Unit 4: Financial Performance, HR and Legislation for Bourne Leisure

VerifiedAdded on 2022/12/28

|22

|4506

|64

Report

AI Summary

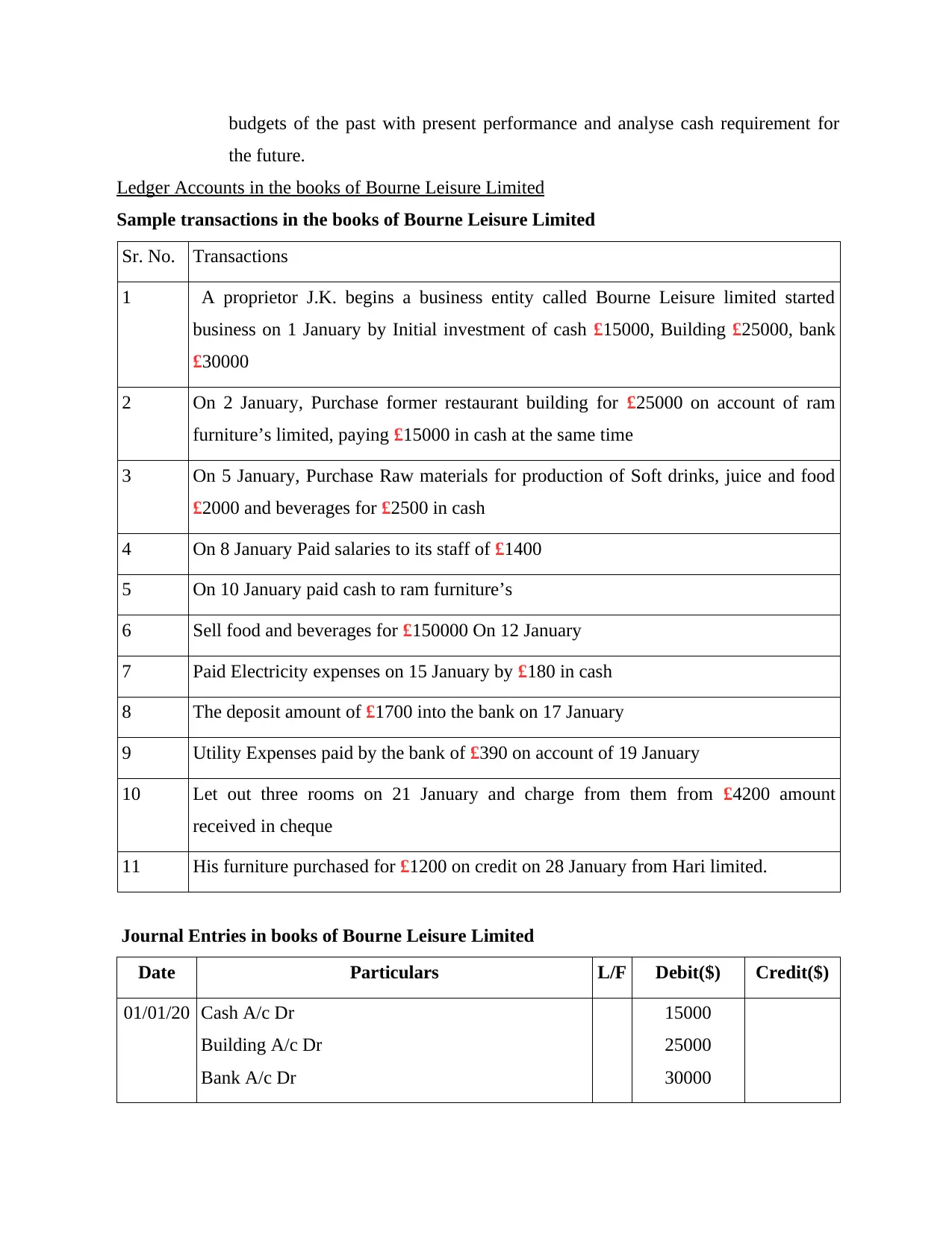

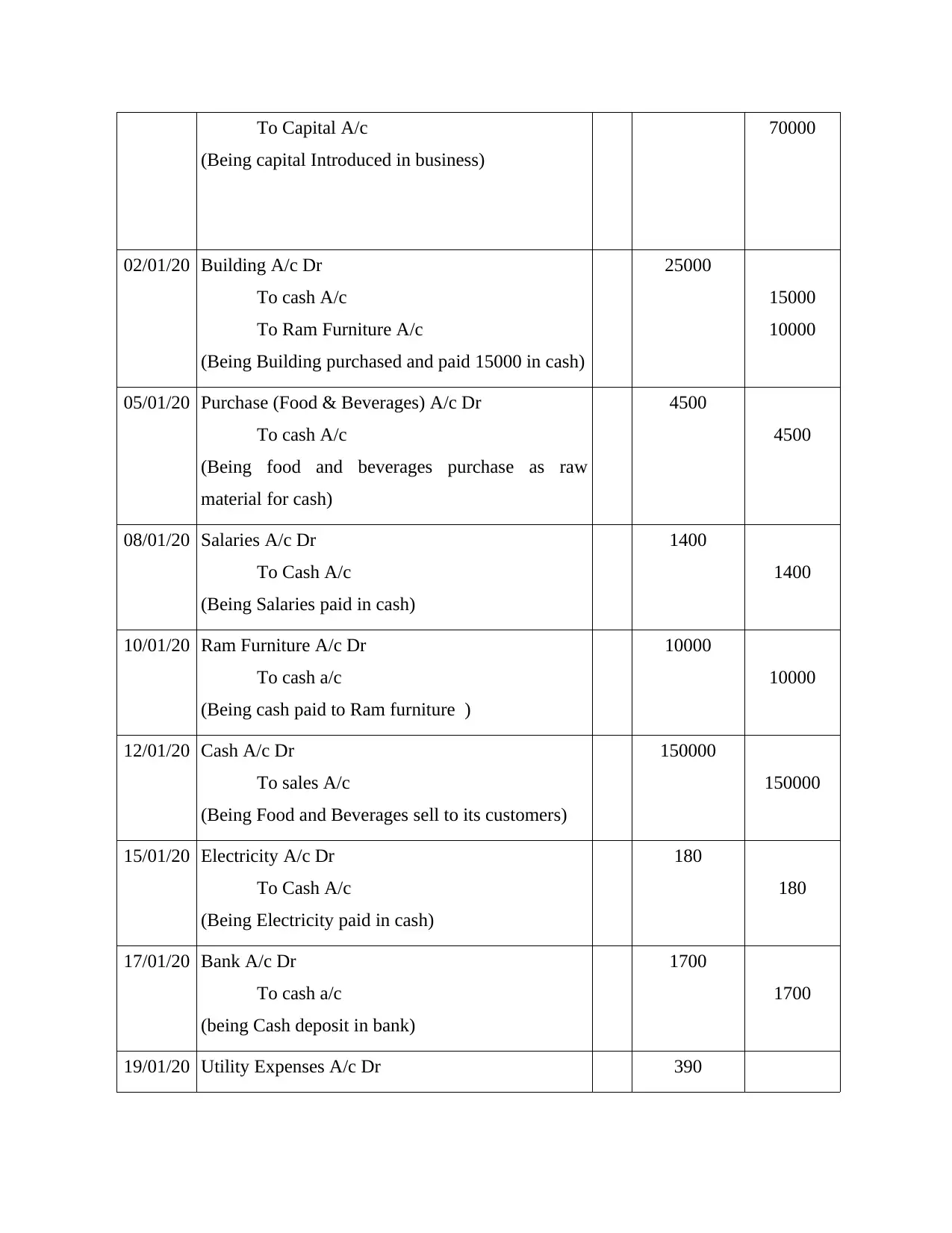

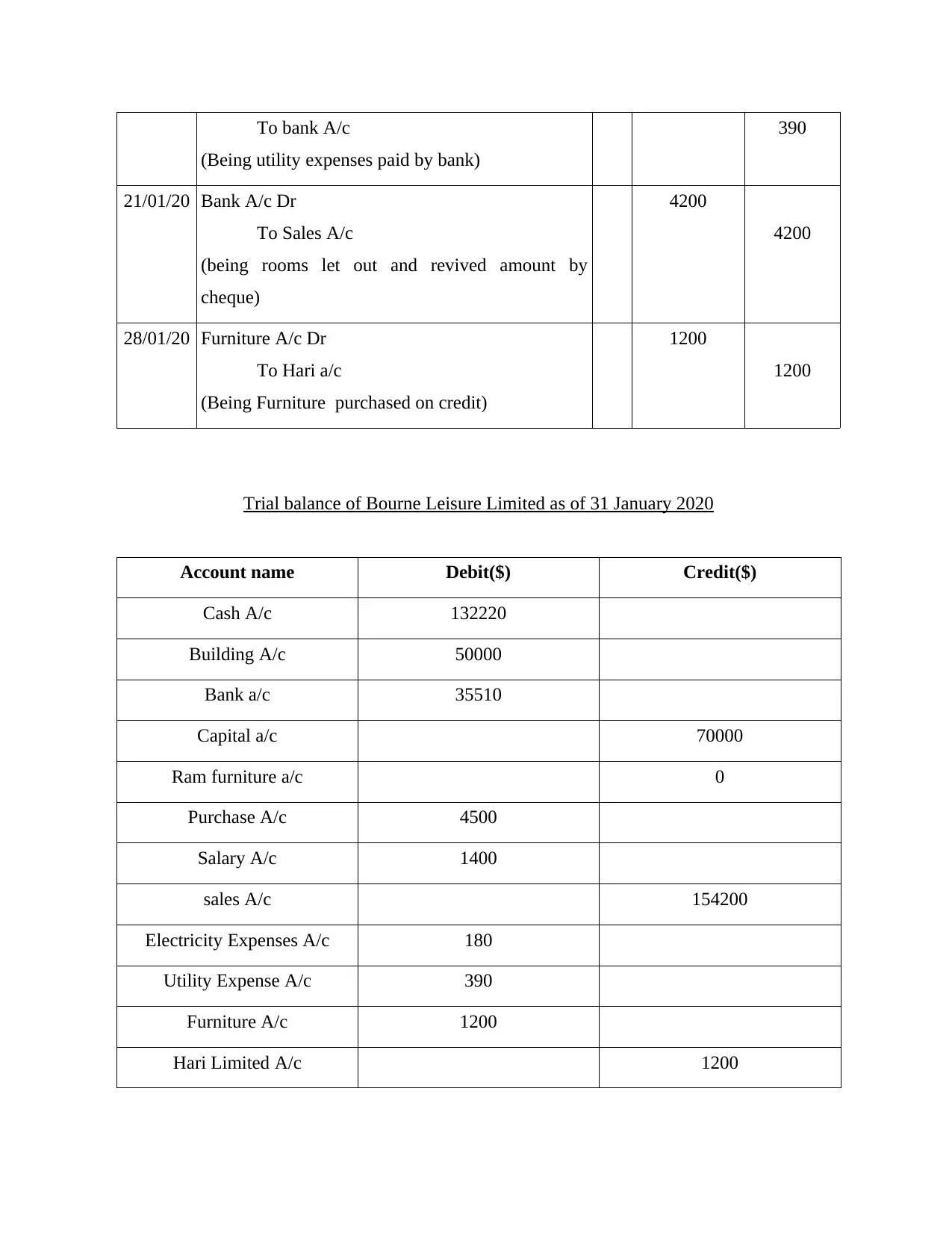

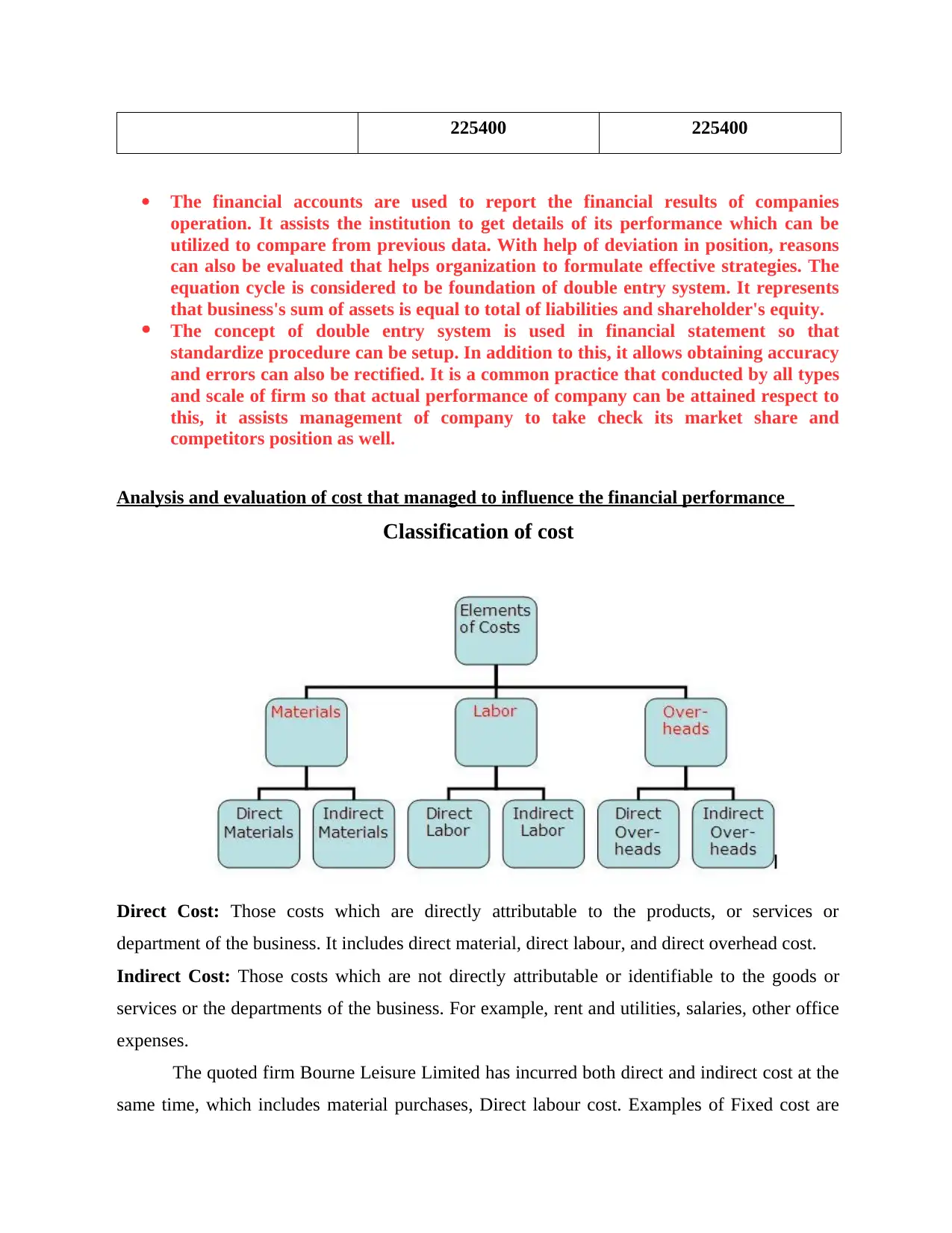

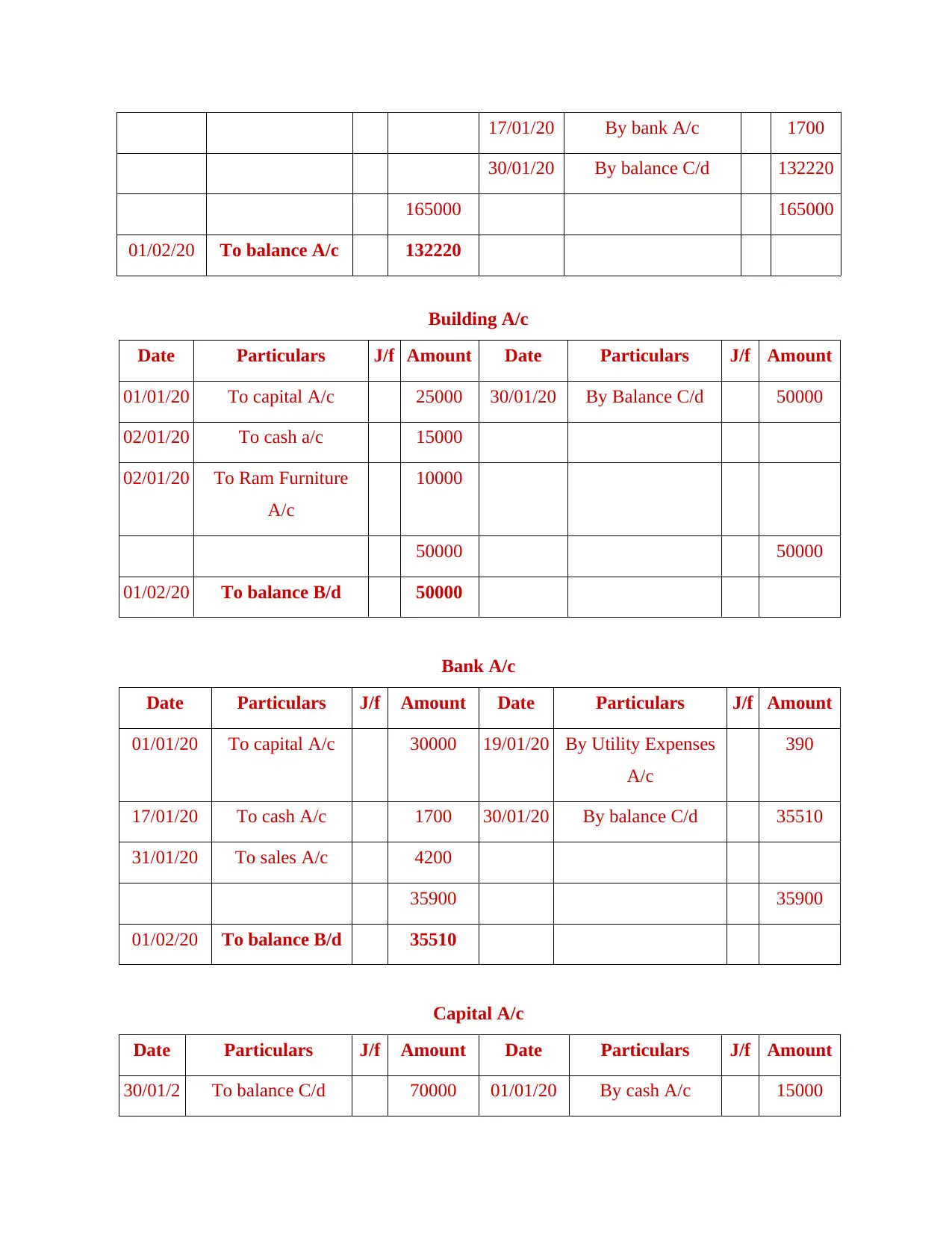

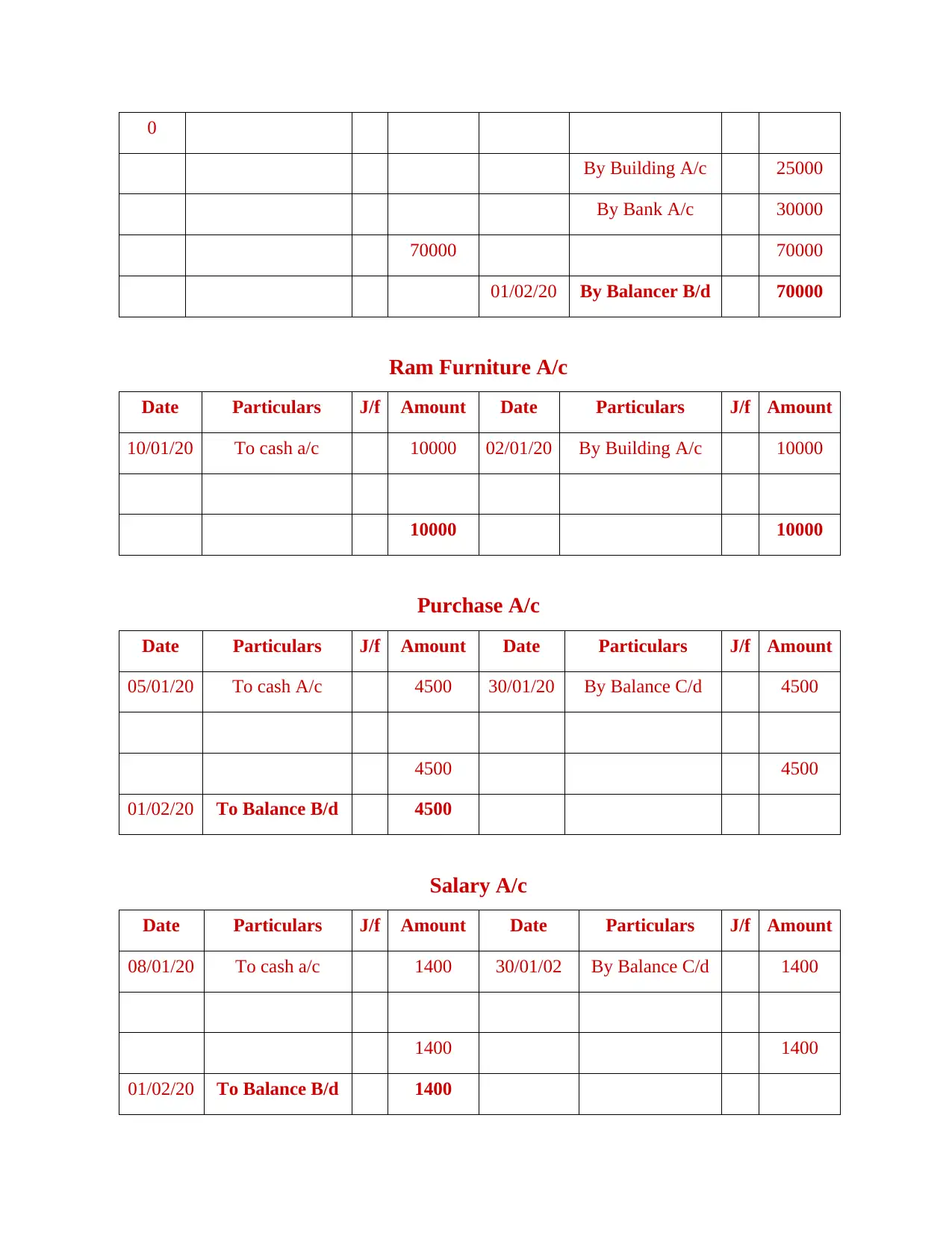

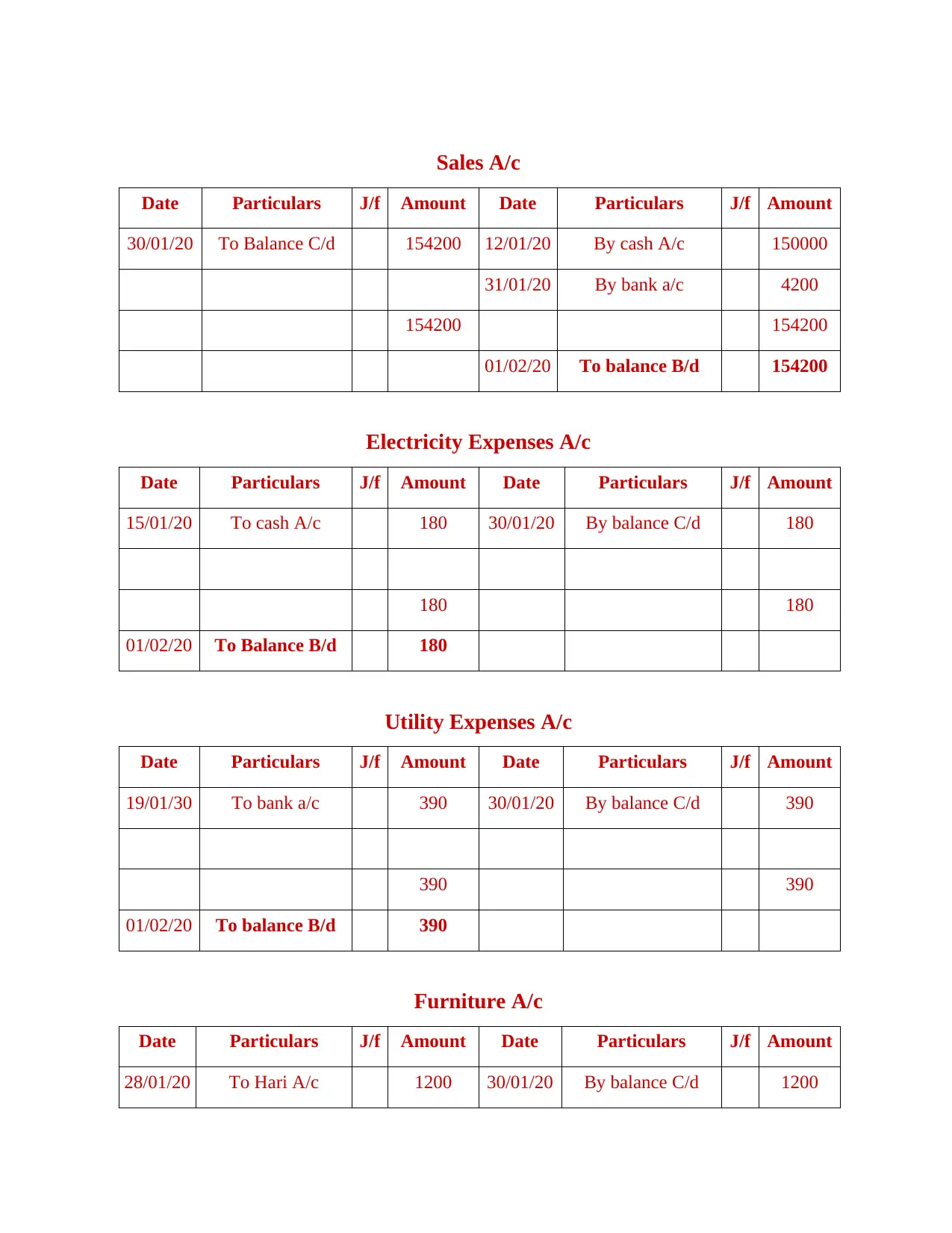

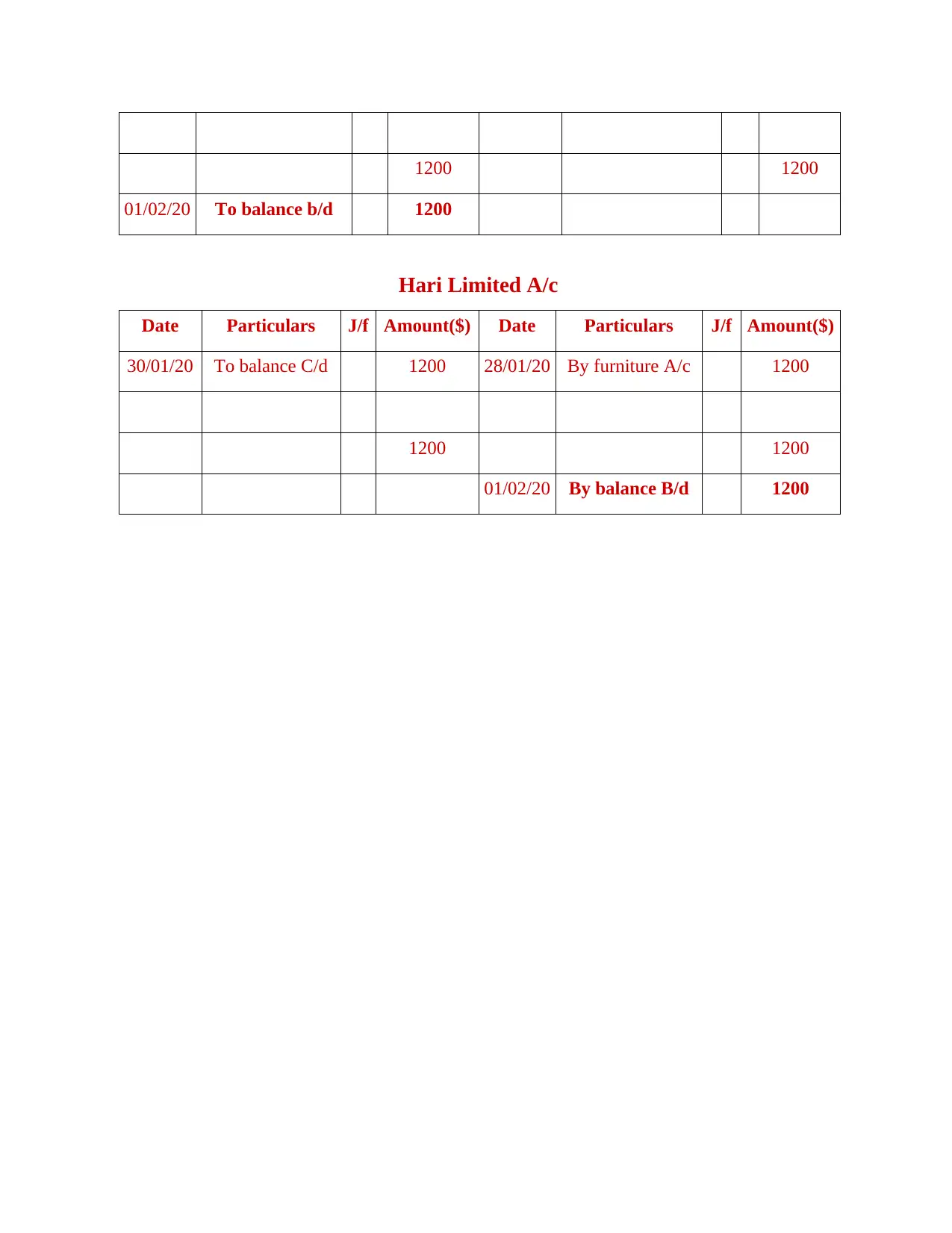

This report provides a detailed analysis of Bourne Leisure Limited's financial performance, focusing on financial statements, ledger accounts, and trial balances. Part A investigates the principles of managing financial performance, including the preparation of financial statements, inventory records, and cash flow statements. Part B reviews the HR lifecycle stages, specifically focusing on the accounting job role, and outlines the importance of recruitment, onboarding, development, retention, and offboarding. The report also examines relevant legislation that hospitality organizations must adhere to, including potential implications of employee welfare and the interrelation of different roles within the hospitality sector. The report concludes with a summary of the key findings and their implications for Bourne Leisure Limited's overall success and financial health, including analysis of cost classification (direct and indirect costs), accurate transaction recording, and the role of financial management in achieving growth.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.