Feasibility Analysis of SSHA Project: Capital Budgeting for Booli

VerifiedAdded on 2023/06/11

|16

|2111

|210

Report

AI Summary

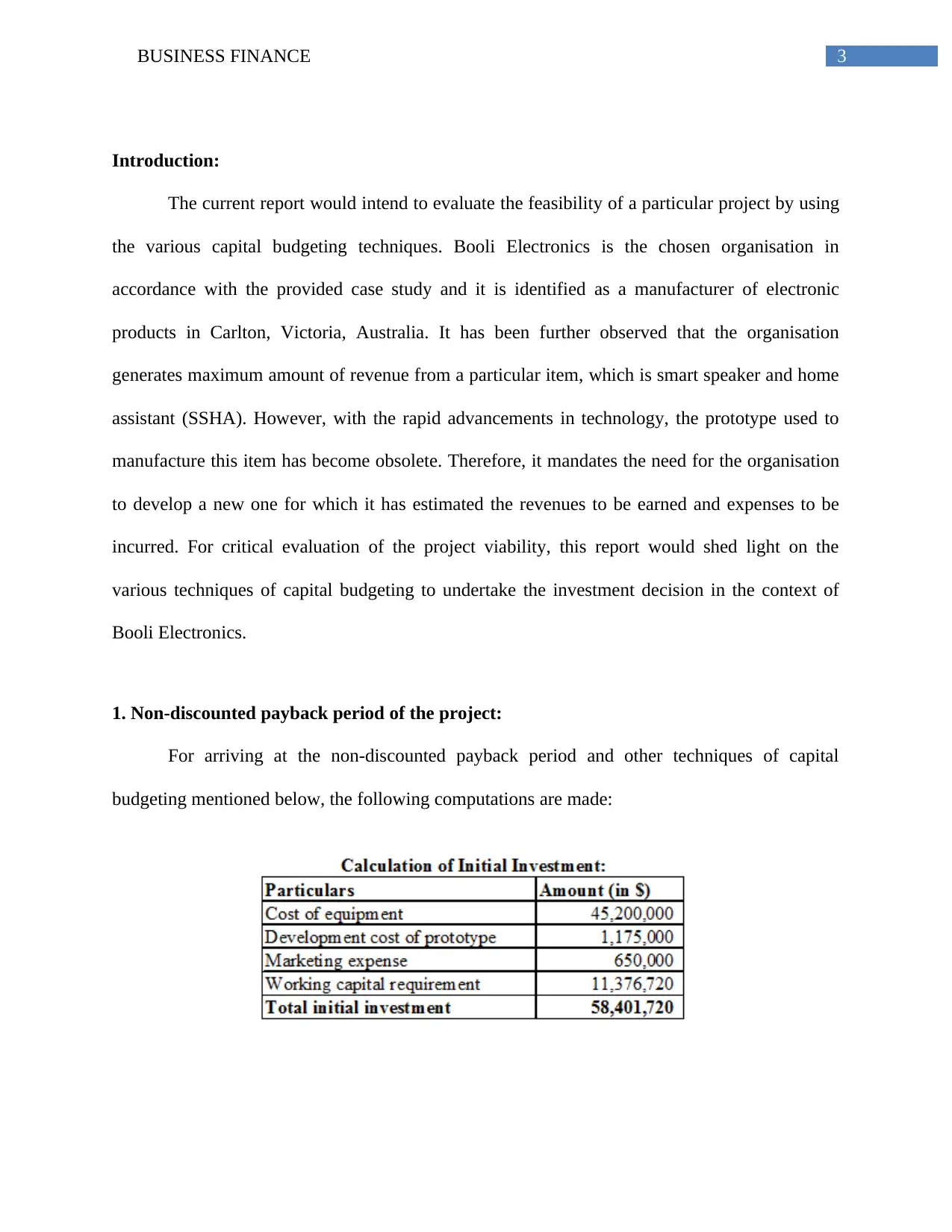

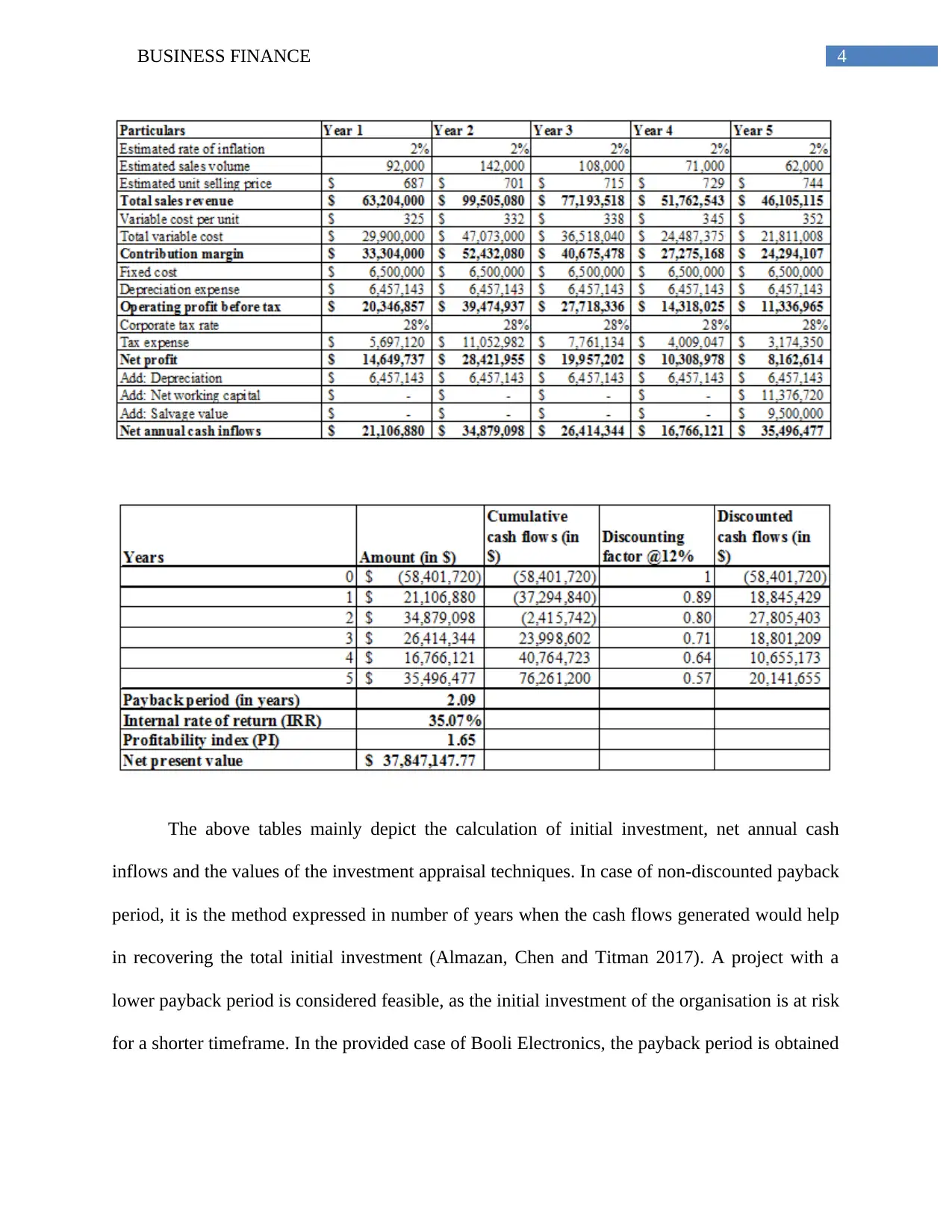

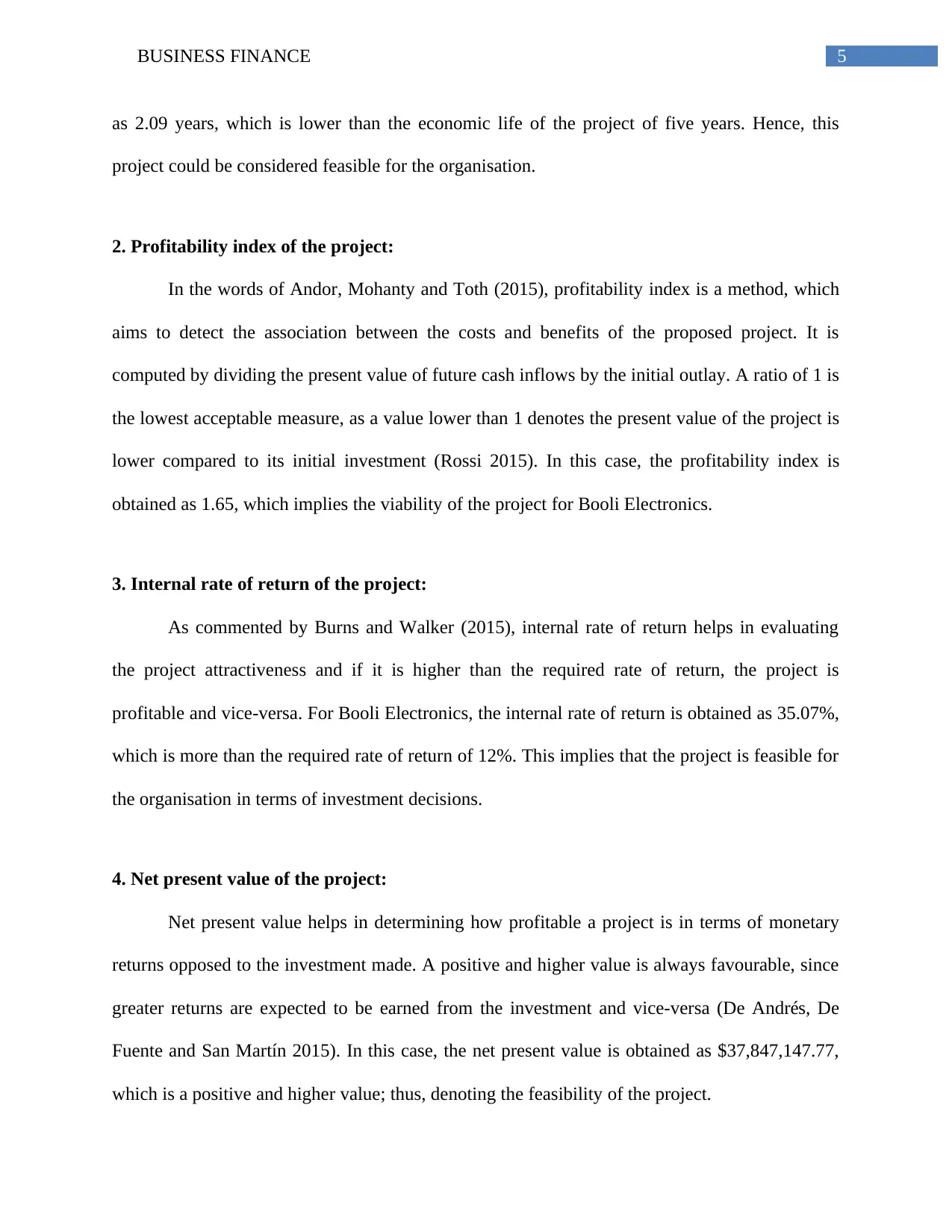

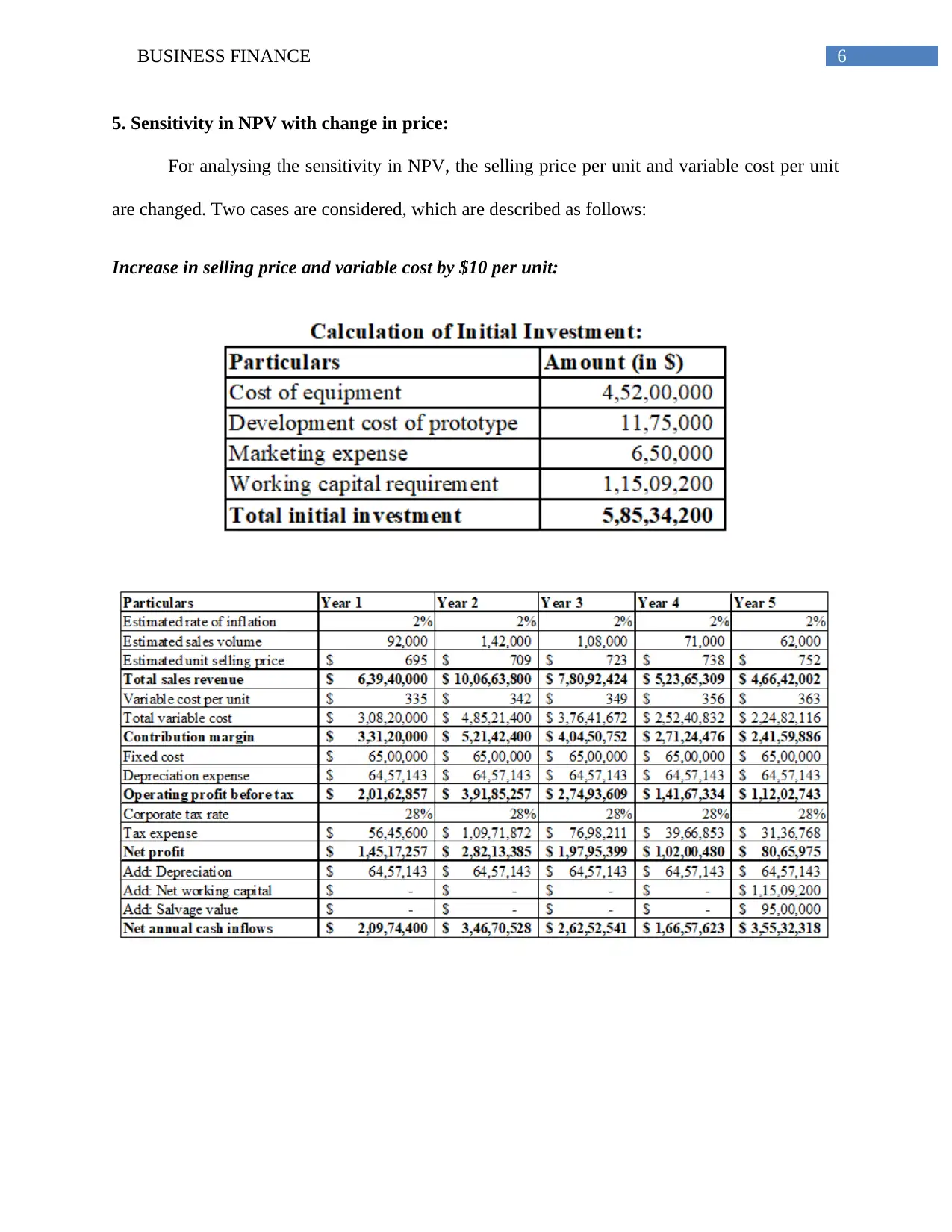

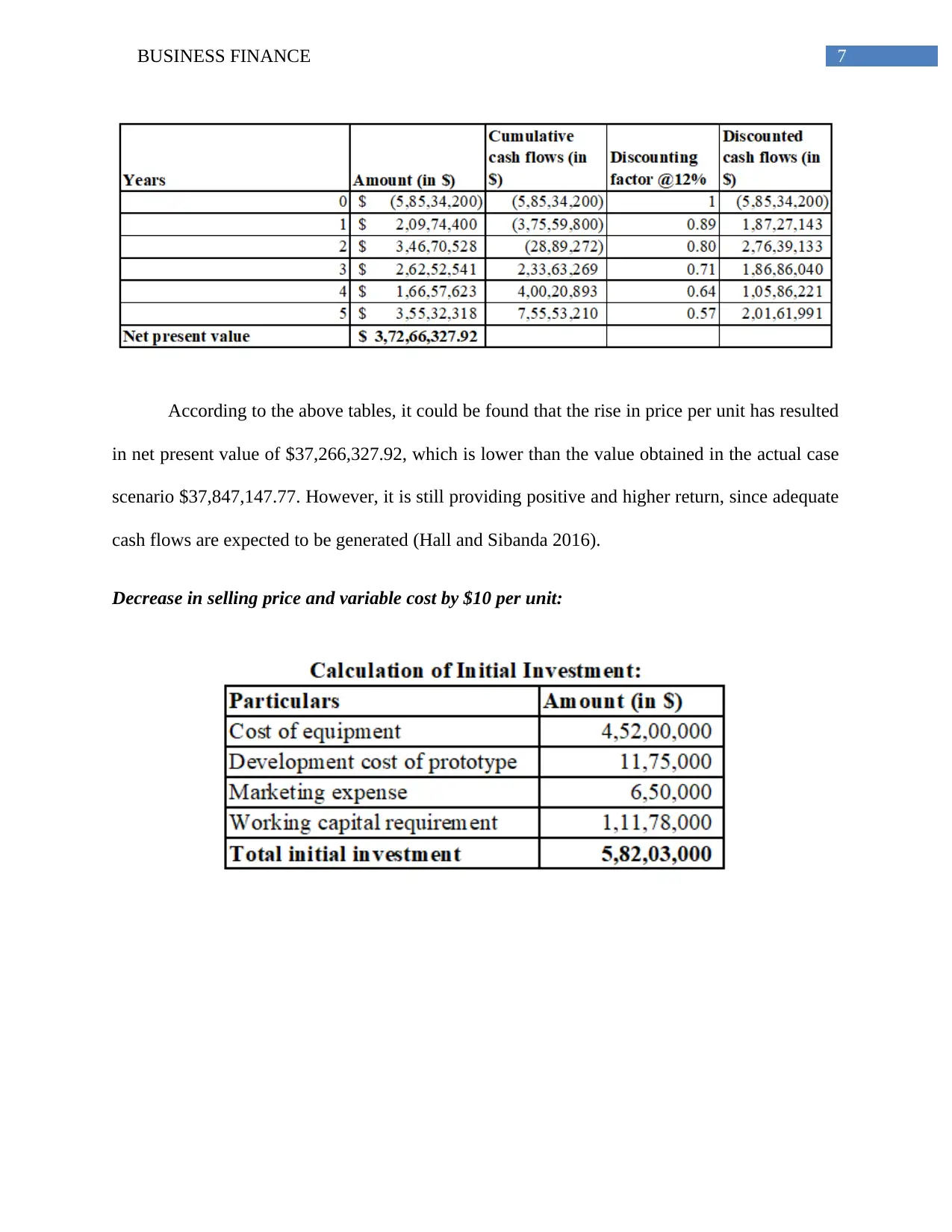

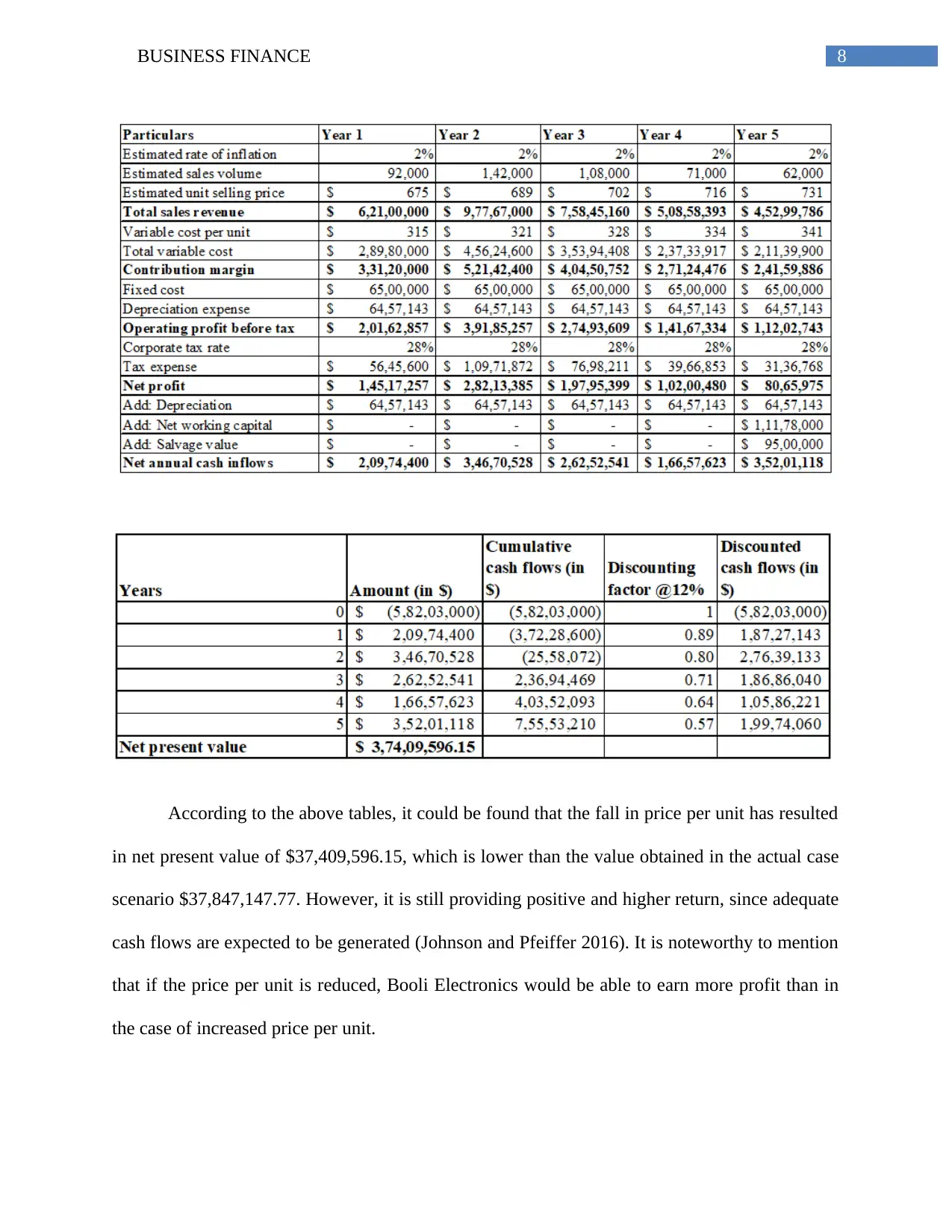

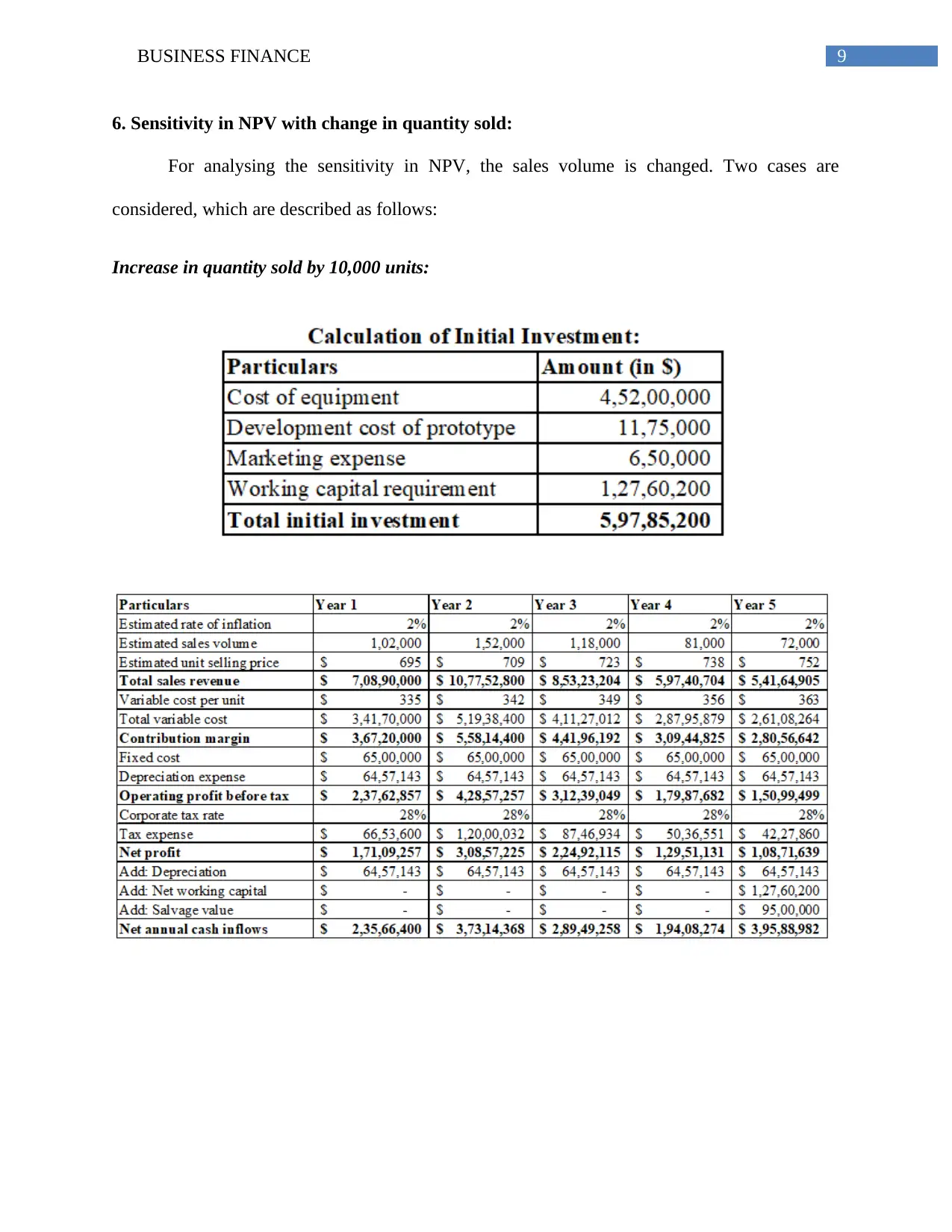

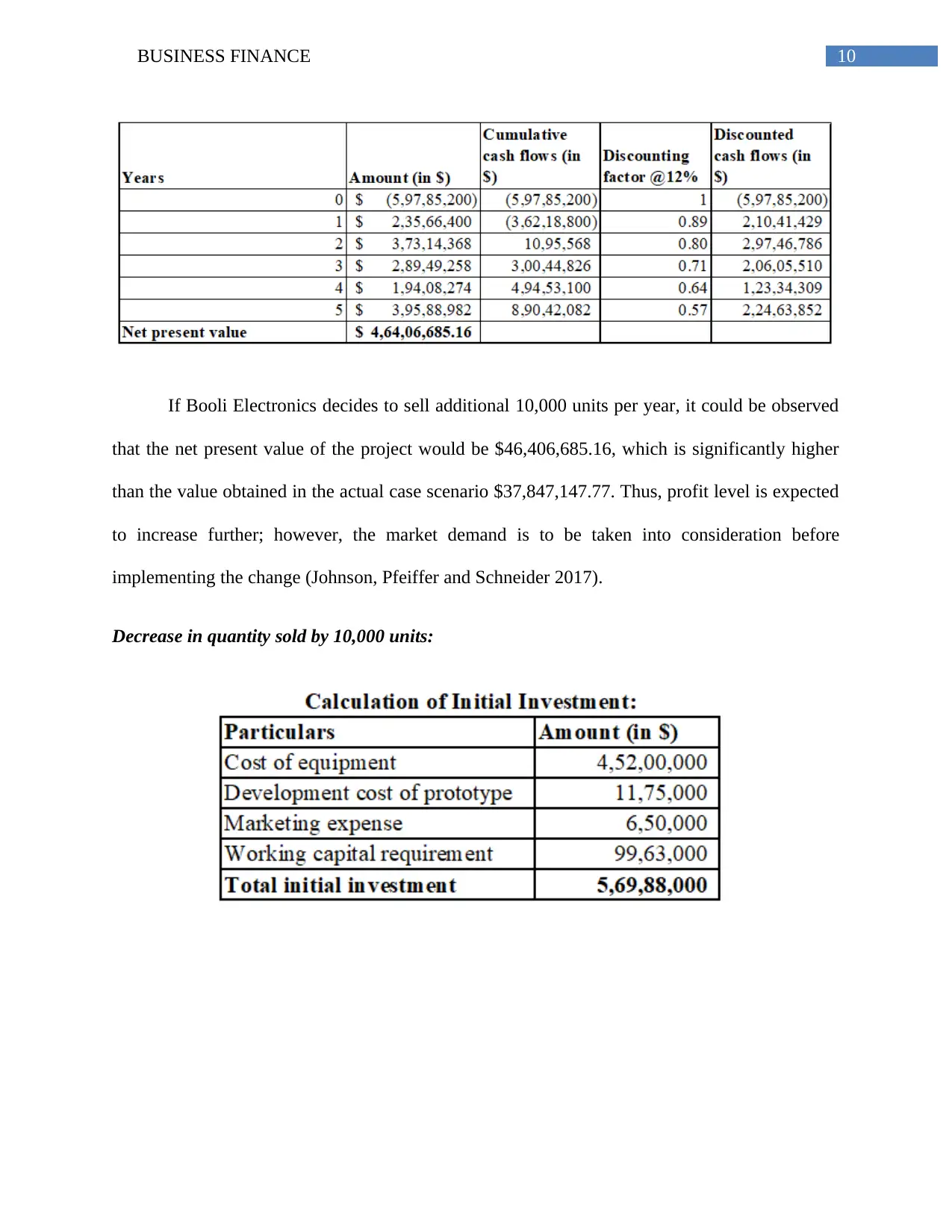

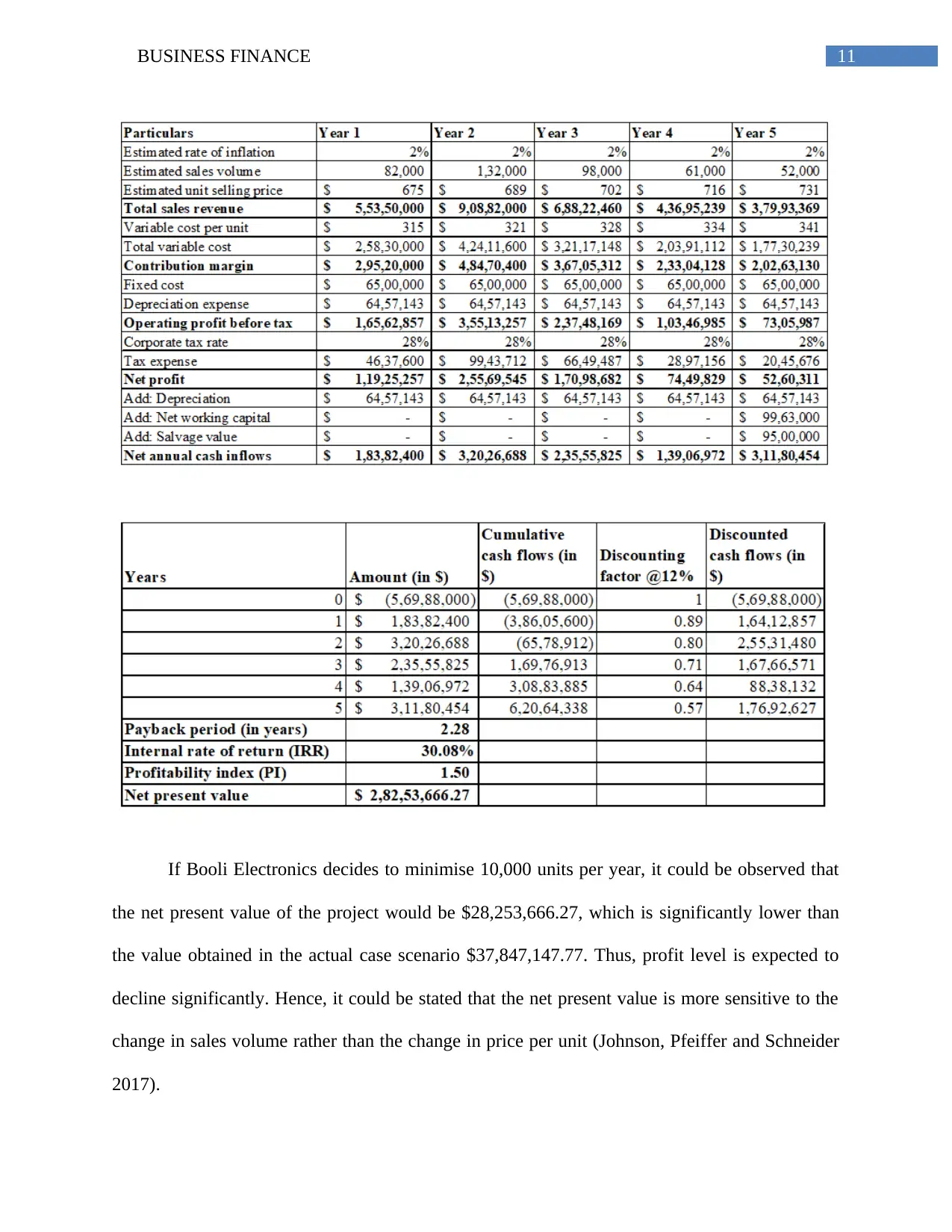

This report assesses the feasibility of a new Smart Speaker and Home Assistant (SSHA) project for Booli Electronics, an Australian manufacturer, using various capital budgeting techniques. The analysis includes non-discounted payback period, profitability index, internal rate of return, and net present value, all indicating the project's viability. Sensitivity analysis explores the impact of changes in price and sales volume on the net present value. The report concludes that the SSHA project is highly profitable and advises Booli Electronics to proceed, while also considering potential impacts on sales of other models and overall market demand. Desklib is your go-to platform for accessing similar solved assignments and comprehensive study tools.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.