Comprehensive Auditing Report: Brambles Limited Financial Analysis

VerifiedAdded on 2020/12/09

|10

|2337

|54

Report

AI Summary

This auditing report provides an in-depth analysis of Brambles Limited's financial performance and operational risks. The report begins with an executive summary outlining the company's operational framework and then delves into the risk of material misstatement at both the financial and assertion levels. It examines the integrity of management, management's experience and knowledge, unusual pressures on management, and the nature of the business. The report also analyzes key financial ratios, including operating cash flow, current ratio, and debt-to-equity, assessing their impact on the risk of material misstatement. The report concludes with recommendations for improving investing activities and mitigating identified risks. The report references several academic sources and online resources to support its analysis. This report is designed to provide a comprehensive understanding of Brambles Limited's financial health and the associated auditing considerations.

AUDITING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................1

PART 2............................................................................................................................................1

Risk of material misstatement at financial levels...................................................................1

PART 3............................................................................................................................................3

Risk of material misstatement at Assertion level...................................................................3

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

EXECUTIVE SUMMARY.............................................................................................................1

PART 2............................................................................................................................................1

Risk of material misstatement at financial levels...................................................................1

PART 3............................................................................................................................................3

Risk of material misstatement at Assertion level...................................................................3

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

EXECUTIVE SUMMARY

A firm is consisting of various operational aspects which will be useful for managing the

activities as well as making appropriate analysis on transactions made in a year. In the present

report, there will be discussions based on operational frameworks of Brambles Limited which

deals in supply logistic group which are specialized in pooling of unit-load equipment. However,

there will be consideration of materiality of organisation at Financial as well as at Assertion

level. However, there will be influences of various information listed in annual report of

organisation on which determination of all factors will bring suitable development in operational

practices.

PART 2

Risk of material misstatement at financial levels

It is mainly known as material risk which can be identified in misleading in financial

statements. Thus, these are risks which have been addressed by accounting professionals or

auditors with respect to have appropriate information regarding data base disclosed by an entity

He, Zeadally & Wu, (2018). Importance of such aspects mainly stated in ascertaining the risks as

well as manipulation of operations.

Integrity of management

Management of all operations as well as analysing integrity of investors in making

investment aand risks which are indulged with this are main aspects which are needed to be

addressed and administered. It will be appropriate in determining the frauds as well as analysing

bottom line signal for employees in a positive manner (Brambles Limited, 2017). It will suggest

most appropriate and acceptable behaviour which will lead firm in attaining success Sookhak &

et.al., (2017). Thus, in relation with analysing operational performance of Brambles Limited, the

company is highly committed in relation with disclosing clear and transparent information

regrading financial health of business.

Management experience, changes and knowledge within a period

In terms of analysing the managerial experiences which determines that there will be

determination of adequate information and operational management in supply chain as well as

retail management Shen & et.al., (2017). Thus, Brambles Limited has been focusing on various

operations and have several planned projects based on improving operational activities and

strengthening the network. Professionals have been approached towards enhancing platform for

1

A firm is consisting of various operational aspects which will be useful for managing the

activities as well as making appropriate analysis on transactions made in a year. In the present

report, there will be discussions based on operational frameworks of Brambles Limited which

deals in supply logistic group which are specialized in pooling of unit-load equipment. However,

there will be consideration of materiality of organisation at Financial as well as at Assertion

level. However, there will be influences of various information listed in annual report of

organisation on which determination of all factors will bring suitable development in operational

practices.

PART 2

Risk of material misstatement at financial levels

It is mainly known as material risk which can be identified in misleading in financial

statements. Thus, these are risks which have been addressed by accounting professionals or

auditors with respect to have appropriate information regarding data base disclosed by an entity

He, Zeadally & Wu, (2018). Importance of such aspects mainly stated in ascertaining the risks as

well as manipulation of operations.

Integrity of management

Management of all operations as well as analysing integrity of investors in making

investment aand risks which are indulged with this are main aspects which are needed to be

addressed and administered. It will be appropriate in determining the frauds as well as analysing

bottom line signal for employees in a positive manner (Brambles Limited, 2017). It will suggest

most appropriate and acceptable behaviour which will lead firm in attaining success Sookhak &

et.al., (2017). Thus, in relation with analysing operational performance of Brambles Limited, the

company is highly committed in relation with disclosing clear and transparent information

regrading financial health of business.

Management experience, changes and knowledge within a period

In terms of analysing the managerial experiences which determines that there will be

determination of adequate information and operational management in supply chain as well as

retail management Shen & et.al., (2017). Thus, Brambles Limited has been focusing on various

operations and have several planned projects based on improving operational activities and

strengthening the network. Professionals have been approached towards enhancing platform for

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

better quality as well as differentiating value which enhances service offerings. As per

considering group wise offerings business has been approached towards improving operational

efficiency. Executing adequate allocation of capital in each activity which comprised on

increasing the cash flows in industry Simeon, (2018). Tend to have adequate innovations and

operational development which will be helpful in leading firm on right locations Hamza & Al

Hussein, (2018). Along with this, as per considering social responsibilities of the organisation on

which operational increment has been based on long term value creation and appropriate

dividend policy as well as payments.

Unusual pressure on management

As per analysing operational framework and the activities which have been performed

by Brambles Limited which is relevant with improving logistic supplies in organisation Demb &

et.al., (2017). Therefore, management of all operations will be adequate in meeting the goals at

right time as well as managing financial needs of business. It is associated with disclosure of

fruitful information and analysing the requirements of firm in meeting target capital. In analysing

the inherent risk in accounting for pooling equipment there has been comparatively higher

volume of assets which creates obstacles and makes adequate increment in professional’s

practices.

Nature of business in entity

The business has been engaged in operating activities relevant with estimation of

professionals in industry. Brambles Limited has been operating in supplying logistics and pooled

equipment Alles & et.al., (2018). Thus, the operational criteria and activities will be adequate in

meeting stability for capital generation. Motive of every industry is based on improving

operational criteria and lead the unit in retaining higher consumer backups Groomer & Murthy,

(2018).

Factors influence operations in industry

There can be various factors or elements which influences operational viabilities and

activities of firm. Considering the operating functions of Brambles Limited which insists that

there are various areas on which business performs Chan & Vasarhelyi, (2018). There can be

influences due to improper allocation of capital, sudden changes in company’s policies, reforms

in economic plans and governmental changes in taxation. Thus, these can affect operations of the

2

considering group wise offerings business has been approached towards improving operational

efficiency. Executing adequate allocation of capital in each activity which comprised on

increasing the cash flows in industry Simeon, (2018). Tend to have adequate innovations and

operational development which will be helpful in leading firm on right locations Hamza & Al

Hussein, (2018). Along with this, as per considering social responsibilities of the organisation on

which operational increment has been based on long term value creation and appropriate

dividend policy as well as payments.

Unusual pressure on management

As per analysing operational framework and the activities which have been performed

by Brambles Limited which is relevant with improving logistic supplies in organisation Demb &

et.al., (2017). Therefore, management of all operations will be adequate in meeting the goals at

right time as well as managing financial needs of business. It is associated with disclosure of

fruitful information and analysing the requirements of firm in meeting target capital. In analysing

the inherent risk in accounting for pooling equipment there has been comparatively higher

volume of assets which creates obstacles and makes adequate increment in professional’s

practices.

Nature of business in entity

The business has been engaged in operating activities relevant with estimation of

professionals in industry. Brambles Limited has been operating in supplying logistics and pooled

equipment Alles & et.al., (2018). Thus, the operational criteria and activities will be adequate in

meeting stability for capital generation. Motive of every industry is based on improving

operational criteria and lead the unit in retaining higher consumer backups Groomer & Murthy,

(2018).

Factors influence operations in industry

There can be various factors or elements which influences operational viabilities and

activities of firm. Considering the operating functions of Brambles Limited which insists that

there are various areas on which business performs Chan & Vasarhelyi, (2018). There can be

influences due to improper allocation of capital, sudden changes in company’s policies, reforms

in economic plans and governmental changes in taxation. Thus, these can affect operations of the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business in performing adequately. Along with this, there can be various duties and

responsibilities of auditors in respect with financial reporting of organisation.

Main motive of professionals is for disclosing the authentic and reliable information among

stakeholders which will assist them in investment decisions. Reports are needed to be prepared

with considering all transactions made in a year. It will be based on valid details and considering

all legal invoices Reiman & Viitanen, (2017). It helps in reducing chances of fraud and unlawful

activities in firm. Thus, as per analysing operational limitations of professionals there will be

sound increment and development of various policies which will lead the organisation in

attaining targeted goals. Accountants will be bound for controlling errors and misleading

information regarding operational activities performed by the professionals in due course of

action.

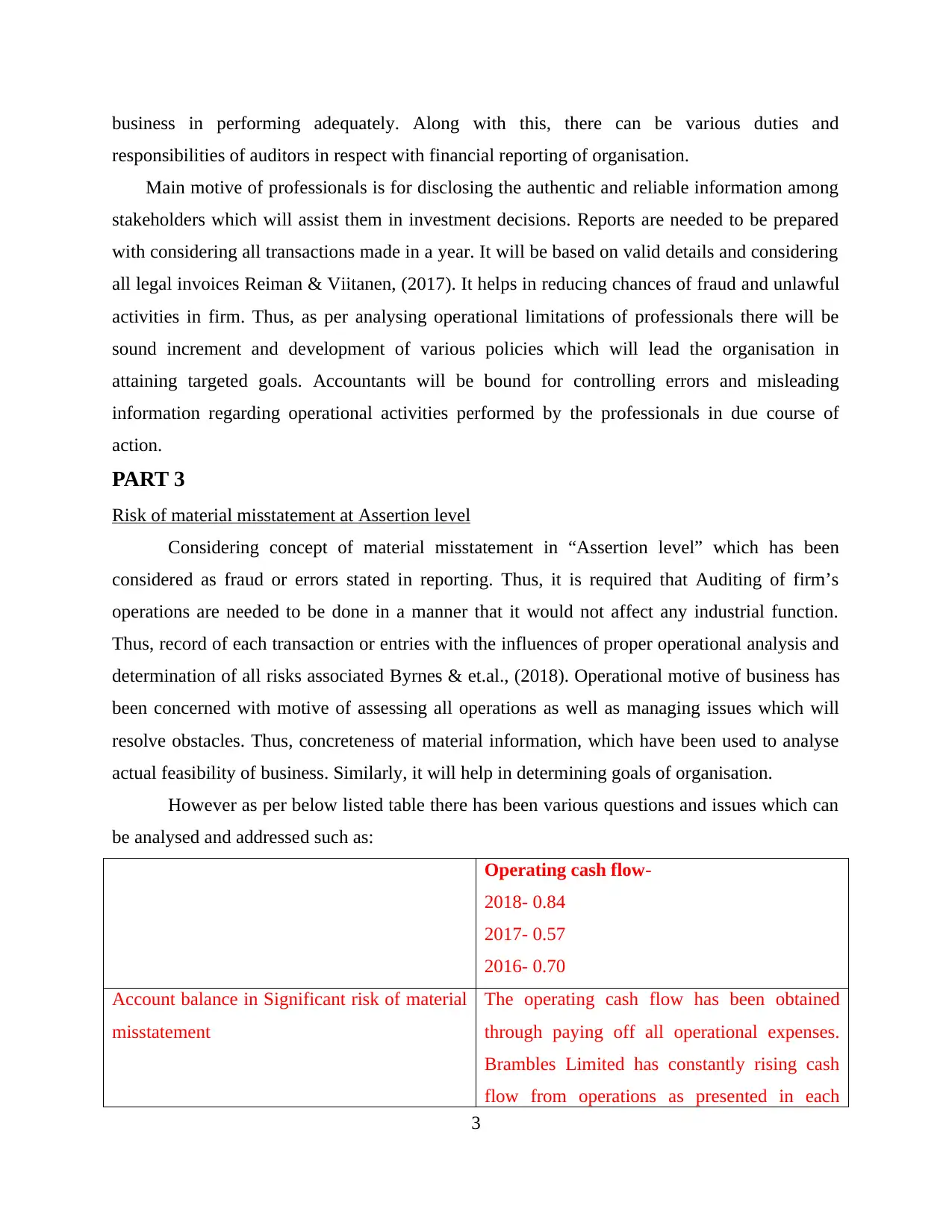

PART 3

Risk of material misstatement at Assertion level

Considering concept of material misstatement in “Assertion level” which has been

considered as fraud or errors stated in reporting. Thus, it is required that Auditing of firm’s

operations are needed to be done in a manner that it would not affect any industrial function.

Thus, record of each transaction or entries with the influences of proper operational analysis and

determination of all risks associated Byrnes & et.al., (2018). Operational motive of business has

been concerned with motive of assessing all operations as well as managing issues which will

resolve obstacles. Thus, concreteness of material information, which have been used to analyse

actual feasibility of business. Similarly, it will help in determining goals of organisation.

However as per below listed table there has been various questions and issues which can

be analysed and addressed such as:

Operating cash flow-

2018- 0.84

2017- 0.57

2016- 0.70

Account balance in Significant risk of material

misstatement

The operating cash flow has been obtained

through paying off all operational expenses.

Brambles Limited has constantly rising cash

flow from operations as presented in each

3

responsibilities of auditors in respect with financial reporting of organisation.

Main motive of professionals is for disclosing the authentic and reliable information among

stakeholders which will assist them in investment decisions. Reports are needed to be prepared

with considering all transactions made in a year. It will be based on valid details and considering

all legal invoices Reiman & Viitanen, (2017). It helps in reducing chances of fraud and unlawful

activities in firm. Thus, as per analysing operational limitations of professionals there will be

sound increment and development of various policies which will lead the organisation in

attaining targeted goals. Accountants will be bound for controlling errors and misleading

information regarding operational activities performed by the professionals in due course of

action.

PART 3

Risk of material misstatement at Assertion level

Considering concept of material misstatement in “Assertion level” which has been

considered as fraud or errors stated in reporting. Thus, it is required that Auditing of firm’s

operations are needed to be done in a manner that it would not affect any industrial function.

Thus, record of each transaction or entries with the influences of proper operational analysis and

determination of all risks associated Byrnes & et.al., (2018). Operational motive of business has

been concerned with motive of assessing all operations as well as managing issues which will

resolve obstacles. Thus, concreteness of material information, which have been used to analyse

actual feasibility of business. Similarly, it will help in determining goals of organisation.

However as per below listed table there has been various questions and issues which can

be analysed and addressed such as:

Operating cash flow-

2018- 0.84

2017- 0.57

2016- 0.70

Account balance in Significant risk of material

misstatement

The operating cash flow has been obtained

through paying off all operational expenses.

Brambles Limited has constantly rising cash

flow from operations as presented in each

3

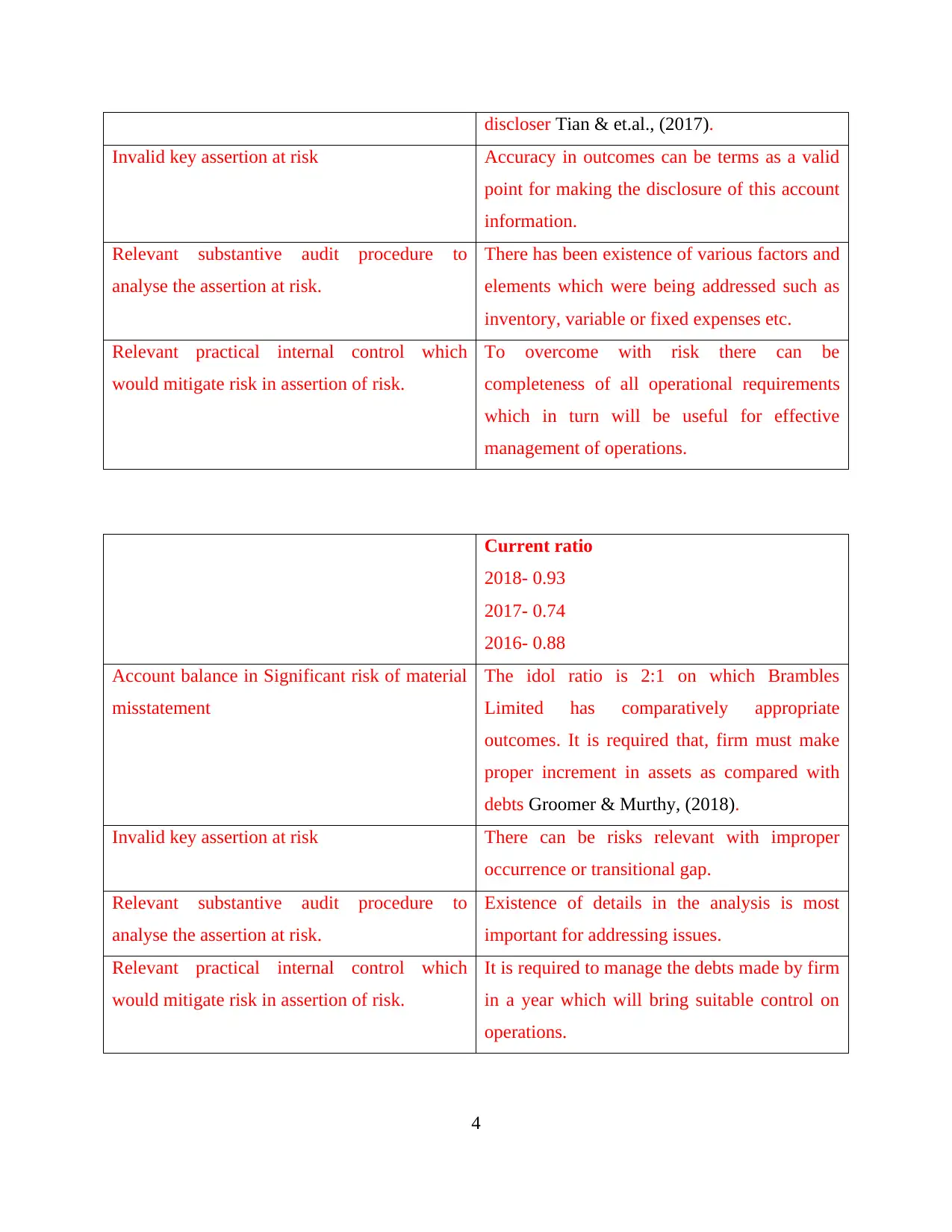

discloser Tian & et.al., (2017).

Invalid key assertion at risk Accuracy in outcomes can be terms as a valid

point for making the disclosure of this account

information.

Relevant substantive audit procedure to

analyse the assertion at risk.

There has been existence of various factors and

elements which were being addressed such as

inventory, variable or fixed expenses etc.

Relevant practical internal control which

would mitigate risk in assertion of risk.

To overcome with risk there can be

completeness of all operational requirements

which in turn will be useful for effective

management of operations.

Current ratio

2018- 0.93

2017- 0.74

2016- 0.88

Account balance in Significant risk of material

misstatement

The idol ratio is 2:1 on which Brambles

Limited has comparatively appropriate

outcomes. It is required that, firm must make

proper increment in assets as compared with

debts Groomer & Murthy, (2018).

Invalid key assertion at risk There can be risks relevant with improper

occurrence or transitional gap.

Relevant substantive audit procedure to

analyse the assertion at risk.

Existence of details in the analysis is most

important for addressing issues.

Relevant practical internal control which

would mitigate risk in assertion of risk.

It is required to manage the debts made by firm

in a year which will bring suitable control on

operations.

4

Invalid key assertion at risk Accuracy in outcomes can be terms as a valid

point for making the disclosure of this account

information.

Relevant substantive audit procedure to

analyse the assertion at risk.

There has been existence of various factors and

elements which were being addressed such as

inventory, variable or fixed expenses etc.

Relevant practical internal control which

would mitigate risk in assertion of risk.

To overcome with risk there can be

completeness of all operational requirements

which in turn will be useful for effective

management of operations.

Current ratio

2018- 0.93

2017- 0.74

2016- 0.88

Account balance in Significant risk of material

misstatement

The idol ratio is 2:1 on which Brambles

Limited has comparatively appropriate

outcomes. It is required that, firm must make

proper increment in assets as compared with

debts Groomer & Murthy, (2018).

Invalid key assertion at risk There can be risks relevant with improper

occurrence or transitional gap.

Relevant substantive audit procedure to

analyse the assertion at risk.

Existence of details in the analysis is most

important for addressing issues.

Relevant practical internal control which

would mitigate risk in assertion of risk.

It is required to manage the debts made by firm

in a year which will bring suitable control on

operations.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

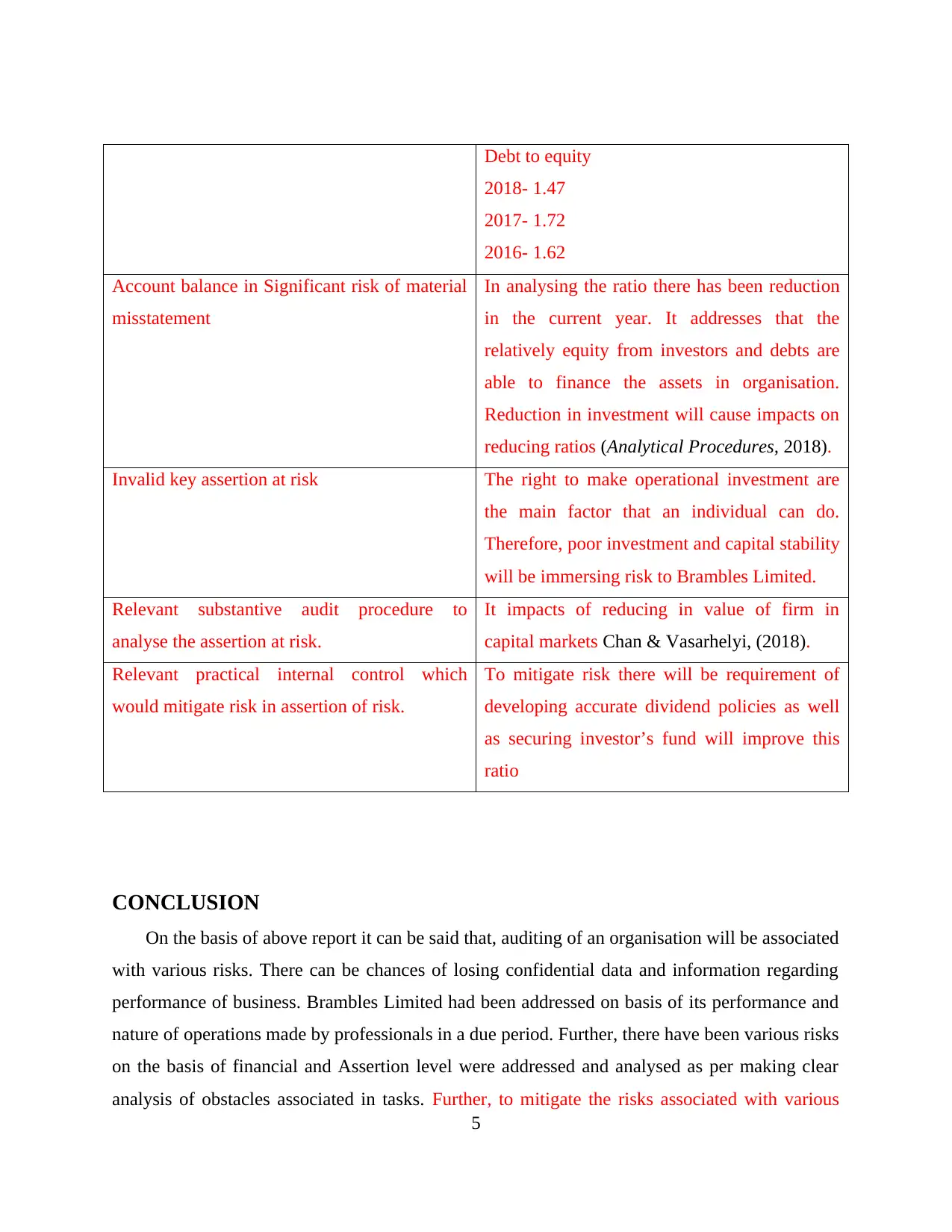

Debt to equity

2018- 1.47

2017- 1.72

2016- 1.62

Account balance in Significant risk of material

misstatement

In analysing the ratio there has been reduction

in the current year. It addresses that the

relatively equity from investors and debts are

able to finance the assets in organisation.

Reduction in investment will cause impacts on

reducing ratios (Analytical Procedures, 2018).

Invalid key assertion at risk The right to make operational investment are

the main factor that an individual can do.

Therefore, poor investment and capital stability

will be immersing risk to Brambles Limited.

Relevant substantive audit procedure to

analyse the assertion at risk.

It impacts of reducing in value of firm in

capital markets Chan & Vasarhelyi, (2018).

Relevant practical internal control which

would mitigate risk in assertion of risk.

To mitigate risk there will be requirement of

developing accurate dividend policies as well

as securing investor’s fund will improve this

ratio

CONCLUSION

On the basis of above report it can be said that, auditing of an organisation will be associated

with various risks. There can be chances of losing confidential data and information regarding

performance of business. Brambles Limited had been addressed on basis of its performance and

nature of operations made by professionals in a due period. Further, there have been various risks

on the basis of financial and Assertion level were addressed and analysed as per making clear

analysis of obstacles associated in tasks. Further, to mitigate the risks associated with various

5

2018- 1.47

2017- 1.72

2016- 1.62

Account balance in Significant risk of material

misstatement

In analysing the ratio there has been reduction

in the current year. It addresses that the

relatively equity from investors and debts are

able to finance the assets in organisation.

Reduction in investment will cause impacts on

reducing ratios (Analytical Procedures, 2018).

Invalid key assertion at risk The right to make operational investment are

the main factor that an individual can do.

Therefore, poor investment and capital stability

will be immersing risk to Brambles Limited.

Relevant substantive audit procedure to

analyse the assertion at risk.

It impacts of reducing in value of firm in

capital markets Chan & Vasarhelyi, (2018).

Relevant practical internal control which

would mitigate risk in assertion of risk.

To mitigate risk there will be requirement of

developing accurate dividend policies as well

as securing investor’s fund will improve this

ratio

CONCLUSION

On the basis of above report it can be said that, auditing of an organisation will be associated

with various risks. There can be chances of losing confidential data and information regarding

performance of business. Brambles Limited had been addressed on basis of its performance and

nature of operations made by professionals in a due period. Further, there have been various risks

on the basis of financial and Assertion level were addressed and analysed as per making clear

analysis of obstacles associated in tasks. Further, to mitigate the risks associated with various

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounts has been addressed here such as operating cash flow, debt to equity and current ratios.

Therefore, it indicates rise in the ratio or balance of each accounts in the current year instead of

debt to equity. In addition, Professionals has been suggested for making necessary improvements

in investing activities.

6

Therefore, it indicates rise in the ratio or balance of each accounts in the current year instead of

debt to equity. In addition, Professionals has been suggested for making necessary improvements

in investing activities.

6

REFERENCES

Books and Journals

Alles, M. & et.al., (2018). Continuous monitoring of business process controls: A pilot

implementation of a continuous auditing system at Siemens. In Continuous Auditing:

Theory and Application (pp. 219-246). Emerald Publishing Limited.

Byrnes, A. & et.al., (2018). Enhanced Recovery After Surgery as an auditing framework for

identifying improvements to perioperative nutrition care of older surgical

patients. European journal of clinical nutrition. 72(6). 913.

Chan, D. Y., & Vasarhelyi, M. A. (2018). Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing

Limited.

Demb, J. & et.al., (2017). Optimizing radiation doses for computed tomography across

institutions: dose auditing and best practices. JAMA internal medicine. 177(6). 810-817.

Groomer, S. M., & Murthy, U. S. (2018). Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application(pp.

105-124). Emerald Publishing Limited.

Hamza, A., & Al Hussein, F. (2018). Auditing the prevalence and effects of smoking to lead a

successful smoking cessation campaign. Auditing. 7(1). 39-43.

He, D., Zeadally, S., & Wu, L. (2018). Certificateless public auditing scheme for cloud-assisted

wireless body area networks. IEEE Systems Journal. 12(1). 64-73.

Reiman, T., & Viitanen, K. (2017). Safety culture assurance by auditing in a nuclear power plant

construction project. In 9th International Conference on the Prevention of Accidents at

Work, WOS 2017 (pp. 161-170). CRC Press.

Shen, J. & et.al., (2017). An efficient public auditing protocol with novel dynamic structure for

cloud data. IEEE Transactions on Information Forensics and Security. 12(10). 2402-

2415.

Simeon, E. D. S. E. I. (2018). Auditing and Fraud Control in Corporate

Organisations. Auditing. 9(8).

Sookhak, M. & et.al., (2017). Dynamic remote data auditing for securing big data storage in

cloud computing. Information Sciences. 380. 101-116.

Tian, H. & et.al., (2017). Dynamic-hash-table based public auditing for secure cloud

storage. IEEE Transactions on Services Computing. 10(5). 701-714.

Online

7

Books and Journals

Alles, M. & et.al., (2018). Continuous monitoring of business process controls: A pilot

implementation of a continuous auditing system at Siemens. In Continuous Auditing:

Theory and Application (pp. 219-246). Emerald Publishing Limited.

Byrnes, A. & et.al., (2018). Enhanced Recovery After Surgery as an auditing framework for

identifying improvements to perioperative nutrition care of older surgical

patients. European journal of clinical nutrition. 72(6). 913.

Chan, D. Y., & Vasarhelyi, M. A. (2018). Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing

Limited.

Demb, J. & et.al., (2017). Optimizing radiation doses for computed tomography across

institutions: dose auditing and best practices. JAMA internal medicine. 177(6). 810-817.

Groomer, S. M., & Murthy, U. S. (2018). Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application(pp.

105-124). Emerald Publishing Limited.

Hamza, A., & Al Hussein, F. (2018). Auditing the prevalence and effects of smoking to lead a

successful smoking cessation campaign. Auditing. 7(1). 39-43.

He, D., Zeadally, S., & Wu, L. (2018). Certificateless public auditing scheme for cloud-assisted

wireless body area networks. IEEE Systems Journal. 12(1). 64-73.

Reiman, T., & Viitanen, K. (2017). Safety culture assurance by auditing in a nuclear power plant

construction project. In 9th International Conference on the Prevention of Accidents at

Work, WOS 2017 (pp. 161-170). CRC Press.

Shen, J. & et.al., (2017). An efficient public auditing protocol with novel dynamic structure for

cloud data. IEEE Transactions on Information Forensics and Security. 12(10). 2402-

2415.

Simeon, E. D. S. E. I. (2018). Auditing and Fraud Control in Corporate

Organisations. Auditing. 9(8).

Sookhak, M. & et.al., (2017). Dynamic remote data auditing for securing big data storage in

cloud computing. Information Sciences. 380. 101-116.

Tian, H. & et.al., (2017). Dynamic-hash-table based public auditing for secure cloud

storage. IEEE Transactions on Services Computing. 10(5). 701-714.

Online

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analytical Procedures. 2018. [Online]. Available through :<

https://www.accaglobal.com/in/en/student/exam-support-resources/professional-exams-

study-resources/p7/technical-articles/analytical-procedures.html >.

Brambles Limited. 2017. [Online]. Available through :<

https://www.brambles.com/Content/cms/pdf/2018/Brambles_2018_Annual_Report_WE

B_280818.pdf >.

8

https://www.accaglobal.com/in/en/student/exam-support-resources/professional-exams-

study-resources/p7/technical-articles/analytical-procedures.html >.

Brambles Limited. 2017. [Online]. Available through :<

https://www.brambles.com/Content/cms/pdf/2018/Brambles_2018_Annual_Report_WE

B_280818.pdf >.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.