Cost Analysis, Break-Even, and Cash Budget Report for Finance

VerifiedAdded on 2021/02/19

|8

|1641

|34

Report

AI Summary

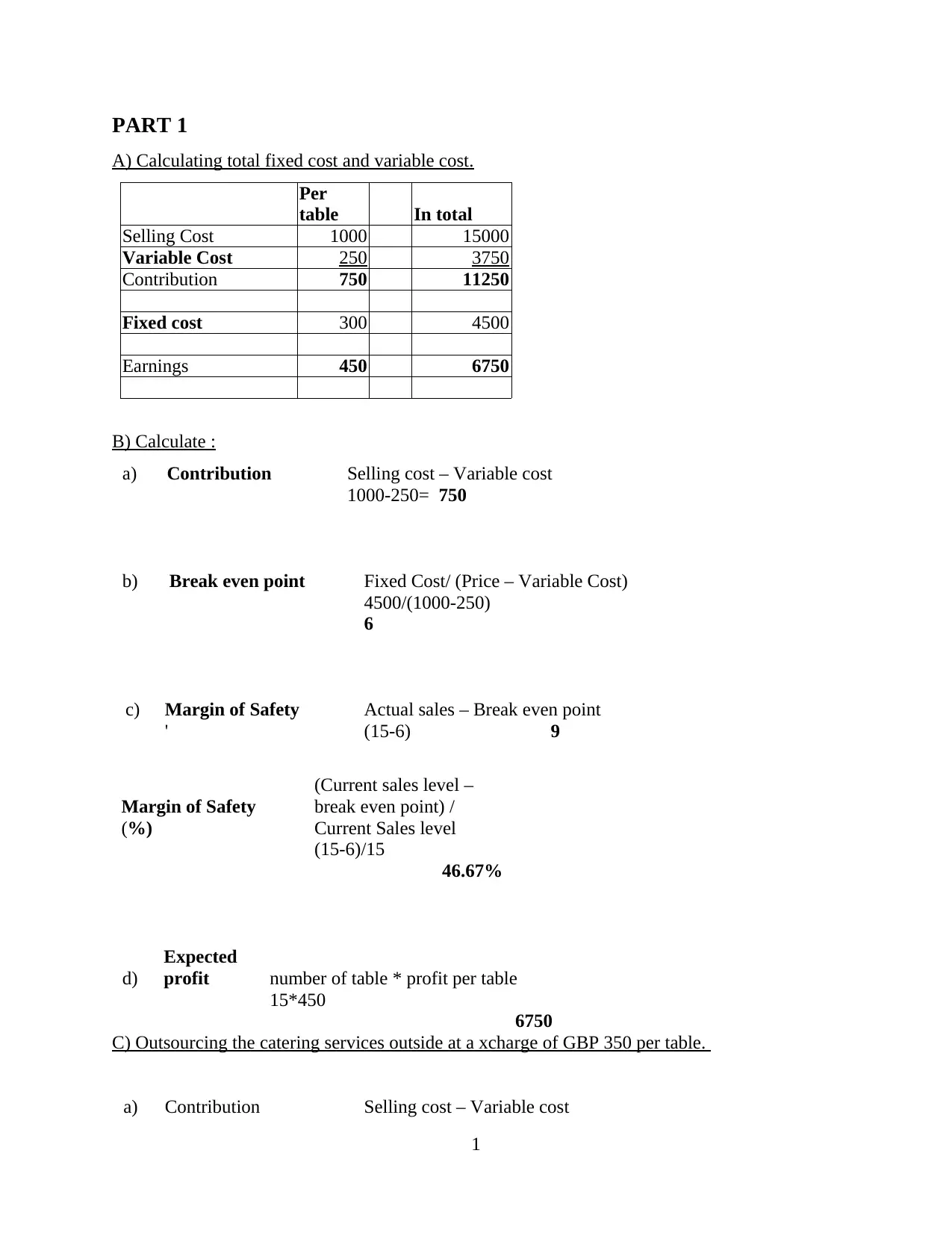

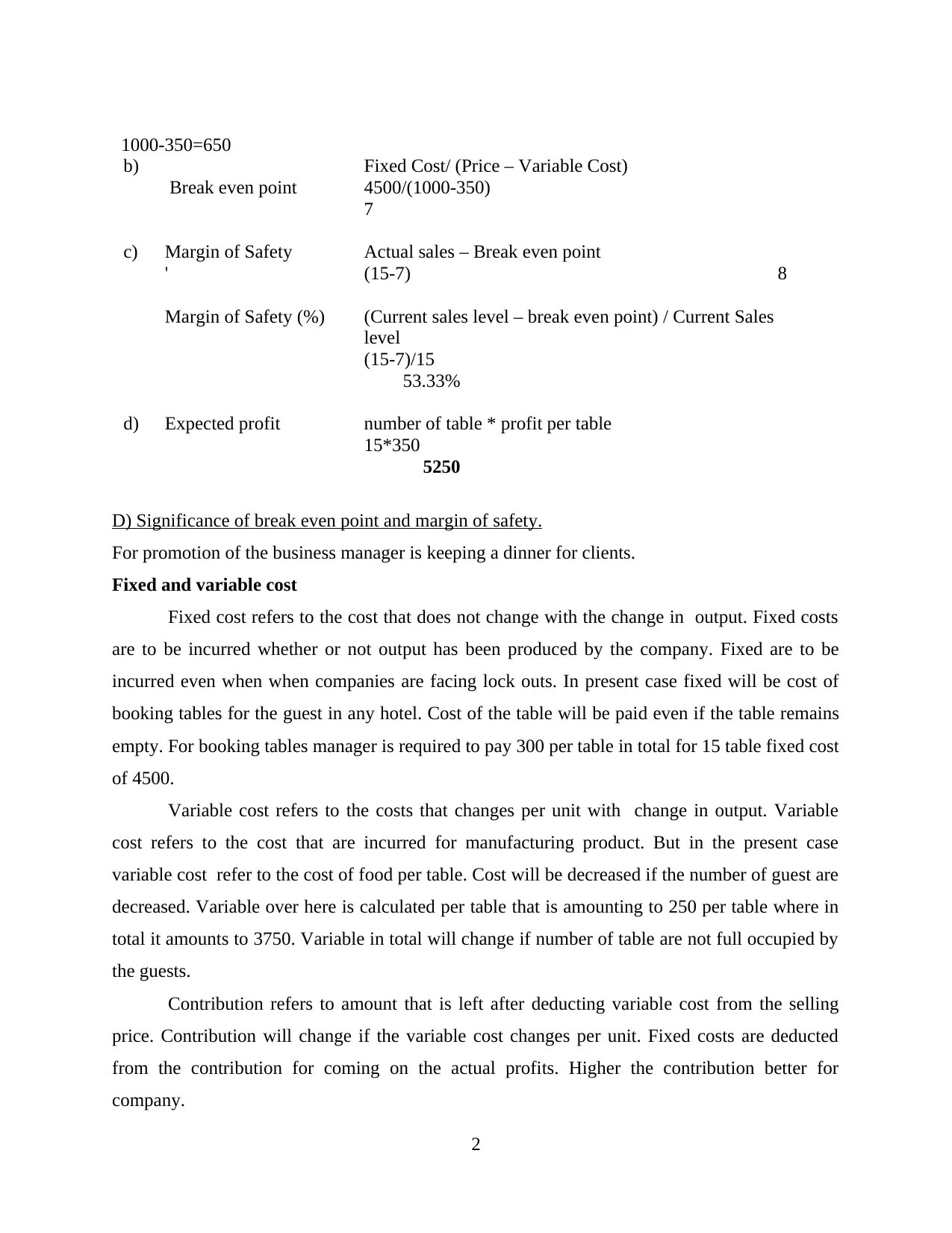

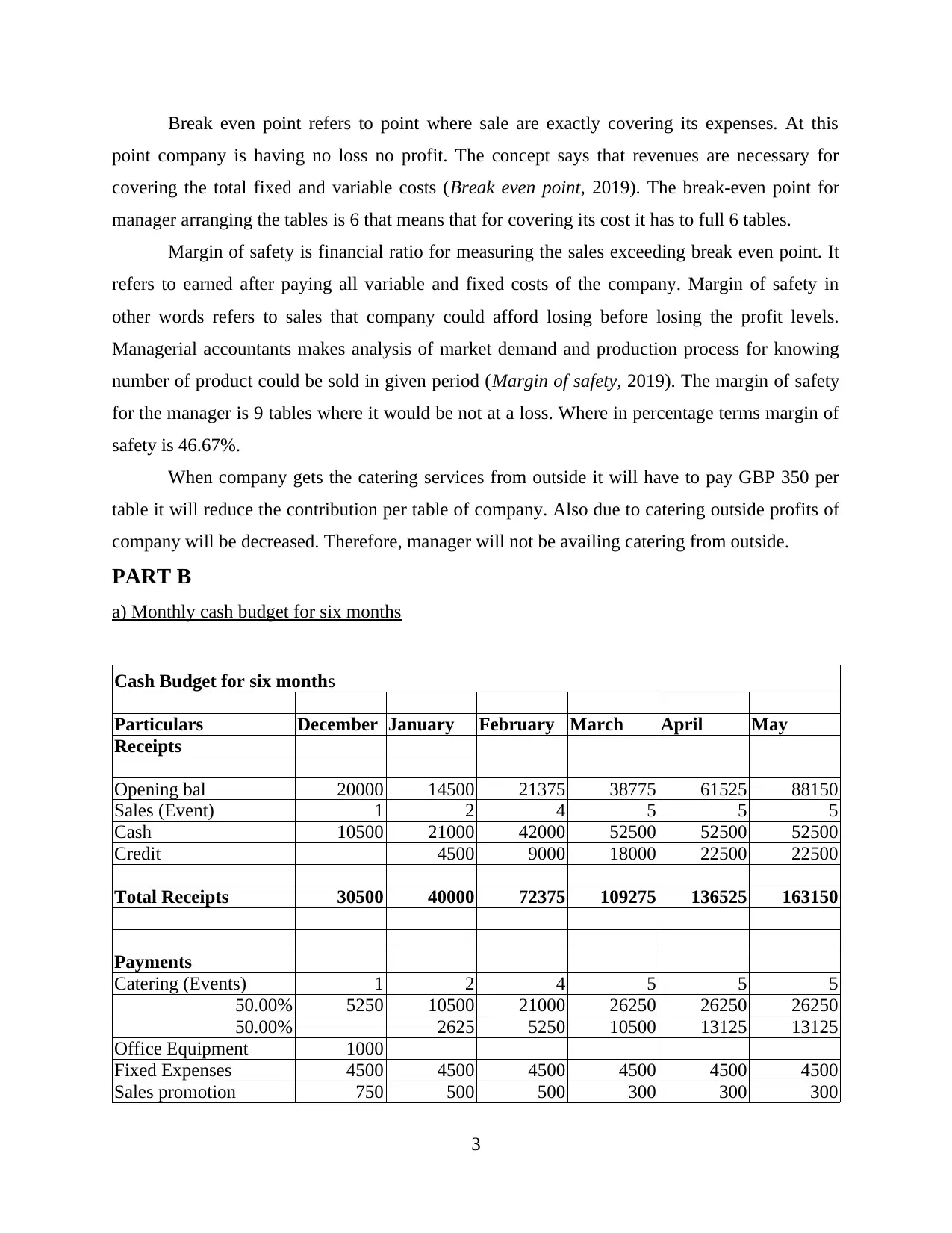

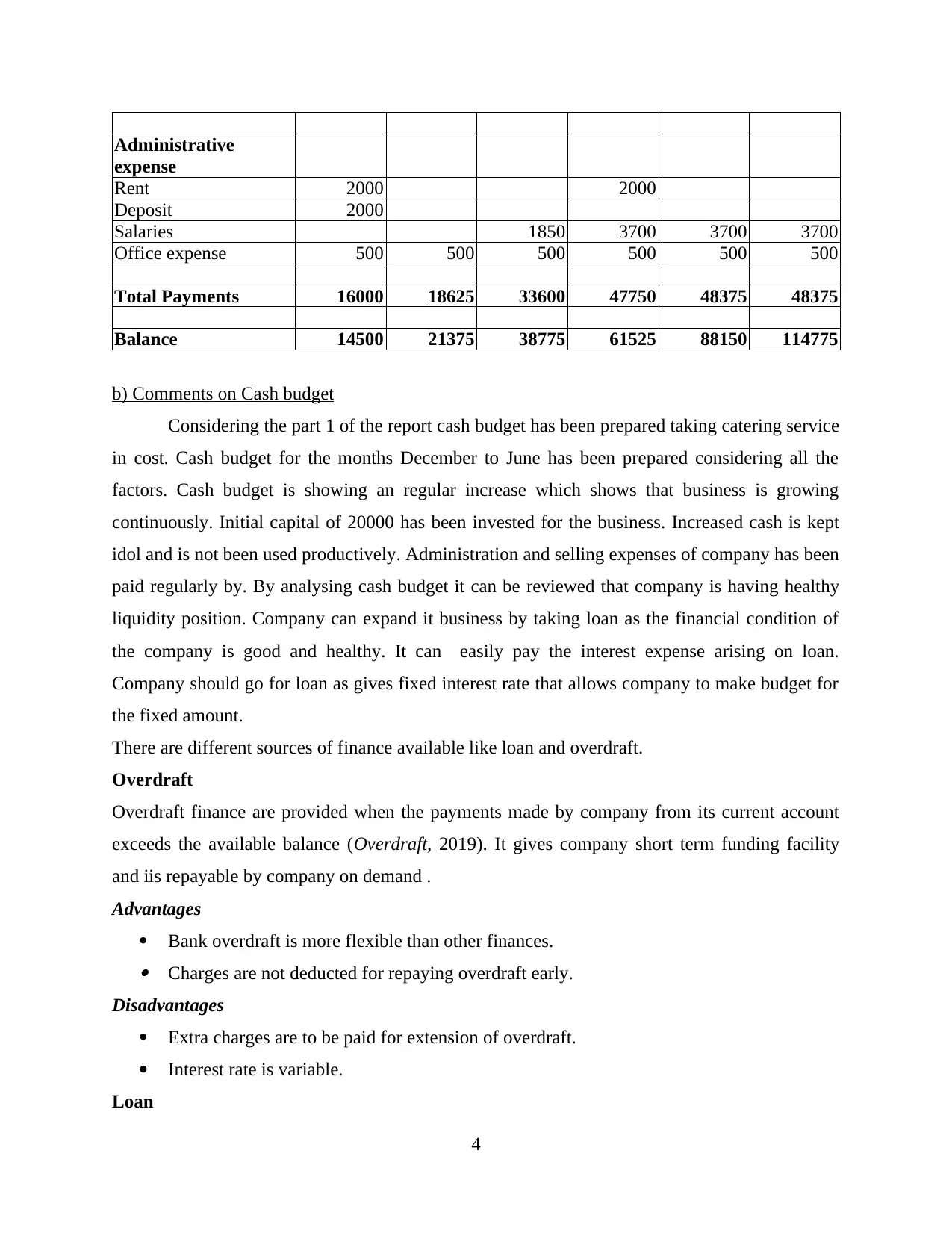

This finance report provides a detailed analysis of costs, break-even points, and cash budgeting for a business scenario. Part 1 includes calculations of total fixed and variable costs, contribution margins, break-even points, and margin of safety. It explores the implications of outsourcing catering services. Part 2 presents a six-month cash budget with comments on the business's financial health and liquidity. The report highlights the significance of break-even points and margin of safety for business promotion and decision-making, including a discussion of financing options like loans and overdrafts. The analysis uses provided data to assess the financial performance and stability of the business, offering insights into its potential for expansion and financial management strategies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.