FINC300: Bond Valuation, Dividend Growth, and Share Pricing Analysis

VerifiedAdded on 2023/03/23

|5

|592

|44

Homework Assignment

AI Summary

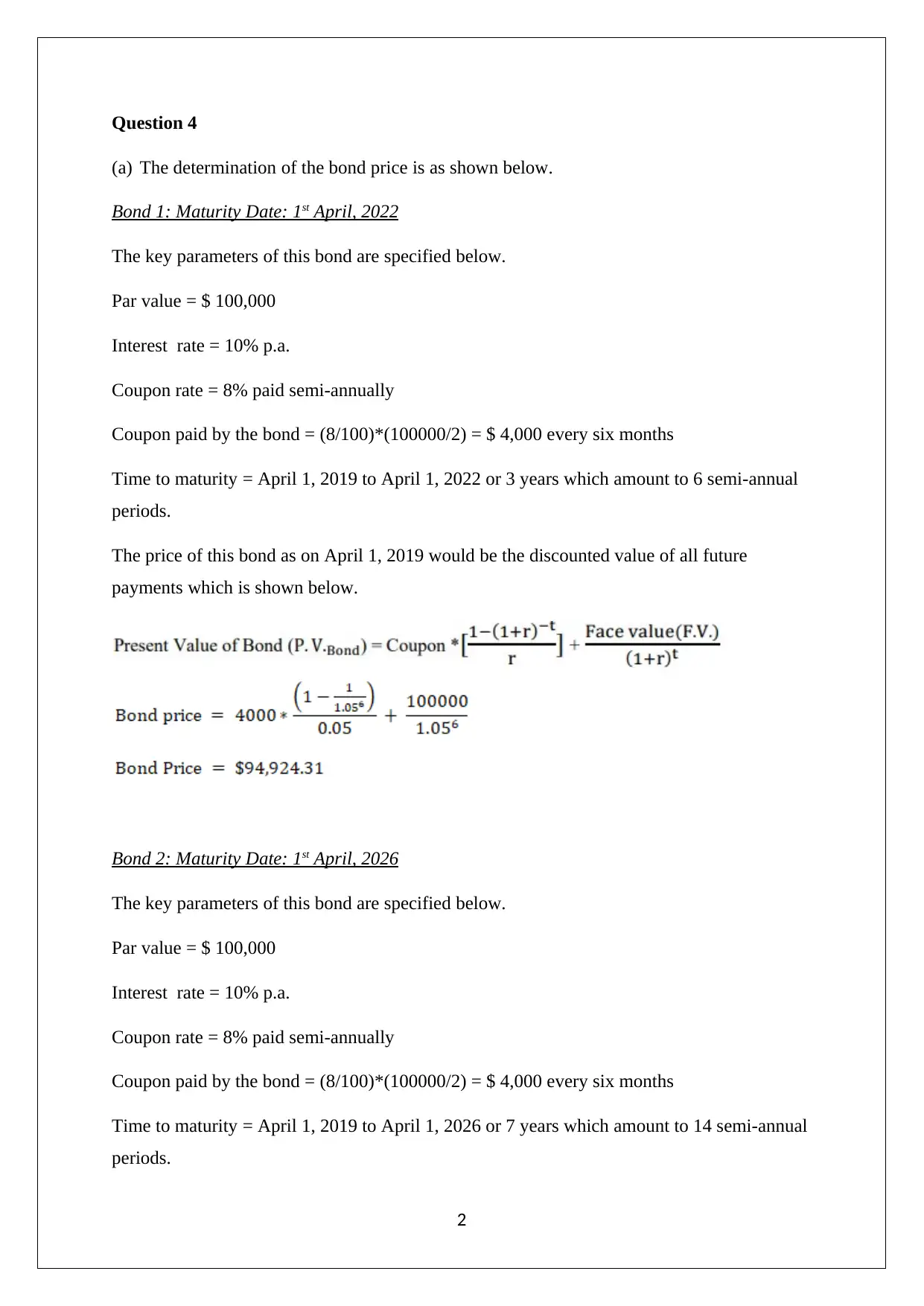

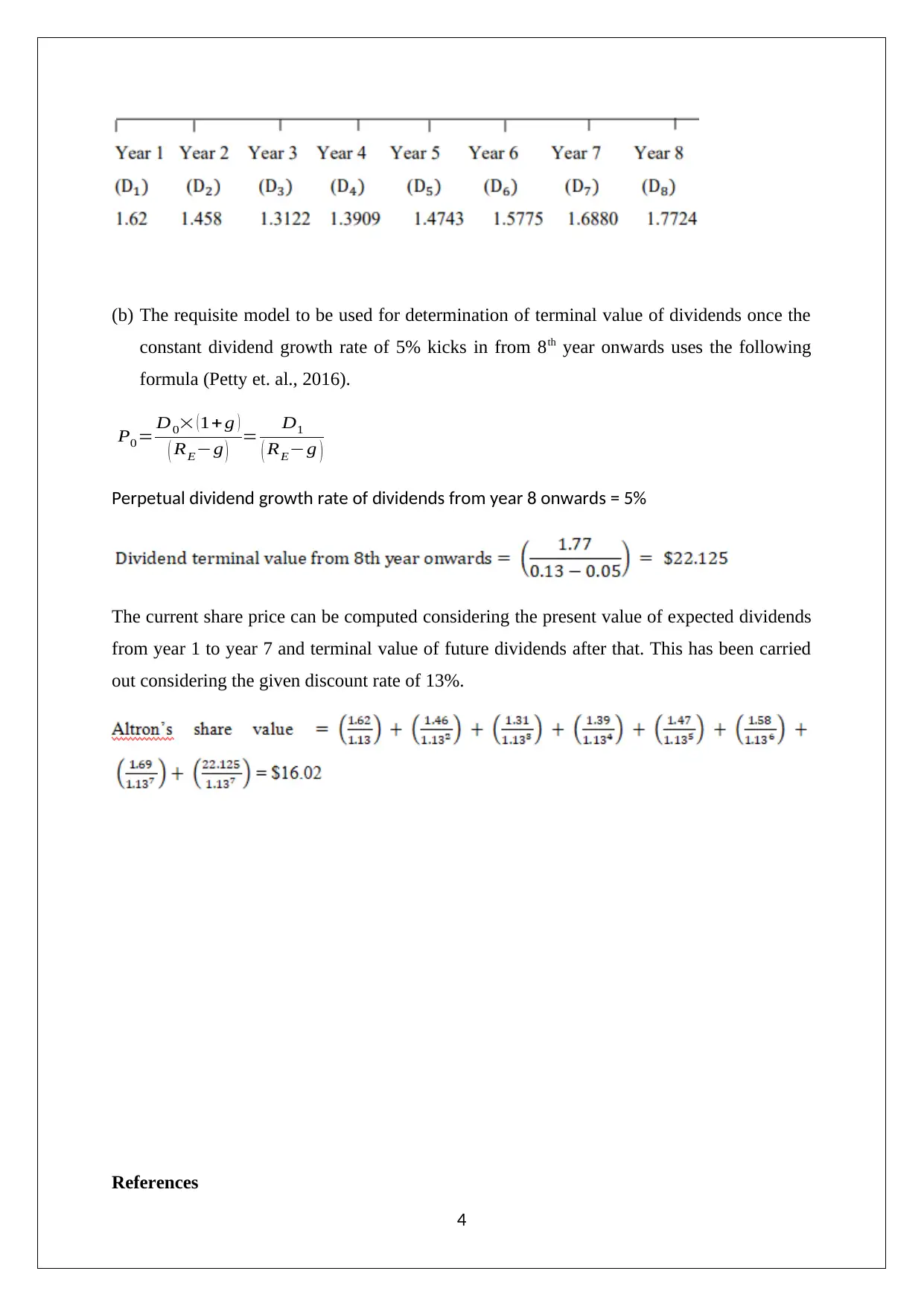

This finance assignment solution addresses two key problems: bond valuation and dividend analysis. The first question calculates the prices of two Australian Government bonds with different maturities, considering changes in market interest rates. It explains the inverse relationship between bond prices and interest rates and highlights the impact of duration on price sensitivity. The second question focuses on Altron Technology's dividend policy, requiring the creation of a timeline showing expected dividends under a fluctuating growth rate. The solution then calculates the value of Altron's share using a discounted cash flow model, incorporating the present value of dividends and a terminal value based on a constant growth rate. The solution includes detailed calculations, formulas, and references to relevant financial literature.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.