Corporate Branch Control and Operations Training: Audit Review

VerifiedAdded on 2023/06/05

|36

|2661

|144

Report

AI Summary

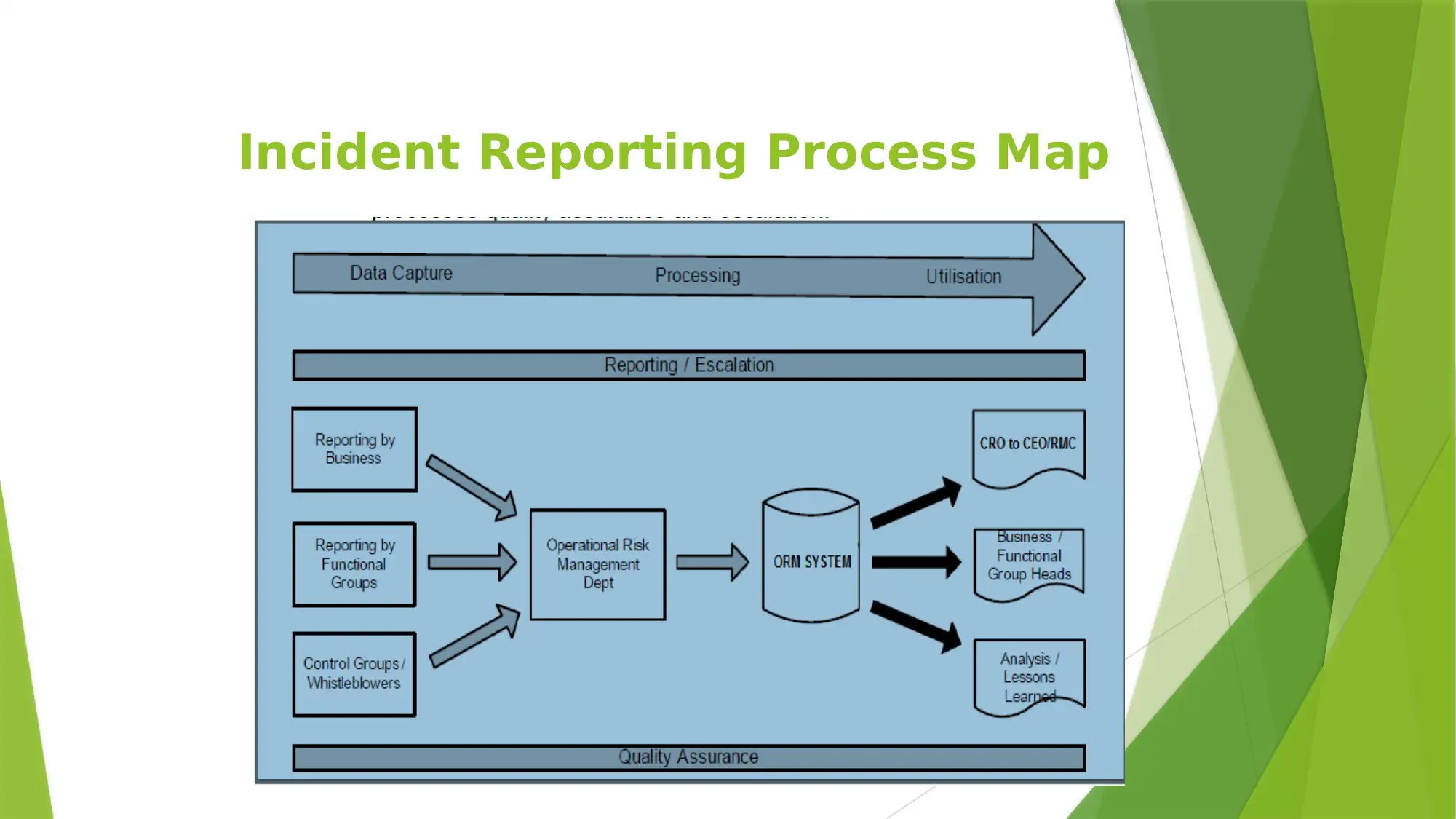

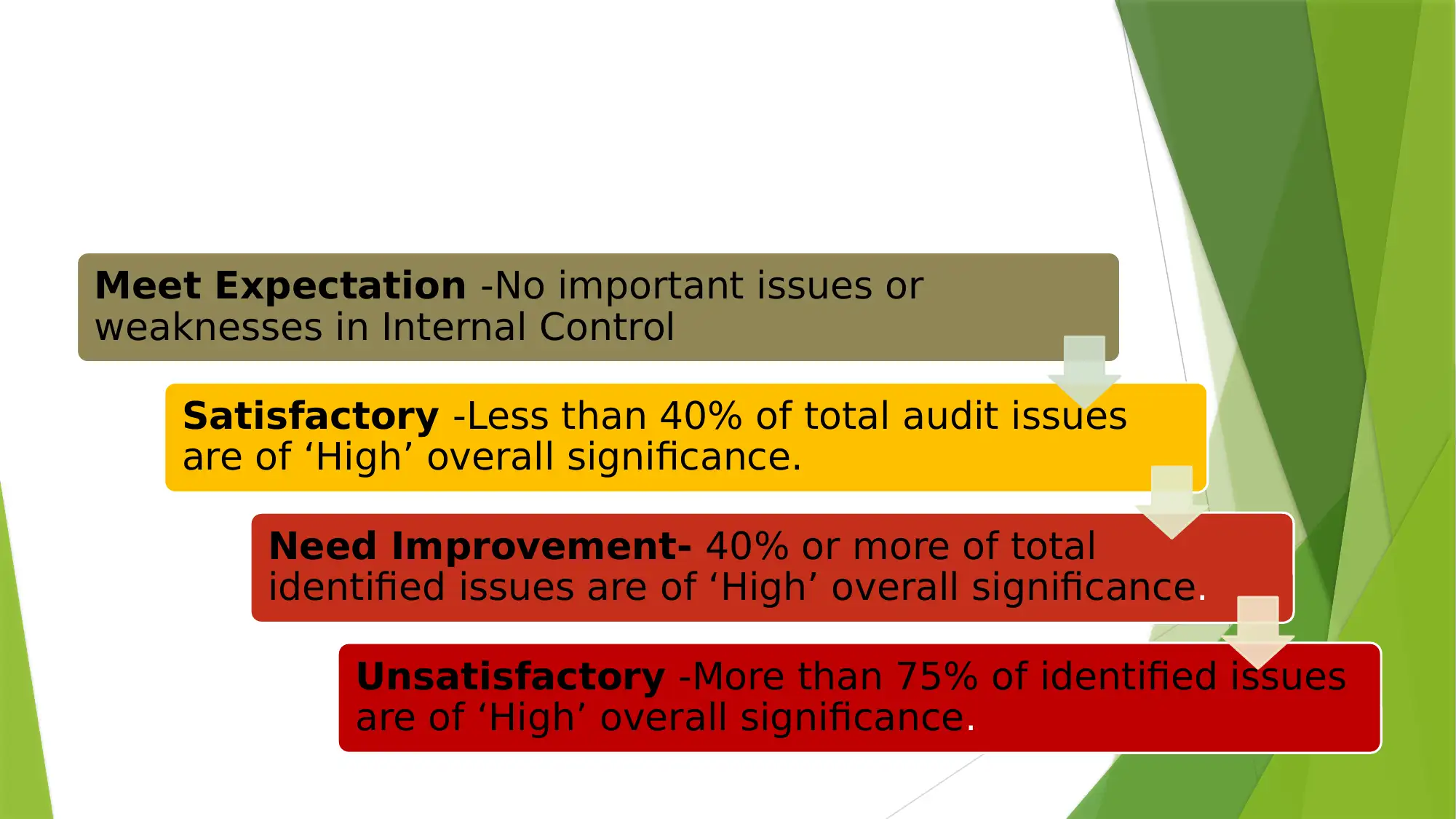

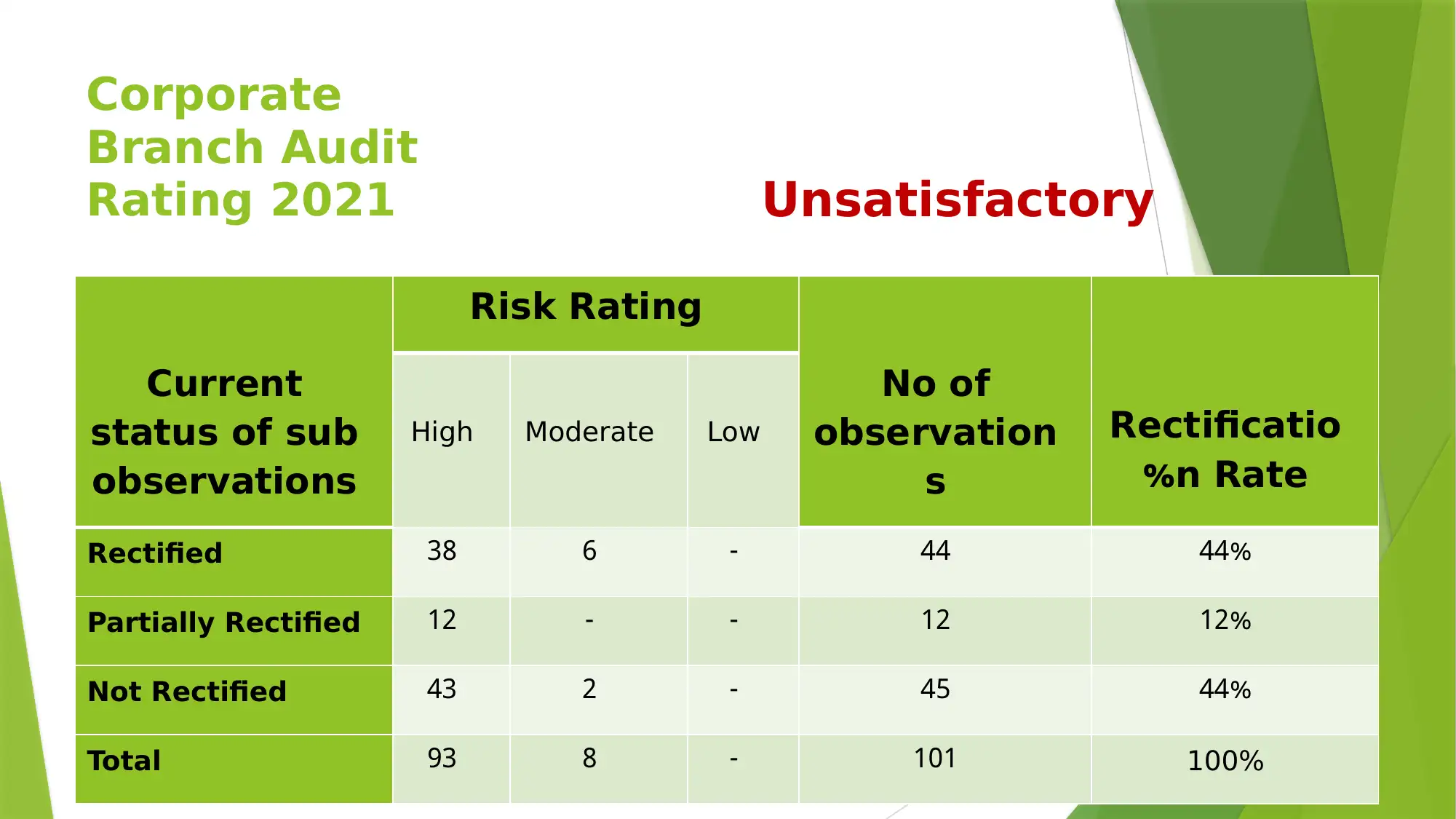

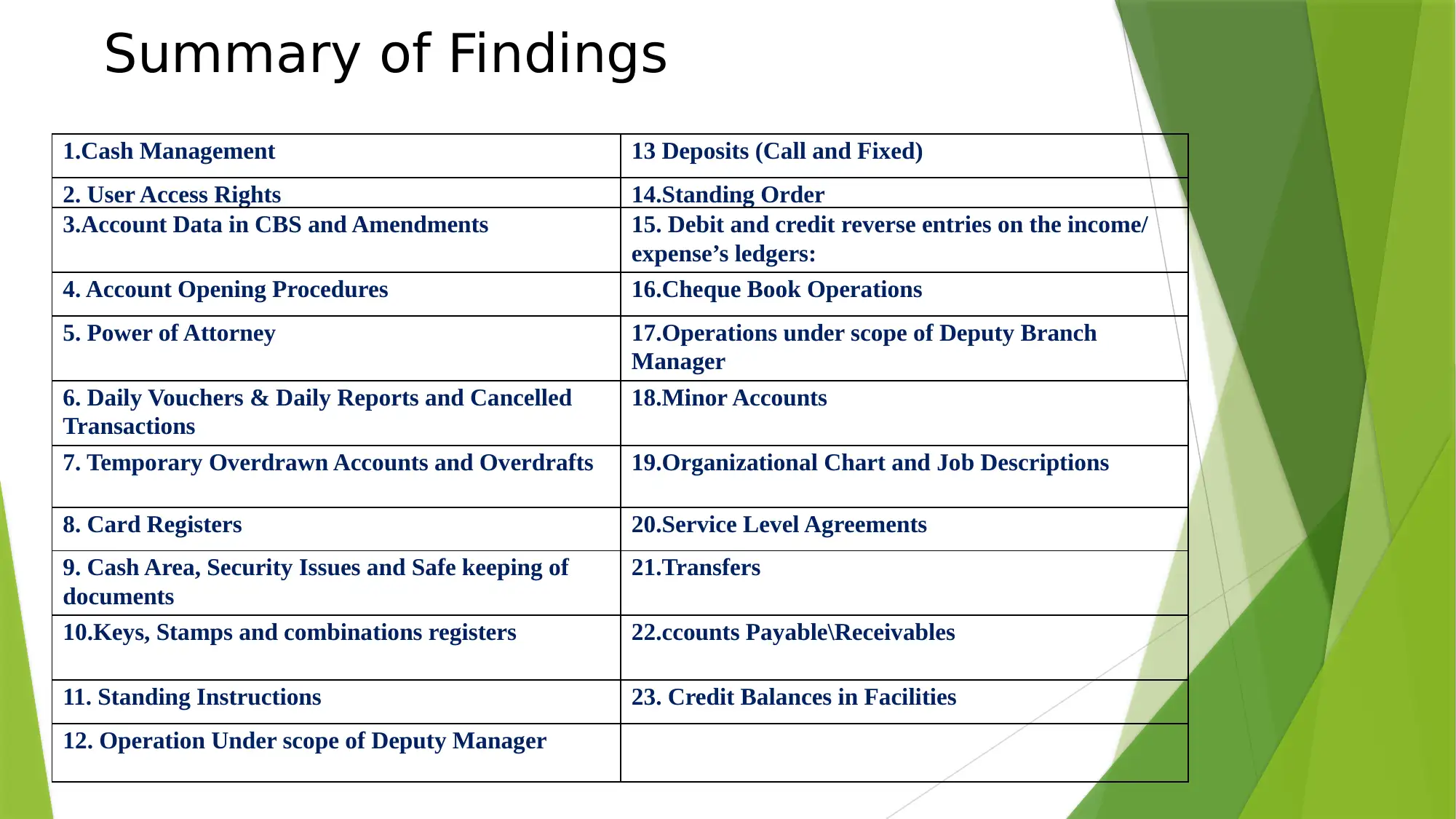

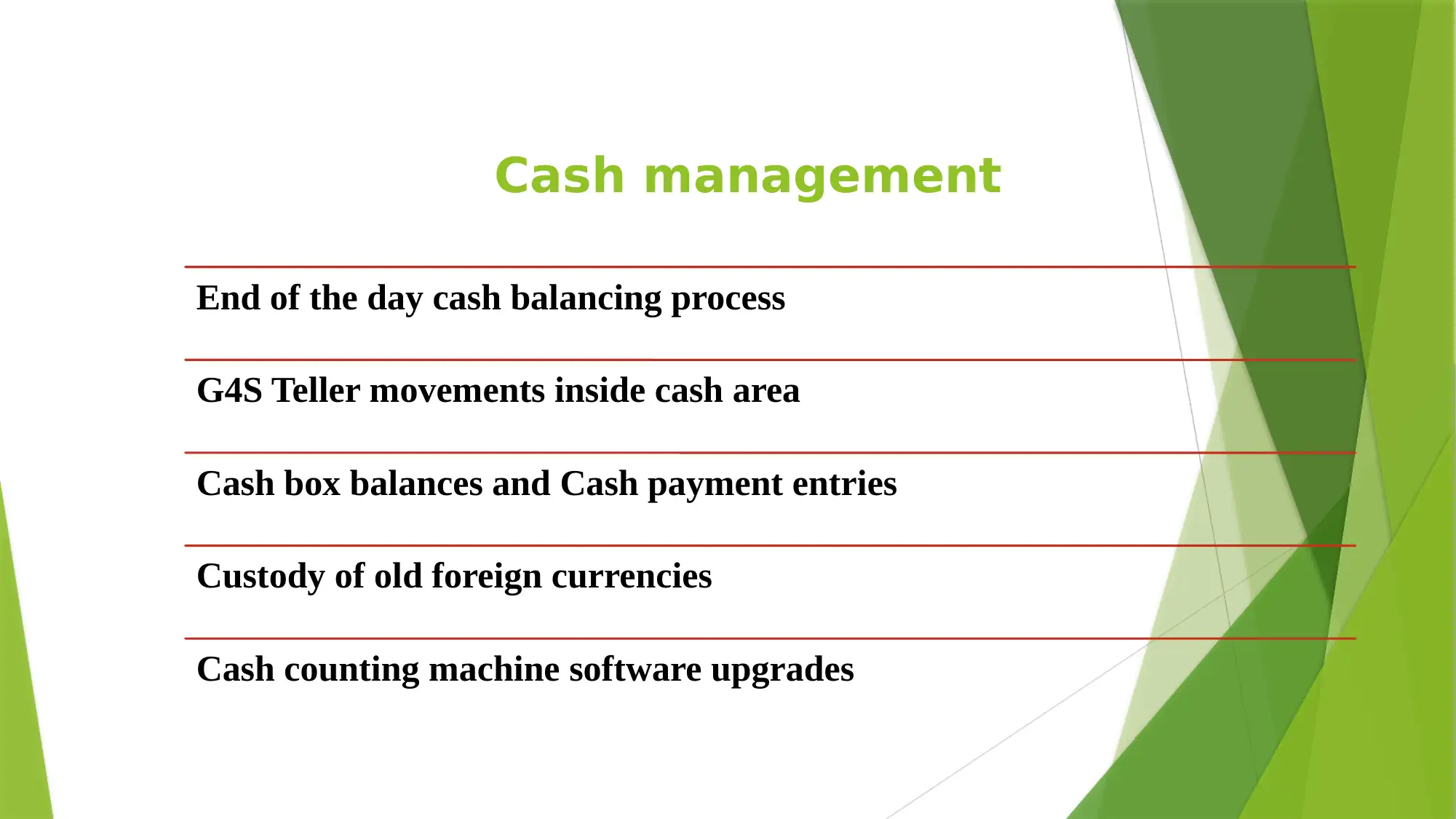

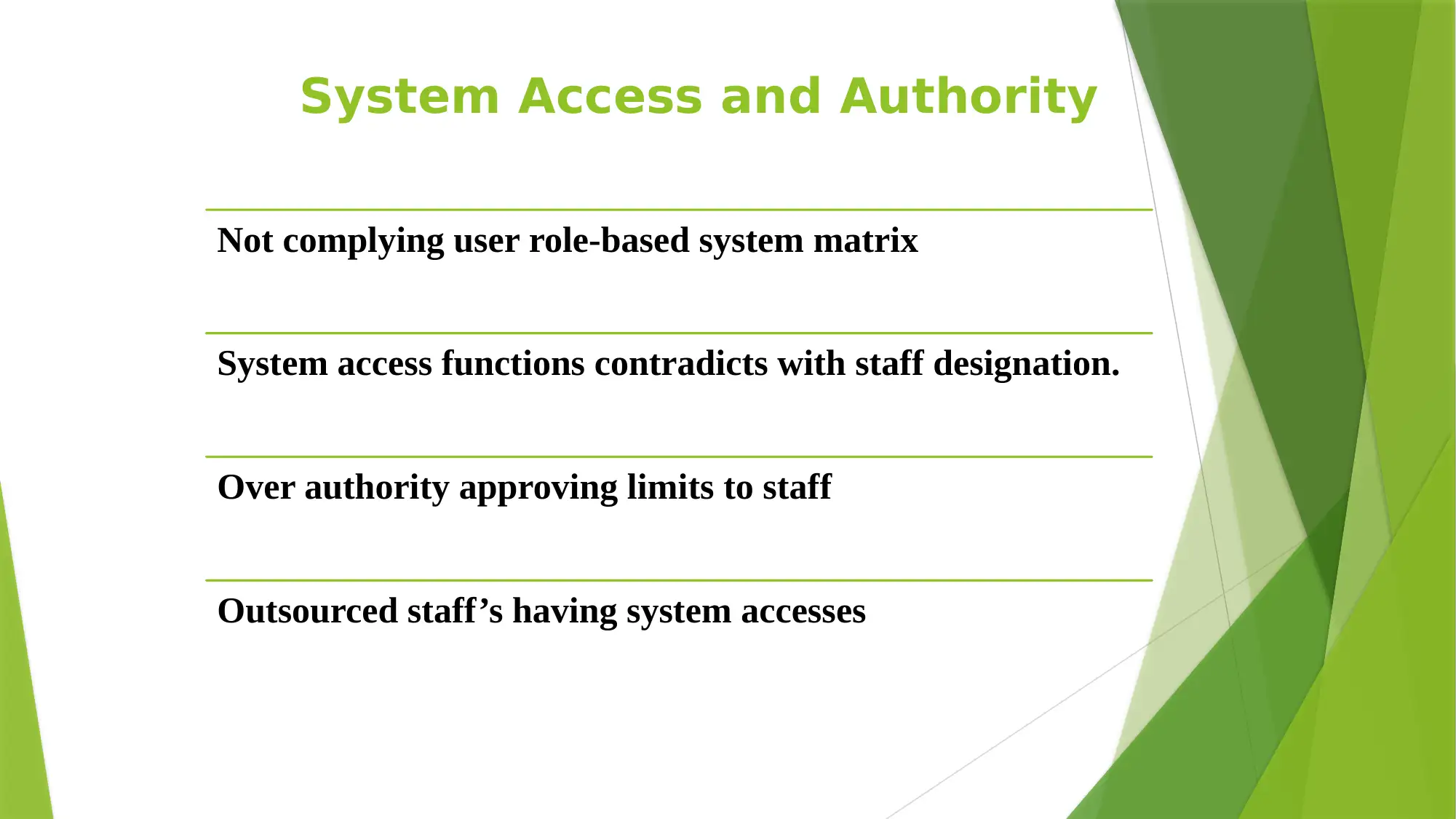

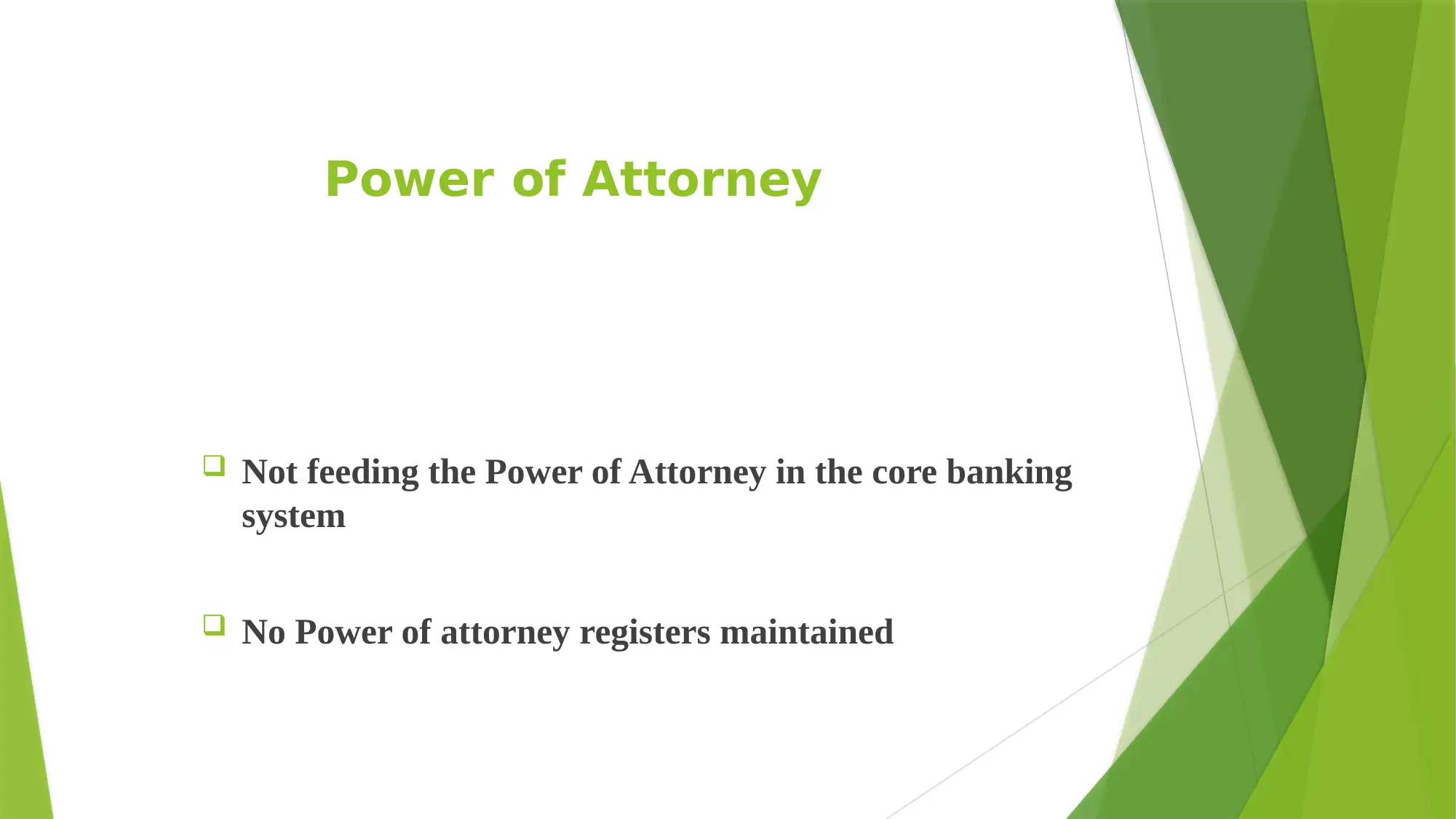

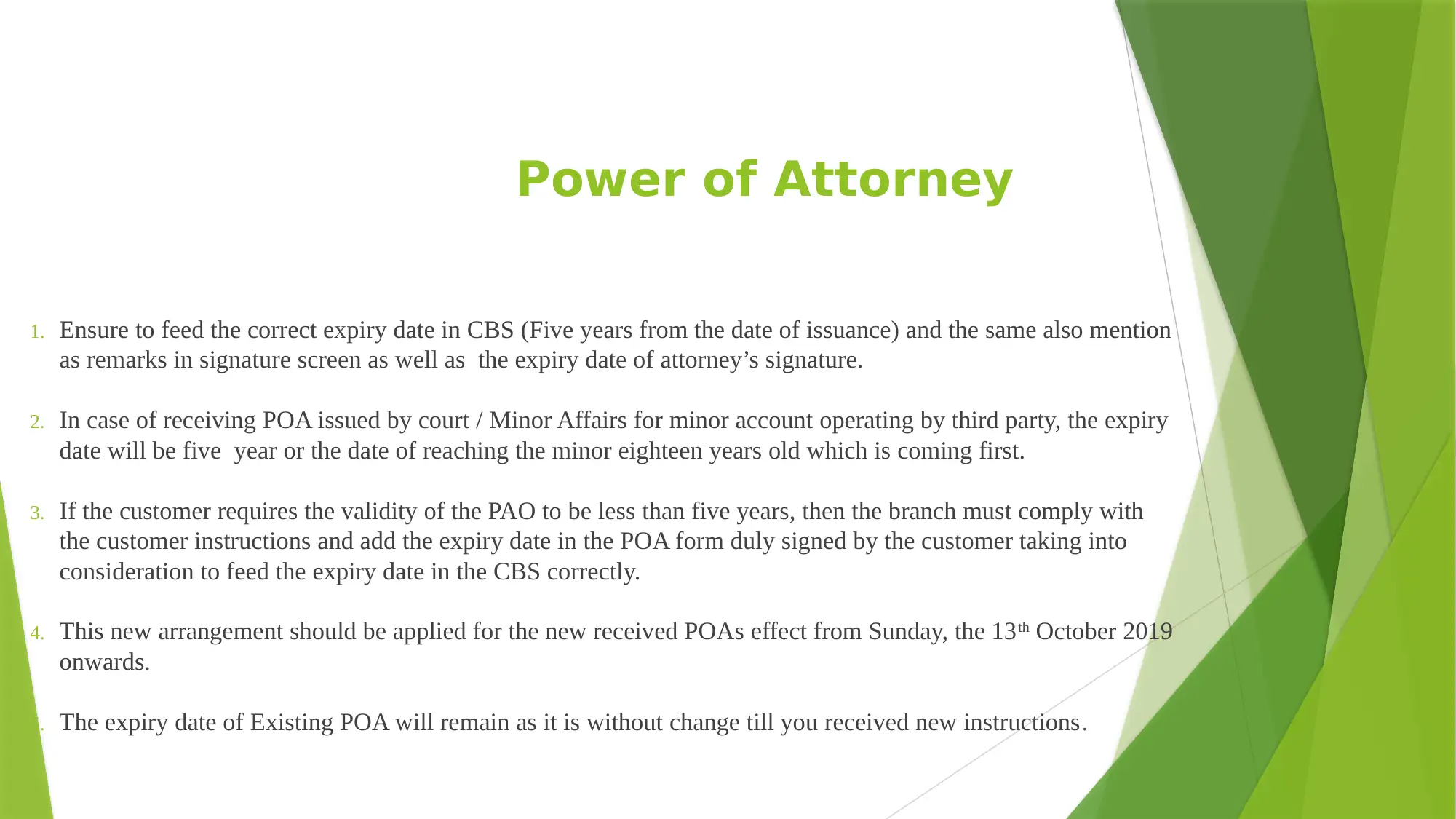

This report provides a comprehensive overview of a branch control and operations training program, focusing on the objectives, functional approach, and scope of branch control. It details the incident reporting process, including the escalation of operational and control errors. The report presents an analysis of internal audit ratings, categorizing them as Meet Expectation, Satisfactory, Need Improvement, and Unsatisfactory. A significant portion of the document is dedicated to the summary of audit findings, covering areas such as cash management, system access, power of attorney, account data, daily vouchers, cards registers, cash area security, stamps, standing instructions, manager's cheques, stop payments, income/expense ledgers, clearing and cheque book operations, organization charts, service level agreements, remittances, and account opening procedures. Each finding is detailed, highlighting non-compliance issues and providing recommendations for corrective measures. The report concludes with a summary of the importance of branch control and operations training in the banking system, emphasizing the significance of the incident reporting process, audit ratings, and adherence to policies and security protocols.

1 out of 36

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.