Auditing Theory: A Detailed Case Study of Boral Limited's Audit

VerifiedAdded on 2023/05/29

|5

|718

|105

Case Study

AI Summary

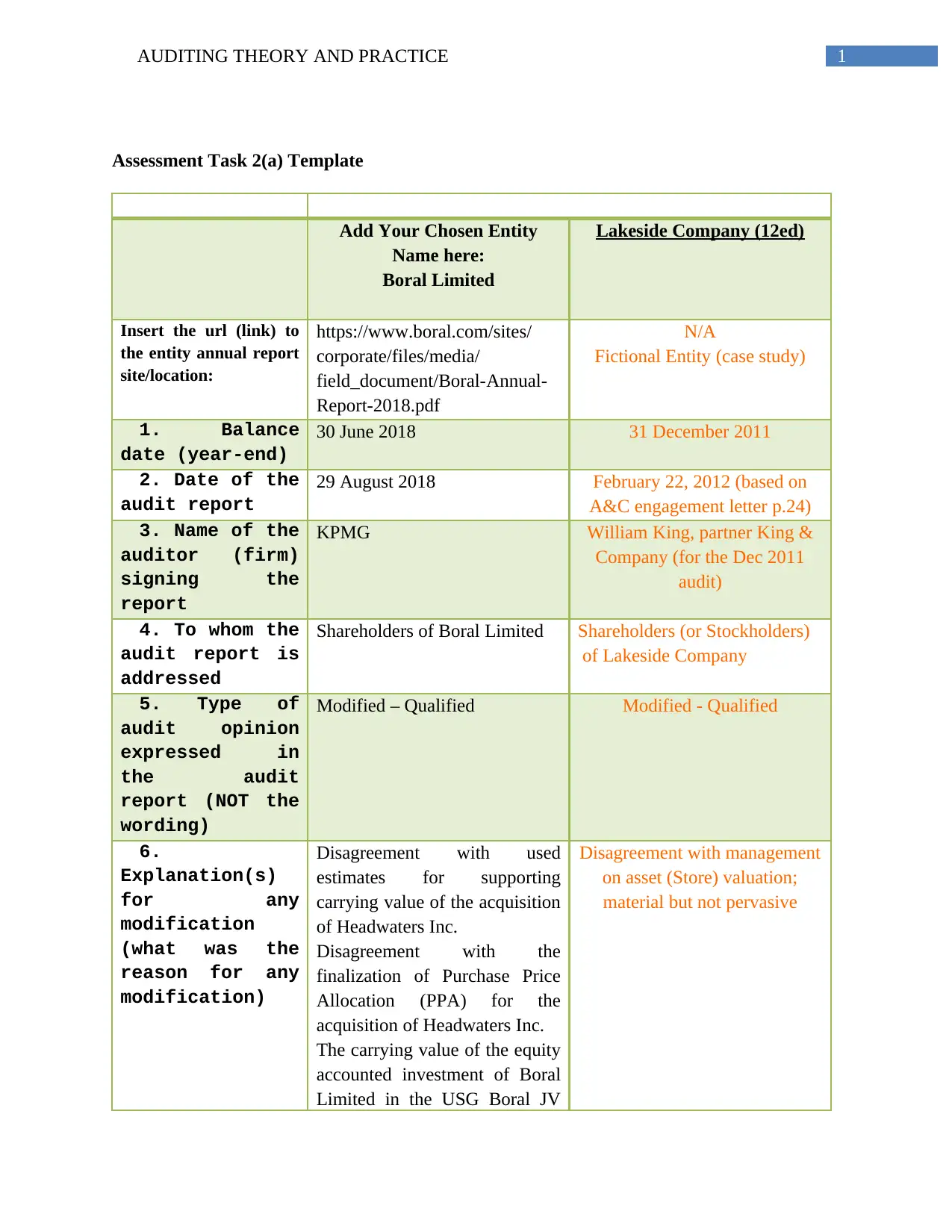

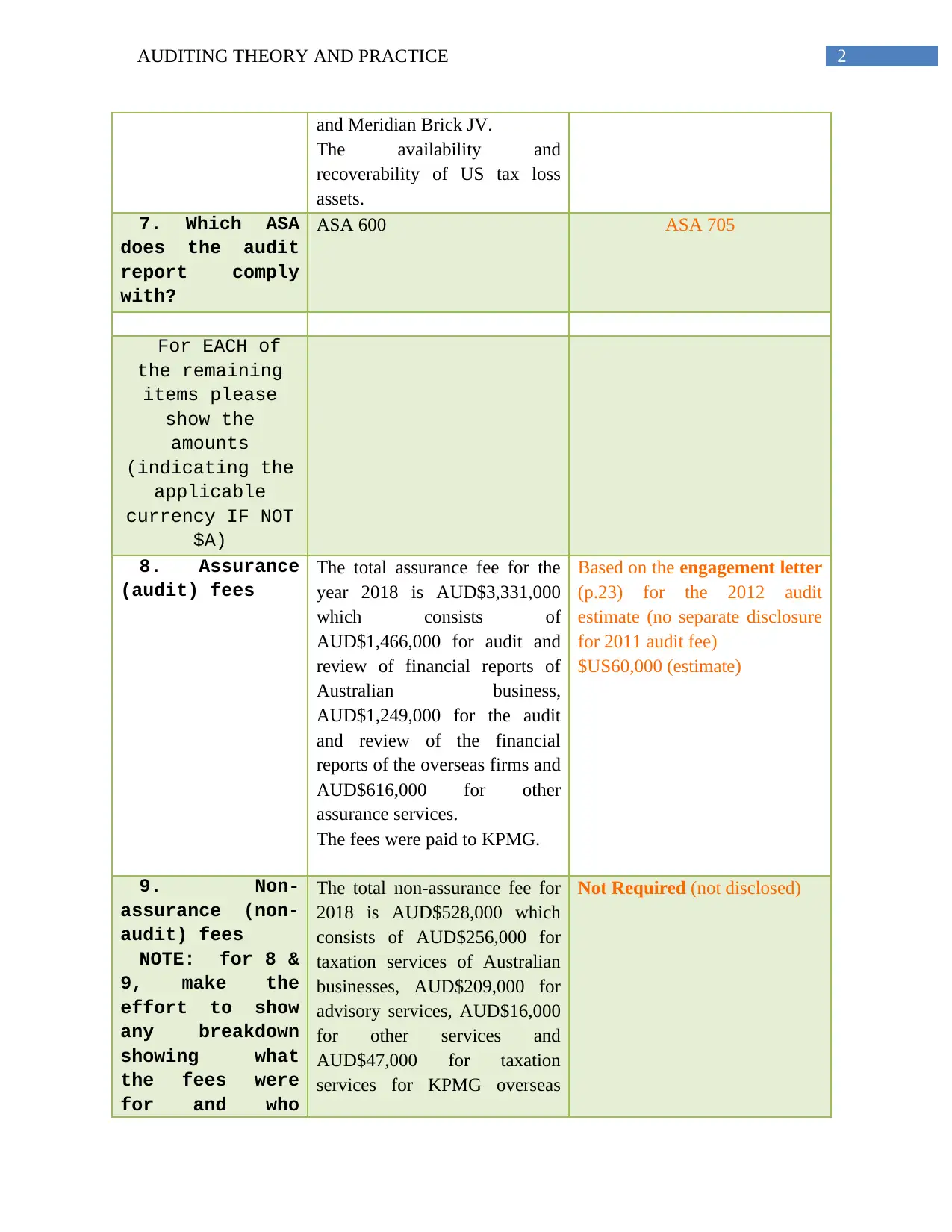

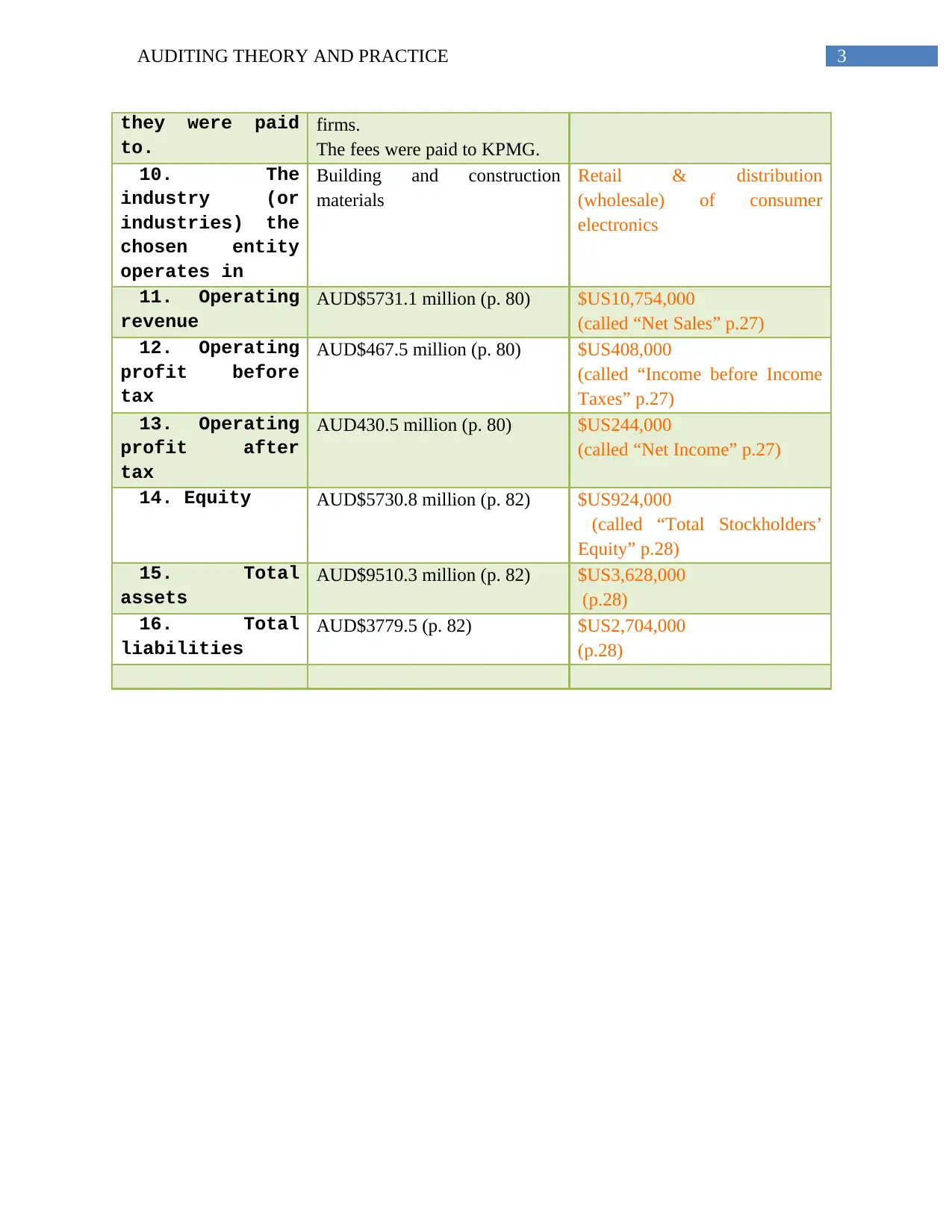

This case study provides an analysis of Boral Limited's audit, focusing on the 2018 annual report. It examines key aspects such as the audit firm (KPMG), the type of audit opinion expressed, disagreements with management, and compliance with ASA 600 and ASA 705. The study also includes a comparison with a fictional entity (Lakeside Company) and analyzes financial data, including operating revenue, profit, equity, assets, and liabilities. Furthermore, it highlights the assurance and non-assurance fees paid to KPMG, providing a comprehensive overview of Boral Limited's auditing practices. Desklib is a platform where you can find similar solved assignments and study resources to aid your academic journey.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.