Business Planning (BPL): Financial Statement & Ratio Analysis

VerifiedAdded on 2023/06/17

|14

|3089

|212

Report

AI Summary

This report provides a comprehensive financial analysis of a business, comparing budgeted and actual performance. It includes statements of profit and loss and financial position, both budgeted and actual. Graphical analysis is used to compare budgeted and actual costs, sales, gross profit, and operating profit. The report also calculates and interprets profitability and liquidity ratios for both budgeted and actual years, providing insights into the company's financial health and performance. The analysis reveals variances between budgeted and actual figures, highlighting areas where the company exceeded or fell short of expectations, and assesses the implications for the business.

Business Planning

(BPL)

(BPL)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Summary.................................................................................................................................................3

Statement of Profit & Loss A/c (Budgeted).............................................................................................4

Statement of Profit & Loss A/c (Actual)...................................................................................................4

Statement of Financial Position (Budgeted)............................................................................................5

Statement of Financial Position (ACTUAL)...............................................................................................6

A pie chart show the different relative size of budgeted reimbursement for the year. Provide a concise

comment on interpretation what the information from the graphical record means............................6

A pie chart showing actual costs for the year Compare 2 pie charts.......................................................7

The next graphs comparing the monetary fund against with the actual public presentation. Provide a

brief comment on interpretation what the data graphs and implication for the business.....................8

A graph comparison for the 12 months of fund against actual sales...................................................8

• Graph comparing Tweleve months of fund against actual gross profit.............................................9

• Graph for 12 months of monetary fund against actual operational profit......................................10

Calculation of accounting ratios including two profitability ratios and two liquidity ratios of budgeted

and actual years....................................................................................................................................11

References.................................................................................................................................................14

Books & Journals...................................................................................................................................14

Summary.................................................................................................................................................3

Statement of Profit & Loss A/c (Budgeted).............................................................................................4

Statement of Profit & Loss A/c (Actual)...................................................................................................4

Statement of Financial Position (Budgeted)............................................................................................5

Statement of Financial Position (ACTUAL)...............................................................................................6

A pie chart show the different relative size of budgeted reimbursement for the year. Provide a concise

comment on interpretation what the information from the graphical record means............................6

A pie chart showing actual costs for the year Compare 2 pie charts.......................................................7

The next graphs comparing the monetary fund against with the actual public presentation. Provide a

brief comment on interpretation what the data graphs and implication for the business.....................8

A graph comparison for the 12 months of fund against actual sales...................................................8

• Graph comparing Tweleve months of fund against actual gross profit.............................................9

• Graph for 12 months of monetary fund against actual operational profit......................................10

Calculation of accounting ratios including two profitability ratios and two liquidity ratios of budgeted

and actual years....................................................................................................................................11

References.................................................................................................................................................14

Books & Journals...................................................................................................................................14

Summary

Business planning is considered as an important component that helps in setting up the business

in a effective manner. The process of business planning in accordance to the financial capacity helps in

determining that how a business will work to achieve the goals and objectives strategically. The planning

which is done financially involves all types of costs that are included for bearing the expenses like

business activities, resources, equipment and materials. All these costs are essential for the business. Also,

it is essential to prepare a projected and actual amount of costs and sales that are required to run the

business smoothly. Therefore, the report will be including the preparation of the evidence of profit and

loss account along with the argument of financial point of in both manners actual as well as budgeted. In

addition to this, the report will be including the graphical analysis of all the types of costs that are

incurred to function the business organization on actual and budgeted basis. The comparative analysis of

budgeted and actual sales, gross profit and operating profit. At last, with the help of the argument of

commercial enterprise place, the profitability and liquidity ratios are calculated on actual and budgeted

basis to ascertain the relevant interpretation based on the value of ratios obtained. This helped in check on

the financial health of the company.

Business planning is considered as an important component that helps in setting up the business

in a effective manner. The process of business planning in accordance to the financial capacity helps in

determining that how a business will work to achieve the goals and objectives strategically. The planning

which is done financially involves all types of costs that are included for bearing the expenses like

business activities, resources, equipment and materials. All these costs are essential for the business. Also,

it is essential to prepare a projected and actual amount of costs and sales that are required to run the

business smoothly. Therefore, the report will be including the preparation of the evidence of profit and

loss account along with the argument of financial point of in both manners actual as well as budgeted. In

addition to this, the report will be including the graphical analysis of all the types of costs that are

incurred to function the business organization on actual and budgeted basis. The comparative analysis of

budgeted and actual sales, gross profit and operating profit. At last, with the help of the argument of

commercial enterprise place, the profitability and liquidity ratios are calculated on actual and budgeted

basis to ascertain the relevant interpretation based on the value of ratios obtained. This helped in check on

the financial health of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

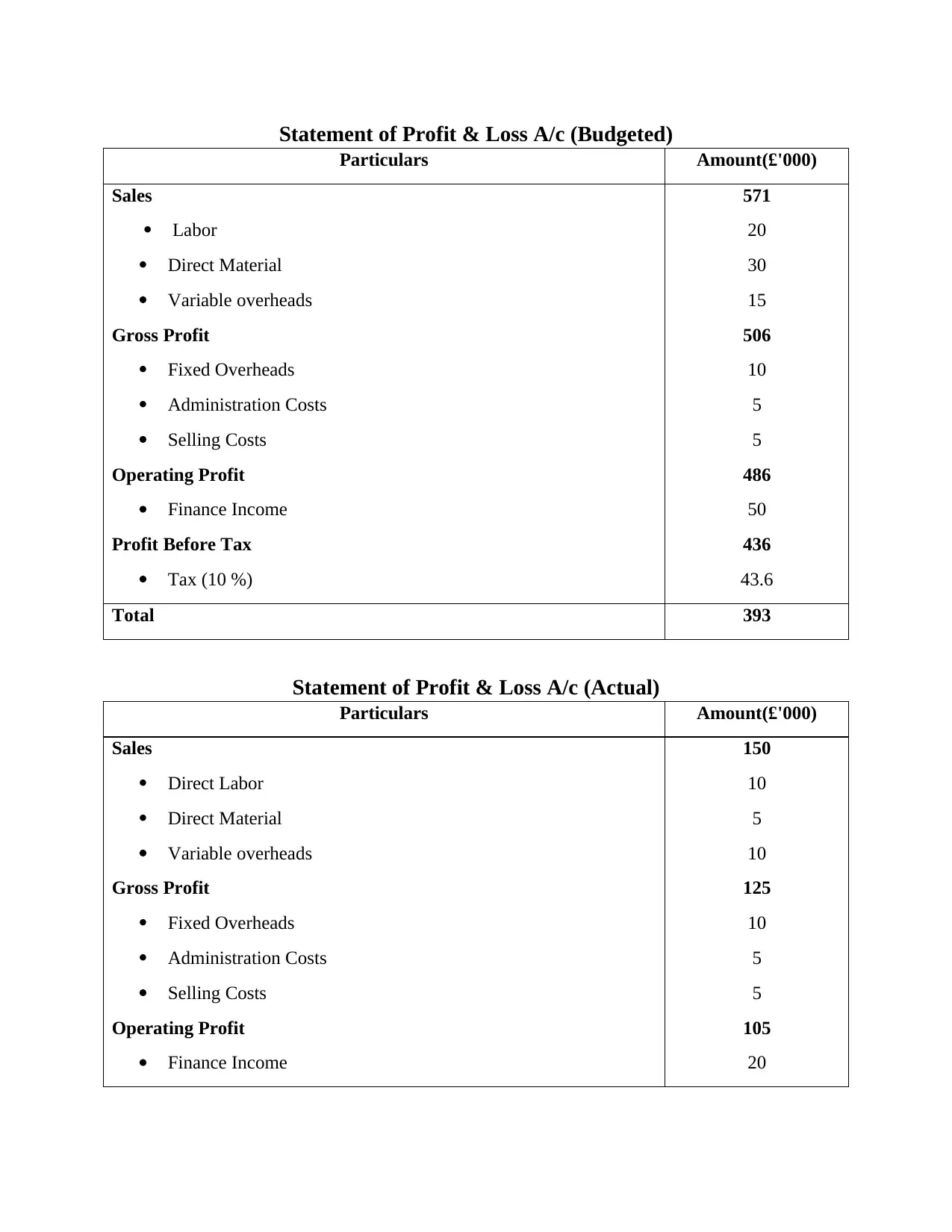

Statement of Profit & Loss A/c (Budgeted)

Particulars Amount(£'000)

Sales

Labor

Direct Material

Variable overheads

Gross Profit

Fixed Overheads

Administration Costs

Selling Costs

Operating Profit

Finance Income

Profit Before Tax

Tax (10 %)

571

20

30

15

506

10

5

5

486

50

436

43.6

Total 393

Statement of Profit & Loss A/c (Actual)

Particulars Amount(£'000)

Sales

Direct Labor

Direct Material

Variable overheads

Gross Profit

Fixed Overheads

Administration Costs

Selling Costs

Operating Profit

Finance Income

150

10

5

10

125

10

5

5

105

20

Particulars Amount(£'000)

Sales

Labor

Direct Material

Variable overheads

Gross Profit

Fixed Overheads

Administration Costs

Selling Costs

Operating Profit

Finance Income

Profit Before Tax

Tax (10 %)

571

20

30

15

506

10

5

5

486

50

436

43.6

Total 393

Statement of Profit & Loss A/c (Actual)

Particulars Amount(£'000)

Sales

Direct Labor

Direct Material

Variable overheads

Gross Profit

Fixed Overheads

Administration Costs

Selling Costs

Operating Profit

Finance Income

150

10

5

10

125

10

5

5

105

20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

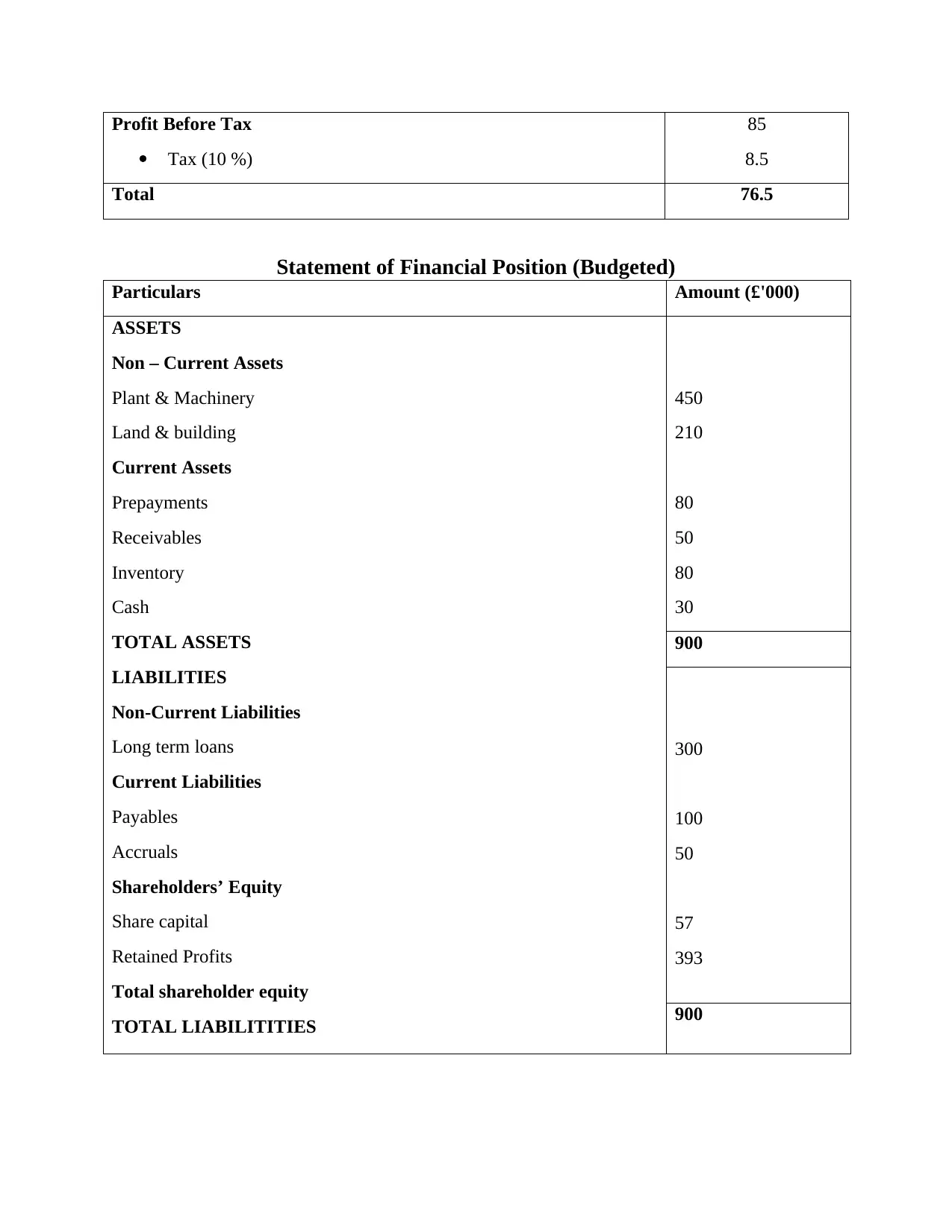

Profit Before Tax

Tax (10 %)

85

8.5

Total 76.5

Statement of Financial Position (Budgeted)

Particulars Amount (£'000)

ASSETS

Non – Current Assets

Plant & Machinery

Land & building

Current Assets

Prepayments

Receivables

Inventory

Cash

TOTAL ASSETS

LIABILITIES

Non-Current Liabilities

Long term loans

Current Liabilities

Payables

Accruals

Shareholders’ Equity

Share capital

Retained Profits

Total shareholder equity

TOTAL LIABILITITIES

450

210

80

50

80

30

900

300

100

50

57

393

900

Tax (10 %)

85

8.5

Total 76.5

Statement of Financial Position (Budgeted)

Particulars Amount (£'000)

ASSETS

Non – Current Assets

Plant & Machinery

Land & building

Current Assets

Prepayments

Receivables

Inventory

Cash

TOTAL ASSETS

LIABILITIES

Non-Current Liabilities

Long term loans

Current Liabilities

Payables

Accruals

Shareholders’ Equity

Share capital

Retained Profits

Total shareholder equity

TOTAL LIABILITITIES

450

210

80

50

80

30

900

300

100

50

57

393

900

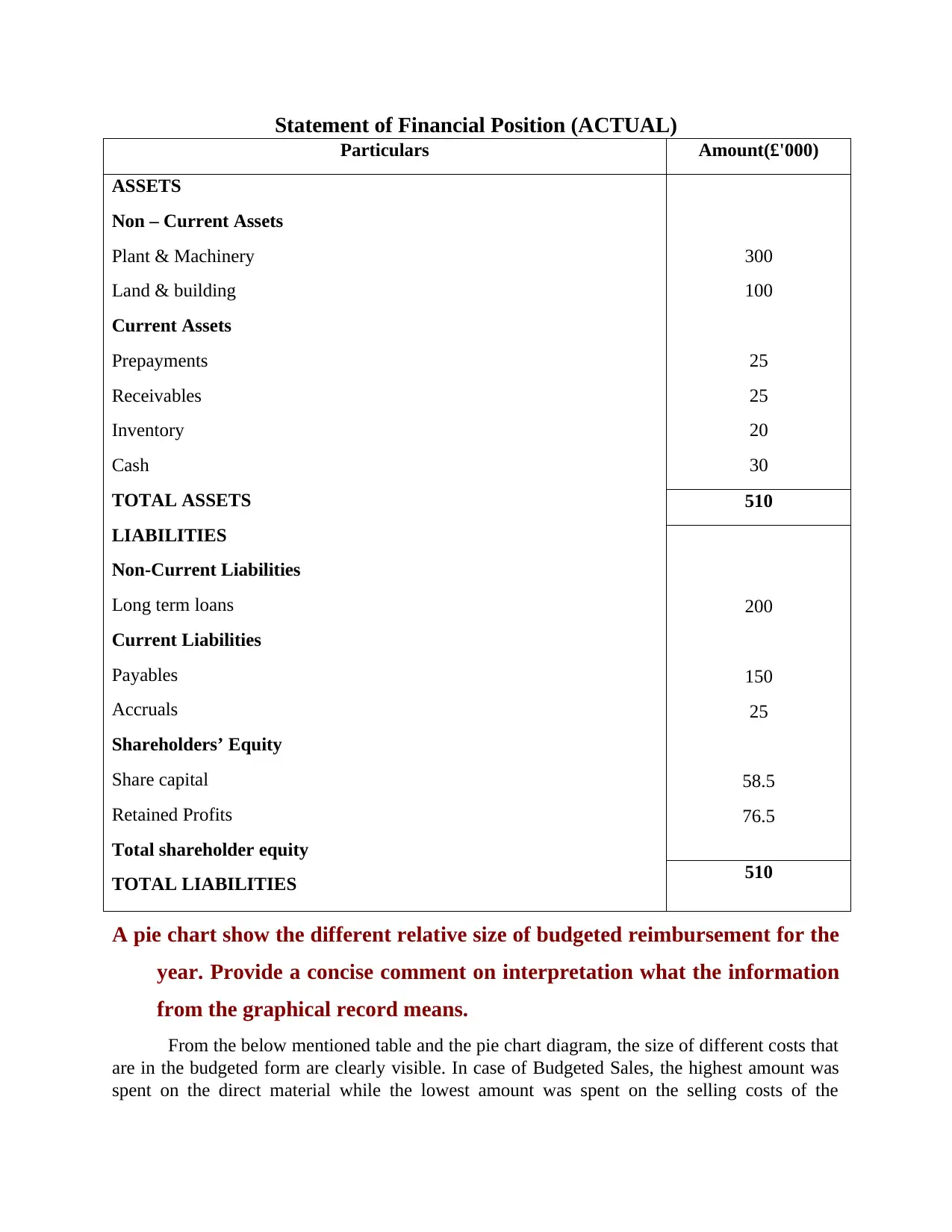

Statement of Financial Position (ACTUAL)

Particulars Amount(£'000)

ASSETS

Non – Current Assets

Plant & Machinery

Land & building

Current Assets

Prepayments

Receivables

Inventory

Cash

TOTAL ASSETS

LIABILITIES

Non-Current Liabilities

Long term loans

Current Liabilities

Payables

Accruals

Shareholders’ Equity

Share capital

Retained Profits

Total shareholder equity

TOTAL LIABILITIES

300

100

25

25

20

30

510

200

150

25

58.5

76.5

510

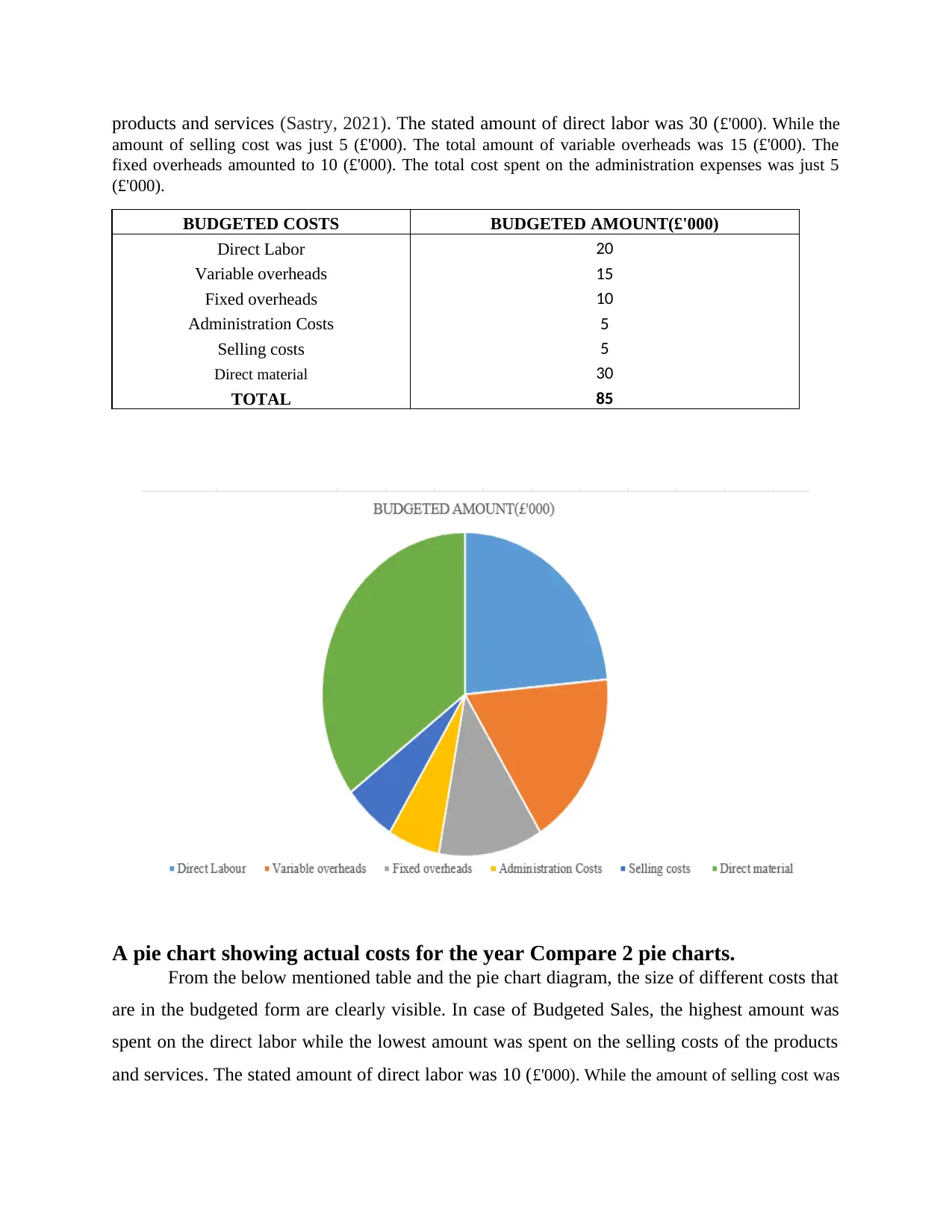

A pie chart show the different relative size of budgeted reimbursement for the

year. Provide a concise comment on interpretation what the information

from the graphical record means.

From the below mentioned table and the pie chart diagram, the size of different costs that

are in the budgeted form are clearly visible. In case of Budgeted Sales, the highest amount was

spent on the direct material while the lowest amount was spent on the selling costs of the

Particulars Amount(£'000)

ASSETS

Non – Current Assets

Plant & Machinery

Land & building

Current Assets

Prepayments

Receivables

Inventory

Cash

TOTAL ASSETS

LIABILITIES

Non-Current Liabilities

Long term loans

Current Liabilities

Payables

Accruals

Shareholders’ Equity

Share capital

Retained Profits

Total shareholder equity

TOTAL LIABILITIES

300

100

25

25

20

30

510

200

150

25

58.5

76.5

510

A pie chart show the different relative size of budgeted reimbursement for the

year. Provide a concise comment on interpretation what the information

from the graphical record means.

From the below mentioned table and the pie chart diagram, the size of different costs that

are in the budgeted form are clearly visible. In case of Budgeted Sales, the highest amount was

spent on the direct material while the lowest amount was spent on the selling costs of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

products and services (Sastry, 2021). The stated amount of direct labor was 30 (£'000). While the

amount of selling cost was just 5 (£'000). The total amount of variable overheads was 15 (£'000). The

fixed overheads amounted to 10 (£'000). The total cost spent on the administration expenses was just 5

(£'000).

BUDGETED COSTS BUDGETED AMOUNT(£'000)

Direct Labor 20

Variable overheads 15

Fixed overheads 10

Administration Costs 5

Selling costs 5

Direct material 30

TOTAL 85

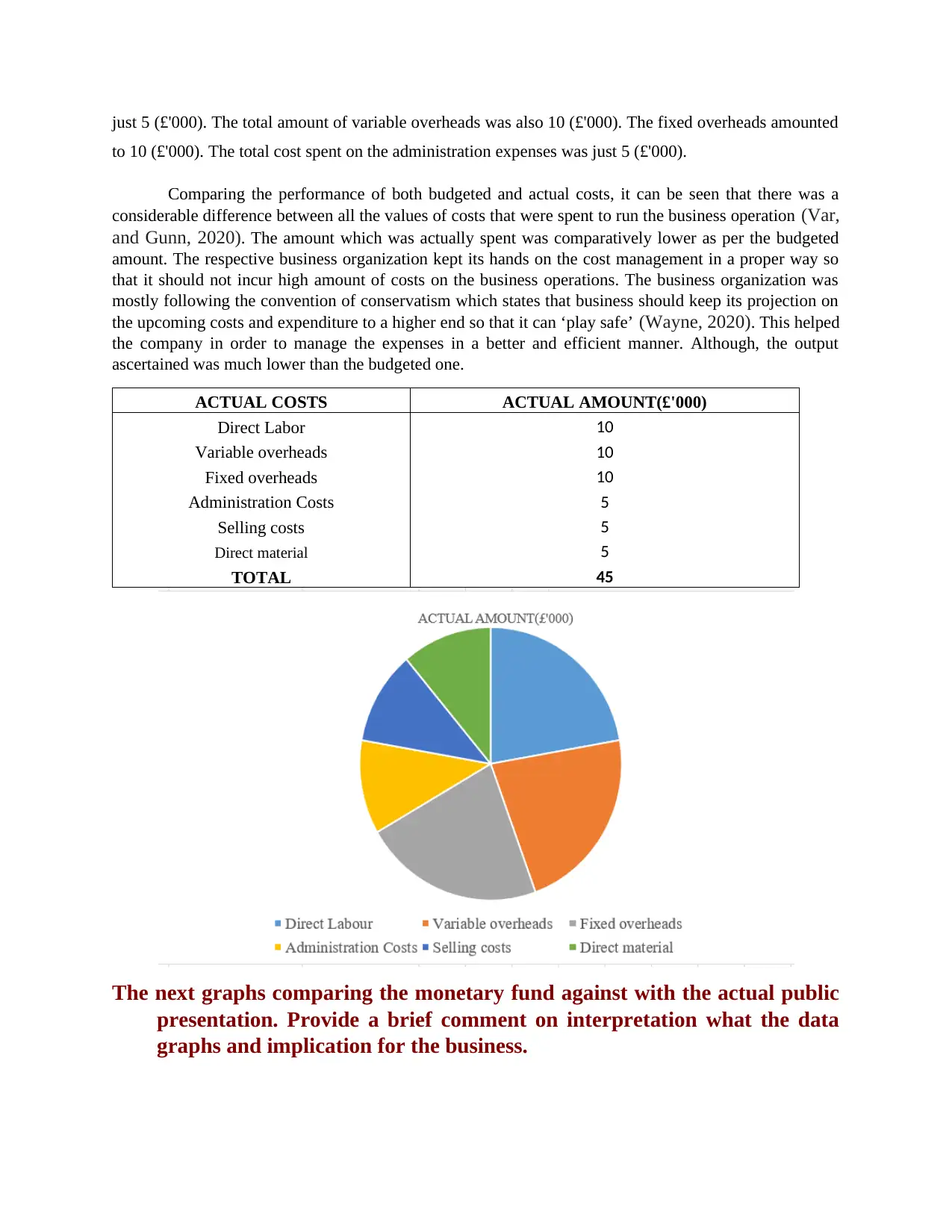

A pie chart showing actual costs for the year Compare 2 pie charts.

From the below mentioned table and the pie chart diagram, the size of different costs that

are in the budgeted form are clearly visible. In case of Budgeted Sales, the highest amount was

spent on the direct labor while the lowest amount was spent on the selling costs of the products

and services. The stated amount of direct labor was 10 (£'000). While the amount of selling cost was

amount of selling cost was just 5 (£'000). The total amount of variable overheads was 15 (£'000). The

fixed overheads amounted to 10 (£'000). The total cost spent on the administration expenses was just 5

(£'000).

BUDGETED COSTS BUDGETED AMOUNT(£'000)

Direct Labor 20

Variable overheads 15

Fixed overheads 10

Administration Costs 5

Selling costs 5

Direct material 30

TOTAL 85

A pie chart showing actual costs for the year Compare 2 pie charts.

From the below mentioned table and the pie chart diagram, the size of different costs that

are in the budgeted form are clearly visible. In case of Budgeted Sales, the highest amount was

spent on the direct labor while the lowest amount was spent on the selling costs of the products

and services. The stated amount of direct labor was 10 (£'000). While the amount of selling cost was

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

just 5 (£'000). The total amount of variable overheads was also 10 (£'000). The fixed overheads amounted

to 10 (£'000). The total cost spent on the administration expenses was just 5 (£'000).

Comparing the performance of both budgeted and actual costs, it can be seen that there was a

considerable difference between all the values of costs that were spent to run the business operation (Var,

and Gunn, 2020). The amount which was actually spent was comparatively lower as per the budgeted

amount. The respective business organization kept its hands on the cost management in a proper way so

that it should not incur high amount of costs on the business operations. The business organization was

mostly following the convention of conservatism which states that business should keep its projection on

the upcoming costs and expenditure to a higher end so that it can ‘play safe’ (Wayne, 2020). This helped

the company in order to manage the expenses in a better and efficient manner. Although, the output

ascertained was much lower than the budgeted one.

The next graphs comparing the monetary fund against with the actual public

presentation. Provide a brief comment on interpretation what the data

graphs and implication for the business.

ACTUAL COSTS ACTUAL AMOUNT(£'000)

Direct Labor 10

Variable overheads 10

Fixed overheads 10

Administration Costs 5

Selling costs 5

Direct material 5

TOTAL 45

to 10 (£'000). The total cost spent on the administration expenses was just 5 (£'000).

Comparing the performance of both budgeted and actual costs, it can be seen that there was a

considerable difference between all the values of costs that were spent to run the business operation (Var,

and Gunn, 2020). The amount which was actually spent was comparatively lower as per the budgeted

amount. The respective business organization kept its hands on the cost management in a proper way so

that it should not incur high amount of costs on the business operations. The business organization was

mostly following the convention of conservatism which states that business should keep its projection on

the upcoming costs and expenditure to a higher end so that it can ‘play safe’ (Wayne, 2020). This helped

the company in order to manage the expenses in a better and efficient manner. Although, the output

ascertained was much lower than the budgeted one.

The next graphs comparing the monetary fund against with the actual public

presentation. Provide a brief comment on interpretation what the data

graphs and implication for the business.

ACTUAL COSTS ACTUAL AMOUNT(£'000)

Direct Labor 10

Variable overheads 10

Fixed overheads 10

Administration Costs 5

Selling costs 5

Direct material 5

TOTAL 45

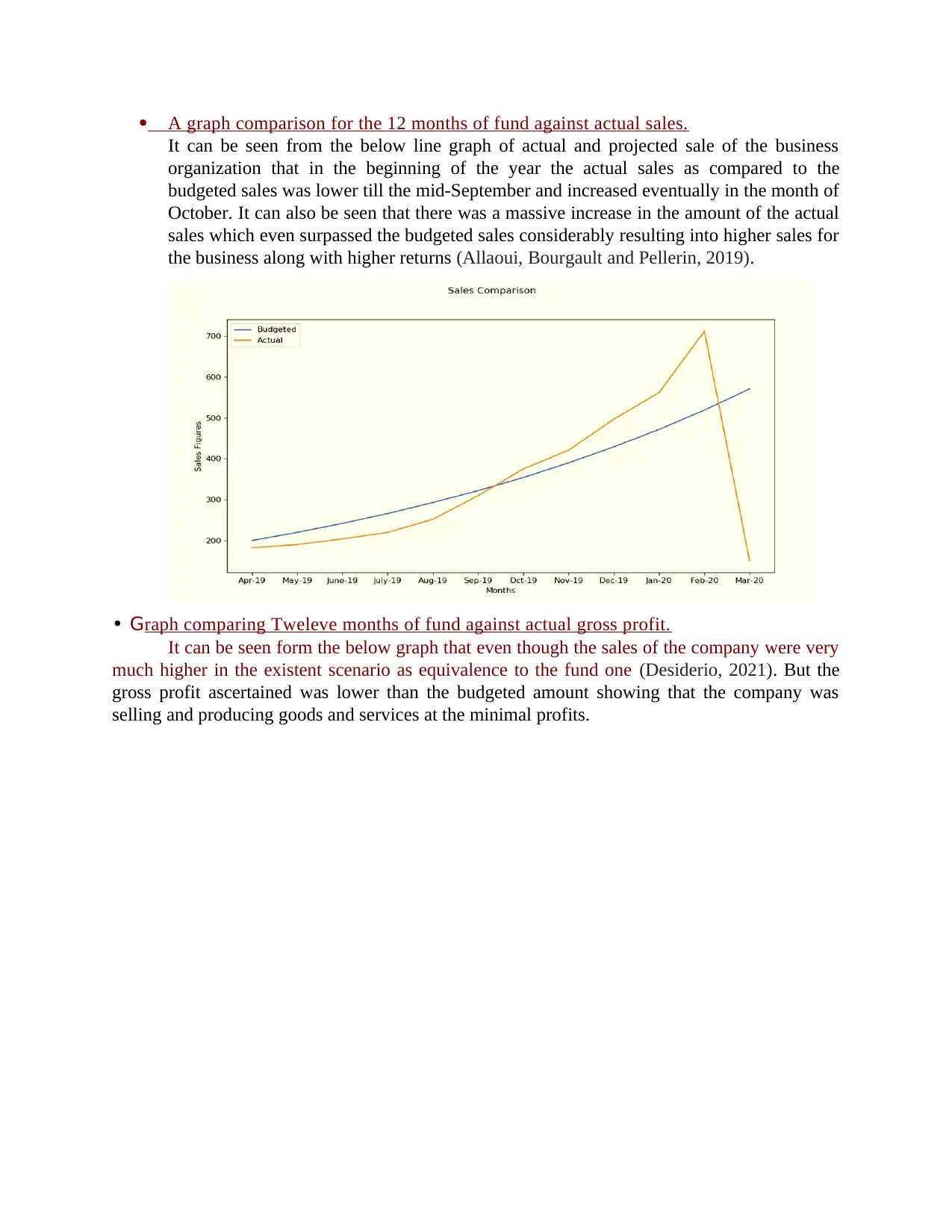

A graph comparison for the 12 months of fund against actual sales.

It can be seen from the below line graph of actual and projected sale of the business

organization that in the beginning of the year the actual sales as compared to the

budgeted sales was lower till the mid-September and increased eventually in the month of

October. It can also be seen that there was a massive increase in the amount of the actual

sales which even surpassed the budgeted sales considerably resulting into higher sales for

the business along with higher returns (Allaoui, Bourgault and Pellerin, 2019).

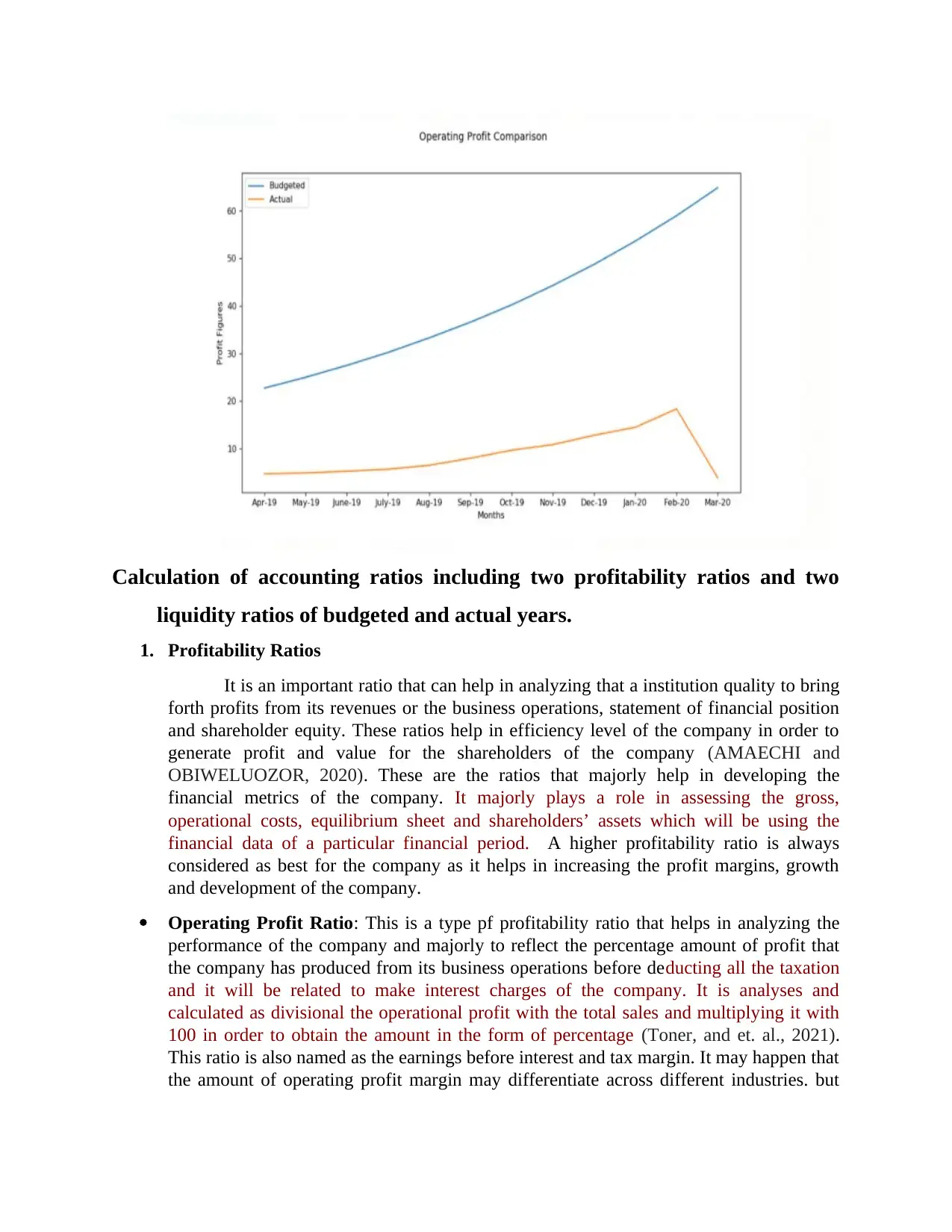

• Graph comparing Tweleve months of fund against actual gross profit.

It can be seen form the below graph that even though the sales of the company were very

much higher in the existent scenario as equivalence to the fund one (Desiderio, 2021). But the

gross profit ascertained was lower than the budgeted amount showing that the company was

selling and producing goods and services at the minimal profits.

It can be seen from the below line graph of actual and projected sale of the business

organization that in the beginning of the year the actual sales as compared to the

budgeted sales was lower till the mid-September and increased eventually in the month of

October. It can also be seen that there was a massive increase in the amount of the actual

sales which even surpassed the budgeted sales considerably resulting into higher sales for

the business along with higher returns (Allaoui, Bourgault and Pellerin, 2019).

• Graph comparing Tweleve months of fund against actual gross profit.

It can be seen form the below graph that even though the sales of the company were very

much higher in the existent scenario as equivalence to the fund one (Desiderio, 2021). But the

gross profit ascertained was lower than the budgeted amount showing that the company was

selling and producing goods and services at the minimal profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

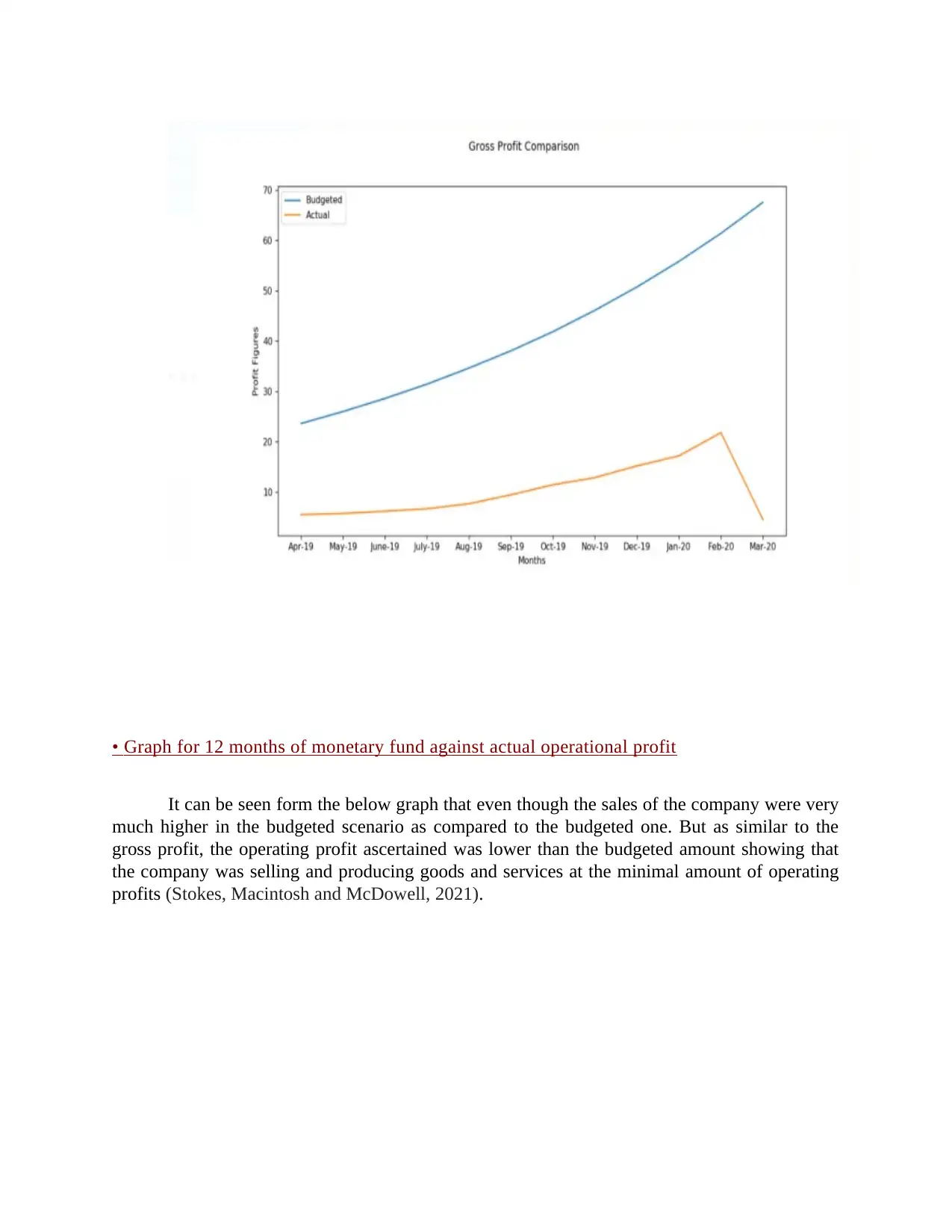

• Graph for 12 months of monetary fund against actual operational profit

It can be seen form the below graph that even though the sales of the company were very

much higher in the budgeted scenario as compared to the budgeted one. But as similar to the

gross profit, the operating profit ascertained was lower than the budgeted amount showing that

the company was selling and producing goods and services at the minimal amount of operating

profits (Stokes, Macintosh and McDowell, 2021).

It can be seen form the below graph that even though the sales of the company were very

much higher in the budgeted scenario as compared to the budgeted one. But as similar to the

gross profit, the operating profit ascertained was lower than the budgeted amount showing that

the company was selling and producing goods and services at the minimal amount of operating

profits (Stokes, Macintosh and McDowell, 2021).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Calculation of accounting ratios including two profitability ratios and two

liquidity ratios of budgeted and actual years.

1. Profitability Ratios

It is an important ratio that can help in analyzing that a institution quality to bring

forth profits from its revenues or the business operations, statement of financial position

and shareholder equity. These ratios help in efficiency level of the company in order to

generate profit and value for the shareholders of the company (AMAECHI and

OBIWELUOZOR, 2020). These are the ratios that majorly help in developing the

financial metrics of the company. It majorly plays a role in assessing the gross,

operational costs, equilibrium sheet and shareholders’ assets which will be using the

financial data of a particular financial period. A higher profitability ratio is always

considered as best for the company as it helps in increasing the profit margins, growth

and development of the company.

Operating Profit Ratio: This is a type pf profitability ratio that helps in analyzing the

performance of the company and majorly to reflect the percentage amount of profit that

the company has produced from its business operations before deducting all the taxation

and it will be related to make interest charges of the company. It is analyses and

calculated as divisional the operational profit with the total sales and multiplying it with

100 in order to obtain the amount in the form of percentage (Toner, and et. al., 2021).

This ratio is also named as the earnings before interest and tax margin. It may happen that

the amount of operating profit margin may differentiate across different industries. but

liquidity ratios of budgeted and actual years.

1. Profitability Ratios

It is an important ratio that can help in analyzing that a institution quality to bring

forth profits from its revenues or the business operations, statement of financial position

and shareholder equity. These ratios help in efficiency level of the company in order to

generate profit and value for the shareholders of the company (AMAECHI and

OBIWELUOZOR, 2020). These are the ratios that majorly help in developing the

financial metrics of the company. It majorly plays a role in assessing the gross,

operational costs, equilibrium sheet and shareholders’ assets which will be using the

financial data of a particular financial period. A higher profitability ratio is always

considered as best for the company as it helps in increasing the profit margins, growth

and development of the company.

Operating Profit Ratio: This is a type pf profitability ratio that helps in analyzing the

performance of the company and majorly to reflect the percentage amount of profit that

the company has produced from its business operations before deducting all the taxation

and it will be related to make interest charges of the company. It is analyses and

calculated as divisional the operational profit with the total sales and multiplying it with

100 in order to obtain the amount in the form of percentage (Toner, and et. al., 2021).

This ratio is also named as the earnings before interest and tax margin. It may happen that

the amount of operating profit margin may differentiate across different industries. but

this ratio also helps in revealing the top and best performers in an industry in accordance

to indicating the need for further development.

Formula Calculation

Operating profit / net sales * 100 Budgeted = 486 / 571 * 100 = 85.11 %

Actual = 105 / 150 * 100 = 70 %

Interpretation: It is analyses that the operating cost of profit margin in both the budgeted

and make financial is make a higher than the 15%. Which is considered for the effective

to achieve higher branding and make effective budgeted in the initial to start the year and

make an expected to earn the money. It will be beneficial for the company to make

budgeted and pay all the operation cost in the recent years.

Net Profit Ratio: It is basically related to provide a basic margin for the growth and

measures to generate the net income and generate the profit of percentage of sales. The

management company will be able to work and achieve higher profit to work and achieve

company's profit and different business division. Net profit margin is usually expressed

as a percentage, but can also be expressed as a decimal (Stich, 2019). The net profit

margin illustrates how every dollar of sales generated by a business turns into profit. Net

profit margin helps stakeholders to assess whether the management of a business is

making enough profit from the business operations and whether operating and overhead

costs are existing or not. This tool of ratio is considered as the most important tool of the

assessing the financial health of the company in the best manner.

Formula Calculation

Operating profit / net sales * 100 Budgeted = 393 / 571 * 100 = 68.82 %

Actual = 76.5 / 150 * 100 = 51%

Interpretation: In the budgeted case, the net income was higher than the existent stating

growth of the company capacity and try to covert sales into potential profit that was

higher with more efficiency. While, it was lower in the actual.

Liquidity Ratios: The liquidity magnitude relation is one of the important types to

measure financial performance that is used to find out a debtor's noises to deal with the

current financial obligation without raising extraneous form of great. Current ratios

include quick ratio, current ratio, and days sales outstanding (Perkin and Abraham, 2021).

It is considered as one of the most important financial accounting ratios as the regular

capacity of the company to deal with the day to day expenses and the short term financial

obligation helps in maintaining a healthy financial situation of the company.

to indicating the need for further development.

Formula Calculation

Operating profit / net sales * 100 Budgeted = 486 / 571 * 100 = 85.11 %

Actual = 105 / 150 * 100 = 70 %

Interpretation: It is analyses that the operating cost of profit margin in both the budgeted

and make financial is make a higher than the 15%. Which is considered for the effective

to achieve higher branding and make effective budgeted in the initial to start the year and

make an expected to earn the money. It will be beneficial for the company to make

budgeted and pay all the operation cost in the recent years.

Net Profit Ratio: It is basically related to provide a basic margin for the growth and

measures to generate the net income and generate the profit of percentage of sales. The

management company will be able to work and achieve higher profit to work and achieve

company's profit and different business division. Net profit margin is usually expressed

as a percentage, but can also be expressed as a decimal (Stich, 2019). The net profit

margin illustrates how every dollar of sales generated by a business turns into profit. Net

profit margin helps stakeholders to assess whether the management of a business is

making enough profit from the business operations and whether operating and overhead

costs are existing or not. This tool of ratio is considered as the most important tool of the

assessing the financial health of the company in the best manner.

Formula Calculation

Operating profit / net sales * 100 Budgeted = 393 / 571 * 100 = 68.82 %

Actual = 76.5 / 150 * 100 = 51%

Interpretation: In the budgeted case, the net income was higher than the existent stating

growth of the company capacity and try to covert sales into potential profit that was

higher with more efficiency. While, it was lower in the actual.

Liquidity Ratios: The liquidity magnitude relation is one of the important types to

measure financial performance that is used to find out a debtor's noises to deal with the

current financial obligation without raising extraneous form of great. Current ratios

include quick ratio, current ratio, and days sales outstanding (Perkin and Abraham, 2021).

It is considered as one of the most important financial accounting ratios as the regular

capacity of the company to deal with the day to day expenses and the short term financial

obligation helps in maintaining a healthy financial situation of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.