University Canada West: Regression Analysis of BP Share Data

VerifiedAdded on 2022/12/30

|10

|1390

|82

Report

AI Summary

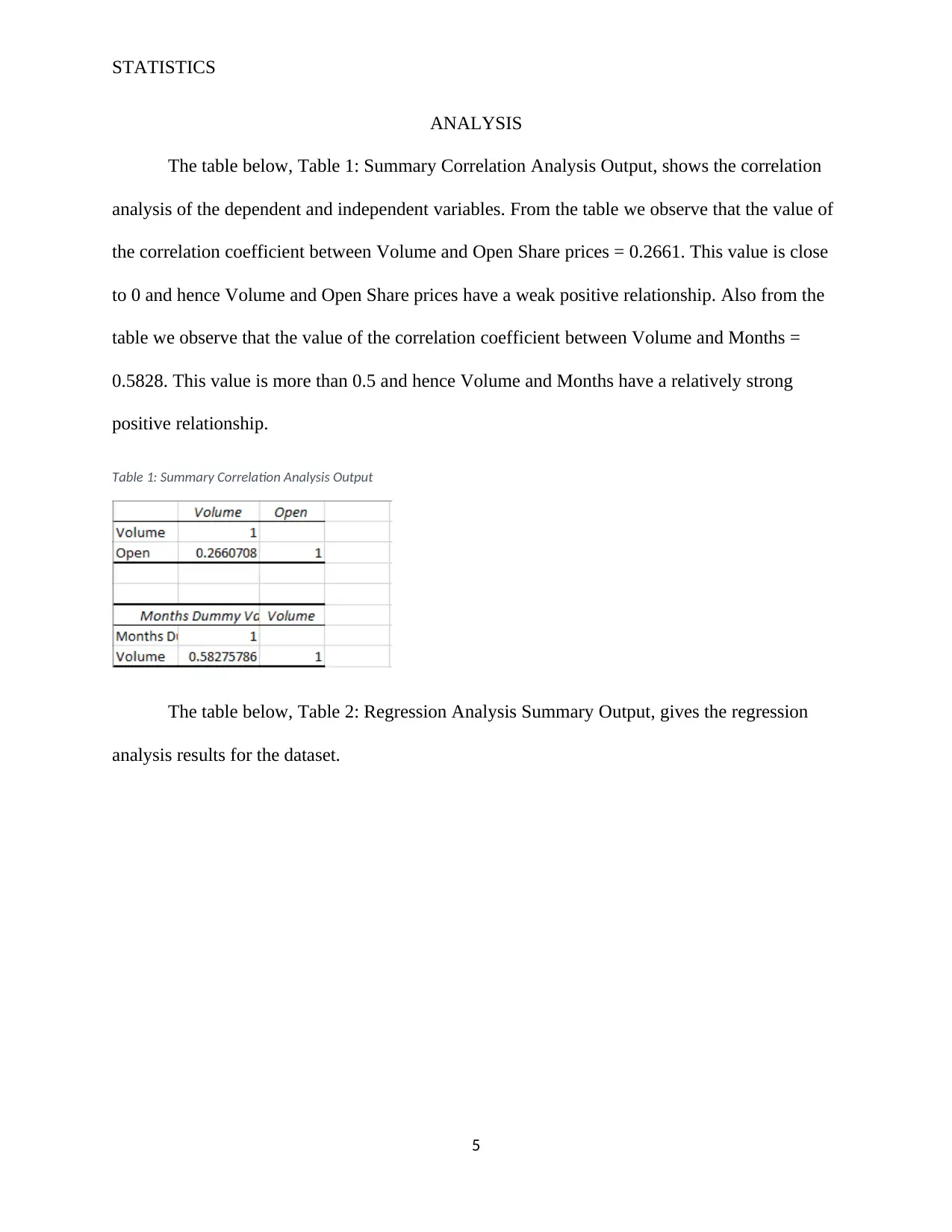

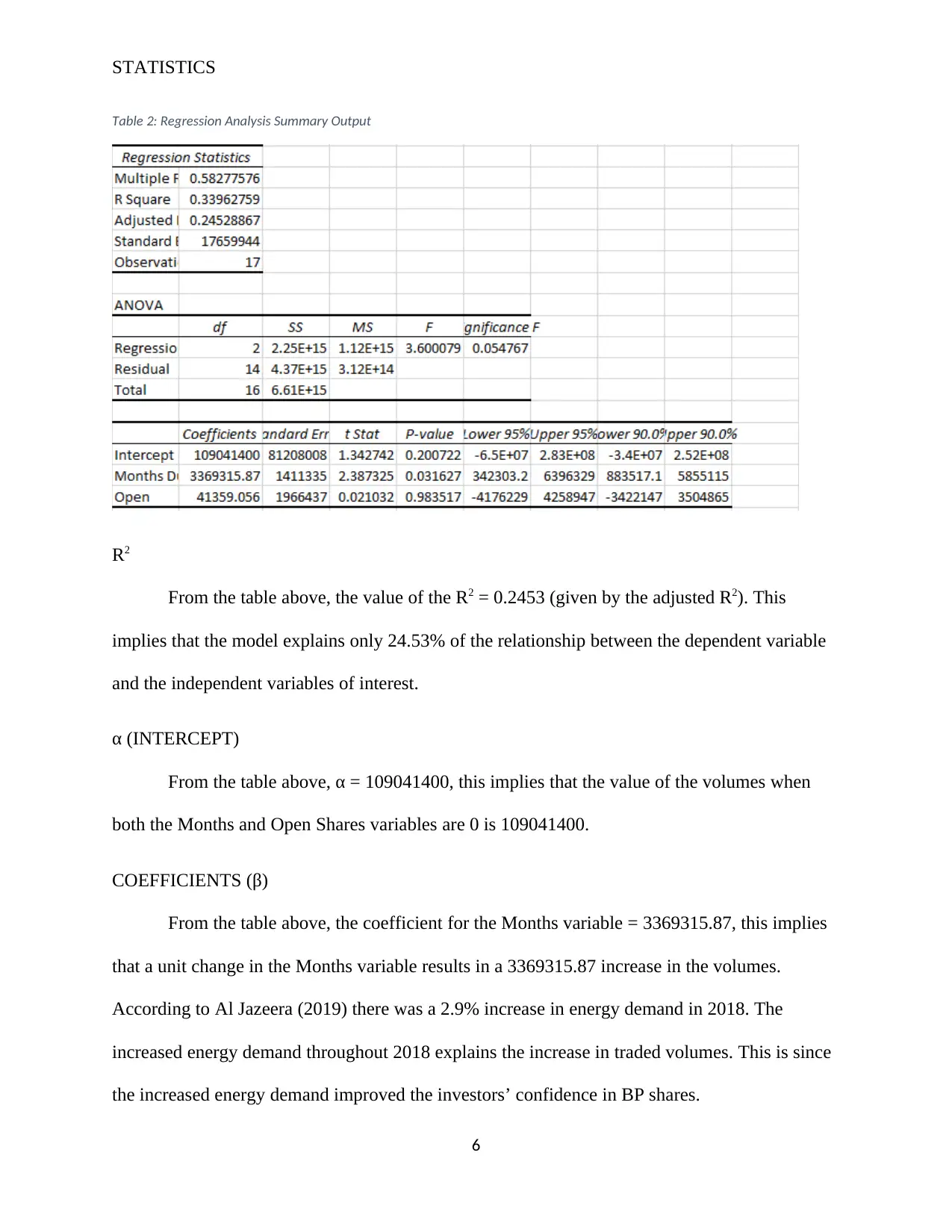

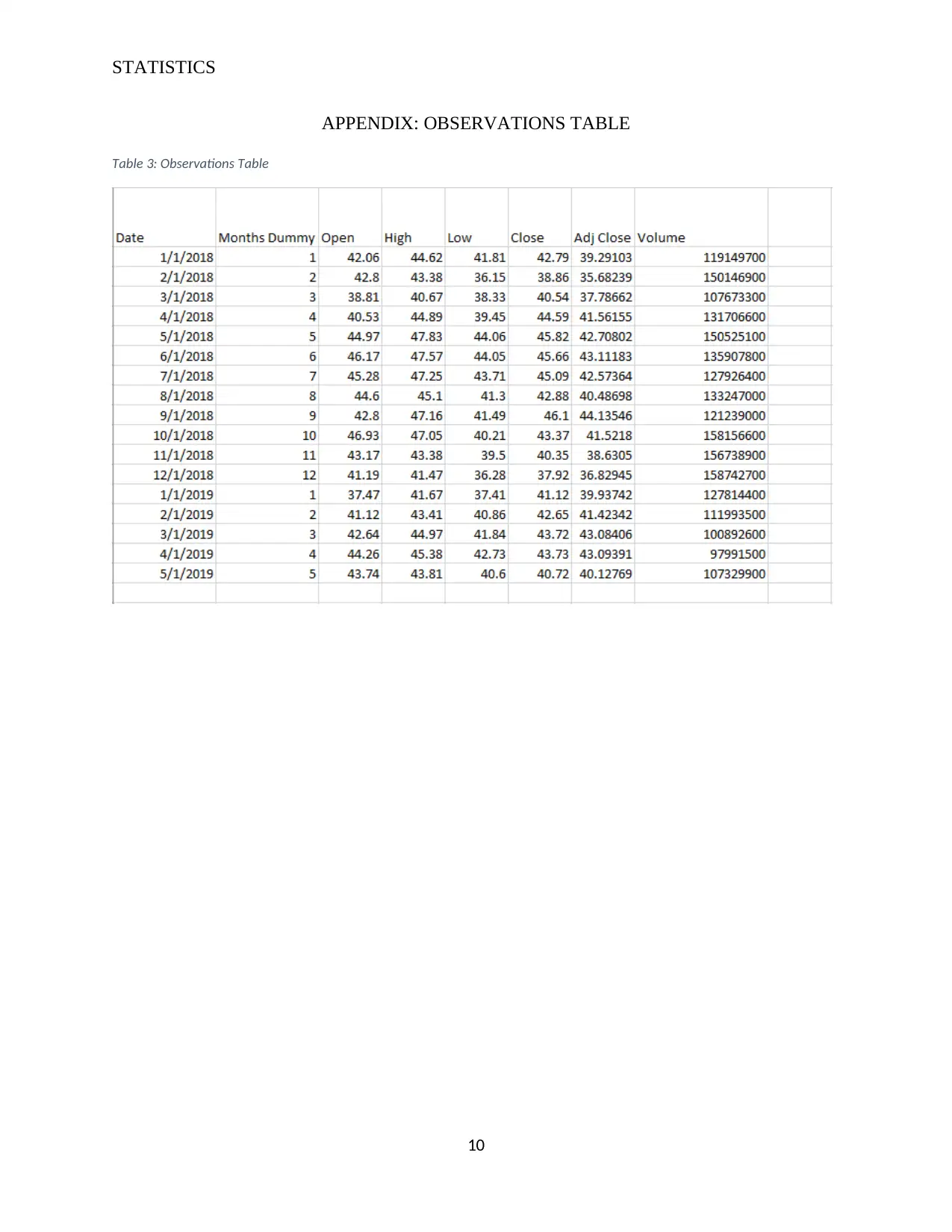

This report presents a regression analysis of British Petroleum (BP) shares, focusing on the relationship between trading volumes (dependent variable) and time period (in months) and opening share prices (independent variables). Data from Yahoo Finance was used, spanning from January 2018 to May 2019. The analysis includes correlation analysis, R-squared, intercept (α), coefficients (β), and t-statistics. The R-squared value indicates that the model explains only 24.53% of the relationship. The analysis concludes that the months of the year are a significant determinant of the traded volumes, while the opening share prices are not significant. The report also discusses the limitations of the model and suggests areas for future research, such as incorporating external factors that affect share prices to improve model accuracy. The paper follows APA style guidelines, as required by the MBAF 502 course at University Canada West.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.