Accounting Fundamentals: Break-Even Point Analysis and Management

VerifiedAdded on 2023/06/18

|8

|1329

|63

Report

AI Summary

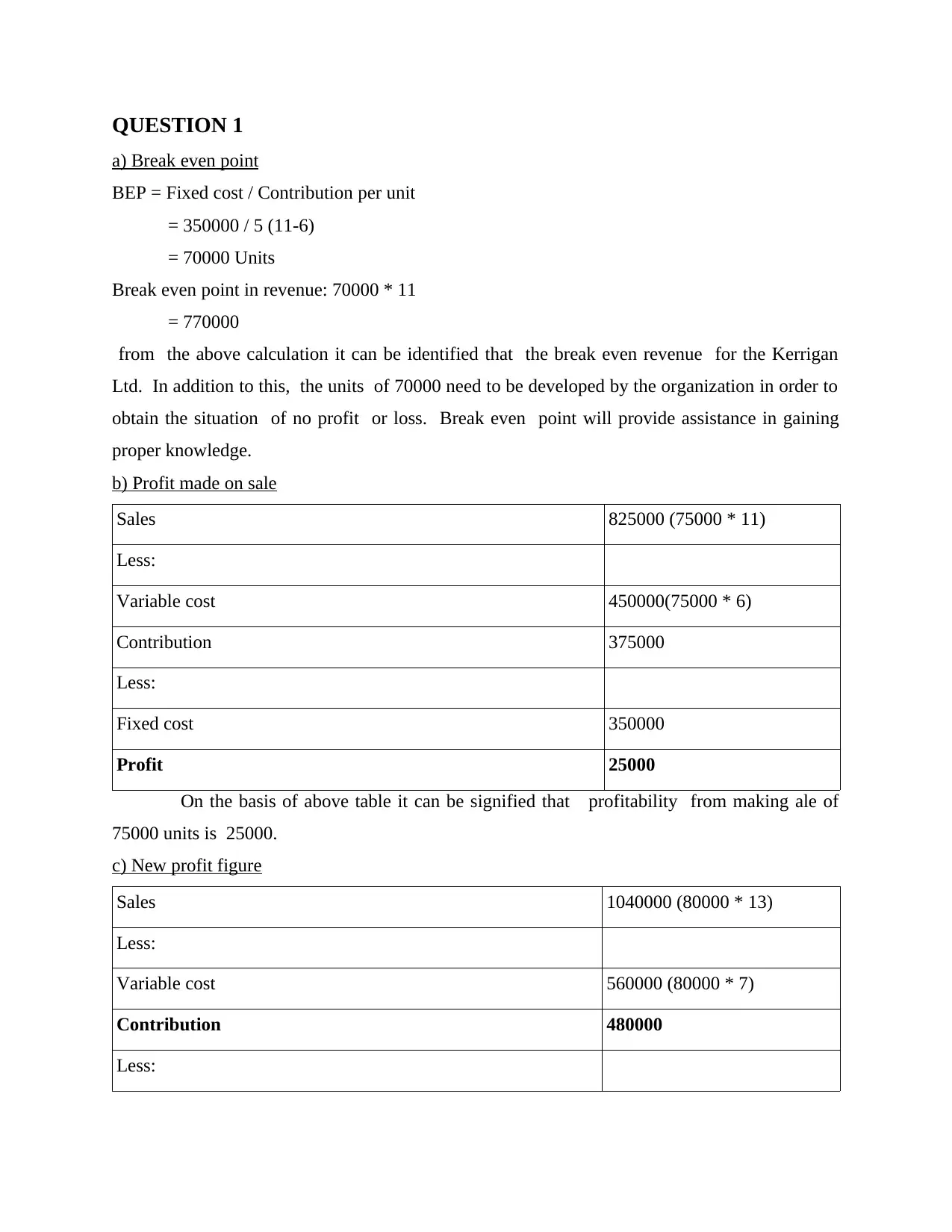

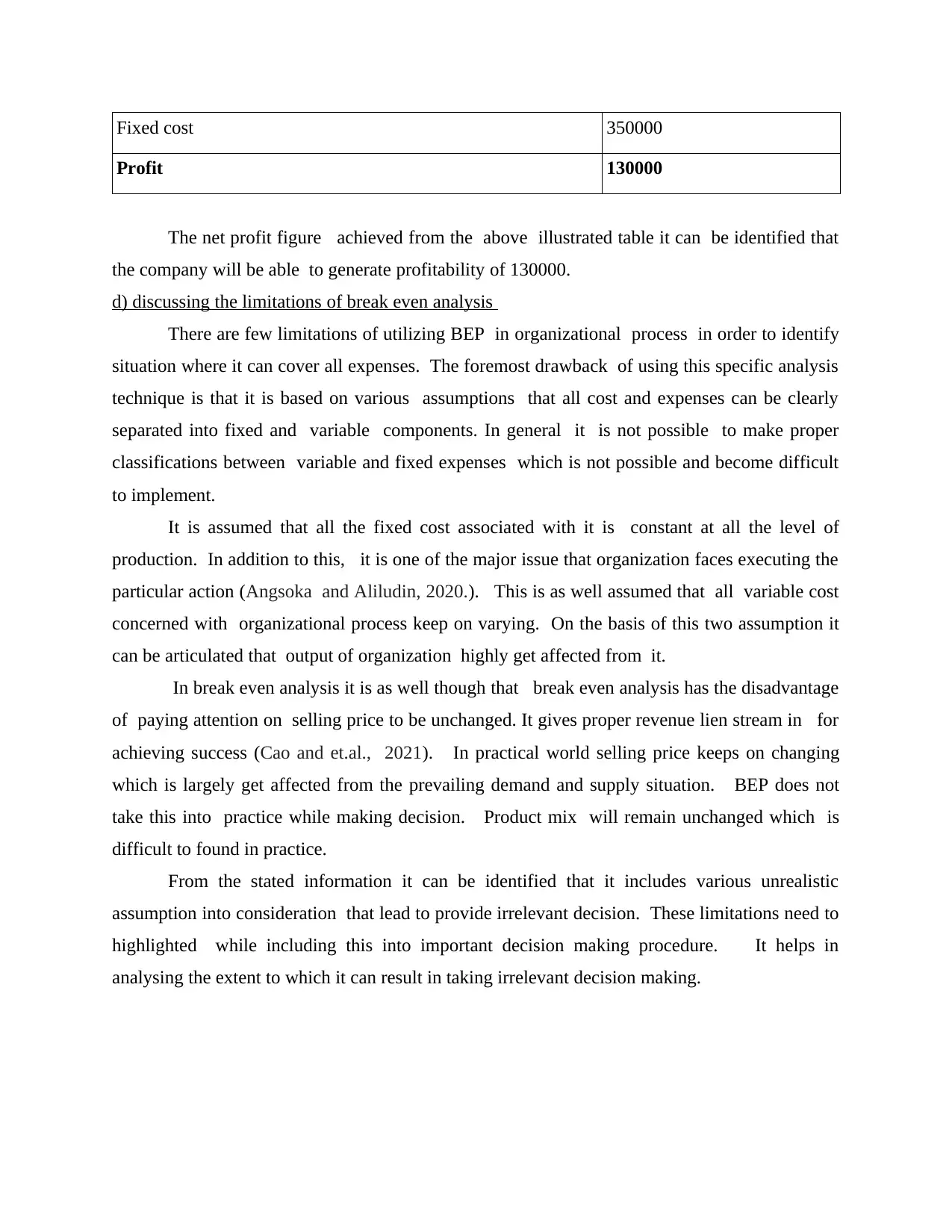

This report provides a detailed analysis of accounting fundamentals, focusing on break-even point (BEP) analysis and management accounting techniques. It includes calculations for break-even point in units and revenue for Kerrigan Ltd., profit calculations based on different sales volumes, and a discussion of the limitations of break-even analysis, such as the assumptions regarding fixed and variable costs, constant selling prices, and product mix. The report also explores the role of management accounting in strategic decision-making, planning, and performance measurement, highlighting its objectives like cost reduction and resource optimization. Furthermore, it discusses techniques management accountants can use to achieve these objectives, including trend analysis, forecasting, inventory valuation, product costing, and constraints analysis. Desklib offers a wide range of study tools and resources for students seeking assistance with accounting and finance topics.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.