Auditing Theory and Practice: Evaluating Boral Limited's Financials

VerifiedAdded on 2023/06/06

|16

|3554

|82

Report

AI Summary

This report evaluates the effectiveness of material information identified by auditors of Boral Limited, an ASX-listed company. The analysis covers auditor independence, non-audit services, the audit committee, remuneration, and key audit matters. It assesses compliance with independence requirements, the nature of non-audit services provided by KPMG, and the remuneration paid for auditing and other services. Key audit matters, including the Headwaters acquisition and the Meridian brick joint venture, are evaluated. The report also examines the composition, function, and responsibilities of the audit committee and the audit opinion expressed, contrasting the responsibilities of management and auditors. The conclusion reflects on the overall effectiveness of the auditor's reporting in the annual report.

Running head: AUDITING THEORY AND PRACTICE

Auditing theory and practice

Name of the University

Name of the student

Authors note

Auditing theory and practice

Name of the University

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING THEORY AND PRACTICE

Executive summary:

The report is prepared for evaluating the effectiveness of the material information identified by

the auditors of the company listed on ASX. For the analysis, Boral limited is the company that

has been chosen and the data for the analysis have been extracted from the annual report

published by company annually. Analysis of the auditors have been done concerning wide range

of areas such as the independence requirements, non audit services, audit committee,

remuneration, key audit matters and outlining the responsibilities of auditors and director of

company. Evaluation of the auditing section presented in the annual report has assisted the user

in identifying the relevance of the audit opinion presented.

AUDITING THEORY AND PRACTICE

Executive summary:

The report is prepared for evaluating the effectiveness of the material information identified by

the auditors of the company listed on ASX. For the analysis, Boral limited is the company that

has been chosen and the data for the analysis have been extracted from the annual report

published by company annually. Analysis of the auditors have been done concerning wide range

of areas such as the independence requirements, non audit services, audit committee,

remuneration, key audit matters and outlining the responsibilities of auditors and director of

company. Evaluation of the auditing section presented in the annual report has assisted the user

in identifying the relevance of the audit opinion presented.

2

AUDITING THEORY AND PRACTICE

Table of Contents

Introduction:....................................................................................................................................3

Discussion:.......................................................................................................................................3

1) Evaluation of the auditor’s assurance services:...........................................................................3

2) Evaluation of Compliance of auditors with independence requirements:...................................3

3) Nature of non audit services:.......................................................................................................3

4) Analysis of remuneration of auditors:.........................................................................................3

5) Evaluation of key audit matters:..................................................................................................3

6) Evaluation of audit committee:...................................................................................................4

7) Audit opinion expressed:.............................................................................................................4

8) Difference between the responsibilities of management and auditors:.......................................4

Conclusion:......................................................................................................................................4

Reference list:..................................................................................................................................4

AUDITING THEORY AND PRACTICE

Table of Contents

Introduction:....................................................................................................................................3

Discussion:.......................................................................................................................................3

1) Evaluation of the auditor’s assurance services:...........................................................................3

2) Evaluation of Compliance of auditors with independence requirements:...................................3

3) Nature of non audit services:.......................................................................................................3

4) Analysis of remuneration of auditors:.........................................................................................3

5) Evaluation of key audit matters:..................................................................................................3

6) Evaluation of audit committee:...................................................................................................4

7) Audit opinion expressed:.............................................................................................................4

8) Difference between the responsibilities of management and auditors:.......................................4

Conclusion:......................................................................................................................................4

Reference list:..................................................................................................................................4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING THEORY AND PRACTICE

Introduction:

The current paper addresses the evaluation of assurances services provided the auditors of

listed company on the Australia stock exchange. For this purpose, analysis of the auditor’s

section has been demonstrated in several areas such as auditor’s remuneration, audit committee,

key audit matters, non audit services and audit opinion. The company that is selected from the

list is Boral limited which is a multinational company engaged in the constriction of materials,

supplying and manufacturing of buildings. There are three divisions of organization comprising

of fast growing Boral interior linings, material business that is well positioned and high

performing business. The analysis of the auditors section has been done by evaluating the

information presented in the financial report of company that is published on the website. The

last section of report identifies whether the material information presented by the auditor in the

annual report is effective or not. Analysis of the audit committee has been done in the context of

the responsibilities, functions, meeting and composition that helps in evaluating the contribution

of such committee to the organization as a whole.

Discussion:

1) Evaluation of the auditor’s assurance services:

An objective and independence assurance is provided by the group audit and risk being a

function of internal audit. It has been ascertained from the annual report that the auditor has not

expressed any opinion in the form of concluding about the assurance thereon relating to the

financial statements. However, for the remuneration report, the opinion by the auditors has been

assured. The objective of auditor is to provide reasonable assurance about the financial report

that is free from any material misstatement due to the consequence of errors and fraud (Power &

Gendron, 2015).

AUDITING THEORY AND PRACTICE

Introduction:

The current paper addresses the evaluation of assurances services provided the auditors of

listed company on the Australia stock exchange. For this purpose, analysis of the auditor’s

section has been demonstrated in several areas such as auditor’s remuneration, audit committee,

key audit matters, non audit services and audit opinion. The company that is selected from the

list is Boral limited which is a multinational company engaged in the constriction of materials,

supplying and manufacturing of buildings. There are three divisions of organization comprising

of fast growing Boral interior linings, material business that is well positioned and high

performing business. The analysis of the auditors section has been done by evaluating the

information presented in the financial report of company that is published on the website. The

last section of report identifies whether the material information presented by the auditor in the

annual report is effective or not. Analysis of the audit committee has been done in the context of

the responsibilities, functions, meeting and composition that helps in evaluating the contribution

of such committee to the organization as a whole.

Discussion:

1) Evaluation of the auditor’s assurance services:

An objective and independence assurance is provided by the group audit and risk being a

function of internal audit. It has been ascertained from the annual report that the auditor has not

expressed any opinion in the form of concluding about the assurance thereon relating to the

financial statements. However, for the remuneration report, the opinion by the auditors has been

assured. The objective of auditor is to provide reasonable assurance about the financial report

that is free from any material misstatement due to the consequence of errors and fraud (Power &

Gendron, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING THEORY AND PRACTICE

2) Evaluation of Compliance of auditors with independence requirements:

The independence and effectiveness of external auditor of Boral limited is reviewed by

the audit committee. Since, the external auditors have the potential to impair independence

because of the services kind that is prohibited. The directors of Boral limited have made

declarations to the best of their belief and knowledge that there are no contraventions in relation

to any applicable code of professional conduct and independence requirements of auditors that is

set in the Corporation Act, 2001. Furthermore, the independence requirements of auditor are not

compromised in carrying out the non auditing services and its related provisions. The

independence declaration of auditor does not seem to be questioned by the director as there is not

any reasonable basis according to Corporation act requirements (Cannon & Bedard, 2016).

3) Nature of non audit services:

The non audit services provided by auditor of Boral limited comprise of services of tax

compliance in Australia, tax compliance services in other jurisdiction that in Australia, assurance

and other advisory related services and due diligence services in relation to the formation of joint

venture of Meridian bricks and Headwaters acquisition. The external auditor of Boral limited is

KPMG and they are paid total of amount of $ 2830000 for non audit services. In relation to the

provision of non audit services, directors are satisfied about the compatibility of auditor

independence as per the advice from audit and risk committee of company. In addition to this,

there is no inconsistency between the Corporation act requirements, process of audit committee

and non audit services.

AUDITING THEORY AND PRACTICE

2) Evaluation of Compliance of auditors with independence requirements:

The independence and effectiveness of external auditor of Boral limited is reviewed by

the audit committee. Since, the external auditors have the potential to impair independence

because of the services kind that is prohibited. The directors of Boral limited have made

declarations to the best of their belief and knowledge that there are no contraventions in relation

to any applicable code of professional conduct and independence requirements of auditors that is

set in the Corporation Act, 2001. Furthermore, the independence requirements of auditor are not

compromised in carrying out the non auditing services and its related provisions. The

independence declaration of auditor does not seem to be questioned by the director as there is not

any reasonable basis according to Corporation act requirements (Cannon & Bedard, 2016).

3) Nature of non audit services:

The non audit services provided by auditor of Boral limited comprise of services of tax

compliance in Australia, tax compliance services in other jurisdiction that in Australia, assurance

and other advisory related services and due diligence services in relation to the formation of joint

venture of Meridian bricks and Headwaters acquisition. The external auditor of Boral limited is

KPMG and they are paid total of amount of $ 2830000 for non audit services. In relation to the

provision of non audit services, directors are satisfied about the compatibility of auditor

independence as per the advice from audit and risk committee of company. In addition to this,

there is no inconsistency between the Corporation act requirements, process of audit committee

and non audit services.

5

AUDITING THEORY AND PRACTICE

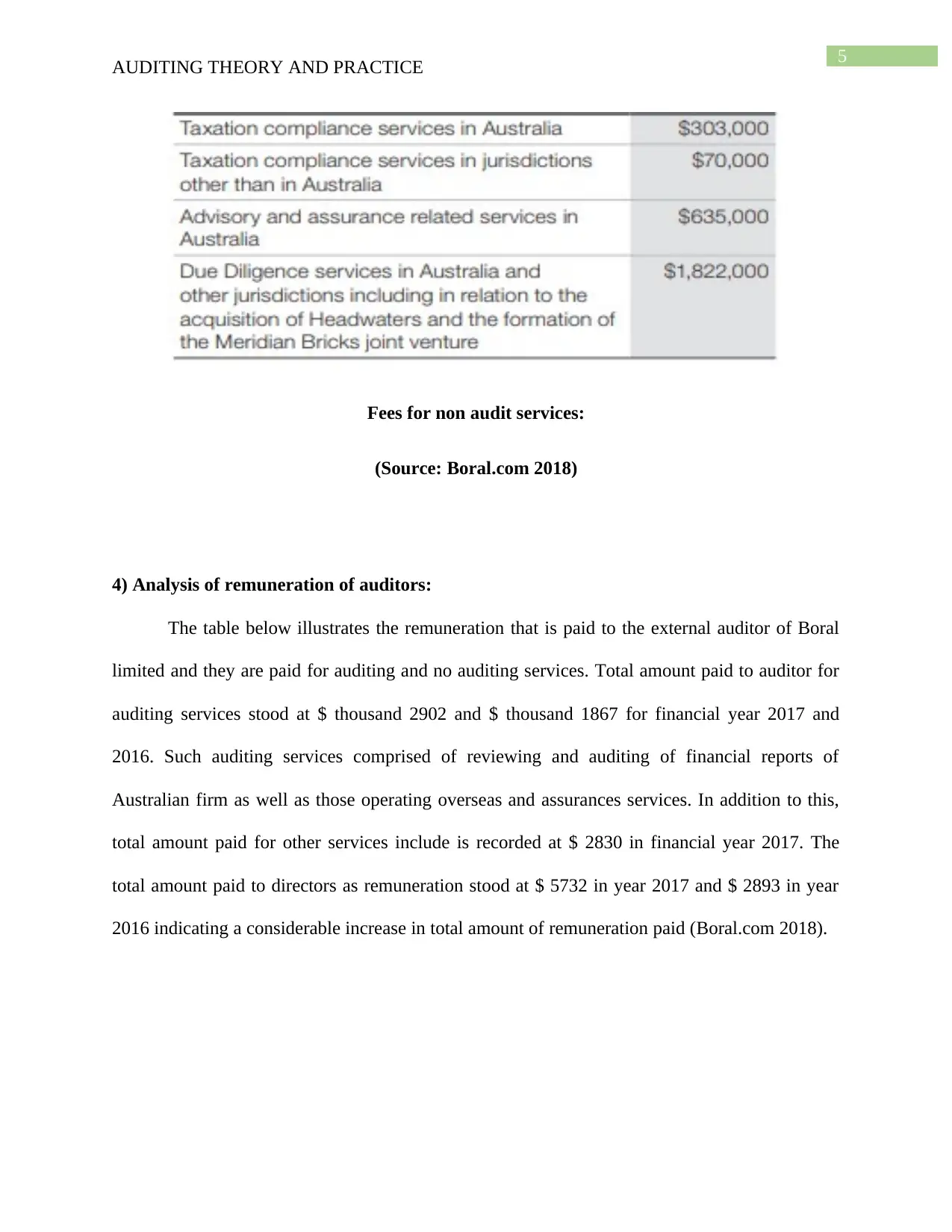

Fees for non audit services:

(Source: Boral.com 2018)

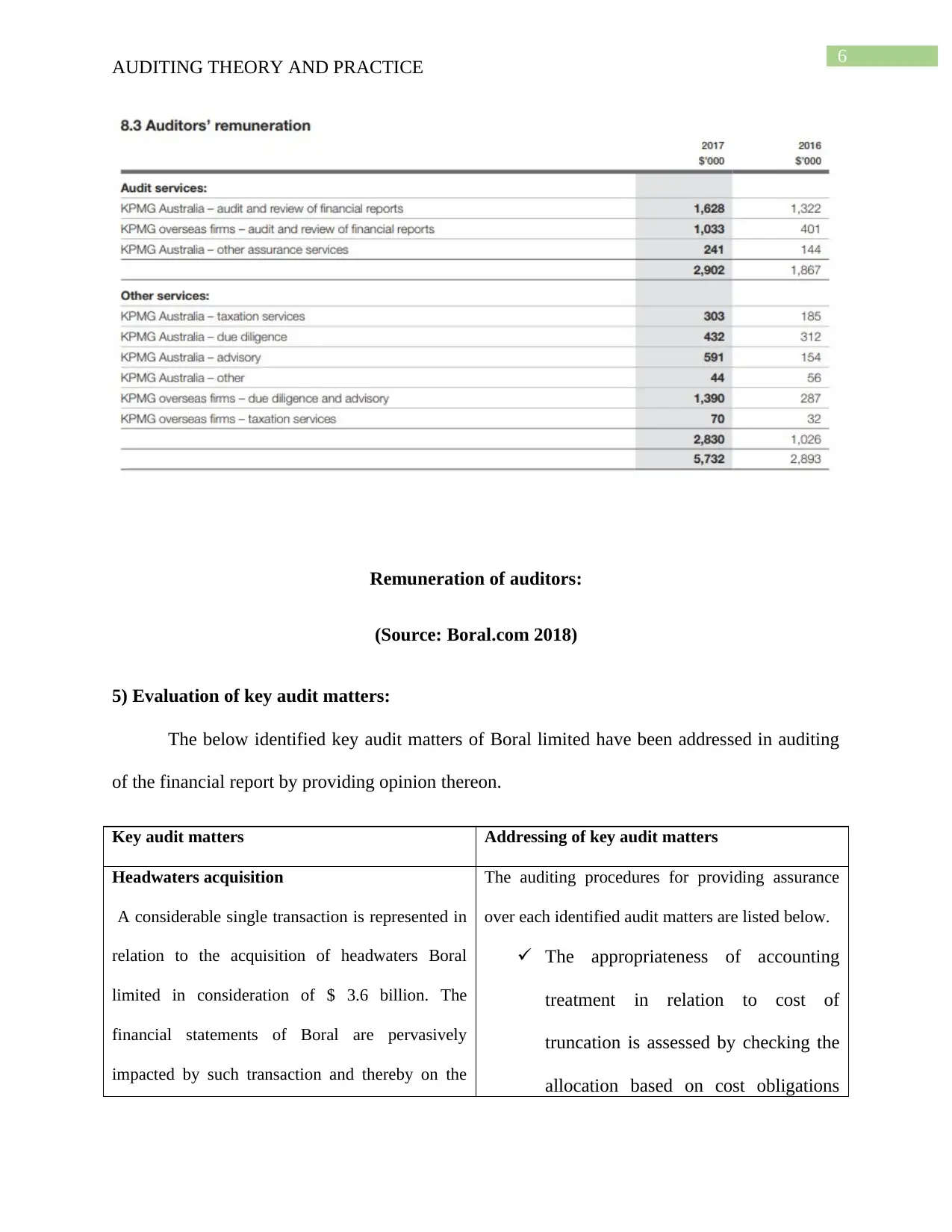

4) Analysis of remuneration of auditors:

The table below illustrates the remuneration that is paid to the external auditor of Boral

limited and they are paid for auditing and no auditing services. Total amount paid to auditor for

auditing services stood at $ thousand 2902 and $ thousand 1867 for financial year 2017 and

2016. Such auditing services comprised of reviewing and auditing of financial reports of

Australian firm as well as those operating overseas and assurances services. In addition to this,

total amount paid for other services include is recorded at $ 2830 in financial year 2017. The

total amount paid to directors as remuneration stood at $ 5732 in year 2017 and $ 2893 in year

2016 indicating a considerable increase in total amount of remuneration paid (Boral.com 2018).

AUDITING THEORY AND PRACTICE

Fees for non audit services:

(Source: Boral.com 2018)

4) Analysis of remuneration of auditors:

The table below illustrates the remuneration that is paid to the external auditor of Boral

limited and they are paid for auditing and no auditing services. Total amount paid to auditor for

auditing services stood at $ thousand 2902 and $ thousand 1867 for financial year 2017 and

2016. Such auditing services comprised of reviewing and auditing of financial reports of

Australian firm as well as those operating overseas and assurances services. In addition to this,

total amount paid for other services include is recorded at $ 2830 in financial year 2017. The

total amount paid to directors as remuneration stood at $ 5732 in year 2017 and $ 2893 in year

2016 indicating a considerable increase in total amount of remuneration paid (Boral.com 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING THEORY AND PRACTICE

Remuneration of auditors:

(Source: Boral.com 2018)

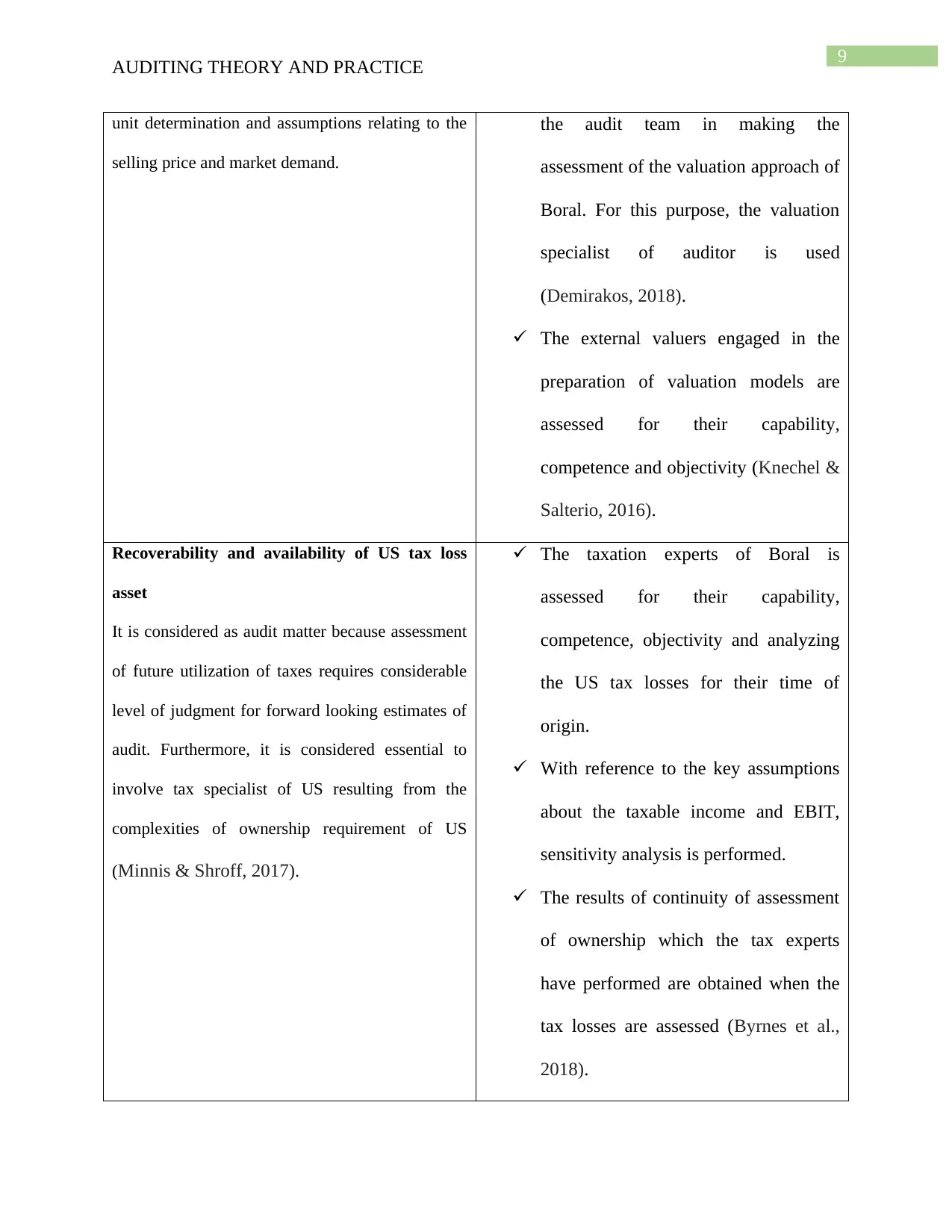

5) Evaluation of key audit matters:

The below identified key audit matters of Boral limited have been addressed in auditing

of the financial report by providing opinion thereon.

Key audit matters Addressing of key audit matters

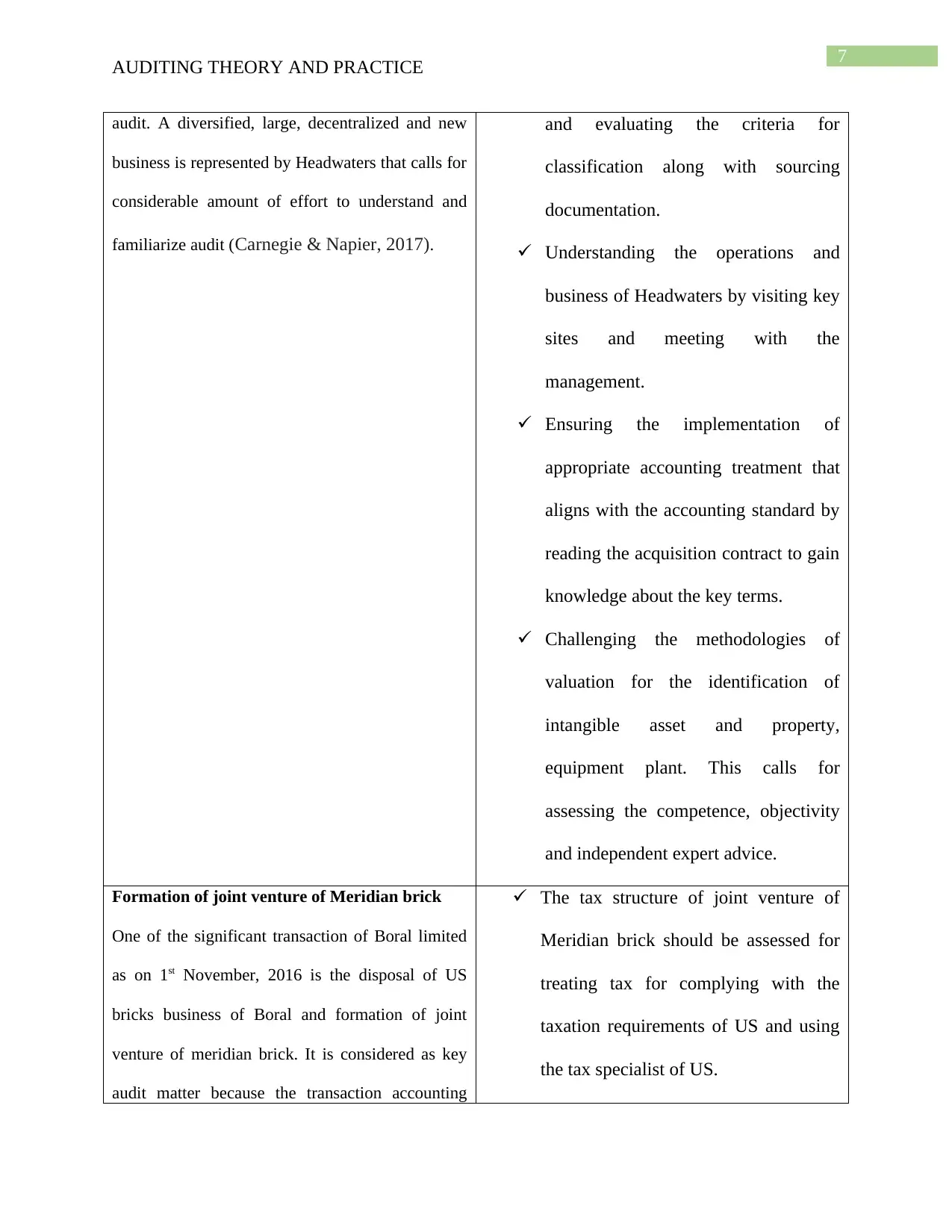

Headwaters acquisition

A considerable single transaction is represented in

relation to the acquisition of headwaters Boral

limited in consideration of $ 3.6 billion. The

financial statements of Boral are pervasively

impacted by such transaction and thereby on the

The auditing procedures for providing assurance

over each identified audit matters are listed below.

The appropriateness of accounting

treatment in relation to cost of

truncation is assessed by checking the

allocation based on cost obligations

AUDITING THEORY AND PRACTICE

Remuneration of auditors:

(Source: Boral.com 2018)

5) Evaluation of key audit matters:

The below identified key audit matters of Boral limited have been addressed in auditing

of the financial report by providing opinion thereon.

Key audit matters Addressing of key audit matters

Headwaters acquisition

A considerable single transaction is represented in

relation to the acquisition of headwaters Boral

limited in consideration of $ 3.6 billion. The

financial statements of Boral are pervasively

impacted by such transaction and thereby on the

The auditing procedures for providing assurance

over each identified audit matters are listed below.

The appropriateness of accounting

treatment in relation to cost of

truncation is assessed by checking the

allocation based on cost obligations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING THEORY AND PRACTICE

audit. A diversified, large, decentralized and new

business is represented by Headwaters that calls for

considerable amount of effort to understand and

familiarize audit (Carnegie & Napier, 2017).

and evaluating the criteria for

classification along with sourcing

documentation.

Understanding the operations and

business of Headwaters by visiting key

sites and meeting with the

management.

Ensuring the implementation of

appropriate accounting treatment that

aligns with the accounting standard by

reading the acquisition contract to gain

knowledge about the key terms.

Challenging the methodologies of

valuation for the identification of

intangible asset and property,

equipment plant. This calls for

assessing the competence, objectivity

and independent expert advice.

Formation of joint venture of Meridian brick

One of the significant transaction of Boral limited

as on 1st November, 2016 is the disposal of US

bricks business of Boral and formation of joint

venture of meridian brick. It is considered as key

audit matter because the transaction accounting

The tax structure of joint venture of

Meridian brick should be assessed for

treating tax for complying with the

taxation requirements of US and using

the tax specialist of US.

AUDITING THEORY AND PRACTICE

audit. A diversified, large, decentralized and new

business is represented by Headwaters that calls for

considerable amount of effort to understand and

familiarize audit (Carnegie & Napier, 2017).

and evaluating the criteria for

classification along with sourcing

documentation.

Understanding the operations and

business of Headwaters by visiting key

sites and meeting with the

management.

Ensuring the implementation of

appropriate accounting treatment that

aligns with the accounting standard by

reading the acquisition contract to gain

knowledge about the key terms.

Challenging the methodologies of

valuation for the identification of

intangible asset and property,

equipment plant. This calls for

assessing the competence, objectivity

and independent expert advice.

Formation of joint venture of Meridian brick

One of the significant transaction of Boral limited

as on 1st November, 2016 is the disposal of US

bricks business of Boral and formation of joint

venture of meridian brick. It is considered as key

audit matter because the transaction accounting

The tax structure of joint venture of

Meridian brick should be assessed for

treating tax for complying with the

taxation requirements of US and using

the tax specialist of US.

8

AUDITING THEORY AND PRACTICE

relating to taxation that required to involve tax

specialist of US.

Across the multiple jurisdictions, there was

complicated contractual arrangements’ seeking for

an increased level of audit.

The contractual arrangement should be

examined for identification of the terms

that is applicable to legal structure of

such joint venture. Such terms have

been assessed for implications

concerning accounting by comparing to

the accounting standards requirement

and criteria.

The net assets of Boral should be

assessed for valuation by using the

procedures that is illustrated in the joint

venture of Meridian brick.

Investment carrying value of joint venture of

Meridian brick and USG Boral.

It is considered as key audit matter because of the

risk due to the variation between average selling

price and market demand for products and auditing

complexities for forward looking estimates. The

assessment of recoverability of the carrying value

of joint venture is done by the application of

considerable judgments (Trotman et al., 2015).

The judgments have been done in relation to the

applicable discount rate for forecasting the cash

flow, indication of impairment, cash generating

The key assumptions of Boral such as

selling price and market demand are

challenged by carrying out comparisons

of different components. Forecast is

approved by comparing the valuation

model data. in addition to this, over the

multiple housing cycle, the actual

historical data is compared (Louwers et

al., 2015).

The determination of cash generating

unit of Boral is assessed for assisting

AUDITING THEORY AND PRACTICE

relating to taxation that required to involve tax

specialist of US.

Across the multiple jurisdictions, there was

complicated contractual arrangements’ seeking for

an increased level of audit.

The contractual arrangement should be

examined for identification of the terms

that is applicable to legal structure of

such joint venture. Such terms have

been assessed for implications

concerning accounting by comparing to

the accounting standards requirement

and criteria.

The net assets of Boral should be

assessed for valuation by using the

procedures that is illustrated in the joint

venture of Meridian brick.

Investment carrying value of joint venture of

Meridian brick and USG Boral.

It is considered as key audit matter because of the

risk due to the variation between average selling

price and market demand for products and auditing

complexities for forward looking estimates. The

assessment of recoverability of the carrying value

of joint venture is done by the application of

considerable judgments (Trotman et al., 2015).

The judgments have been done in relation to the

applicable discount rate for forecasting the cash

flow, indication of impairment, cash generating

The key assumptions of Boral such as

selling price and market demand are

challenged by carrying out comparisons

of different components. Forecast is

approved by comparing the valuation

model data. in addition to this, over the

multiple housing cycle, the actual

historical data is compared (Louwers et

al., 2015).

The determination of cash generating

unit of Boral is assessed for assisting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING THEORY AND PRACTICE

unit determination and assumptions relating to the

selling price and market demand.

the audit team in making the

assessment of the valuation approach of

Boral. For this purpose, the valuation

specialist of auditor is used

(Demirakos, 2018).

The external valuers engaged in the

preparation of valuation models are

assessed for their capability,

competence and objectivity (Knechel &

Salterio, 2016).

Recoverability and availability of US tax loss

asset

It is considered as audit matter because assessment

of future utilization of taxes requires considerable

level of judgment for forward looking estimates of

audit. Furthermore, it is considered essential to

involve tax specialist of US resulting from the

complexities of ownership requirement of US

(Minnis & Shroff, 2017).

The taxation experts of Boral is

assessed for their capability,

competence, objectivity and analyzing

the US tax losses for their time of

origin.

With reference to the key assumptions

about the taxable income and EBIT,

sensitivity analysis is performed.

The results of continuity of assessment

of ownership which the tax experts

have performed are obtained when the

tax losses are assessed (Byrnes et al.,

2018).

AUDITING THEORY AND PRACTICE

unit determination and assumptions relating to the

selling price and market demand.

the audit team in making the

assessment of the valuation approach of

Boral. For this purpose, the valuation

specialist of auditor is used

(Demirakos, 2018).

The external valuers engaged in the

preparation of valuation models are

assessed for their capability,

competence and objectivity (Knechel &

Salterio, 2016).

Recoverability and availability of US tax loss

asset

It is considered as audit matter because assessment

of future utilization of taxes requires considerable

level of judgment for forward looking estimates of

audit. Furthermore, it is considered essential to

involve tax specialist of US resulting from the

complexities of ownership requirement of US

(Minnis & Shroff, 2017).

The taxation experts of Boral is

assessed for their capability,

competence, objectivity and analyzing

the US tax losses for their time of

origin.

With reference to the key assumptions

about the taxable income and EBIT,

sensitivity analysis is performed.

The results of continuity of assessment

of ownership which the tax experts

have performed are obtained when the

tax losses are assessed (Byrnes et al.,

2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING THEORY AND PRACTICE

6) Evaluation of audit committee:

The formal charter of audit committee sets out the requirement of composition,

responsibilities and roles, membership and structure.

Composition of audit committee:

The audit committee of Boral limited provides assistance in effective operations of the

board of directors. The composition of audit committee involves only non executive directors

who are independent and the members are Eileen Doyle, Paul Rayner and Karen Moses.

Function of audit committee:

The procedure for ensuring the rotation of engagement partner of external audit is

monitored by audit committee.

The formalization of process for the appointment and selection of new auditors is

required to be done by the auditors.

The effectiveness, quality of performance and independence of auditors is evaluated

along with reviewing of the scope of internal audit is done by the audit committee

(Dumay et al., 2018).

Responsibilities of audit committee:

The responsibilities of audit committee is to provide oversight and conduct review of the

Quality and integrity of the disclosures and financial statements of Boral limited

AUDITING THEORY AND PRACTICE

6) Evaluation of audit committee:

The formal charter of audit committee sets out the requirement of composition,

responsibilities and roles, membership and structure.

Composition of audit committee:

The audit committee of Boral limited provides assistance in effective operations of the

board of directors. The composition of audit committee involves only non executive directors

who are independent and the members are Eileen Doyle, Paul Rayner and Karen Moses.

Function of audit committee:

The procedure for ensuring the rotation of engagement partner of external audit is

monitored by audit committee.

The formalization of process for the appointment and selection of new auditors is

required to be done by the auditors.

The effectiveness, quality of performance and independence of auditors is evaluated

along with reviewing of the scope of internal audit is done by the audit committee

(Dumay et al., 2018).

Responsibilities of audit committee:

The responsibilities of audit committee is to provide oversight and conduct review of the

Quality and integrity of the disclosures and financial statements of Boral limited

11

AUDITING THEORY AND PRACTICE

Financial information provided to the public and shareholder of company should be

reviewed.

Reviewing the accounting, auditing and process of financial reporting of Boral limited

Managing and identifying the significant risk areas by establishing process and system of

management and the board (Chan & Vasarhelyi, 2018).

The committee meets its responsibilities under the charter as it is entrusted with the

necessary resources and power. All this include explanation of additional information and

right of management access.

Committee is also entrusted with the responsibility of monitoring and establishing

financial and accounting control procedures and policies for ensuring that the financial

records are reliable and accurate.

7) Audit opinion expressed:

The auditor of Boral limited has formed an opinion on the financial report that the

accompanying financial reports prepared by the company is according to the requirements of

Corporation Act, 2001, Corporation regulation act and Australian accounting standard that gives

a fair and true view of the financial performance of company. The audit of the financial

statements comprising of statement of change in equity, statement of comprehensive income,

income statement, statement of cash flow have been conducted according to the Australian

auditing standard (Chen et al., 2017). The evidence of audit that has been obtained is considered

appropriate and sufficient for providing basis of opinion.

8) Difference between the responsibilities of management and auditors:

The responsibilities of auditor and director differ and the differences are outlined in the

annual report of the Boral limited. Director’s responsibility lies in the preparation of the annual

AUDITING THEORY AND PRACTICE

Financial information provided to the public and shareholder of company should be

reviewed.

Reviewing the accounting, auditing and process of financial reporting of Boral limited

Managing and identifying the significant risk areas by establishing process and system of

management and the board (Chan & Vasarhelyi, 2018).

The committee meets its responsibilities under the charter as it is entrusted with the

necessary resources and power. All this include explanation of additional information and

right of management access.

Committee is also entrusted with the responsibility of monitoring and establishing

financial and accounting control procedures and policies for ensuring that the financial

records are reliable and accurate.

7) Audit opinion expressed:

The auditor of Boral limited has formed an opinion on the financial report that the

accompanying financial reports prepared by the company is according to the requirements of

Corporation Act, 2001, Corporation regulation act and Australian accounting standard that gives

a fair and true view of the financial performance of company. The audit of the financial

statements comprising of statement of change in equity, statement of comprehensive income,

income statement, statement of cash flow have been conducted according to the Australian

auditing standard (Chen et al., 2017). The evidence of audit that has been obtained is considered

appropriate and sufficient for providing basis of opinion.

8) Difference between the responsibilities of management and auditors:

The responsibilities of auditor and director differ and the differences are outlined in the

annual report of the Boral limited. Director’s responsibility lies in the preparation of the annual

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.