Corporate Accounting Report: Boral's Headwaters Acquisition Analysis

VerifiedAdded on 2021/06/15

|6

|1104

|26

Report

AI Summary

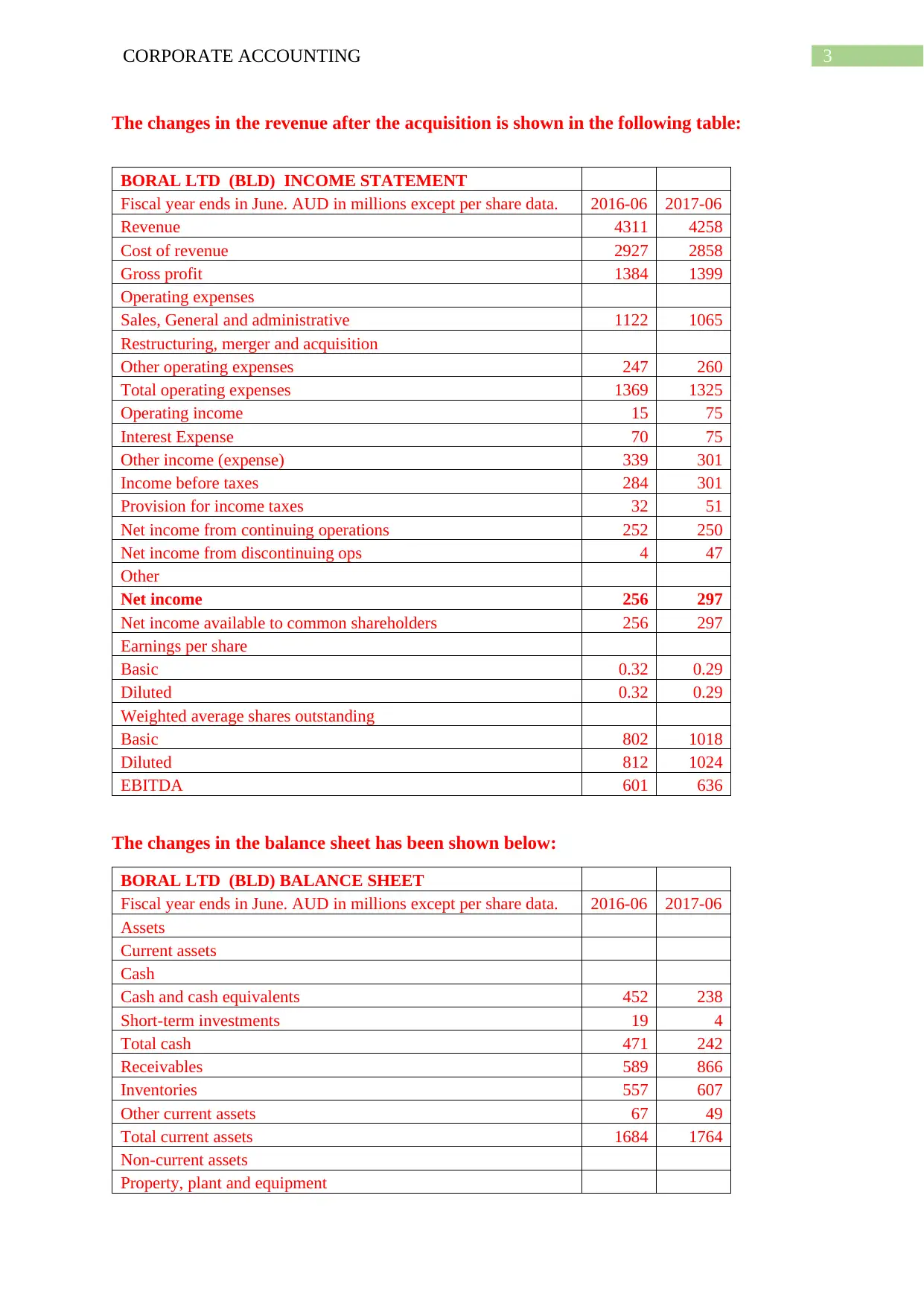

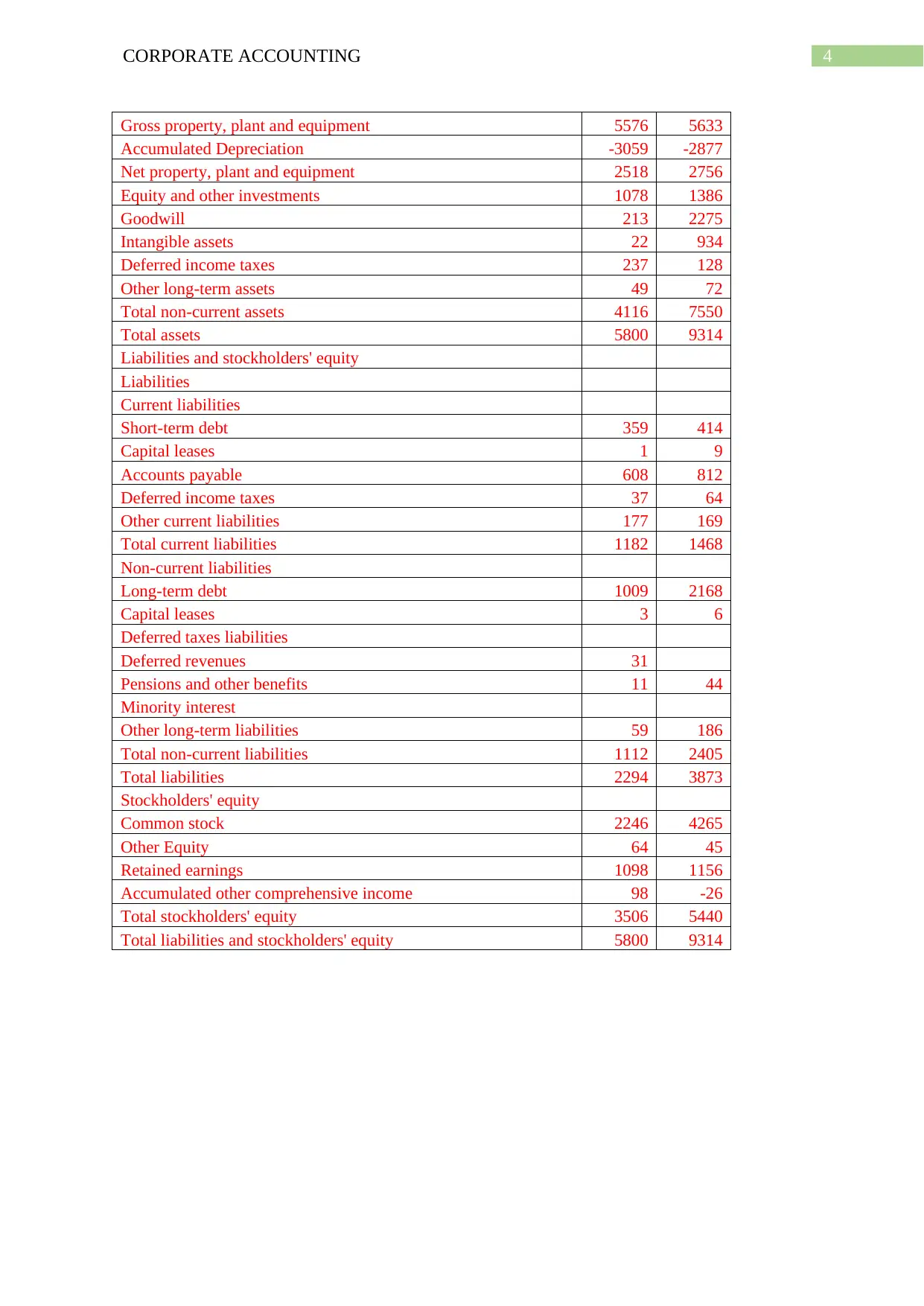

This report analyzes the acquisition of Headwaters by Boral, a publically listed company on the Australian Stock Exchange. The acquisition, driven by diversification and strategic goals, involved a 100% share purchase. The report details the accounting methods used, including the acquisition method under GAAP, and the financial implications on Boral's financial statements. It examines the consideration transferred, including cash, non-controlling interest, and goodwill. The report provides a comparative analysis of Boral's income statement and balance sheet before and after the acquisition, highlighting changes in revenue, expenses, assets, and liabilities. Key aspects such as the recording of goodwill, acquisition-related costs, and the impact on earnings per share are discussed. The analysis emphasizes the strategic rationale behind the acquisition and its impact on the company's financial performance. The report is a detailed analysis of the acquisition process, its accounting treatment, and its implications on the financial performance of Boral. This report showcases the practical application of corporate accounting principles in a real-world scenario.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.