Accounting Theory and Issues: A Case Study of Brambles Ltd Financials

VerifiedAdded on 2023/05/27

|17

|3433

|476

Report

AI Summary

This report assesses the financial statements of Brambles Ltd, focusing on its compliance with the IASB reporting framework and the conceptual reporting framework. It analyzes the application of accounting standards and relevant accounting concepts, examining issues related to sales forecasting, profitability assumptions, and the recognition of assets, liabilities, income, and expenditure. The report also evaluates the qualitative characteristics of Brambles Ltd's financial statements, including relevance, reliability, comparability, and understandability, and how they impact decision-making. The stakeholder theory is deemed appropriate for the company, highlighting the interrelated relationships between the customers and business, communities, investors, employees and people that have stake in Brambles Industries Ltd. The analysis concludes with recommendations for improvements in financial reporting practices to enhance transparency and decision-making usefulness. The report uses figures from the Brambles Ltd 2018 annual report to support its analysis.

Running head: ACCOUNTING THEORY AND ISSUES

Accounting Theory and Issues

Name of the Student

Name of the University

Authors Note

Course ID

Accounting Theory and Issues

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING THEORY AND ISSUES

Executive Summary:

The objective of this report is to assess the financial statements of Brambles Ltd that has its

operation in Australia. The report would consider the IASB reporting framework and

determine whether the company complies with the conceptual reporting framework.

The report would take into the account the application of accounting standards and necessary

concepts which is applied on Brambles Ltd, affecting the overall reporting quality. The

assessment would conclude with the discussion regarding the application of conceptual

reporting framework in Brambles Ltd.

The current report is related with the application of conceptual framework in bookkeeping

process for recognizing and reporting on noteworthy items that are specified in the yearly

report of the business. The chosen corporation for the project is Brambles Ltd.

Executive Summary:

The objective of this report is to assess the financial statements of Brambles Ltd that has its

operation in Australia. The report would consider the IASB reporting framework and

determine whether the company complies with the conceptual reporting framework.

The report would take into the account the application of accounting standards and necessary

concepts which is applied on Brambles Ltd, affecting the overall reporting quality. The

assessment would conclude with the discussion regarding the application of conceptual

reporting framework in Brambles Ltd.

The current report is related with the application of conceptual framework in bookkeeping

process for recognizing and reporting on noteworthy items that are specified in the yearly

report of the business. The chosen corporation for the project is Brambles Ltd.

2ACCOUNTING THEORY AND ISSUES

Table of Contents

Introduction:...............................................................................................................................3

Company Background:...............................................................................................................3

Theory Appropriate for the Brambles Industries Ltd:................................................................4

Brambles Industries Accounting Issues:....................................................................................4

Conceptual Framework Accounting Objectives:.......................................................................5

Recognition Criteria:..................................................................................................................8

Recognition of Expenditure:....................................................................................................11

Qualitative Characteristics of Financial Statements:...............................................................12

Fundamental Qualitative Characteristics:............................................................................12

Enhancing Qualitative Characteristics:....................................................................................12

Sufficient information for Decision Making:...........................................................................13

Recommendations:...................................................................................................................13

Conclusion:..............................................................................................................................14

References:...............................................................................................................................15

Table of Contents

Introduction:...............................................................................................................................3

Company Background:...............................................................................................................3

Theory Appropriate for the Brambles Industries Ltd:................................................................4

Brambles Industries Accounting Issues:....................................................................................4

Conceptual Framework Accounting Objectives:.......................................................................5

Recognition Criteria:..................................................................................................................8

Recognition of Expenditure:....................................................................................................11

Qualitative Characteristics of Financial Statements:...............................................................12

Fundamental Qualitative Characteristics:............................................................................12

Enhancing Qualitative Characteristics:....................................................................................12

Sufficient information for Decision Making:...........................................................................13

Recommendations:...................................................................................................................13

Conclusion:..............................................................................................................................14

References:...............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING THEORY AND ISSUES

Introduction:

The conceptual framework is referred as the system of ideas and objectives that

results in the formation of the reliable set of rules and values. Particularly, in the areas of

accounting, the rule and standards sets down the function, nature and limits of financial

accounting as well as financial statements. The conceptual framework is usually viewed as

the analytical tool carrying numerous variation and contexts (Díaz et al. 2015). The

conceptual framework is useful in making conceptual differences and organization of ideas.

The stronger conceptual framework captures things that are real and it is executed in a

manner which is easy to remember and implement.

The present report is associated with the implementation of conceptual framework in

accounting procedure for identifying and reporting on significant items that are stated in the

annual report of the company. The chosen company for the assignment is Brambles Ltd. The

IASB introduced the conceptual framework to assist the board in developing the new

accounting standards that can enhance the process of reporting. The introduction of

conceptual framework would result in harmonization of the accounting practices of a

business. A qualitative discussion would be presented in this report regarding the Brambles

Ltd financial statements.

Company Background:

Brambles Industries Limited offers both the domestic and international supply chain

logistics solutions. The company provides reusable pallets, containers and crates. Brambles

circular business models continues to the share and reuse as the world’s largest pool of

reusable crates, pallets and containers (Brambles 2018). This allows the company to serve its

customers whereas minimising the effect on the environment and enhancing the efficiency as

well as safety of the supply chains across the world. Brambles Ltd platforms creates an

Introduction:

The conceptual framework is referred as the system of ideas and objectives that

results in the formation of the reliable set of rules and values. Particularly, in the areas of

accounting, the rule and standards sets down the function, nature and limits of financial

accounting as well as financial statements. The conceptual framework is usually viewed as

the analytical tool carrying numerous variation and contexts (Díaz et al. 2015). The

conceptual framework is useful in making conceptual differences and organization of ideas.

The stronger conceptual framework captures things that are real and it is executed in a

manner which is easy to remember and implement.

The present report is associated with the implementation of conceptual framework in

accounting procedure for identifying and reporting on significant items that are stated in the

annual report of the company. The chosen company for the assignment is Brambles Ltd. The

IASB introduced the conceptual framework to assist the board in developing the new

accounting standards that can enhance the process of reporting. The introduction of

conceptual framework would result in harmonization of the accounting practices of a

business. A qualitative discussion would be presented in this report regarding the Brambles

Ltd financial statements.

Company Background:

Brambles Industries Limited offers both the domestic and international supply chain

logistics solutions. The company provides reusable pallets, containers and crates. Brambles

circular business models continues to the share and reuse as the world’s largest pool of

reusable crates, pallets and containers (Brambles 2018). This allows the company to serve its

customers whereas minimising the effect on the environment and enhancing the efficiency as

well as safety of the supply chains across the world. Brambles Ltd platforms creates an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING THEORY AND ISSUES

invisible backbone of international supply chains, mainly serving the fast moving customer

goods, beverage, fresh produce retail and general manufacturing industries. Large brands

across the world trust Brambles to assist them in transporting life essentials in more effective,

safely and sustainable manner.

Theory Appropriate for the Brambles Industries Ltd:

On assessing the annual financial statement for Brambles Industries Ltd the

stakeholder theory is held appropriate for the company. The main purpose of choosing the

stakeholder theory is place focus on the interrelated relationships between the customers and

business, communities, investors, employees and people that have stake in Brambles

Industries Ltd. The stakeholder theory enables Brambles Industries Ltd to create value for its

shareholders as well as its stakeholders that are involved in the day to activities of the

business.

Brambles Industries Accounting Issues:

Issues associated to sales forecasting and related expenses: The accounting issues for

Brambles is involves the sales forecast and associated expenditure that facilitates financial

estimations for the future comparison. The inherent sales estimations regarding the financial

performance might turn out to be unreliable. The sales might decline substantially from the

earlier years with the cost of doing business can increase without any notice. Furthermore,

Brambles sales cycle might be longer than anticipated. Therefore, these accounting issues can

result in immediate financial problems that might affect the strategic planning.

Inappropriate profitability assumptions: As evident in case of Brambles, the strategic

planning of the company is dependent on the success of the financial planning. Brambles is

dependent on the equity capital financing for meeting its strategic objectives and may turn out

to be disappointing if the cash management is untimely. Brambles Industries Ltd profitability

invisible backbone of international supply chains, mainly serving the fast moving customer

goods, beverage, fresh produce retail and general manufacturing industries. Large brands

across the world trust Brambles to assist them in transporting life essentials in more effective,

safely and sustainable manner.

Theory Appropriate for the Brambles Industries Ltd:

On assessing the annual financial statement for Brambles Industries Ltd the

stakeholder theory is held appropriate for the company. The main purpose of choosing the

stakeholder theory is place focus on the interrelated relationships between the customers and

business, communities, investors, employees and people that have stake in Brambles

Industries Ltd. The stakeholder theory enables Brambles Industries Ltd to create value for its

shareholders as well as its stakeholders that are involved in the day to activities of the

business.

Brambles Industries Accounting Issues:

Issues associated to sales forecasting and related expenses: The accounting issues for

Brambles is involves the sales forecast and associated expenditure that facilitates financial

estimations for the future comparison. The inherent sales estimations regarding the financial

performance might turn out to be unreliable. The sales might decline substantially from the

earlier years with the cost of doing business can increase without any notice. Furthermore,

Brambles sales cycle might be longer than anticipated. Therefore, these accounting issues can

result in immediate financial problems that might affect the strategic planning.

Inappropriate profitability assumptions: As evident in case of Brambles, the strategic

planning of the company is dependent on the success of the financial planning. Brambles is

dependent on the equity capital financing for meeting its strategic objectives and may turn out

to be disappointing if the cash management is untimely. Brambles Industries Ltd profitability

5ACCOUNTING THEORY AND ISSUES

assumptions is excessively optimistic as there may be inadequate retained earnings available

for making re-investment in strategic planning.

Conceptual Framework Accounting Objectives:

In financial reporting, the conceptual framework is regarded as the theory of

accounting which is prepared by the standard setting body against which the practical

problems can be objectively tested. The conceptual framework is regarded as the body of

fundamentals and interrelated objectives (Sheppes et al. 2014). The objectives of the

conceptual framework is to recognize the goals and purpose of financial reporting as well as

the underlying fundamentals that assist in attaining those objectives. The objectives of the

conceptual framework is stated below;

a. The objectives of conceptual framework is to introduce consistency in accounting

practice which is usually followed by several businesses. This implies that the

alternative treatments that are available for transactions should be reduced to

introduce consistent accounting practice.

b. The objective of conceptual framework is to make sure that the annual financial

statements of businesses are peppered in a manner that the relevant information are

represented in the financial statements (Bridgett et al. 2015). This would enable the

shareholders, probable investors, creditors and lenders to make use of the relevant

information in undertaking decision relating to the future investments and current

shareholder’s holdings of shares. The financial statements are often viewed as the

performance matrix report for a business. As evident in the situation of Brambles Ltd,

the financial statement of the Brambles reflects noteworthy information that are

required by the shareholders to make decision regarding the future investments. The

statement of profit and loss, statement of financial position and cash flow statement is

prepared effectively that can offer the shareholders with the in depth information

assumptions is excessively optimistic as there may be inadequate retained earnings available

for making re-investment in strategic planning.

Conceptual Framework Accounting Objectives:

In financial reporting, the conceptual framework is regarded as the theory of

accounting which is prepared by the standard setting body against which the practical

problems can be objectively tested. The conceptual framework is regarded as the body of

fundamentals and interrelated objectives (Sheppes et al. 2014). The objectives of the

conceptual framework is to recognize the goals and purpose of financial reporting as well as

the underlying fundamentals that assist in attaining those objectives. The objectives of the

conceptual framework is stated below;

a. The objectives of conceptual framework is to introduce consistency in accounting

practice which is usually followed by several businesses. This implies that the

alternative treatments that are available for transactions should be reduced to

introduce consistent accounting practice.

b. The objective of conceptual framework is to make sure that the annual financial

statements of businesses are peppered in a manner that the relevant information are

represented in the financial statements (Bridgett et al. 2015). This would enable the

shareholders, probable investors, creditors and lenders to make use of the relevant

information in undertaking decision relating to the future investments and current

shareholder’s holdings of shares. The financial statements are often viewed as the

performance matrix report for a business. As evident in the situation of Brambles Ltd,

the financial statement of the Brambles reflects noteworthy information that are

required by the shareholders to make decision regarding the future investments. The

statement of profit and loss, statement of financial position and cash flow statement is

prepared effectively that can offer the shareholders with the in depth information

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING THEORY AND ISSUES

about company’s overall performance and how the business is using the shareholders

fund.

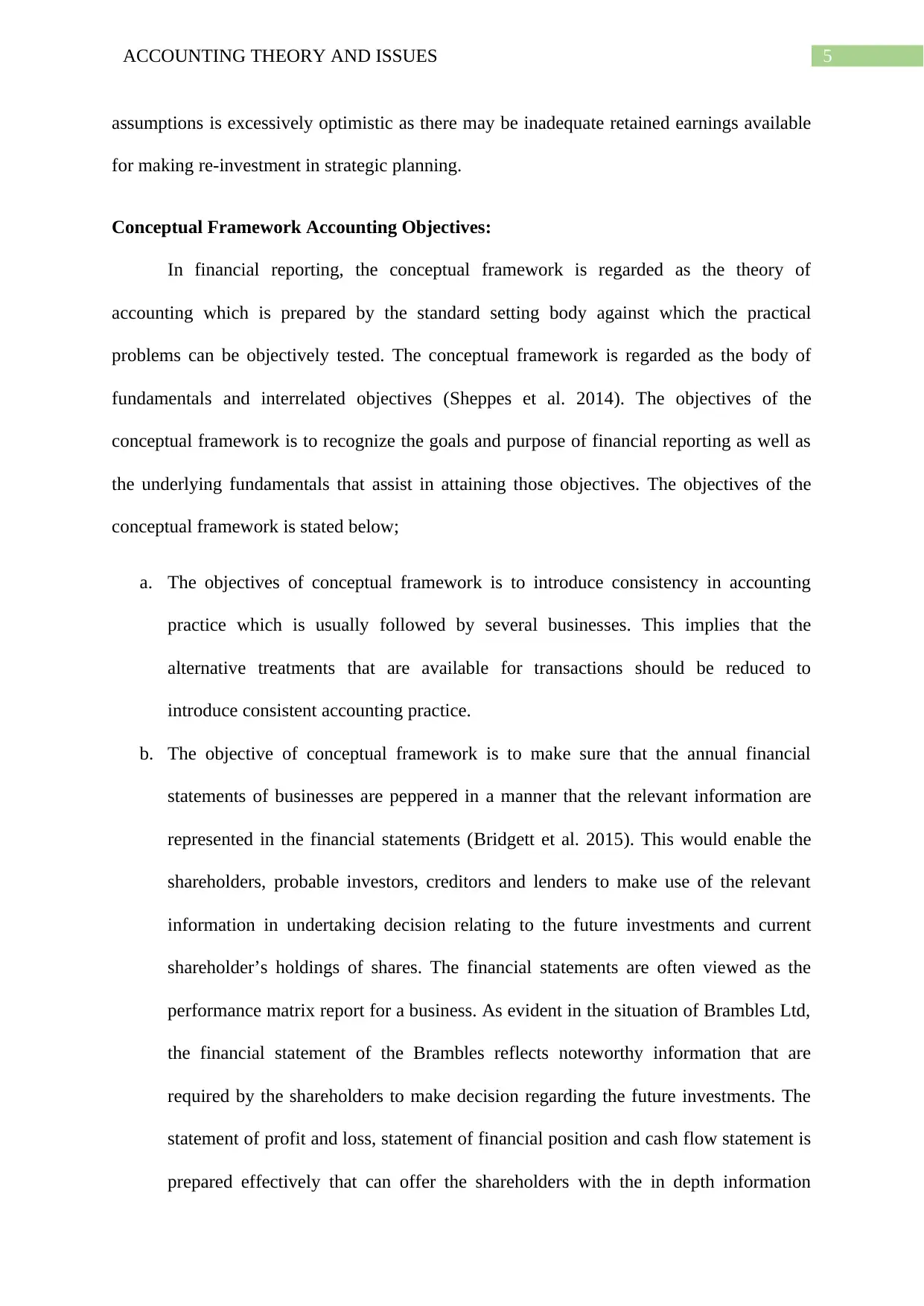

c. Another conceptual framework objective is to effectively report the sum of cash

produced by a company. The conceptual framework is useful in determining the

resources that the business would be required for producing future inflow of cash

(Macve 2015). On analysing the annual report of Brambles, the key drivers of the

cash flow form the profitability, capital expenditure and movements in the working

capital. Over the period of five years a strong growth in profitability for Brambles Ltd

has been witnessed. This is largely driven by significant investments in capital

expenses to support the growth. The capital expenditure of Brambles Ltd has

increased to support the growth of pallets operations with one-time change in the

process of payment which ultimately increased the working capital (Brambles 2018).

The significant improvement during the 2018 replicates improved EBITDA, stronger

working capital management, greater collection of assets and US$ 150 million inflow

of cash originating from the repayment of HFG joint venture loan, which offset

increased the cash capital expenses.

Figure 1: Cash flow from Operations of Brambles Ltd

(Source: Brambles 2018)

about company’s overall performance and how the business is using the shareholders

fund.

c. Another conceptual framework objective is to effectively report the sum of cash

produced by a company. The conceptual framework is useful in determining the

resources that the business would be required for producing future inflow of cash

(Macve 2015). On analysing the annual report of Brambles, the key drivers of the

cash flow form the profitability, capital expenditure and movements in the working

capital. Over the period of five years a strong growth in profitability for Brambles Ltd

has been witnessed. This is largely driven by significant investments in capital

expenses to support the growth. The capital expenditure of Brambles Ltd has

increased to support the growth of pallets operations with one-time change in the

process of payment which ultimately increased the working capital (Brambles 2018).

The significant improvement during the 2018 replicates improved EBITDA, stronger

working capital management, greater collection of assets and US$ 150 million inflow

of cash originating from the repayment of HFG joint venture loan, which offset

increased the cash capital expenses.

Figure 1: Cash flow from Operations of Brambles Ltd

(Source: Brambles 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND ISSUES

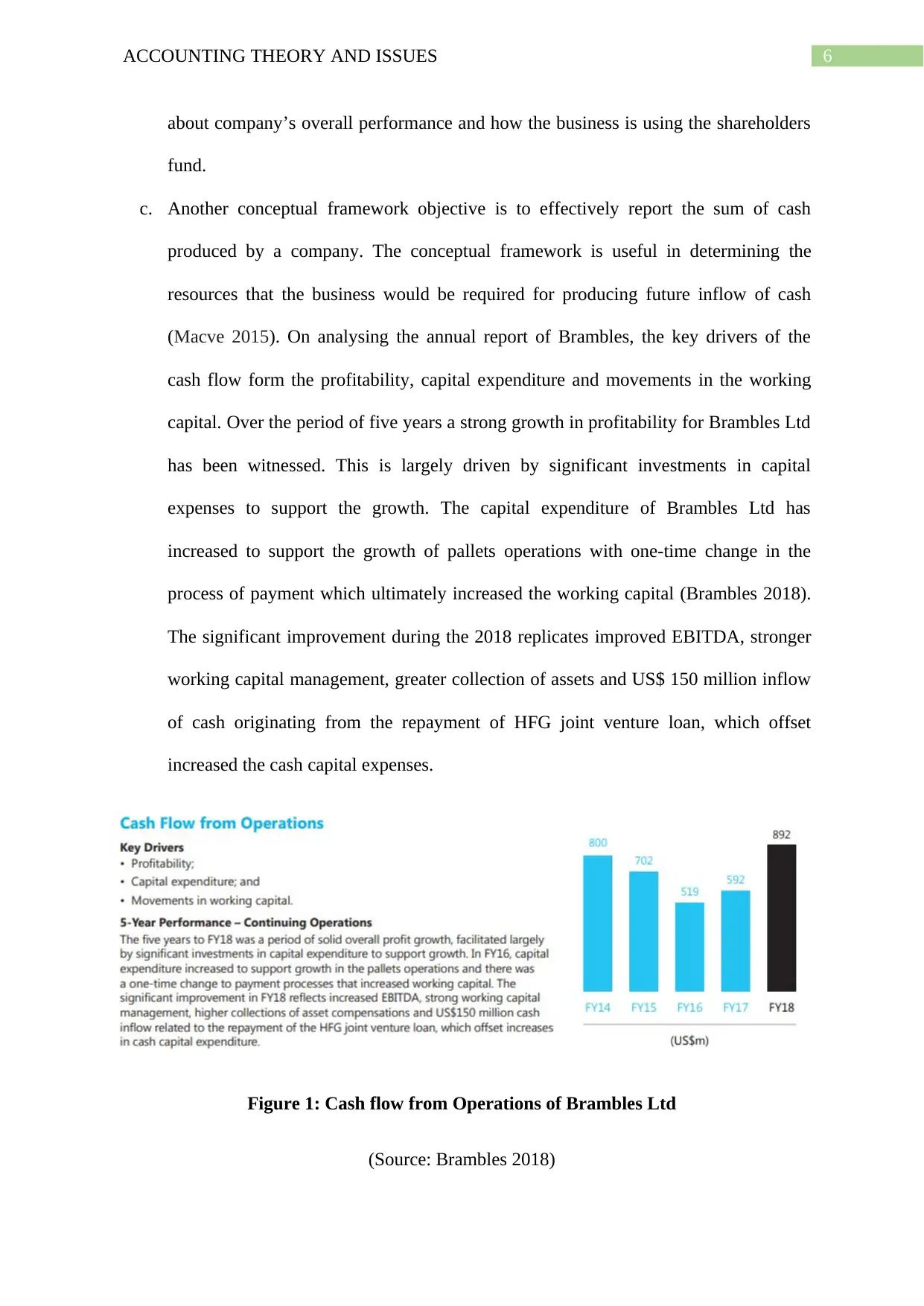

d. The conceptual framework is considered useful in predicting all the necessary

information that relates to the assets, liabilities, income and expenditure of the

business. This information is considered helpful in provide a clear understanding of

the business financial terms (Barker and Teixeira 2018). The Brambles Ltd in its

statement of profit and loss account reflected the growth in sales, direct cost

efficiencies and indirect reduction in costs all through the group.

Figure 2: Figure representing Profit and Loss Account of Brambles Ltd

(Source: Brambles 2018)

d. The conceptual framework is considered useful in predicting all the necessary

information that relates to the assets, liabilities, income and expenditure of the

business. This information is considered helpful in provide a clear understanding of

the business financial terms (Barker and Teixeira 2018). The Brambles Ltd in its

statement of profit and loss account reflected the growth in sales, direct cost

efficiencies and indirect reduction in costs all through the group.

Figure 2: Figure representing Profit and Loss Account of Brambles Ltd

(Source: Brambles 2018)

8ACCOUNTING THEORY AND ISSUES

The central objective of the conceptual framework of reporting is to make sure that

the financial statement of the business is prepared in compliance with the framework

requirements (Libby 2017). The framework acts as the means of objectively representing the

financial statements since the guidelines that are mentioned in the conceptual framework is

aimed at helping the business in preparing the annual report that displays all the relevant

information to the general public. The conceptual framework promotes simplicity and clarity

in offering financial information so that all the related parties of the company can better

understand the financial information and then form a decision for making investment.

Recognition Criteria:

The recognition criteria must be followed to fairly represent the financial statements

of a business. This also requires recording the items based on the requirements of the

conceptual framework. The AASB has issued accounting standard that lay down the

guidelines to be valued for treating the financial items and hence make sure that the annual

reports represent true and fair view (Spiceland et al. 2018). The criteria for identifying the

item is related to the economic benefits and items reliability. There are numerous items that

are significant and the same has been identified by the Brambles Ltd is discussed below;

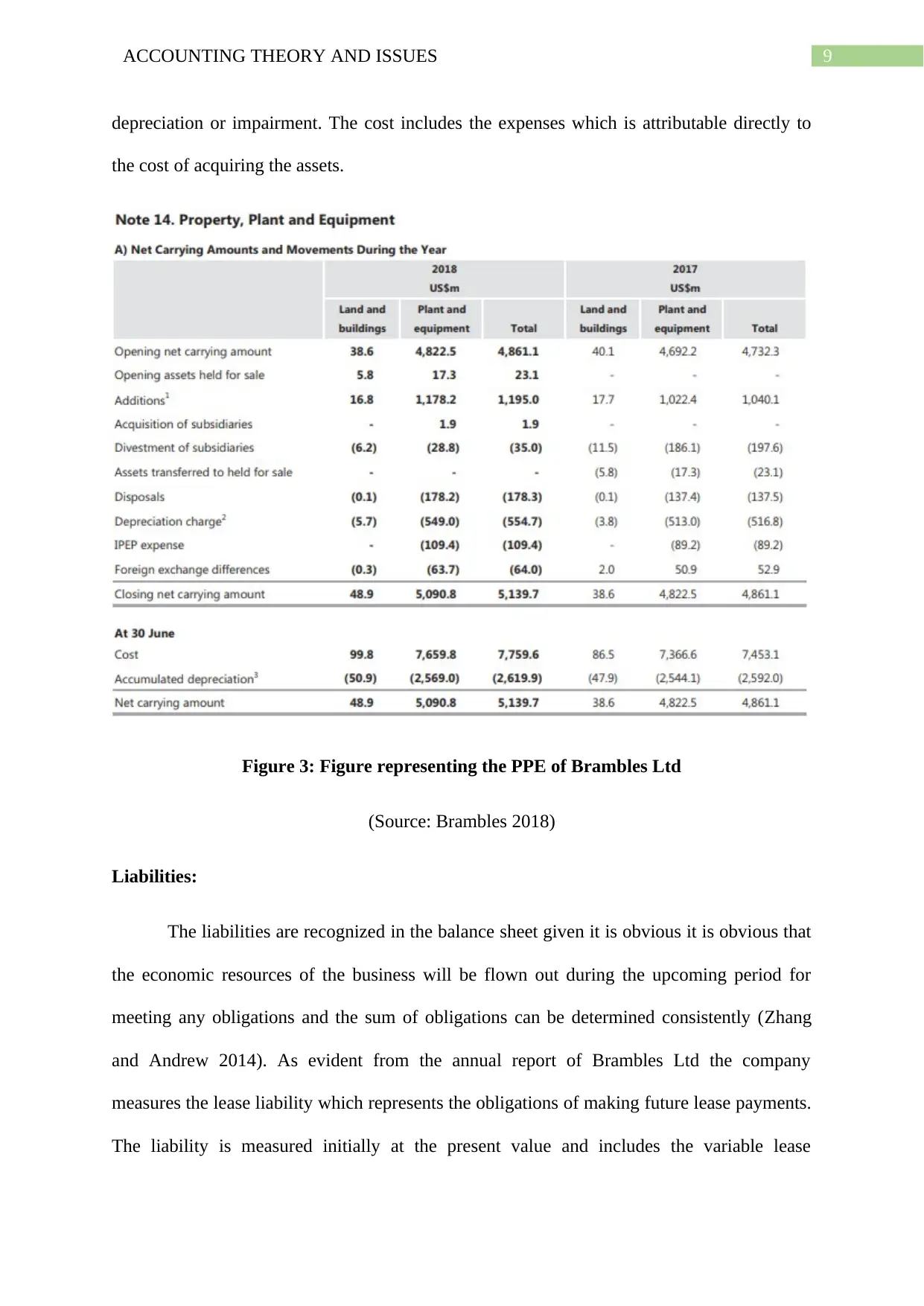

Assets:

As per the general purpose financial framework the assets should be subdivided in

short and long term type which is better known as current and non-current assets individually.

Brambles ltd assets are presented in the statement of financial position as current and non-

current assets (Handel, Valerio and Sánchez Puerta 2016). Brambles Ltd also reports the

intangible assets in the form of investments that is reflected under the non-current assets of

the business. Brambles Ltd identifies the financial assets based on the fair value through the

profit and loss (Brambles 2018). It identifies the PPE at their stated cost which is net of any

The central objective of the conceptual framework of reporting is to make sure that

the financial statement of the business is prepared in compliance with the framework

requirements (Libby 2017). The framework acts as the means of objectively representing the

financial statements since the guidelines that are mentioned in the conceptual framework is

aimed at helping the business in preparing the annual report that displays all the relevant

information to the general public. The conceptual framework promotes simplicity and clarity

in offering financial information so that all the related parties of the company can better

understand the financial information and then form a decision for making investment.

Recognition Criteria:

The recognition criteria must be followed to fairly represent the financial statements

of a business. This also requires recording the items based on the requirements of the

conceptual framework. The AASB has issued accounting standard that lay down the

guidelines to be valued for treating the financial items and hence make sure that the annual

reports represent true and fair view (Spiceland et al. 2018). The criteria for identifying the

item is related to the economic benefits and items reliability. There are numerous items that

are significant and the same has been identified by the Brambles Ltd is discussed below;

Assets:

As per the general purpose financial framework the assets should be subdivided in

short and long term type which is better known as current and non-current assets individually.

Brambles ltd assets are presented in the statement of financial position as current and non-

current assets (Handel, Valerio and Sánchez Puerta 2016). Brambles Ltd also reports the

intangible assets in the form of investments that is reflected under the non-current assets of

the business. Brambles Ltd identifies the financial assets based on the fair value through the

profit and loss (Brambles 2018). It identifies the PPE at their stated cost which is net of any

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING THEORY AND ISSUES

depreciation or impairment. The cost includes the expenses which is attributable directly to

the cost of acquiring the assets.

Figure 3: Figure representing the PPE of Brambles Ltd

(Source: Brambles 2018)

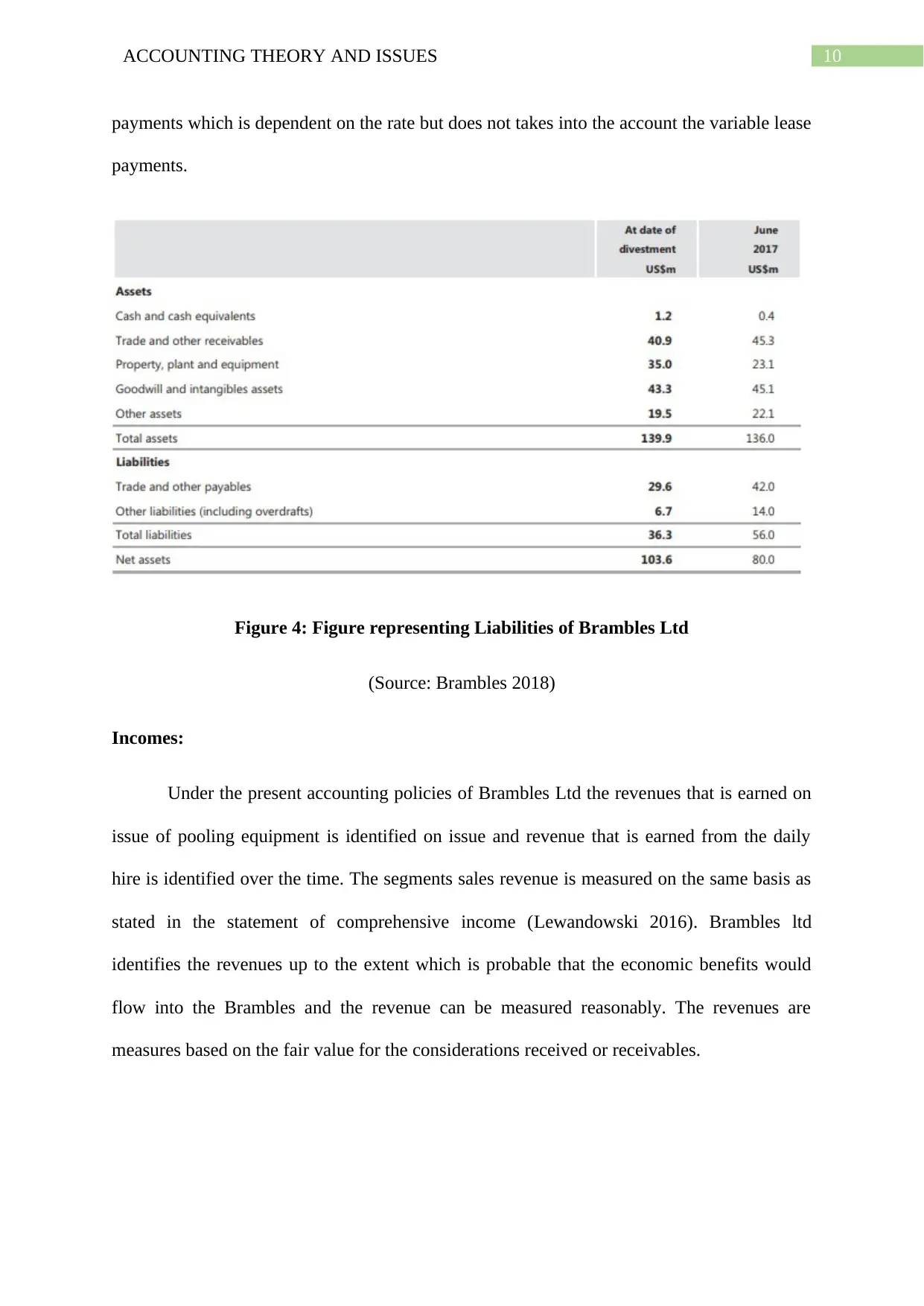

Liabilities:

The liabilities are recognized in the balance sheet given it is obvious it is obvious that

the economic resources of the business will be flown out during the upcoming period for

meeting any obligations and the sum of obligations can be determined consistently (Zhang

and Andrew 2014). As evident from the annual report of Brambles Ltd the company

measures the lease liability which represents the obligations of making future lease payments.

The liability is measured initially at the present value and includes the variable lease

depreciation or impairment. The cost includes the expenses which is attributable directly to

the cost of acquiring the assets.

Figure 3: Figure representing the PPE of Brambles Ltd

(Source: Brambles 2018)

Liabilities:

The liabilities are recognized in the balance sheet given it is obvious it is obvious that

the economic resources of the business will be flown out during the upcoming period for

meeting any obligations and the sum of obligations can be determined consistently (Zhang

and Andrew 2014). As evident from the annual report of Brambles Ltd the company

measures the lease liability which represents the obligations of making future lease payments.

The liability is measured initially at the present value and includes the variable lease

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING THEORY AND ISSUES

payments which is dependent on the rate but does not takes into the account the variable lease

payments.

Figure 4: Figure representing Liabilities of Brambles Ltd

(Source: Brambles 2018)

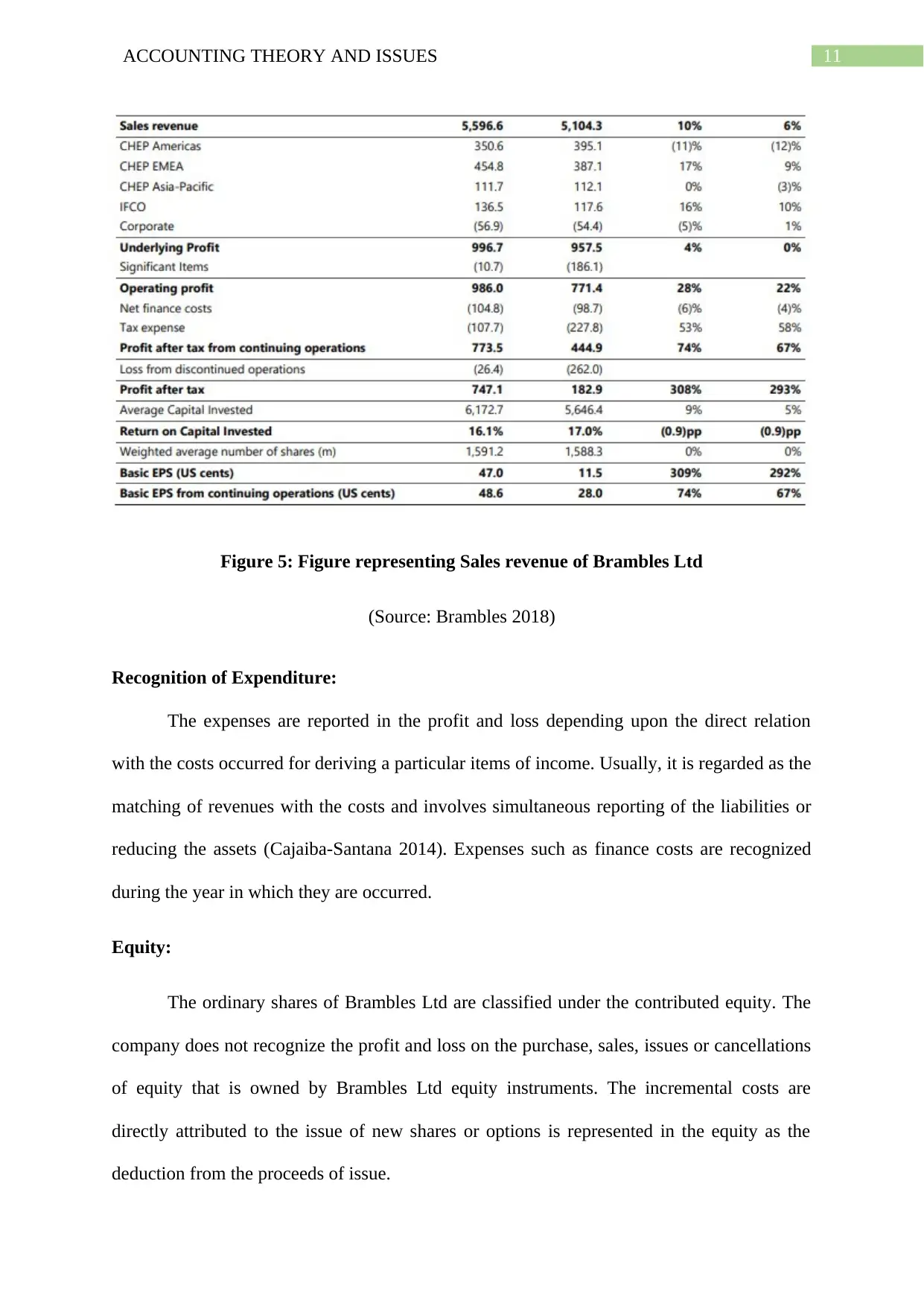

Incomes:

Under the present accounting policies of Brambles Ltd the revenues that is earned on

issue of pooling equipment is identified on issue and revenue that is earned from the daily

hire is identified over the time. The segments sales revenue is measured on the same basis as

stated in the statement of comprehensive income (Lewandowski 2016). Brambles ltd

identifies the revenues up to the extent which is probable that the economic benefits would

flow into the Brambles and the revenue can be measured reasonably. The revenues are

measures based on the fair value for the considerations received or receivables.

payments which is dependent on the rate but does not takes into the account the variable lease

payments.

Figure 4: Figure representing Liabilities of Brambles Ltd

(Source: Brambles 2018)

Incomes:

Under the present accounting policies of Brambles Ltd the revenues that is earned on

issue of pooling equipment is identified on issue and revenue that is earned from the daily

hire is identified over the time. The segments sales revenue is measured on the same basis as

stated in the statement of comprehensive income (Lewandowski 2016). Brambles ltd

identifies the revenues up to the extent which is probable that the economic benefits would

flow into the Brambles and the revenue can be measured reasonably. The revenues are

measures based on the fair value for the considerations received or receivables.

11ACCOUNTING THEORY AND ISSUES

Figure 5: Figure representing Sales revenue of Brambles Ltd

(Source: Brambles 2018)

Recognition of Expenditure:

The expenses are reported in the profit and loss depending upon the direct relation

with the costs occurred for deriving a particular items of income. Usually, it is regarded as the

matching of revenues with the costs and involves simultaneous reporting of the liabilities or

reducing the assets (Cajaiba-Santana 2014). Expenses such as finance costs are recognized

during the year in which they are occurred.

Equity:

The ordinary shares of Brambles Ltd are classified under the contributed equity. The

company does not recognize the profit and loss on the purchase, sales, issues or cancellations

of equity that is owned by Brambles Ltd equity instruments. The incremental costs are

directly attributed to the issue of new shares or options is represented in the equity as the

deduction from the proceeds of issue.

Figure 5: Figure representing Sales revenue of Brambles Ltd

(Source: Brambles 2018)

Recognition of Expenditure:

The expenses are reported in the profit and loss depending upon the direct relation

with the costs occurred for deriving a particular items of income. Usually, it is regarded as the

matching of revenues with the costs and involves simultaneous reporting of the liabilities or

reducing the assets (Cajaiba-Santana 2014). Expenses such as finance costs are recognized

during the year in which they are occurred.

Equity:

The ordinary shares of Brambles Ltd are classified under the contributed equity. The

company does not recognize the profit and loss on the purchase, sales, issues or cancellations

of equity that is owned by Brambles Ltd equity instruments. The incremental costs are

directly attributed to the issue of new shares or options is represented in the equity as the

deduction from the proceeds of issue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.