BPL 011: Comprehensive Analysis of Budgeted vs. Actual Finances

VerifiedAdded on 2022/12/09

|20

|2277

|499

Report

AI Summary

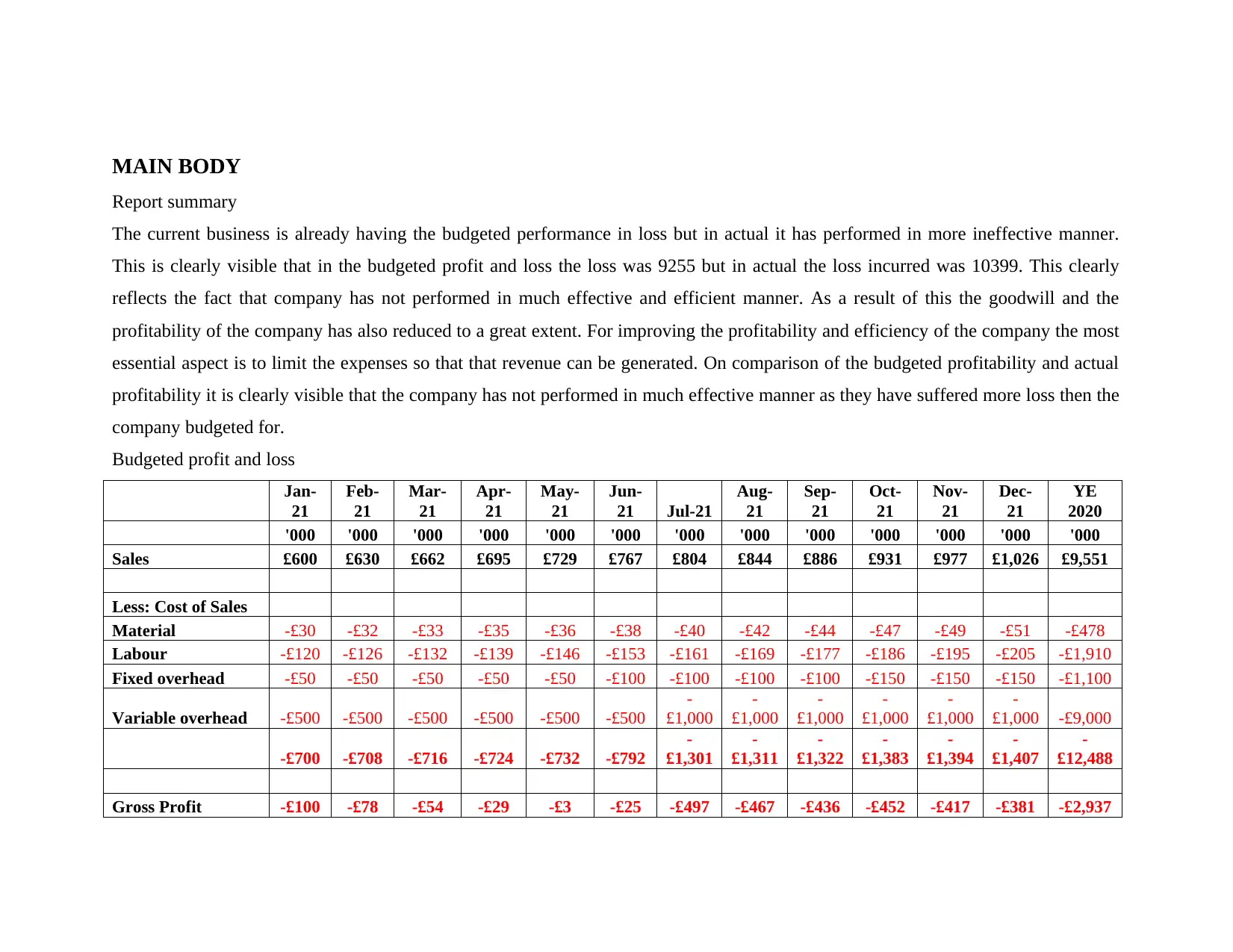

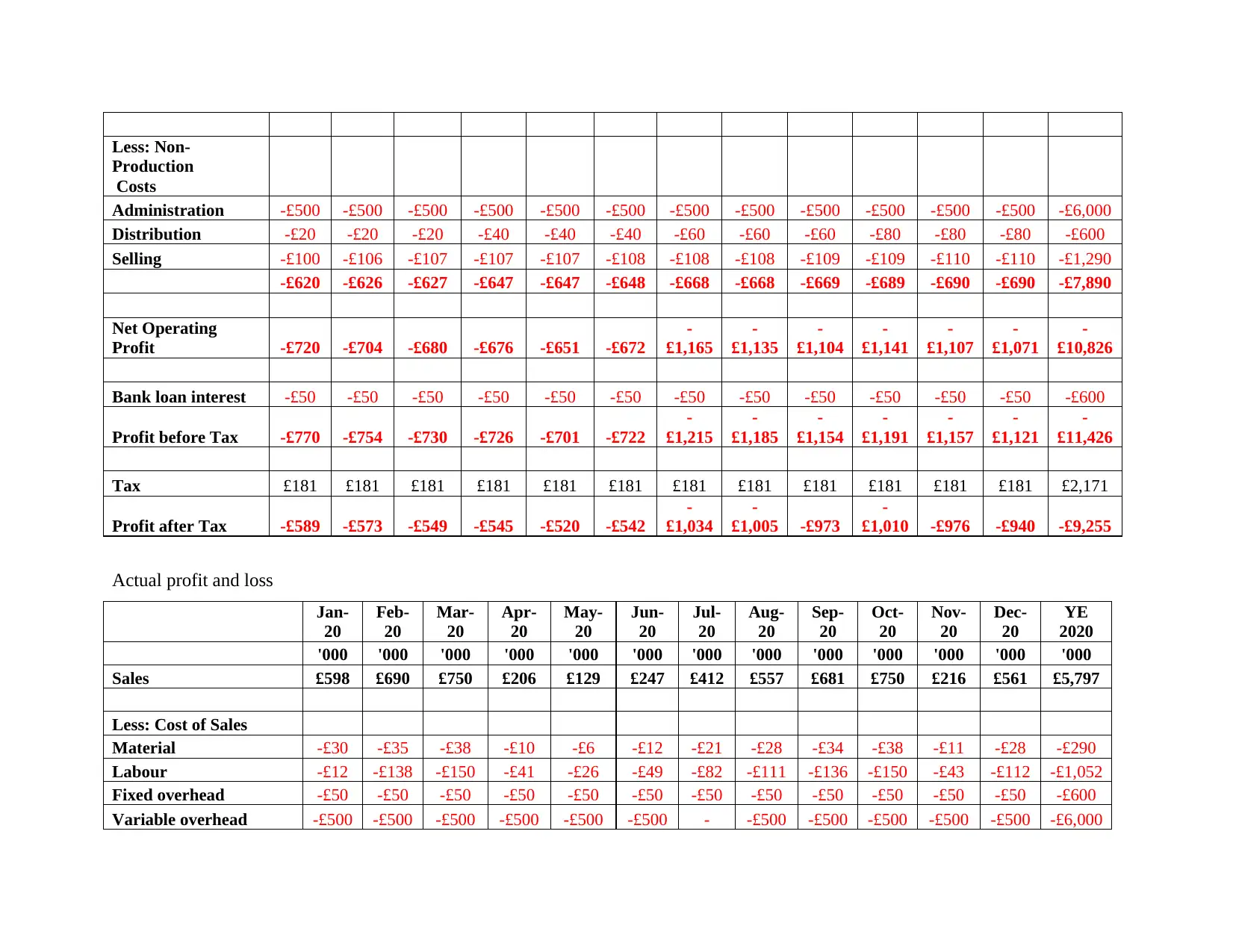

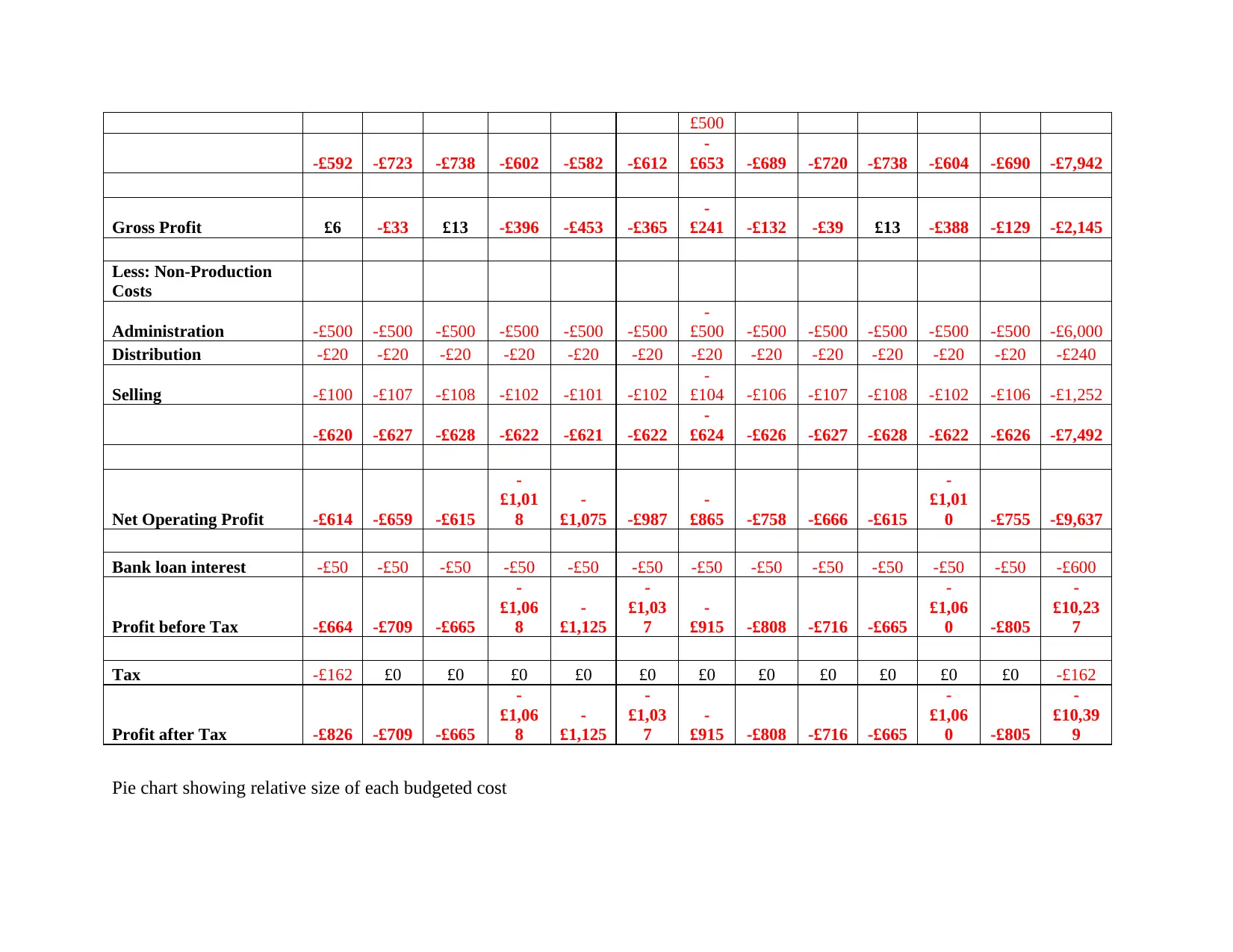

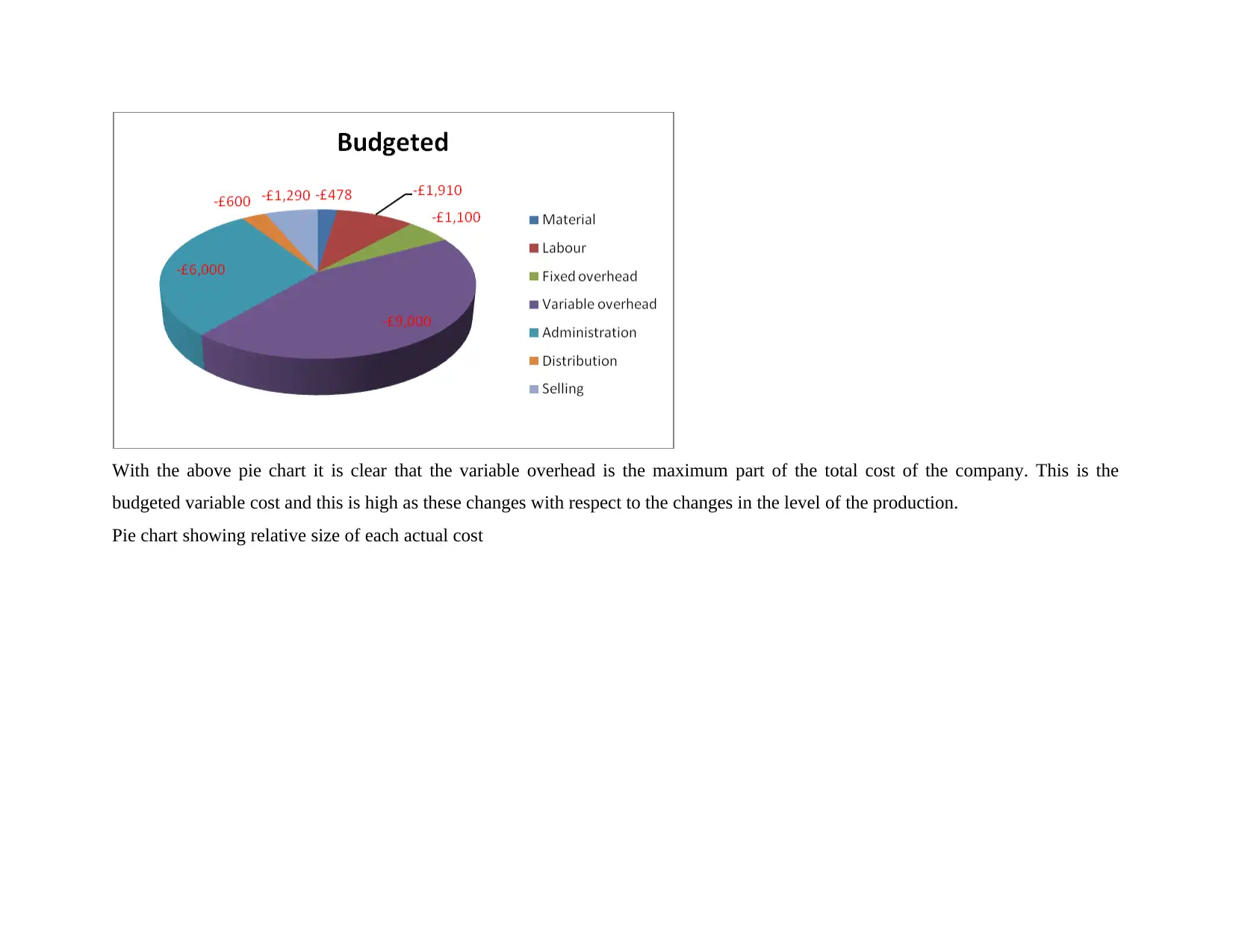

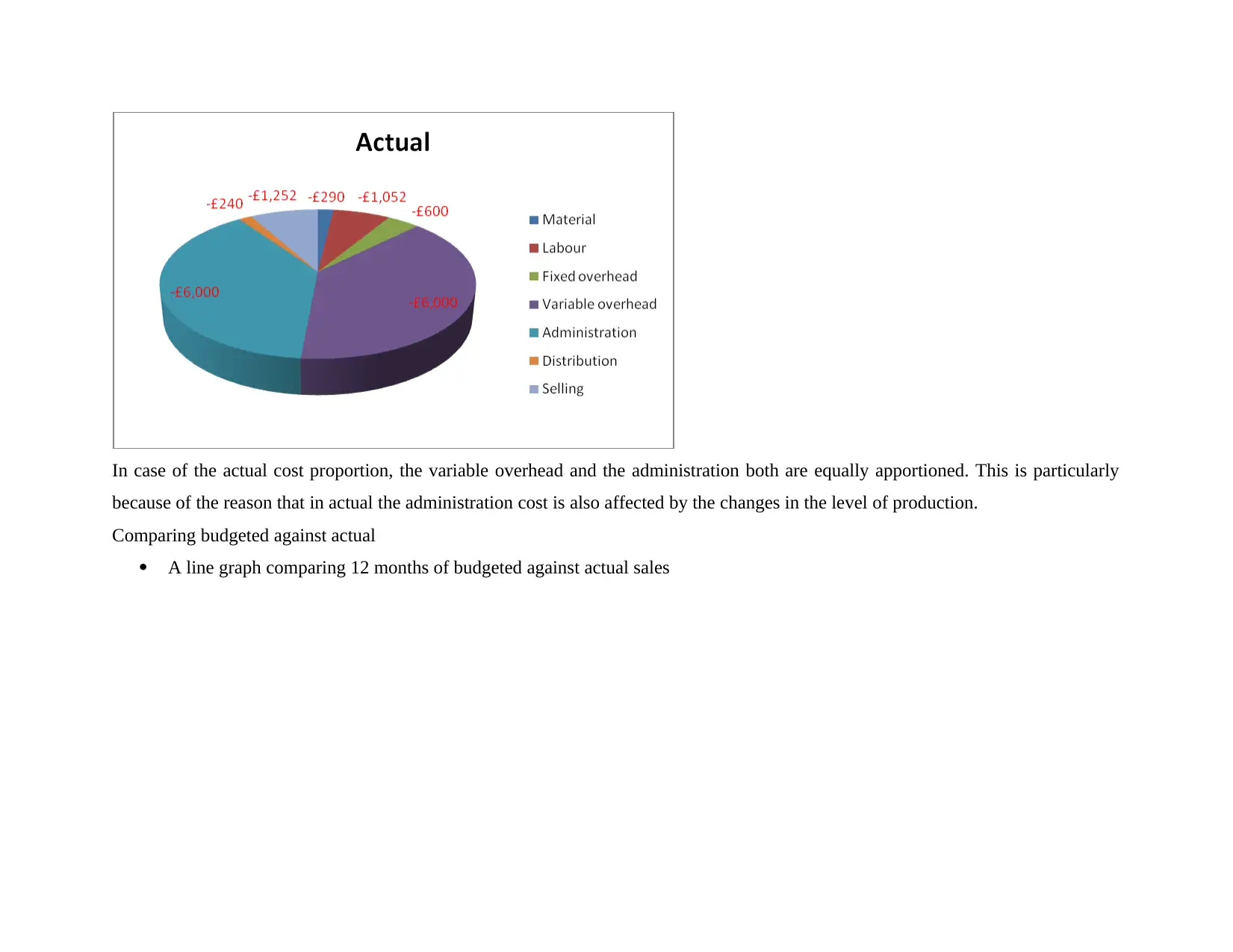

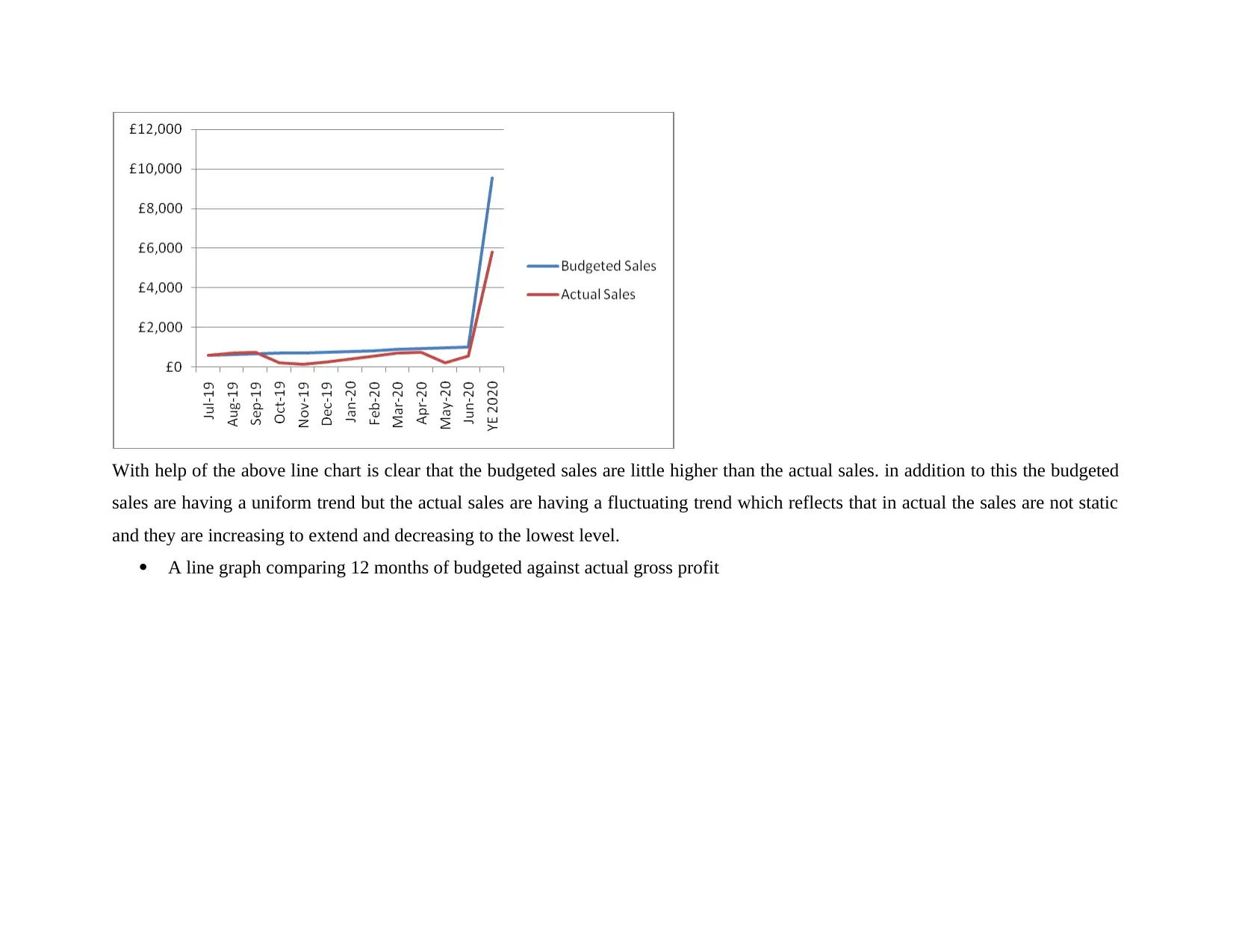

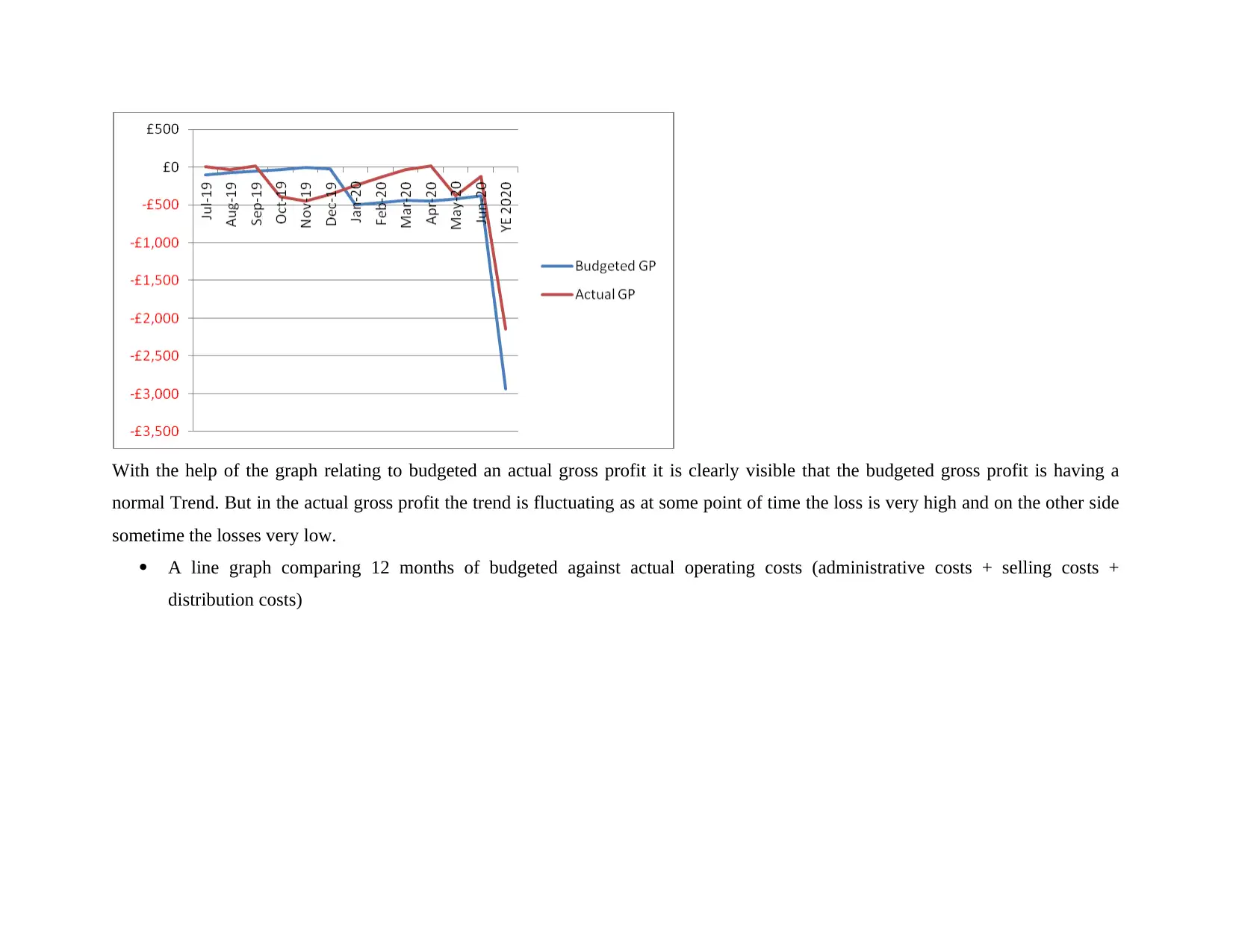

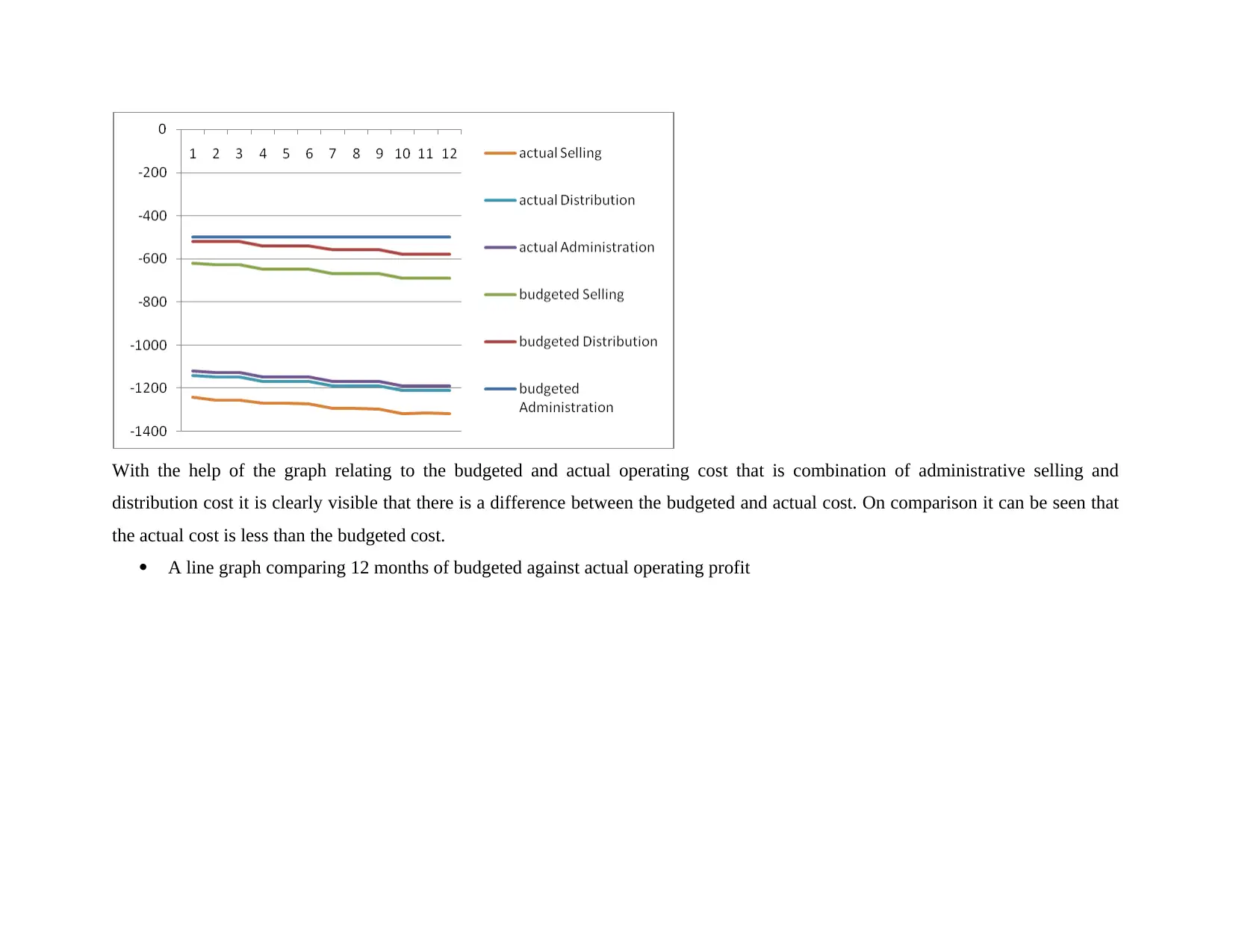

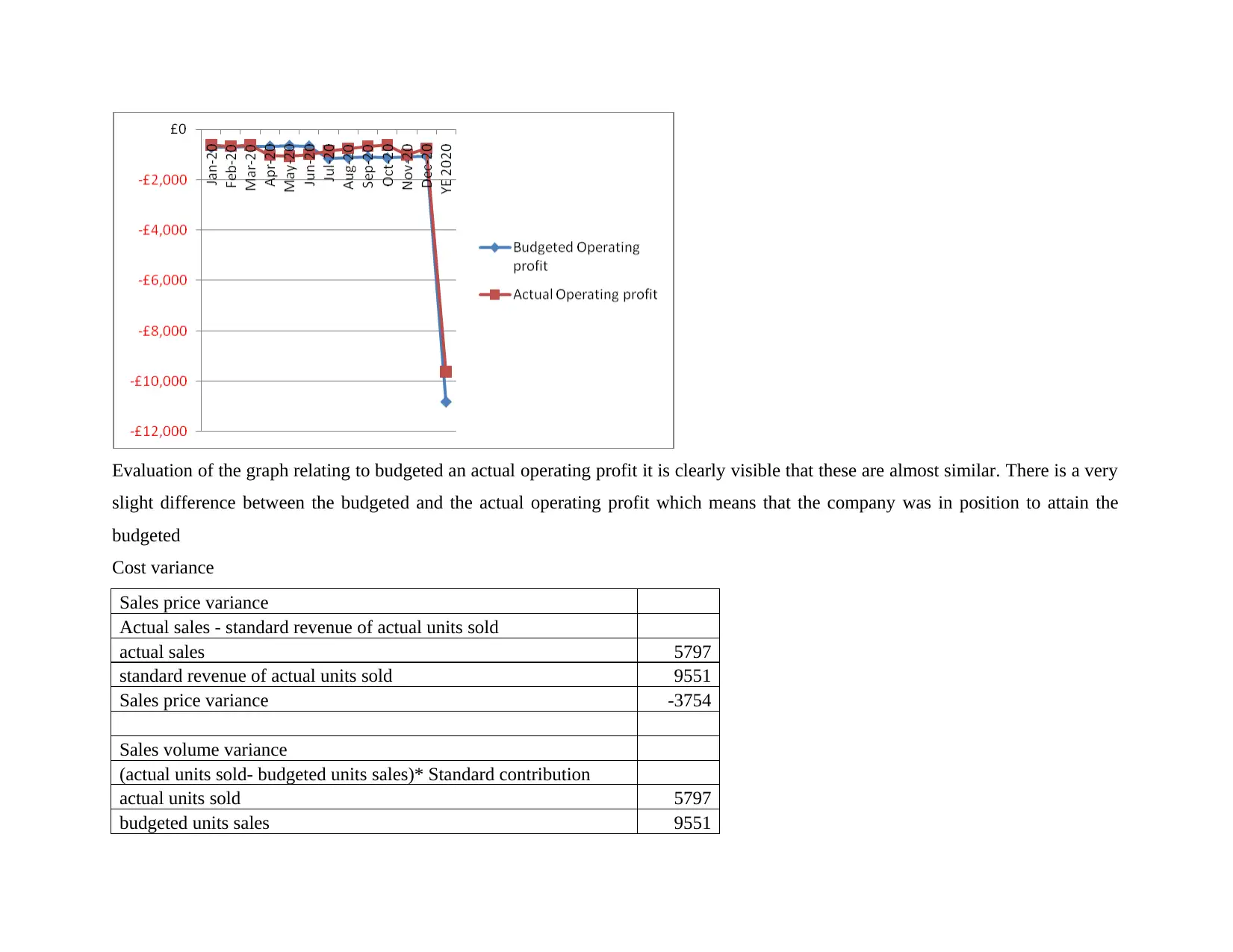

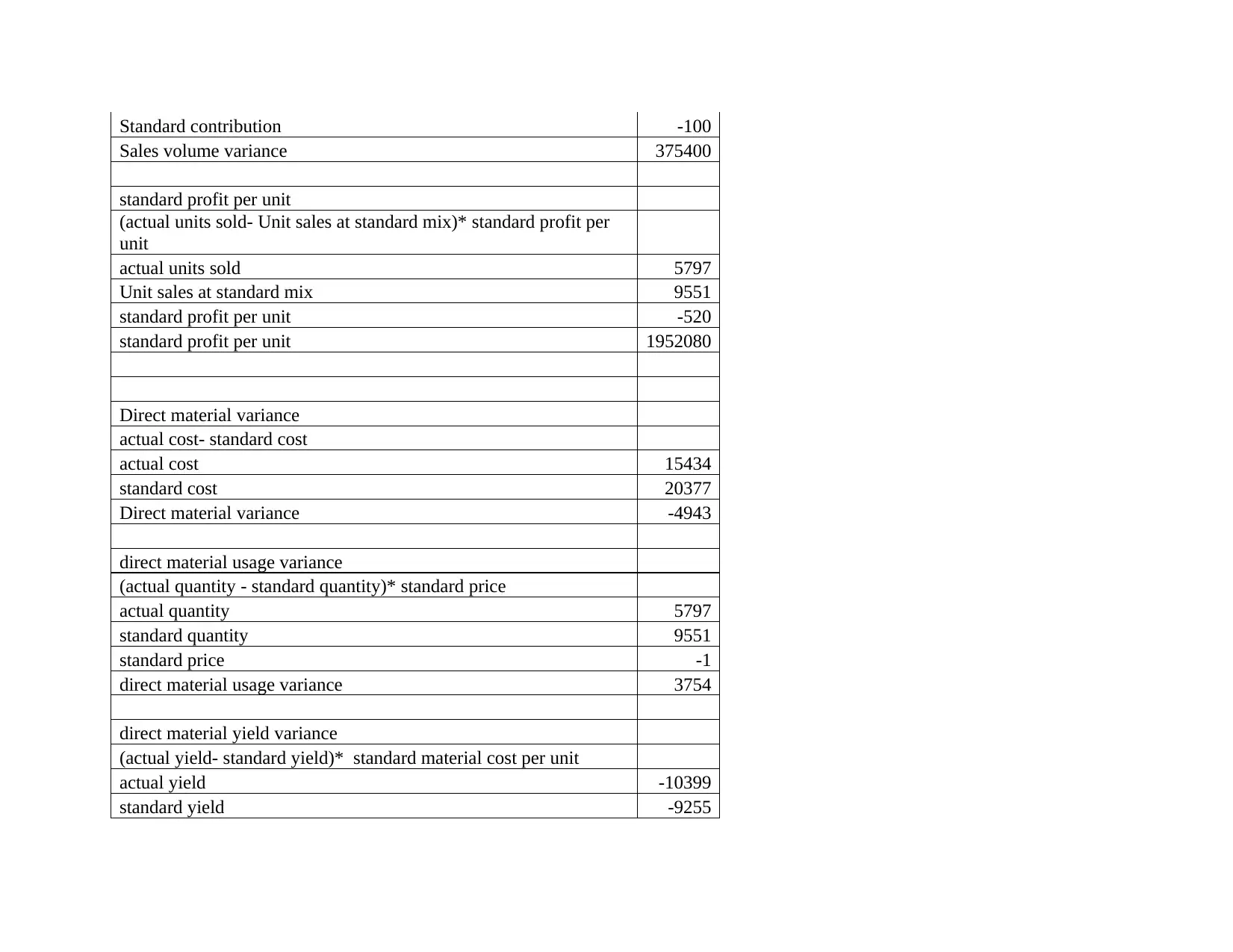

This report provides a detailed analysis of the financial performance of a business, comparing budgeted figures with actual results. The report highlights that the actual performance was less effective than the budgeted performance, resulting in higher losses. It includes an analysis of profit and loss statements, comparing sales, cost of sales, and non-production costs. The report uses pie charts and line graphs to visualize cost breakdowns and sales trends, and it evaluates variance in sales price and volume, direct materials, and labor. Financial ratios, including profitability, liquidity, and activity ratios, are calculated and analyzed to assess the company's financial health. The report also includes budgeted and actual balance sheets to provide a comprehensive view of the company's financial position, along with calculations of key financial ratios to evaluate performance. Overall, the analysis reveals areas where the company underperformed and provides insights into its financial strengths and weaknesses.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.