Improving Accounting System at Borger Management Inc.: A Project

VerifiedAdded on 2019/09/30

|9

|3318

|265

Project

AI Summary

This project analyzes the accounting system of Borger Management, Inc., a property management company facing challenges due to the use of multiple incompatible accounting software systems. The company's current process involves manual data conversion, leading to errors, high consultant costs, and delayed financial reporting. The project outlines the problem, affected business activities, and the performance gap. It then details the requirements for a new system, including stakeholder considerations, business environment factors, new capabilities, cost limitations, and security requirements. The project explores four alternative solutions: hiring an in-house staff, hiring a software designer, using Software as a Service (SaaS), and renegotiating with consultants. It provides a risk assessment for each solution, evaluating the probability and impact of potential risks. The project concludes by ranking the solutions and suggesting that a single integrated accounting system would improve efficiency, reduce costs, and enhance the accuracy of financial reporting. The project suggests that the most promising solution is to hire a software designer to create a new accounting system and use it to replace the current system.

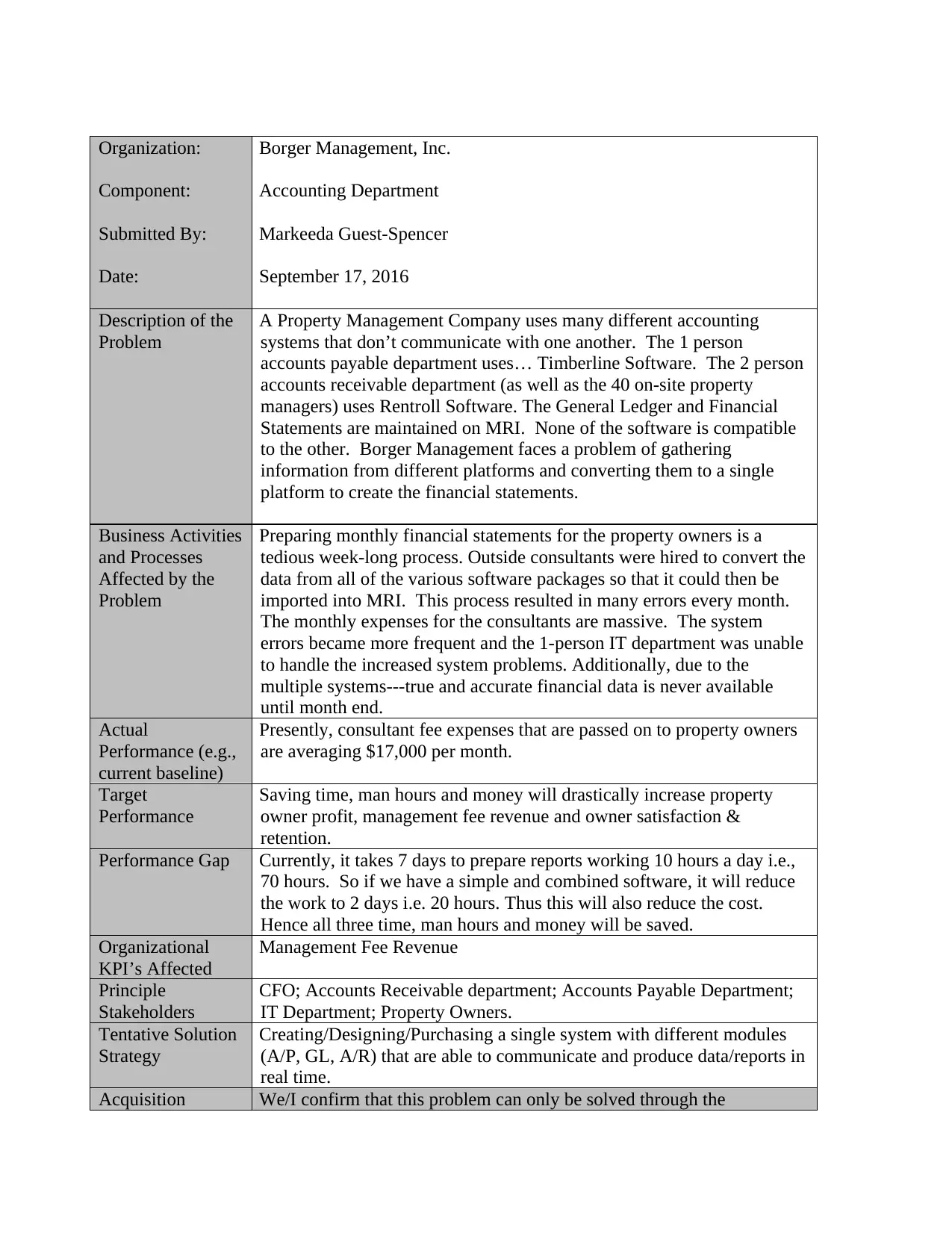

Organization:

Component:

Submitted By:

Date:

Borger Management, Inc.

Accounting Department

Markeeda Guest-Spencer

September 17, 2016

Description of the

Problem

A Property Management Company uses many different accounting

systems that don’t communicate with one another. The 1 person

accounts payable department uses… Timberline Software. The 2 person

accounts receivable department (as well as the 40 on-site property

managers) uses Rentroll Software. The General Ledger and Financial

Statements are maintained on MRI. None of the software is compatible

to the other. Borger Management faces a problem of gathering

information from different platforms and converting them to a single

platform to create the financial statements.

Business Activities

and Processes

Affected by the

Problem

Preparing monthly financial statements for the property owners is a

tedious week-long process. Outside consultants were hired to convert the

data from all of the various software packages so that it could then be

imported into MRI. This process resulted in many errors every month.

The monthly expenses for the consultants are massive. The system

errors became more frequent and the 1-person IT department was unable

to handle the increased system problems. Additionally, due to the

multiple systems---true and accurate financial data is never available

until month end.

Actual

Performance (e.g.,

current baseline)

Presently, consultant fee expenses that are passed on to property owners

are averaging $17,000 per month.

Target

Performance

Saving time, man hours and money will drastically increase property

owner profit, management fee revenue and owner satisfaction &

retention.

Performance Gap Currently, it takes 7 days to prepare reports working 10 hours a day i.e.,

70 hours. So if we have a simple and combined software, it will reduce

the work to 2 days i.e. 20 hours. Thus this will also reduce the cost.

Hence all three time, man hours and money will be saved.

Organizational

KPI’s Affected

Management Fee Revenue

Principle

Stakeholders

CFO; Accounts Receivable department; Accounts Payable Department;

IT Department; Property Owners.

Tentative Solution

Strategy

Creating/Designing/Purchasing a single system with different modules

(A/P, GL, A/R) that are able to communicate and produce data/reports in

real time.

Acquisition We/I confirm that this problem can only be solved through the

Component:

Submitted By:

Date:

Borger Management, Inc.

Accounting Department

Markeeda Guest-Spencer

September 17, 2016

Description of the

Problem

A Property Management Company uses many different accounting

systems that don’t communicate with one another. The 1 person

accounts payable department uses… Timberline Software. The 2 person

accounts receivable department (as well as the 40 on-site property

managers) uses Rentroll Software. The General Ledger and Financial

Statements are maintained on MRI. None of the software is compatible

to the other. Borger Management faces a problem of gathering

information from different platforms and converting them to a single

platform to create the financial statements.

Business Activities

and Processes

Affected by the

Problem

Preparing monthly financial statements for the property owners is a

tedious week-long process. Outside consultants were hired to convert the

data from all of the various software packages so that it could then be

imported into MRI. This process resulted in many errors every month.

The monthly expenses for the consultants are massive. The system

errors became more frequent and the 1-person IT department was unable

to handle the increased system problems. Additionally, due to the

multiple systems---true and accurate financial data is never available

until month end.

Actual

Performance (e.g.,

current baseline)

Presently, consultant fee expenses that are passed on to property owners

are averaging $17,000 per month.

Target

Performance

Saving time, man hours and money will drastically increase property

owner profit, management fee revenue and owner satisfaction &

retention.

Performance Gap Currently, it takes 7 days to prepare reports working 10 hours a day i.e.,

70 hours. So if we have a simple and combined software, it will reduce

the work to 2 days i.e. 20 hours. Thus this will also reduce the cost.

Hence all three time, man hours and money will be saved.

Organizational

KPI’s Affected

Management Fee Revenue

Principle

Stakeholders

CFO; Accounts Receivable department; Accounts Payable Department;

IT Department; Property Owners.

Tentative Solution

Strategy

Creating/Designing/Purchasing a single system with different modules

(A/P, GL, A/R) that are able to communicate and produce data/reports in

real time.

Acquisition We/I confirm that this problem can only be solved through the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

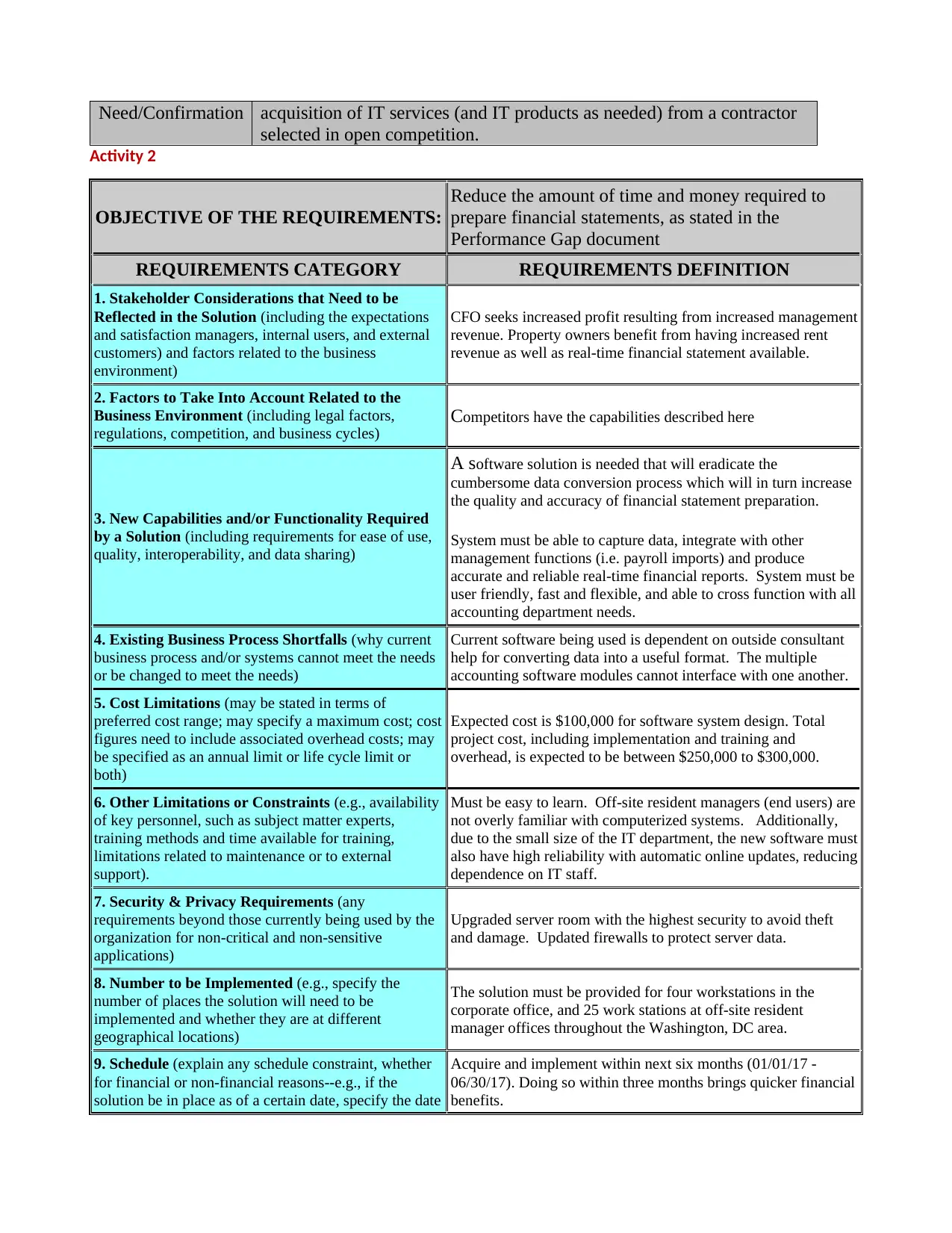

Need/Confirmation acquisition of IT services (and IT products as needed) from a contractor

selected in open competition.

Activity 2

OBJECTIVE OF THE REQUIREMENTS:

Reduce the amount of time and money required to

prepare financial statements, as stated in the

Performance Gap document

REQUIREMENTS CATEGORY REQUIREMENTS DEFINITION

1. Stakeholder Considerations that Need to be

Reflected in the Solution (including the expectations

and satisfaction managers, internal users, and external

customers) and factors related to the business

environment)

CFO seeks increased profit resulting from increased management

revenue. Property owners benefit from having increased rent

revenue as well as real-time financial statement available.

2. Factors to Take Into Account Related to the

Business Environment (including legal factors,

regulations, competition, and business cycles)

Competitors have the capabilities described here

3. New Capabilities and/or Functionality Required

by a Solution (including requirements for ease of use,

quality, interoperability, and data sharing)

A software solution is needed that will eradicate the

cumbersome data conversion process which will in turn increase

the quality and accuracy of financial statement preparation.

System must be able to capture data, integrate with other

management functions (i.e. payroll imports) and produce

accurate and reliable real-time financial reports. System must be

user friendly, fast and flexible, and able to cross function with all

accounting department needs.

4. Existing Business Process Shortfalls (why current

business process and/or systems cannot meet the needs

or be changed to meet the needs)

Current software being used is dependent on outside consultant

help for converting data into a useful format. The multiple

accounting software modules cannot interface with one another.

5. Cost Limitations (may be stated in terms of

preferred cost range; may specify a maximum cost; cost

figures need to include associated overhead costs; may

be specified as an annual limit or life cycle limit or

both)

Expected cost is $100,000 for software system design. Total

project cost, including implementation and training and

overhead, is expected to be between $250,000 to $300,000.

6. Other Limitations or Constraints (e.g., availability

of key personnel, such as subject matter experts,

training methods and time available for training,

limitations related to maintenance or to external

support).

Must be easy to learn. Off-site resident managers (end users) are

not overly familiar with computerized systems. Additionally,

due to the small size of the IT department, the new software must

also have high reliability with automatic online updates, reducing

dependence on IT staff.

7. Security & Privacy Requirements (any

requirements beyond those currently being used by the

organization for non-critical and non-sensitive

applications)

Upgraded server room with the highest security to avoid theft

and damage. Updated firewalls to protect server data.

8. Number to be Implemented (e.g., specify the

number of places the solution will need to be

implemented and whether they are at different

geographical locations)

The solution must be provided for four workstations in the

corporate office, and 25 work stations at off-site resident

manager offices throughout the Washington, DC area.

9. Schedule (explain any schedule constraint, whether

for financial or non-financial reasons--e.g., if the

solution be in place as of a certain date, specify the date

Acquire and implement within next six months (01/01/17 -

06/30/17). Doing so within three months brings quicker financial

benefits.

selected in open competition.

Activity 2

OBJECTIVE OF THE REQUIREMENTS:

Reduce the amount of time and money required to

prepare financial statements, as stated in the

Performance Gap document

REQUIREMENTS CATEGORY REQUIREMENTS DEFINITION

1. Stakeholder Considerations that Need to be

Reflected in the Solution (including the expectations

and satisfaction managers, internal users, and external

customers) and factors related to the business

environment)

CFO seeks increased profit resulting from increased management

revenue. Property owners benefit from having increased rent

revenue as well as real-time financial statement available.

2. Factors to Take Into Account Related to the

Business Environment (including legal factors,

regulations, competition, and business cycles)

Competitors have the capabilities described here

3. New Capabilities and/or Functionality Required

by a Solution (including requirements for ease of use,

quality, interoperability, and data sharing)

A software solution is needed that will eradicate the

cumbersome data conversion process which will in turn increase

the quality and accuracy of financial statement preparation.

System must be able to capture data, integrate with other

management functions (i.e. payroll imports) and produce

accurate and reliable real-time financial reports. System must be

user friendly, fast and flexible, and able to cross function with all

accounting department needs.

4. Existing Business Process Shortfalls (why current

business process and/or systems cannot meet the needs

or be changed to meet the needs)

Current software being used is dependent on outside consultant

help for converting data into a useful format. The multiple

accounting software modules cannot interface with one another.

5. Cost Limitations (may be stated in terms of

preferred cost range; may specify a maximum cost; cost

figures need to include associated overhead costs; may

be specified as an annual limit or life cycle limit or

both)

Expected cost is $100,000 for software system design. Total

project cost, including implementation and training and

overhead, is expected to be between $250,000 to $300,000.

6. Other Limitations or Constraints (e.g., availability

of key personnel, such as subject matter experts,

training methods and time available for training,

limitations related to maintenance or to external

support).

Must be easy to learn. Off-site resident managers (end users) are

not overly familiar with computerized systems. Additionally,

due to the small size of the IT department, the new software must

also have high reliability with automatic online updates, reducing

dependence on IT staff.

7. Security & Privacy Requirements (any

requirements beyond those currently being used by the

organization for non-critical and non-sensitive

applications)

Upgraded server room with the highest security to avoid theft

and damage. Updated firewalls to protect server data.

8. Number to be Implemented (e.g., specify the

number of places the solution will need to be

implemented and whether they are at different

geographical locations)

The solution must be provided for four workstations in the

corporate office, and 25 work stations at off-site resident

manager offices throughout the Washington, DC area.

9. Schedule (explain any schedule constraint, whether

for financial or non-financial reasons--e.g., if the

solution be in place as of a certain date, specify the date

Acquire and implement within next six months (01/01/17 -

06/30/17). Doing so within three months brings quicker financial

benefits.

and why)

10. Other Requirements Not Specified Above (e.g.,

any related to vendors, consultants, partnerships with

other entities, unique user interface requirements,

documentation needs, special certification

requirements)

Due to IT department size and expertise, the new software must

require minimal in-house support; online training and tech

support is necessary.

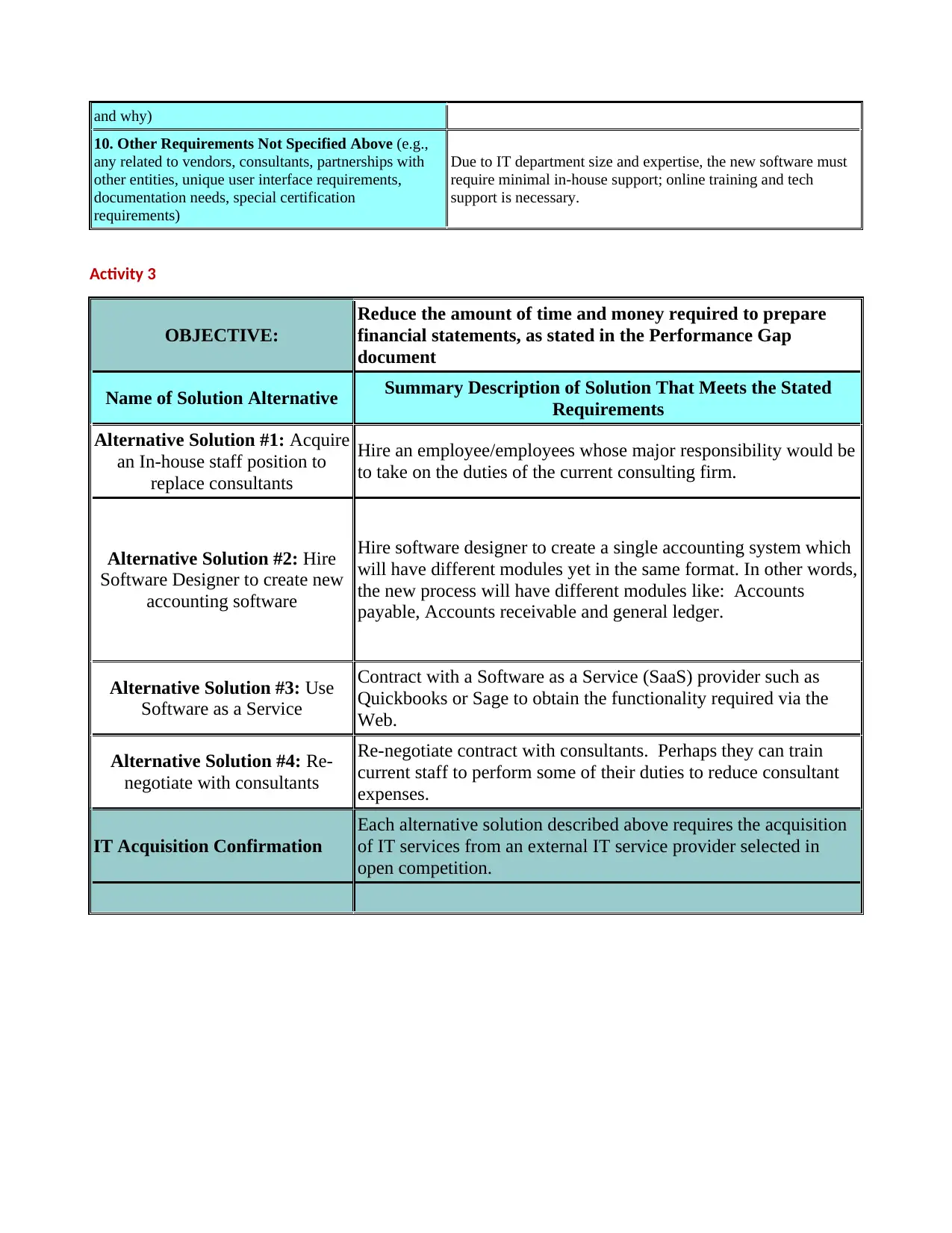

Activity 3

OBJECTIVE:

Reduce the amount of time and money required to prepare

financial statements, as stated in the Performance Gap

document

Name of Solution Alternative Summary Description of Solution That Meets the Stated

Requirements

Alternative Solution #1: Acquire

an In-house staff position to

replace consultants

Hire an employee/employees whose major responsibility would be

to take on the duties of the current consulting firm.

Alternative Solution #2: Hire

Software Designer to create new

accounting software

Hire software designer to create a single accounting system which

will have different modules yet in the same format. In other words,

the new process will have different modules like: Accounts

payable, Accounts receivable and general ledger.

Alternative Solution #3: Use

Software as a Service

Contract with a Software as a Service (SaaS) provider such as

Quickbooks or Sage to obtain the functionality required via the

Web.

Alternative Solution #4: Re-

negotiate with consultants

Re-negotiate contract with consultants. Perhaps they can train

current staff to perform some of their duties to reduce consultant

expenses.

IT Acquisition Confirmation

Each alternative solution described above requires the acquisition

of IT services from an external IT service provider selected in

open competition.

10. Other Requirements Not Specified Above (e.g.,

any related to vendors, consultants, partnerships with

other entities, unique user interface requirements,

documentation needs, special certification

requirements)

Due to IT department size and expertise, the new software must

require minimal in-house support; online training and tech

support is necessary.

Activity 3

OBJECTIVE:

Reduce the amount of time and money required to prepare

financial statements, as stated in the Performance Gap

document

Name of Solution Alternative Summary Description of Solution That Meets the Stated

Requirements

Alternative Solution #1: Acquire

an In-house staff position to

replace consultants

Hire an employee/employees whose major responsibility would be

to take on the duties of the current consulting firm.

Alternative Solution #2: Hire

Software Designer to create new

accounting software

Hire software designer to create a single accounting system which

will have different modules yet in the same format. In other words,

the new process will have different modules like: Accounts

payable, Accounts receivable and general ledger.

Alternative Solution #3: Use

Software as a Service

Contract with a Software as a Service (SaaS) provider such as

Quickbooks or Sage to obtain the functionality required via the

Web.

Alternative Solution #4: Re-

negotiate with consultants

Re-negotiate contract with consultants. Perhaps they can train

current staff to perform some of their duties to reduce consultant

expenses.

IT Acquisition Confirmation

Each alternative solution described above requires the acquisition

of IT services from an external IT service provider selected in

open competition.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

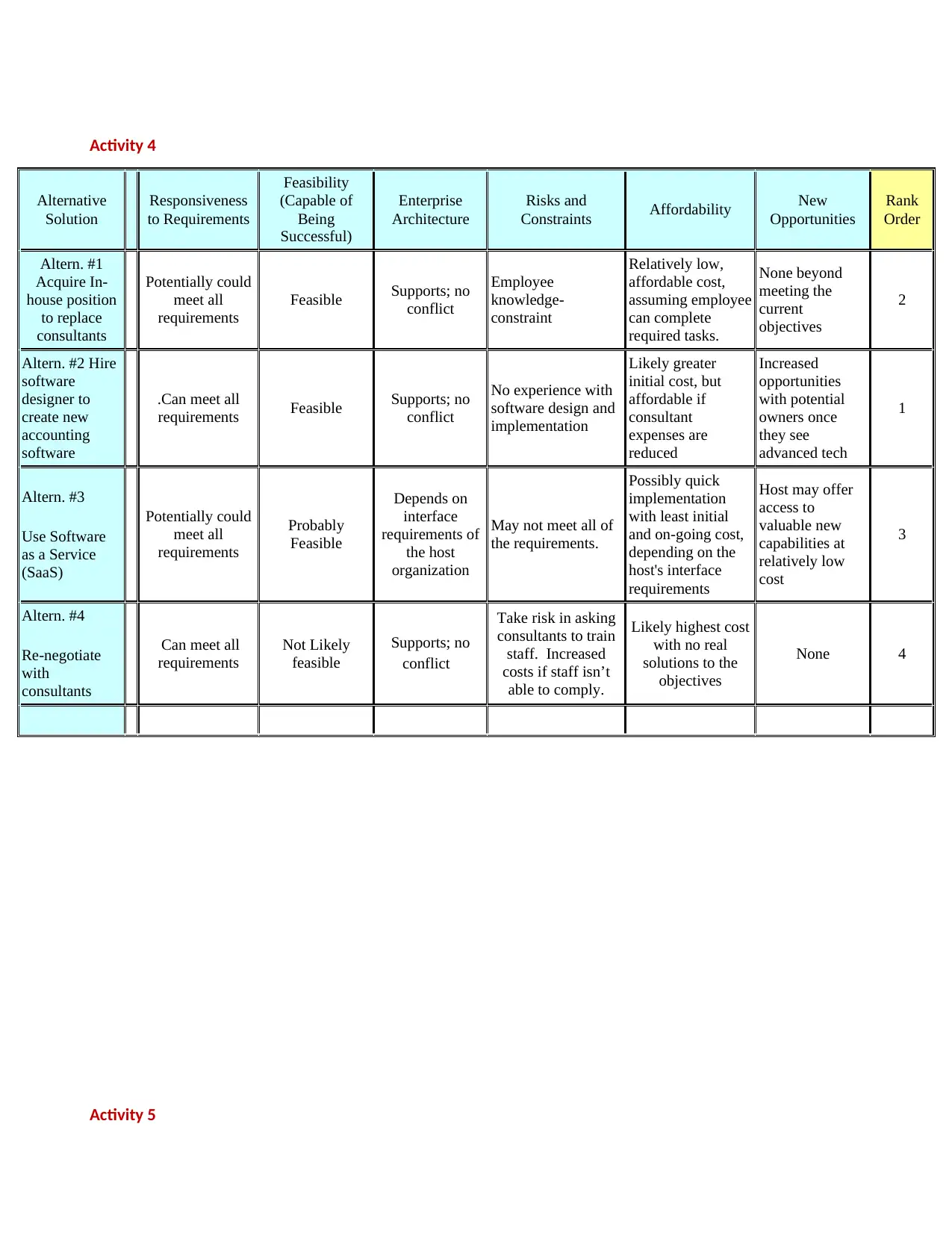

Activity 4

Alternative

Solution

Responsiveness

to Requirements

Feasibility

(Capable of

Being

Successful)

Enterprise

Architecture

Risks and

Constraints Affordability New

Opportunities

Rank

Order

Altern. #1

Acquire In-

house position

to replace

consultants

Potentially could

meet all

requirements

Feasible Supports; no

conflict

Employee

knowledge-

constraint

Relatively low,

affordable cost,

assuming employee

can complete

required tasks.

None beyond

meeting the

current

objectives

2

Altern. #2 Hire

software

designer to

create new

accounting

software

.Can meet all

requirements Feasible Supports; no

conflict

No experience with

software design and

implementation

Likely greater

initial cost, but

affordable if

consultant

expenses are

reduced

Increased

opportunities

with potential

owners once

they see

advanced tech

1

Altern. #3

Use Software

as a Service

(SaaS)

Potentially could

meet all

requirements

Probably

Feasible

Depends on

interface

requirements of

the host

organization

May not meet all of

the requirements.

Possibly quick

implementation

with least initial

and on-going cost,

depending on the

host's interface

requirements

Host may offer

access to

valuable new

capabilities at

relatively low

cost

3

Altern. #4

Re-negotiate

with

consultants

.Can meet all

requirements

Not Likely

feasible

Supports; no

conflict .

Take risk in asking

consultants to train

staff. Increased

costs if staff isn’t

able to comply.

Likely highest cost

with no real

solutions to the

objectives

None 4

Activity 5

Alternative

Solution

Responsiveness

to Requirements

Feasibility

(Capable of

Being

Successful)

Enterprise

Architecture

Risks and

Constraints Affordability New

Opportunities

Rank

Order

Altern. #1

Acquire In-

house position

to replace

consultants

Potentially could

meet all

requirements

Feasible Supports; no

conflict

Employee

knowledge-

constraint

Relatively low,

affordable cost,

assuming employee

can complete

required tasks.

None beyond

meeting the

current

objectives

2

Altern. #2 Hire

software

designer to

create new

accounting

software

.Can meet all

requirements Feasible Supports; no

conflict

No experience with

software design and

implementation

Likely greater

initial cost, but

affordable if

consultant

expenses are

reduced

Increased

opportunities

with potential

owners once

they see

advanced tech

1

Altern. #3

Use Software

as a Service

(SaaS)

Potentially could

meet all

requirements

Probably

Feasible

Depends on

interface

requirements of

the host

organization

May not meet all of

the requirements.

Possibly quick

implementation

with least initial

and on-going cost,

depending on the

host's interface

requirements

Host may offer

access to

valuable new

capabilities at

relatively low

cost

3

Altern. #4

Re-negotiate

with

consultants

.Can meet all

requirements

Not Likely

feasible

Supports; no

conflict .

Take risk in asking

consultants to train

staff. Increased

costs if staff isn’t

able to comply.

Likely highest cost

with no real

solutions to the

objectives

None 4

Activity 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

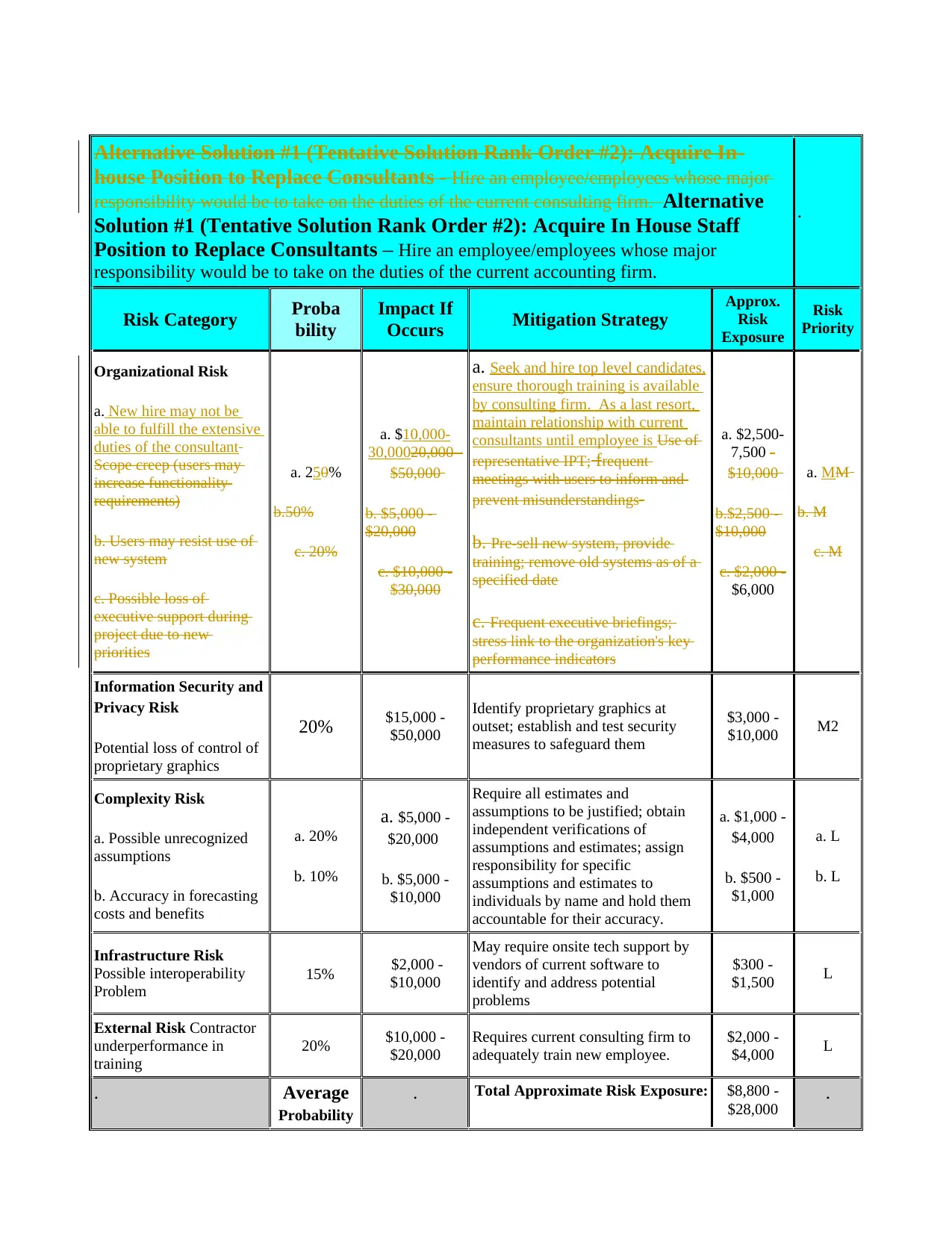

Alternative Solution #1 (Tentative Solution Rank Order #2): Acquire In-

house Position to Replace Consultants - Hire an employee/employees whose major

responsibility would be to take on the duties of the current consulting firm. Alternative

Solution #1 (Tentative Solution Rank Order #2): Acquire In House Staff

Position to Replace Consultants – Hire an employee/employees whose major

responsibility would be to take on the duties of the current accounting firm.

.

Risk Category Proba

bility

Impact If

Occurs Mitigation Strategy

Approx.

Risk

Exposure

Risk

Priority

Organizational Risk

a. New hire may not be

able to fulfill the extensive

duties of the consultant

Scope creep (users may

increase functionality

requirements)

b. Users may resist use of

new system

c. Possible loss of

executive support during

project due to new

priorities

a. 250%

b.50%

c. 20%

a. $10,000-

30,00020,000 -

$50,000

b. $5,000 -

$20,000

c. $10,000 -

$30,000

a. Seek and hire top level candidates,

ensure thorough training is available

by consulting firm. As a last resort,

maintain relationship with current

consultants until employee is Use of

representative IPT; frequent

meetings with users to inform and

prevent misunderstandings

b. Pre-sell new system, provide

training; remove old systems as of a

specified date

c. Frequent executive briefings;

stress link to the organization's key

performance indicators

a. $2,500-

7,500 -

$10,000

b.$2,500 -

$10,000

c. $2,000 -

$6,000

a. MM

b. M

c. M

Information Security and

Privacy Risk

Potential loss of control of

proprietary graphics

20% $15,000 -

$50,000

Identify proprietary graphics at

outset; establish and test security

measures to safeguard them

$3,000 -

$10,000 M2

Complexity Risk

a. Possible unrecognized

assumptions

b. Accuracy in forecasting

costs and benefits

a. 20%

b. 10%

a. $5,000 -

$20,000.

b. $5,000 -

$10,000

Require all estimates and

assumptions to be justified; obtain

independent verifications of

assumptions and estimates; assign

responsibility for specific

assumptions and estimates to

individuals by name and hold them

accountable for their accuracy.

a. $1,000 -

$4,000

b. $500 -

$1,000

a. L

b. L

Infrastructure Risk

Possible interoperability

Problem

. 15% .$2,000 -

$10,000

May require onsite tech support by

vendors of current software to

identify and address potential

problems

$300 -

$1,500 L

External Risk Contractor

underperformance in

training

20% $10,000 -

$20,000

Requires current consulting firm to

adequately train new employee.

$2,000 -

$4,000 L

. Average

Probability

. Total Approximate Risk Exposure: $8,800 -

$28,000 .

house Position to Replace Consultants - Hire an employee/employees whose major

responsibility would be to take on the duties of the current consulting firm. Alternative

Solution #1 (Tentative Solution Rank Order #2): Acquire In House Staff

Position to Replace Consultants – Hire an employee/employees whose major

responsibility would be to take on the duties of the current accounting firm.

.

Risk Category Proba

bility

Impact If

Occurs Mitigation Strategy

Approx.

Risk

Exposure

Risk

Priority

Organizational Risk

a. New hire may not be

able to fulfill the extensive

duties of the consultant

Scope creep (users may

increase functionality

requirements)

b. Users may resist use of

new system

c. Possible loss of

executive support during

project due to new

priorities

a. 250%

b.50%

c. 20%

a. $10,000-

30,00020,000 -

$50,000

b. $5,000 -

$20,000

c. $10,000 -

$30,000

a. Seek and hire top level candidates,

ensure thorough training is available

by consulting firm. As a last resort,

maintain relationship with current

consultants until employee is Use of

representative IPT; frequent

meetings with users to inform and

prevent misunderstandings

b. Pre-sell new system, provide

training; remove old systems as of a

specified date

c. Frequent executive briefings;

stress link to the organization's key

performance indicators

a. $2,500-

7,500 -

$10,000

b.$2,500 -

$10,000

c. $2,000 -

$6,000

a. MM

b. M

c. M

Information Security and

Privacy Risk

Potential loss of control of

proprietary graphics

20% $15,000 -

$50,000

Identify proprietary graphics at

outset; establish and test security

measures to safeguard them

$3,000 -

$10,000 M2

Complexity Risk

a. Possible unrecognized

assumptions

b. Accuracy in forecasting

costs and benefits

a. 20%

b. 10%

a. $5,000 -

$20,000.

b. $5,000 -

$10,000

Require all estimates and

assumptions to be justified; obtain

independent verifications of

assumptions and estimates; assign

responsibility for specific

assumptions and estimates to

individuals by name and hold them

accountable for their accuracy.

a. $1,000 -

$4,000

b. $500 -

$1,000

a. L

b. L

Infrastructure Risk

Possible interoperability

Problem

. 15% .$2,000 -

$10,000

May require onsite tech support by

vendors of current software to

identify and address potential

problems

$300 -

$1,500 L

External Risk Contractor

underperformance in

training

20% $10,000 -

$20,000

Requires current consulting firm to

adequately train new employee.

$2,000 -

$4,000 L

. Average

Probability

. Total Approximate Risk Exposure: $8,800 -

$28,000 .

18.33%

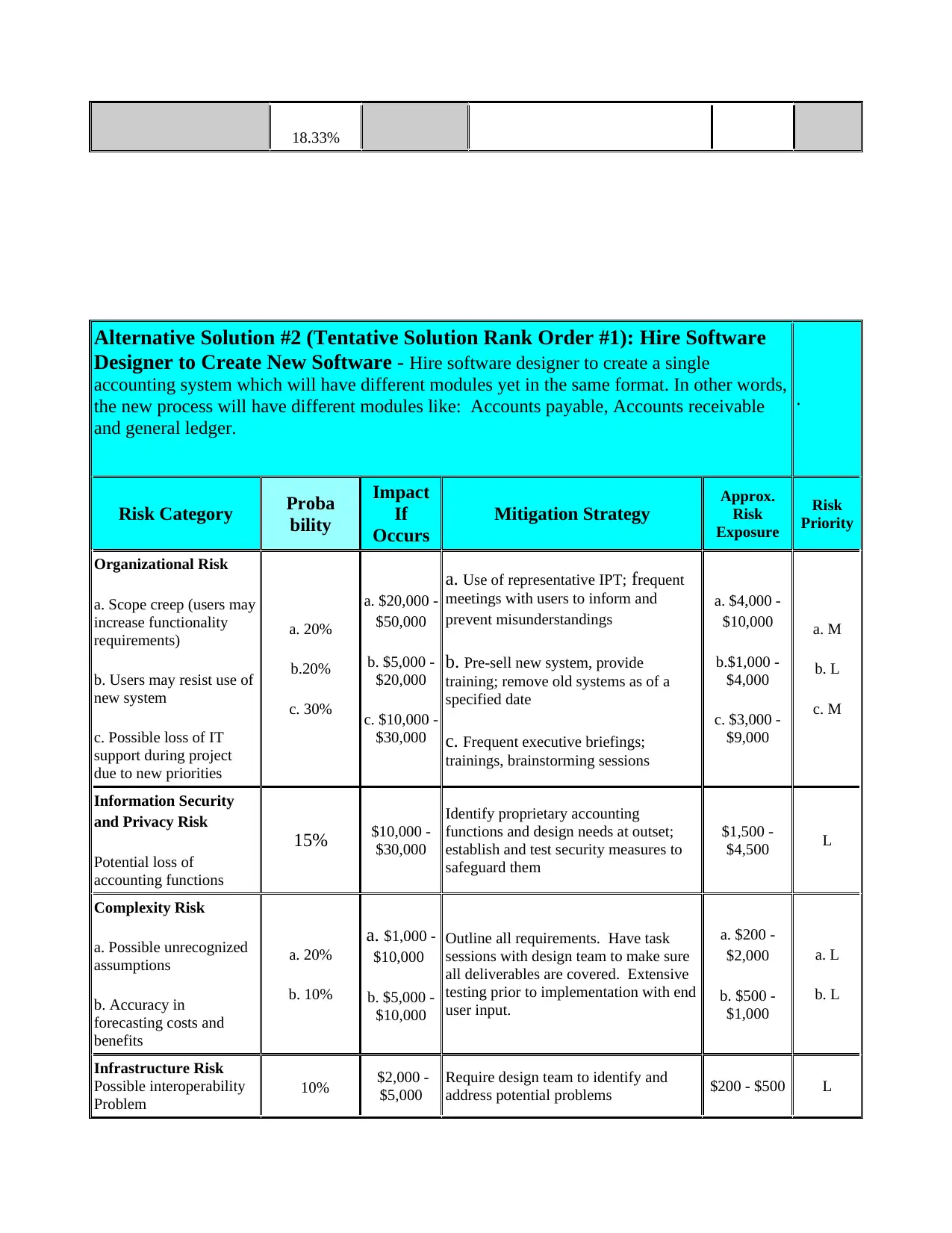

Alternative Solution #2 (Tentative Solution Rank Order #1): Hire Software

Designer to Create New Software - Hire software designer to create a single

accounting system which will have different modules yet in the same format. In other words,

the new process will have different modules like: Accounts payable, Accounts receivable

and general ledger.

.

Risk Category Proba

bility

Impact

If

Occurs

Mitigation Strategy

Approx.

Risk

Exposure

Risk

Priority

Organizational Risk

a. Scope creep (users may

increase functionality

requirements)

b. Users may resist use of

new system

c. Possible loss of IT

support during project

due to new priorities

a. 20%

b.20%

c. 30%

a. $20,000 -

$50,000

b. $5,000 -

$20,000

c. $10,000 -

$30,000

a. Use of representative IPT; frequent

meetings with users to inform and

prevent misunderstandings

b. Pre-sell new system, provide

training; remove old systems as of a

specified date

c. Frequent executive briefings;

trainings, brainstorming sessions

a. $4,000 -

$10,000

b.$1,000 -

$4,000

c. $3,000 -

$9,000

a. M

b. L

c. M

Information Security

and Privacy Risk

Potential loss of

accounting functions

15% $10,000 -

$30,000

Identify proprietary accounting

functions and design needs at outset;

establish and test security measures to

safeguard them

$1,500 -

$4,500 L

Complexity Risk

a. Possible unrecognized

assumptions

b. Accuracy in

forecasting costs and

benefits

a. 20%

b. 10%

a. $1,000 -

$10,000.

b. $5,000 -

$10,000

Outline all requirements. Have task

sessions with design team to make sure

all deliverables are covered. Extensive

testing prior to implementation with end

user input.

a. $200 -

$2,000

b. $500 -

$1,000

a. L

b. L

Infrastructure Risk

Possible interoperability

Problem

. 10% .$2,000 -

$5,000

Require design team to identify and

address potential problems $200 - $500 L

Alternative Solution #2 (Tentative Solution Rank Order #1): Hire Software

Designer to Create New Software - Hire software designer to create a single

accounting system which will have different modules yet in the same format. In other words,

the new process will have different modules like: Accounts payable, Accounts receivable

and general ledger.

.

Risk Category Proba

bility

Impact

If

Occurs

Mitigation Strategy

Approx.

Risk

Exposure

Risk

Priority

Organizational Risk

a. Scope creep (users may

increase functionality

requirements)

b. Users may resist use of

new system

c. Possible loss of IT

support during project

due to new priorities

a. 20%

b.20%

c. 30%

a. $20,000 -

$50,000

b. $5,000 -

$20,000

c. $10,000 -

$30,000

a. Use of representative IPT; frequent

meetings with users to inform and

prevent misunderstandings

b. Pre-sell new system, provide

training; remove old systems as of a

specified date

c. Frequent executive briefings;

trainings, brainstorming sessions

a. $4,000 -

$10,000

b.$1,000 -

$4,000

c. $3,000 -

$9,000

a. M

b. L

c. M

Information Security

and Privacy Risk

Potential loss of

accounting functions

15% $10,000 -

$30,000

Identify proprietary accounting

functions and design needs at outset;

establish and test security measures to

safeguard them

$1,500 -

$4,500 L

Complexity Risk

a. Possible unrecognized

assumptions

b. Accuracy in

forecasting costs and

benefits

a. 20%

b. 10%

a. $1,000 -

$10,000.

b. $5,000 -

$10,000

Outline all requirements. Have task

sessions with design team to make sure

all deliverables are covered. Extensive

testing prior to implementation with end

user input.

a. $200 -

$2,000

b. $500 -

$1,000

a. L

b. L

Infrastructure Risk

Possible interoperability

Problem

. 10% .$2,000 -

$5,000

Require design team to identify and

address potential problems $200 - $500 L

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

External Risk Designer

underperformance 10% $5,000 -

$10,000

Require certification of the software

design firm.

$500 -

$1,000 L

.

Average

Probability

16.87%

. Total Approximate Risk Exposure: $10,900 -

$32,000 .

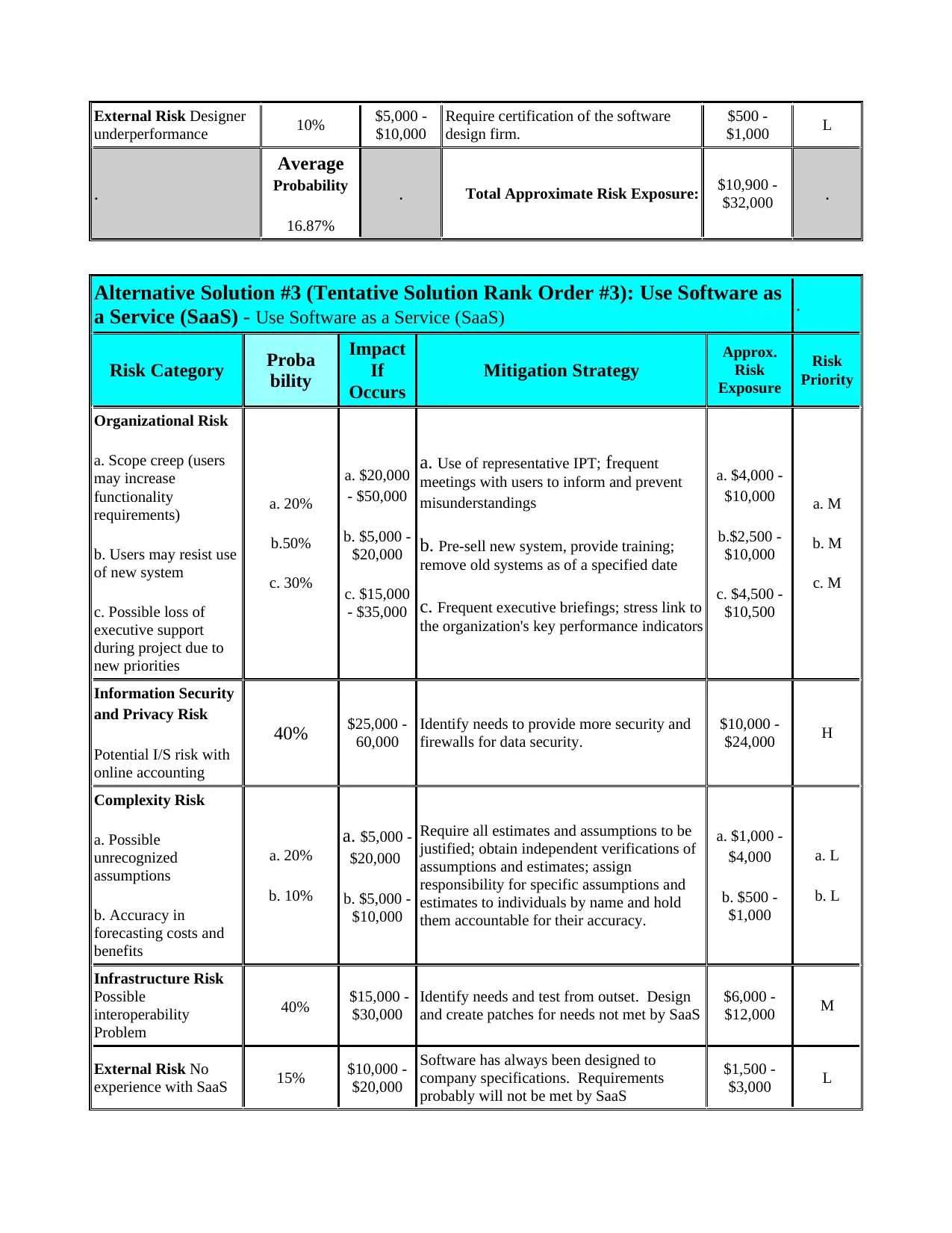

Alternative Solution #3 (Tentative Solution Rank Order #3): Use Software as

a Service (SaaS) - Use Software as a Service (SaaS) .

Risk Category Proba

bility

Impact

If

Occurs

Mitigation Strategy

Approx.

Risk

Exposure

Risk

Priority

Organizational Risk

a. Scope creep (users

may increase

functionality

requirements)

b. Users may resist use

of new system

c. Possible loss of

executive support

during project due to

new priorities

a. 20%

b.50%

c. 30%

a. $20,000

- $50,000

b. $5,000 -

$20,000

c. $15,000

- $35,000

a. Use of representative IPT; frequent

meetings with users to inform and prevent

misunderstandings

b. Pre-sell new system, provide training;

remove old systems as of a specified date

c. Frequent executive briefings; stress link to

the organization's key performance indicators

a. $4,000 -

$10,000

b.$2,500 -

$10,000

c. $4,500 -

$10,500

a. M

b. M

c. M

Information Security

and Privacy Risk

Potential I/S risk with

online accounting

40% $25,000 -

60,000

Identify needs to provide more security and

firewalls for data security.

$10,000 -

$24,000 H

Complexity Risk

a. Possible

unrecognized

assumptions

b. Accuracy in

forecasting costs and

benefits

a. 20%

b. 10%

a. $5,000 -

$20,000.

b. $5,000 -

$10,000

Require all estimates and assumptions to be

justified; obtain independent verifications of

assumptions and estimates; assign

responsibility for specific assumptions and

estimates to individuals by name and hold

them accountable for their accuracy.

a. $1,000 -

$4,000

b. $500 -

$1,000

a. L

b. L

Infrastructure Risk

Possible

interoperability

Problem

. 40% .$15,000 -

$30,000

Identify needs and test from outset. Design

and create patches for needs not met by SaaS

$6,000 -

$12,000 M

External Risk No

experience with SaaS 15% $10,000 -

$20,000

Software has always been designed to

company specifications. Requirements

probably will not be met by SaaS

$1,500 -

$3,000 L

underperformance 10% $5,000 -

$10,000

Require certification of the software

design firm.

$500 -

$1,000 L

.

Average

Probability

16.87%

. Total Approximate Risk Exposure: $10,900 -

$32,000 .

Alternative Solution #3 (Tentative Solution Rank Order #3): Use Software as

a Service (SaaS) - Use Software as a Service (SaaS) .

Risk Category Proba

bility

Impact

If

Occurs

Mitigation Strategy

Approx.

Risk

Exposure

Risk

Priority

Organizational Risk

a. Scope creep (users

may increase

functionality

requirements)

b. Users may resist use

of new system

c. Possible loss of

executive support

during project due to

new priorities

a. 20%

b.50%

c. 30%

a. $20,000

- $50,000

b. $5,000 -

$20,000

c. $15,000

- $35,000

a. Use of representative IPT; frequent

meetings with users to inform and prevent

misunderstandings

b. Pre-sell new system, provide training;

remove old systems as of a specified date

c. Frequent executive briefings; stress link to

the organization's key performance indicators

a. $4,000 -

$10,000

b.$2,500 -

$10,000

c. $4,500 -

$10,500

a. M

b. M

c. M

Information Security

and Privacy Risk

Potential I/S risk with

online accounting

40% $25,000 -

60,000

Identify needs to provide more security and

firewalls for data security.

$10,000 -

$24,000 H

Complexity Risk

a. Possible

unrecognized

assumptions

b. Accuracy in

forecasting costs and

benefits

a. 20%

b. 10%

a. $5,000 -

$20,000.

b. $5,000 -

$10,000

Require all estimates and assumptions to be

justified; obtain independent verifications of

assumptions and estimates; assign

responsibility for specific assumptions and

estimates to individuals by name and hold

them accountable for their accuracy.

a. $1,000 -

$4,000

b. $500 -

$1,000

a. L

b. L

Infrastructure Risk

Possible

interoperability

Problem

. 40% .$15,000 -

$30,000

Identify needs and test from outset. Design

and create patches for needs not met by SaaS

$6,000 -

$12,000 M

External Risk No

experience with SaaS 15% $10,000 -

$20,000

Software has always been designed to

company specifications. Requirements

probably will not be met by SaaS

$1,500 -

$3,000 L

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

.

Average

Probability

28.12%

. Total Approximate Risk Exposure: $22,500 -

$74,500 .

Activity 6

Complete this template based on what I’ve already prepared (Use alternatives

2 & 3 from Activity 5)

Activity 7

Complete this template based on what I’ve already prepared.

http://iteconcorp.com/T7EconomicAnalysis.html

Activity 9 (this is complete)

Acquisition of new accounting software will reduce labor hours, time, errors and overall costs. Improved

business quality and maintenance of data are huge benefits. This acquisition could result in savings of

$300,000 annually.

Activity 10 (Use template provided below)

Acquisition Strategy Statement

Name of IT Services Acquisition Project: Hire Software Designer to Create New Software

Submitted by: Markeeda Guest-Spencer Date Submitted: 10/29/16

1. Proposal Summary.

[Under this heading, briefly summarize the entire proposal, including costs, benefits, risks, and

schedule. Provide a high-level description of the proposed IT services/products acquisition project,

why it is needed, and how the proposed IT services and system implementation will meet that need.

Average

Probability

28.12%

. Total Approximate Risk Exposure: $22,500 -

$74,500 .

Activity 6

Complete this template based on what I’ve already prepared (Use alternatives

2 & 3 from Activity 5)

Activity 7

Complete this template based on what I’ve already prepared.

http://iteconcorp.com/T7EconomicAnalysis.html

Activity 9 (this is complete)

Acquisition of new accounting software will reduce labor hours, time, errors and overall costs. Improved

business quality and maintenance of data are huge benefits. This acquisition could result in savings of

$300,000 annually.

Activity 10 (Use template provided below)

Acquisition Strategy Statement

Name of IT Services Acquisition Project: Hire Software Designer to Create New Software

Submitted by: Markeeda Guest-Spencer Date Submitted: 10/29/16

1. Proposal Summary.

[Under this heading, briefly summarize the entire proposal, including costs, benefits, risks, and

schedule. Provide a high-level description of the proposed IT services/products acquisition project,

why it is needed, and how the proposed IT services and system implementation will meet that need.

Briefly indicate who and/or what will benefit, when the costs and benefits will occur, and how risk will

be managed.]

2. System Life Cycle (SLC).

[Under this heading, describe or otherwise present the proposed project's system life cycle (SLC). Do

not confuse this with the system development life cycle (SDLC). The SLC, which has roots in systems

engineering, covers the system from initiation to disposal. At minimum, the SLC includes these

phases: planning, acquisition, implementation, operations, and disposal. Depicting the SLC is usually

best accomplished using a graphic with a timeline. It is sometimes (not always) advantageous for the

graphic to go a little deeper into the principal phases and show key activities, reviews, and milestones

that may be of special interest to executive reviewers. An example could be an acquisition project

involving outsourcing and executives might want to know when the outsourcing agreement is

scheduled to be signed.]

3. Basic Acquisition Approach.

[Under this heading, provide a summary statement of your basic acquisition approach and then use the

subheadings below to give details of the activities. In this summary statement, identify the IT services

and products (if included) to be acquired and describe at a high-level the approach that will be used to

identify qualified sources of the desired IT services. If the contractor to be selected is to recommend,

install, develop, or otherwise provide services related to a product, this aspect needs to be addressed in

the acquisition approach. After writing the summary statement, describe the actions that were or are to

be followed in each of the below areas identified by subheadings. Include the subheadings in your

document.]

Market Research. [Briefly described the market research planned and any results to date.]

Use of Competition. [Describe how competition will be built into the acquisition process to help

obtain the best price and/or best value and not exclude potentially qualified IT services contractors.]

Potential Sources. [Identify the potential contractors qualified to provide the services required.]

Contract Type. [Identify the type of contract planned to be awarded and give the reason for its

selection.

Contract Incentives and Penalties. [Describe any incentives and penalties that you plan to build into

the contract with the IT services contractor.]

Risk Assessment. [Identify important risks, including risks associated with the contract type selected,

and how those risks will be managed.]

be managed.]

2. System Life Cycle (SLC).

[Under this heading, describe or otherwise present the proposed project's system life cycle (SLC). Do

not confuse this with the system development life cycle (SDLC). The SLC, which has roots in systems

engineering, covers the system from initiation to disposal. At minimum, the SLC includes these

phases: planning, acquisition, implementation, operations, and disposal. Depicting the SLC is usually

best accomplished using a graphic with a timeline. It is sometimes (not always) advantageous for the

graphic to go a little deeper into the principal phases and show key activities, reviews, and milestones

that may be of special interest to executive reviewers. An example could be an acquisition project

involving outsourcing and executives might want to know when the outsourcing agreement is

scheduled to be signed.]

3. Basic Acquisition Approach.

[Under this heading, provide a summary statement of your basic acquisition approach and then use the

subheadings below to give details of the activities. In this summary statement, identify the IT services

and products (if included) to be acquired and describe at a high-level the approach that will be used to

identify qualified sources of the desired IT services. If the contractor to be selected is to recommend,

install, develop, or otherwise provide services related to a product, this aspect needs to be addressed in

the acquisition approach. After writing the summary statement, describe the actions that were or are to

be followed in each of the below areas identified by subheadings. Include the subheadings in your

document.]

Market Research. [Briefly described the market research planned and any results to date.]

Use of Competition. [Describe how competition will be built into the acquisition process to help

obtain the best price and/or best value and not exclude potentially qualified IT services contractors.]

Potential Sources. [Identify the potential contractors qualified to provide the services required.]

Contract Type. [Identify the type of contract planned to be awarded and give the reason for its

selection.

Contract Incentives and Penalties. [Describe any incentives and penalties that you plan to build into

the contract with the IT services contractor.]

Risk Assessment. [Identify important risks, including risks associated with the contract type selected,

and how those risks will be managed.]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.