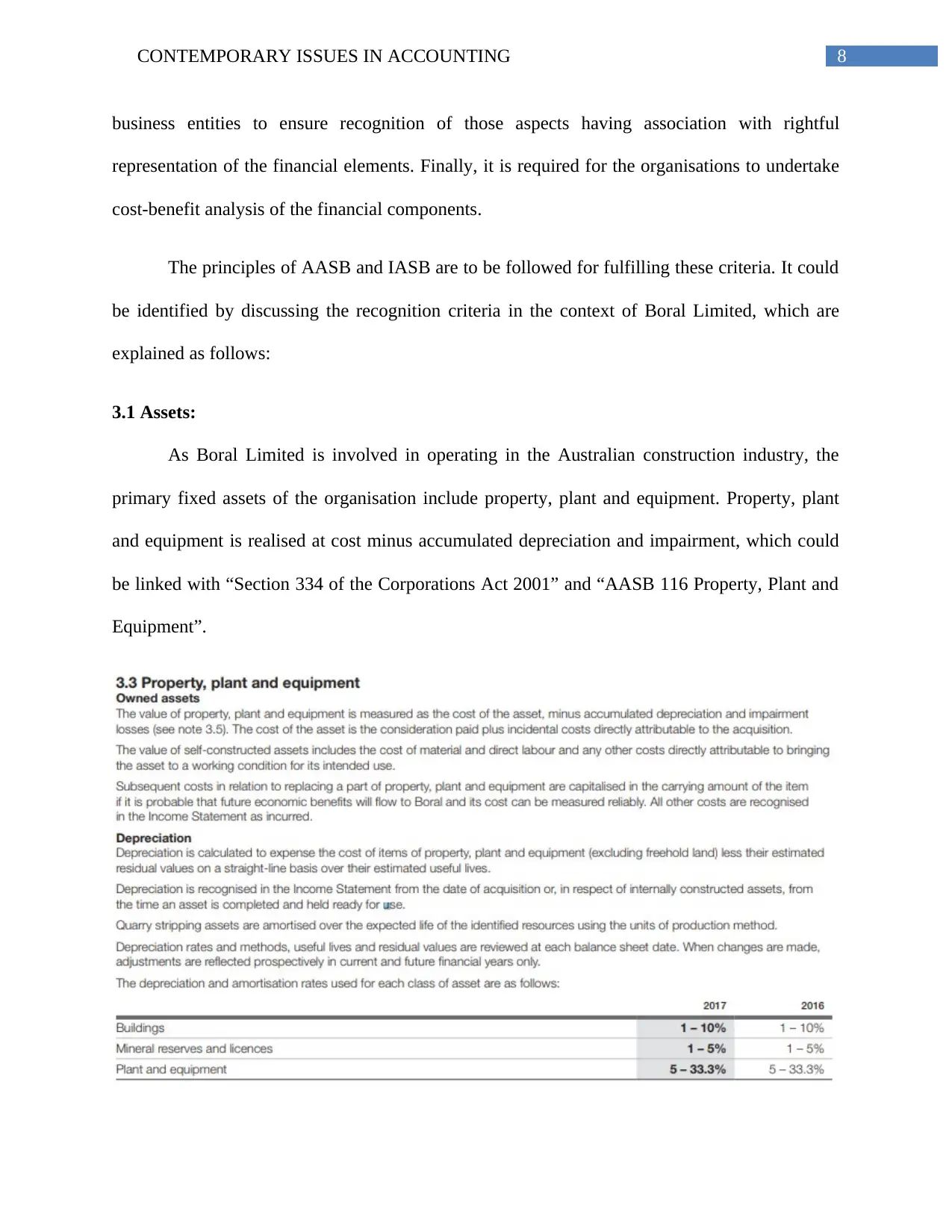

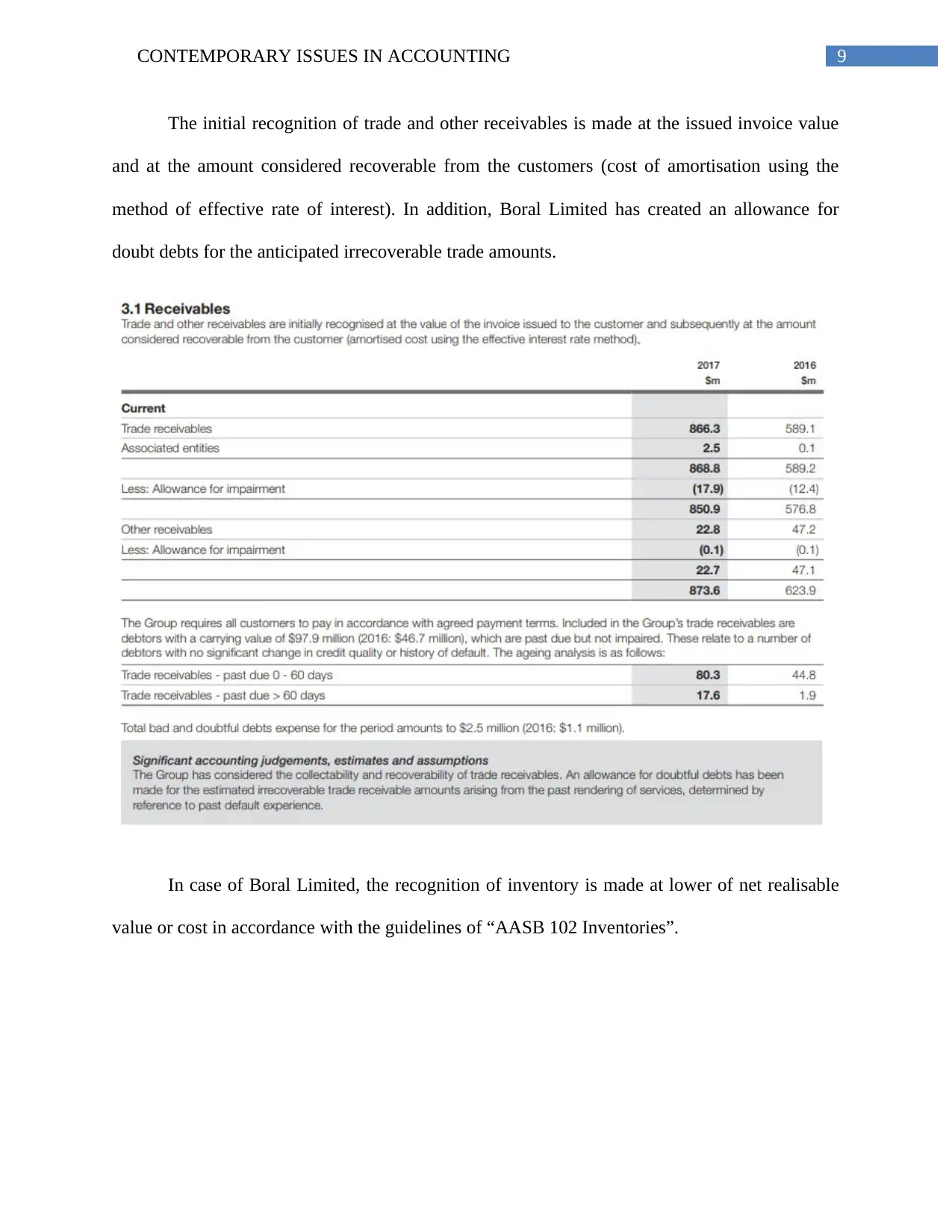

Boral Limited's Financial Reporting Under Conceptual Framework

VerifiedAdded on 2023/06/13

|18

|2502

|148

Report

AI Summary

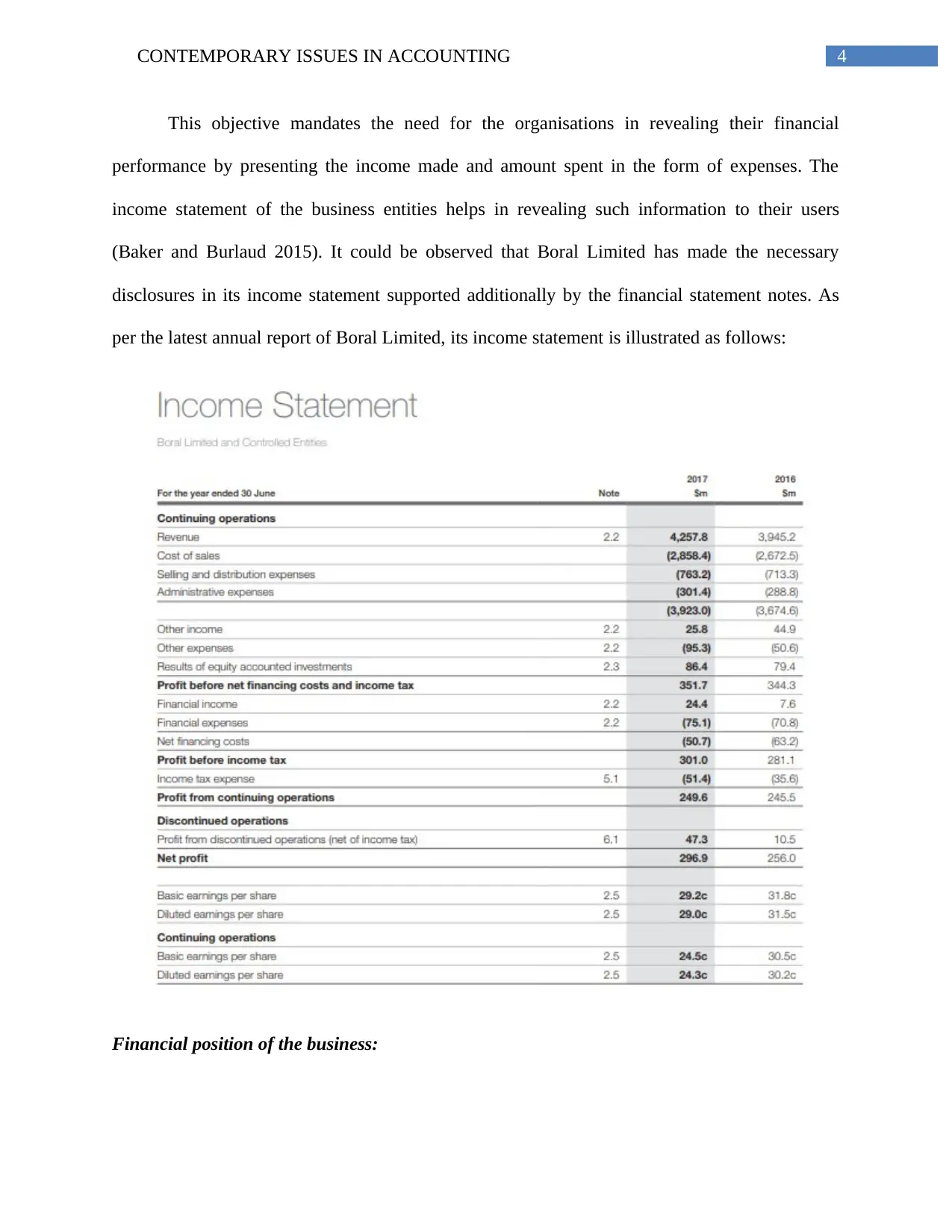

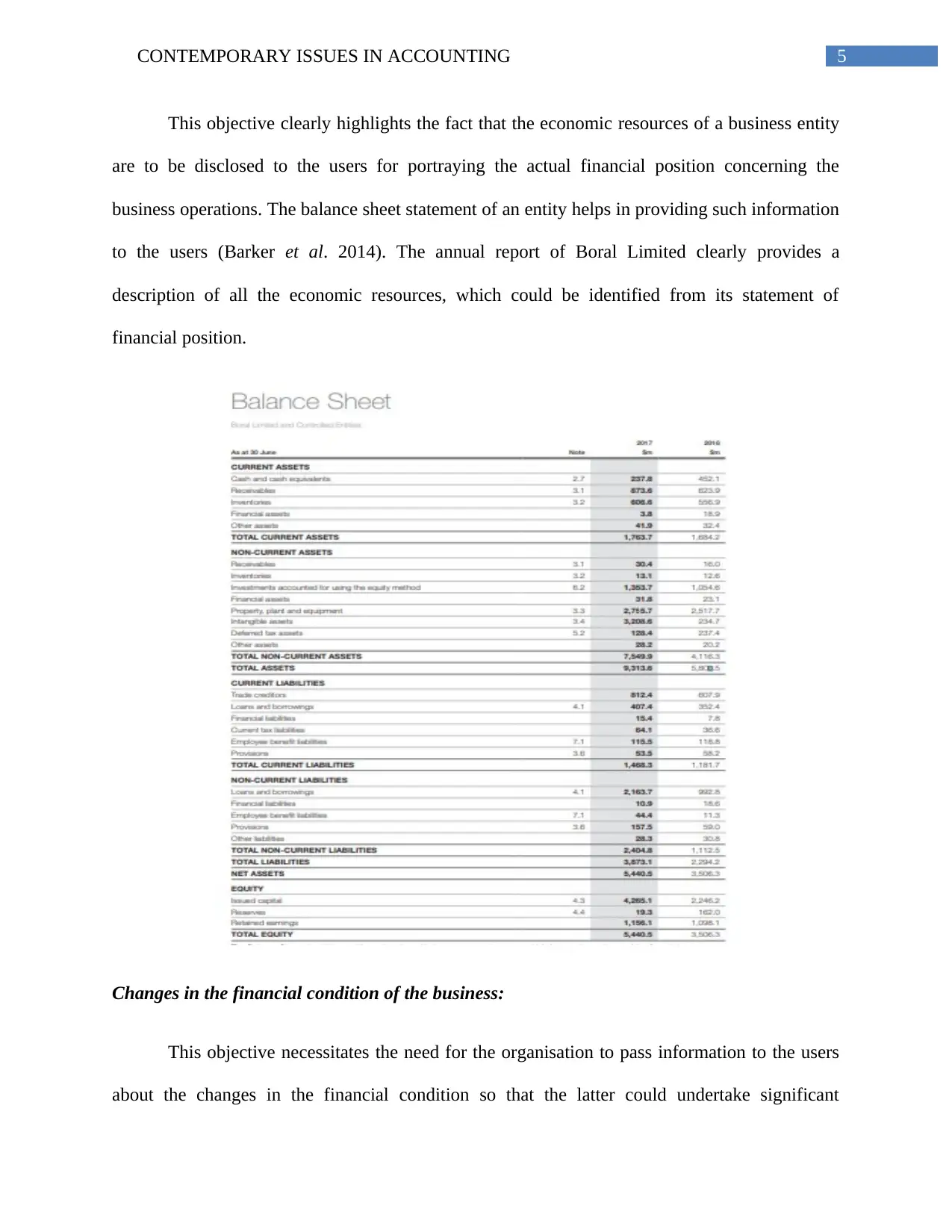

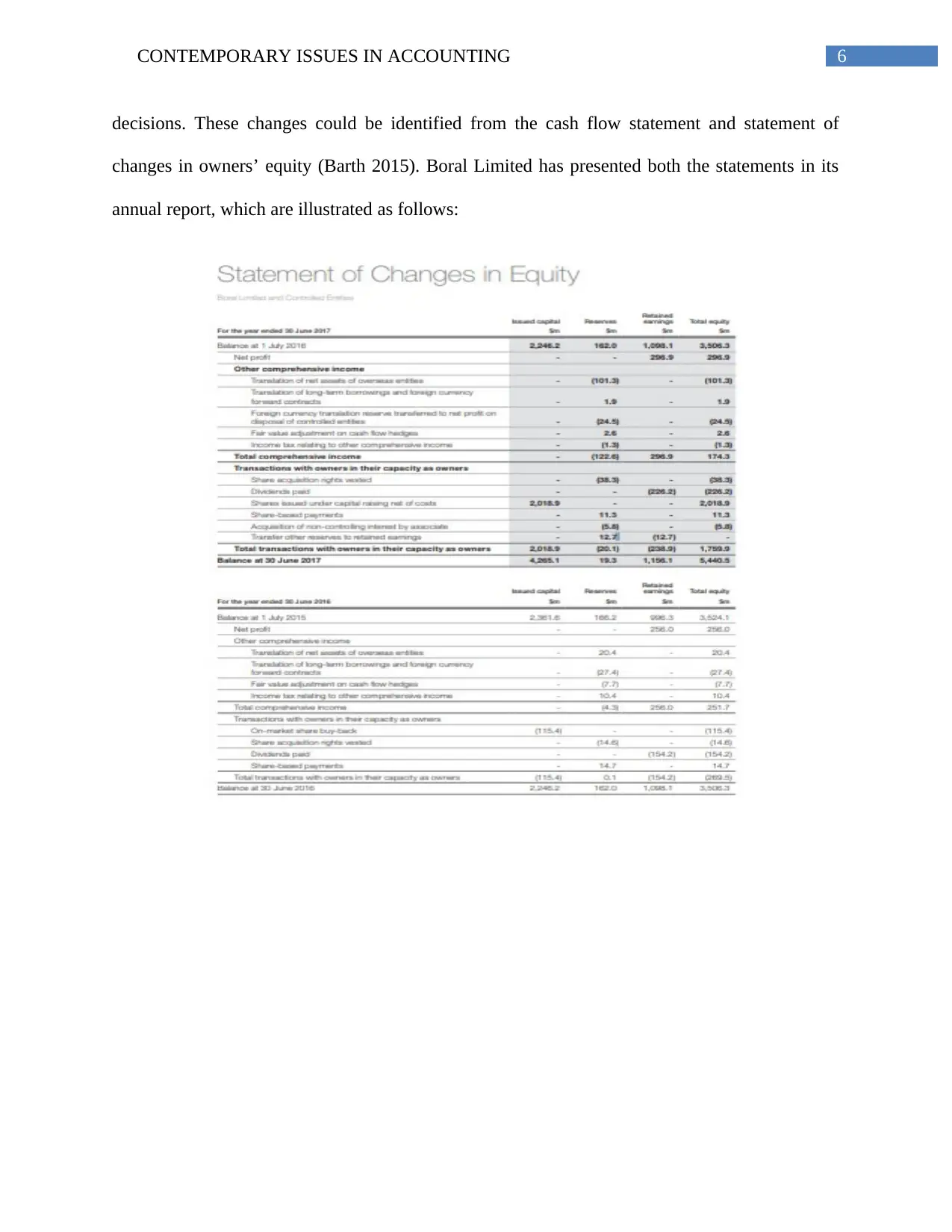

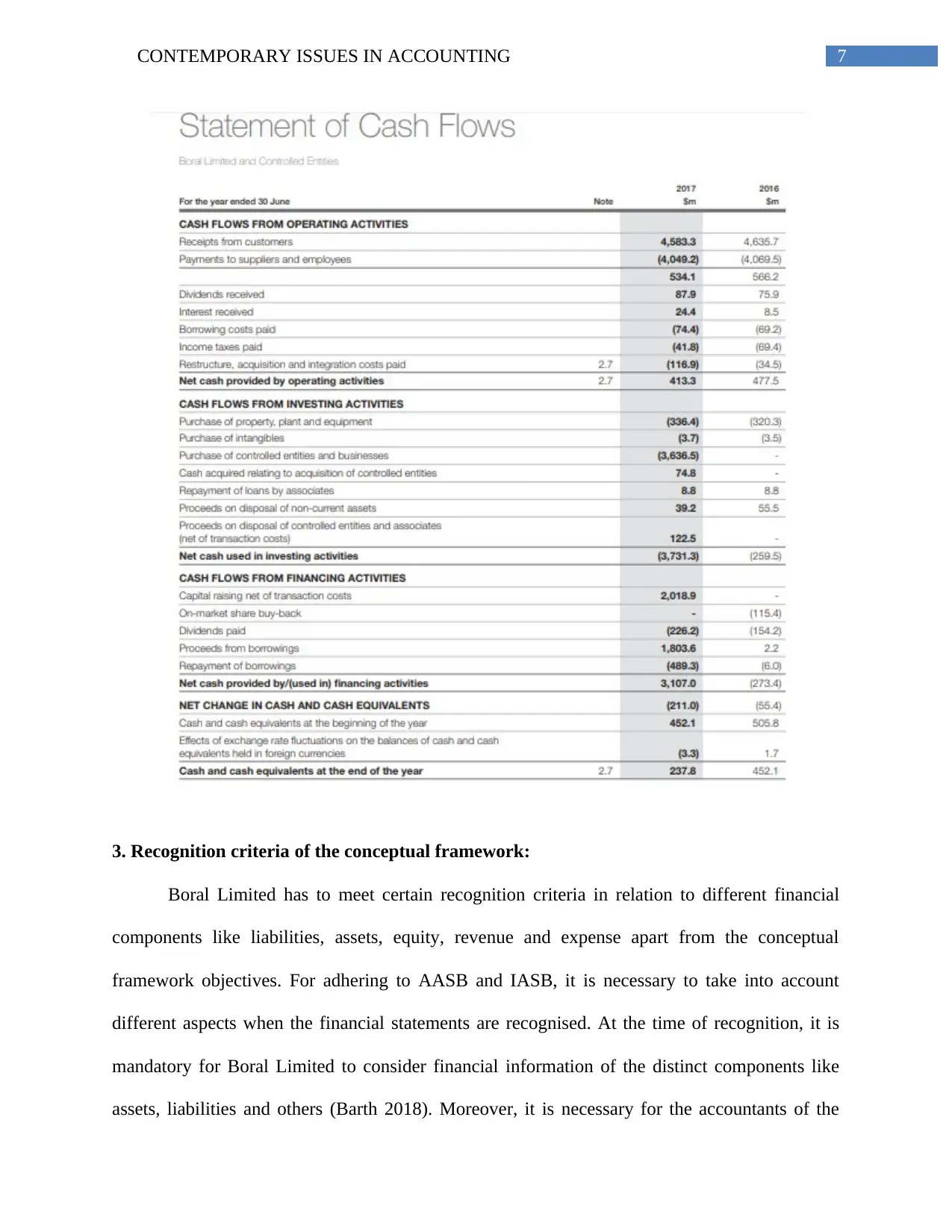

This report examines Boral Limited's adherence to the AASB and IASB conceptual framework in its financial reporting practices. It assesses the company's alignment with the objectives of the framework, including the presentation of financial performance, position, and changes in financial condition. The report further evaluates Boral Limited's recognition criteria for assets, liabilities, equity, revenue, and expenses, ensuring compliance with relevant accounting standards. Finally, it analyzes the presence of fundamental and enhancing qualitative characteristics within Boral Limited's financial statements, confirming the reliability, relevance, verifiability, comparability, timeliness, and understandability of its reported financial information. The analysis confirms that Boral Limited effectively complies with the guidelines and principles of the conceptual framework.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.