Accounting Fundamentals: Break-Even Analysis and Management

VerifiedAdded on 2023/06/18

|7

|1286

|307

Report

AI Summary

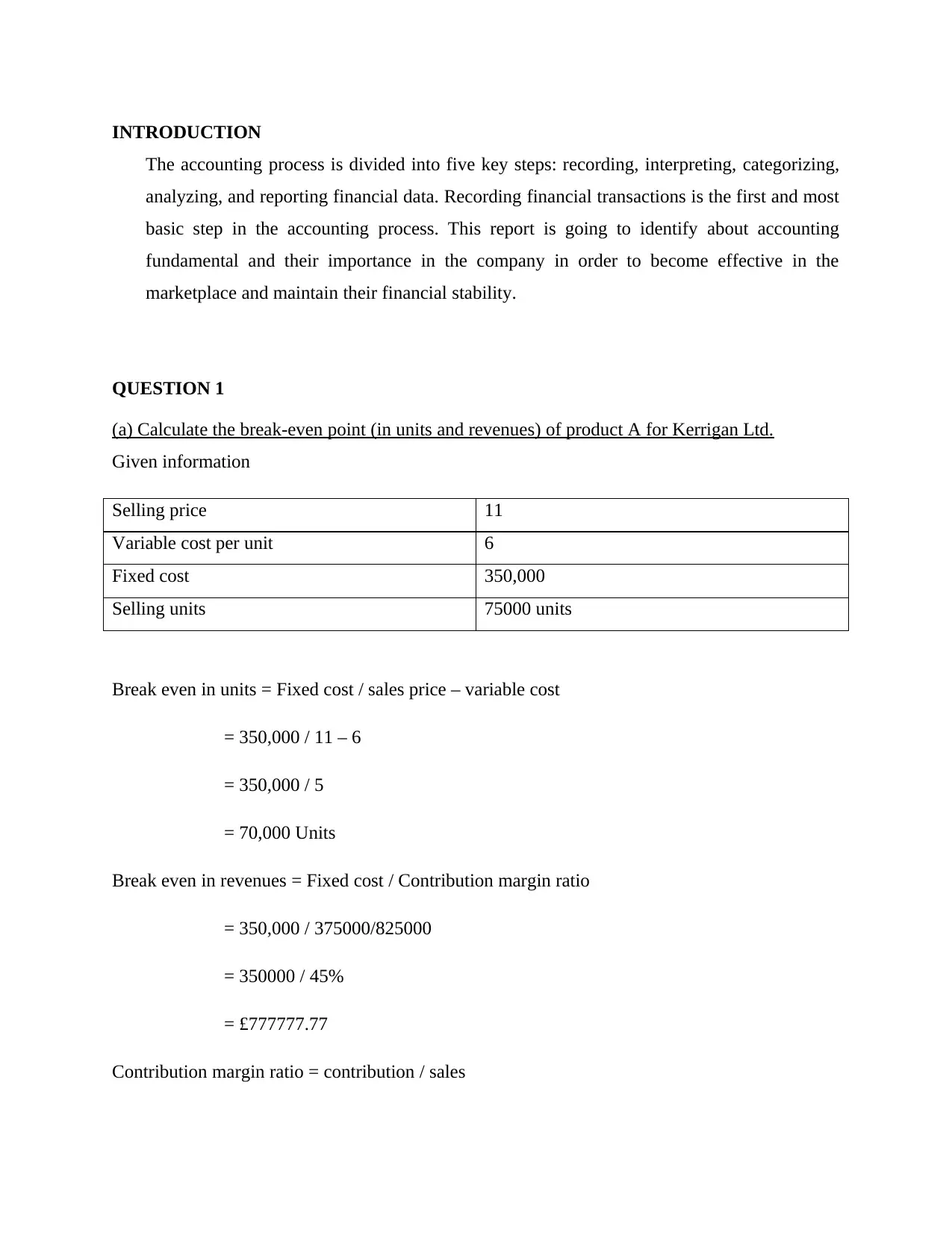

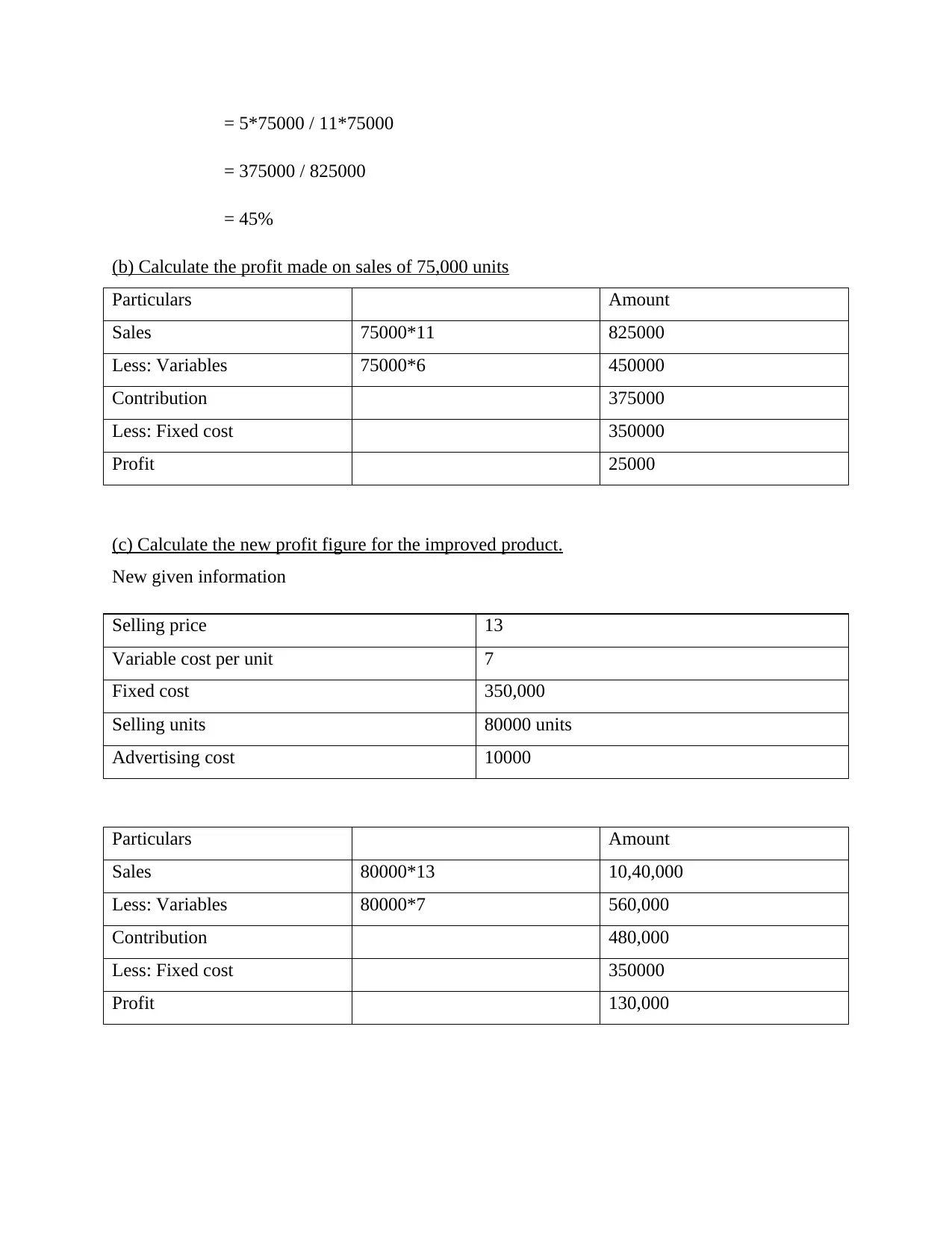

This report provides an overview of accounting fundamentals, focusing on break-even analysis and management accounting techniques. It includes calculations for break-even points in units and revenues for Kerrigan Ltd, along with profit calculations under different scenarios. The report also discusses the limitations of break-even analysis and highlights the significance of management accounting, contrasting it with financial accounting. Furthermore, it explores three key techniques used by management accountants—marginal analysis, financial statement analysis, and budgetary control—to achieve organizational objectives. The report emphasizes the importance of these accounting practices in systematically recording transactions, analyzing financial data, and supporting effective decision-making within an organization. Desklib offers students access to similar solved assignments and past papers.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.