8297 -4.5721

3.8793 7.1055 3.0009

1.2519 -0.5262 -3.8954

1.9571 -3.4551 3.9858

2.3947 -1.9554 0.9269

-1.9988 1.1997 2.9212

0.2843 5.3080 -1.5875

0.7043 2.0563 4.0810

4.9198 -1.9970 -3.6294

1.1000 4.0199 2.4877

3.5355 11.6499 3.6688

1.7924 6.2753 4.7770

2.0550 7.9967 4.9689

-1.5113 3.9085 1.5828

4.8278 2.5635 8.5712

-3.1798 -1.1291 -1.7682

2.9316 12.7358 5.0019

4.3630 10.4935 -1.0221

2.7663 2.8330 6.3052

2.3289 2.0185 4.1564

-3.6231 -8.5860 5.8536

4.2213 2.8800 8.3957

0.6908 -2.1342 -0.5676

0.6182 2.7741 0.4854

5SFFBSTATISTICS FOR BUSINESS AND FINANCE

2.0812 4.7157 8.2078

1.8879 -5.5533 -1.3381

-1.5195 -5.4513 0.1886

3.6964 5.1127 5.9342

-1.5635 1.0601 3.0681

2.2936 -1.9581 9.5031

2.4237 7.2929 4.4437

-0.4197 -2.7324 -5.4717

-3.1533 11.1902 -3.2570

5.3439 3.7004 4.5473

-1.7549 0.1048 -2.2222

0.8485 -4.5949 1.1647

1.0437 -1.9870 2.5595

-2.1236 -0.6504 1.0857

1.9550 3.8535 5.5919

-6.4625 -9.8242 -2.1897

-2.6799 0.8424 -5.1014

7.9719 12.2870 7.4232

0.0505 -1.7853 -0.9453

-1.7686 0.0234 -6.4147

-5.2068 -18.5328 -2.1543

-0.4137 -1.6365 2.3738

6.3905 8.0717 -3.6620

0.2696 6.0078 6.7332

1.5208 -6.6320 1.5387

0.0911 3.7186 -1.8712

3.4990 2.8765 5.9175

2.0812 4.7157 8.2078

1.8879 -5.5533 -1.3381

-1.5195 -5.4513 0.1886

3.6964 5.1127 5.9342

-1.5635 1.0601 3.0681

2.2936 -1.9581 9.5031

2.4237 7.2929 4.4437

-0.4197 -2.7324 -5.4717

-3.1533 11.1902 -3.2570

5.3439 3.7004 4.5473

-1.7549 0.1048 -2.2222

0.8485 -4.5949 1.1647

1.0437 -1.9870 2.5595

-2.1236 -0.6504 1.0857

1.9550 3.8535 5.5919

-6.4625 -9.8242 -2.1897

-2.6799 0.8424 -5.1014

7.9719 12.2870 7.4232

0.0505 -1.7853 -0.9453

-1.7686 0.0234 -6.4147

-5.2068 -18.5328 -2.1543

-0.4137 -1.6365 2.3738

6.3905 8.0717 -3.6620

0.2696 6.0078 6.7332

1.5208 -6.6320 1.5387

0.0911 3.7186 -1.8712

3.4990 2.8765 5.9175

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6SFFBSTATISTICS FOR BUSINESS AND FINANCE

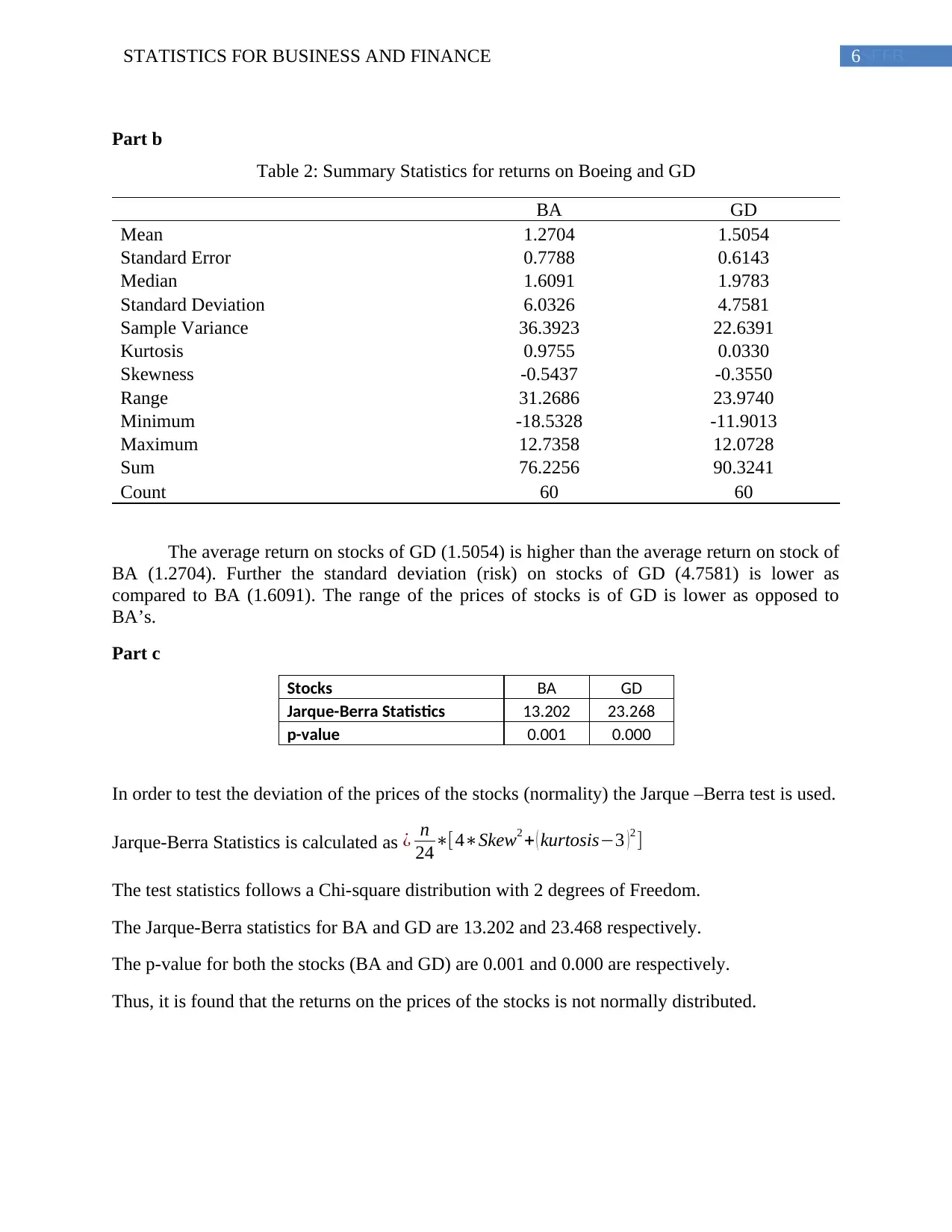

Part b

Table 2: Summary Statistics for returns on Boeing and GD

BA GD

Mean 1.2704 1.5054

Standard Error 0.7788 0.6143

Median 1.6091 1.9783

Standard Deviation 6.0326 4.7581

Sample Variance 36.3923 22.6391

Kurtosis 0.9755 0.0330

Skewness -0.5437 -0.3550

Range 31.2686 23.9740

Minimum -18.5328 -11.9013

Maximum 12.7358 12.0728

Sum 76.2256 90.3241

Count 60 60

The average return on stocks of GD (1.5054) is higher than the average return on stock of

BA (1.2704). Further the standard deviation (risk) on stocks of GD (4.7581) is lower as

compared to BA (1.6091). The range of the prices of stocks is of GD is lower as opposed to

BA’s.

Part c

Stocks BA GD

Jarque-Berra Statistics 13.202 23.268

p-value 0.001 0.000

In order to test the deviation of the prices of the stocks (normality) the Jarque –Berra test is used.

Jarque-Berra Statistics is calculated as ¿ n

24∗[4∗Skew2 + ( kurtosis−3 )2 ]

The test statistics follows a Chi-square distribution with 2 degrees of Freedom.

The Jarque-Berra statistics for BA and GD are 13.202 and 23.468 respectively.

The p-value for both the stocks (BA and GD) are 0.001 and 0.000 are respectively.

Thus, it is found that the returns on the prices of the stocks is not normally distributed.

Part b

Table 2: Summary Statistics for returns on Boeing and GD

BA GD

Mean 1.2704 1.5054

Standard Error 0.7788 0.6143

Median 1.6091 1.9783

Standard Deviation 6.0326 4.7581

Sample Variance 36.3923 22.6391

Kurtosis 0.9755 0.0330

Skewness -0.5437 -0.3550

Range 31.2686 23.9740

Minimum -18.5328 -11.9013

Maximum 12.7358 12.0728

Sum 76.2256 90.3241

Count 60 60

The average return on stocks of GD (1.5054) is higher than the average return on stock of

BA (1.2704). Further the standard deviation (risk) on stocks of GD (4.7581) is lower as

compared to BA (1.6091). The range of the prices of stocks is of GD is lower as opposed to

BA’s.

Part c

Stocks BA GD

Jarque-Berra Statistics 13.202 23.268

p-value 0.001 0.000

In order to test the deviation of the prices of the stocks (normality) the Jarque –Berra test is used.

Jarque-Berra Statistics is calculated as ¿ n

24∗[4∗Skew2 + ( kurtosis−3 )2 ]

The test statistics follows a Chi-square distribution with 2 degrees of Freedom.

The Jarque-Berra statistics for BA and GD are 13.202 and 23.468 respectively.

The p-value for both the stocks (BA and GD) are 0.001 and 0.000 are respectively.

Thus, it is found that the returns on the prices of the stocks is not normally distributed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7SFFBSTATISTICS FOR BUSINESS AND FINANCE

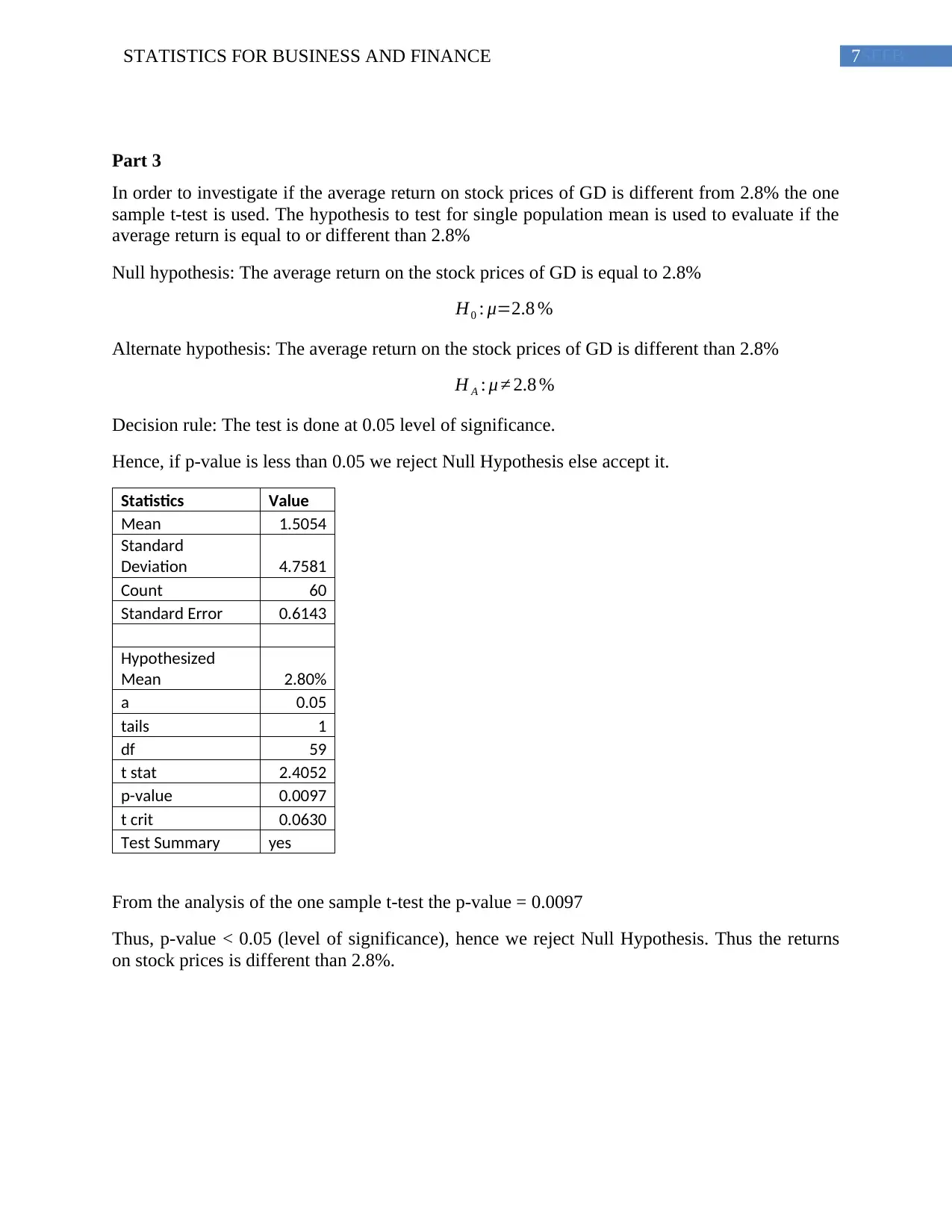

Part 3

In order to investigate if the average return on stock prices of GD is different from 2.8% the one

sample t-test is used. The hypothesis to test for single population mean is used to evaluate if the

average return is equal to or different than 2.8%

Null hypothesis: The average return on the stock prices of GD is equal to 2.8%

H0 : μ=2.8 %

Alternate hypothesis: The average return on the stock prices of GD is different than 2.8%

H A : μ ≠ 2.8 %

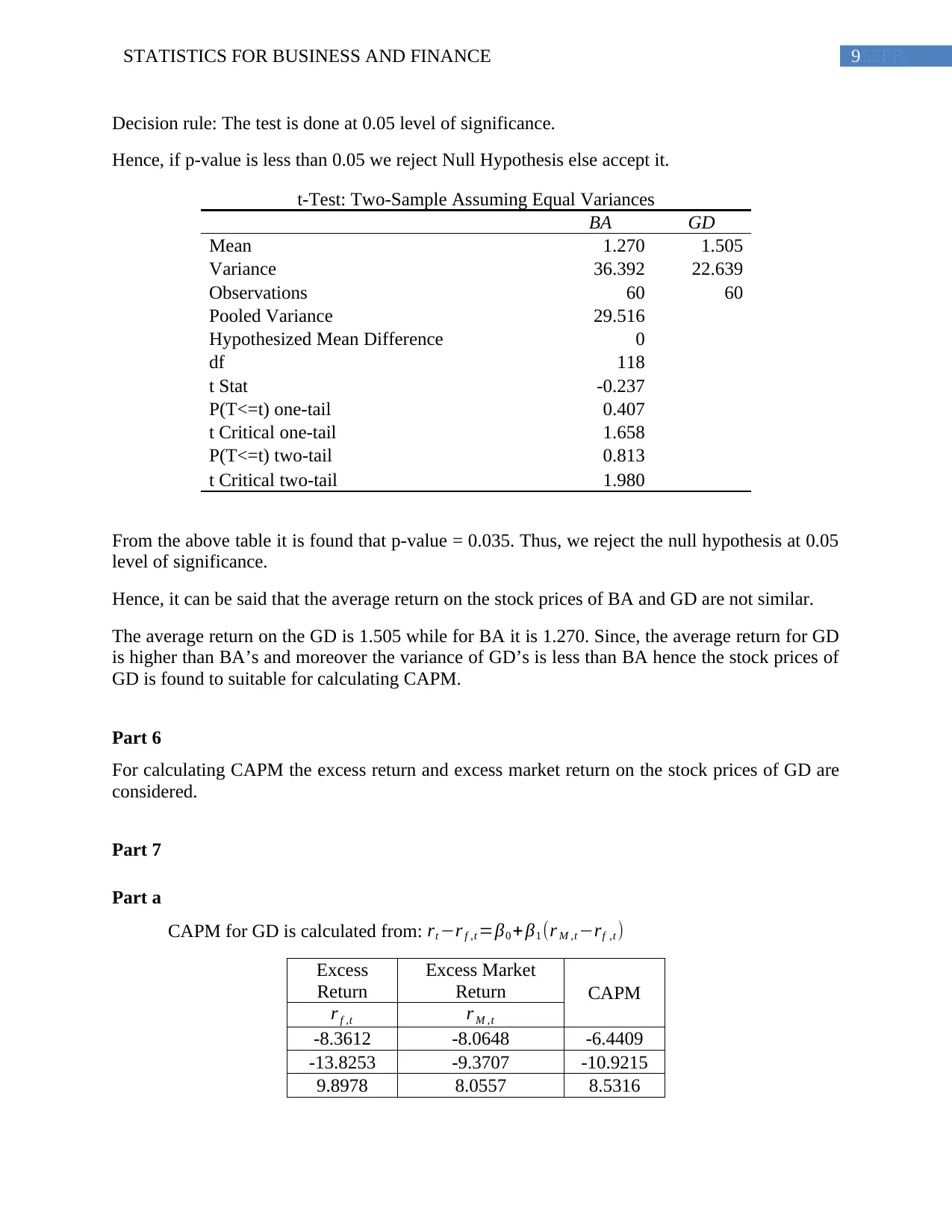

Decision rule: The test is done at 0.05 level of significance.

Hence, if p-value is less than 0.05 we reject Null Hypothesis else accept it.

Statistics Value

Mean 1.5054

Standard

Deviation 4.7581

Count 60

Standard Error 0.6143

Hypothesized

Mean 2.80%

a 0.05

tails 1

df 59

t stat 2.4052

p-value 0.0097

t crit 0.0630

Test Summary yes

From the analysis of the one sample t-test the p-value = 0.0097

Thus, p-value < 0.05 (level of significance), hence we reject Null Hypothesis. Thus the returns

on stock prices is different than 2.8%.

Part 3

In order to investigate if the average return on stock prices of GD is different from 2.8% the one

sample t-test is used. The hypothesis to test for single population mean is used to evaluate if the

average return is equal to or different than 2.8%

Null hypothesis: The average return on the stock prices of GD is equal to 2.8%

H0 : μ=2.8 %

Alternate hypothesis: The average return on the stock prices of GD is different than 2.8%

H A : μ ≠ 2.8 %

Decision rule: The test is done at 0.05 level of significance.

Hence, if p-value is less than 0.05 we reject Null Hypothesis else accept it.

Statistics Value

Mean 1.5054

Standard

Deviation 4.7581

Count 60

Standard Error 0.6143

Hypothesized

Mean 2.80%

a 0.05

tails 1

df 59

t stat 2.4052

p-value 0.0097

t crit 0.0630

Test Summary yes

From the analysis of the one sample t-test the p-value = 0.0097

Thus, p-value < 0.05 (level of significance), hence we reject Null Hypothesis. Thus the returns

on stock prices is different than 2.8%.

8SFFBSTATISTICS FOR BUSINESS AND FINANCE

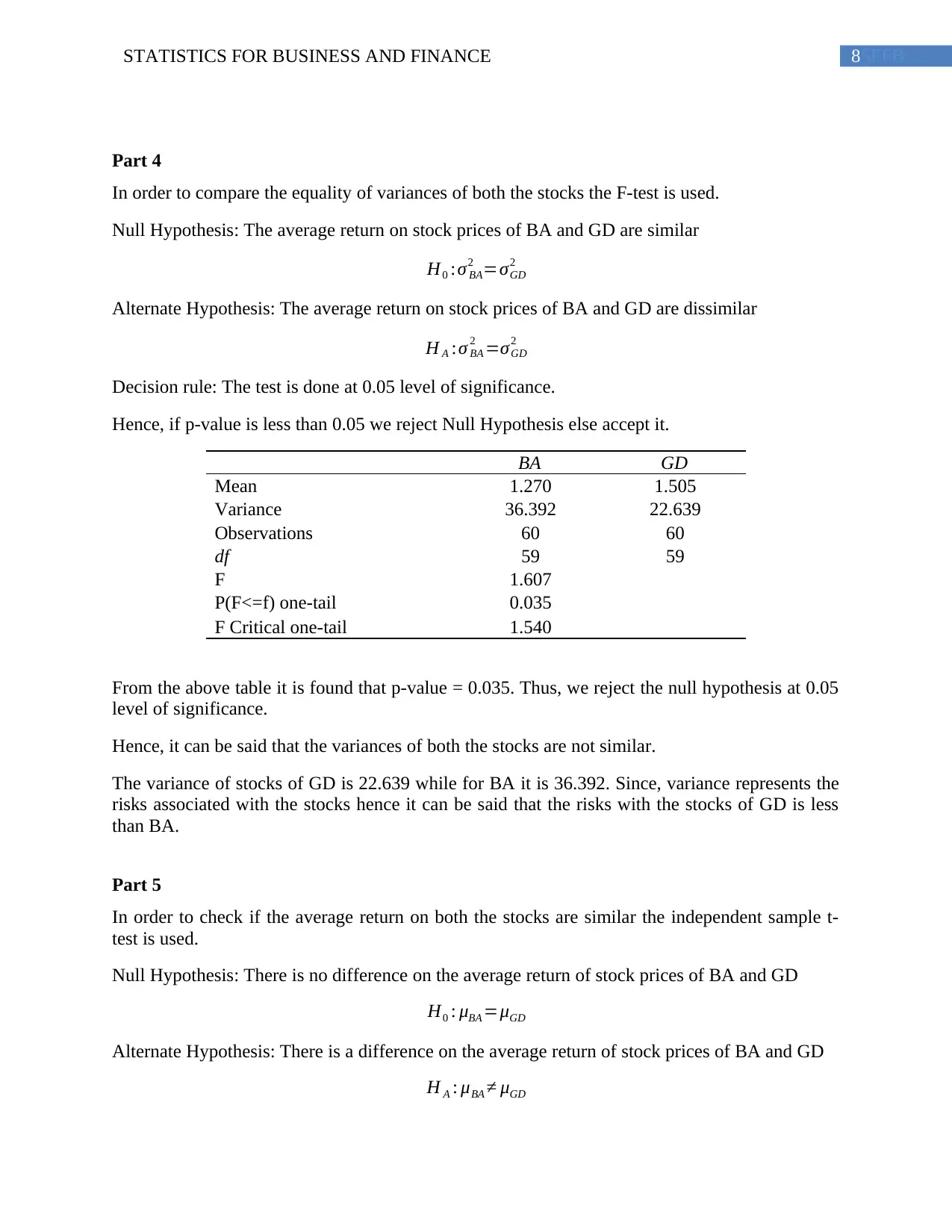

Part 4

In order to compare the equality of variances of both the stocks the F-test is used.

Null Hypothesis: The average return on stock prices of BA and GD are similar

H0 :σ BA

2 =σGD

2

Alternate Hypothesis: The average return on stock prices of BA and GD are dissimilar

H A :σ BA

2 =σGD

2

Decision rule: The test is done at 0.05 level of significance.

Hence, if p-value is less than 0.05 we reject Null Hypothesis else accept it.

BA GD

Mean 1.270 1.505

Variance 36.392 22.639

Observations 60 60

df 59 59

F 1.607

P(F<=f) one-tail 0.035

F Critical one-tail 1.540

From the above table it is found that p-value = 0.035. Thus, we reject the null hypothesis at 0.05

level of significance.

Hence, it can be said that the variances of both the stocks are not similar.

The variance of stocks of GD is 22.639 while for BA it is 36.392. Since, variance represents the

risks associated with the stocks hence it can be said that the risks with the stocks of GD is less

than BA.

Part 5

In order to check if the average return on both the stocks are similar the independent sample t-

test is used.

Null Hypothesis: There is no difference on the average return of stock prices of BA and GD

H0 : μBA =μGD

Alternate Hypothesis: There is a difference on the average return of stock prices of BA and GD

H A : μBA ≠ μGD

Part 4

In order to compare the equality of variances of both the stocks the F-test is used.

Null Hypothesis: The average return on stock prices of BA and GD are similar

H0 :σ BA

2 =σGD

2

Alternate Hypothesis: The average return on stock prices of BA and GD are dissimilar

H A :σ BA

2 =σGD

2

Decision rule: The test is done at 0.05 level of significance.

Hence, if p-value is less than 0.05 we reject Null Hypothesis else accept it.

BA GD

Mean 1.270 1.505

Variance 36.392 22.639

Observations 60 60

df 59 59

F 1.607

P(F<=f) one-tail 0.035

F Critical one-tail 1.540

From the above table it is found that p-value = 0.035. Thus, we reject the null hypothesis at 0.05

level of significance.

Hence, it can be said that the variances of both the stocks are not similar.

The variance of stocks of GD is 22.639 while for BA it is 36.392. Since, variance represents the

risks associated with the stocks hence it can be said that the risks with the stocks of GD is less

than BA.

Part 5

In order to check if the average return on both the stocks are similar the independent sample t-

test is used.

Null Hypothesis: There is no difference on the average return of stock prices of BA and GD

H0 : μBA =μGD

Alternate Hypothesis: There is a difference on the average return of stock prices of BA and GD

H A : μBA ≠ μGD

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9SFFBSTATISTICS FOR BUSINESS AND FINANCE

Decision rule: The test is done at 0.05 level of significance.

Hence, if p-value is less than 0.05 we reject Null Hypothesis else accept it.

t-Test: Two-Sample Assuming Equal Variances

BA GD

Mean 1.270 1.505

Variance 36.392 22.639

Observations 60 60

Pooled Variance 29.516

Hypothesized Mean Difference 0

df 118

t Stat -0.237

P(T<=t) one-tail 0.407

t Critical one-tail 1.658

P(T<=t) two-tail 0.813

t Critical two-tail 1.980

From the above table it is found that p-value = 0.035. Thus, we reject the null hypothesis at 0.05

level of significance.

Hence, it can be said that the average return on the stock prices of BA and GD are not similar.

The average return on the GD is 1.505 while for BA it is 1.270. Since, the average return for GD

is higher than BA’s and moreover the variance of GD’s is less than BA hence the stock prices of

GD is found to suitable for calculating CAPM.

Part 6

For calculating CAPM the excess return and excess market return on the stock prices of GD are

considered.

Part 7

Part a

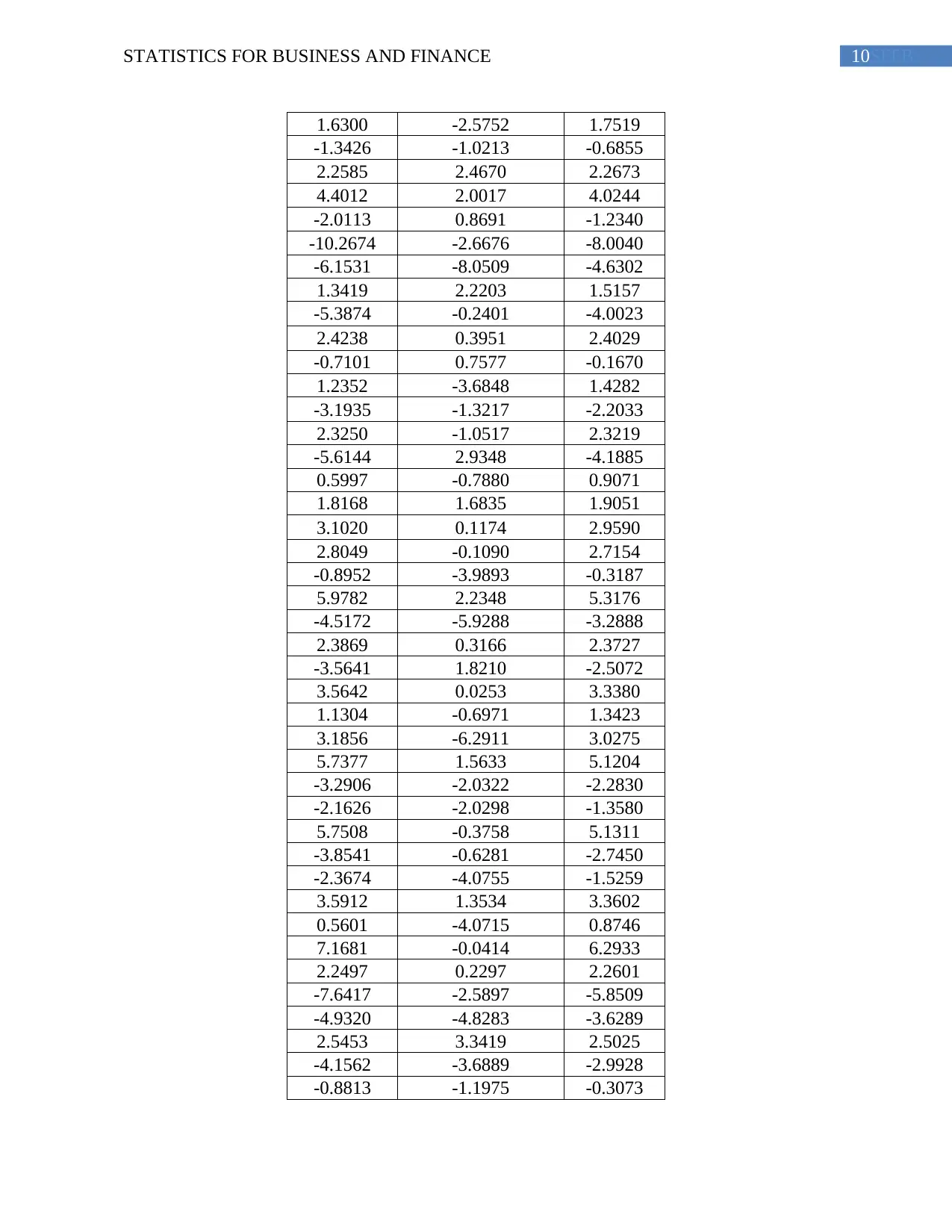

CAPM for GD is calculated from: rt −r f ,t =β0 + β1 (r M ,t −rf ,t )

Excess

Return

Excess Market

Return CAPM

r f ,t r M ,t

-8.3612 -8.0648 -6.4409

-13.8253 -9.3707 -10.9215

9.8978 8.0557 8.5316

Decision rule: The test is done at 0.05 level of significance.

Hence, if p-value is less than 0.05 we reject Null Hypothesis else accept it.

t-Test: Two-Sample Assuming Equal Variances

BA GD

Mean 1.270 1.505

Variance 36.392 22.639

Observations 60 60

Pooled Variance 29.516

Hypothesized Mean Difference 0

df 118

t Stat -0.237

P(T<=t) one-tail 0.407

t Critical one-tail 1.658

P(T<=t) two-tail 0.813

t Critical two-tail 1.980

From the above table it is found that p-value = 0.035. Thus, we reject the null hypothesis at 0.05

level of significance.

Hence, it can be said that the average return on the stock prices of BA and GD are not similar.

The average return on the GD is 1.505 while for BA it is 1.270. Since, the average return for GD

is higher than BA’s and moreover the variance of GD’s is less than BA hence the stock prices of

GD is found to suitable for calculating CAPM.

Part 6

For calculating CAPM the excess return and excess market return on the stock prices of GD are

considered.

Part 7

Part a

CAPM for GD is calculated from: rt −r f ,t =β0 + β1 (r M ,t −rf ,t )

Excess

Return

Excess Market

Return CAPM

r f ,t r M ,t

-8.3612 -8.0648 -6.4409

-13.8253 -9.3707 -10.9215

9.8978 8.0557 8.5316

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10SFFBSTATISTICS FOR BUSINESS AND FINANCE

1.6300 -2.5752 1.7519

-1.3426 -1.0213 -0.6855

2.2585 2.4670 2.2673

4.4012 2.0017 4.0244

-2.0113 0.8691 -1.2340

-10.2674 -2.6676 -8.0040

-6.1531 -8.0509 -4.6302

1.3419 2.2203 1.5157

-5.3874 -0.2401 -4.0023

2.4238 0.3951 2.4029

-0.7101 0.7577 -0.1670

1.2352 -3.6848 1.4282

-3.1935 -1.3217 -2.2033

2.3250 -1.0517 2.3219

-5.6144 2.9348 -4.1885

0.5997 -0.7880 0.9071

1.8168 1.6835 1.9051

3.1020 0.1174 2.9590

2.8049 -0.1090 2.7154

-0.8952 -3.9893 -0.3187

5.9782 2.2348 5.3176

-4.5172 -5.9288 -3.2888

2.3869 0.3166 2.3727

-3.5641 1.8210 -2.5072

3.5642 0.0253 3.3380

1.1304 -0.6971 1.3423

3.1856 -6.2911 3.0275

5.7377 1.5633 5.1204

-3.2906 -2.0322 -2.2830

-2.1626 -2.0298 -1.3580

5.7508 -0.3758 5.1311

-3.8541 -0.6281 -2.7450

-2.3674 -4.0755 -1.5259

3.5912 1.3534 3.3602

0.5601 -4.0715 0.8746

7.1681 -0.0414 6.2933

2.2497 0.2297 2.2601

-7.6417 -2.5897 -5.8509

-4.9320 -4.8283 -3.6289

2.5453 3.3419 2.5025

-4.1562 -3.6889 -2.9928

-0.8813 -1.1975 -0.3073

1.6300 -2.5752 1.7519

-1.3426 -1.0213 -0.6855

2.2585 2.4670 2.2673

4.4012 2.0017 4.0244

-2.0113 0.8691 -1.2340

-10.2674 -2.6676 -8.0040

-6.1531 -8.0509 -4.6302

1.3419 2.2203 1.5157

-5.3874 -0.2401 -4.0023

2.4238 0.3951 2.4029

-0.7101 0.7577 -0.1670

1.2352 -3.6848 1.4282

-3.1935 -1.3217 -2.2033

2.3250 -1.0517 2.3219

-5.6144 2.9348 -4.1885

0.5997 -0.7880 0.9071

1.8168 1.6835 1.9051

3.1020 0.1174 2.9590

2.8049 -0.1090 2.7154

-0.8952 -3.9893 -0.3187

5.9782 2.2348 5.3176

-4.5172 -5.9288 -3.2888

2.3869 0.3166 2.3727

-3.5641 1.8210 -2.5072

3.5642 0.0253 3.3380

1.1304 -0.6971 1.3423

3.1856 -6.2911 3.0275

5.7377 1.5633 5.1204

-3.2906 -2.0322 -2.2830

-2.1626 -2.0298 -1.3580

5.7508 -0.3758 5.1311

-3.8541 -0.6281 -2.7450

-2.3674 -4.0755 -1.5259

3.5912 1.3534 3.3602

0.5601 -4.0715 0.8746

7.1681 -0.0414 6.2933

2.2497 0.2297 2.2601

-7.6417 -2.5897 -5.8509

-4.9320 -4.8283 -3.6289

2.5453 3.3419 2.5025

-4.1562 -3.6889 -2.9928

-0.8813 -1.1975 -0.3073

11SFFBSTATISTICS FOR BUSINESS AND FINANCE

0.4645 -1.0513 0.7962

-1.2493 -4.4586 -0.6091

3.3869 -0.2500 3.1927

-4.3897 -8.6625 -3.1843

-7.1614 -4.7399 -5.4571

5.2722 5.8209 4.7386

-3.1633 -2.1675 -2.1786

-8.6837 -4.0376 -6.7054

-4.0853 -7.1378 -2.9346

0.6338 -2.1537 0.9351

-5.4480 4.6045 -4.0521

4.9142 -1.5494 4.4450

-0.2953 -0.3132 0.1732

-3.3592 -1.3969 -2.3392

4.4595 2.0410 4.0722

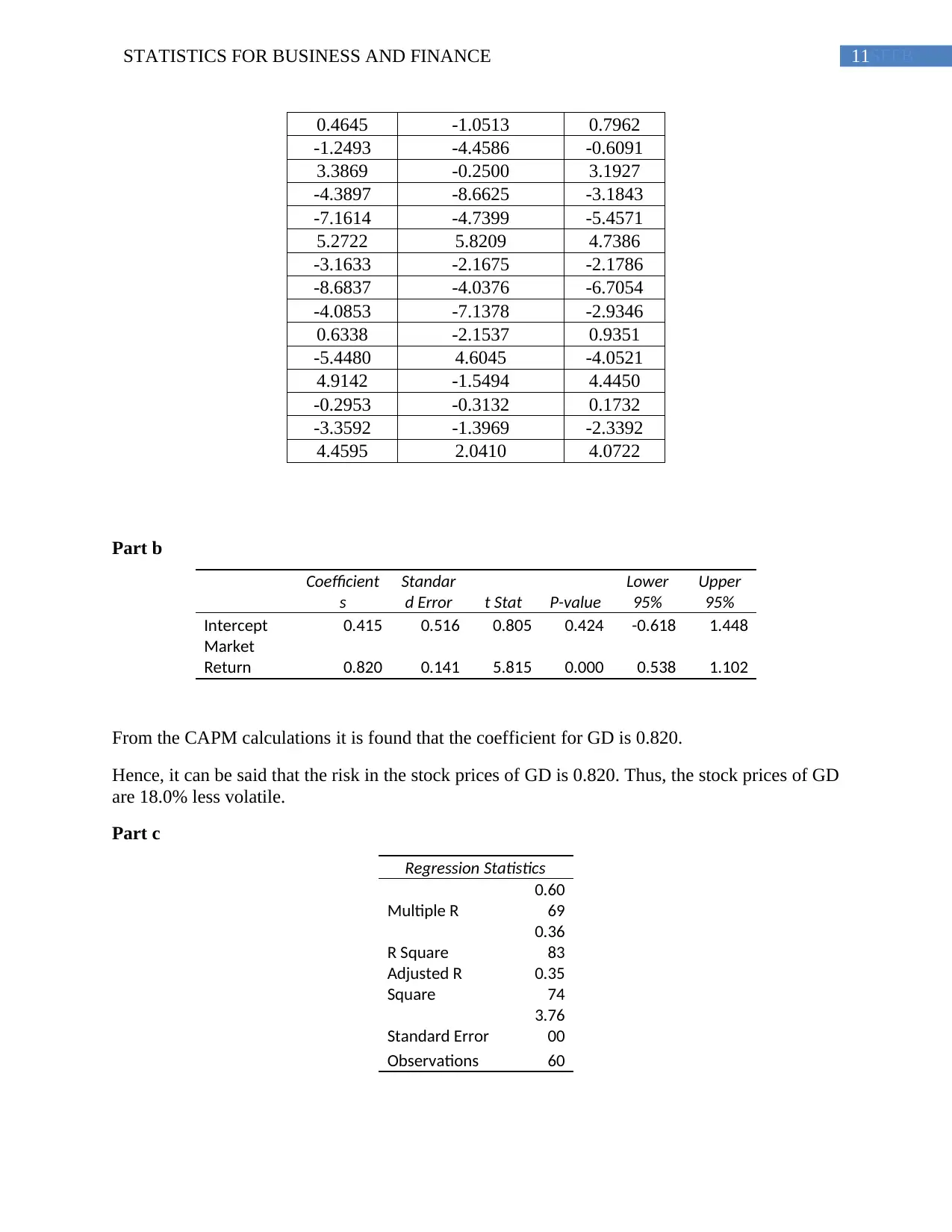

Part b

Coefficient

s

Standar

d Error t Stat P-value

Lower

95%

Upper

95%

Intercept 0.415 0.516 0.805 0.424 -0.618 1.448

Market

Return 0.820 0.141 5.815 0.000 0.538 1.102

From the CAPM calculations it is found that the coefficient for GD is 0.820.

Hence, it can be said that the risk in the stock prices of GD is 0.820. Thus, the stock prices of GD

are 18.0% less volatile.

Part c

Regression Statistics

Multiple R

0.60

69

R Square

0.36

83

Adjusted R

Square

0.35

74

Standard Error

3.76

00

Observations 60

0.4645 -1.0513 0.7962

-1.2493 -4.4586 -0.6091

3.3869 -0.2500 3.1927

-4.3897 -8.6625 -3.1843

-7.1614 -4.7399 -5.4571

5.2722 5.8209 4.7386

-3.1633 -2.1675 -2.1786

-8.6837 -4.0376 -6.7054

-4.0853 -7.1378 -2.9346

0.6338 -2.1537 0.9351

-5.4480 4.6045 -4.0521

4.9142 -1.5494 4.4450

-0.2953 -0.3132 0.1732

-3.3592 -1.3969 -2.3392

4.4595 2.0410 4.0722

Part b

Coefficient

s

Standar

d Error t Stat P-value

Lower

95%

Upper

95%

Intercept 0.415 0.516 0.805 0.424 -0.618 1.448

Market

Return 0.820 0.141 5.815 0.000 0.538 1.102

From the CAPM calculations it is found that the coefficient for GD is 0.820.

Hence, it can be said that the risk in the stock prices of GD is 0.820. Thus, the stock prices of GD

are 18.0% less volatile.

Part c

Regression Statistics

Multiple R

0.60

69

R Square

0.36

83

Adjusted R

Square

0.35

74

Standard Error

3.76

00

Observations 60

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.