Bonza Handtools Ltd. Project: Profitability and Cost Analysis Report

VerifiedAdded on 2020/05/28

|8

|2391

|280

Project

AI Summary

This project analyzes the financial performance of Bonza Handtools Ltd., focusing on improving profitability through various proposals. The first part evaluates three suggestions from senior staff, including price increases, product quality enhancements, and promotional campaigns, using variance analysis to compare their impacts on profit. The second part provides cost and profit analysis under different scenarios, considering factory capacity and pricing strategies. The third part addresses overhead allocation, comparing traditional and activity-based costing methods, and calculating overhead rates. The final part elaborates on the application of activity-based costing, explaining its segmentation of overheads, identification of cost drivers, and advantages over traditional methods, using Toyota as an example. The project provides a comprehensive overview of financial analysis, cost management, and strategic decision-making within a business context.

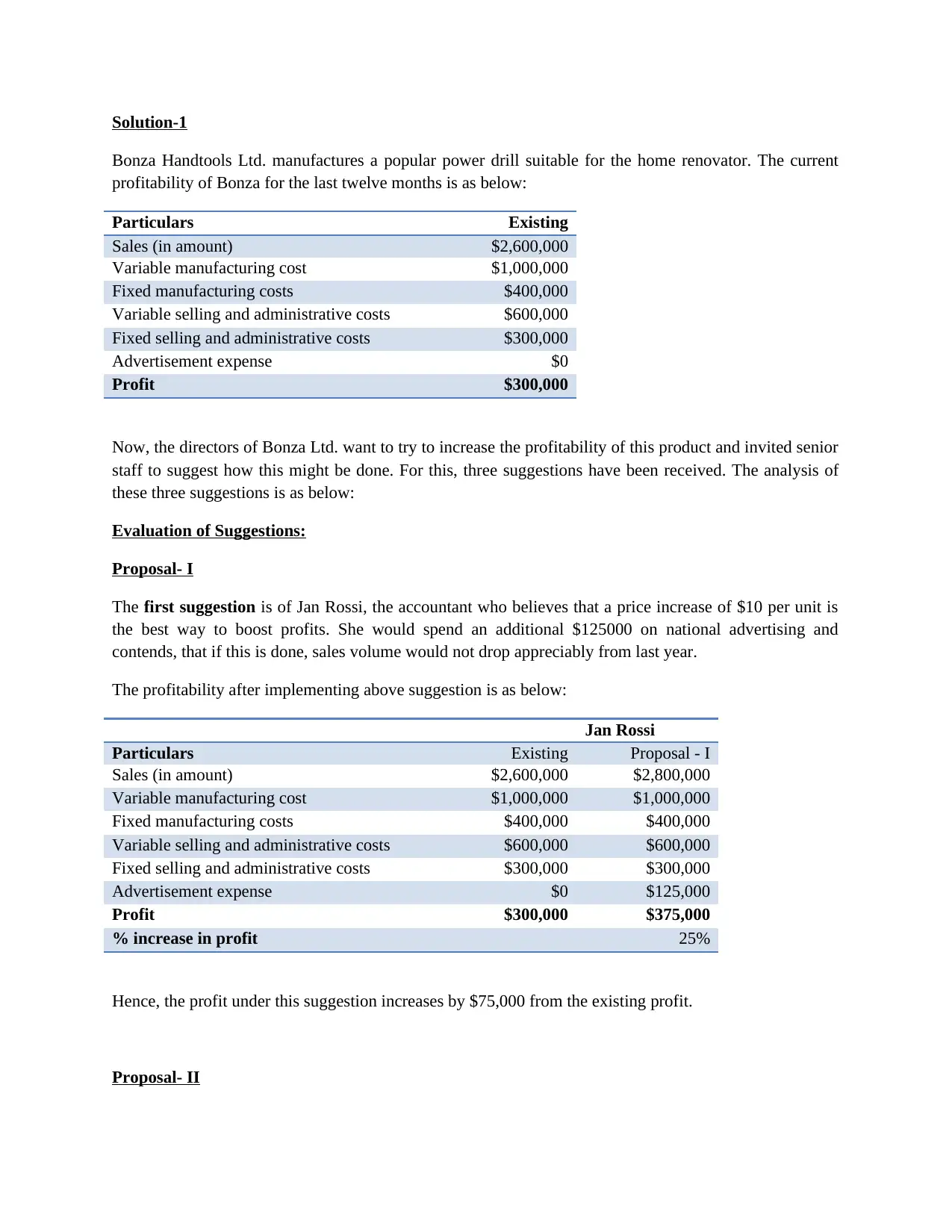

Solution-1

Bonza Handtools Ltd. manufactures a popular power drill suitable for the home renovator. The current

profitability of Bonza for the last twelve months is as below:

Particulars Existing

Sales (in amount) $2,600,000

Variable manufacturing cost $1,000,000

Fixed manufacturing costs $400,000

Variable selling and administrative costs $600,000

Fixed selling and administrative costs $300,000

Advertisement expense $0

Profit $300,000

Now, the directors of Bonza Ltd. want to try to increase the profitability of this product and invited senior

staff to suggest how this might be done. For this, three suggestions have been received. The analysis of

these three suggestions is as below:

Evaluation of Suggestions:

Proposal- I

The first suggestion is of Jan Rossi, the accountant who believes that a price increase of $10 per unit is

the best way to boost profits. She would spend an additional $125000 on national advertising and

contends, that if this is done, sales volume would not drop appreciably from last year.

The profitability after implementing above suggestion is as below:

Jan Rossi

Particulars Existing Proposal - I

Sales (in amount) $2,600,000 $2,800,000

Variable manufacturing cost $1,000,000 $1,000,000

Fixed manufacturing costs $400,000 $400,000

Variable selling and administrative costs $600,000 $600,000

Fixed selling and administrative costs $300,000 $300,000

Advertisement expense $0 $125,000

Profit $300,000 $375,000

% increase in profit 25%

Hence, the profit under this suggestion increases by $75,000 from the existing profit.

Proposal- II

Bonza Handtools Ltd. manufactures a popular power drill suitable for the home renovator. The current

profitability of Bonza for the last twelve months is as below:

Particulars Existing

Sales (in amount) $2,600,000

Variable manufacturing cost $1,000,000

Fixed manufacturing costs $400,000

Variable selling and administrative costs $600,000

Fixed selling and administrative costs $300,000

Advertisement expense $0

Profit $300,000

Now, the directors of Bonza Ltd. want to try to increase the profitability of this product and invited senior

staff to suggest how this might be done. For this, three suggestions have been received. The analysis of

these three suggestions is as below:

Evaluation of Suggestions:

Proposal- I

The first suggestion is of Jan Rossi, the accountant who believes that a price increase of $10 per unit is

the best way to boost profits. She would spend an additional $125000 on national advertising and

contends, that if this is done, sales volume would not drop appreciably from last year.

The profitability after implementing above suggestion is as below:

Jan Rossi

Particulars Existing Proposal - I

Sales (in amount) $2,600,000 $2,800,000

Variable manufacturing cost $1,000,000 $1,000,000

Fixed manufacturing costs $400,000 $400,000

Variable selling and administrative costs $600,000 $600,000

Fixed selling and administrative costs $300,000 $300,000

Advertisement expense $0 $125,000

Profit $300,000 $375,000

% increase in profit 25%

Hence, the profit under this suggestion increases by $75,000 from the existing profit.

Proposal- II

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

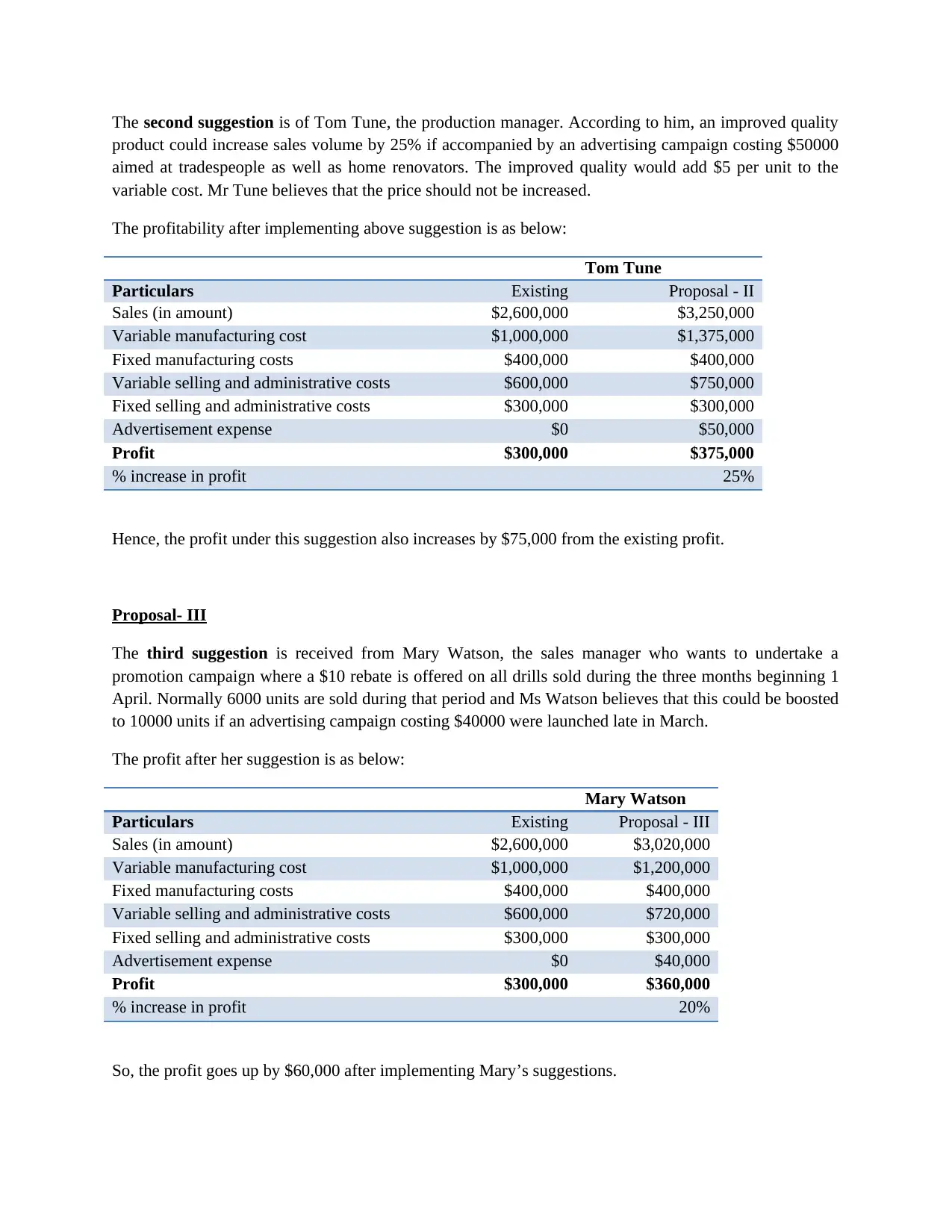

The second suggestion is of Tom Tune, the production manager. According to him, an improved quality

product could increase sales volume by 25% if accompanied by an advertising campaign costing $50000

aimed at tradespeople as well as home renovators. The improved quality would add $5 per unit to the

variable cost. Mr Tune believes that the price should not be increased.

The profitability after implementing above suggestion is as below:

Tom Tune

Particulars Existing Proposal - II

Sales (in amount) $2,600,000 $3,250,000

Variable manufacturing cost $1,000,000 $1,375,000

Fixed manufacturing costs $400,000 $400,000

Variable selling and administrative costs $600,000 $750,000

Fixed selling and administrative costs $300,000 $300,000

Advertisement expense $0 $50,000

Profit $300,000 $375,000

% increase in profit 25%

Hence, the profit under this suggestion also increases by $75,000 from the existing profit.

Proposal- III

The third suggestion is received from Mary Watson, the sales manager who wants to undertake a

promotion campaign where a $10 rebate is offered on all drills sold during the three months beginning 1

April. Normally 6000 units are sold during that period and Ms Watson believes that this could be boosted

to 10000 units if an advertising campaign costing $40000 were launched late in March.

The profit after her suggestion is as below:

Mary Watson

Particulars Existing Proposal - III

Sales (in amount) $2,600,000 $3,020,000

Variable manufacturing cost $1,000,000 $1,200,000

Fixed manufacturing costs $400,000 $400,000

Variable selling and administrative costs $600,000 $720,000

Fixed selling and administrative costs $300,000 $300,000

Advertisement expense $0 $40,000

Profit $300,000 $360,000

% increase in profit 20%

So, the profit goes up by $60,000 after implementing Mary’s suggestions.

product could increase sales volume by 25% if accompanied by an advertising campaign costing $50000

aimed at tradespeople as well as home renovators. The improved quality would add $5 per unit to the

variable cost. Mr Tune believes that the price should not be increased.

The profitability after implementing above suggestion is as below:

Tom Tune

Particulars Existing Proposal - II

Sales (in amount) $2,600,000 $3,250,000

Variable manufacturing cost $1,000,000 $1,375,000

Fixed manufacturing costs $400,000 $400,000

Variable selling and administrative costs $600,000 $750,000

Fixed selling and administrative costs $300,000 $300,000

Advertisement expense $0 $50,000

Profit $300,000 $375,000

% increase in profit 25%

Hence, the profit under this suggestion also increases by $75,000 from the existing profit.

Proposal- III

The third suggestion is received from Mary Watson, the sales manager who wants to undertake a

promotion campaign where a $10 rebate is offered on all drills sold during the three months beginning 1

April. Normally 6000 units are sold during that period and Ms Watson believes that this could be boosted

to 10000 units if an advertising campaign costing $40000 were launched late in March.

The profit after her suggestion is as below:

Mary Watson

Particulars Existing Proposal - III

Sales (in amount) $2,600,000 $3,020,000

Variable manufacturing cost $1,000,000 $1,200,000

Fixed manufacturing costs $400,000 $400,000

Variable selling and administrative costs $600,000 $720,000

Fixed selling and administrative costs $300,000 $300,000

Advertisement expense $0 $40,000

Profit $300,000 $360,000

% increase in profit 20%

So, the profit goes up by $60,000 after implementing Mary’s suggestions.

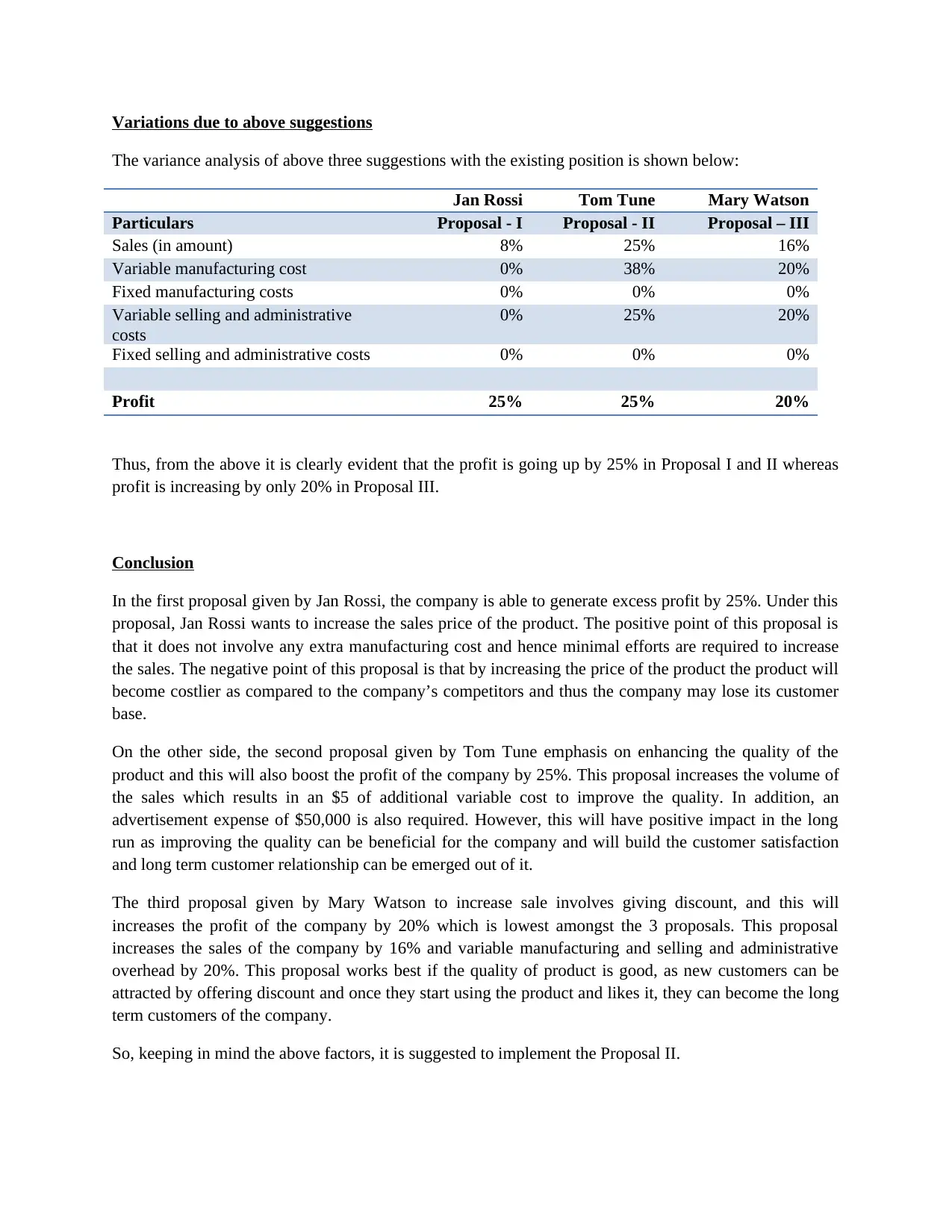

Variations due to above suggestions

The variance analysis of above three suggestions with the existing position is shown below:

Jan Rossi Tom Tune Mary Watson

Particulars Proposal - I Proposal - II Proposal – III

Sales (in amount) 8% 25% 16%

Variable manufacturing cost 0% 38% 20%

Fixed manufacturing costs 0% 0% 0%

Variable selling and administrative

costs

0% 25% 20%

Fixed selling and administrative costs 0% 0% 0%

Profit 25% 25% 20%

Thus, from the above it is clearly evident that the profit is going up by 25% in Proposal I and II whereas

profit is increasing by only 20% in Proposal III.

Conclusion

In the first proposal given by Jan Rossi, the company is able to generate excess profit by 25%. Under this

proposal, Jan Rossi wants to increase the sales price of the product. The positive point of this proposal is

that it does not involve any extra manufacturing cost and hence minimal efforts are required to increase

the sales. The negative point of this proposal is that by increasing the price of the product the product will

become costlier as compared to the company’s competitors and thus the company may lose its customer

base.

On the other side, the second proposal given by Tom Tune emphasis on enhancing the quality of the

product and this will also boost the profit of the company by 25%. This proposal increases the volume of

the sales which results in an $5 of additional variable cost to improve the quality. In addition, an

advertisement expense of $50,000 is also required. However, this will have positive impact in the long

run as improving the quality can be beneficial for the company and will build the customer satisfaction

and long term customer relationship can be emerged out of it.

The third proposal given by Mary Watson to increase sale involves giving discount, and this will

increases the profit of the company by 20% which is lowest amongst the 3 proposals. This proposal

increases the sales of the company by 16% and variable manufacturing and selling and administrative

overhead by 20%. This proposal works best if the quality of product is good, as new customers can be

attracted by offering discount and once they start using the product and likes it, they can become the long

term customers of the company.

So, keeping in mind the above factors, it is suggested to implement the Proposal II.

The variance analysis of above three suggestions with the existing position is shown below:

Jan Rossi Tom Tune Mary Watson

Particulars Proposal - I Proposal - II Proposal – III

Sales (in amount) 8% 25% 16%

Variable manufacturing cost 0% 38% 20%

Fixed manufacturing costs 0% 0% 0%

Variable selling and administrative

costs

0% 25% 20%

Fixed selling and administrative costs 0% 0% 0%

Profit 25% 25% 20%

Thus, from the above it is clearly evident that the profit is going up by 25% in Proposal I and II whereas

profit is increasing by only 20% in Proposal III.

Conclusion

In the first proposal given by Jan Rossi, the company is able to generate excess profit by 25%. Under this

proposal, Jan Rossi wants to increase the sales price of the product. The positive point of this proposal is

that it does not involve any extra manufacturing cost and hence minimal efforts are required to increase

the sales. The negative point of this proposal is that by increasing the price of the product the product will

become costlier as compared to the company’s competitors and thus the company may lose its customer

base.

On the other side, the second proposal given by Tom Tune emphasis on enhancing the quality of the

product and this will also boost the profit of the company by 25%. This proposal increases the volume of

the sales which results in an $5 of additional variable cost to improve the quality. In addition, an

advertisement expense of $50,000 is also required. However, this will have positive impact in the long

run as improving the quality can be beneficial for the company and will build the customer satisfaction

and long term customer relationship can be emerged out of it.

The third proposal given by Mary Watson to increase sale involves giving discount, and this will

increases the profit of the company by 20% which is lowest amongst the 3 proposals. This proposal

increases the sales of the company by 16% and variable manufacturing and selling and administrative

overhead by 20%. This proposal works best if the quality of product is good, as new customers can be

attracted by offering discount and once they start using the product and likes it, they can become the long

term customers of the company.

So, keeping in mind the above factors, it is suggested to implement the Proposal II.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

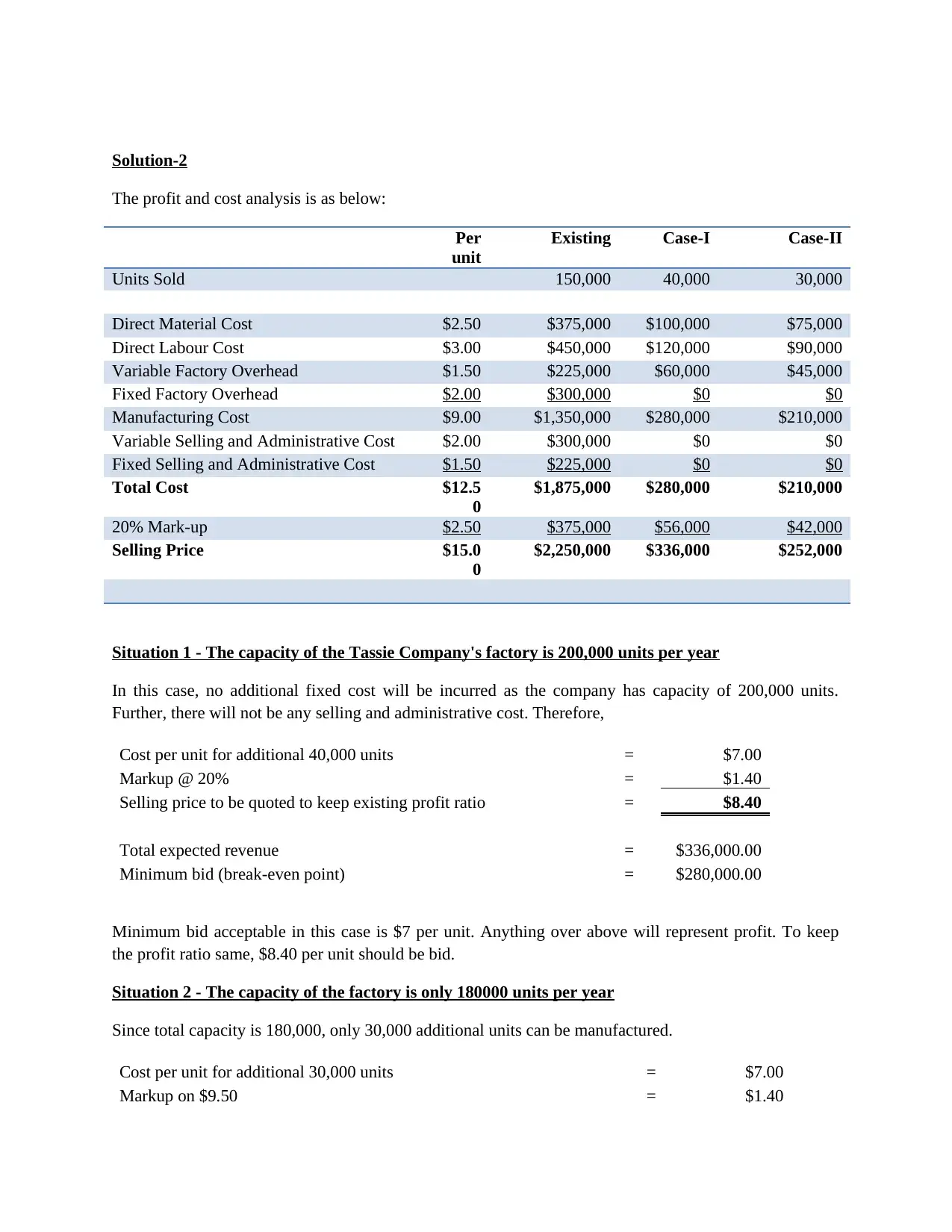

Solution-2

The profit and cost analysis is as below:

Per

unit

Existing Case-I Case-II

Units Sold 150,000 40,000 30,000

Direct Material Cost $2.50 $375,000 $100,000 $75,000

Direct Labour Cost $3.00 $450,000 $120,000 $90,000

Variable Factory Overhead $1.50 $225,000 $60,000 $45,000

Fixed Factory Overhead $2.00 $300,000 $0 $0

Manufacturing Cost $9.00 $1,350,000 $280,000 $210,000

Variable Selling and Administrative Cost $2.00 $300,000 $0 $0

Fixed Selling and Administrative Cost $1.50 $225,000 $0 $0

Total Cost $12.5

0

$1,875,000 $280,000 $210,000

20% Mark-up $2.50 $375,000 $56,000 $42,000

Selling Price $15.0

0

$2,250,000 $336,000 $252,000

Situation 1 - The capacity of the Tassie Company's factory is 200,000 units per year

In this case, no additional fixed cost will be incurred as the company has capacity of 200,000 units.

Further, there will not be any selling and administrative cost. Therefore,

Cost per unit for additional 40,000 units = $7.00

Markup @ 20% = $1.40

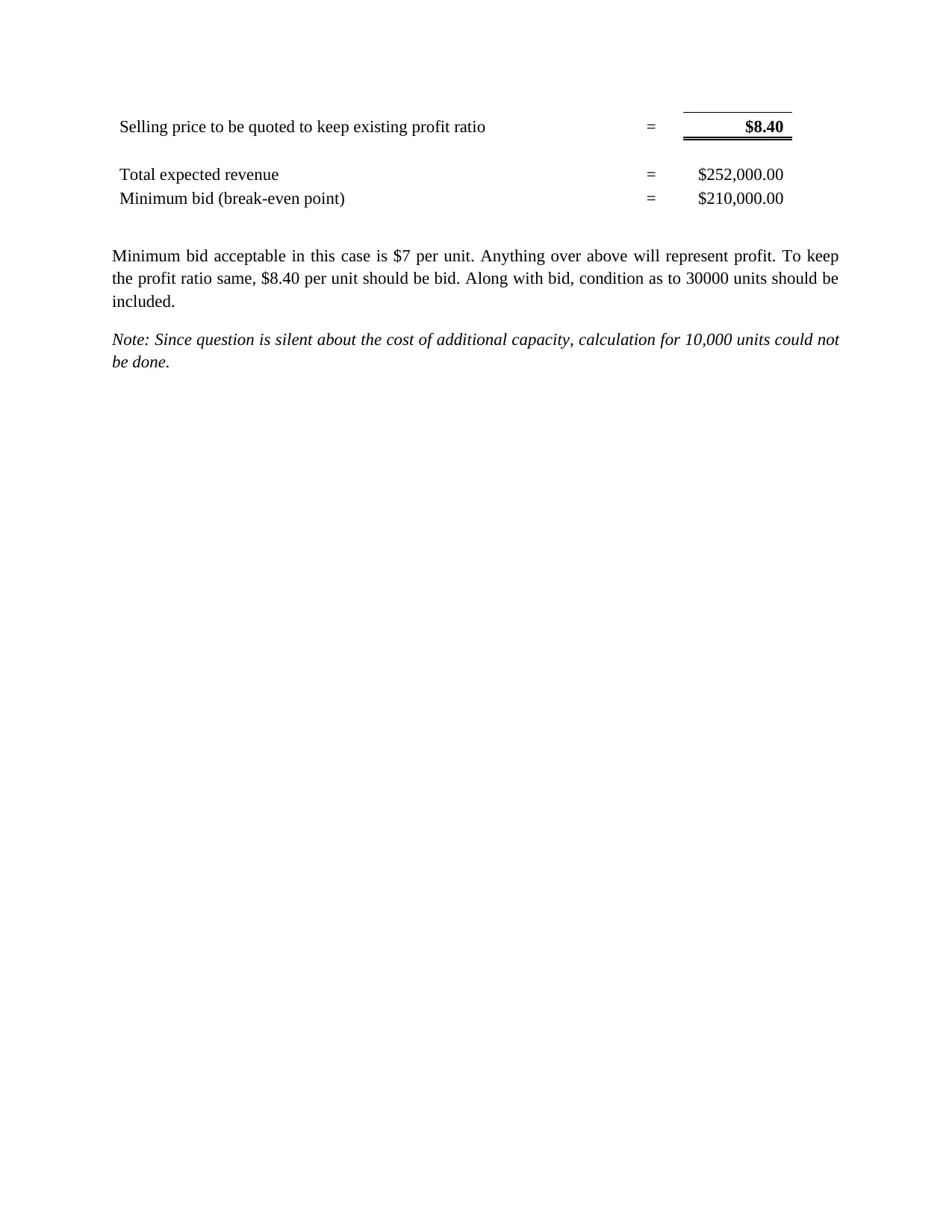

Selling price to be quoted to keep existing profit ratio = $8.40

Total expected revenue = $336,000.00

Minimum bid (break-even point) = $280,000.00

Minimum bid acceptable in this case is $7 per unit. Anything over above will represent profit. To keep

the profit ratio same, $8.40 per unit should be bid.

Situation 2 - The capacity of the factory is only 180000 units per year

Since total capacity is 180,000, only 30,000 additional units can be manufactured.

Cost per unit for additional 30,000 units = $7.00

Markup on $9.50 = $1.40

The profit and cost analysis is as below:

Per

unit

Existing Case-I Case-II

Units Sold 150,000 40,000 30,000

Direct Material Cost $2.50 $375,000 $100,000 $75,000

Direct Labour Cost $3.00 $450,000 $120,000 $90,000

Variable Factory Overhead $1.50 $225,000 $60,000 $45,000

Fixed Factory Overhead $2.00 $300,000 $0 $0

Manufacturing Cost $9.00 $1,350,000 $280,000 $210,000

Variable Selling and Administrative Cost $2.00 $300,000 $0 $0

Fixed Selling and Administrative Cost $1.50 $225,000 $0 $0

Total Cost $12.5

0

$1,875,000 $280,000 $210,000

20% Mark-up $2.50 $375,000 $56,000 $42,000

Selling Price $15.0

0

$2,250,000 $336,000 $252,000

Situation 1 - The capacity of the Tassie Company's factory is 200,000 units per year

In this case, no additional fixed cost will be incurred as the company has capacity of 200,000 units.

Further, there will not be any selling and administrative cost. Therefore,

Cost per unit for additional 40,000 units = $7.00

Markup @ 20% = $1.40

Selling price to be quoted to keep existing profit ratio = $8.40

Total expected revenue = $336,000.00

Minimum bid (break-even point) = $280,000.00

Minimum bid acceptable in this case is $7 per unit. Anything over above will represent profit. To keep

the profit ratio same, $8.40 per unit should be bid.

Situation 2 - The capacity of the factory is only 180000 units per year

Since total capacity is 180,000, only 30,000 additional units can be manufactured.

Cost per unit for additional 30,000 units = $7.00

Markup on $9.50 = $1.40

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Selling price to be quoted to keep existing profit ratio = $8.40

Total expected revenue = $252,000.00

Minimum bid (break-even point) = $210,000.00

Minimum bid acceptable in this case is $7 per unit. Anything over above will represent profit. To keep

the profit ratio same, $8.40 per unit should be bid. Along with bid, condition as to 30000 units should be

included.

Note: Since question is silent about the cost of additional capacity, calculation for 10,000 units could not

be done.

Total expected revenue = $252,000.00

Minimum bid (break-even point) = $210,000.00

Minimum bid acceptable in this case is $7 per unit. Anything over above will represent profit. To keep

the profit ratio same, $8.40 per unit should be bid. Along with bid, condition as to 30000 units should be

included.

Note: Since question is silent about the cost of additional capacity, calculation for 10,000 units could not

be done.

Solution-3

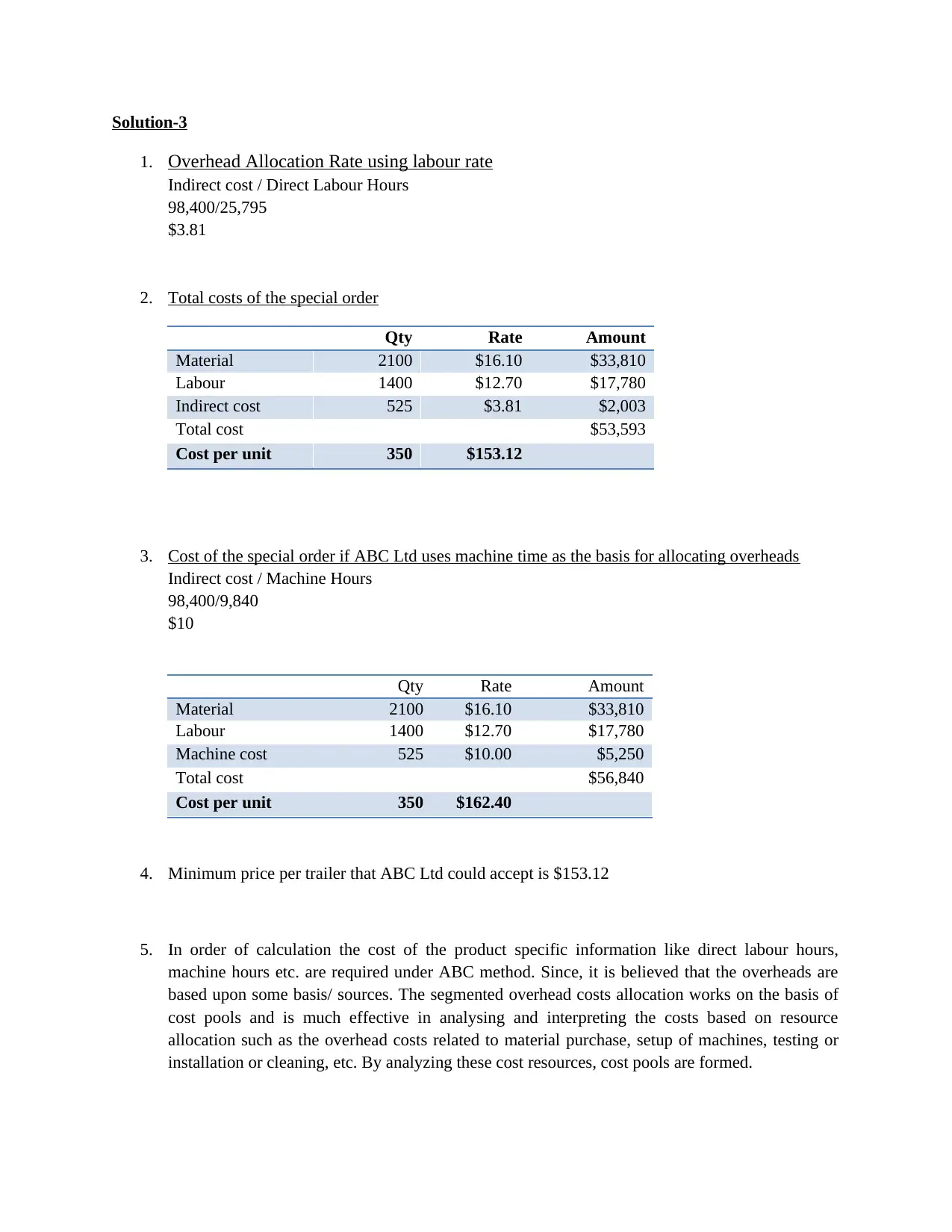

1. Overhead Allocation Rate using labour rate

Indirect cost / Direct Labour Hours

98,400/25,795

$3.81

2. Total costs of the special order

Qty Rate Amount

Material 2100 $16.10 $33,810

Labour 1400 $12.70 $17,780

Indirect cost 525 $3.81 $2,003

Total cost $53,593

Cost per unit 350 $153.12

3. Cost of the special order if ABC Ltd uses machine time as the basis for allocating overheads

Indirect cost / Machine Hours

98,400/9,840

$10

Qty Rate Amount

Material 2100 $16.10 $33,810

Labour 1400 $12.70 $17,780

Machine cost 525 $10.00 $5,250

Total cost $56,840

Cost per unit 350 $162.40

4. Minimum price per trailer that ABC Ltd could accept is $153.12

5. In order of calculation the cost of the product specific information like direct labour hours,

machine hours etc. are required under ABC method. Since, it is believed that the overheads are

based upon some basis/ sources. The segmented overhead costs allocation works on the basis of

cost pools and is much effective in analysing and interpreting the costs based on resource

allocation such as the overhead costs related to material purchase, setup of machines, testing or

installation or cleaning, etc. By analyzing these cost resources, cost pools are formed.

1. Overhead Allocation Rate using labour rate

Indirect cost / Direct Labour Hours

98,400/25,795

$3.81

2. Total costs of the special order

Qty Rate Amount

Material 2100 $16.10 $33,810

Labour 1400 $12.70 $17,780

Indirect cost 525 $3.81 $2,003

Total cost $53,593

Cost per unit 350 $153.12

3. Cost of the special order if ABC Ltd uses machine time as the basis for allocating overheads

Indirect cost / Machine Hours

98,400/9,840

$10

Qty Rate Amount

Material 2100 $16.10 $33,810

Labour 1400 $12.70 $17,780

Machine cost 525 $10.00 $5,250

Total cost $56,840

Cost per unit 350 $162.40

4. Minimum price per trailer that ABC Ltd could accept is $153.12

5. In order of calculation the cost of the product specific information like direct labour hours,

machine hours etc. are required under ABC method. Since, it is believed that the overheads are

based upon some basis/ sources. The segmented overhead costs allocation works on the basis of

cost pools and is much effective in analysing and interpreting the costs based on resource

allocation such as the overhead costs related to material purchase, setup of machines, testing or

installation or cleaning, etc. By analyzing these cost resources, cost pools are formed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Afterwards, the drivers of these cost pools are identified and the costs are allocated on the basis

of these drivers.

Thus, under segmented overhead cost pool accounting, the costs are properly allocated and thus

the resultant cost per activity or cost per product computed is more accurate and reliable as it

involves allocation of cost on the basis of cost pools and cost drivers. For example, the cost of

packaging is a cost pool and the number of products packed is the cost driver. Thus, the cost per

product is allocated by dividing the total packaging costs with the total number of products

packed. Thus, activity based costing is more reliable and provide accurate results.

Solution-4

Activity based costing is a cost allocation system which allocates the costs on the basis of segmenting the

overheads in the cost pools and then identifying the cost drivers. Segmenting of overheads means

dividing the overheads on the basis of their nature and then allocating these costs to the individual

products and services. The overheads are of two types, the direct overheads, like material cost and labour

costs which can be directly identified to the products and another are indirect overheads like rent, utilities

expenses, office expenses, depreciation, advertising, etc. These overheads can not be directly allocated

and they cannot be directly linked to products. Thus, some cost allocation basis is required to charge these

costs to the product and computing the total cost per unit.

So, for above overheads to be allocated to products, the activity based costing is used and for using this

method segmentation of costs are required. Under this method the overheads are segmented according to

their nature for example, costs related to packing, material cost, installation costs etc. and then their

respective cost drivers are identified. These drivers are identified basis the management experience and

the nature of overheads, for example, the driver for direct material cost is number of units of raw material

purchased, the driver for packaging cost if the number of products packed etc. This is a more accurate and

reliable method, however the cost of implementing this method is quite high. Whereas under the

traditional method or absorption costing mthod, the costs are allocated on the basis of blanket rate or

common allocation rate. This blanket rates are calculated on the basis of direct labour hours or machine

hours depending upon the nature of business. thus, all the overheads irrespective of their nature are

allocated on the basis of this rate. So, this is not an accurate method as compared to activity based

costing.

For example, the Toyato has adopted the overhead segmenting process to improve its process and reduce

the costs. The company has various type of overheads, like selling and administration overhead, legal

expenses, printing & stationery etc. The proper categorization of all these costs is of utmost priority, for

this all the costs are grouped according to their nature, for example labour costs are identified and then

they are further bifurcated between wages related to material handling, cleaning of machines, production

supplies, etc. this bifurcation is known as segmenting of overheads. After this, the cost drivers are

identified, which are number of labour hours spent on material handling, cleaning of machines, on

production supplies, etc. then, the costs identified are allocated on the basis of these labour hours spent.

Thus, the costs allocated are based on a reasonable basis and result in proper and accurate allocation.

of these drivers.

Thus, under segmented overhead cost pool accounting, the costs are properly allocated and thus

the resultant cost per activity or cost per product computed is more accurate and reliable as it

involves allocation of cost on the basis of cost pools and cost drivers. For example, the cost of

packaging is a cost pool and the number of products packed is the cost driver. Thus, the cost per

product is allocated by dividing the total packaging costs with the total number of products

packed. Thus, activity based costing is more reliable and provide accurate results.

Solution-4

Activity based costing is a cost allocation system which allocates the costs on the basis of segmenting the

overheads in the cost pools and then identifying the cost drivers. Segmenting of overheads means

dividing the overheads on the basis of their nature and then allocating these costs to the individual

products and services. The overheads are of two types, the direct overheads, like material cost and labour

costs which can be directly identified to the products and another are indirect overheads like rent, utilities

expenses, office expenses, depreciation, advertising, etc. These overheads can not be directly allocated

and they cannot be directly linked to products. Thus, some cost allocation basis is required to charge these

costs to the product and computing the total cost per unit.

So, for above overheads to be allocated to products, the activity based costing is used and for using this

method segmentation of costs are required. Under this method the overheads are segmented according to

their nature for example, costs related to packing, material cost, installation costs etc. and then their

respective cost drivers are identified. These drivers are identified basis the management experience and

the nature of overheads, for example, the driver for direct material cost is number of units of raw material

purchased, the driver for packaging cost if the number of products packed etc. This is a more accurate and

reliable method, however the cost of implementing this method is quite high. Whereas under the

traditional method or absorption costing mthod, the costs are allocated on the basis of blanket rate or

common allocation rate. This blanket rates are calculated on the basis of direct labour hours or machine

hours depending upon the nature of business. thus, all the overheads irrespective of their nature are

allocated on the basis of this rate. So, this is not an accurate method as compared to activity based

costing.

For example, the Toyato has adopted the overhead segmenting process to improve its process and reduce

the costs. The company has various type of overheads, like selling and administration overhead, legal

expenses, printing & stationery etc. The proper categorization of all these costs is of utmost priority, for

this all the costs are grouped according to their nature, for example labour costs are identified and then

they are further bifurcated between wages related to material handling, cleaning of machines, production

supplies, etc. this bifurcation is known as segmenting of overheads. After this, the cost drivers are

identified, which are number of labour hours spent on material handling, cleaning of machines, on

production supplies, etc. then, the costs identified are allocated on the basis of these labour hours spent.

Thus, the costs allocated are based on a reasonable basis and result in proper and accurate allocation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References:

1. Civilserviceindia.com. (2018). Overhead Cost and Control, Controlling Overhead Costs. [online]

Available at: https://www.civilserviceindia.com/subject/Management/notes/overhead-cost-and-

control.html [Accessed 21 Jan. 2018].

2. Bragg, S. and Bragg, S. (2018). Overhead allocation. [online] AccountingTools. Available at:

https://www.accountingtools.com/articles/2017/5/14/overhead-allocation [Accessed 21 Jan.

2018].

1. Civilserviceindia.com. (2018). Overhead Cost and Control, Controlling Overhead Costs. [online]

Available at: https://www.civilserviceindia.com/subject/Management/notes/overhead-cost-and-

control.html [Accessed 21 Jan. 2018].

2. Bragg, S. and Bragg, S. (2018). Overhead allocation. [online] AccountingTools. Available at:

https://www.accountingtools.com/articles/2017/5/14/overhead-allocation [Accessed 21 Jan.

2018].

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.