FIN715: Performance Analysis of Bond Mutual Funds: Risk and Return

VerifiedAdded on 2022/09/27

|13

|1543

|25

Report

AI Summary

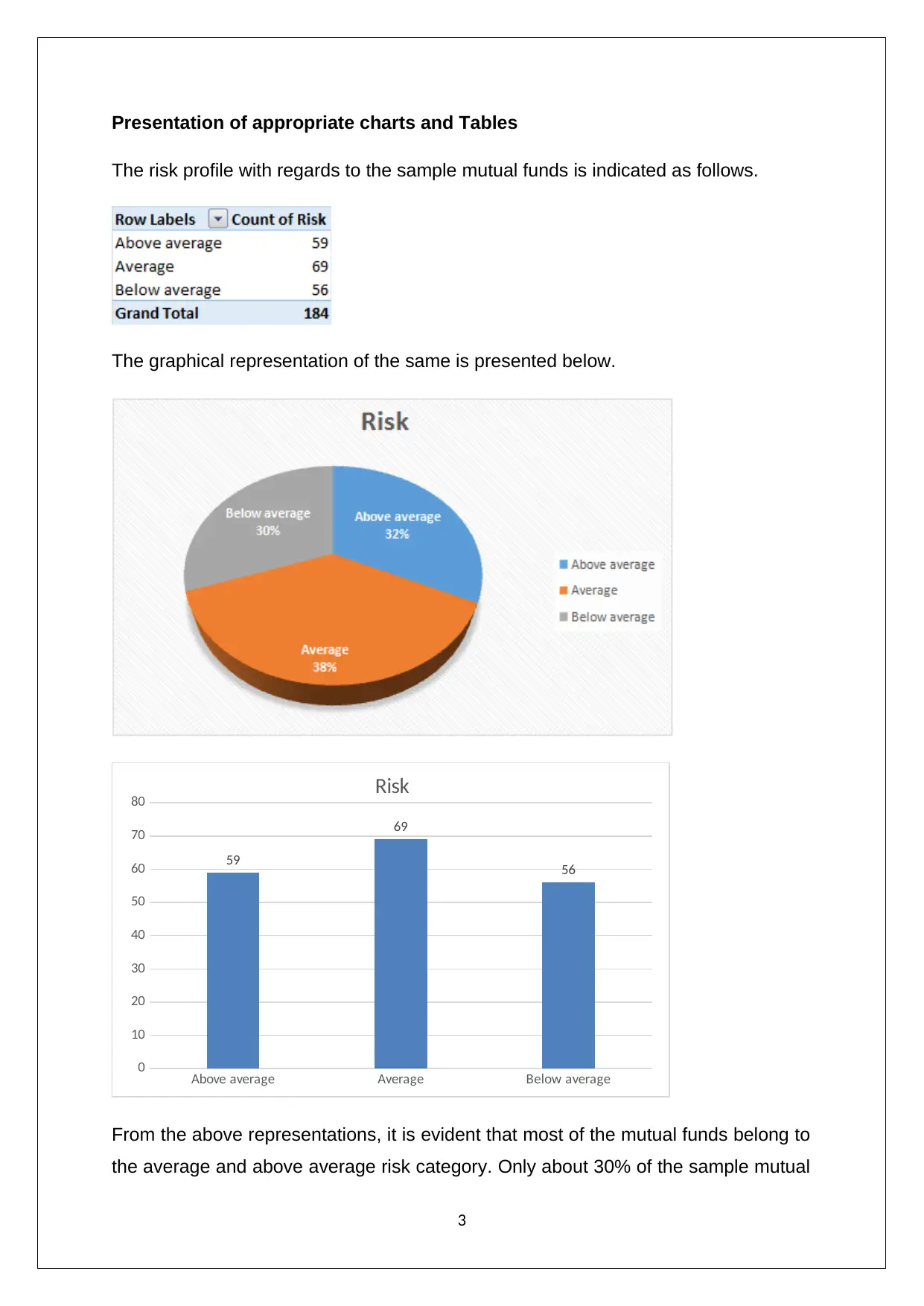

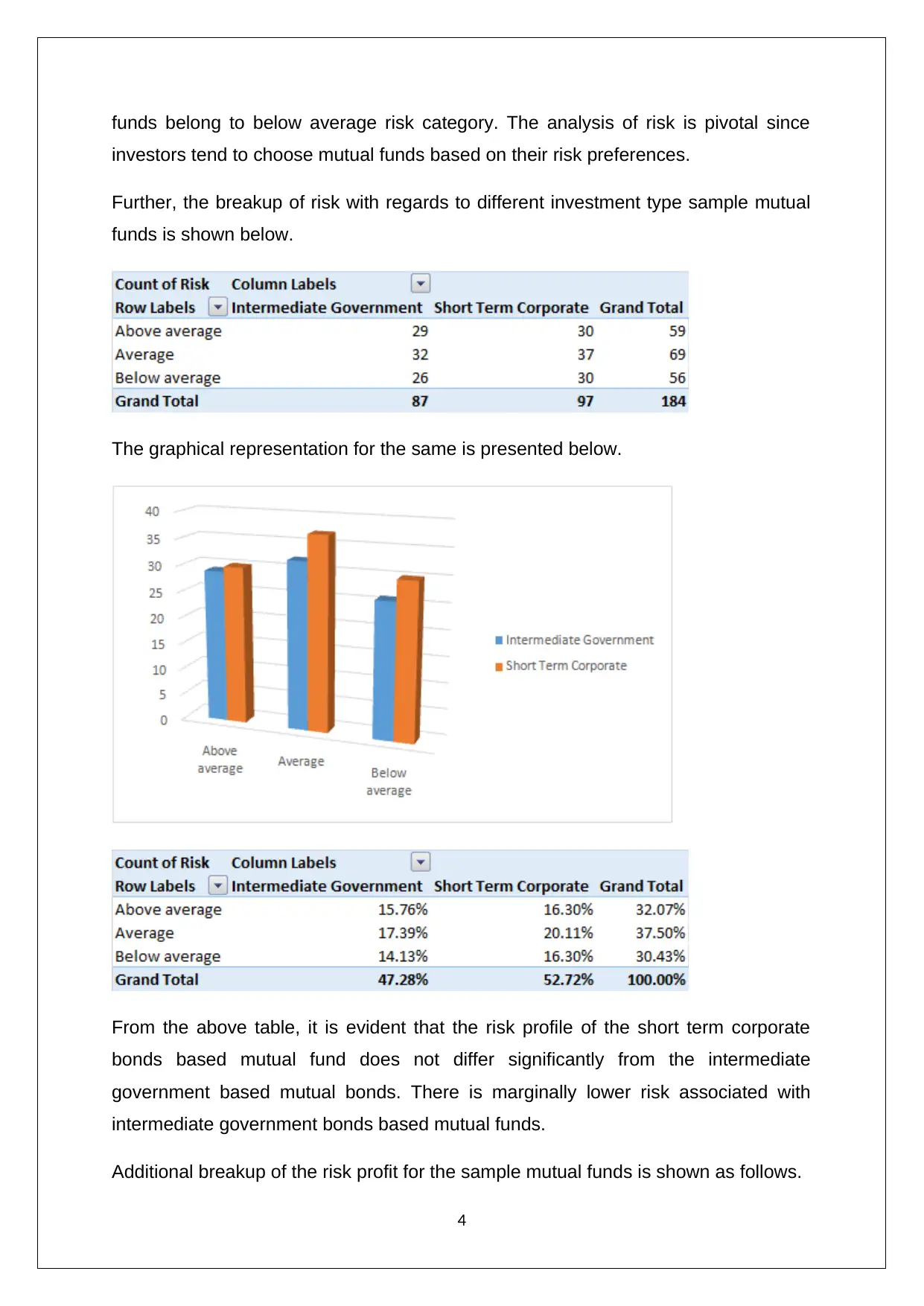

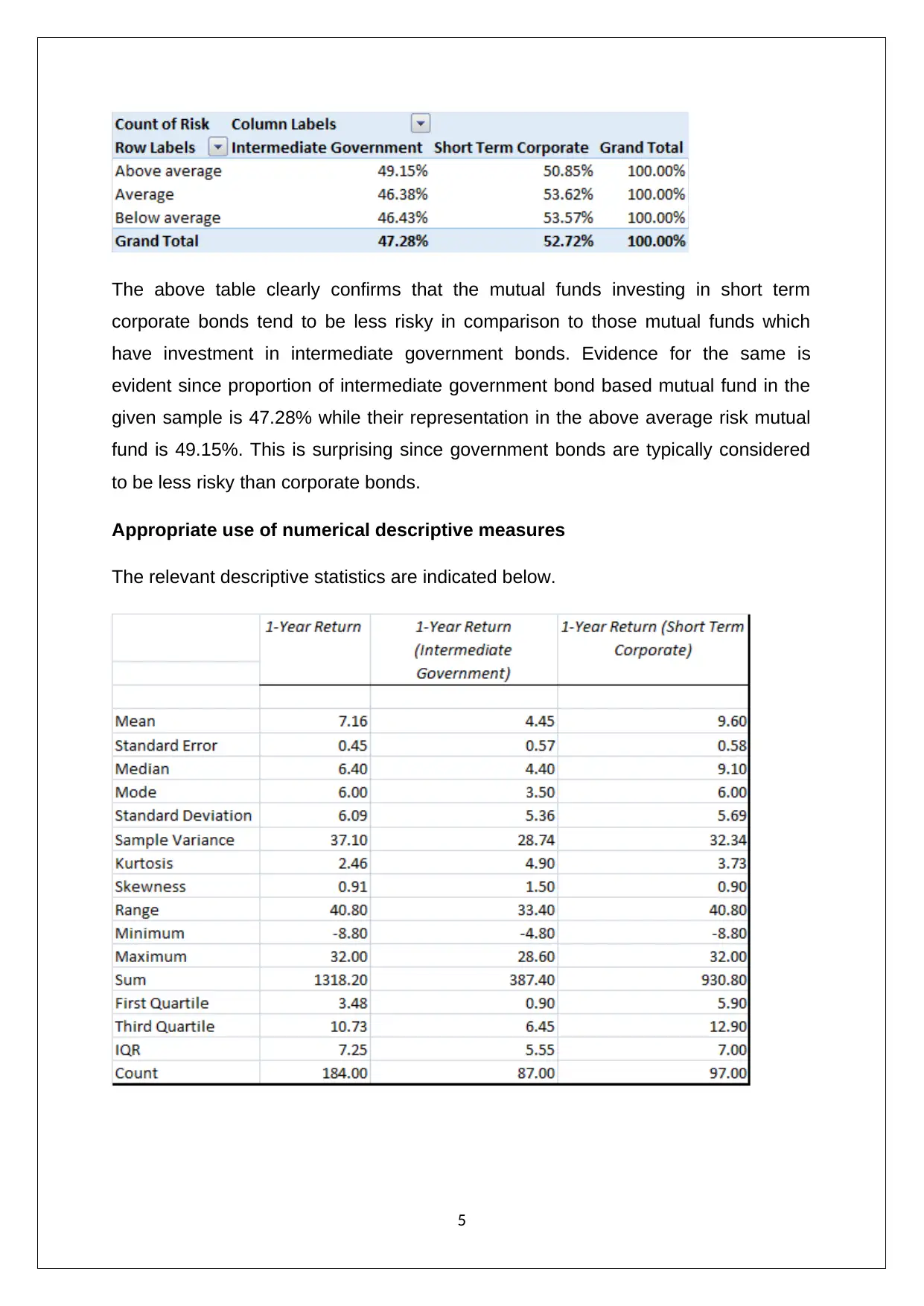

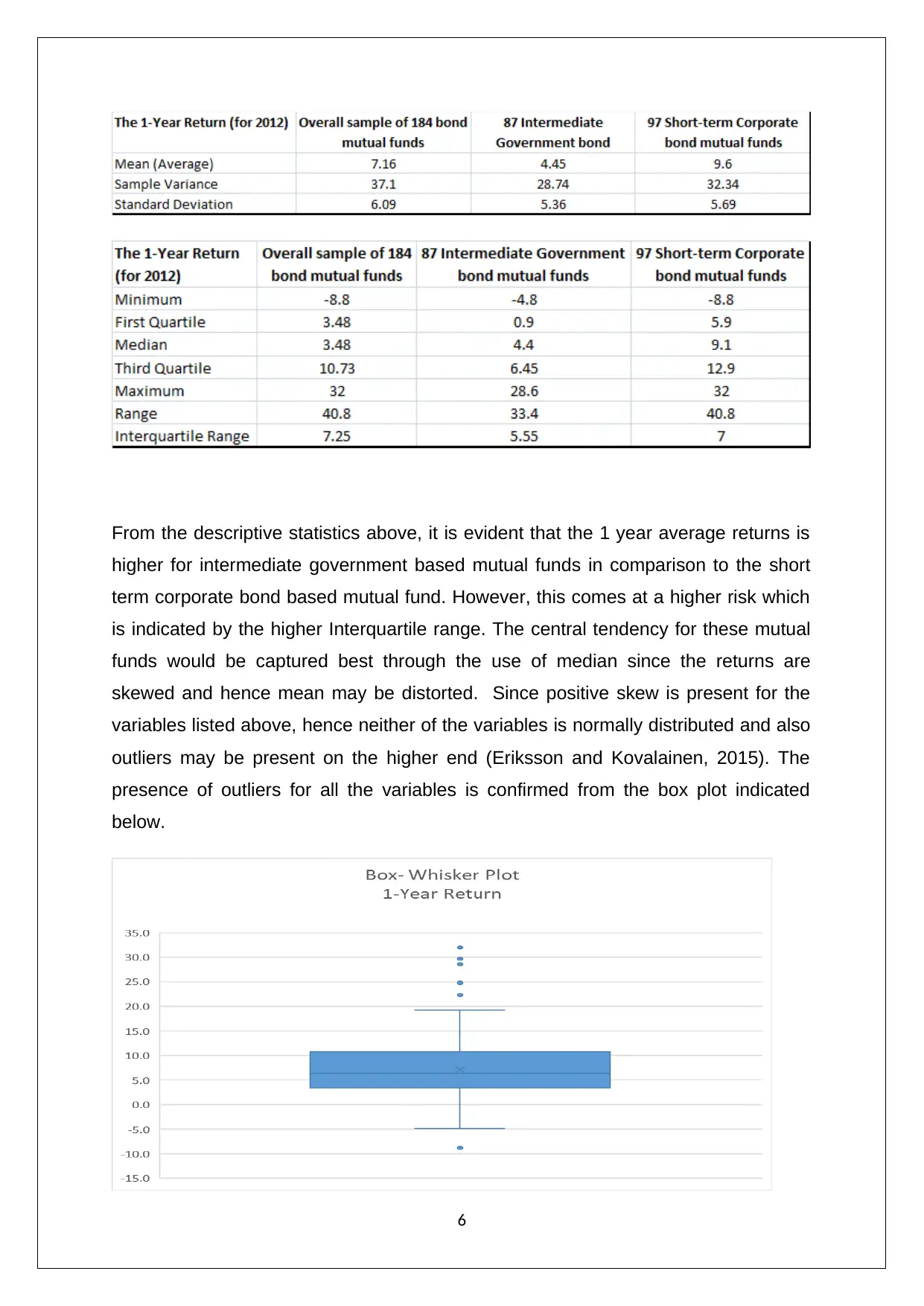

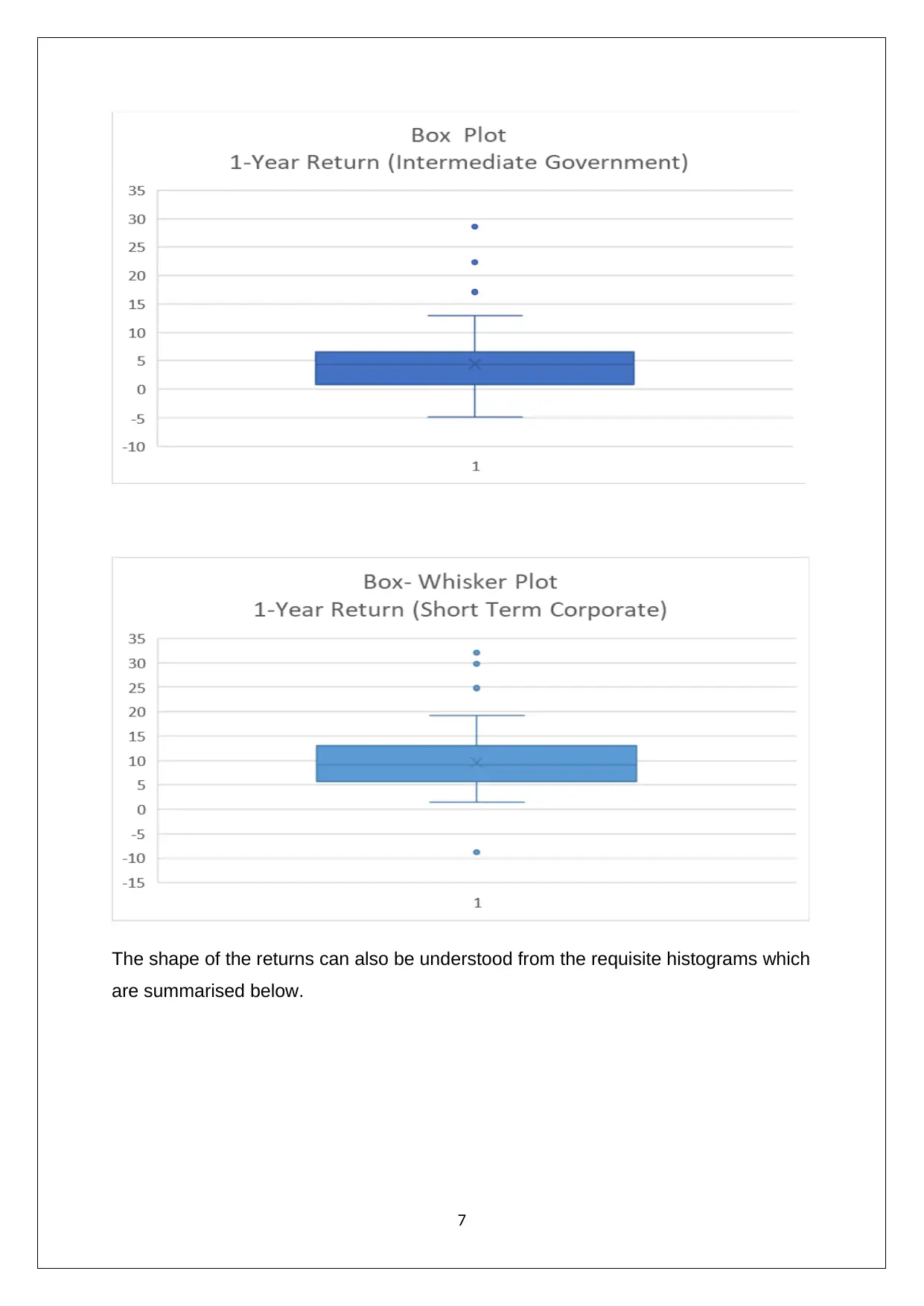

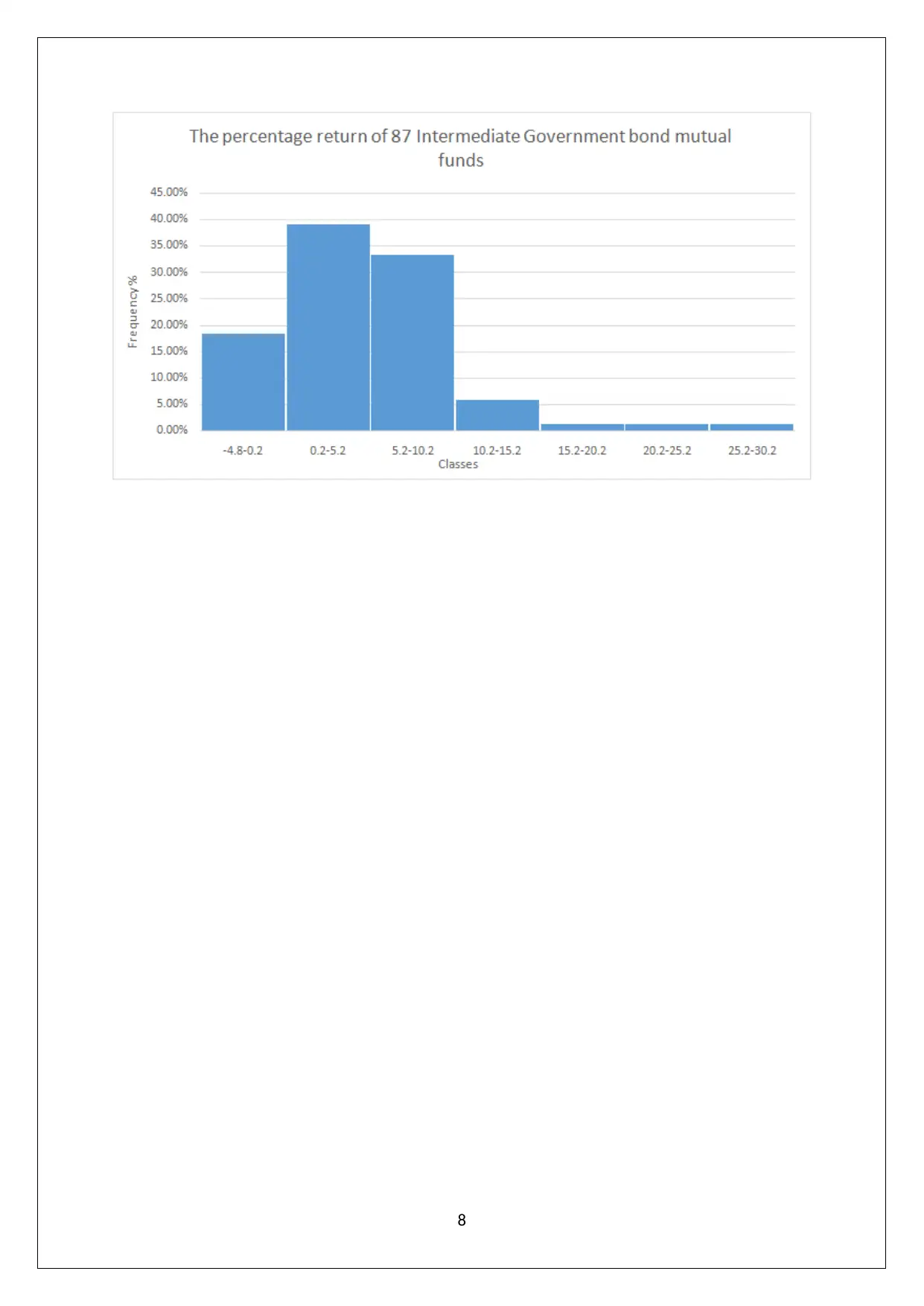

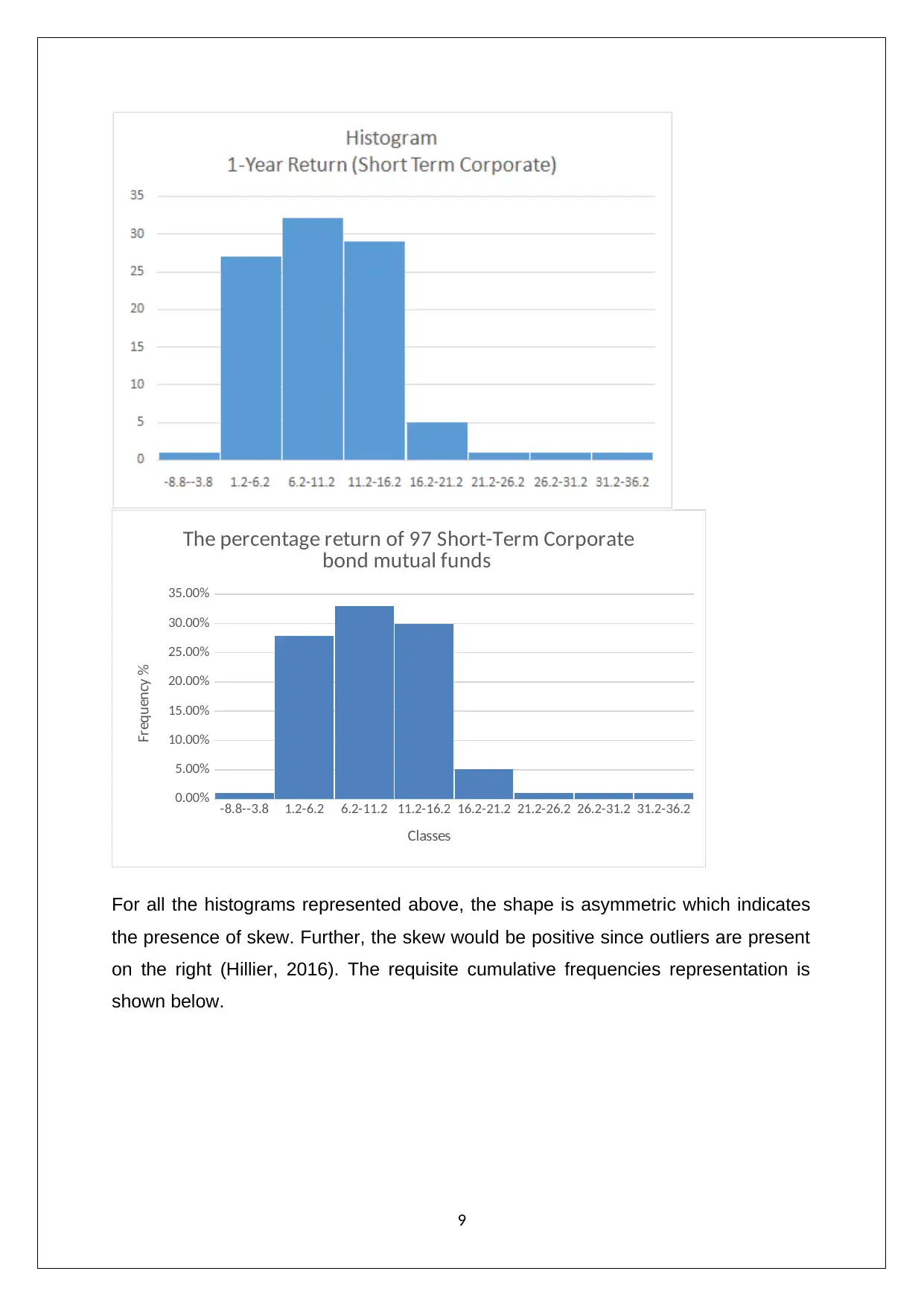

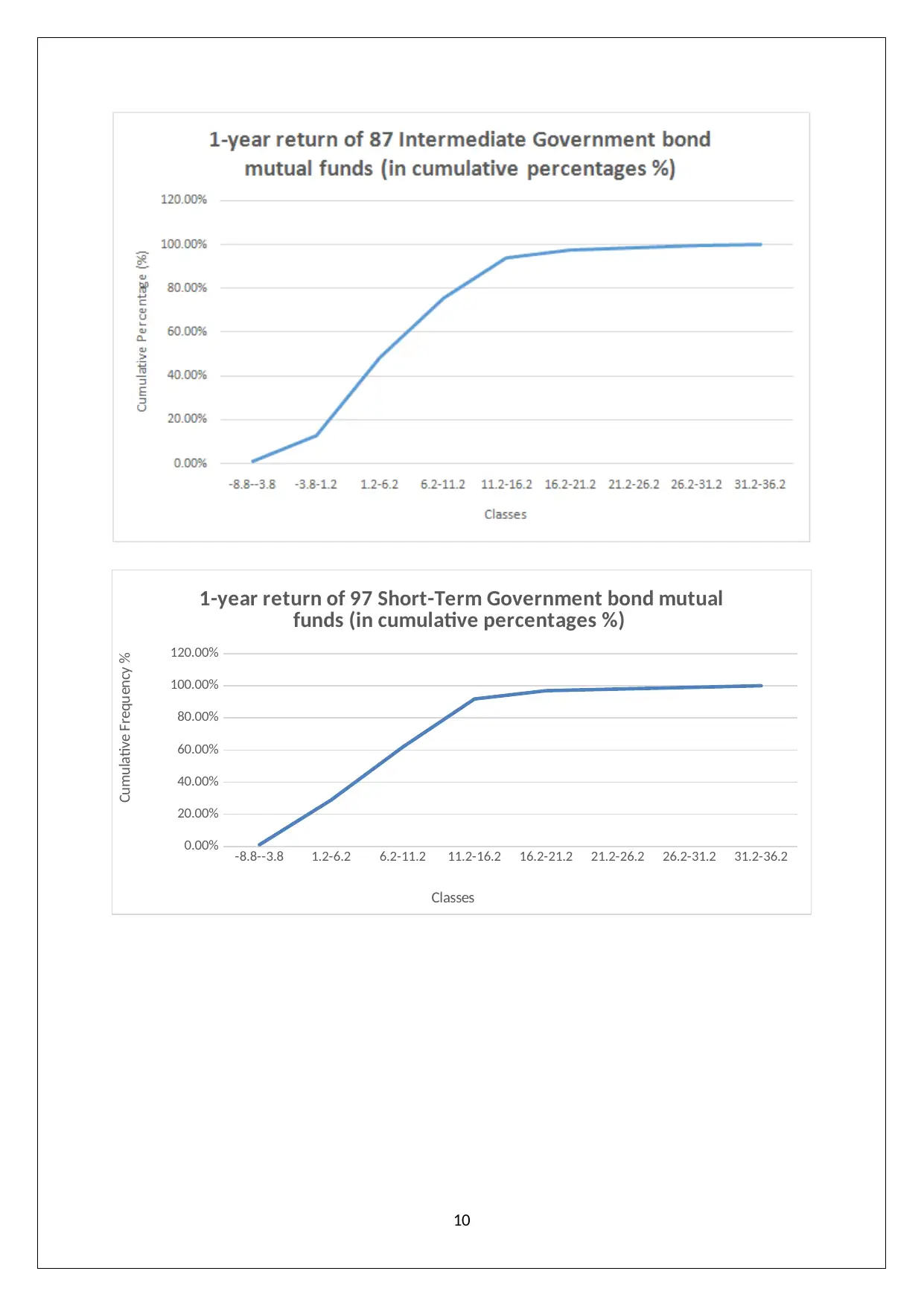

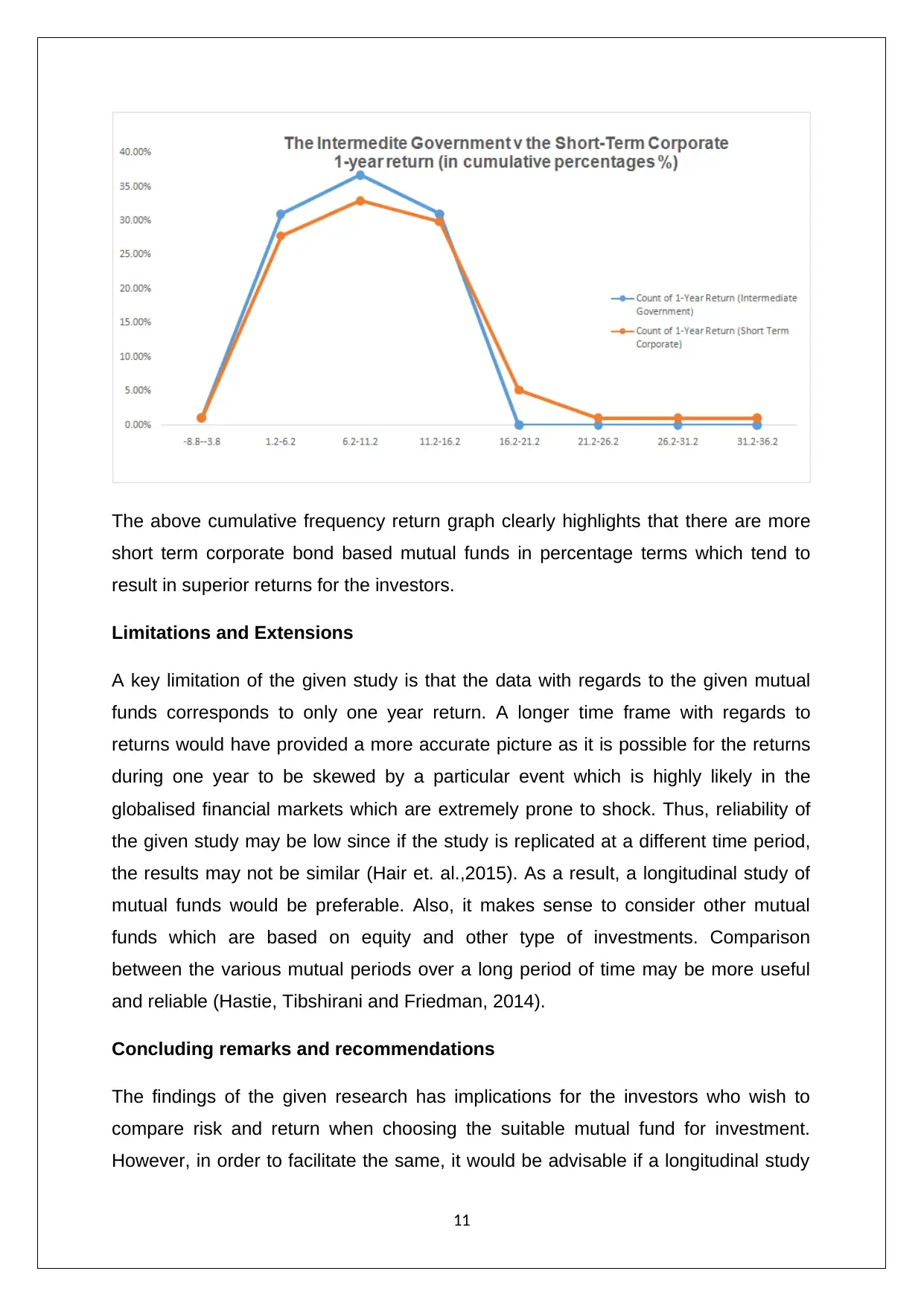

This report provides a comprehensive analysis of bond mutual funds, focusing on the performance of short-term corporate bonds versus intermediate government bonds. The study utilizes historical data from 184 mutual funds and employs descriptive statistical techniques to evaluate risk and return profiles. The report begins with an introduction to mutual funds, highlighting the importance of informed investment choices, followed by a review of relevant literature. The analysis includes the presentation of charts and tables illustrating risk profiles and the relationship between risk and investment type. The descriptive statistics, including measures of central tendency and dispersion, are used to compare the performance of different bond types. The report discusses the limitations of the study, such as the reliance on a single-year return data, and suggests potential extensions, including longitudinal studies and the inclusion of other investment types. The findings are aimed at assisting investors in making informed decisions by comparing risk and return characteristics, with recommendations for investors based on their risk appetites.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.