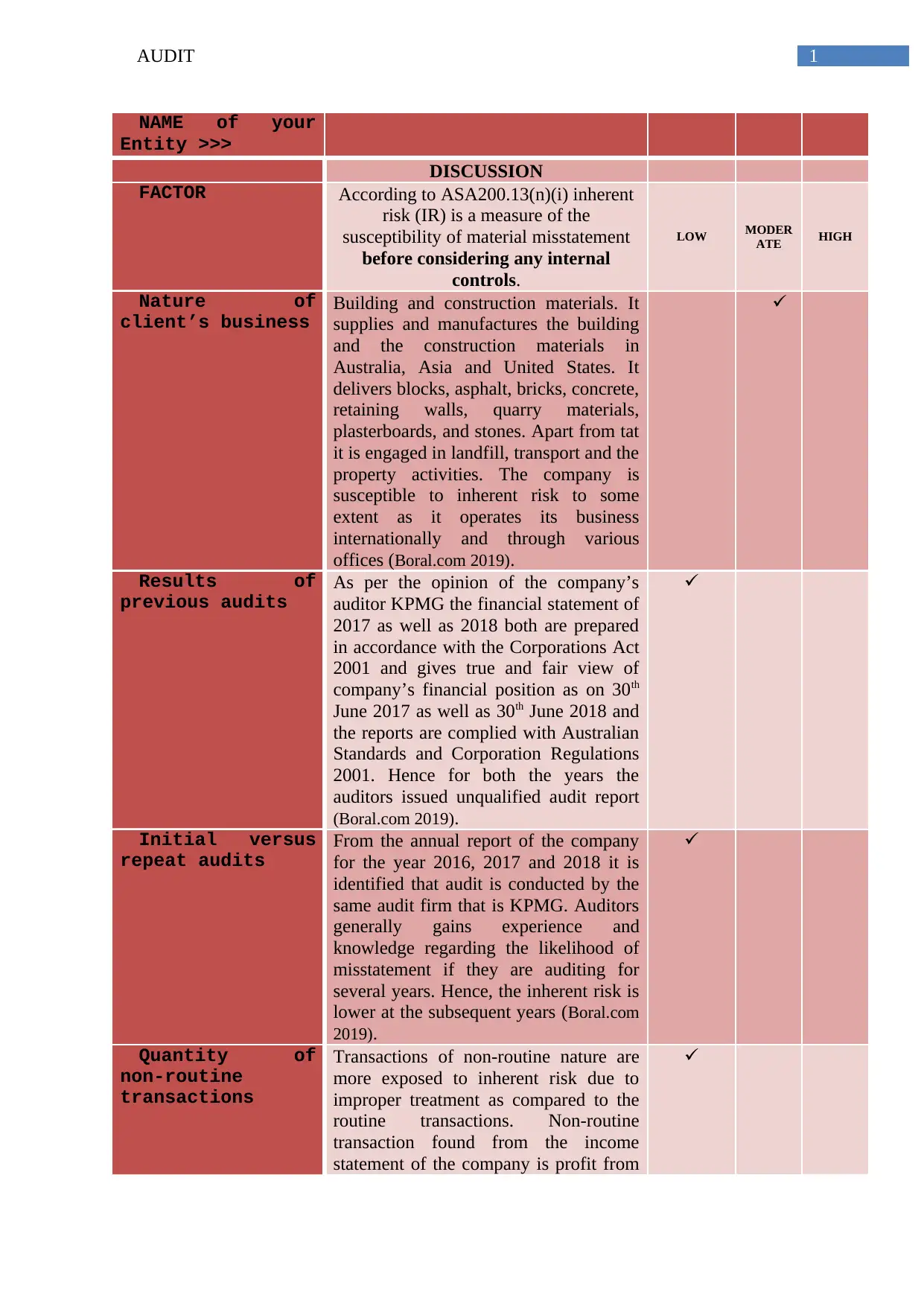

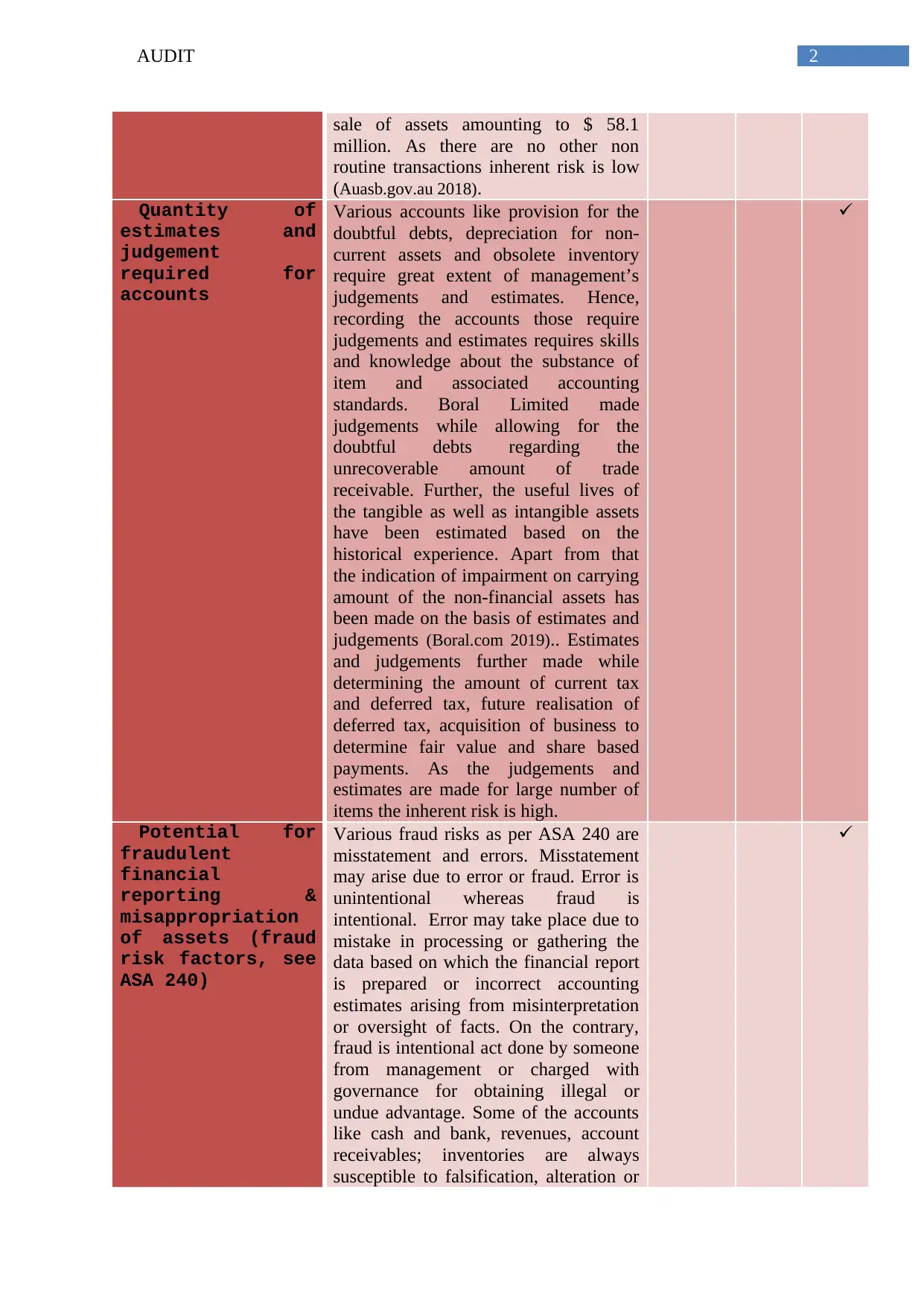

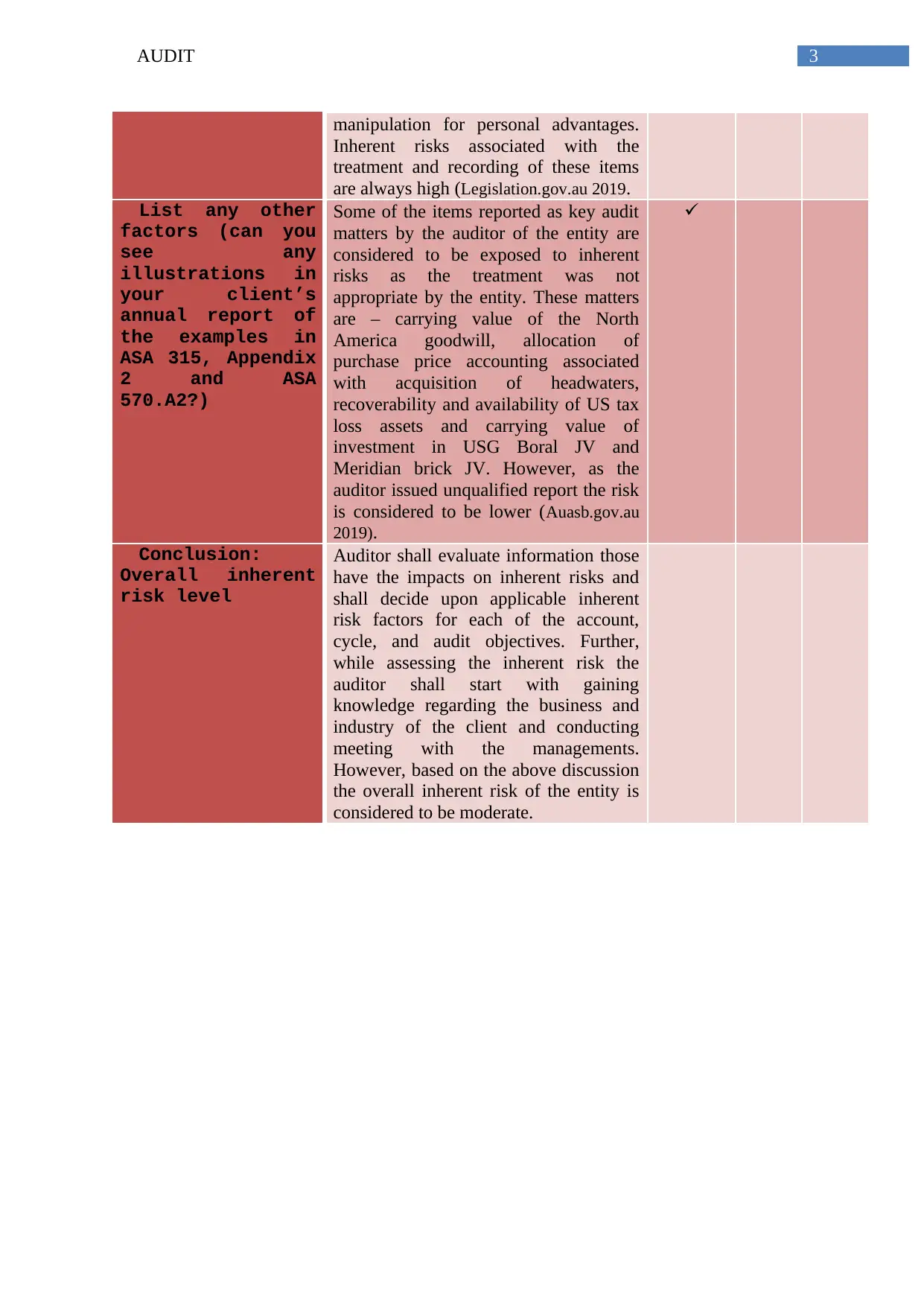

Finance Audit: Inherent Risk Assessment of Boral Limited, Australia

VerifiedAdded on 2023/04/22

|5

|1039

|408

Report

AI Summary

This report provides an assessment of the inherent risks associated with the audit of Boral Limited, a building and construction materials company operating in Australia, Asia, and the United States. The assessment considers factors such as the nature of the client's business, results of previous audits, the presence of non-routine transactions, the quantity of estimates and judgements required in financial reporting, and the potential for fraudulent financial reporting. The auditor's unqualified reports for 2017 and 2018, conducted by KPMG, indicate compliance with Australian Standards and Corporation Regulations. The report identifies key audit matters, including the carrying value of North America goodwill and the allocation of purchase price accounting, as areas exposed to inherent risks. Overall, the inherent risk for Boral Limited is determined to be moderate, based on a review of the company's annual reports and consideration of relevant auditing standards. Desklib offers a range of solved assignments and past papers for students seeking further assistance with their studies.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.