Report on Recommendation for Balloon Purchase: Branson Ltd Analysis

VerifiedAdded on 2021/06/14

|14

|1860

|26

Report

AI Summary

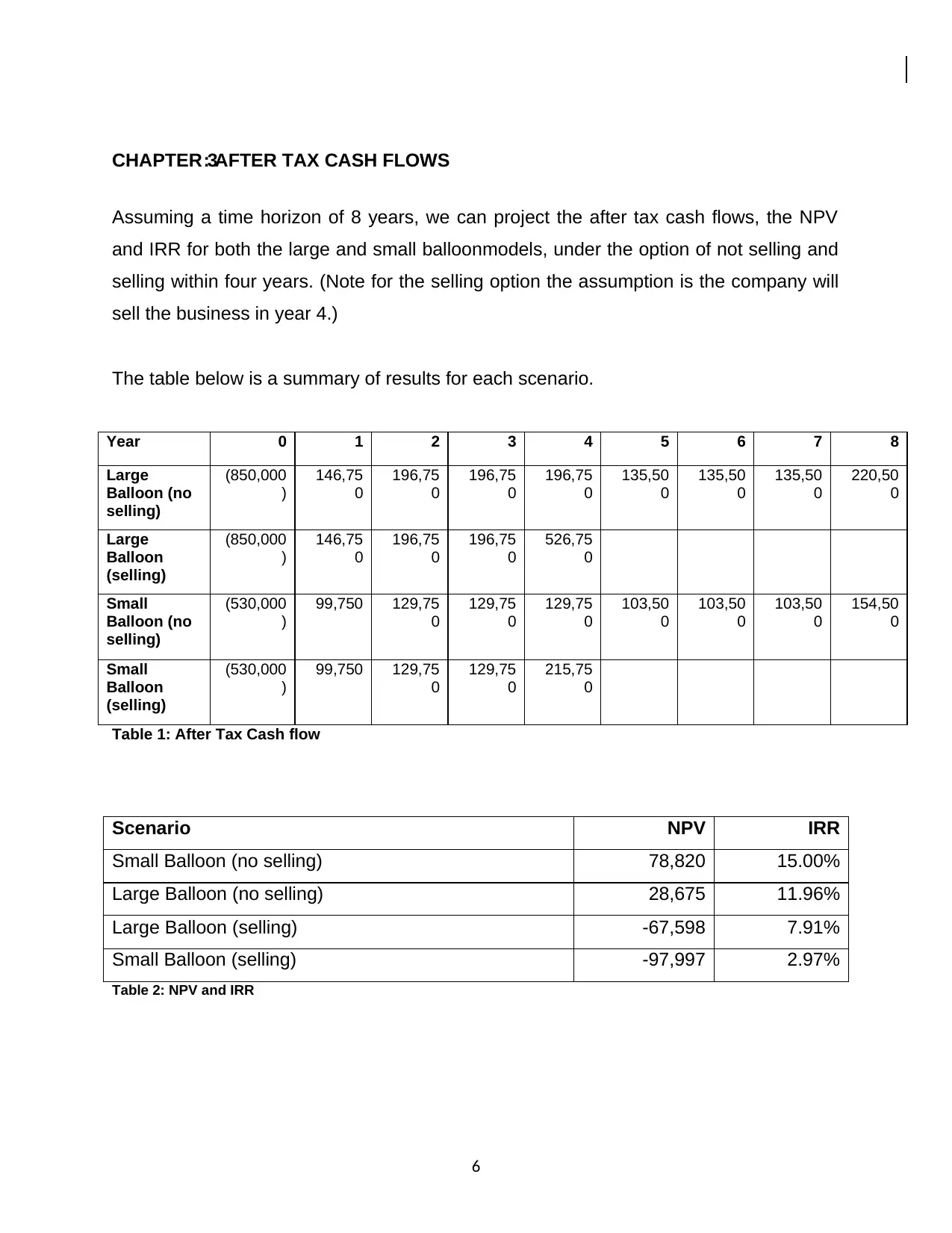

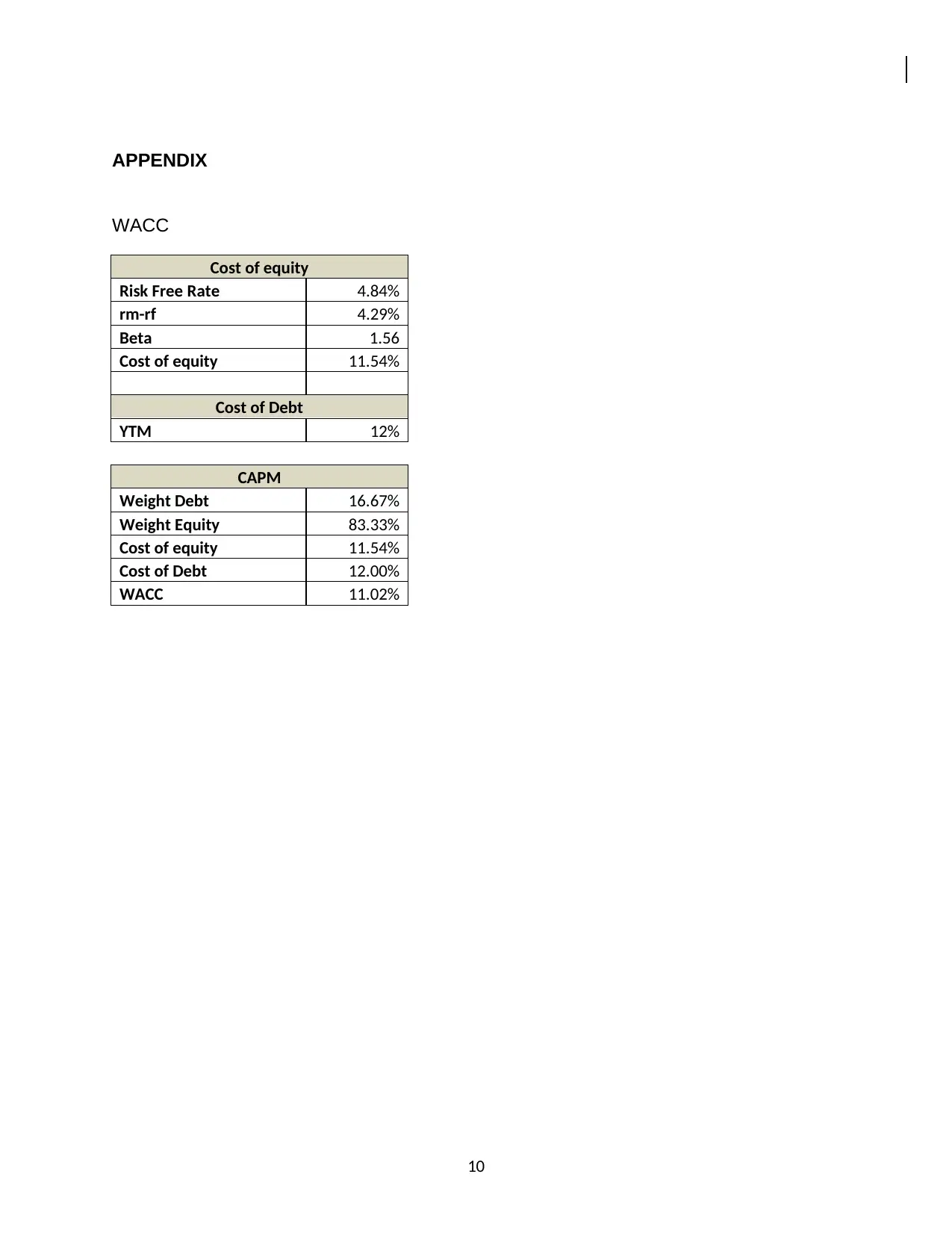

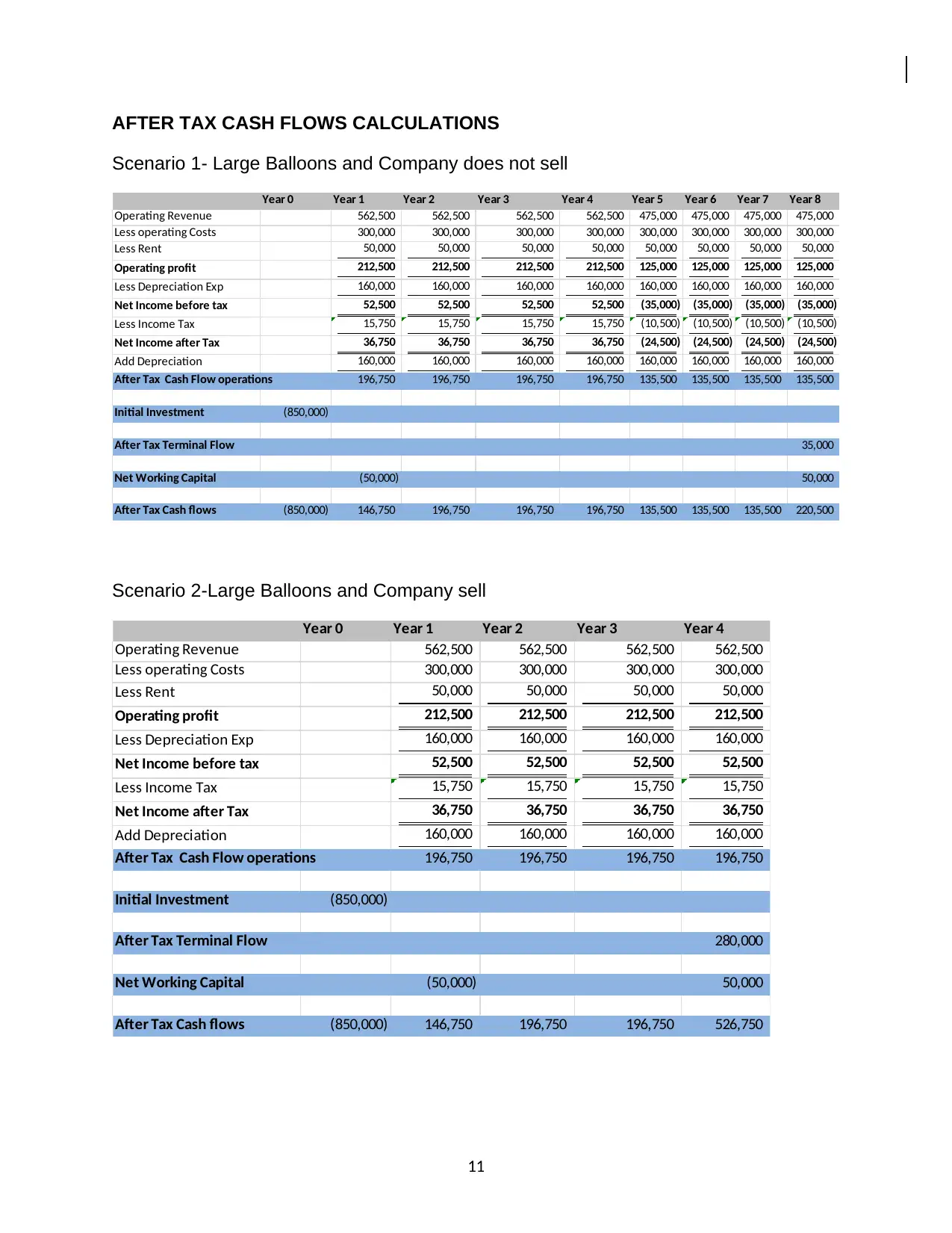

This report provides a financial analysis and recommendation for Branson Ltd regarding the purchase of new balloons. The company needs to decide whether to replace their current balloons with either a large or small model, considering the option of selling the business within four years. The analysis utilizes capital budgeting techniques, including Net Present Value (NPV) and Internal Rate of Return (IRR), to evaluate the profitability of each scenario. The report calculates the Weighted Average Cost of Capital (WACC) to determine the appropriate discount rate, considering the cost of equity and debt. The after-tax cash flows, NPV, and IRR are calculated for different scenarios: large balloons with and without selling the business, and small balloons with and without selling. Based on the financial analysis, the report recommends that Branson Ltd should not sell the business within four years and should operate the business for at least eight years, opting for the smaller balloon model due to its higher NPV and long-term profitability. The report concludes that Branson Ltd should proceed with the small balloon model for the next eight years.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.